Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

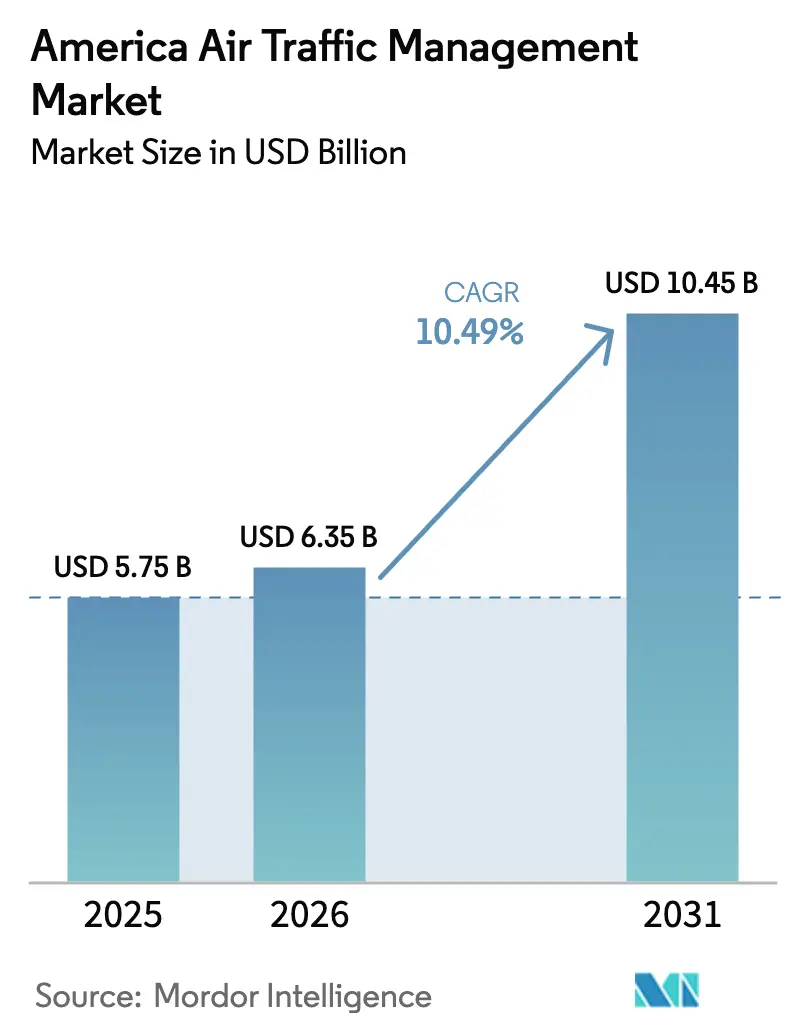

| Base Year Market Size (2025) | USD 5.75 Billion |

| Market Size (2026) | USD 6.35 Billion |

| Market Size (2031) | USD 10.45 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

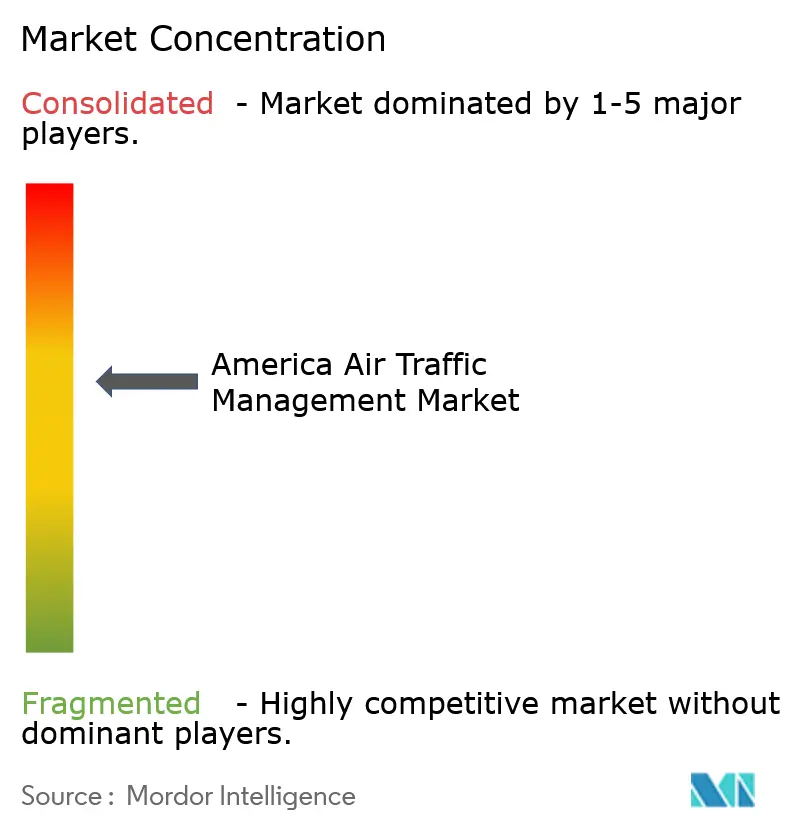

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

America Air Traffic Management Market Analysis by Mordor Intelligence

The American air traffic management market size is expected to grow from USD 5.75 billion in 2025 to USD 6.35 billion in 2026 and is forecast to reach USD 9.47 billion by 2031 at a 10.48% CAGR over 2026-2031. Robust regulatory funding for the Federal Aviation Administration (FAA) NextGen program, sustained controller-workforce shortages, and rising adoption of satellite-based surveillance underpin this expansion. Digital and remote-tower deployments are transforming cost structures for secondary airports, while integration of unmanned traffic management (UTM) frameworks is blurring the boundary between conventional and emerging operations. Vendors that can deliver cyber-hardened, cloud-native solutions are capturing market share as operators modernize legacy infrastructure amid a rapidly evolving threat landscape.

Key Report Takeaways

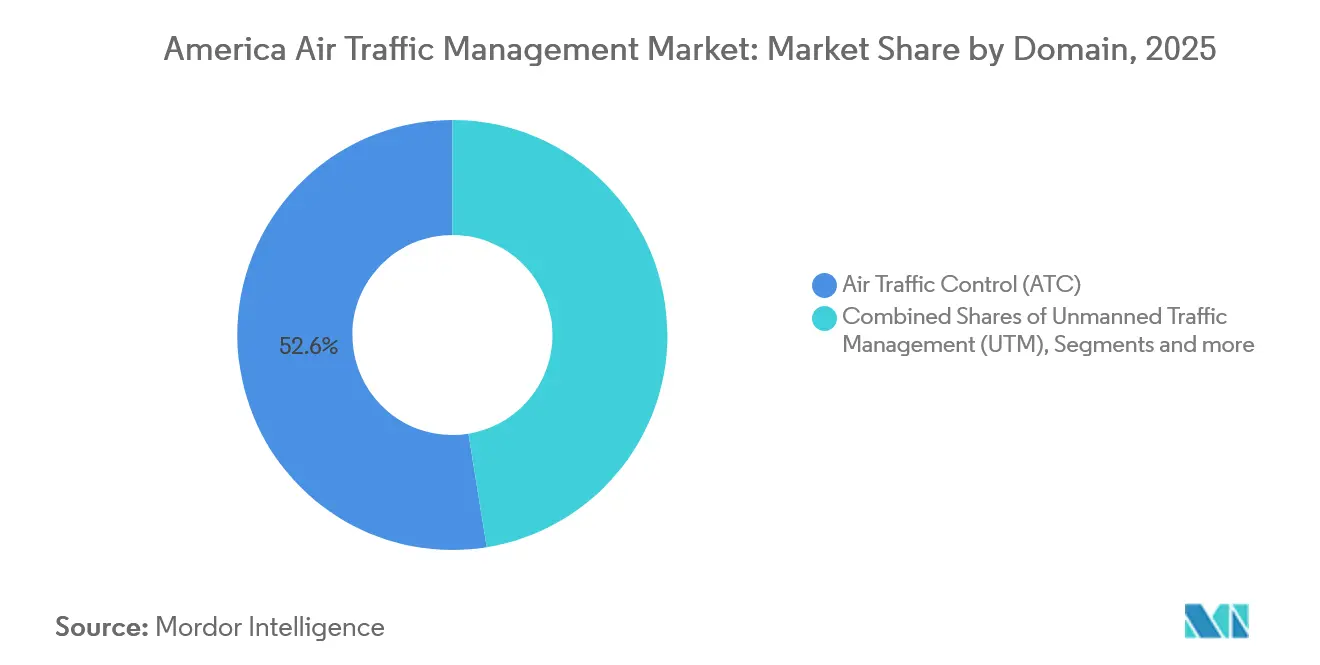

- By domain, air traffic control led with 52.55% of the American air traffic management market share in 2025, while unmanned traffic management recorded the fastest projected CAGR at 10.45% through 2031.

- By component, hardware accounted for 57.23% of the American air traffic management market in 2025; software is forecast to expand at an 8.35% CAGR through 2031.

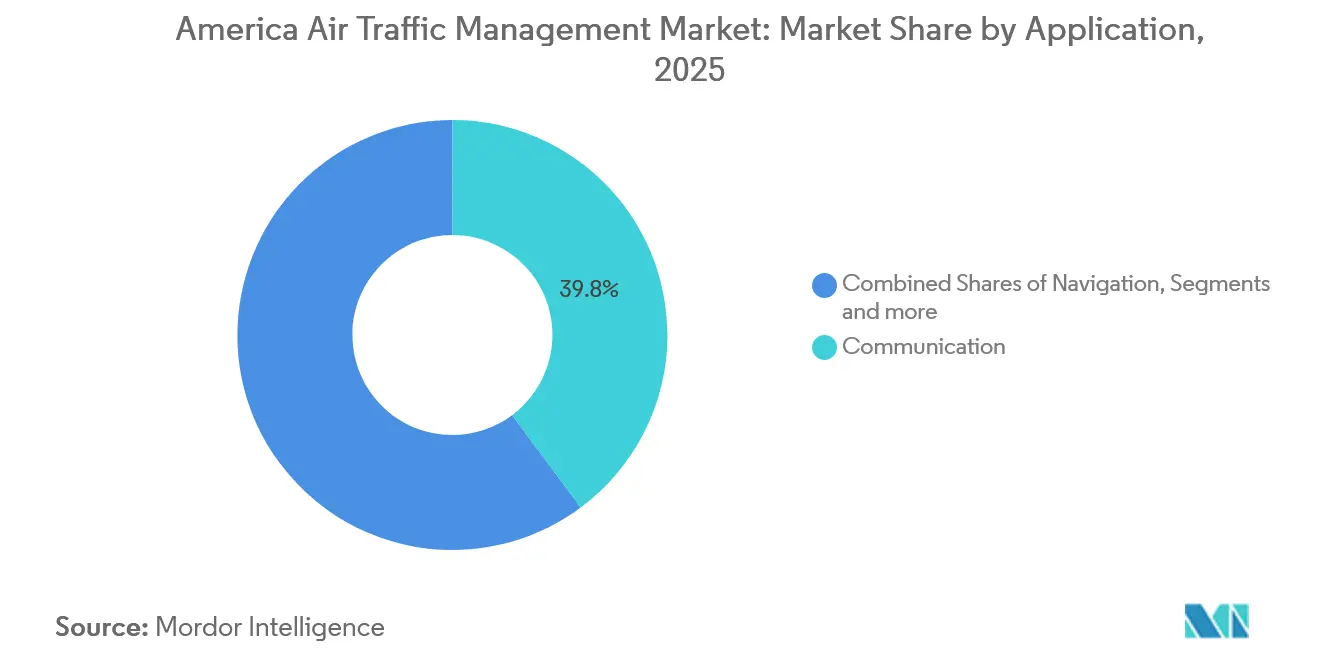

- By application, communication systems accounted for 39.83% of the American air traffic management market in 2025, and automation and decision-support are advancing at a 9.74% CAGR through 2031.

- By end use, commercial aviation accounted for 64.16% of revenue in 2025, while urban air mobility and drone operations are expected to grow at a 9.32% CAGR through 2031.

- By geography, the United States captured 52.73% of the American air traffic management market share in 2025, whereas Brazil is projected to post an 8.61% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

America Air Traffic Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FAA multi-billion NextGen investment pipeline sustains long-term demand | +1.9% | United States core, spillover to Canada and Mexico | Long term (≥ 4 years) |

| Controller shortage accelerating tower and terminal automation uptake | +1.7% | North America primary, emerging in Brazil | Medium term (2-4 years) |

| Satellite-based ADS-B boosting cross-ocean surveillance contracts | +1.5% | Global, emphasis on trans-Pacific and trans-Atlantic routes | Medium term (2-4 years) |

| Remote/digital-tower cost savings for secondary airports | +1.3% | North America and Europe, expanding to Latin America | Short term (≤ 2 years) |

| Cyber-hardening mandates for critical ATM infrastructure | +1.0% | Global, led by North America and Europe | Short term (≤ 2 years) |

| U-space/UTM integration for drone and AAM traffic | +0.9% | United States and Canada leading, Brazil following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FAA Multi-Billion NextGen Investment Pipeline Sustains Long-Term Demand

Congress funded USD 3.2 billion for facility and equipment upgrades in fiscal 2024, with an additional USD 8 billion committed for radar replacement and digital infrastructure through 2029.[1]Federal Aviation Administration, “Controller Workforce Plan 2024-2027,” FAA.GOV Predictable cash flows allow suppliers to scale R&D in performance-based navigation, data communications, and System Wide Information Management modules that improve throughput by 15-20%. The American air traffic management market consequently enjoys stable procurement cycles that shield vendors from traffic-volume volatility.

Controller Shortage Accelerates Automation Adoption

Certified controller headcount dropped to 11,500 in 2024, over 20% below FAA staffing goals, prompting reliance on AI-powered conflict-detection and remote-tower solutions. NAV CANADA’s 42-airport remote-tower network cut operating costs 35%, validating the business case for distributed operations.[2]NAV CANADA, “Annual Report 2024,” NAVCANADA.CA Automation vendors now bundle predictive analytics with digital-tower kits, expanding the American air traffic management market.

Satellite ADS-B Transforms Oceanic Surveillance Economics

Aireon’s space-based constellation covers 95% of global airspace, enabling 3-minute separation over oceans versus 15-minute radar intervals.[3]Aireon, “Global Space-Based ADS-B Coverage Milestone,” AIREON.COM Airlines saved USD 300 million in fuel during 2025 by flying optimal tracks, and ANSPs subscribe rather than invest in expensive radars. Subscription fees create recurring revenue, boosting the American air traffic management industry’s service component.

Remote Towers Reshape Secondary Airport Economics

The first US digital-tower went live at Leesburg Executive Airport in 2024, after European pilots proved 30-50% cost savings. AI video analytics, 4K cameras, and object-tracking overlays extend controller situational awareness, letting one operator manage multiple low-volume fields. Latin American regulators are drafting rules that allow similar models, broadening the American air traffic management market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy system obsolescence inflates sustainment costs | −1.2% | North America primary, aging globally | Medium term (2-4 years) |

| Fragmented ANSP governance across the Americas | −0.9% | Pan-American, cross-border ops | Long term (≥ 4 years) |

| Skilled-workforce gap delaying modernization roll-outs | −0.8% | Global, acute in North America & Brazil | Medium term (2-4 years) |

| Evolving cyber threat landscape raises compliance burden | −0.7% | Global, high-risk facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy System Obsolescence Creates Modernization Bottlenecks

Aging ATM infrastructure, with some systems dating back to the 1970s, faces escalating maintenance costs and component obsolescence, which can delay modernization timelines by 12-18 months while consuming budgets intended for capability enhancements. The FAA’s Terminal Doppler Weather Radar network alone requires USD 500 million in upgrades to remain operational through 2030, and spare parts for legacy systems are priced at premium levels because OEM production lines shut down a decade ago.[4]Government Accountability Office, “Air Traffic Control Modernization: Progress and Challenges,” GAO.GOV

Fragmented Governance Impedes Regional Harmonization

The Americas encompass 35 sovereign Air Navigation Service Providers that apply divergent technical standards, certification processes, and operating procedures, complicating cross-border traffic management and interoperability of technologies. ICAO’s Performance-Based Navigation rollout shows uneven progress: Chile and Colombia achieved Required Navigation Performance 0.3 on most trunk routes, whereas others still rely on conventional VOR airways, limiting route flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Domain: Convergence of ATC and UTM

Air Traffic Control accounted for 52.55% revenue in 2025, while Unmanned Traffic Management posted a 10.45% CAGR forecast. The American air traffic management market size for UTM solutions is projected to reach USD 1.2 billion by 2031. FAA trials demonstrated that automated separation is viable for BVLOS operations, prompting regulators to codify performance standards. Suppliers that deliver single-pane views for manned and unmanned traffic reduce console clutter, appealing to resource-constrained towers. Migration toward common service buses enables modular upgrades, positioning integrated domain products as the default procurement model within the American air traffic management market.

Early adopters of UTM invest in geofencing, telemetry validation, and digital Certificates of Authorization to streamline drone logistics. Latin American cargo carriers plan pilot routes over sparsely populated Amazon corridors, relying on satcom UTM links. These hybrid operations demand elastic compute back-ends that fuse ADS-B, multilateration, and drone telemetry in milliseconds. Vendors offering scalable APIs monetize data feeds for insurance, weather, and vertiport-scheduling apps, adding subscription layers atop core surveillance and expanding America's air traffic management industry's revenue streams.

By Component: Software Upswings, Hardware Stabilizes

Hardware dominated with a 57.23% share in 2025 because radar and VHF systems entail lump-sum contracts. Yet, Software is growing at an 8.35% CAGR due to cloud migration and AI analytics. The American air traffic management software market is forecast to reach USD 3.3 billion by 2031. Open architectures decouple functions from proprietary boards, allowing ANSPs to push updates quarterly rather than triennially. Microsoft Azure and AWS obtained FedRAMP authorizations that unlock elastic compute for trajectory prediction during thunderstorm bursts.

Services sustain steady double-digit growth as operators outsource cybersecurity audits, regression testing, and phased cutovers. Consultancy revenue gains traction when legacy‐site migrations require shadow operations for 6-12 months. The pivot to software-defined infrastructure ultimately compresses hardware margins but creates annuity opportunities, reshaping competitive positioning in the American air traffic management market.

By Application: Automation and Decision-Support Surge

Communication systems retained 39.83% slice, driven by CPDLC rollouts across en-route centers. However, Automation and Decision-Support commands the growth spotlight at 9.74% CAGR. Machine-learning engines analyze wind data, demand patterns, and runway occupancy, issuing reroute suggestions that cut delays by up to 25% during peak storms. The American air traffic management market size for automation modules is expected to exceed USD 2 billion by 2031.

Surveillance portfolios now integrate synthetic-aperture radar, ADS-B, and passive RF sensors to safeguard mixed-use corridors. Navigation upgrades leverage dual-frequency GPS and SBAS corrections, facilitating Required Navigation Performance 0.3 in mountainous terrain. These layered capabilities feed predictive algorithms, closing the loop between sensing and automation in the American air traffic management industry.

By End-Use: UAM as Catalyst

Commercial Aviation continues to supply 64.16% revenue, yet UAM and Drone Operations forecast 9.32% CAGR. Joby Aviation secured its FAA certification in 2024, moving type-certification closer. Municipalities in Los Angeles, Miami, and Mexico City earmarked vertiport budgets, signaling early infrastructure demand. The American air traffic management market must orchestrate low-altitude, high-cycle-rate flights around class B airspace without overloading controllers.

Military and Government customers invest in resilient voice networks that interoperate with civilian data services during disaster relief. Cyber-hardened gateways filter classified traffic, ensuring no bleed-over to public channels. Steady defense outlays cushion suppliers from civil traffic swings, maintaining base volumes within the American air traffic management industry.

Geography Analysis

North America is projected to account for 71% of the revenue in 2025, with the United States contributing 52.73%. The United States segment of the Americas air traffic management market is expected to reach approximately USD 5.5 billion by 2031, driven by domestic programs. NextGen deployments, remote-tower pilots in Colorado, and TFDM rollouts across 89 airports drive sustained procurement. Canada’s NAV CANADA leverages user-fee predictability to fund continual tech refresh, including space-based ADS-B subscriptions that trimmed oceanic separation and saved airlines CAD 100 million (USD 72 million) in 2025.

Latin America contributes the remaining 29% and offers higher growth. Brazil is expected to post an 8.61% CAGR as DECEA modernizes terminal radars around São Paulo and Rio and introduces Performance-Based Navigation in 62 airports. Mexico’s SENEAM collaborates with Thales on a national VHF digital link and will extend multilateration to Baja corridors by 2027. Argentina, Colombia, and Peru are utilizing funding from the CAF - Banco de Desarrollo de América Latina (Development Bank of Latin America) and the World Bank to upgrade air traffic control infrastructure. This includes replacing outdated ASR-9 radar systems. These modernization efforts are creating opportunities for medium-sized procurement bids in areas such as radar technology, sensor upgrades, and related technical services..

Regional integration lags as sovereign airspace policies diverge. COCESNA unifies six Central American states, but bilateral harmonization between larger economies remains a work in progress. ICAO-led SWIM demonstrations showed 15% route-time reduction on Miami-Bogotá corridors, yet permanent adoption awaits legislative alignment. Over the forecast period, multilateral financing and capacity-building programs should narrow the digital divide, expanding the American air traffic management market.

Competitive Landscape

The American air traffic management market includes established primes RTX Corporation, Lockheed Martin, Honeywell, Thales, and Indra, which account for the majority of 2025 revenue. Market entry barriers rise as contracts bundle cyber certifications and long warranty periods. Thales’s USD 150 million buyout of Cobham’s ATM unit fortified its radar portfolio and U.S. manufacturing base in 2024.

Software-first challengers like Altitude Angel and AirMap focus on UTM APIs and partner with telcos for 5G network slicing. L3Harris won USD 180 million in 2024 to upgrade Terminal Doppler Weather Radars with dual-polarization, highlighting demand for niche expertise. Honeywell rolled out Forge for Aviation, a SaaS analytics suite that lowers upfront costs for regional ANSPs.

Competitive intensity centers on cloud deployments, AI decision engines, and quantum-safe encryption. Incumbents co-invest with hyperscale providers to shorten accreditation timelines, while midsize firms tout agile sprints that add features quarterly. As procurement cycles tighten, partnerships between primes and dynamic ISVs emerge, balancing certification muscle with innovation speed in the American air traffic management industry.

America Air Traffic Management Industry Leaders

L3Harris Technologies Inc.

RTX Corporation

THALES

Indra Sistemas S.A.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Collins Aerospace was awarded a USD 438 million contract by the Federal Aviation Administration to support the Radar System Replacement program, a cornerstone of the agency's effort to modernize the US National Airspace System. The program is a key part of the Department of Transportation's Brand New Air Traffic Control System.

- December 2025: The United States Department of Transportation and the FAA awarded an up to USD 32.5 billion contract to Peraton to revamp the aging US air traffic control system, previously valued at USD 1.5 billion.

- November 2024: Indra secured a contract from the Federal Aviation Administration (FAA) to modernize the country's air traffic management (ATM) ground-air communications system. The upgrade involves replacing the existing analog radio systems (UHF and VHF) with advanced digital radio equipment, which supports both analog and VoIP operations.

America Air Traffic Management Market Report Scope

Air traffic management encompasses the systems, software, and services that enable safe and efficient aircraft movement through controlled airspace. Core functions include communication, navigation, surveillance, traffic flow management, aeronautical information distribution, and emerging unmanned traffic coordination.

The American air traffic management market is segmented by domain, component, application, end-use, and geography. By domain, the market covers air traffic control, air traffic flow and capacity management, aeronautical information management, and unmanned traffic management. By component, it breaks down into hardware, software, and services. By application, it is classified into communication, navigation, surveillance, and automation, and decision-Support. By end-use, the study considers commercial aviation, military and government, and urban air mobility/drone operations. Geographically, the analysis spans North America and South America. The report offers market size by value for all segments in USD Billion.

By Domain

| Air Traffic Control (ATC) |

| Air Traffic Flow and Capacity Management (ATFCM) |

| Aeronautical Information Management (AIM) |

| Unmanned Traffic Management (UTM) |

By Component

| Hardware |

| Software |

| Services |

By Application

| Communication |

| Navigation |

| Surveillance |

| Automation and Decision-Support |

By End-use

| Commercial Aviation |

| Military and Government |

| Urban Air Mobility/Drone Operations |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Domain | Air Traffic Control (ATC) | |

| Air Traffic Flow and Capacity Management (ATFCM) | ||

| Aeronautical Information Management (AIM) | ||

| Unmanned Traffic Management (UTM) | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application | Communication | |

| Navigation | ||

| Surveillance | ||

| Automation and Decision-Support | ||

| By End-use | Commercial Aviation | |

| Military and Government | ||

| Urban Air Mobility/Drone Operations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the America air traffic management market by 2031?

It is forecast to reach USD 10.45 billion, expanding at 10.49% CAGR from 2026.

Which application is expanding fastest?

Automation and Decision-Support, at a 9.74% CAGR as AI conflict-resolution tools gain acceptance.

Why is software spending rising rapidly?

Cloud-native platforms and continuous feature updates drive an 8.35% CAGR for software compared with slower hardware cycles.

Which country offers the highest growth in Latin America?

Brazil, posting an 8.61% CAGR through 2031 on the back of radar and PBN modernization.

How are cybersecurity mandates influencing contracts?

ANSP tenders now require quantum-resistant encryption and ISO 27001 pipelines, favoring vendors with mature security credentials.

What segment benefits most from UAM emergence?

Unmanned Traffic Management, expected to touch USD 1.2 billion in value by 2031 as eVTOL services scale.

Page last updated on: