Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 4.70 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Household Coffee Machine Market Analysis by Mordor Intelligence

The US Household Coffee Machine Market size is estimated at USD 3.47 billion in 2026, and is expected to reach USD 4.70 billion by 2031, at a CAGR of 6.30% during the forecast period (2026-2031).

Demand resilience is anchored in single-serve convenience, rising at-home espresso culture, and the steady rollout of smart, voice-enabled appliances. Producers are strengthening value propositions through premium stainless-steel designs, refillable pod formats, and app-driven personalization, each broadening margins while calming price sensitivity. Component sourcing pressures and green-coffee price volatility remain headwinds, yet companies are offsetting these inputs with SKU rationalization and higher average selling prices. Environmental regulation of disposable pods looms as a critical pivot point, encouraging firms to speed up plant-based or fully recyclable pod programs.

Key Report Takeaways

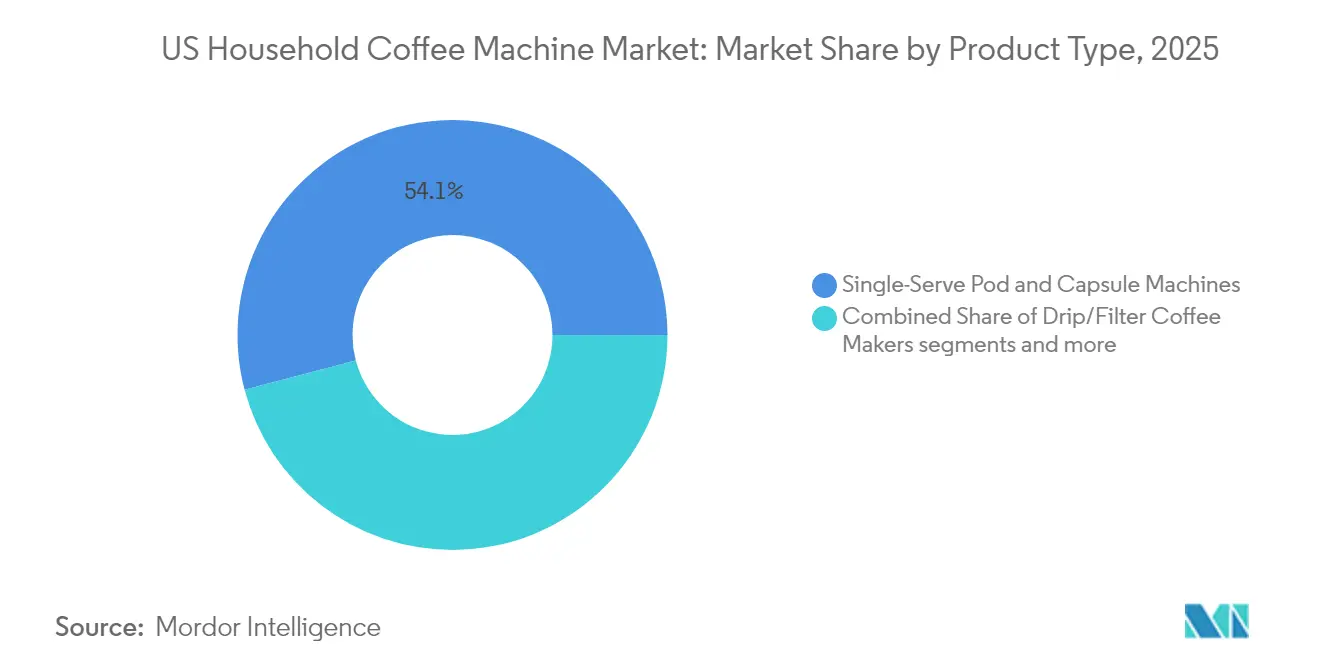

- By product type, single-serve pod and capsule machines led with 54.10% of the US household coffee machine market revenue share in 2025; espresso machines are projected to post the fastest 8.62% CAGR through 2031.

- By technology, semi-automatic units held 35.10% of the US household coffee machine market share in 2025, while smart/connected machines are forecast to expand at a 9.35% CAGR to 2031.

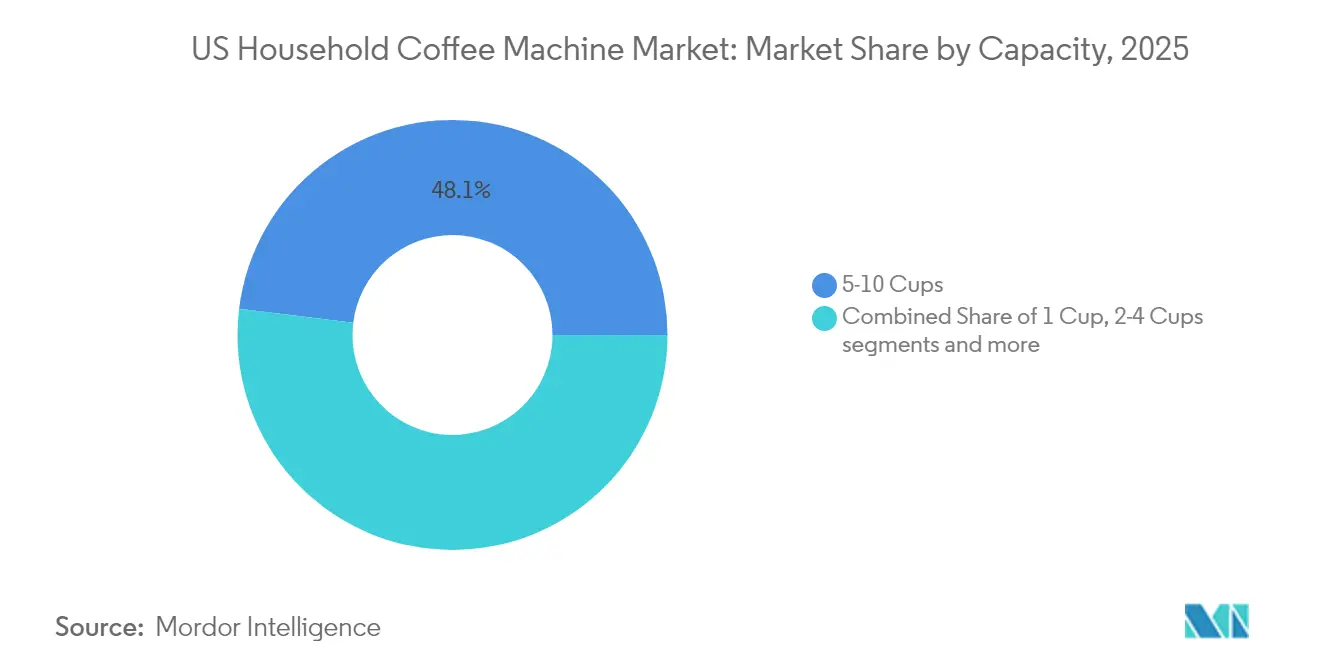

- By capacity, 5–10 cup brewers accounted for 48.05% of the US household coffee machine market size in 2025; single-cup systems are advancing at an 7.68% CAGR through 2031.

- By price range, mid-range models (USD 101-300) captured 39.10% of the US household coffee machine market sales in 2025, yet premium units (USD 301-700) will see a 6.55% CAGR to 2031.

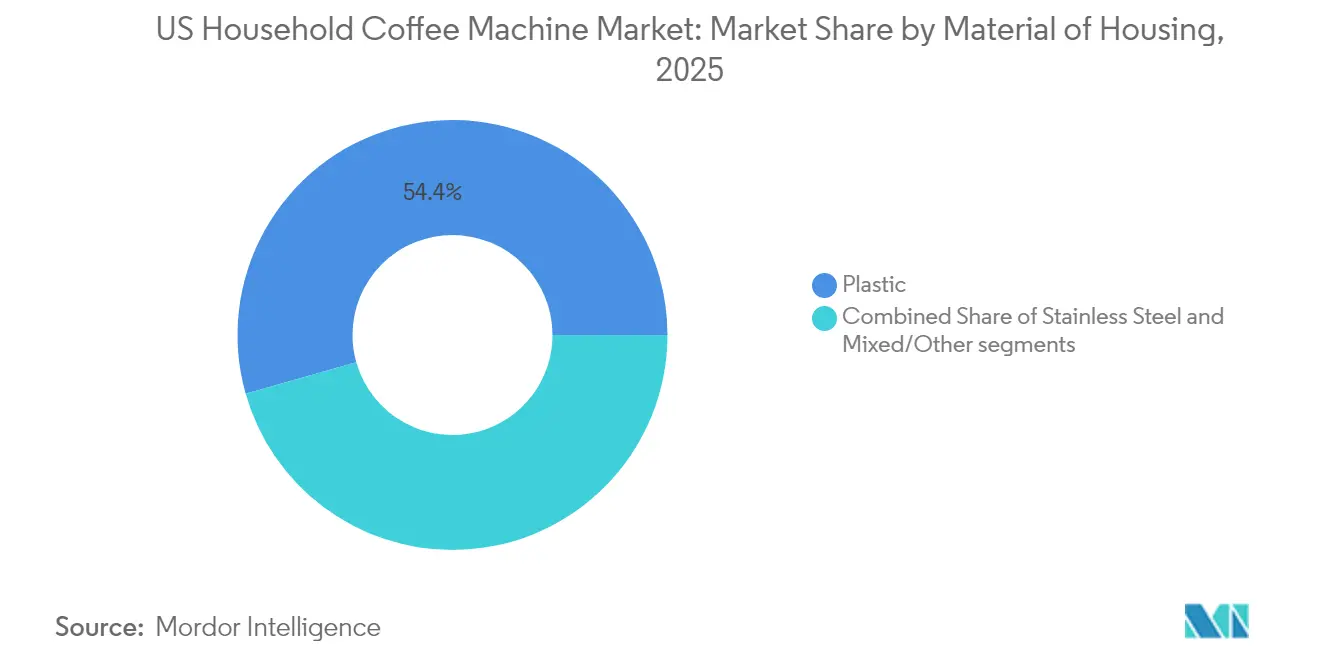

- By Material of Housing (Value), plastic led with 54.40% of the US household coffee machine market revenue share in 2025; stainless steel is advancing at a 5.55% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets retained 38.75% of the US household coffee machine market share in 2025; online channels are set to climb at a 11.98% CAGR to 2031.

- By region, South region retained 35.95% of the US household coffee machine market share in 2025; west region is set to climb at a 7.20%CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Household Coffee Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-serve convenience adoption | +1.8% | Urban concentrations nationwide | Medium term (2-4 years) |

| Specialty espresso at home | +1.5% | Affluent metros | Long term (≥ 4 years) |

| Smart/IoT coffee machine | +1.2% | Tech-forward regions | Medium term (2-4 years) |

| Premium stainless-steel aesthetics | +0.9% | High-income cohorts | Long term (≥ 4 years) |

| Hybrid work-from-home consumption | +0.8% | Knowledge-worker hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Adoption of Single-Serve Pod Machines Due to Convenience in US Households

Keurig has seeded more than 40 million active brewers, putting single-serve capability into nearly one-third of US homes and deepening an ecosystem that delivers annuity-like pod revenue. Rival brands are answering with proprietary capsule lines that attempt to capture similar attachment rates. Convenience spans speed, portion control, and consistent quality, all of which resonate with time-pressed consumers. Hardware upgrades—such as quieter pumps and brew-strength selectors—help sustain replacement demand even as household penetration matures. Notably, Keurig’s Q4 2024 brewer shipments rose 7.3% year over year, hinting at hardware stability despite soft pod volumes [1]Investor Relations Team, “Q4 2024 Earnings Presentation,” Keurig Dr Pepper, investors.keurigdrpepper.com .

Growing Consumer Preference for Specialty Espresso-Based Beverages Fuelling At-Home Espresso Machine Sales

De’Longhi recorded 14% 2024 revenue growth, with coffee systems contributing 62% of turnover, underscoring strong consumer desire for barista-style beverages at home [2]Annual Report 2024, “Sustainability in Practice,” De’Longhi Group, delonghigroup.com . Automatic tamping, precision grind sensors, and one-touch milk texturing have lowered skill barriers and widened the espresso addressable base. Breville’s Barista Express Impress exemplifies premiumization, marrying Italian group-head components with North American software to command higher price points. Social media tutorials and subscription micro-roasters complete the “café at home” narrative, reinforcing equipment upgrades.

Rising Penetration of Smart/IoT-Enabled Appliances Integrating with Voice Assistants in US Households

Bosch’s Home Connect interface allows remote starts, recipe uploads, and maintenance alerts, turning a routine brew cycle into data-rich engagement. Manufacturers monetize post-purchase relationships through app-based consumable reminders and software unlocks for custom profiles. Voice-assistant triggers fold coffee into broader smart-home routines, raising switching costs for consumers once preferences are stored in the cloud. Early adopters help refine machine-learning calibration, setting higher performance expectations for subsequent releases.

Premiumization Trend with Stainless-Steel and Designer Coffee Makers Encouraged by Higher Disposable Incomes

Hamilton Beach reported that premium SKUs contribute 40% to the total US small-appliance revenue, with its premium sub-brand, Lotus, strategically positioned to capitalize on this growth segment[3]2024 Form 10-K, Hamilton Beach Brands Holding Company, hamiltonbeachbrands.com . Smeg has effectively demonstrated that retro styling and coordinated color schemes can support price points exceeding USD 700. Limited-edition collaborations and customizable finishes have elevated coffee machines into aspirational products, reflecting broader trends in the luxury home market. In the premium segment, stainless steel construction has become a standard requirement, offering durability, superior heat retention, and a professional kitchen aesthetic that justifies higher pricing. Manufacturers are increasingly utilizing celebrity chef endorsements and design accolades to reinforce their premium market positioning.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental scrutiny of single-use pods | -1.4% | Eco-focused states | Medium term (2-4 years) |

| Drip-machine saturation | -0.8% | Mature suburban markets | Long term (≥ 4 years) |

| Supply-chain disruptions in the electronic components market are driving up average selling prices (ASPs) and increasing inventory management risks, particularly for smart and connected appliance manufacturers | -0.6% | National | Short term (≤ 2 years) |

| The perceived disparity in roasting quality between home appliances and café-prepared coffee is hindering adoption among premium coffee consumers. | -0.4% | National, with a stronger impact in metropolitan regions characterized by a well-established café culture | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns Over Single-Use Plastic/Aluminium Pods Leading to Regulatory Scrutiny

The USD 1.5 million settlement with the SEC regarding K-Cup recyclability claims highlights the escalating financial risks associated with sustainability-related disclosures. The growing adoption of municipal extended-producer-responsibility regulations is shifting the burden of waste management costs onto manufacturers, creating pressure to innovate and adapt. This regulatory environment is driving significant investment in research and development, particularly in sustainable packaging solutions. For instance, Keurig is set to launch K-Rounds, which are designed to be plant-based or fully compostable, aligning with evolving consumer and regulatory expectations. While these compliance-driven investments are increasing capital expenditures, companies that proactively embrace sustainability initiatives stand to gain a competitive advantage. Early movers can enhance their brand equity, appeal to the expanding base of eco-conscious consumers, and potentially mitigate future regulatory and reputational risks.

Saturation of the Drip Coffee Machine Segment Limiting Incremental Unit Growth

Drip-machine manufacturers are increasingly focusing on replacement cycles as a strategic response to the saturation of unit penetration in the market. Hamilton Beach, which holds a leading share in unit sales, reported a 4.6% revenue growth in 2024. This performance highlights a critical trend: market growth is being driven by premium upgrades and enhanced product features rather than an increase in unit volume. To remain competitive, brands are introducing advanced innovations such as micro-filtered brew baskets, hot-plate temperature optimization algorithms, and mobile-enabled prompts. These technological advancements are designed to accelerate the transition from older models to newer ones, thereby sustaining consumer interest. However, despite these efforts, the profit margins in the drip-machine segment remain narrower compared to the more lucrative pod and espresso machine categories, presenting a challenge for manufacturers aiming to maximize profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Convenience Leadership With Espresso Momentum

Single-serve systems controlled 54.10% of 2025 revenue, cementing their role as the everyday solution for speed-conscious consumers. Espresso machines, though smaller in base, are forecast to rise 8.62% annually as households chase authentic café texture. Innovation such as De’Longhi’s Bean Switch dual-hopper lets users pivot beans without purging, fusing convenience with craft. Combination brewers straddle multiple tastes within one chassis, easing counter-space friction. Drip, percolator, and French press formats persist but rely on niche artisanal enthusiasts, emphasizing manual ritual over automation.

For manufacturers, balancing pod profitability with espresso-driven premium ASPs shapes portfolio planning across the US household coffee machine market. Consumer narratives now celebrate skill progression: entry-level pod units introduce varietal exploration, while aspirational messaging guides users toward semi-automatic espresso platforms. Brands layer loyalty apps and roasting partnerships onto this ladder, ensuring repeat interaction beyond the initial sale. This ecosystem approach underpins hardware design decisions and marketing cadence across peak gifting seasons in the US household coffee machine market.

By Technology: The Pivot From Semi-Automatic Foundations to Connected Ecosystems

Semi-automatic machines retained a 35.10% share in 2025, confirming their appeal to hobbyists who value dosage control without full manual effort. Yet the smart cohort is scaling at 9.35% CAGR as Wi-Fi modules and firmware updates extend appliance lifecycles. Connected dashboards harvest brew-cycle analytics, guiding future feature releases and creating subscription upsell hooks. Fully automatic and super-automatic tiers address luxury seekers wanting zero-friction espresso, with voice-activated frothing now mainstream in showroom demos.

Manual pour-over stations and moka pots anchor the craft segment, but their modest growth underscores mainstream gravitation toward guided consistency. Expect firmware-driven flavour profiles—downloadable holiday blends, for instance—to differentiate next-gen releases, reinforcing software as the new value frontier in the US household coffee machine market.

By Capacity: Mid-Volume Dominance With Single-Cup Upswing

Brewers sized for 5–10 cups commanded 48.05% of 2025 sales, mirroring multi-person households and weekend entertaining. Single-cup appliances are forecast to expand 7.68% annually, propelled by household downsizing and beverage personalization. Variable reservoir designs now let families toggle between batch and pod modes, reducing counter clutter. Larger-than-10-cup offerings find traction in at-home entertaining and small-office micro-kitchens, while 2–4-cup niches speak to solo professionals and student housing.

Higher per-cup margin on pods incentivizes brand push toward single-cup hardware, but maintaining a balanced capacity mix helps hedge against demographic shifts. This segmentation accordingly guides inventory buys for retail partners within the US household coffee machine market.

By Price Range: Mid-Range Mass With Premium Tailwinds

Units priced USD 101-300 captured 39.10% of 2025 turnover, anchoring value-centric demand. Premium tiers between USD 301-700 are projected to grow 6.55% CAGR as households justify higher outlays for brushed-metal finishes, PID temperature control, and smartphone pairing. Budget-conscious consumers find solace in economy models, yet these models grapple with rising costs due to electronics inflation. Meanwhile, luxury segments leverage brand prestige and seamless interior design integration to maintain their allure.

Manufacturers deliberately ladder SKUs—basic pod brewers lead customers into step-up bundles with milk carafes and connected modules, preserving engagement across economic cycles. Such tiered strategies will remain pivotal throughout the US household coffee machine market.

By Material of Housing: Plastic Practicality Versus Stainless-Steel Prestige

Plastic bodies still own 54.40% share due to manufacturing efficiency and lightweight shipping. Stainless-steel shells, however, are pacing at 5.55% CAGR because consumers equate metal with durability and professional calibre. Hybrid builds mix polymer frames with metal facings, achieving cost-engineering balance while conveying premium cues. Glass and ceramic inserts cater to specialty segments demanding thermal neutrality or aesthetic contrast.

Raw-material decisions also intersect with sustainability messaging: recycled ocean-bound plastics and low-carbon steel are emerging badge claims, aligning with broader ESG commitments across the US household coffee machine market.

By Distribution Channel: E-Commerce Surge Reshaping Retail Mix

In 2025, supermarkets and hypermarkets represented a 38.75% market share, driven by the ability to offer in-aisle product comparisons and bundled coffee-bean promotions. Online platforms, expanding at a 11.98% CAGR, leverage extended product assortments and dynamic pricing models, reinforcing their role in enhancing product launch visibility. Hamilton Beach demonstrated this trend, with e-commerce accounting for 44% of its domestic sales, emphasizing the strategic importance of digital channels for driving sales volumes and gathering actionable consumer insights. Specialty retailers and department stores remain essential for providing experiential product demonstrations, while brand-owned websites focus on optimizing profit margins and capturing first-party data.

The transformation of distribution channels highlights the critical role of omnichannel strategies, requiring manufacturers to optimize engagement across diverse touchpoints while addressing channel conflicts and ensuring pricing consistency. Companies like Hamilton Beach are investing in digital transformation initiatives to enhance their competitive positioning in the rapidly growing e-commerce segment. Warehouse clubs appeal to bulk buyers and cost-conscious consumers but face growth limitations due to membership requirements and a narrower product range compared to online marketplaces. The shift toward online purchasing is particularly evident in the premium segment, where consumers conduct extensive research, relying on detailed product specifications, expert reviews, and peer recommendations available through digital platforms.

Geography Analysis

In 2025, the South region contributed 35.95% to the overall market revenue. Southern states, buoyed by rapid population inflows, exhibit hybrid preferences: single-serve pods for weekday speed and espresso features for culturally influenced palates. E-commerce adoption overcomes limited specialty-store footprints, giving smaller brands a direct route to new users. Hispanic demographic strength raises demand for Cafecito-ready pressure profiles.

In 2025, the West region contributed 7.10% to the total market revenue. The region demonstrates a convergence of environmental consciousness and technological innovation. Manufacturers leveraging app-based energy management systems and biodegradable capsule compatibility are outperforming market averages. High residential real estate prices are driving demand for premium countertop designs, boosting the adoption of stainless steel and designer coffee machines. Additionally, the prevalence of cross-channel shopping—where consumers research online and purchase from boutique stores—has necessitated agility among fulfillment partners in the US household coffee machine market.

In the Northeast, espresso-centric habits and above-average disposable incomes fuel demand for premium connected machines. Retailers such as Williams-Sonoma curate European brands, reinforcing the perception of espresso as an everyday luxury. Environmental sensibilities spur interest in refillable stainless pods and energy-efficient standby modes.

The Midwest remains the bastion of drip volume, where large-capacity carafes satisfy multi-generation households. Price-value equations dominate, positioning mid-range semi-automatic offerings as sweet-spot purchases. Weather-driven indoor routines amplify brewer replacement activity each winter, sustaining baseline turnover.

Competitive Landscape

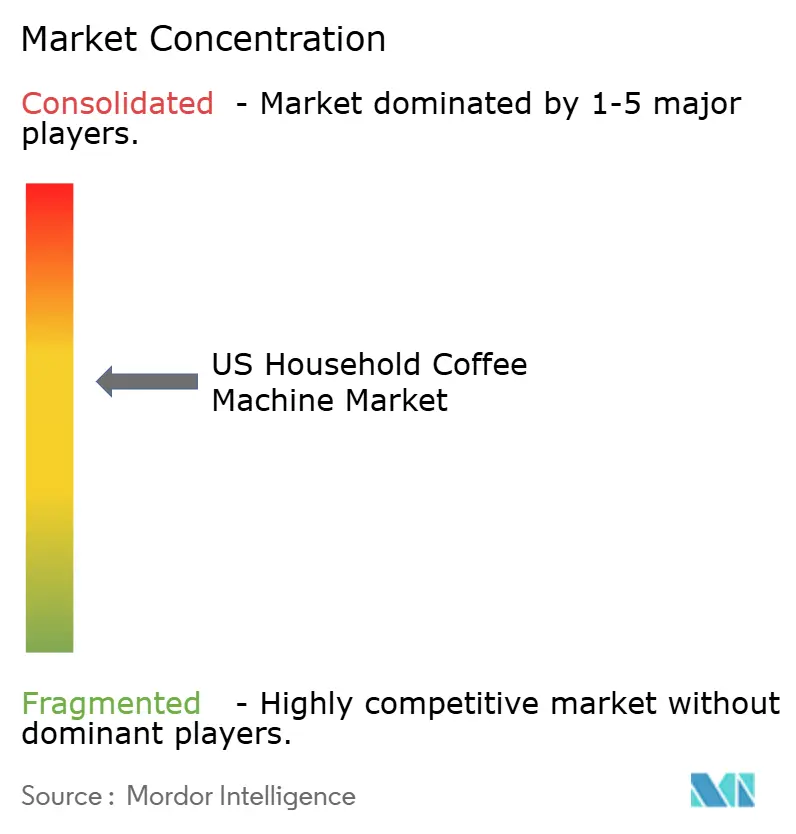

The coffee machine market in the US is moderately concentrated. Keurig and Nespresso are key players in the value share within the pod ecosystem, leveraging their closed-loop consumables to secure consistent repeat revenue and maintain high gross margins. In response, established appliance brands such as Hamilton Beach, De’Longhi, and Breville are introducing advanced drip and espresso machines, strategically targeting both mass-market and specialty distribution channels. The pace of innovation remains robust: Keurig addresses environmental concerns with its K-Rounds, De’Longhi enhances product flexibility with its Bean Switch feature, and Breville incorporates shot-by-shot auto-tamping technology to elevate user experience.

Strategy clusters are distinct. Platform captains (Keurig, Nespresso) expand brewer footprints to lock in pod pull-through. Premium artisans (Breville, De’Longhi) amplify craftsmanship narratives and leverage influencer demonstrations. Mass-value players (Hamilton Beach, Black+Decker) differentiate on price-to-feature ratios. Disruptors like SharkNinja sprint on industrial design and viral-ready marketing; its Ninja Luxe Café helped lift 2024 net sales 32%.

Smart-home integration is a shared battleground. Firms with legacy mechanical engineering are accelerating software partnerships to avoid ceding interface control to third-party hubs. Parallel advances in sustainable materials provide new vectors for competitive messaging across the US household coffee machine market.

US Household Coffee Machine Industry Leaders

Keurig Dr Pepper Inc.

Nestlé S.A. (Nespresso USA)

Hamilton Beach Brands Holding Company

De'Longhi Group

Breville Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hamilton Beach suspended guidance due to tariff risks, with e-commerce at 40% of US sales.

- March 2025: SharkNinja announced plans to launch 25 new products in the coming year, building on the exceptional consumer response to the Ninja Luxe Café product line and the company's 32% revenue growth in 2024 to USD 5.5 billion.

- February 2025: Nestlé highlighted coffee as the top growth driver, launching Nescafé Espresso Concentrate.

- October 2024: De’Longhi Launches Fully Automatic Coffee Machine to Strengthen Retail Presence at Target. The globally recognized small home appliance brand has strategically expanded its distribution network, introducing a premium at-home coffee and espresso maker across more than 1,100 Target stores to capture a broader consumer base in the mass market segment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States household coffee machine market as the value of new drip, single-serve pod, espresso, combination, French press, percolator, and smart/connected brewers sold for domestic use; refurbished units and commercial-grade equipment purchased by cafés, offices, or convenience stores are left outside the frame.

Scope exclusion: Food-service and office coffee systems, countertop grinders sold separately, and used equipment are not counted.

Segmentation Overview

- By Product Type

- Drip/Filter Coffee Makers

- Single-Serve Pod & Capsule Machines

- Espresso Machines

- Combination Coffee & Espresso Machines

- French Press & Manual Brewers

- Percolators & Moka Pots

- By Technology

- Manual

- Semi-Automatic

- Fully Automatic

- Super-Automatic

- Smart/Connected

- By Capacity – Number of Cups

- 1 Cup

- 2–4 Cups

- 5–10 Cups

- Above 10 Cups

- By Price Range

- Economy (≤ USD 100)

- Mid-Range (USD 101–300)

- Premium (USD 301–700)

- Luxury (≥ USD 701)

- By Material of Housing

- Plastic

- Stainless Steel

- Mixed/Other

- By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Appliance Retailers

- Department Stores

- Online (E-commerce)

- Brand E-Stores

- Warehouse Clubs

- By Region – United States

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance product managers, component suppliers, kitchen-retail buyers, and specialty-coffee trainers across the Northeast, Midwest, South, and West. Discussions verified household demand patterns, average selling prices, pod machine penetration, and likely regulatory impacts; survey feedback from recent buyers clarified capacity and feature preferences that secondary data could not surface.

Desk Research

Our team began with public datasets such as the National Coffee Association's annual consumption tracker, U.S. Census Bureau retail appliance sales, Harmonized Tariff Schedule 8516.71 import data, and Federal Reserve disposable-income series, which together outline demand, price, and volume baselines. Trade association briefs (Housewares Executive), patent filings on automatic brew technologies, and appliance safety standards issued by UL were then reviewed to flag regulatory or design shifts that move volumes. Paid sources, namely D&B Hoovers for brand-level revenue splits and Dow Jones Factiva for shipment news, supplied directional checks on manufacturer performance. These examples are illustrative; numerous other public and subscriber sources informed datapoints, cross-checks, and context.

Market-Sizing & Forecasting

We applied a top-down and bottom-up hybrid model. National import plus domestic shipment volumes were reconstructed from customs codes and manufacturer disclosures, multiplied by validated average retail prices, and then verified against sampled brand sell-through reported by big-box retailers. Key drivers, daily coffee drinker share, single-serve capsule adoption, median household income, housing starts, and online small-appliance penetration, feed a multivariate regression blended with ARIMA smoothing to project 2025-2030 demand. Where bottom-up supplier roll-ups under or overshot these results, values were adjusted through iterative triangulation.

Data Validation & Update Cycle

Analyst pairs perform variance scans versus third-party indices, rerun sensitivities, and escalate anomalies for senior review. Reports refresh each year, with interim updates triggered by material events such as tariff shifts or technology breakthroughs, ensuring clients receive the latest reconciled view at delivery.

Why Our US Household Coffee Machine Baseline Earns Confidence

Published U.S. coffee machine figures vary widely because firms mix residential and commercial scopes, assume different price ladders, or lock forecasts for several years.

Key gap drivers include scope creep into office or vending segments, optimistic average selling prices for premium espresso lines, and outdated consumption ratios. Mordor's disciplined household-only lens, yearly refresh cadence, and variable-specific validation narrow these divergences and give decision-makers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.26 B (2025) | Mordor Intelligence | - |

| USD 9.67 B (2023) | Regional Consultancy A | Blends commercial and vending equipment; lacks recent retailer sell-through checks |

| USD 7.55 B (2023) | Industry Journal B | Uses single ASP across segments; relies on three-year-old consumption survey |

In sum, while headline values differ, our household-exclusive scope, transparent variable choices, and regular updates make Mordor's baseline the most traceable and decision-ready foundation for sizing opportunities in the U.S. home coffee brewing arena.

Key Questions Answered in the Report

What is the current value of the US household coffee machine market?

The market is valued at USD 3.47 billion in 2026 and is forecast to reach USD 4.7 billion by 2031 at a 6.30% CAGR.

Which coffee machine type holds the largest share in the United States?

Single-serve pod and capsule machines lead, capturing 54.10% of 2025 revenue.

Why are smart coffee machines growing rapidly?

Smart brewers integrate with home-assistant platforms, enable remote control, and provide usage analytics, driving a 9.35% CAGR in the connected segment.

How significant is environmental regulation on single-serve pods?

Increased regulatory scrutiny, as evidenced by Keurig's SEC settlement, is projected to reduce the forecasted CAGR, prompting manufacturers to shift focus toward plant-based or recyclable alternatives.

Which distribution channel is expanding the fastest?

Online retail is advancing at a 11.98% CAGR as shoppers favor broad selection, reviews, and direct-to-door convenience.

Who are the leading companies in the US household coffee machine market?

Keurig Dr Pepper and Nestlé’s Nespresso together control about 46% value share, followed by Hamilton Beach, De’Longhi, Breville, and emergent challenger SharkNinja.

Page last updated on: