Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

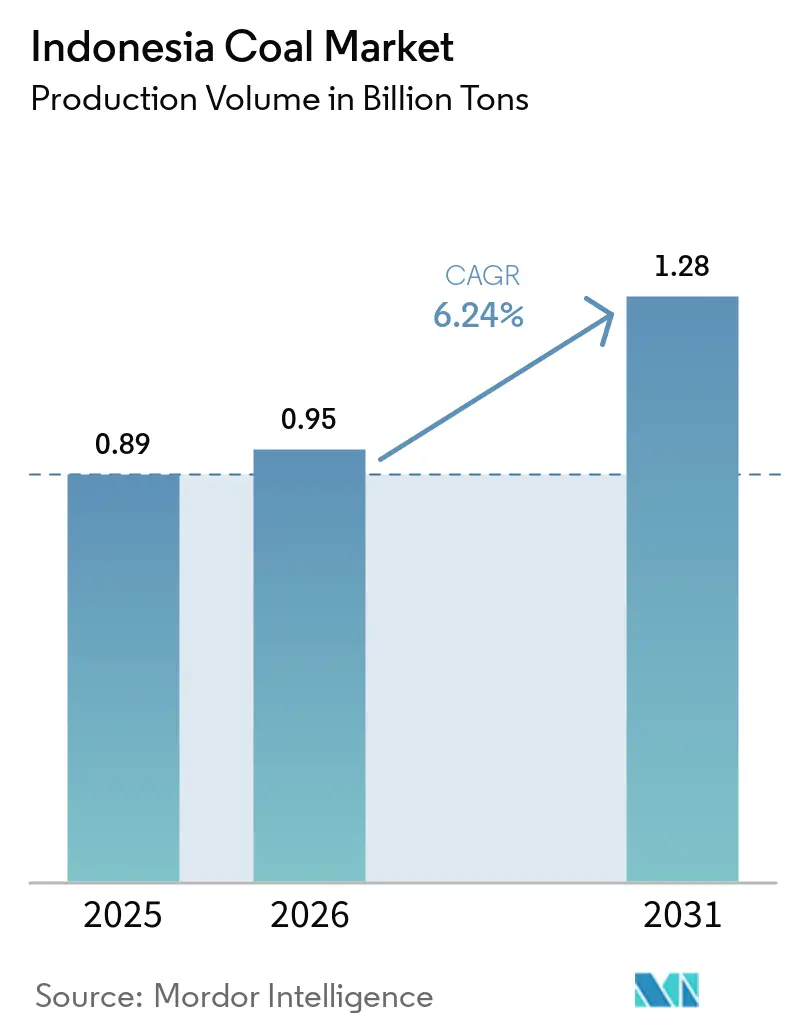

| Base Year Market Size (2025) | 0.89 Billion tons |

| Market Volume (2026) | 0.95 Billion tons |

| Market Volume (2031) | 1.28 Billion tons |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Coal Market Analysis by Mordor Intelligence

The Indonesia Coal market size is expected to grow from 0.89 Billion tons in 2025 to 0.95 Billion tons in 2026 and is forecast to reach 1.28 Billion tons by 2031 at 6.24% CAGR over 2026-2031.

The market’s scale reflects Indonesia’s position as the world’s largest thermal-coal exporter and its entrenched role in the country’s power mix. Ongoing PLN baseload demand, a nickel smelting boom, and a widening China-plus-One strategy collectively underpin demand growth, despite intensifying decarbonization rhetoric. Integrated miners continue to secure long-term offtake contracts that stabilize cash flows, while strategic reserve quality gives premium-grade producers additional pricing power. At the same time, regulatory reforms encouraging gasification and dimethyl-ether projects are opening new domestic outlets for low-rank coal. These parallel trends signal that the Indonesian coal market will remain resilient even as global capital costs for coal rise.

Key Report Takeaways

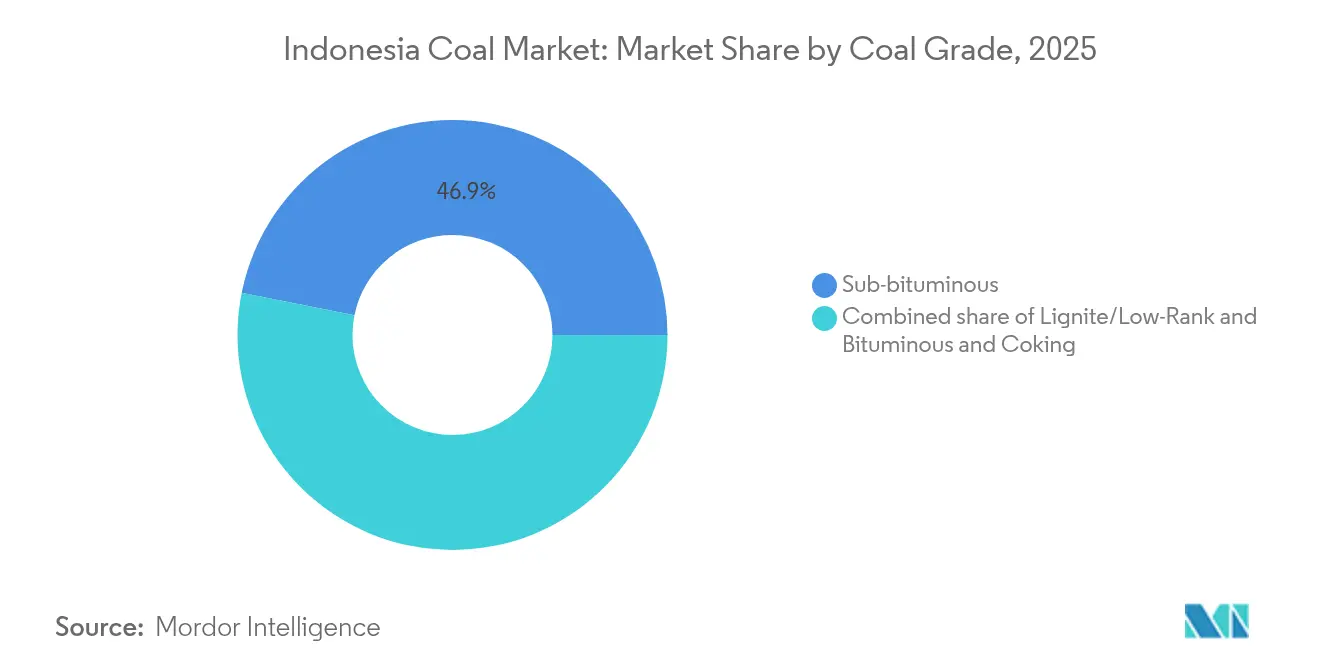

- By coal grade, sub-bituminous coal accounted for 46.85% of the Indonesian coal market share in 2025, whereas bituminous and coking coal grade is expected to grow at an 7.86% CAGR between 2026 and 2031.

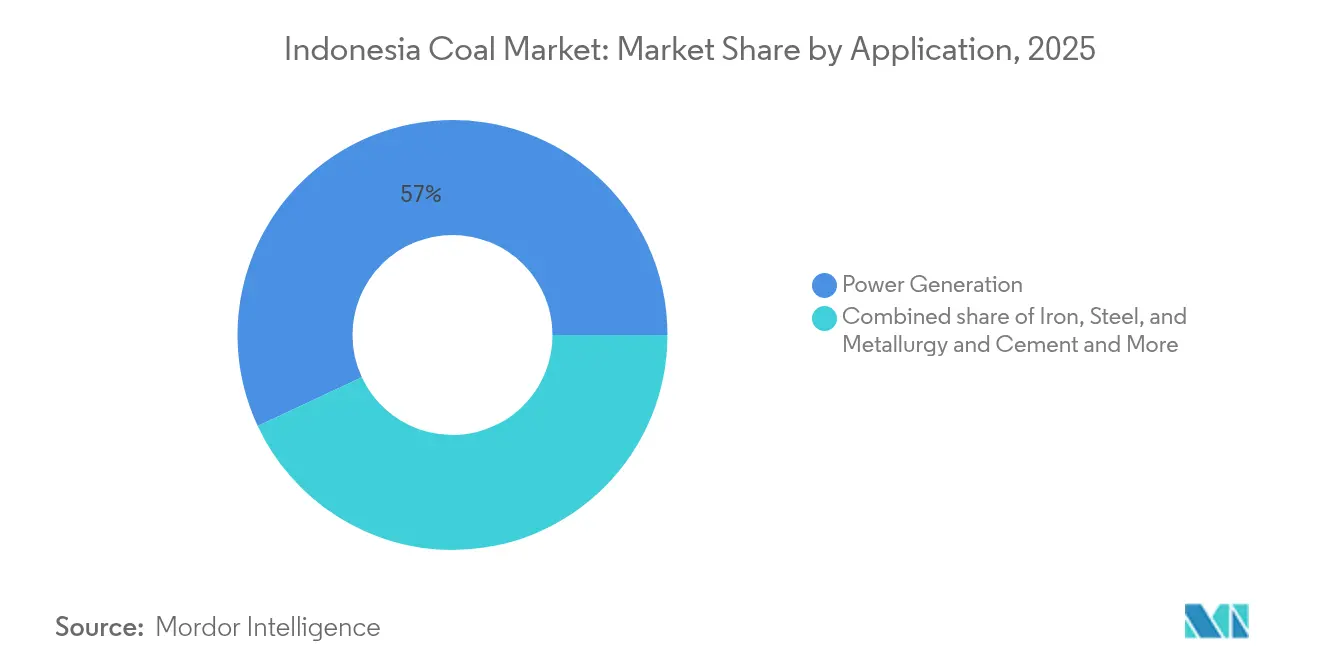

- By application, power generation retained a 56.95% share of the Indonesian coal market in 2025, while the iron, steel, and metallurgy segment is set to grow at an 8.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Coal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged PLN-led baseload demand for low-CV thermal coal | +2.1% | Indonesia domestic | Medium term (2-4 years) |

| Surge in coal-fired captive power for nickel & EV-battery smelters | +1.8% | Indonesia core, APAC spillover | Short term (≤ 2 years) |

| China-plus-One strategy shifting seaborne demand to Indonesia | +1.5% | Global seaborne markets | Medium term (2-4 years) |

| Government "Gasification & DME" incentives for low-rank coal | +0.9% | Indonesia domestic | Long term (≥ 4 years) |

| CCUS pilots unlocking high-CV export premiums | +0.7% | Global export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prolonged PLN-led Baseload Demand for Low-CV Thermal Coal

PLN’s limited headroom for rapid renewable build-out keeps coal in the core of Indonesia’s power dispatch stack.[1]PLN, “RUPTL 2021-2030,” pln.co.id Subsidized electricity tariffs require the utility to prioritize the lowest-cost generation fuel, and sub-bituminous coal remains the most cost-effective option delivered to Java-Bali load centers. Grid stability needs further reinforcement of dispatch preference because coal plants provide frequency and voltage services at a lower marginal cost than battery storage. Financially, PLN’s budget allocation for coal procurement is predictable, reducing counterparties’ credit risk and enabling miners to structure multi-year offtake agreements that lock in volumes. Consequently, the Indonesian coal market benefits from a structural demand floor that persists even as renewable penetration rises incrementally.

Surge in Coal-fired Captive Power for Nickel & EV-battery Smelters

Indonesia’s 2020 nickel-ore export ban sparked capital inflows exceeding USD 15 billion into nickel processing complexes that require uninterrupted power for electric-furnace operations.[2]Center for Strategic and International Studies, “Nickel Processing in Indonesia,” csis.org Chinese-backed smelters routinely install on-site coal plants sized at 200-350 MW, providing a dedicated market immune to PLN’s dispatch priorities. This trend is strengthening the Indonesia coal market, as captive arrangements typically involve dollar-linked power-purchase agreements, which grant miners higher realizations than utility deliveries. The business model thus secures premium margins while diversifying revenue streams. Demand expands further as downstream players move into precursor-cathode and battery materials, linking coal usage paradoxically to the low-carbon economy. These trends keep industrial offtake growth ahead of national average consumption through 2030.

China-plus-One Strategy Shifting Seaborne Demand to Indonesia

Trade realignment since 2022 has seen Northeast Asian utilities and traders shift their focus to Indonesian cargoes as a hedge against geopolitical risk.[3]International Energy Agency, “Coal 2024,” iea.org This shift has provided strong support to the Indonesia coal market. China imported 543 million tons of coal in 2024, with Indonesian origin covering the majority of the incremental tonnage as buyers curtailed their exposure to Australian and Russian sources. Shorter sailing distances result in freight savings of USD 3-4 per ton compared to South African or Colombian supply, thereby strengthening Indonesia’s landed-cost advantage. Forward indicators such as coal-charter activity out of Samarinda and Kalimantan ports show sustained spot-market liquidity even during price corrections. By reducing single-source dependency, the China-plus-One policy anchors a resilient export outlet for Indonesian producers.

Government “Gasification & DME” Incentives for Low-rank Coal

Revised mining regulation PP 25/2024 obliges permit holders to demonstrate concrete value-addition plans, such as syngas, methanol, or DME production, before qualifying for license extensions. Fiscal perks include accelerated depreciation, VAT exemptions, and import-duty relief on gasification equipment. Pilot projects in South Sumatra aim to convert up to 6 million tons per year of lignite once commercialized, potentially absorbing output that would otherwise fetch discounts in export markets. Downstream integration diversifies domestic demand and positions Indonesia as a regional supplier of coal-derived chemicals, thereby cushioning the Indonesian coal market from volatility in seaborne steam coal benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Domestic Market Obligation (DMO) price caps | -1.2% | Indonesia domestic | Short term (≤ 2 years) |

| Accelerated coal-plant retirement under JETP funding | -0.8% | Indonesia, APAC region | Medium term (2-4 years) |

| Provincial moratoria on new mining permits (Kalimantan, Sumatra) | -1.1% | Kalimantan, Sumatra provinces | Short term (≤ 2 years) |

| Rising ESG-driven trade financing costs for Indonesian coal | -0.6% | Global trade financing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Domestic Market Obligation (DMO) Price Caps

Indonesia’s DMO mechanism obliges miners to sell 25% of annual output at a government-set benchmark that trails export parity by up to USD 30 per ton during high-price cycles.[4]Ministry of Energy and Mineral Resources, “Domestic Market Obligation Regulations,” esdm.go.id This enforced discount compresses margin expansion opportunities and incentivizes firms to skew production toward higher-CV grades, which are earmarked exclusively for export. Financiers increasingly mark down reserve valuations that are exposed to DMO ceilings, complicating debt-raising for expansion. Although the policy shields PLN and industrial buyers from price spikes, it reduces investment appetite in new low-rank coal projects, thereby dampening incremental supply growth in the Indonesian coal market.

Accelerated Coal-plant Retirement under JETP Funding

The USD 20 billion Just Energy Transition Partnership proposes to retire up to 5 GW of subcritical coal capacity before 2030, starting with the 660 MW Cirebon-1 unit. Early closure mechanically lowers domestic demand once decommissioning occurs, and associated refinancing covenants restrict the building of replacement coal assets. Utilities must balance lost generation with renewable additions or higher-efficiency ultra-supercritical units, creating planning uncertainty for coal suppliers in the Indonesia coal market. While rollout logistics depend on multilateral-funding milestones, the direction of travel is clear: an eventual tightening of the domestic demand outlook beyond the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coal Grade: Premium Grades Gain Market Share

Sub-bituminous coal accounted for 46.85% of the Indonesia coal market in 2025, leveraging abundant East and South Kalimantan seams that deliver cost-competitive fuel to both domestic and export buyers. Despite this current dominance, bituminous and coking coal output is forecast to grow at an 7.86% CAGR between 2026 and 2031, lifting its share of the Indonesian coal market from 26.40% in 2025 to nearly one-third by 2031. Higher-CV grades unlock premiums of USD 15-20 per ton and align with emerging ultra-supercritical power-plant specifications in Asia. Metallurgical coal demand from regional blast furnaces further reinforces pricing power for producers with suitable reserve quality. Lignite remains oriented toward domestic gasification pilots and legacy low-efficiency boilers, implying flat growth. Production geography mirrors grade distribution; East Kalimantan operators, such as Kaltim Prima Coal, focus on premium grades, whereas Sumatra miners largely supply sub-bituminous coal to PLN. This quality segmentation enables portfolio balancing, as companies hedge against market swings by adjusting blend ratios between grades according to price differentials and logistics economics.

By Application: Iron, Steel, and Metallurgy Drives Growth

The power generation application captured 56.95% of the Indonesia coal market share in 2025, underscoring the fuel’s pre-eminent role in national baseload generation. However, the iron, steel, and metallurgy segment is forecast to post an 8.68% CAGR through 2031, outpacing all other segments as downstream battery-metal processing proliferates. The Indonesian coal market size allocated to industrial captive units is projected to increase from 51.60 million tons in 2026 to more than 84.20 million tons by 2031, reflecting the construction of new integrated stainless-steel and cathode-precursor complexes in Sulawesi and North Maluku. Electricity remains indispensable to PLN’s load curve, yet its growth rate moderates to mid-single digits once the current coal-plant pipeline is completed. In contrast, smelter offtake is tied to contractual power-purchase agreements that guarantee coal burn irrespective of utility dispatch. Demand in the iron and steel sector remains steady as domestic rebar consumption tracks Indonesia’s expansive toll-road and urban-rail programs, albeit at a slower expansion pace than smelter power. Cement firms’ incremental fuel demand aligns with urbanization and new capital-city infrastructure in East Kalimantan, but their cumulative coal requirement stays below 5% of total volume. The captive-power surge thus reorients incremental growth toward industrial users, giving miners a diversified outlet less exposed to PLN policy shifts.

Geography Analysis

East Kalimantan controls 38% of Indonesia’s 11.59 billion-ton proven coal reserve base, anchoring the nation’s export logistics and supporting the reliability of the Indonesian coal market’s supply. The province’s Samarinda and Bontang ports offer year-round, deep-water loading that supports Capesize charters and shortens voyage times to key North Asian consumers. South Kalimantan contributes additional output, albeit with lower-CV coal that primarily fills PLTU power plant contracts and spot tenders in the Philippines or Vietnam. Sumatra’s Musi Basin holds significant lignite assets and supplies PLN’s Sumbagsel grid; however, draft limitations on the Musi River constrain shipment sizes, resulting in higher freight costs that narrow export competitiveness.

Provincial governments have begun revising royalty structures to increase fiscal revenue, exemplified by East Kalimantan’s Perda 1/2024, which increases local levies by 2 percentage points; this policy is likely to prompt similar moves in peer provinces. Infrastructure remains a swing factor; ongoing rail spur upgrades linking North Maluku mines to Obi Island smelters will unlock incremental capacity dedicated to captive power in the Indonesia coal market. Meanwhile, the revocation of 526,144 hectares of forest concessions indicates tighter ecological oversight, particularly in biodiversity-rich Papua and West Papua, which may potentially delay the development of greenfield mines. Permit issuance momentum diverges by region: Central Kalimantan’s de facto moratorium curtails licenses, whereas South Sumatra actively courts investment under its gasification roadmap.

Taken together, geographic dynamics produce a supply landscape that is both concentrated for exports and regionally fragmented for domestic consumption, reinforcing Indonesia’s position as a price setter in Pacific Basin thermal-coal trade while allowing policy levers at the provincial level to shape marginal growth.

Competitive Landscape

The Indonesian coal market is moderately concentrated, with integrated majors such as Bumi Resources, Adaro Energy, and Bayan Resources collectively controlling more than half of the national output, yet competing vigorously on grade mix, logistics, and cost structure. These producers own dedicated hauling roads, barge fleets, and export terminals, compressing unit costs to below USD 40 per ton free on board and securing delivery reliability for term buyers. Bayan Resources posted an industry-leading net profit margin of 25.7% in 2024, following the debottlenecking of its Tabang concession and the implementation of high-wall mining, which improved the efficiency of strip ratios. Adaro remains the benchmark for ultra-low-sulfur coal, enabling premium realization in Japan and Korea. Mid-tier firms, such as Geo Energy and Delta Dunia, position themselves as flexible contractors or niche-grade suppliers, leveraging outsourced mining services to scale quickly without incurring heavy capital expenditures (capex).

Financially, Indonesia coal companies hold a combined cash balance of USD 6.8 billion, furnishing headroom for downstream investments in gasification or CCUS pilots. Bumi Resources’ pledge to sustain an annual production of 78-80 million tons by tapping its 2.4 billion-ton reserve base signals supply continuity, while its articulated USD 6 billion revenue target for 2025 underscores confidence in its price and volume outlook. Competitive differentiation is shifting toward carbon-compliance optionality; miners with pilot CCUS tie-ins or renewable offsets can secure longer-dated contracts with ESG-sensitive buyers, preserving market access as financing screens tighten.

Indonesia Coal Industry Leaders

PT Bumi Resources Tbk

PT Adaro Energy Indonesia Tbk

PT Bayan Resources Tbk

PT Bukit Asam Tbk

PT Indo Tambangraya Megah Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Indonesia's mining ministry has identified 18 projects, collectively valued at USD 38.6 billion, aimed at harnessing the nation's natural resources. These projects have been presented to Danantara Indonesia, the sovereign wealth fund, for potential investment.

- February 2025: The Indonesian government announced plans to revoke forest-management permits covering 526,144 hectares, signaling stricter ecological oversight over future mine expansions.

- December 2024: As of December 30, 2024, national coal production in Indonesia hit 812.04 million tons, as reported by the Ministry of Energy and Mineral Resources (ESDM). Data from ESDM's Minerba One Data Indonesia (MODI) reveals that out of the total production, domestic consumption accounted for 365.70 million tons. In contrast, coal exports reached 417.57 million tons, falling short of the 2024 target of 490 million tons.

- November 2024: Indonesia's government has set a bold target to eliminate coal-fired power generation by 2040, pulling the deadline forward from an earlier 2056 goal. This announcement, made during the G20 Summit in Rio de Janeiro, Brazil, also reaffirms the nation's commitment to constructing over 75 GW of renewable energy capacity by the same 2040 deadline.

Indonesia Coal Market Report Scope

Coal is a sedimentary deposit primarily constituted of carbon and is readily combustible. Coal is black or brownish-black in color and contains more than 50% carbonaceous material by weight and more than 70% by volume (including inherent moisture). It comprises plant remains that are compacted, hardened, chemically altered, and metamorphosed by heat and pressure throughout geologic time. Coal can be found worldwide. However, it is most common in areas where prehistoric forests and marshes formerly flourished before being buried and compressed over millions of years.

The report provides the market size and forecasts for the Indonesian Coal Market in terms of production volume (tons) for all the aforementioned segments. The Indonesian coal market report includes:

By Coal Grade

| Lignite/Low-Rank |

| Sub-bituminous |

| Bituminous and Coking |

By Application

| Power Generation |

| Iron, Steel, and Metallurgy |

| Cement and Other Applications |

| By Coal Grade | Lignite/Low-Rank |

| Sub-bituminous | |

| Bituminous and Coking | |

| By Application | Power Generation |

| Iron, Steel, and Metallurgy | |

| Cement and Other Applications |

Key Questions Answered in the Report

What is the projected Indonesia coal market size by 2031?

The Indonesia coal market size is forecast to reach 1,278.96 million tons by 2031, expanding at a 6.24% CAGR.

Which application segment is growing fastest in the Indonesia coal market?

Iron, Steel, and Metallurgy is projected to register a 8.68% CAGR through 2031, outpacing all other applications.

How significant is Indonesia’s role in global coal trade flows?

Indonesia captured 34% of global seaborne coal trade in 2023, reinforcing its status as the world’s largest thermal-coal exporter.

What regulatory factor most constrains coal-producer margins domestically?

The Domestic Market Obligation policy, which caps prices for 25% of production sold domestically, trims margins by up to USD 30 per ton during high-price periods.

How will the Just Energy Transition Partnership (JETP) affect coal demand?

JETP’s targeted retirement of 5 GW of subcritical capacity before 2030 will gradually lower PLN’s coal consumption, tempering long-term domestic demand growth.

Why are premium bituminous and coking grades set to gain share?

Higher-energy grades attract price premiums and align with efficient power-plant and steel-making requirements, driving a forecast 7.86% CAGR for the segment between 2026-2031.

Page last updated on: