Pharmaceutical Contract Development And Manufacturing Organization (CDMO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

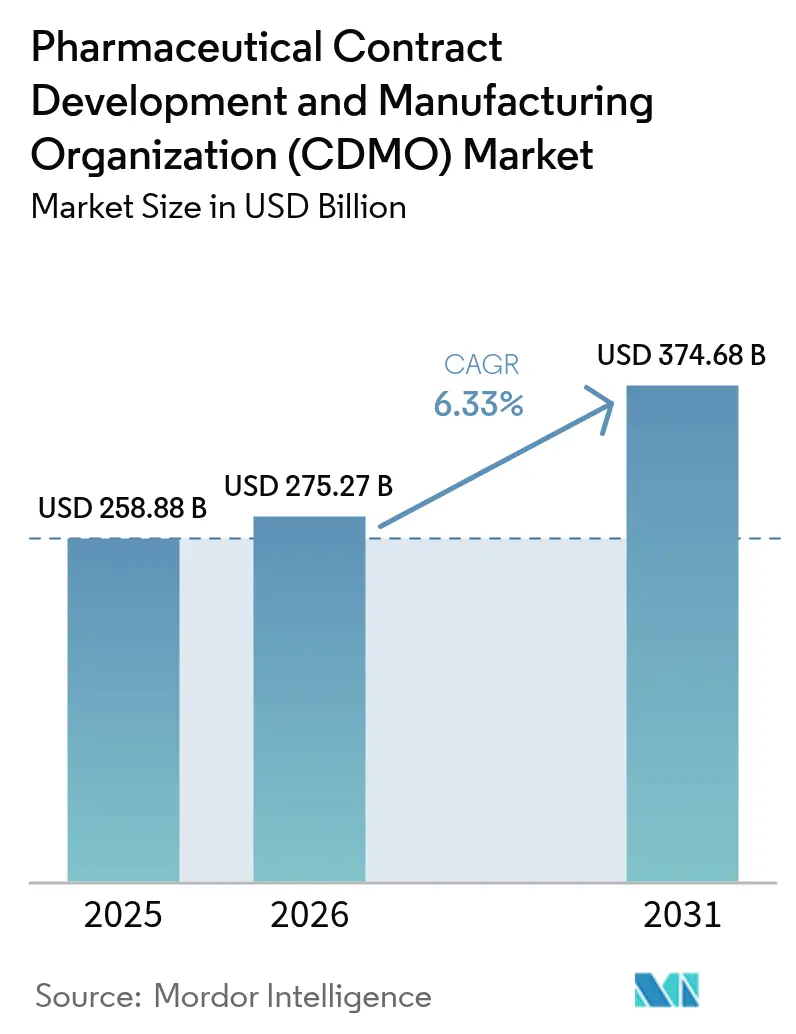

| Market Size (2026) | USD 275.27 Billion |

| Market Size (2031) | USD 374.68 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Contract Development And Manufacturing Organization (CDMO) Market Analysis by Mordor Intelligence

The Pharmaceutical contract development and manufacturing organization (CDMO) market size is expected to grow from USD 258.88 billion in 2025 to USD 275.27 billion in 2026 and is forecast to reach USD 374.68 billion by 2031 at 6.33% CAGR over 2026-2031. Robust outsourcing demand for complex biologics, the rise of high-potency APIs (HPAPIs), and artificial-intelligence-enabled–enabled process-development platforms underpin this trajectory. Peptide-based GLP-1 therapies, expanding vaccine programs, and sustained investment in digitally connected plants further amplify the need for specialist partners able to absorb capital and regulatory risks. North American innovators continue to anchor high-value biologics and gene-therapy work, while Asia-Pacific cost advantages accelerate capacity expansion. Consolidation—typified by Novo Holdings’ USD 16.5 billion purchase of Catalent—signals a decisive shift toward end-to-end providers that combine development, scale-up, and commercial production.

Key Report Takeaways

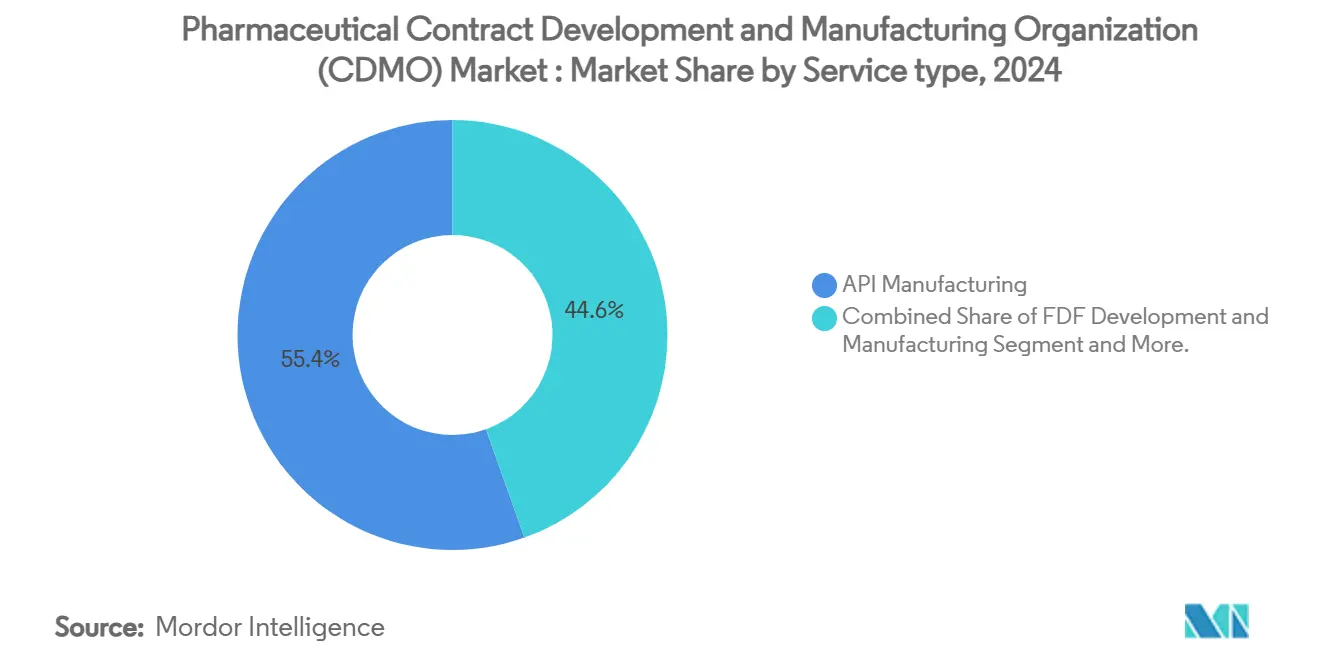

- By service type, API manufacturing held 54.92% of the Pharmaceutical contract development and manufacturing organization (CDMO) market share in 2025, while finished-dosage-form (FDF) development and manufacturing is forecast to expand at 7.18% CAGR through 2031.

- By molecule type, small-molecule APIs captured 61.70% of the Pharmaceutical contract development and manufacturing organization (CDMO) market size in 2025; HPAPIs are projected to grow at an 8.05% CAGR to 2031.

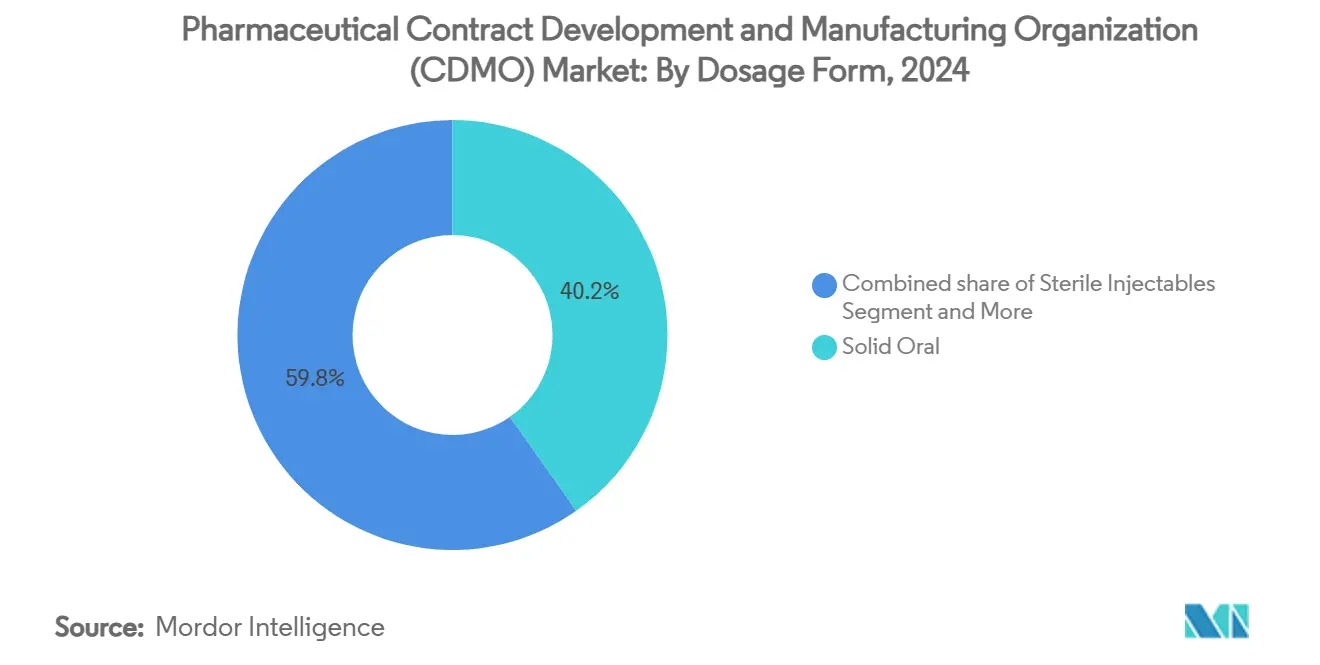

- By dosage form, solid orals accounted for 39.88% share of the Pharmaceutical contract development and manufacturing organization (CDMO) market size in 2025, whereas sterile injectables are advancing at 9.05% CAGR.

- By therapeutic area, oncology commanded 32.15% revenue share in 2025, while infectious-disease and vaccine projects post the fastest 8.16% CAGR outlook.

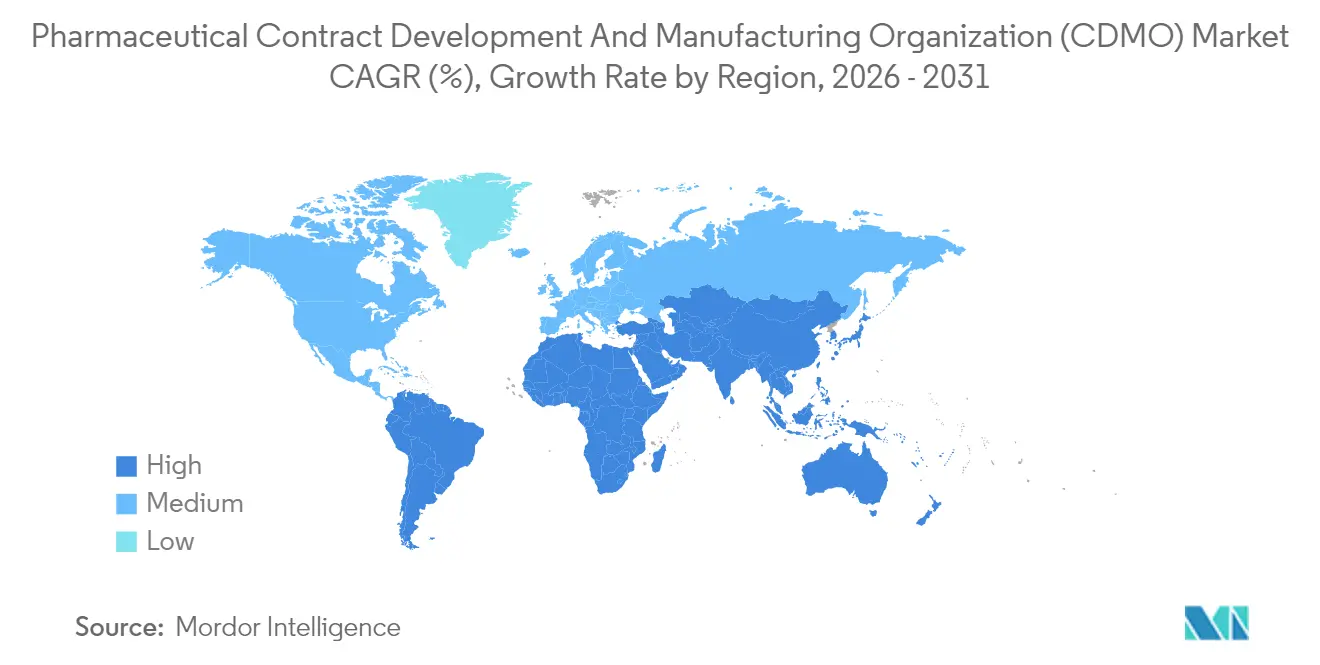

- By geography, North America led with 37.95% of the Pharmaceutical contract development and manufacturing organization (CDMO) market share in 2025; Asia-Pacific records the highest 7.18% CAGR projection.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Contract Development And Manufacturing Organization (CDMO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing outsourcing volume by large pharmaceutical companies | +1.8% | North America, Europe | Medium term (2-4 years) |

| Surge in biologics and complex-molecule pipelines | +1.5% | North America, EU; APAC emerging | Long term (≥ 4 years) |

| Cost and speed advantage of manufacturing in emerging markets | +1.2% | Core APAC; MEA & South America spill-over | Short term (≤ 2 years) |

| Consolidation toward one-stop CDMOs | +0.9% | Global | Medium term (2-4 years) |

| AI-enabled rapid process-development platforms | +0.7% | North America, Europe; APAC expanding | Medium term (2-4 years) |

| GLP-1 and peptide HPAPI capacity build-outs | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Outsourcing Volume by Large Pharmaceutical Companies

Escalating R&D costs and pipeline complexity drive pharmaceutical majors to off-load non-core manufacturing. Asset-light models free capital for discovery while leveraging CDMO expertise to maintain global supply continuity. Lonza’s USD 1.2 billion Vacaville site purchase from Roche underpins this transition, adding 330,000 L of biologics capacity to support blockbuster antibody demand. Outsourcing is most intense for sterile biologics and gene-editing therapies, where regulatory rigor and technical barriers heighten the value of specialist partners.

Surge in Biologics and Complex-Molecule Pipelines

Biological entities now dominate new-drug filings, propelled by antibody-drug conjugates, mRNA vaccines, and cell-based therapeutics. Samsung Biologics secured USD 1.4 billion in new 2024 contracts and is expanding antibody-drug-conjugate suites, illustrating spiraling demand for cGMP biologics supply [1]Samsung Biologics, “Samsung Biologics Financial Results 2024,” samsung.com Source: Economic Times, “India CDMO market to reach $22-25 billion by 2035: Report,” economictimes.indiatimes.com . Biologics’ stringent cold-chain, contamination-control, and analytics requirements solidify a preference for full-scope CDMOs with proven regulatory track records.

Cost and Speed Advantage of Manufacturing in Emerging Markets

Regional incentives, labor arbitrage, and faster approvals underpin APAC’s ascent. India targets a USD 22–25 billion Pharmaceutical contract development and manufacturing organization (CDMO) market size by 2035, backed by streamlined environmental clearances and tax holidays. Brazil and Saudi Arabia likewise channel public funds into diabetes-drug and vaccine plants to foster local resilience.

Consolidation Toward One-Stop CDMOs

Drug sponsors shave months off timelines by handing a molecule to a single partner from pre-clinical tox through global launch. Novo Holdings’ 2024 Catalent takeover fused development, viral-vector, and fill-finish expertise under one roof. Larger platforms exploit shared quality systems and digital twins to de-risk tech transfer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region regulatory requirements | -0.8% | North America, EU | Long term (≥ 4 years) |

| Capacity-utilization and lead-time risk | -0.6% | Global, biologics acute | Medium term (2-4 years) |

| High capex for sterile biologics suites | -0.5% | Developed markets | Medium term (2-4 years) |

| Scarcity of skilled aseptic-manufacturing talent | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Regulatory Requirements

Divergent dossiers and rolling updates such as the European Medicines Agency’s new fee rules raise compliance budgets and prolong variation lead times EMA. CDMOs must operate duplicate quality-management systems and align data-integrity protocols across FDA, EMA, and PMDA audits, challenging smaller entrants.

High Capex for Sterile Biologics Suites

Each Class A/B cell-culture wing commands USD 100 million plus validation, locking outsized capital for up to five years. Lonza earmarked CHF 500 million to refurbish Vacaville’s fermentation halls into next-generation antibody production, underscoring significant fixed-cost hurdles. Limited suppliers of single-use bioreactors and isolators compound procurement delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: API Manufacturing Remains the Anchor

Active Pharmaceutical Ingredient (API) Manufacturing is the largest segment in the Pharmaceutical Contract Development and Manufacturing Organization (CDMO) market, holding a significant market share of approximately 68% in 2023. This segment is pivotal due to its role in the production of essential components for pharmaceutical drugs, which are critical for the healthcare industry. The dominance of this segment is driven by the increasing demand for APIs, particularly for small molecule drugs, which constitute a major portion of the pharmaceutical market. Technological advancements in API synthesis and the growing trend of outsourcing API production to specialized CDMOs have further bolstered this segment's growth. Additionally, the rising prevalence of chronic diseases and the need for innovative therapies have amplified the demand for high-quality APIs. The segment also benefits from stringent regulatory requirements, which encourage pharmaceutical companies to partner with experienced CDMOs for API manufacturing. Overall, the API manufacturing segment remains a cornerstone of the CDMO market, driving innovation and ensuring the availability of critical pharmaceutical ingredients.

By Molecule Type: Small Molecules Hold Scale; HPAPIs Accelerate

Small molecules captured 62.34% of 2024 value, aided by mature regulatory pathways and broad therapeutic applicability. Reaction-efficiency gains and green-chemistry mandates encourage hybrid batch-continuous plants that drive cost competitiveness. However, oncology’s migration toward antibody-drug conjugates, selective degrader molecules, and micro-dosed cytotoxics pushes HPAPIs to an 8.32% CAGR. CDMOs retrofit suites with negative-pressure isolators and closed-handling skids to comply with <1 μg/m³ OEL thresholds.

The Pharmaceutical contract development and manufacturing organization (CDMO) market size devoted to HPAPIs is forecast to double over the next five years as peptide-based GLP-1s and next-gen chemotherapeutics move through Phase III. HPAPI projects typically command 25-30% pricing premiums due to containment and analytical complexity, supporting higher margins for specialized providers.

By Dosage Form: Solid Orals Dominate; Sterile Injectables Surge

Solid oral products retained 40.23% share in 2024. Robust tableting lines, wet-granulation flexibility, and unrivaled patient acceptance anchor this format. Efforts to extend franchise exclusivity via abuse-deterrent coatings and multiparticulate capsules sustain demand in mature markets. Further, fixed-dose combinations for metabolic disease streamline adherence.

Sterile injectables register the fastest 9.32% CAGR on the back of biologics, long-acting antipsychotics, and biosimilar launches. The Pharmaceutical contract development and manufacturing organization (CDMO) market size for sterile fill-finish is projected to eclipse USD 70 billion by 2030 as dual-chamber syringes, auto-injectors, and lyophilized vials gain regulatory approvals. Simtra BioPharma’s USD 250 million expansion highlights capital intensity and the allure of premium parenteral margins[2]Simtra BioPharma, “Sterile Fill-Finish Expansion,” simtra.com.

By Therapeutic Area: Oncology Retains the Lead; Vaccines Rise

Oncology accounted for 32.43% of 2024 CDMO revenue, reflecting high value per gram and constant pipeline replenishment. HPAPI suites, single-use perfusion bioreactors, and conjugation lines support small-batch precision medicines. Demand spikes for checkpoint inhibitors and radioligand therapies keep capacity tight and prices firm.

Infectious-disease and vaccine programs grow at 8.42% CAGR. Government pandemic-preparedness funding exemplified by Moderna’s USD 590 million H5N1 mRNA contract—sustains lipid-nanoparticle-formulation and aseptic-fill investments [3]Moderna, “Moderna Receives $590 Million US Government Contract,” modernatx.com. Expanded adult immunization schedules and antimicrobial-resistance initiatives diversify volumes beyond COVID-19 boosters. Meanwhile, GLP-1–driven endocrine products accelerate metabolic-disorder output, further crowding HPAPI slots.

Geography Analysis

North America retained 37.95% revenue share in 2025, buoyed by premier biologics programs, FDA Orphan-Drug incentives, and a deep venture-capital pool. The United States sustains premium pricing as cGMP compliance costs and stringent data-integrity audits elevate barriers to entry. Canada benefits from free-trade access and skilled resources, whereas Mexico lures secondary packaging and regional solid-oral projects. Thermo Fisher’s USD 4.1 billion filtration-business acquisition reinforces North American vertical-integration strategies.Asia-Pacific logs the fastest 7.18% CAGR through 2031. China and South Korea bankroll mega-plants for mAbs and oligonucleotides, though geopolitical risk nudges US sponsors toward India and Southeast Asia. The Pharmaceutical contract development and manufacturing organization (CDMO) market size in India alone could surpass USD 22 billion by 2035, aided by PLI incentives and harmonized quality standards.Samsung Biologics’ fourth plant, topping 600,000 L, cements Incheon as the world’s largest single-site biologics hub. Australia leverages expedited regulatory pathways for early-phase oncology and cell-therapy trials.

Europe presents steady expansion anchored in quality leadership. Germany’s continuous-manufacturing clusters and the United Kingdom’s advanced-therapy corridor offset Brexit friction through mutual-recognition waivers. The EMA’s updated variation fees raise short-term compliance costs but assure global sponsors of consistent review rigor. Eastern Europe gains traction as an overflow destination for solid-oral generics and secondary packaging. Sustainability regulations incentivize solvent-recovery units and low-energy lyophilization, driving process innovation.

Regulatory Landscape

CDMOs operate under converging cGMP expectations that assign explicit accountability for outsourced activities, increasing the importance of written quality agreements and audit readiness across API, drug product, and packaging. In the United States, FDA cGMP regulations under 21 CFR Part 211 cover manufacturing controls, and for retail OTC drugs they also include tamper-evident packaging requirements (21 CFR 211.132), reinforcing packaged-product integrity as part of compliance for contract manufacturing and packaging networks.

In Europe, EMA-aligned requirements continue to emphasize submission and control of labeling and packaging materials (including mock-ups and specimens) during authorization activities, while EU GMP documentation expectations (notably Chapter 4) tighten traceability across chain-of-contract setups. Separately, the EU Pharmaceutical Package reform advanced with European Council compromise texts published in March 2026, which may reshape how sponsors and CDMOs structure manufacturing and distribution responsibilities within the region amid supply-chain authorization and sourcing constraints.

Competitive Landscape

The CDMO market is characterized by a high degree of competition and ongoing consolidation, reflecting current CDMO market trends. Global players are expanding their operations in key regions, while local firms are enhancing their capabilities to compete internationally. Mergers and acquisitions are a common strategy, enabling companies to broaden their service offerings and geographical reach. Investment in advanced manufacturing technologies, such as continuous manufacturing and digital integration, is also prevalent, driving CDMO industry growth.

Niche disruptors leverage continuous flow, micro-reactor scale-out, and on-demand formulation to serve precision-medicine pipelines with batch sizes in the tens of grams. Capacity shortages in HPAPI and viral-vector fill-finish create price elasticity that rewards early movers. Competitive intensity will heighten as digital-native entrants compress tech-transfer cycles and as large pharma refines multi-sourcing frameworks to mitigate geopolitical risk.

Pharmaceutical Contract Development And Manufacturing Organization (CDMO) Industry Leaders

Catalent Inc.

Recipharm AB

Jubilant Pharmova Ltd

Patheon Inc. (Thermo Fisher Scientific Inc.)

Boehringer Ingelheim Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment concentration in sterile fill-finish and drug-device combination capability creates near-term whitespace for CDMOs that can integrate aseptic manufacture with final assembly, packaging, and cold-chain handling under one quality system. April 2026 infrastructure commitments from PCI Pharma Services (over USD 1 billion across the United States and Europe) point to demand for end-to-end sterile fill-finish plus drug-device delivery combinations, consistent with the report's acceleration in sterile injectables and complex biologics work.

Specialized injectable packaging capacity in Europe and new GMP footprint builds in the United States also indicate opportunities in late-phase and commercial launch services that combine packaging, labeling, and distribution with regulatory-compliant change control. Sharp's January 2026 investment (over EUR 20 million) to expand injectable packaging, assembly, and cold-chain storage in Belgium and the Netherlands, and Tjoapack's December 2025 plan for a 170,000 square foot GMP facility in Clinton, Tennessee, underscore ongoing capacity expansion where sponsors need redundancy and speed for parenterals and patient-centric formats (including autoinjector-linked supply chains). Together, these moves support a shift toward packaging as a commercialization enabler alongside development, analytical release, and logistics integration, particularly for sterile products and advanced modalities.

Recent Industry Developments

- July 2026: Catalent expanded its partnership with Nanoscope Therapeutics to support late-phase development and commercial supply activities for the optogenetic gene therapy candidate MCO-010, including commercial-compliant packaging and distribution. The expansion reinforces the importance of integrated packaging and global distribution capabilities for advanced-therapy programs transitioning toward commercialization.

- September 2025: Thermo Fisher Scientific completed the acquisition of Sanofi's Ridgefield, New Jersey site, adding sterile fill-finish and packaging capacity in the United States. The transaction strengthens domestic drug product manufacturing options for sponsors seeking resilient North American supply and tighter coordination between fill-finish and packaged finished goods.

- July 2024: Catalent completed a USD 25 million expansion of its clinical supply facility in Schorndorf, Germany, enhancing clinical packaging and distribution capabilities. The added capacity supports sponsors running multi-region trials that require rapid labeling changes, controlled distribution, and reliable clinical resupply.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers outsourced pharmaceutical development and manufacturing work delivered by CDMOs, where revenue comes from services such as API and finished dosage development, scale-up, commercial manufacturing, and related packaging support. Coverage spans small molecules and biologics.

Scope exclusions: In-house development and manufacturing done fully within pharmaceutical or biotech companies (without a paid CDMO service contract) is not counted.

Segmentation Overview

- By Service Type

- API Manufacturing

- Small Molecule

- Large Molecule

- High-Potency (HPAPI)

- FDF Development and Manufacturing

- Solid Dose

- Liquid Dose

- Injectable Dose

- Secondary Packaging

- API Manufacturing

- By Molecule Type

- Small Molecule

- Large Molecule (Biologics and Biosimilars)

- High-Potency APIs

- By Dosage Form

- Solid Oral

- Sterile Injectables

- Topicals and Transdermals

- Specialty/Novel (e.g., ODT, Long-acting)

- By Therapeutic Area

- Oncology

- Metabolic and Endocrine

- Cardiovascular

- CNS and Psychiatry

- Infectious Diseases and Vaccines

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a clean fact base on pharmaceutical production activity, trade flows, and regulatory activity that shape outsourcing demand. We refer to public sources such as the US FDA databases (including inspections and approvals), the European Medicines Agency, and the World Health Organization, since these provide signals on product pipelines and manufacturing oversight.

To ground model inputs, we also use statistics and reference publications such as OECD health data, UN Comtrade for cross-border shipment patterns, and peer-reviewed journals that discuss API, sterile manufacturing, and tech transfer trends. Company annual reports, investor presentations, and press releases are used to understand capacity additions, shifts in service mix, and regional expansion. Where needed, select paid subscriptions are used only for company financials and patent databases to cross-check revenue direction and the pace of development activity. This list is illustrative, and we reviewed additional sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with CDMO executives, plant and quality leaders, commercial managers, and procurement or technical operations respondents from pharma and biotech buyers. Because this is a global market, we balance coverage across the Americas, EMEA, and APAC so assumptions on outsourcing intensity, service pricing, and capacity utilization can be checked against what is happening locally.

The respondent feedback is used to confirm how outsourcing is contracted in practice, especially around clinical-stage development handoffs, sterile and high-potency line constraints, and how secondary services such as packaging are treated in revenue reporting.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 19% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 24% | EMEA: 30% |

| Smaller Players: 19% | Managers: 57% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where pharma outsourcing demand is reconstructed from observable development and manufacturing activity, then mapped to CDMO service revenue pools across regions. Once the demand pool is set, we use selective bottom-up checks to sanity check totals, mainly through sampled CDMO revenue ranges, service mix splits, and volume times ASP checks for common outputs such as API kilograms and sterile fill-finish batches.

Key inputs that influence the model include the number and mix of products moving through clinical phases, the share of outsourced versus captive manufacturing, sterile and high-potency capacity additions, utilization and lead-time signals shared by interviewees, and typical price progression from development to commercial stages. These inputs are kept practical so they can be refreshed with public data and then validated with expert feedback. For forecasting, scenario analysis is used around pipeline conversion, capacity tightness in sterile and biologics lines, and outsourcing budgets. The final forecast path is aligned to the consensus view gathered in primary discussions. Where bottom-up information is missing for smaller or private CDMOs, we handle gaps by applying service-mix proxies and region-level pricing bands before rechecking totals.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple signals. In practice, we compare model totals against independent indicators such as approval activity, inspection volumes, and reported capacity expansions. If a region or service line shows a sharp jump, we review the assumptions behind utilization, pricing, or outsourcing share, then re-contact relevant experts to confirm whether it reflects a real market shift.

Before sign-off, the work goes through multi-step analyst review where formulas, unit consistency, and currency conversions are checked, and variances are explained in plain language. Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity additions, major regulatory changes, or demand shocks. Right before delivery, we do a final update pass so clients receive the latest view rather than an older snapshot.

Mordor Intelligence's Pharmaceutical Contract Development and Manufacturing Organization Cdmo Market Estimate Compared With Other Published Estimates

Published market sizes for pharmaceutical CDMOs often do not match because the boundaries are not identical, and the timing of the data cut also varies. Differences usually come from what service lines are counted, whether clinical development revenue is merged with manufacturing revenue, and how companies treat packaging and secondary services.

Key gap drivers are usually scope and conversion logic. Some estimates lean more heavily on broad outsourcing narratives, while others anchor sizing to observable activity such as clinical phase volumes, sterile capacity constraints, and the share of work that is actually outsourced. Currency timing also matters in a global market, since exchange rates and regional mix can shift the USD total even when local demand is stable.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 258.88 B (2025) | |

| Industry Publisher A | USD 197.40 B (2025) | Uses a narrower revenue pool that appears to weight manufacturing more than end-to-end development, and it can also treat packaging and related add-on services more selectively, which pulls down the counted service value. |

| Industry Publisher B | USD 166.00 B (2025) | Starts from a smaller base year value and applies a faster growth curve, which suggests a tighter definition of what qualifies as a CDMO service and a different split between clinical-stage work and commercial manufacturing revenue. |

By tracking phase-wise demand signals and capacity tightness across API and sterile production, Mordor Intelligence keeps the 2025 value tied to services that are actually contracted out, instead of mixing in adjacent internal activity. The spread in the table is mainly explained by how development revenue and secondary services are handled, plus base-year choices, which is why we keep the scope rules explicit and the checks repeatable.

Key Questions Answered in the Report

What is the current size of the pharmaceutical contract development and manufacturing organization (CDMO) market?

The Pharmaceutical CDMO market size stands at USD 275.27 billion in 2026 and is projected to reach USD 374.68 billion by 2031, reflecting a 6.33% CAGR.

Which CDMO service segment generates the greatest revenue today?

API manufacturing leads with 54.92% of 2025 revenue, supported by entrenched small-molecule infrastructure and rising demand for high-potency APIs.

Which region holds the largest market share and which is expanding the quickest?

North America captured 37.95% of 2025 global revenue, while Asia-Pacific records the fastest 7.18% CAGR thanks to cost advantages and large-scale capacity additions.

How are high-potency APIs (HPAPIs) and sterile injectables performing?

HPAPIs expand at an 8.05% CAGR, propelled by oncology and targeted-therapy pipelines, and sterile injectables advance at a 9.05% CAGR on the back of biologics and vaccine demand.

What is the fastest-growing service category?

Finished-dosage-form (FDF) development and manufacturing posts the highest 7.18% CAGR through 2031 as drug sponsors seek patient-centric formats and accelerated life-cycle management.

Page last updated on: