Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.71 Billion |

| Market Size (2026) | USD 12.01 Billion |

| Market Size (2031) | USD 14.31 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Wallcovering Market Analysis by Mordor Intelligence

The US wallcovering market size is projected to be USD 11.71 billion in 2025, USD 12.01 billion in 2026, and reach USD 14.31 billion by 2031, growing at a CAGR of 3.56% from 2026 to 2031. Expansion is underpinned by a rebound in residential construction, persistent renovation outlays, and rapid adoption of digitally printed, on-demand products. Total housing starts, which climbed to 1.354 million units in 2024, have regenerated builder confidence, while renovation spending of USD 485 billion has cemented an aftermarket revenue floor. Within this landscape, the US wallcovering market benefits from rising do-it-yourself participation, e-commerce visualization tools, and stricter indoor-air-quality regulations, which position low-VOC substrates as premium propositions. Competitive dynamics remain moderate, paint conglomerates leverage channel breadth and cross-category bundling, whereas specialist brands pursue design exclusivity and fast-cycle customization. Regulatory pressure on volatile organic compound (VOC) emissions and fire performance continues to push material innovation toward non-woven, paper, and textile backings that offer sustainability differentiation without compromising code compliance.

Key Report Takeaways

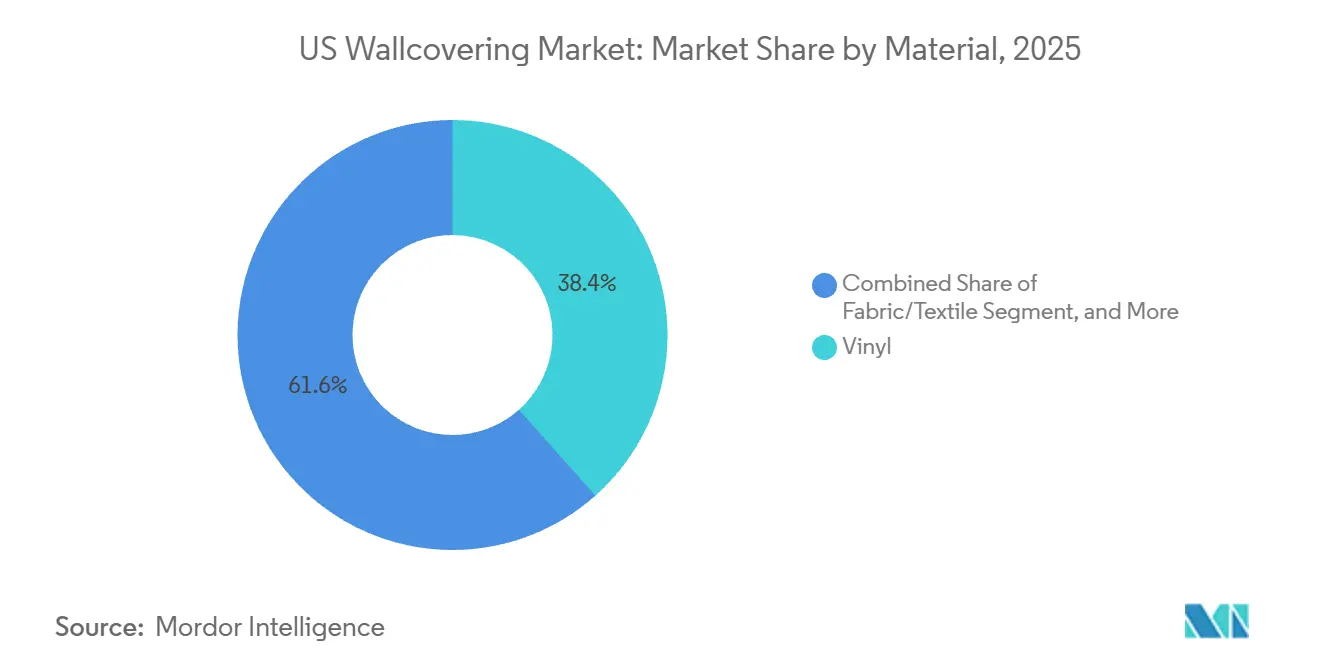

- By material, vinyl commanded 38.43% of the US wallcovering market share in 2025, while fabric and textile wall coverings are forecast to record the fastest 4.43% CAGR through 2031.

- By product type, wallpaper led with 39.32% revenue share in 2025, whereas wall panel sales are projected to expand at a 4.63% CAGR between 2026 and 2031.

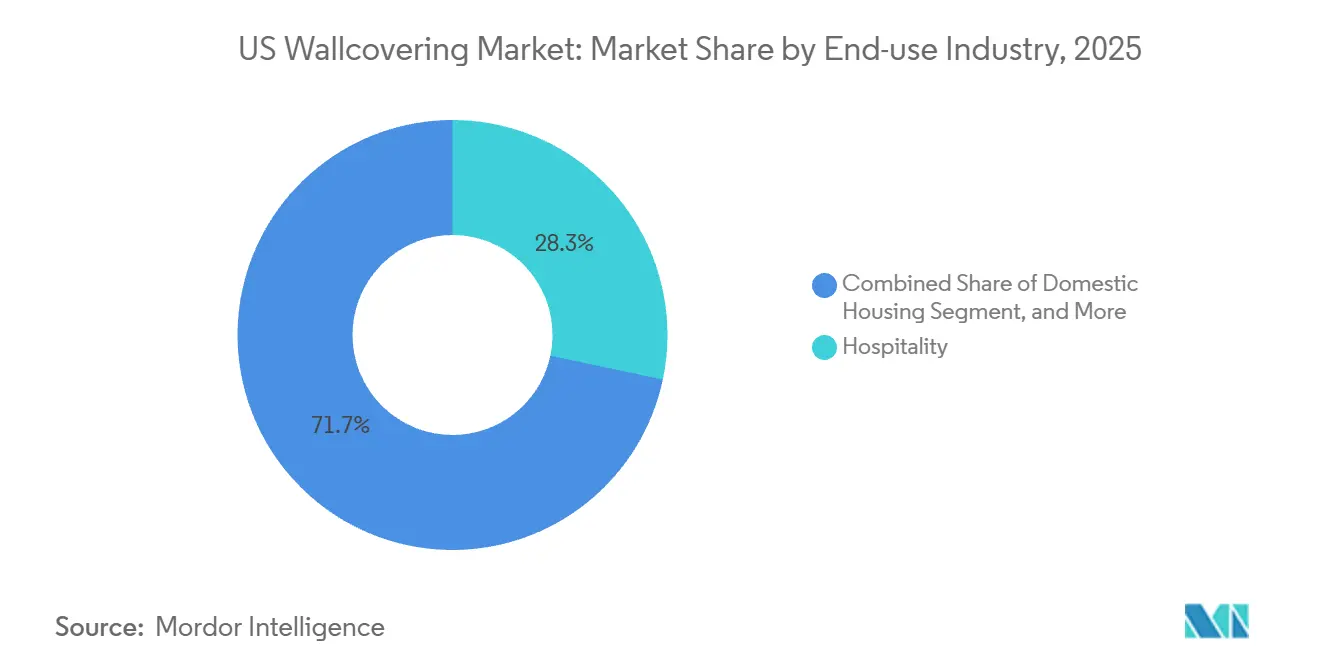

- By end-use industry, hospitality accounted for 28.32% of 2025 revenue, yet domestic housing is set to grow at a market-beating 5.78% CAGR through 2031.

- By distribution channel, specialty stores held a 31.21% share in 2025, and franchise stores are expected to post a 5.21% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Wallcovering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebounding Residential Construction Activity | +1.2% | Sun Belt concentration | Medium term (2-4 years) |

| Recovery in Wall Panel Sales Through Renovation Demand | +0.9% | Major metro retrofit corridors | Medium term (2-4 years) |

| Increasing Demand for Digitally Printed Solutions | +0.7% | Coastal urban markets | Short term (≤ 2 years) |

| Preference for Non-woven and Paper-based Wallpapers | +0.5% | Northeast and West Coast | Long term (≥ 4 years) |

| Shift Toward Eco-Friendly Wallcoverings | +0.4% | States with strict VOC rules | Long term (≥ 4 years) |

| Growth of E-commerce Customization Platforms | +0.6% | Suburban millennial clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rebounding Residential Construction Activity

Single-family housing starts reached 1.026 million units in 2024, an 8.1% annual rise as mortgage rates stabilized below 7% and household formation regained momentum. Builders allocate 2-4% of interior-finish budgets to accent surfaces, creating fresh specification opportunities for the US wallcovering market. Sun Belt states generated 53% of national starts, concentrating distributor and installer activity. Model homes featuring distinctive wallcoverings convert to buyer upgrades in roughly 15-20% of closings, reinforcing aftermarket pull-through. Because installation occurs 12-18 months after permitting, the uplift manifests as a medium-term revenue driver.

Recovery in Wall Panel Sales Through Renovation Demand

Commercial landlords accelerated retrofits in 2025, adopting acoustic wall panels with noise-reduction coefficients of 0.15-0.45 in 30-40% of Class A office upgrades.[1] MDC Wallcoverings, “Acoustic Wall Panel Product Specifications,” mdcwall.com Interlocking panels mount directly over drywall and cut labor hours by up to 50%, a compelling economic advantage for both contractors and do-it-yourself consumers. Retailers such as Home Depot and Lowe’s merchandised DIY-friendly kits, broadening reach into residential spaces. This installation speed, coupled with acoustic gains, underpins the segment’s forecast-leading 4.63% CAGR.

Increasing Demand for Digitally Printed Solutions

Wide-format inkjet systems like Roland DG’s VersaCAMM VS-640i deliver 1,200 dpi output, enabling cost-effective runs as low as 10 linear feet.[2] Roland DG, “VersaCAMM VS Series Product Information,” rolanddg.com E-commerce providers Spoonflower and Wallpops reported 35-40% growth in orders in 2024 as consumers uploaded custom artwork.[3]Spoonflower, “Custom Wallpaper Design Platform,” spoonflower.com On-demand production collapses inventory risk, allowing niche entrants to compete on design rather than scale. Customization regularly commands a 15-25% price premium, buoying revenue in the domestic housing channel and reinforcing the United States wallcovering market’s value proposition against paint.

Preference for Non-woven and Paper-based Wallpapers

Non-woven substrates held roughly 30% share of wallpaper volume in 2025 because their paste-the-wall application trims installation time by up to 30%. Paper-based products certified by the Forest Stewardship Council align with LEED v4.1 low-emitting criteria and contribute to corporate sustainability mandates.[4] Forest Stewardship Council, “FSC Certification Standards,” fsc.org Manufacturers increasingly embed up to 40% post-consumer fiber, signaling a shift toward circular materials. Cost parity with vinyl remains a hurdle, yet tightening VOC regulations and consumer eco-preferences position these substrates for steady adoption through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Competition from Paints and Coatings | -1.4% | Nationwide DIY retail | Medium term (2-4 years) |

| Volatile Raw Material Prices (PVC and Pulp) | -0.8% | Exposure to global commodity cycles | Short term (≤ 2 years) |

| Skilled Labor Shortage for Installation | -0.5% | High-growth metros | Long term (≥ 4 years) |

| Rising Environmental Regulations on VOC Emissions | -0.3% | California and Northeast | Medium term (2-4 years) |

| Supply Chain Disruptions for Specialty Paper | -0.3% | Import-dependent mills | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong Competition from Paints and Coatings

Paint captures roughly 85-90% of interior wall-finishing spend, leveraging lower cost, faster application, and wide contractor familiarity. Sherwin-Williams alone posted USD 6.16 billion net sales in its Paint Stores Group for Q3 2024, underscoring the scale differential facing the US wallcovering market. Premium paint lines with texture additives now mimic wallpaper aesthetics, while consumer perception surveys reveal 60-65% of homeowners see wallpaper removal as a hassle. The DIY channel intensifies the threat because a gallon of quality paint covers 350-400 square feet at USD 30-50, versus USD 50-150 per wallpaper roll covering 25-30 square feet.

Volatile Raw Material Prices (PVC and Pulp)

Polyvinyl chloride resin traded between USD 0.52-0.68 per pound during 2024, squeezing margins for vinyl manufacturers that rely on PVC for 40-50% of their substrate cost. Paper-based suppliers faced pulp price swings of USD 1,150-1,300 per metric ton in the same period. Larger producers hedge 30-40% of annual volume via forward contracts, but smaller firms lack that leverage, creating competitive bifurcation. When commodity spikes outpace a 90-120-day retail repricing window, gross margin compresses by 200-300 basis points, dampening reinvestment capacity across the US wallcovering market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Fabric and Textile Gains on Sustainability Credentials

Fabric and Textile substrates are projected to expand at a 4.43% CAGR, eclipsing overall US wallcovering market growth. In 2025, Vinyl maintained a 38.43% market share lead due to its durability and washability in healthcare corridors, yet its share is eroding under regulatory and recycling pressure. Paper-based products certified by FSC accounted for roughly 20% of volume, thriving in residential spaces despite their moisture sensitivity. Wood veneers, metal foils, and grasscloth together serve less than 10% of demand but capture premium price points that bolster revenue mix.

The segment’s trajectory is reinforced by LEED v4.1 credits and GREENGUARD Gold thresholds that Fabric and Textile options meet without additional treatments. Acoustic damping and tactile differentiation add value in hospitality suites and executive offices. Installation remains the primary hurdle, as seam-matching and paste-the-wall techniques require professional labor, capping DIY penetration but sustaining specialty-contractor margins. Over the forecast period, the United States wallcovering market for Fabric and Textile is expected to gain a growing share of high-value projects, even as Vinyl maintains volume supremacy in price-sensitive environments.

By Product Type: Wall Panels Leverage Installation Speed

Wall Panels headline growth at a 4.63% CAGR through 2031, driven by acoustic performance mandates and DIY-friendly systems. Wallpaper nonetheless anchored 39.32% of 2025 revenue, a testament to its pattern versatility in both hospitality and domestic accent walls. Tile and Metal wall coverings address niche demands in commercial kitchens and design-statement lobbies, respectively.

Interlocking panel kits reduce labor hours by nearly half compared to traditional hanging, trimming installed cost and accelerating project timelines. Acoustic cores with fabric or printed facings satisfy open-office retrofits that seek noise mitigation without constructing hard partitions. Meanwhile, Wallpaper’s integration with digital printing has refreshed pattern diversity, allowing on-demand production of limited runs and murals. The United States wallcovering market size tied to Wallpaper will therefore persist, yet incremental share gains will skew toward panelized solutions that satisfy cost and speed imperatives.

By End-use Industry: Domestic Housing Surges on DIY Platforms

Domestic Housing is forecast to grow at a robust 5.78% CAGR, catalyzed by peel-and-stick technologies and visualization apps that lower the skill threshold for millennial and Gen Z homeowners. In contrast, Hospitality held the largest share, 28.32%, in 2025, as hotel and restaurant refresh cycles rely on Type II vinyl for durability. Healthcare, Retail, Corporate Offices, Education, and Industrial Facilities round out demand, each with specific performance criteria such as antimicrobial coatings or chemical resistance.

Peel-and-stick lines from Wallpops, Tempaper, and Rust-Oleum enable damage-free removal, redefining wallpaper from a permanent investment to a short-cycle design element. Hospitality’s 5-7-year renovation rhythm sustains baseline volume, while healthcare procurement is expanding adoption of silver-ion antimicrobial technology to curb hospital-acquired infections. As DIY platforms scale, the US wallcovering market share for Domestic Housing will widen, yet Hospitality will continue to deliver the highest absolute square-footage consumption.

By Distribution Channel: Franchise Stores Capture Mid-Market Renovators

Specialty Stores secured 31.21% of 2025 revenue with curated assortments, in-home consultations, and installer referrals. Franchise Stores, including Sherwin-Williams’ company-operated network and Benjamin Moore’s independent retailers, are projected to advance at a 5.21% CAGR by pairing brand recognition with neighborhood proximity. E-commerce accounted for roughly one-quarter of 2025 sales, driven by augmented-reality tools from Wizart that let users overlay patterns onto room photos.

Hybrid fulfillment models, such as buy online, pick up in store, mitigate color-matching uncertainty and shorten lead times. For manufacturers, omnichannel integration, harmonizing digital discovery, sample logistics, and professional installation, has emerged as a parity mandate. Successful execution determines exposure to the growing US wallcovering market size in millennial home-renovation cycles.

Geography Analysis

Regional variation inside the United States shapes both demand clusters and product preference. Sun Belt states, Texas, Florida, Arizona, and North Carolina, collectively delivered more than half of all 2024 single-family starts. This construction density concentration brings wholesale distributors and certified installers together, lowering logistics costs and boosting inventory turns. Conversely, the Northeast exhibits the highest penetration of non-woven and paper-based products due to stronger environmental preferences and tighter indoor air-quality codes.

West Coast metros such as Los Angeles, San Francisco, and Seattle display above-average adoption of digitally printed, custom murals, supported by design-centric consumer bases and innovative hospitality projects. Midwestern states remain price-sensitive, favoring durable vinyl wallpapers in healthcare corridors and educational facilities. Rural markets lag in specialty-store coverage, making big-box retailers and franchise paint outlets the primary access points.

E-commerce plays an outsized role in remote geographies where showroom access is limited. However, color fidelity concerns and tactile evaluation needs challenge pure online conversion rates, prompting retailers to expand loaner-sample programs. Freight cost surcharges on rigid panels inhibit penetration in Alaska and Hawaii, whereas peel-and-stick wallpaper ships economically under parcel rates. These logistical nuances underscore how geography modulates the US wallcovering market’s growth vectors at the metro level.

Competitive Landscape

The market is moderately fragmented. Paint conglomerates such as Sherwin-Williams and PPG leverage architectural-coating footprints to cross-sell wallcoverings, bundling finish schedules for contractors and project specifiers. Sherwin-Williams’ USD 3.6 billion acquisition of Sika AG’s North American distribution network in 2024 expanded its contractor branches by 400 locations, illustrating its channel-reach strategy. PPG added low-VOC adhesive capacity through a USD 150 million plant upgrade in Delaware, aligning production assets with environmental demand.

Specialist manufacturers, notably York Wallcoverings and Brewster Home Fashions, differentiate through celebrity collaborations and direct-to-consumer customization portals. York’s “Design Studio” enables pattern, color, and scale tweaks delivered within 10 days. Digital-native disruptors like Spoonflower capitalize on user-generated content, printing one-of-a-kind murals that circumvent wholesale distribution. Technology partnerships, including Wizart’s augmented-reality plug-in for retailer sites, have become table stakes for younger buyers who research entirely online.

Consolidation is expected to continue as scale players acquire digital specialists to capture millennial segments and backfill design agility. At the same time, niche firms will defend high-margin niches through superior artistry, limited-edition drops, and eco-innovations such as recycled-fiber backings. The overall competitive narrative suggests a gradual tilt toward omnichannel ecosystems that marry convenience, customization, and environmental assurance, propelling the US wallcovering market toward its forecast value ceiling.

US Wallcovering Industry Leaders

F. Schumacher & Co.

Crossville Inc.

York Wallcoverings Inc.

Benjamin Moore & Co.

Brewster Home Fashions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sherwin-Williams extended its ColorSnap Visualizer to deliver algorithmic wallpaper-matching at 4,800 stores, embedding cross-category upsell into its mobile app.

- November 2025: PPG Industries finalized a USD 150 million upgrade to its Delaware, Ohio facility, adding water-based adhesive lines for low-VOC wallcovering substrates.

- September 2025: Mohawk Industries partnered with Crossville to co-develop porcelain tile wallcoverings targeting hospitality and retail retrofits.

- July 2025: York Wallcoverings debuted its “Design Studio” portal, offering fully customizable wallpapers shipped in 10 days.

US Wallcovering Market Report Scope

Wallcoverings protect the wall surface from accidental marks or scratches, besides imparting an air of quality and grandeur to uncovered walls. They also help neutralize the interior and customize it with various colors and patterns. Also, these coverings are cost-effective. The two common areas of application of wallcoverings include residential and commercial. Residential wall coverings are primarily used in homes and small businesses to enhance rooms and express individual style.

The US Wallcovering Market Report is Segmented by Material (Paper-Based, Fabric/Textile, Wood-Based, Vinyl, and Other Materials), Product Type (Wall Panel, Wallpaper, Tile, Metal Wall Covering, and Other Product Types), End-use Industry (Hospitality, Healthcare, Retail, Corporate Offices, Education, Domestic Housing, Industrial Facilities, and Other End-use Industries), and Distribution Channel (Specialty Store, Franchise Store, E-commerce, and Other Distribution Channels). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Paper-Based |

| Fabric/Textile |

| Wood-Based |

| Vinyl |

| Other Materials |

By Product Type

| Wall Panel | |

| Wallpaper | Vinyl Wallpaper |

| Non-woven Wallpaper | |

| Paper-based Wallpaper | |

| Fabric Wallpaper | |

| Other Wallpaper Types | |

| Tile | |

| Metal Wall Covering | |

| Other Product Types |

By End-use Industry

| Hospitality |

| Healthcare |

| Retail |

| Corporate Offices |

| Education |

| Domestic Housing |

| Industrial Facilities |

| Other End-use Industries |

By Distribution Channel

| Specialty Store |

| Franchise store |

| E-commerce |

| Other Distribution Channels |

| By Material | Paper-Based | |

| Fabric/Textile | ||

| Wood-Based | ||

| Vinyl | ||

| Other Materials | ||

| By Product Type | Wall Panel | |

| Wallpaper | Vinyl Wallpaper | |

| Non-woven Wallpaper | ||

| Paper-based Wallpaper | ||

| Fabric Wallpaper | ||

| Other Wallpaper Types | ||

| Tile | ||

| Metal Wall Covering | ||

| Other Product Types | ||

| By End-use Industry | Hospitality | |

| Healthcare | ||

| Retail | ||

| Corporate Offices | ||

| Education | ||

| Domestic Housing | ||

| Industrial Facilities | ||

| Other End-use Industries | ||

| By Distribution Channel | Specialty Store | |

| Franchise store | ||

| E-commerce | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How large is the US wallcovering market in 2026?

The US wallcovering market size reached USD 12.01 billion in 2026 and is forecast to climb to USD 14.31 billion by 2031.

Which product category is expected to grow the fastest through 2031?

Wall Panels are projected to expand at a 4.63% CAGR, outpacing all other product types.

What is driving demand in residential applications?

Peel-and-stick wallpapers, e-commerce visualization tools, and millennial DIY activity together fuel a 5.78% CAGR for Domestic Housing.

Why are non-woven and paper-based wallpapers gaining traction?

They meet low-VOC and sustainability criteria, align with LEED v4.1 credits, and offer easier paste-the-wall installation.

Which distribution channel is forecast to gain share?

Franchise paint stores are expected to post a 5.21% CAGR by pairing local inventory with designer partnerships.

Page last updated on: