Ophthalmic Examination Chairs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

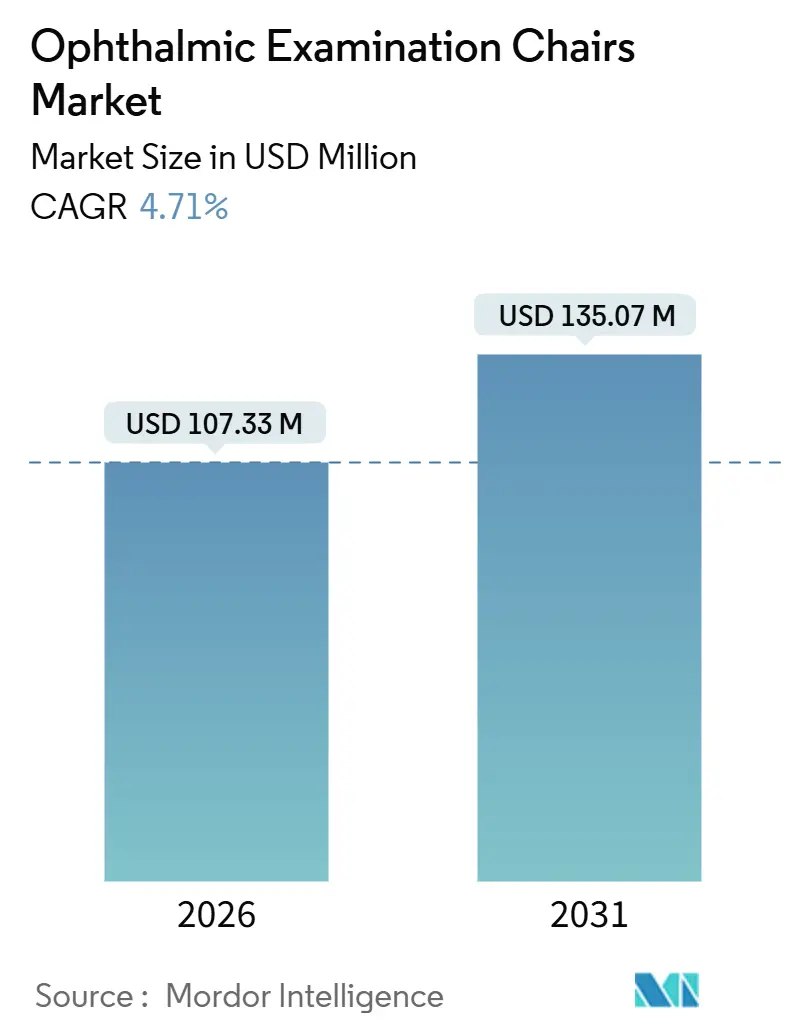

| Market Size (2026) | USD 107.33 Million |

| Market Size (2031) | USD 135.07 Million |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

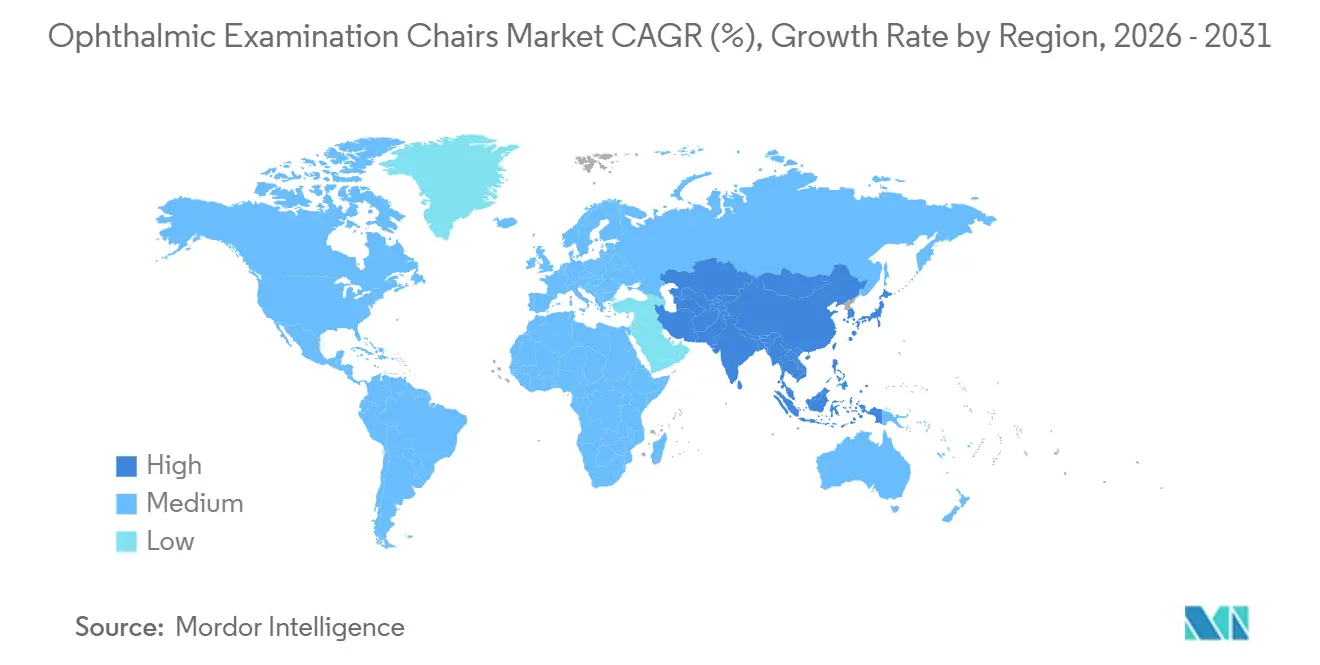

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmic Examination Chairs Market Analysis by Mordor Intelligence

The Ophthalmic Examination Chairs Market size is estimated at USD 107.33 million in 2026, and is expected to reach USD 135.07 million by 2031, at a CAGR of 4.71% during the forecast period (2026-2031).

Heightened demand for routine and surgical eye-care visits among aging populations, the growing incidence of diabetes-related vision disorders, and the worldwide expansion of ambulatory surgical centers are the primary forces driving the ophthalmic examination chairs market. Clinics are directing capital toward automatic, electric models that improve patient throughput, reduce clinician fatigue, and integrate smoothly with digital imaging systems. At the same time, stretched hospital budgets and the decade-plus service life of existing equipment temper replacement cycles, creating a balanced but opportunity-rich landscape. Vendors that bundle chairs with diagnostic platforms, antimicrobial upholstery, and tele-ophthalmology compatibility are positioned to capture outsized share as procurement teams seek holistic solutions.

Key Report Takeaways

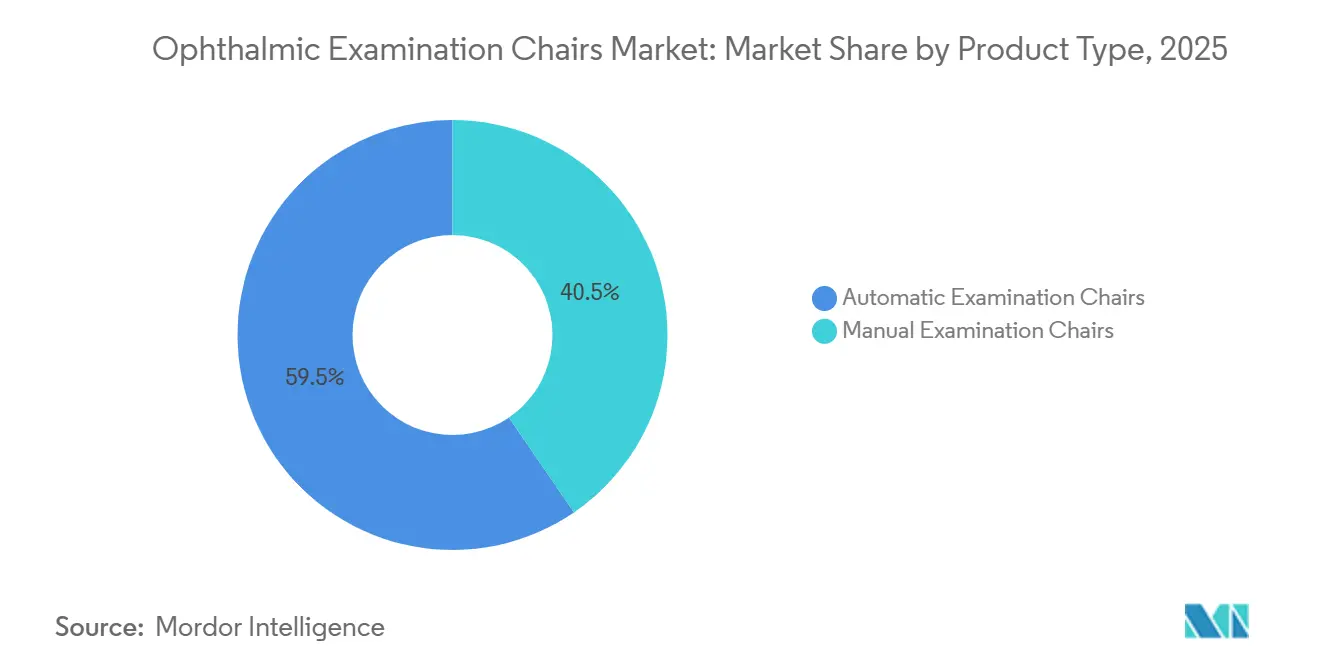

- By product type, automatic chairs led with 59.55% revenue share in 2025 and are projected to grow at a 6.25% CAGR through 2031.

- By mechanism, electric motorized models accounted for 68.53% of the ophthalmic examination chairs market share in 2025 and are projected to expand at a 6.85% CAGR through 2031.

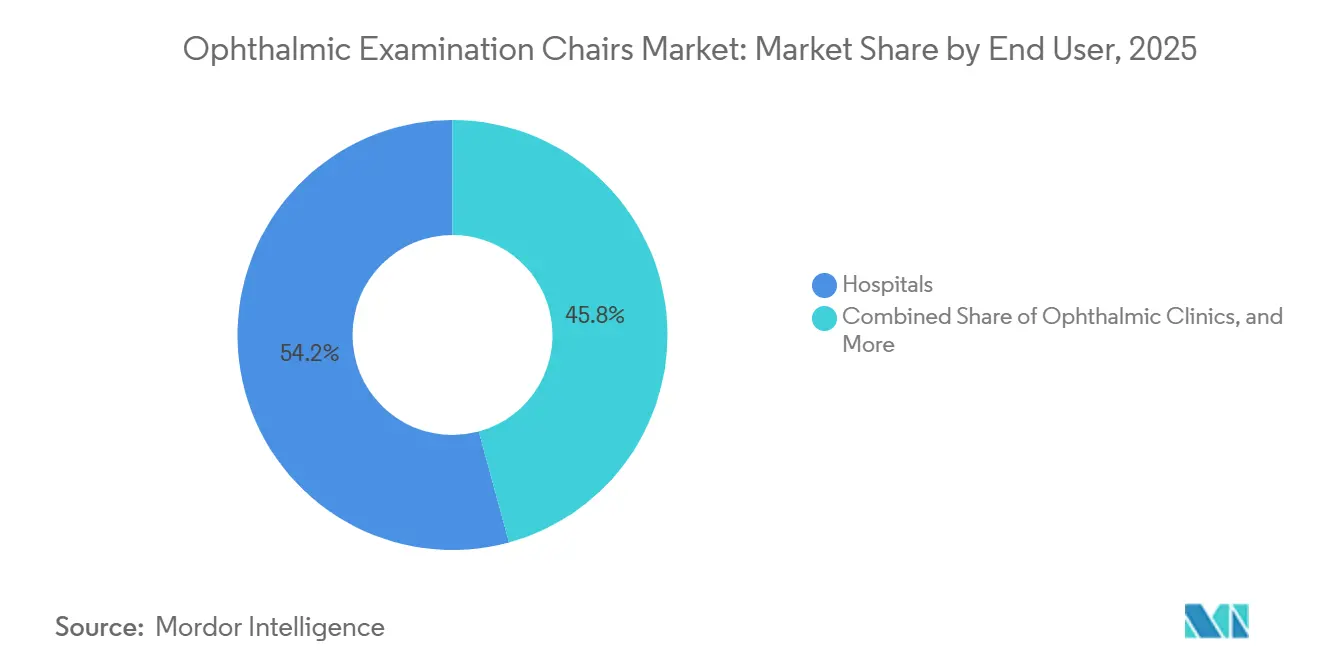

- By end user, hospitals accounted for 54.23% of demand in 2025, while ambulatory surgical centers are forecast to record the highest CAGR of 7.55% between 2026 and 2031.

- By geography, North America retained 38.25% of global revenues in 2025; Asia-Pacific is the fastest-growing region at a 6.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ophthalmic Examination Chairs Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Eye Diseases and Aging Population | +1.8% | Global, acute in South and East Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Technological Advancement in Electric or Motorized Chairs | +1.3% | North America and core EU, spill-over to APAC metros | Medium term (2-4 years) |

| Healthcare Infrastructure Investment in Emerging Economies | +1.1% | China and India core, spill-over to Middle East, Africa, Latin America | Medium term (2-4 years) |

| Tele-Ophthalmology-Ready Chairs Enabling Remote Diagnostics | +0.9% | North America, Western Europe, pilot adoption in APAC | Short term (≤ 2 years) |

| Demand for Antimicrobial And Sustainable Upholstery Materials | +0.5% | Global, strong regulatory push in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Eye Diseases and Aging Population

Global vision-impairment rates continue to escalate as diabetes and longer life expectancies drive higher incidences of cataract, glaucoma, and age-related macular degeneration. Health ministries in China and India have enlarged diabetic-retinopathy screening programs, each new clinic requiring two to four examination chairs to manage patient load. Adults aged 65 and older represent the fastest-growing cohort and consume a disproportionate amount of ophthalmic services, a demographic surge that keeps the ophthalmic examination chairs market on a steady expansion path[1]Weber D.J., “Role of Copper-Impregnated Surfaces in Reducing Healthcare-Associated Infections,” American Journal of Infection Control. Targeted screening initiatives aimed at female patients in Bangladesh and Nigeria highlight persistent gender-based treatment gaps, adding incremental demand for portable, low-maintenance chairs in community settings. The structural nature of these epidemiologic trends underpins long-run visibility for manufacturers that can deliver accessible, ergonomic equipment.

Technological Advancement in Electric or Motorized Chairs

Motorized chairs enable precision height, tilt, and recline functions, accelerating diagnostic workflows and minimizing clinician strain. Carl Zeiss Meditec’s VISUREF 1000, introduced in May 2025, syncs chair positioning with automated refraction protocols, cutting per-patient setup time and reinforcing the central role of electric models in modern practice[2]Carl Zeiss Meditec, “Zeiss Invests in Ocumeda,” ZEISS. Hybrid designs pairing electric height adjustment with manual tilt controls have emerged as a cost-conscious bridge for mid-tier clinics that want core automation without the full electronics spend. Infection-control priorities also favor electric mechanisms, which reduce hand and foot contact versus hydraulic pumps, an advantage amplified by stricter post-pandemic hygiene audits. Unequal purchasing power means penetration remains deepest in North America and Western Europe, but falling component costs are broadening accessibility across urban China, Brazil, and the Gulf states.

Healthcare Infrastructure Investment in Emerging Economies

China’s Healthy China 2030 and India’s National Programme for Control of Blindness and Visual Impairment are channeling public capital into district-level eye hospitals, each outfitted with mid-tier electric chairs priced between USD 3,000 and USD 7,000. Saudi Arabia’s Vision 2030 has spurred private specialty hospital development, while Brazil, Mexico, and Colombia are seeing insurer-driven network expansions that prioritize outpatient ophthalmology units. Tender pipelines in public systems can stretch beyond 18 months, slowing near-term revenue recognition for vendors, yet the volume of announced projects creates a multi-year upswing for the ophthalmic examination chairs market. Local assembly partnerships in Vietnam and Egypt are trimming import duties and positioning regional manufacturers to meet rising demand with shorter lead times.

Tele-Ophthalmology-Ready Chairs Enabling Remote Diagnostics

Tele-ophthalmology matured from pandemic necessity to mainstream service model, especially for diabetic retinopathy screening and post-operative monitoring. Examination chairs now incorporate accessory rails and wiring conduits for handheld fundus cameras and portable slit lamps, enabling technician-acquired images for remote physician review. Carl Zeiss Meditec’s October 2025 investment of EUR 10 million in Ocumeda underscores the strategic convergence of seating hardware with cloud software that routes retinal scans from rural clinics to specialists. Paradoxically, remote monitoring increases in-clinic chair usage because freed time slots are reallocated to complex cases that require in-person evaluation. Regulatory guidance from the FDA in 2024 on software-as-a-medical-device has further standardized connectivity requirements, indirectly influencing chair architecture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Powered Chairs | -1.2% | Global, most acute in cost-sensitive APAC and Africa | Medium term (2-4 years) |

| Stringent Certification and Regulatory Compliance Costs | -0.8% | EU under MDR, North America under FDA, exporting nations | Long term (≥ 4 years) |

| Long Replacement Cycles Reducing Refresh Demand | -0.9% | Global, strongest in North America and Western Europe | Long term (≥ 4 years) |

| Supply-Chain Bottlenecks for Hydraulic Components | -0.6% | Global, pronounced where sourcing depends on EU or China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Powered Chairs

Fully electric chairs cost 40% to 70% more than hydraulic equivalents, with flagship models exceeding USD 10,000 per unit. Independent practices in India, Indonesia, and Sub-Saharan Africa often operate on annual capital budgets below USD 50,000, forcing compromises on automation. Annual maintenance contracts for motor assemblies average 8% to 12% of the purchase price, whereas hydraulic chairs require only occasional seal replacements handled in-house. Leasing penetration remains below 15% across emerging economies, compared with more than 40% in North America, limiting financing avenues. The result is a persistent affordability gap that slows migration to motorized platforms, despite documented ergonomic and infection-control advantages.

Stringent Certification and Regulatory Compliance Costs

While ophthalmic chairs fall under FDA Class I and do not require a 510(k) filing, electric models must pass IEC 60601-1 electrical safety testing, adding roughly USD 25,000 in additional certification fees. The EU’s Medical Device Regulation has lengthened CE-marking cycles to 12-18 months and raised notified-body costs above USD 100,000 per product line, a hurdle that deters smaller innovators. These financial and timeline burdens discourage incremental feature releases, slowing the uptake of antimicrobial fabrics and tele-health accessories, and indirectly concentrating the ophthalmic examination chairs market among companies with robust regulatory teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Drives Throughput Gains

Automatic models controlled 59.55% of 2025 revenues and continue to compound at 6.25% through 2031, underscoring their pivotal role in high-volume clinics striving to trim patient setup times. This dominance translates into the largest share of the ophthalmic examination chairs market. Electric height and tilt cut repetitive manual actions, improving accessibility for elderly patients and supporting ADA compliance. Manual chairs, though growing more slowly, remain vital in resource-restricted regions where mechanical simplicity and low acquisition cost override automation benefits. Hybrid variants that pair motorized vertical movement with manual tilt are carving out a niche in the mid-market in Latin America and Eastern Europe.

Clinical workflow integration is minimal for manual options, yet these units serve mobile eye camps and humanitarian missions where portability matters more than speed. Competitive intensity at the premium end centers on precision positioning, upholstery durability, and electronic memory presets, while the manual category has devolved into a price battle with limited differentiation beyond warranty length. Regulatory treatment stays neutral for both types, although automatic units must satisfy additional electrical safety tests that add to overall price.

By Mechanism: Electric Motorization Redefines Clinical Standards

Electric motorized chairs accounted for 68.53% of global revenues in 2025 and are climbing at a 6.85% CAGR, cementing their status as the preferred mechanism in modern surgical and diagnostic settings. Their share, when paired with associated instruments, further expands the market size for ophthalmic examination chairs captured by vertically integrated vendors. Precision positioning is indispensable for optical coherence tomography and fluorescein angiography, fueling adoption in North America, Japan, and top-tier Chinese hospitals. Hydraulic chairs offer a cost-effective alternative in areas with unreliable electricity, serving rural Africa and South Asia. Pneumatic models occupy a narrow niche in pediatric and low-volume private practices that emphasize simplicity.

Emerging electro-mechanical hybrids shave 20% to 30% off electric list prices while retaining automated height adjustment, attracting budget-sensitive buyers that still want ergonomic gains. Infection-control benefits and the ability to preload procedural positions keep electric models on a clear technology trajectory. Supply-chain resilience also favors electronics; motor and control components enjoy diversified sourcing, whereas hydraulic parts rely on a tighter network of European and Chinese suppliers vulnerable to geopolitical disruptions.

By End User: ASCs Capture Procedural Migration

Hospitals accounted for 54.23% of chair demand in 2025, leveraging larger capital budgets to acquire bundled equipment suites from a single vendor. However, ambulatory surgical centers are expanding fastest, posting a 7.55% CAGR to 2031 as cataract surgeries, laser capsulotomies, and intravitreal injections continue to migrate from hospital outpatient departments. The ophthalmic examination chairs market share within ASCs rises accordingly, driven by compact, multi-purpose designs that seamlessly shift between diagnostic and minor surgical tasks. Infection-control features, antimicrobial upholstery, and rapid reconfiguration capacity are vital for ASC accreditation audits.

Independent ophthalmic clinics and retail chains form a stable mid-tier, gravitating toward electric units priced between USD 4,000 and USD 8,000. Mobile screening units, academic labs, and military facilities comprise a modest yet strategically important segment that often serves as a pilot for advanced telehealth integrations. Regulatory requirements remain broadly similar across end users, but ASC accreditation bodies impose stricter safety and cleanliness standards, indirectly dictating equipment specifications and favoring suppliers with robust compliance documentation.

Geography Analysis

North America retained 38.25% of the ophthalmic examination chairs market in 2025, buoyed by high per-capita health spending, entrenched ASC activity, and mature tele-ophthalmology networks. Over 6,000 Medicare-certified ASCs performed more than 3.5 million eye procedures in that year, sustaining steady replacement demand[3]Centers for Medicare & Medicaid Services, “CY 2024 Payment Policies. Canada’s purchasing cycles hinge on provincial budgets, with rural outreach programs deploying portable chairs to close care gaps. Mexico, propelled by private hospital chains serving domestic and inbound medical tourists, is emerging as a growth pocket that values mid-tier electric models imported from the United States and Japan.

Asia-Pacific is the fastest-growing region, with 6.21% growth through 2031, driven by hospital construction in China and India, rising diabetes incidence, and widening insurance coverage. County-level hospital upgrades in China and district vision centers in India both specify mid-range electric chairs that balance cost and automation, lifting the overall ophthalmic examination chairs market. Japan and South Korea contribute stable replacement demand, while Australia’s regional-city buildouts bolster incremental sales. Cost sensitivity in Vietnam, Indonesia, and rural India still points many buyers toward hydraulic formats, yet declining component prices are tilting future orders toward electric options.

Europe’s market is mature and largely replacement-oriented. The EU MDR has stretched certification timelines to 18 months, slowing new-model rollouts and nudging smaller vendors out of contention. Germany, France, and the United Kingdom anchor demand, but Eastern European nations are capturing EU structural funds to modernize eye-care infrastructure, often opting for hybrid or mid-tier electric chairs. Sustainability mandates in Scandinavia and Germany require bio-based upholstery and energy-efficient motors, adding premiums that some public buyers absorb to meet environmental goals.

The Middle East and Africa divide into high-income GCC states and resource-constrained Sub-Saharan regions. Saudi Arabia and the United Arab Emirates channel Vision 2030 capital into specialty eye hospitals outfitted with premium electric chairs from European and Japanese brands. South Africa shows balanced public and private ordering patterns. Most of Sub-Saharan Africa relies on donor funding, which prioritizes durable manual or hydraulic models suitable for outreach programs.

South America’s growth clusters in Brazil, Argentina, and Colombia. Brazil’s public SUS system favors locally assembled chairs to satisfy domestic content rules, spurring joint ventures between global brands and Brazilian distributors. Import tariffs of up to 20% across the region incentivize regional manufacturing hubs that can shorten lead times and manage currency volatility. Private ophthalmology chains in Chile and Peru lean toward mid-tier electric chairs that blend automation and price sensitivity.

Competitive Landscape

Competition is moderate and intensifying as specialized ophthalmic equipment firms and diversified medical furniture suppliers converge on the same buyers. Haag-Streit, Topcon, Carl Zeiss Meditec, VELA Medical, and Medi-Plinth collectively account for the bulk of global revenues but leave ample room for regional entrants. EssilorLuxottica’s 80% acquisition of Heidelberg Engineering in July 2024 exemplifies a vertical integration strategy that bundles chairs with imaging systems into unified procurement packages. Carl Zeiss Meditec’s 2025 stake in Ocumeda highlights the convergence of software and hardware, positioning the firm to deliver chairs as data-capture nodes within tele-ophthalmology ecosystems.

Chinese contenders like BTC Medical Equipment and Takagi Seiko are gaining traction in Asia-Pacific by pricing mid-tier electric chairs 30% to 40% below Western equivalents. They face hurdles in North America and Europe where buyers value proven service networks and extended warranties. Regulatory costs also favor incumbents with in-house compliance teams that can absorb IEC 60601-1 and EU MDR overheads. The ophthalmic examination chairs industry rewards long product life cycles; replacement intervals of 10 to 15 years mean share gains accumulate gradually, reinforcing the advantage of firms that secure multiyear service contracts.

White-space innovation centers on antimicrobial upholstery, modular designs that toggle between diagnostic and surgical configurations, and motorized presets that cut setup time. Suppliers able to combine these features with remote-diagnostic compatibility are positioned to capture upcoming tenders from health systems modernizing post-pandemic workflows. Supply-chain resilience, especially the diversification of motor and electronics sourcing, is becoming a silent differentiator as geopolitical risks disrupt legacy hydraulic-component channels anchored in Europe and China.

Ophthalmic Examination Chairs Industry Leaders

Carl Zeiss Meditec

Haag-Streit Group (Reliance Medical)

Medi-Plinth Equipment Ltd.

Topcon Corporation

VELA Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: EssilorLuxottica announced the acquisition of Signifeye, a Belgian network of 15 eye centers.

- August 2025: L V Prasad Eye Institute broke ground on the Kasaraneni Paripurna Lakshmi Eye Center in Andhra Pradesh, India.

Global Ophthalmic Examination Chairs Market Report Scope

As per the report's scope, ophthalmic examination chairs are specialized clinical chairs designed for eye care settings. They provide adjustable seating and positioning to support patients during ophthalmic exams and procedures. Typically, they feature reclining backrests, height adjustment, and rotation to facilitate comfortable patient access for ophthalmologists. These chairs enhance efficiency, ergonomics, and patient stability in diagnostic and surgical eye care environments.

The ophthalmic examination chairs market segmentation includes product type, mechanism, end user, and geography. By product type, the market is segmented into automatic examination chairs and manual examination chairs. By mechanism, the market is segmented into electric-motorized, hydraulic, pneumatic, and electromechanical-hybrid. By end user, the market is segmented into hospitals, ophthalmic clinics, ambulatory surgical centers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report covers estimated market sizes and trends for 17 countries across major regions worldwide. The Market Forecasts are Provided in Terms of Value (USD).

| Automatic Examination Chairs |

| Manual Examination Chairs |

| Electric Motorized |

| Hydraulic |

| Pneumatic |

| Electro-Mechanical Hybrid |

| Hospitals |

| Ophthalmic Clinics |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Automatic Examination Chairs | |

| Manual Examination Chairs | ||

| By Mechanism | Electric Motorized | |

| Hydraulic | ||

| Pneumatic | ||

| Electro-Mechanical Hybrid | ||

| By End User | Hospitals | |

| Ophthalmic Clinics | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global ophthalmic examination chairs market today?

The ophthalmic examination chairs market size was USD 107.33 million in 2026 and is forecast to reach USD 135.07 million by 2031.

Which product mechanism is gaining the most traction?

Electric motorized chairs lead with 68.53% of 2025 revenues and are advancing at a 6.85% CAGR through 2031.

Why are ambulatory surgical centers important buyers?

ASCs are shifting a growing volume of cataract and laser procedures out of hospitals, driving a 7.55% CAGR for chair purchases that favor compact, multi-functional designs.

Which region offers the fastest growth outlook?

Asia-Pacific is projected to expand at 6.21% between 2026 and 2031 due to hospital construction in China and India and widening insurance coverage.

How does tele-ophthalmology affect chair specifications?

Chairs increasingly include accessory mounts and connectivity features so technicians can capture images for remote specialists, a trend reinforced by investments like Zeiss’s stake in Ocumeda.

What is the main barrier to adopting advanced powered chairs in emerging markets?

A 40% to 70% price premium over hydraulic models, coupled with limited leasing options, slows uptake among clinics with tight capital budgets.

Page last updated on: