Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

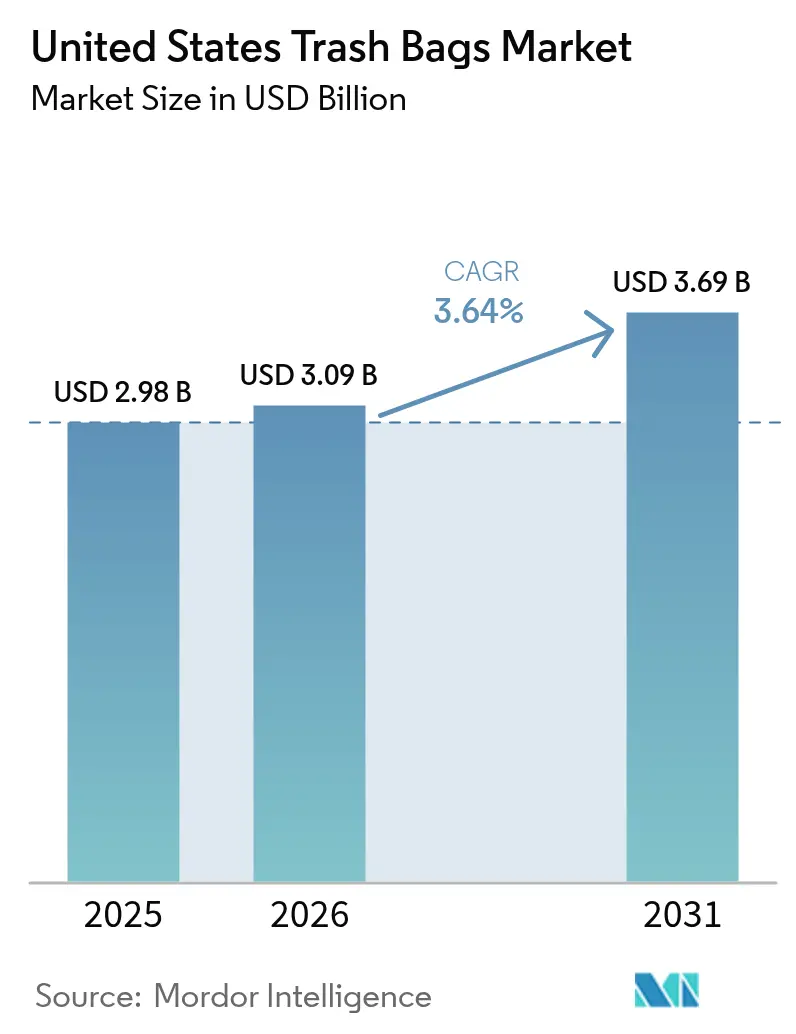

| Base Year Market Size (2025) | USD 2.98 Billion |

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 3.69 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Trash Bags Market Analysis by Mordor Intelligence

United States trash bags market size in 2026 is estimated at USD 3.09 billion, growing from 2025 value of USD 2.98 billion with 2031 projections showing USD 3.69 billion, growing at 3.64% CAGR over 2026-2031. Waste-segregation mandates from healthcare, foodservice, and municipal sectors are the principal growth engine, while packaging waste-28.1% of the 292.4 million-ton municipal solid waste (MSW) stream in 2024-reinforces steady household and commercial demand.[1]“Advancing Sustainable Materials Management: 2018 Fact Sheet,” U.S. Environmental Protection Agency, epa.gov Resin price swings linked to Gulf Coast production constraints add cost volatility, yet material innovation in compostable films and recycled-content polyethylene sustains margin defense. Institutional buyers accelerate adoption of antimicrobial and color-coded containment solutions to comply with Centers for Disease Control and Prevention (CDC) infection-control protocols. Meanwhile, subscription-based e-commerce channels reconfigure procurement patterns, enabling bulk purchasing and automated replenishment for commercial facilities.

Key Report Takeaways

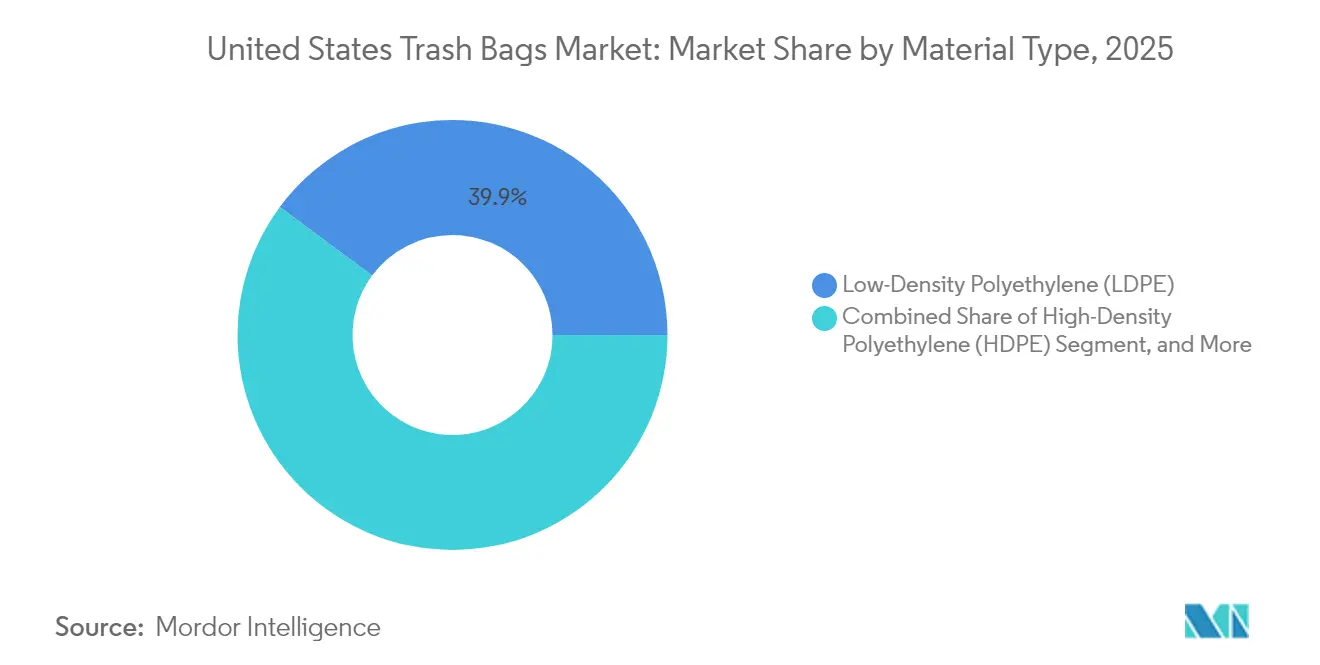

- By material type, Low-Density Polyethylene (LDPE) held 39.85% of the United States trash bags market share in 2025. Bio-based/biodegradable plastics are projected to expand at a 4.52% CAGR through 2031, the fastest growth rate among all materials.

- By capacity, the above-30-gallon segment is advancing at a 4.91% CAGR between 2026 and 2031.

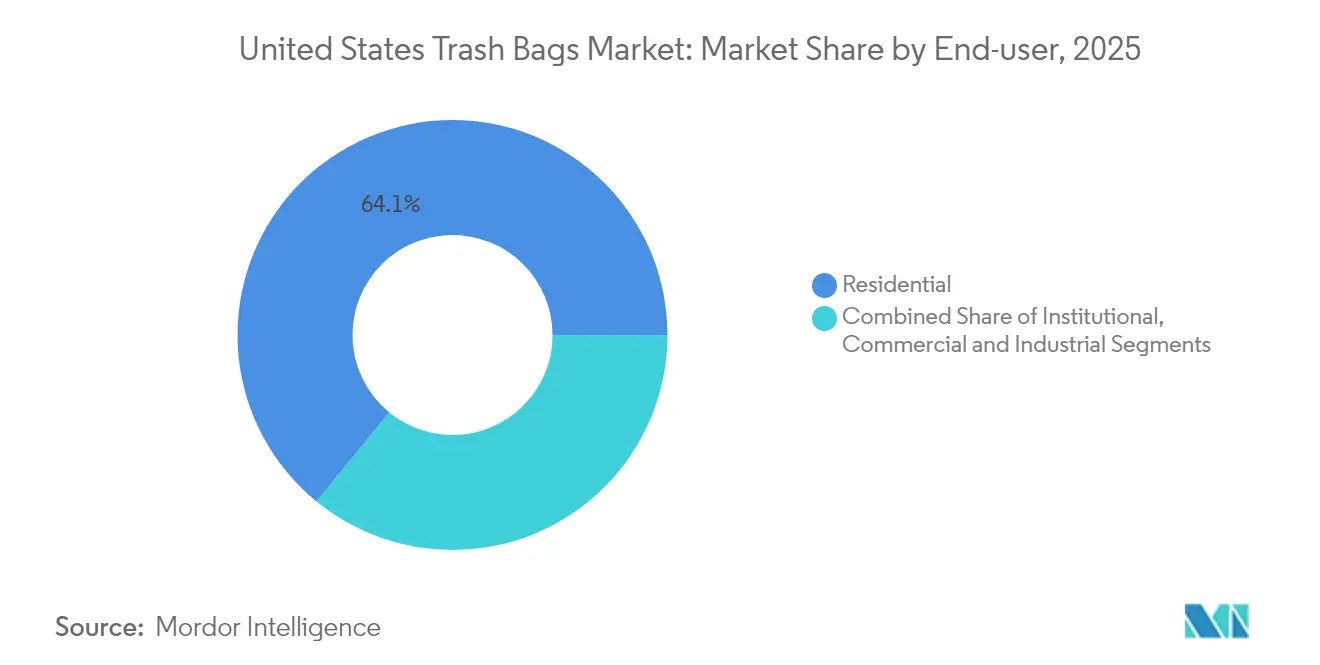

- By end-user, institutional applications are forecast to grow at a 4.74% CAGR, while residential demand retained 64.10% of the United States trash bags market size in 2025.

- By distribution channel, online retail recorded the highest CAGR at 5.05%, in contrast to offline retail’s 54.10% revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Trash Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for compostable and oxo-biodegradable bags | +0.9% | National, concentrated in CA, OR, WA, VT | Medium term (2-4 years) |

| Rising hygiene and waste-segregation mandates | +0.7% | National, emphasis on healthcare/institutional | Short term (≤ 2 years) |

| E-grocery boom increasing household bag consumption | +0.6% | National, urban concentration | Short term (≤ 2 years) |

| Adoption of antimicrobial additive-infused bags | +0.4% | National, healthcare/foodservice focus | Medium term (2-4 years) |

| State-level EPR nudging thicker recyclable bags | +0.5% | CA, CO, ME, OR, MN, MD | Long term (≥ 4 years) |

| Smart dispenser subscriptions for refill bags | +0.3% | National, commercial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for compostable and Oxo-biodegradable bags

Municipal organics diversion mandates create a verified customer base for ASTM D6400-certified liners. Vermont’s Universal Recycling Law, for example, compels businesses that generate more than 26 gallons of food waste weekly to adopt certified compostable containment, while USD 32 million in federal infrastructure grants awarded in 2024 is expanding industrial composting capacity from 185 to a projected 275 facilities by 2027.[2]“Universal Recycling Law Implementation Guide,” Vermont Agency of Natural Resources, anr.vermont.gov Despite strong policy pull, polylactic acid (PLA) liners still require ≥ 140 °F industrial composting temperatures and experience moisture sensitivity during transport; laboratory studies show degradation windows ranging from 90 days in optimized facilities to 180 days in less-controlled environments.

Rising hygiene and waste-segregation mandates

CDC infection-control guidance instructs healthcare providers to differentiate general, regulated medical, and pharmaceutical waste streams, prompting purchases of color-coded or antimicrobial bags certified under FDA 21 CFR 178.3297. A 500-bed hospital generates 25–30 pounds of waste per occupied bed each day, 85% of which still falls under “general” MSW, yet cannot commingle with retail refuse due to cross-contamination risk. The Joint Commission requires all 6,090 U.S.-accredited hospitals to document waste-handling protocols, enlarging the addressable institutional volume.

E-grocery boom increasing household bag consumption

E-commerce food sales reached USD 9.3 billion in 2024, and each delivered order introduces 4–7 discrete packaging components into the residential waste stream. Research shows households discard 23–35% more material than in-store shoppers, and 78% place all delivery packaging into conventional trash bags rather than specialized recycling programs. New York City recorded a 12% increase in residential MSW tonnage in direct correlation with on-demand grocery adoption, demonstrating regional intensity in urban markets.

Adoption of antimicrobial additive-infused bags

Silver or copper nanoparticle formulations achieve 99.9% bacterial reduction within 24 hours per ISO 22196 tests, addressing pathogen-control requirements in hospitals and restaurant back-of-house operations. Patent US 11,234,567 codifies a dispersion method that preserves tensile strength, enabling healthcare-compliant films without sacrifice of load-bearing capacity. The National Restaurant Association’s 2024 survey found 67% of establishments prioritize antimicrobial packaging to satisfy revised ServSafe standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictions on single-use plastics | -0.8% | CA, OR, WA, NY, expanding nationally | Short term (≤ 2 years) |

| Volatility in virgin resin prices | -0.5% | National, Gulf Coast production centers | Short term (≤ 2 years) |

| Composting infrastructure curbing conventional bags | -0.4% | Regional, expanding with infrastructure | Medium term (2-4 years) |

| Trash compactors reducing bag consumption | -0.3% | Commercial/industrial facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Restrictions on single-use plastics

California’s SB 54 imposes graduated producer fees and market-access limitations that add compliance costs equivalent to 8–12% of product revenue, while 127 plastic regulation bills introduced across 35 states in 2024 indicate broadening policy risk.[3]“2024 Plastic Legislation Tracking,” National Conference of State Legislatures, ncsl.org Producers that fail to meet recycled-content or reduction targets may face shelf-space bans.

Volatility in virgin resin prices

LDPE film-grade prices fluctuated 18–25% per quarter in 2024 as Hurricane Francine temporarily idled six petrochemical complexes, cutting domestic output by 15%. Raw materials account for 65–75% of total manufacturing costs; margin protection, therefore, hinges on dynamic pricing clauses, hedging instruments, or feedstock diversification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bio-based Films Gain Momentum

Low-Density Polyethylene commanded 39.85% of the United States trash bags market share in 2025, supported by low cost and broad processing infrastructure. Yet bio-based/biodegradable plastics are on track for a 4.52% CAGR, the highest among all materials, propelled by municipal composting mandates. Within this segment, PBAT-PLA blends that meet ASTM D6400 standards can achieve industrial compostability within ninety days and run on existing blown-film lines, mitigating capital outlay for converters. A derivative patent, US 11,456,789, details chain-extending additives that enhance tear resistance to match LDPE. Post-consumer recycled (PCR) polyethylene is another fast-emerging subset because EPR statutes specify minimum PCR thresholds for bags used in curbside programs.

Regulatory oversight guides formulation choices. FDA 21 CFR 174.5 regulates recycled materials in indirect food-contact articles, while ASTM D6400 certification is vital for access to organics diversion tenders. Producers that can combine PCR inclusion and compostability credentials enjoy premium positioning, particularly in California, Oregon, and Vermont, where procurement policies award compliance points for each attribute.

By Capacity/Bag Size: Large Formats for Commercial Efficiency

The above-30-gallon category is the fastest-growing band at a 4.91% CAGR, riding on central waste-station designs in hospitals, airports, and educational campuses. Larger liners extend collection intervals and cut janitorial labor by 25-40%, outcomes backed by CDC studies on infection-risk mitigation. Manufacturing these large formats requires multi-layer die heads and tighter gauge-control systems to avoid weak sidewalls; only the top tier of converters now owns such capabilities, reinforcing competitive barriers.

The 13-30-gallon bracket held 38.20% of the United States trash bags market size in 2025, favored for versatility in residential kitchens and commercial restrooms. Up to 3-gallon and 3-13-gallon bags remain niche but indispensable for food-prep zones and biomedical sample transport. Meanwhile, trash-compactor liners in the 2.0-3.0-mil gauge class command higher price points but fewer units sold, slightly diluting overall volume growth for standard gauges.

By End-user: Hospitals Propel Institutional Uptake

Residential consumption accounted for 64.10% of 2025 revenue, anchored by routine household disposal. However, institutional facilities-hospitals, long-term care centers, government buildings-are forecast to grow at 4.74% CAGR, notably faster than the aggregate market. A 500-bed hospital may segregate fifteen waste fractions, each needing a distinct liner color, antimicrobial efficacy, or load specification. CDC infection-control protocols and Joint Commission compliance audits hard-wire these requirements into multiyear procurement contracts, creating sticky demand. Commercial and industrial (C&I) users focus on cost-out programs; micro-layered film structures that deliver thinner gauges without tensile loss appeal strongly to big-box retail and quick-service restaurant chains.

Academic work confirms antimicrobial liners can cut surface cross-contamination by 45-60%, helping hospitals justify premiums of 8-15% over conventional products. That cost delta is often recouped through reduced healthcare-associated infection (HAI) penalties.

By Distribution Channel: Digital Platforms Rewrite Logistics

Online retail, encompassing both direct-to-consumer and B2B portals, is logging a 5.05% CAGR through 2031 by offering tiered subscription bundles, bulk-order discounts, and real-time tracking. Hospitals adopting centralized e-procurement shaved 30-40% off administrative overhead by automating approvals and consolidating shipments across multiple campuses. Integration with smart dispensers amplifies savings by syncing reorder triggers with consumption data.

Even with these gains, offline retail still controls 54.10% of 2025 revenue by leveraging storefront immediacy and merchandising end-caps. DIY big-box outlets cater to emergency household restocking, especially during weather events when online lead times stretch. Distributors serving C&I accounts add value through technical training and liner-fit audits, a service bundle not easily replicated by pure-play e-commerce entrants.

Geography Analysis

West Coast states form the epicenter of sustainable packaging regulation. California’s SB 54 stipulates a 65% recycling rate and 25% recycled content in all plastic packaging by 2032, pushing local buyers to specify thicker, higher-grade films with PCR content. Oregon and Washington have adopted parallel frameworks, accelerating the shift toward bio-based liners. Vermont’s Universal Recycling Law fuels demand for compostable liners in New England, although those sales remain smaller in absolute dollar terms.

The Northeast balances strong environmental policy with mature recycling infrastructure; 175+ municipalities in Massachusetts now operate curbside organics collection that accepts ASTM D6400-certified bags. Household waste generation averages 4.2 pounds per capita per day, below the 4.9-pound national norm, reflecting higher diversion rates. Although volumes are modest, unit margins are higher because of consumer willingness to pay for certified products.

The Southeast and Gulf Coast constitute the country’s polymer backbone, with Louisiana alone housing 45% of the United States' LDPE capacity. Competitive resin pricing lowers conversion costs, yet recurring hurricane disruptions require robust contingency inventories. Growth corridors in Texas, Florida, and North Carolina-fueled by migration and tourism-are raising MSW tonnage, but fragmented local regulation slows uptake of premium sustainable liners.

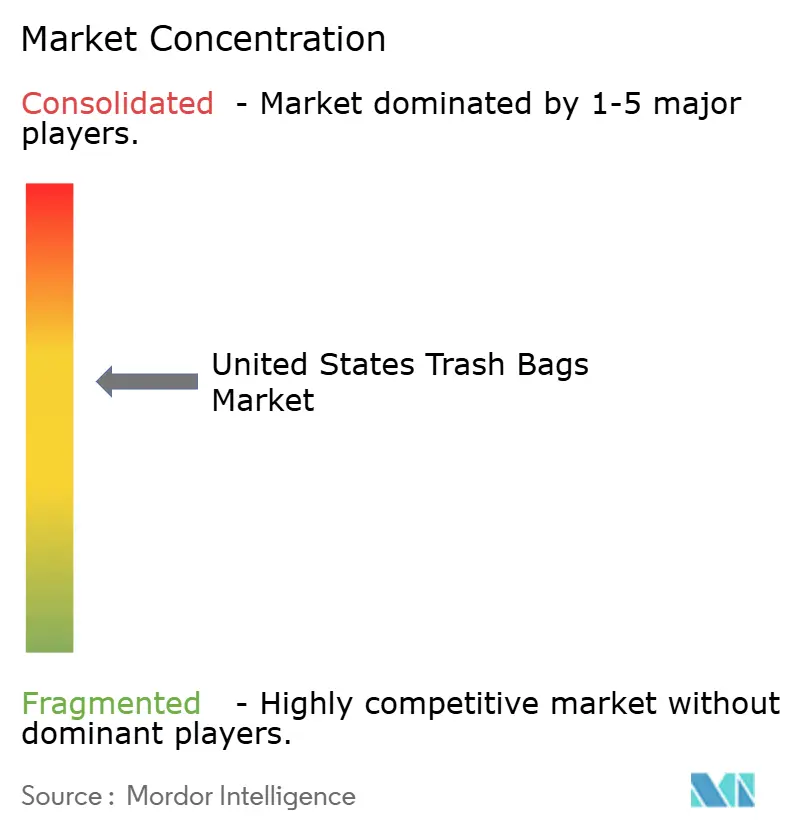

Competitive Landscape

The United States trash bags market is moderately consolidated. Reynolds Consumer Products and The Clorox Company (Glad) collectively control a significant share of branded retail aisles, while Novolex, Inteplast, and Heritage Bag dominate private-label and institutional contracts. Reynolds invests USD 15 million in an Illinois center dedicated to compostable and recycled-content R&D, aiming to keep Hefty at the performance frontier. The Clorox Company recently introduced Glad ForceFlex Plus bags with 50% PCR and ASTM D6400 certification, positioning the brand as a dual-attribute leader.

Novolex’s acquisition of Advanced Plastics Manufacturing expands PBAT-PLA output by 40%, signaling a strategic intent to service organics-diversion programs. Inteplast’s USD 45 million investment in recycled-content lines in Texas enables a rapid response to PCR mandates in California, Colorado, and Maine. Patent analytics reveal 25% year-on-year growth in filings related to antimicrobial polymers and smart dispensing, with smaller innovators like Crown Poly and Aluf Plastics carving out niches through technological edge.

Overall, the top five players hold roughly 60–65% of revenue, yielding a competitive intensity that supports brand investment yet leaves room for niche entrants with differentiated sustainability or IoT value propositions.

United States Trash Bags Industry Leaders

Amcor plc

Reynolds Consumer Products Inc.

Novolex Holdings, LLC

Inteplast Group Corporation

Riverside Paper Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Glad expanded its sustainability portfolio with ForceFlex MaxStrength trash bags made from recovered plastic materials, broadening recycled-content offerings for mainstream retail.

- June 2025: Novolex secured BPI commercial compostability certification for its shopping and lawn trash-bag lines, paving the way for wider adoption in municipal organics-collection programs.

- May 2025: Washington enacted SB 5284, a statewide packaging extended-producer-responsibility law that places recycled-content and stewardship requirements on plastic trash-bag producers beginning in 2026.

- April 2025: Glad introduced a kitchen trash-bag line marketed as “2× stronger,” engineered to reduce tearing and leakage-key consumer pain points.

United States Trash Bags Market Report Scope

The report on the US trash bags market provides the demand value of trash bags offered by various vendors operating in the market. The market has been tracked from a consumption perspective. This report analyzes factors such as the impact of raw materials, drivers, and challenges in the market based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The trash bags market in the United States is divided into three sub-segments based on end user: residential, commercial, and industrial. The market sizes and forecasts for all the above segments are provided in terms of value (USD).

By Material Type

| High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) |

| Bio-based/Biodegradable Plastics (PLA, PBAT, PHA) |

| Other Material Types |

By Capacity / Bag Size

| Up to 3 Gallons |

| 3–13 Gallons |

| 13–30 Gallons |

| Above 30 Gallons |

By End-user

| Residential |

| Institutional (HoReCa, Healthcare, Education) |

| Commercial and Industrial |

By Distribution Channel

| Offline Retail (Supermarkets, Warehouse Clubs, Convenience Stores) |

| Online Retail |

| B2B / Institutional Sales |

| By Material Type | High-Density Polyethylene (HDPE) |

| Low-Density Polyethylene (LDPE) | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Bio-based/Biodegradable Plastics (PLA, PBAT, PHA) | |

| Other Material Types | |

| By Capacity / Bag Size | Up to 3 Gallons |

| 3–13 Gallons | |

| 13–30 Gallons | |

| Above 30 Gallons | |

| By End-user | Residential |

| Institutional (HoReCa, Healthcare, Education) | |

| Commercial and Industrial | |

| By Distribution Channel | Offline Retail (Supermarkets, Warehouse Clubs, Convenience Stores) |

| Online Retail | |

| B2B / Institutional Sales |

Key Questions Answered in the Report

How large is the United States trash bags market in 2026?

The market is valued at USD 3.09 billion in 2026 with a forecast CAGR of 3.64% through 2031.

Which material dominates liner production?

LDPE holds 39.85% of United States trash bags market share, although bio-based alternatives are the fastest-growing segment.

Why are above-30-gallon bags growing quickly?

Hospitals, airports, and other institutions favor large liners for labor efficiency, giving this segment a 4.91% CAGR forecast.

How are extended producer responsibility (EPR) laws affecting supplier strategy?

EPR mandates push manufacturers to integrate PCR content and produce thicker, mechanically recyclable films to maintain market access.

What advantages do smart dispenser systems offer?

They automate re-ordering, cut inventory labor by up to 80%, and align liner type with waste-stream segregation rules.

Which distribution channel is expanding fastest?

Online retail is advancing at a 5.05% CAGR due to subscription models and platform-based bulk procurement.

Page last updated on: