Urban Air Mobility Market Size and Share

Market Overview

| Study Period | 2019 - 2040 |

|---|---|

| Market Size (2025) | USD 5 Billion |

| Market Size (2040) | USD 69.83 Billion |

| Growth Rate (2025 - 2040) | 19.22% CAGR |

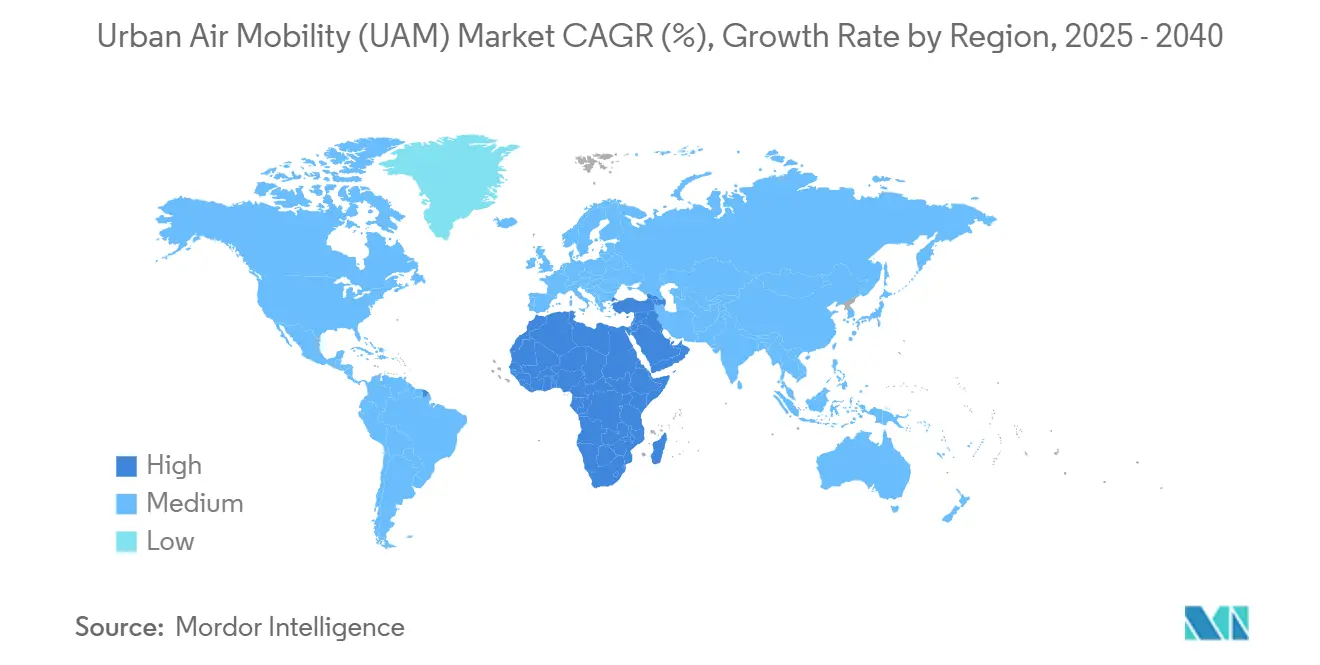

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

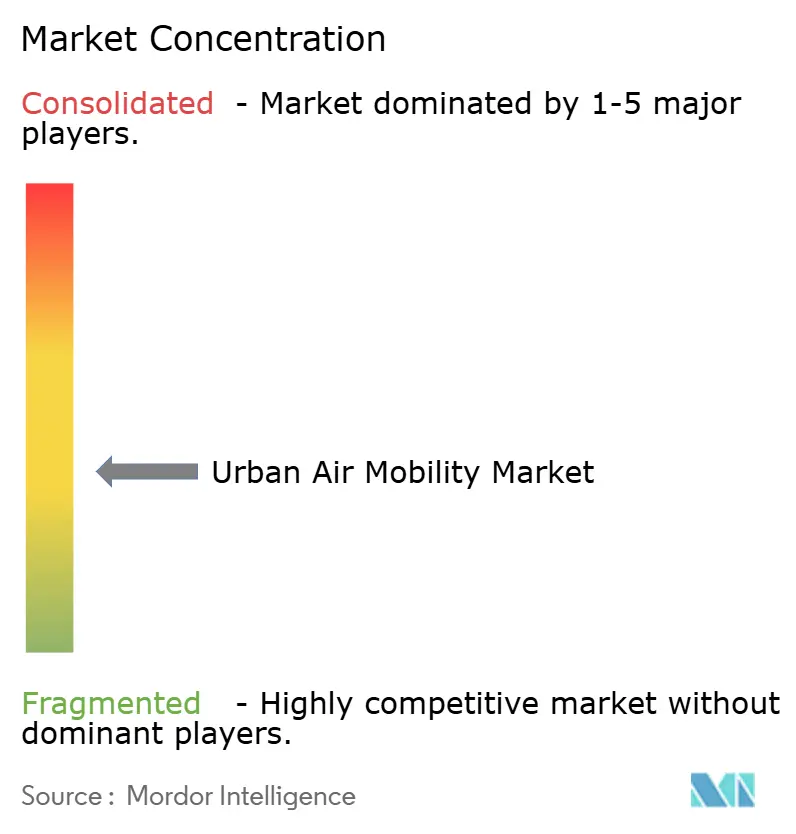

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Urban Air Mobility Market Analysis by Mordor Intelligence

The urban air mobility (UAM) market size is estimated at USD 5.00 billion in 2025, and is expected to reach USD 69.83 billion by 2040, at a CAGR of 19.22% during the forecast period. Battery-energy-density breakthroughs have extended eVTOL range beyond 150 km, opening profitable intercity corridors and strengthening the business case for premium services. Faster certification, helped by the Federal Aviation Administration’s powered-lift rule, lowers regulatory risk and encourages large capital deployments.[1] Federal Aviation Administration, “With New Rule, FAA Is Ready for Air Travel of the Future,” faa.gov Strategic alliances between aerospace pioneers and automotive manufacturers are compressing production costs, while public-private-partnership models are financing vertiport networks at a pace not seen in legacy aviation infrastructure. Together, these forces are positioning the UAM market for rapid global scale-up.

Key Report Takeaways

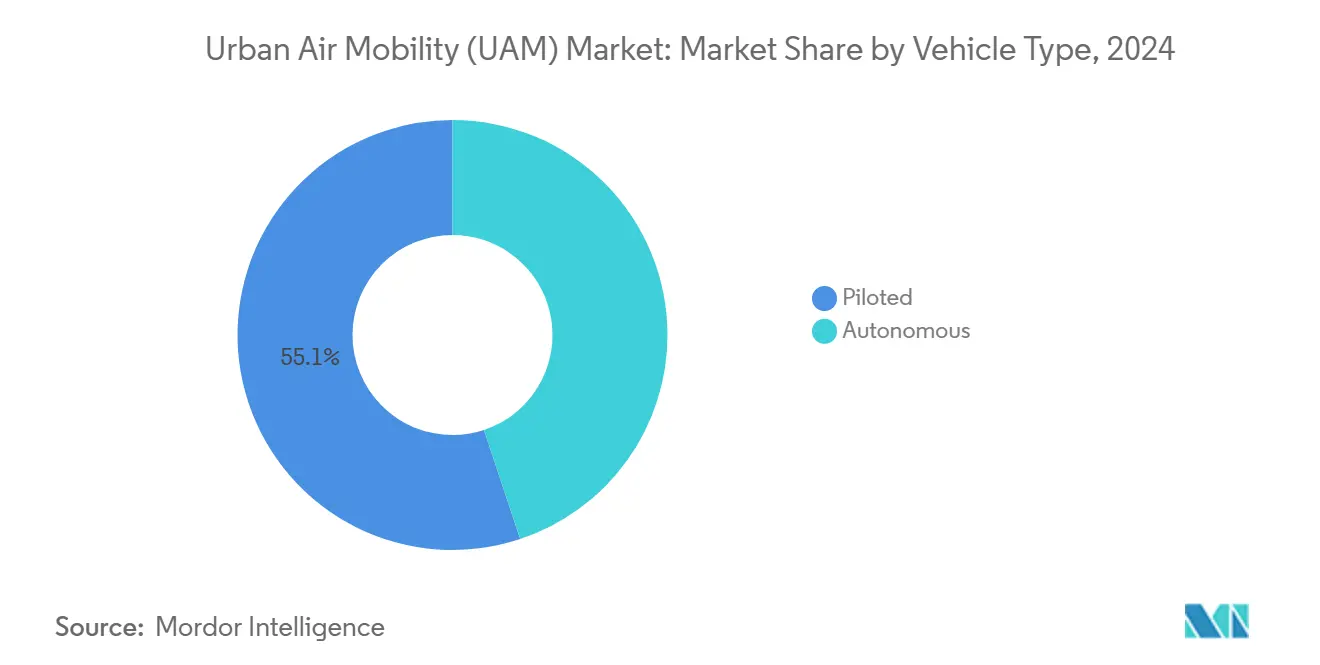

- By vehicle type, piloted eVTOLs led with 55.10% of the UAM market share in 2024; autonomous systems are projected to expand at a 21.51% CAGR through 2040.

- By range, intracity services accounted for 59.81% of the UAM market in 2024, while intercity routes are set to grow at a 22.82% CAGR to 2040.

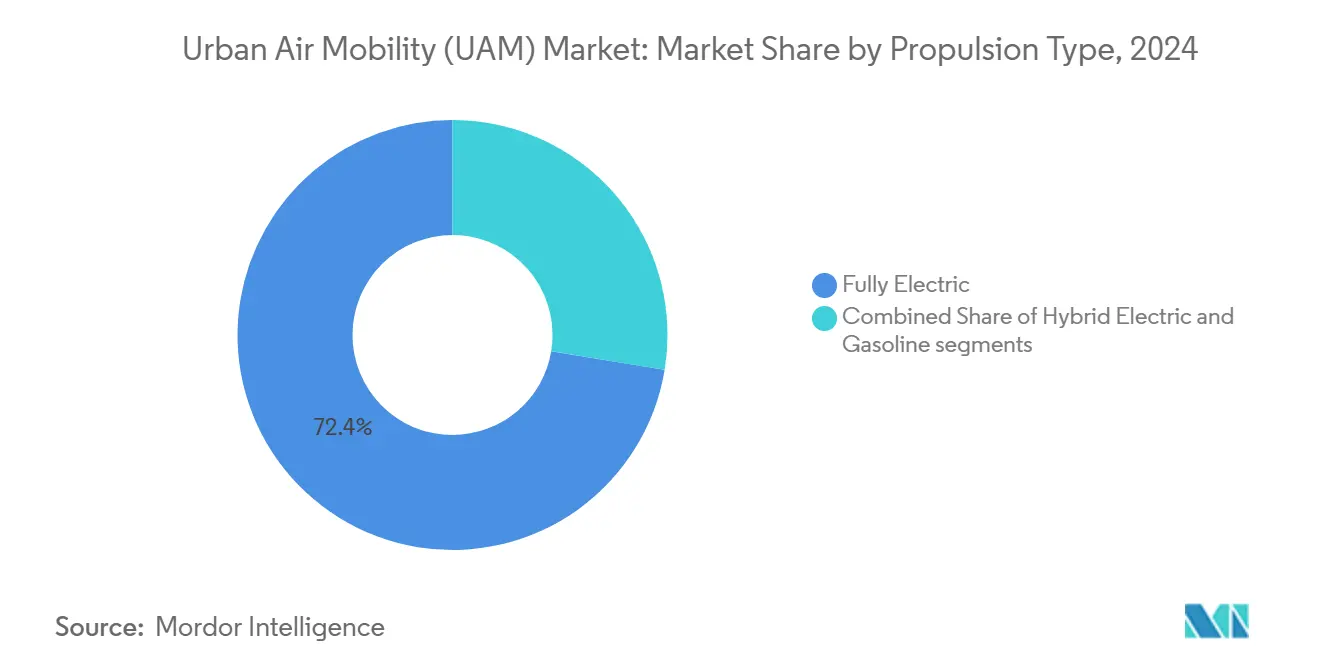

- By propulsion, fully electric aircraft commanded 72.41% revenue share in 2024; hybrid-electric concepts are forecast to post a 24.18% CAGR to 2040.

- By application, passenger air taxis held a 63.25% share of the UAM market size in 2024; cargo logistics is advancing at a 25.26% CAGR into 2040.

- By end user, ride-sharing platforms controlled 46.50% revenue in 2024, whereas e-commerce operators show the fastest growth at 26.77% CAGR.

- By geography, North America captured 46.89% of 2024 revenue; the Middle East and Africa region is projected to surge at a 28.21% CAGR to 2040.

Global Urban Air Mobility Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid battery-energy-density gains push eVTOL range beyond 150 km | +7.1% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Automotive-grade supply chains drive down eVTOL unit costs | +5.4% | Global, with early adoption in Asia-Pacific | Medium term (2-4 years) |

| Vertiport PPP financing models unlock infrastructure rollout | +4.2% | North America, Europe, and Middle East | Long term (≥ 4 years) |

| Regulatory "sandbox" corridors accelerate certification timelines | +3.5% | North America, Europe, and UAE | Short term (≤ 2 years) |

| Premium airport-shuttle demand from mega-hub expansions | +2.9% | Middle East, Asia-Pacific, and North America | Medium term (2-4 years) |

| AI-enabled UTM platforms de-risk high-density airspace operations | +2.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Battery-Energy-Density Gains Push eVTOL Range Beyond 150 km

Solid-state cells now deliver 450–550 Wh/kg, up to 90% higher than earlier lithium-ion chemistries.[2] ECNS, “Solid-State Battery Advancements Set to Propel eVTOLs,” ecns.cn Flight tests have shown 48-minute, single-charge missions, meeting the threshold for profitable intercity shuttles. Longer range lets operators aggregate demand across multiple city pairs and raises daily aircraft utilization, directly lowering cost per seat-mile. These performance gains also satisfy key safety metrics regulators require, smoothing the certification journey. As a result, intercity routes are forecast to capture a progressively larger slice of the UAM market revenue over the coming decade.

Automotive-Grade Supply Chains Drive Down eVTOL Unit Costs

Partnerships between eVTOL builders and automobile OEMs are embedding mass-production know-how into aerospace programs. Toyota’s investment in Joby Aviation and shared component sourcing will cut airframe costs by 35% before 2028. Standardized parts, lean assembly lines, and automotive-quality control processes shorten ramp-up cycles and stabilize pricing. Lower acquisition costs feed through to reduced fares, expanding the accessible customer base and reinforcing demand across the UAM market.

Vertiport PPP Financing Models Unlock Infrastructure Rollout

Municipalities are adopting public-private-partnership structures that distribute risk while tapping private capital for construction. The Greater Orlando Aviation Authority’s two-stage procurement scheme demonstrated how airports can accelerate site development without straining public budgets. Similar models in Miami-Dade and Dubai have bundled real-estate concessions, operations contracts, and service-level agreements into financeable packages. With clear design guidance from Engineering Brief 105A, investors face less uncertainty, and network density is rising—an essential precondition for the next phase of the UAM market.

Regulatory “Sandbox” Corridors Accelerate Certification Timelines

The US Special Federal Aviation Regulations on powered-lift aircraft created test corridors where manufacturers prove compliance in live environments.[3]Federal Register, “Integration of Powered-Lift: Pilot Certification and Operations,” federalregister.gov Joby Aviation completed three of five certification stages by operating inside these corridors, achieving record progress rates. Sandbox data feeds directly into rulemaking, shortening the interval between prototype and commercial launch and boosting investor confidence across the UAM market.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow vertiport permitting in tier-1 cities | -4.80% | North America and Europe | Medium term (2-4 years) |

| Public-acceptance headwinds on noise and visual pollution | -3.80% | Global, with higher impact in Europe | Short term (≤ 2 years) |

| Battery raw-material price volatility | -2.90% | Global | Medium term (2-4 years) |

| Pilot-shortage bottleneck before full autonomy | -2.30% | Global; higher impact in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Slow Vertiport Permitting in Tier-1 Cities

Approval processes in major metros routinely involve more than ten agencies, driving timelines well past two years and inflating holding costs. In Los Angeles, a single downtown site required coordination among zoning, environmental, and emergency-response departments before construction could start. Delays push operators toward suburban nodes, limiting early-stage route density and postponing the full value proposition of the UAM market.

Public-Acceptance Headwinds on Noise and Visual Pollution

European surveys show that 64% of residents expressed concern over rotor noise despite eVTOLs measuring below comparable helicopter decibel levels. Visual-line-of-sight privacy worries further dampen support in densely populated districts. In response, the European Union Aviation Safety Agency issued environmental technical specifications, while manufacturers are refining blade designs and flight profiles to mitigate tonal peaks. Acceptance campaigns have begun shifting sentiment once communities witness quieter demonstration flights, yet perception remains a near-term drag on the UAM market.

Segment Analysis

By Vehicle Type: Autonomy Drives Future Growth

Piloted aircraft controlled 55.10% of 2024 revenue, reflecting regulators’ preference for familiar cockpit concepts during the industry’s opening phase. Joby Aviation’s S4 advanced through three FAA certification stages in 2025, underscoring the near-term dominance of crewed platforms. This segment captured the largest slice of the UAM market, giving financiers confidence while larger infrastructure networks take shape. Operators also leverage existing pilot-training pipelines to scale services in premium airport-shuttle corridors, where customer willingness to pay offsets higher crew costs.

Autonomous craft, now a smaller category, is forecast to grow at a 21.51% CAGR to 2040, the fastest of any vehicle type. Wisk Aero’s collaboration with NASA accelerates detect-and-avoid validation, a prerequisite for uncrewed commercial service. Removing pilots could cut direct operating expenses by about 26%, translating into wider geographic coverage and lower fares. As AI-enabled UTM platforms mature, autonomy is expected to alter operating models across the UAM market, shifting the competitive focus to software reliability and fleet orchestration.

Note: Segment shares of all individual segments available upon report purchase

By Range: Intercity Connections Accelerate Adoption

Intracity segments under 100 km held 59.81% of the UAM market size in 2024, driven by congestion-relief routes linking city centers to airports. Skyports Infrastructure opened several downtown vertiports that year, anchoring early consumer awareness. Operators favor these short hops because battery reserves remain generous even with energy-intensive vertical phases, enabling predictable schedules and rapid asset turns.

Intercity missions above 100 km show the highest momentum, projected to rise at a 22.82% CAGR. Solid-state batteries and hybrid-electric propulsion now meet range and payload needs for linking close megacities and bypassing road bottlenecks. Regional governments in the Middle East see these corridors as enablers of tourism and decentralized economic zones, supporting accelerated deployment. Intercity adoption widens the addressable customer pool and magnifies network effects, reinforcing long-term expansion of the UAM market.

By Propulsion Type: Electric Solutions Lead Sustainability Push

Fully electric architectures secured 72.00% revenue in 2024, underscoring the sector’s zero-emission ambition. Simpler drivetrains, fewer moving parts, and lower scheduled maintenance produce favorable direct operating costs even before fuel savings are included. Joby Aviation and Archer Aviation committed exclusively to electric configurations and reached key certification milestones by early 2025, aerospacetestinginternational.com. These economics underpin the largest block of the UAM market demand.

Hybrid-electric systems will expand at a 24.18% CAGR, bridging until battery metrics align with ultra-long routes. Vertical Aerospace’s partnership with Honeywell on advanced generators illustrates how hybrids aim to stretch range while retaining many electric advantages. As energy storage advances, hybrids may cede share, but over the next decade, they ease route planning constraints and diversify revenue, stabilizing growth for the broader UAM market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Cargo Logistics Emerges as Growth Leader

Passenger air taxis dominated revenue at 63.25% in 2024, benefiting from first-mover visibility and premium fare structures. Partnership models such as Joby–Delta bundle ground and air legs into single itineraries, elevating customer experience jobyaviation.com. These alliances helped anchor early trust and produced the lion’s share of UAM market activity.

Cargo logistics is advancing at a 25.26% CAGR, the strongest trajectory among use cases. AutoFlight secured a production certificate for its CarryAll platform in January 2025. Removing passenger lifts' design constraints simplifies interiors and expedites approvals for uncrewed flights. Rising same-day delivery expectations among e-commerce giants align neatly with eVTOL payload and range envelopes, amplifying future demand inside the UAM market.

By End User: E-commerce Firms Drive Innovative Applications

Ride-sharing aggregators held 46.50% of 2024 revenue, extending their app ecosystems into the sky. NASA research shows that integrating ridesharing can multiply preferred trips by two orders of magnitude once price and convenience converge ntrs.nasa.gov. Ground-air multimodal booking smooths customer adoption and cements platform loyalty.

E-commerce operators are the fastest-moving cohort, with a 26.77% CAGR to 2040. In May 2025, AIR completed night cargo flight tests with a 550-pound payload, validating around-the-clock supply-chain missions. Automated loading systems and warehouse-vertiport co-location further streamline logistics. As drone delivery regulations mature, heavy-lift eVTOLs promise to slash transit times on urban spokes, injecting new momentum into the UAM market.

Geography Analysis

North America remained the largest region, accounting for 46.89% of 2024 revenue, supported by the FAA’s clear certification pathway and deep venture funding pools. Fixed-base-operator chains Atlantic and Signature began constructing vertiport clusters at major airports during early 2025, adding operational depth across high-yield corridors. The United States Air Force’s Agility Prime program further accelerates technology readiness, turning military test data into civilian certification evidence. These developments anchor the North American UAM market and provide a template for other regions.

The Middle East and Africa region shows the steepest growth curve, projected at a 28.21% CAGR from 2025 to 2040. Abu Dhabi finalized an agreement with Archer Aviation to launch the first commercial air-taxi services, positioning the UAE as a global showcase. Sovereign funds channel significant capital into vertiport infrastructure, and diverse geography creates compelling intercity use cases over desert and mountain terrain. Early mover advantage and cohesive regulatory backing promise to propel regional leadership within the UAM market.

Europe retains a strong position through progressive regulation and sustainability mandates. EASA adopted a comprehensive UAM framework in 2024, giving operators clear operational rules. Public-acceptance surveys published in 2025 indicate 83% positive sentiment when residents are informed about eVTOL noise and safety standards, easa.europa.eu. Cities like Paris and London aim to debut services before major international events, leveraging green mobility goals to attract infrastructure funding. This coordinated approach keeps Europe firmly embedded in the advancing UAM market.

Competitive Landscape

Competition is intense yet moderately concentrated, with aerospace start-ups, automotive entrants, and historic OEMs all racing toward type certification. Vertical integration is gaining ground: Archer Aviation obtained FAA approval for its pilot-training academy in February 2025, enabling the company to manage workforce pipelines internally. Strategic alliances remain central, evidenced by Joby’s partnership with Uber and Delta in passenger transport and with Jetex for VIP services. These collaborations expand market reach while spreading development risk across complementary players.

The competitive field is gradually consolidating. Capital-intensive certification has already triggered mergers and portfolio divestitures among smaller projects that failed to secure follow-on funding. Analysts at the 2025 TVF forum singled out Archer, Joby, Beta, and Eve as the most likely to achieve near-term certification. Technological differentiation is shifting toward avionics software, battery thermal management, and automated traffic-management integration rather than airframe aesthetics.

White space remains for specialized niches. In 2024, German start-up ERC-System introduced an eVTOL tailored for medical evacuation. The US Army awarded Lift Aircraft a contract to study modular medical payloads, signaling military interest beyond logistics EVTOL.news. Such vertical applications diversify revenue and mitigate head-to-head rivalry in passenger markets, enlarging the overall urban air mobility market opportunity.

Urban Air Mobility Industry Leaders

-

Guangzhou EHang Intelligent Technology Co., Ltd.

-

Airbus SE

-

Archer Aviation Inc.

-

Volocopter GmbH (Diamond Aircraft Industries GmbH)

-

Joby Aviation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Archer Aviation completed its first piloted conventional take-off and landing with the Midnight aircraft, showcasing dual VTOL/CTOL versatility.

- June 2025: SITA and Urban-Air Port partnered to build a software-defined vertiport management system that integrates passenger, aircraft, and power flows.

- June 2025: Eve Air Mobility secured up to USD 15.8 million from Brazil’s FINEP to progress autonomous flight, hybrid-electric propulsion, and advanced ATM technologies

- May 2025: Wisk Aero and NASA deepened their research partnership to advance autonomous flight technologies for urban air mobility applications, focusing on traffic-management integration

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

The study treats the urban air mobility market as all commercially built electric or hybrid-electric vertical take-off and landing aircraft (eVTOLs) designed for passenger or light-cargo services within and between metropolitan areas. This includes piloted or autonomous platforms, supporting software, and the revenues earned from scheduled, on-demand, or logistics flights.

Scope exclusion: Conventional rotorcraft powered solely by turbine engines fall outside our definition.

Segmentation Overview

- By Vehicle Type

- Piloted

- Autonomous

- By Range

- Intracity ( Less than 100 km)

- Intercity (Greater than 100 km)

- By Propulsion Type

- Fully Electric

- Hybrid Electric

- Gasoline

- By Application

- Passenger Air Taxi

- Intra-city Shuttle

- Emergency Medical Services

- Cargo and Logistics

- By End User

- Ride-Sharing Operators

- Corporate and VIP Clients

- E-commerce and Logistics Firms

- Healthcare Providers

- Military and Government Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- South America

- Brazil

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed air-taxi CTOs, airport planners, battery suppliers, and regulators across North America, Europe, and Asia-Pacific. Dialogs clarified realistic entry-into-service dates, typical fare expectations, fleet utilization targets, and vertiport throughput, thereby closing data gaps that literature alone cannot resolve.

Desk Research

Our analysts first combed public domain sources such as FAA concept-of-operations drafts, EASA Special Condition guidelines, ICAO traffic data, UN urbanization tables, and battery energy-density studies from peer-reviewed journals. Company 10-Ks, investor decks, and vertiport planning documents enrich baseline assumptions. Paid databases, D&B Hoovers for corporate revenue splits and Dow Jones Factiva for program milestones, provide additional fact checks. This list is illustrative; numerous other publications help refine and corroborate inputs.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model starts with urban population pockets, average trip lengths, and current modal splits to derive an addressable demand pool. Penetration rates are stress-tested against eVTOL order backlogs, certified aircraft counts, battery Wh/kg road maps, vertiport roll-out schedules, passenger willingness-to-pay surveys, and regulatory milestone tracking. Select supplier roll-ups (sample ASP × volumes) validate totals and adjust anomalies. Multivariate regression plus scenario analysis projects demand to 2040, letting battery cost curves and regulatory pace shift growth bands. When bottom-up evidence is thin, interpolation uses nearest proxy fleets and utilization coefficients vetted during interviews.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance benchmarking, and anomaly flags. Models refresh every twelve months, with mid-cycle updates if certification slippage, funding shocks, or major policy moves materially change forecasts. Before release, a fresh validation run ensures clients receive our latest view.

Why Mordor's Urban Air Mobility Baseline Commands Reliability

Published figures often diverge because firms mix helicopters with eVTOLs, apply single-line CAGR extensions, or freeze currency and battery-price assumptions. Our disciplined scope, annual refresh cadence, and dual-path modeling minimize such drift.

Key gap drivers include differing treatment of vertiport infrastructure income, whether cargo drones are folded into totals, and the conversion rates applied when translating preorder announcements into delivered fleets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.00 B (2025) | Mordor Intelligence | - |

| USD 4.60 B (2024) | Global Consultancy A | Omits intercity segments, relies on single CAGR extension |

| USD 4.99 B (2024) | Industry Association B | Counts only air-taxi revenue, no cargo services |

| USD 4.87 B (2024) | Trade Journal C | Top-down estimate without supplier cross-checks |

In sum, the modest premium in Mordor's baseline reflects fuller segment coverage, primary-validated penetration curves, and an update rhythm attuned to fast-moving certification and funding news, giving decision-makers a transparent and repeatable starting point.

Key Questions Answered in the Report

How fast is the urban air mobility market expected to grow?

The market is projected to expand from USD 5.00 billion in 2025 to USD 69.83 billion by 2040, reflecting a 19.22% CAGR.

Which application will create the largest near-term revenue pool?

Passenger air taxis led with 63.25% revenue in 2024 and remain the anchor segment through 2040, especially on premium airport-shuttle routes.

When could fully autonomous eVTOL services arrive at scale?

Autonomous systems are forecast to grow at a 21.51% CAGR and gain meaningful market share after 2030, once detect-and-avoid and UTM standards mature.

What cost advantages come from automotive-style manufacturing?

Partnerships with car OEMs are expected to lower eVTOL unit costs by 35.00% before 2028, translating into about 40.00% cheaper cost per passenger-mile than conventional helicopters.

Which regions will see the fastest growth?

The Middle East and Africa are on track for a 28.21% CAGR to 2040, driven by UAE and Saudi initiatives that pair generous funding with supportive regulation

What are the biggest operational bottlenecks to watch?

Lengthy vertiport permitting cycles and pilot shortages together shave almost 7.10% off potential CAGR until infrastructure streamlines and autonomy reduces crew demand.

Page last updated on: