Unmanned Surface Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

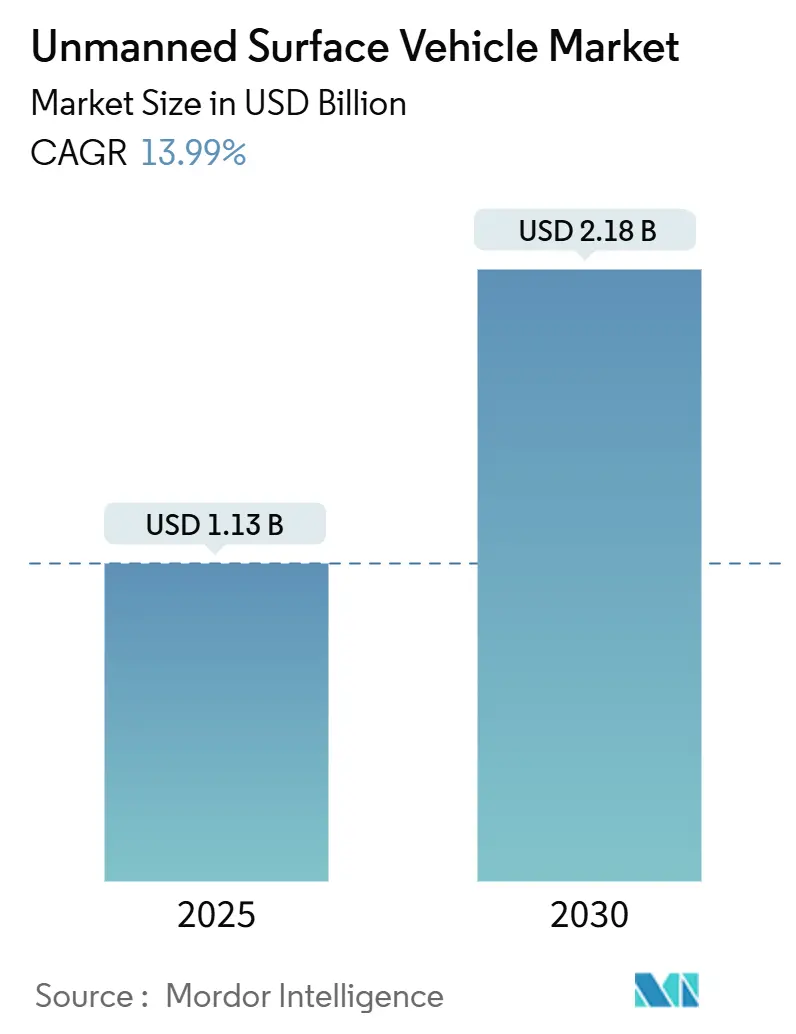

| Market Size (2025) | USD 1.13 Billion |

| Market Size (2030) | USD 2.18 Billion |

| Growth Rate (2025 - 2030) | 13.99% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unmanned Surface Vehicle Market Analysis by Mordor Intelligence

The unmanned surface vessel (USV) market size stands at USD 1.13 billion in 2025 and is forecasted to climb to USD 2.18 billion by 2030, advancing at a 13.98% CAGR. Rising defense investment in distributed maritime operations, sharp progress in artificial-intelligence navigation suites, and broader commercial uptake for offshore wind and environmental monitoring keep demand momentum high. Program funding from the US Department of Defense (DoD), large-scale procurement initiatives by European navies, and energy companies’ push to curb inspection costs spur near-term adoption of autonomous surface fleets. System reliability gains, falling sensor and processor prices, and class-society acceptance of remote operation protocols further expand the addressable customer base. Yet, the USV market also navigates regulatory fragmentation, cyber-risk exposure, and competition from unmanned air and sub-surface systems, which may temper deployment speed if not managed proactively.

Key Report Takeaways

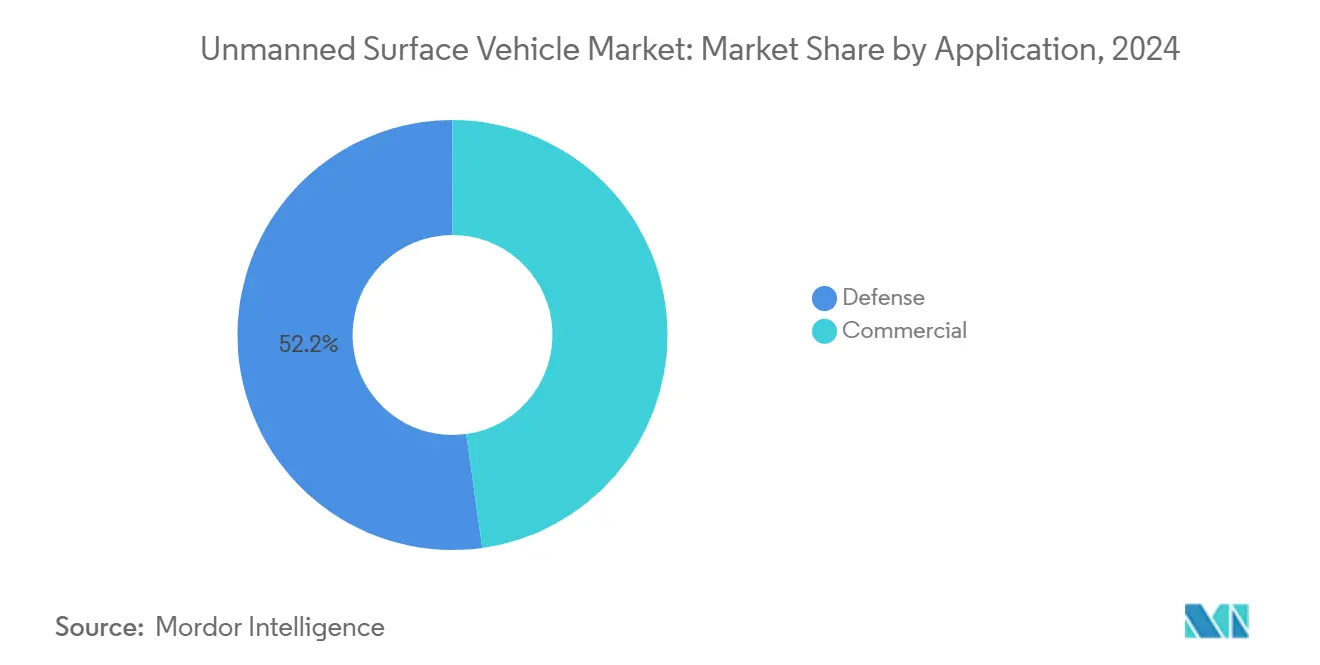

- By application, defense held 52.21% of the USV market share in 2024, while commercial missions are forecasted to register the fastest 14.81% CAGR to 2030.

- By mode of operation, autonomous platforms captured 56.48% revenue in 2024 and are projected to expand at a 17.41% CAGR through 2030.

- By size, large vessels led with a 32.40% share in 2024; small vessels are on track for a 31.10% CAGR, the highest among all classes.

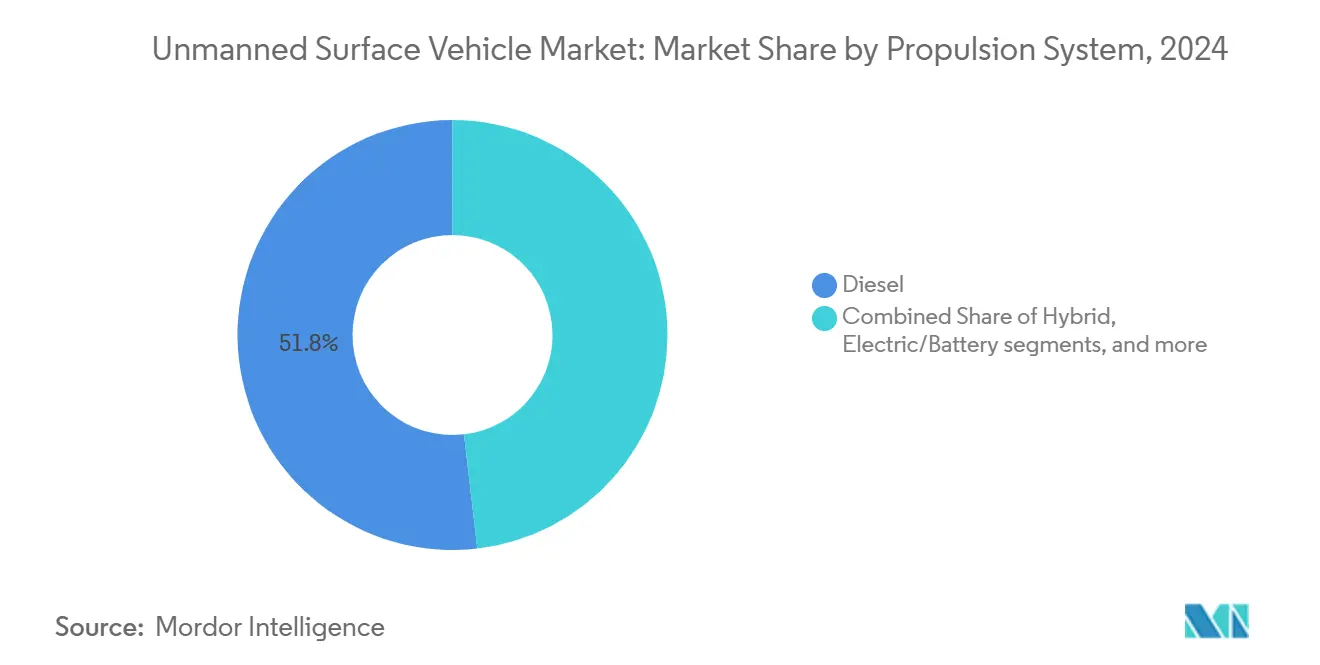

- By propulsion, diesel retained a 51.84% share in 2024, yet solar propulsion is expected to accelerate at a 23.08% CAGR up to 2030.

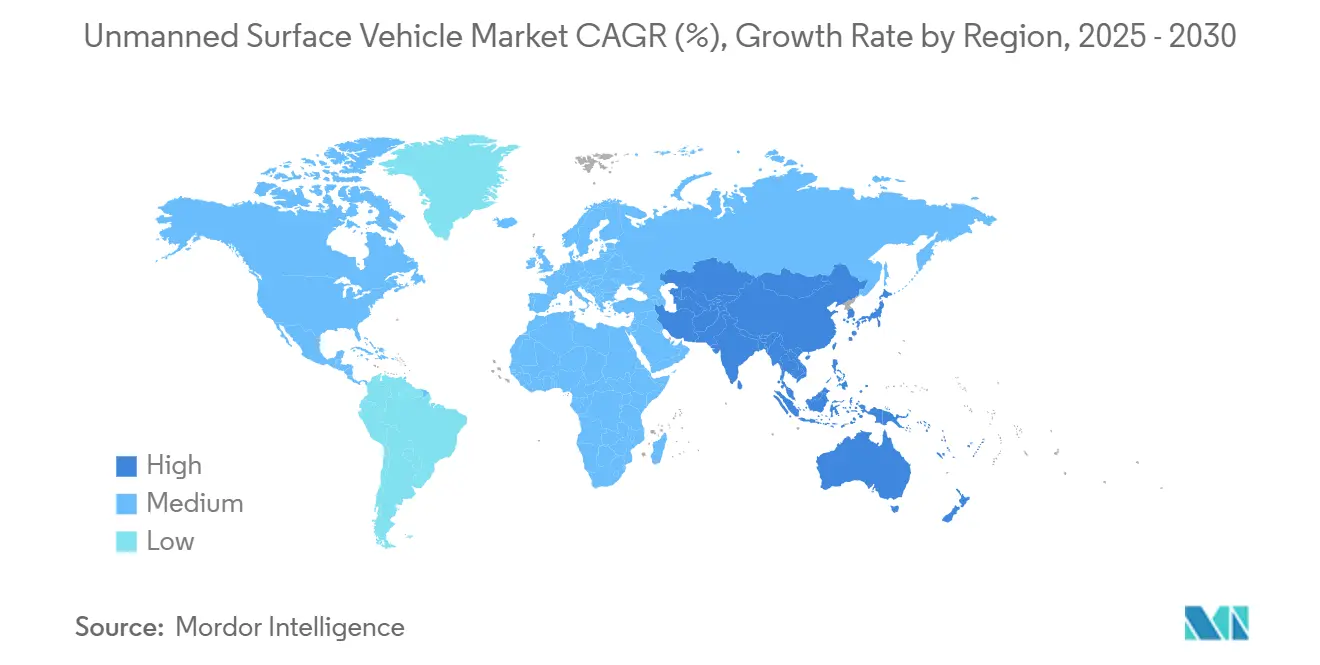

- By geography, North America commanded 36.10% of the 2024 revenue pool and is anticipated to post a 16.23% CAGR over the forecast horizon.

Global Unmanned Surface Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strategic naval shift toward distributed and autonomous surface fleets | +3.2% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Advancements and cost reductions in maritime autonomy systems | +2.8% | Global, concentrated in technology hubs | Short term (≤ 2 years) |

| Expanding use of USVs for offshore renewable energy site monitoring | +2.1% | Europe and APAC core, spillover to North America | Medium term (2-4 years) |

| Regulatory push for ocean health and climate data collection | +1.4% | Global, with NOAA and European agencies leading | Long term (≥ 4 years) |

| Breakthroughs in hybrid and solar propulsion enabling long-endurance missions | +1.8% | Global, early adoption in research institutions | Medium term (2-4 years) |

| Increased insurance sector readiness for autonomous maritime risk coverage | +1.1% | North America and Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strategic Naval Shift Toward Distributed and Autonomous Surface Fleets

Global navies continue to restructure force concepts, embedding the USV market assets as persistent sensors and logistics nodes that preserve manned fleet safety in high-threat waters. The US Marine Corps proved autonomous cargo resupply using Textron’s ALPV during 2024 trials, cutting manpower exposure in contested zones. Singapore’s Maritime Security Command subsequently achieved a 60% reduction in crewed patrol boat deployment after fielding MARSEC USVs for harbor surveillance. Taiwan’s Endeavor Manta program illustrates how smaller navies harness indigenous USVs for asymmetric deterrence amid tightening regional security budgets. Distributed fleet architectures let commanders network low-cost hulls across broad sea lanes, collecting ISR data while reserving frigates and destroyers for complex engagement decisions. Adoption accelerates as procurement agencies validate cost-effectiveness, prompting vendors to standardize command-and-control interfaces that integrate seamlessly with existing combat-management systems.

Advancements and Cost Reductions in Maritime Autonomy Systems

Rapid sensor miniaturization and AI-enabled perception have slashed the entry price for fully autonomous surface navigation. DARPA’s USX-1 Defiant sailed congested sea lanes without human override 2024, leveraging language-model mission planning to avoid dynamic obstacles.[1]Source: DARPA, “USX-1 Defiant Achieves Autonomous Navigation Milestone,” darpa.mil Commercial autonomy kits now cost roughly one-third less than in 2023, due to edge-compute chipsets that boost onboard processing while cutting power draw. Sea Machines integrated its SM300 suite across 15 hull types in a year, demonstrating scalable retrofits that broaden the USV market beyond defense prime contractors. High-precision, anti-jamming GNSS receivers, once reserved for top-tier military fleets, retail at 40% cheaper than a year earlier, extending reliable navigation to smaller operators. As integration expense falls, port authorities receive a rising volume of permit applications for autonomous trials, showing that affordability drives market penetration and regulatory engagement.

Expanding Use of USVs for Offshore Renewable Energy Site Monitoring

Europe’s offshore wind build-out pushes developers to adopt always-on monitoring that limits turbine downtime and satisfies strict environmental mandates. Vattenfall employs Saildrone craft to map sea-state and wildlife interactions around North Sea turbines, reporting inspection cost savings reaching 40% versus manned vessels. Fugro’s Blue Essence surveyed Scotland’s Beatrice array in 2024, identifying subsea cable risks 18 months earlier than planned manned surveys.[2]Source: Fugro, “Blue Essence USV Completes Beatrice Survey,” fugro.com The EU Marine Strategy Framework Directive obliges year-round biodiversity tracking at renewable sites, encouraging long-endurance USV market deployments. Solar-powered HydroSurv craft logged 30-day offshore missions, collecting environmental data without returning to port, while AI-assisted analytics converted raw feeds to actionable maintenance cues for operators and regulators alike.

Breakthroughs in Hybrid and Solar Propulsion Enabling Long-Endurance Missions

Energy harvesting innovations lengthen mission windows from days to months, redefining deployment economics. The University of Florence’s Alotta platform finished a 180-day Mediterranean trial powered by solar and wind capture systems that removed fuel logistics costs. NOAA and Saildrone partnered on eight-week Arctic climate runs aboard wind-assisted SD-3000 hulls, maintaining continuous satellite telemetry even under polar winter skies. Improved lithium-iron-phosphate batteries delivered 25% higher energy density in 2024, granting smaller craft the reserves needed for complex sensor operation at extended range. SeaTrac’s SP-48 paired wave-energy converters with solar panels, achieving net-positive power in moderate seas and giving researchers the option of indefinite deployment cycles. These advances let scientific and commercial users book true blue-water missions impractical for earlier USV market offerings anchored to diesel-fuel supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of clear international regulatory standards for autonomous ships | -2.1% | Global, with varying national interpretations | Medium term (2-4 years) |

| Persistent cybersecurity risks in unmanned maritime operations | -1.8% | Global, heightened in contested regions | Short term (≤ 2 years) |

| Operational limitations in GNSS-denied or contested environments | -1.2% | Regional hotspots, military applications | Medium term (2-4 years) |

| Capability redundancies with unmanned aerial and underwater systems | -0.9% | Defense markets primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Clear International Regulatory Standards for Autonomous Ships

The International Maritime Organization’s MASS Code remains in draft stage, leaving ship owners to navigate a patchwork of national rules that slows procurement and inflates compliance costs. The United Kingdom mandates human oversight for every autonomous mission. In contrast, Norway licenses fully unmanned voyages inside designated fjords, forcing manufacturers to design configuration variants that satisfy divergent flag-state demands.[3]Source: International Maritime Organization, “MASS Code Development,” imo.org Port authorities, lacking shared inspection templates, subject arriving USVs to ad-hoc entry negotiations that prolong turnaround times. Insurance carriers hesitate to underwrite casualty scenarios without uniform liability frameworks, a gap that raises operating expenditure. The resulting uncertainty compels some renewable-energy developers to continue chartering crewed support vessels, limiting near-term USV market scale-up in commercially attractive zones.

Persistent Cybersecurity Risks in Unmanned Maritime Operations

Maritime cyber attacks jumped 76% in 2024, with hackers exploiting communication channels of autonomous craft to steal data or override commands. A notable breach of Norwegian offshore support USVs forced emergency recovery, illustrating how compromised protocols risk environmental disasters and reputational damage. Wide adoption of open-source navigation stacks broadens attack surfaces, while quantum computing progress threatens existing encryption. Mandatory cybersecurity audits add cost and time to fleet rollouts. Elevated insurance surcharges, in some cases topping 40% of base premium, signal persistent exposure, dampening investment appetite among conservative ship-owners and state agencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Dominant Defense Expenditure Sustains Leadership

Defense operations accounted for 52.21% of the USV market revenue in 2024, a position underpinned by navies prioritizing ISR and mine-countermeasure missions in contested littorals. The segment is projected to expand at a 14.81% CAGR through 2030, buoyed by multibillion-dollar procurement frameworks such as the US Navy’s Ghost Fleet Overlord initiative that demands persistent, distributed sensors across Indo-Pacific routes. L3Harris’s C-Worker platform exemplifies how modular payload bays deliver tailored surveillance kits without redesigning core hull architecture, a feature echoed in European and Asia-Pacific acquisition plans. Governments integrate USVs to lower casualty risk, extend presence in anti-access zones, and free capital ships for frontline engagements. Complementing ministry budgets, joint R&D programs distribute costs and quicken capability cycles, accelerating translation of laboratory autonomy breakthroughs into deployable fleets.

Commercial applications, although smaller, demonstrate accelerating uptake as offshore energy operators and scientific agencies validate prolonged unmanned missions. Continuous seabed survey contracts command a rising share of hydrographic budgets, as Blue Essence and comparable craft gather higher-resolution bathymetric data than crewed vessels permitted by weather windows. Environmental monitors leverage 24/7 sampling to meet emerging ESG reporting obligations, expanding addressable revenues for service providers. The interplay of dual-use technologies ensures that military advances—high-bandwidth satcom, multi-sensor fusion—rapidly migrate to civil markets, reinforcing a virtuous cycle that underpins overall USV market expansion.

By Mode of Operation: Autonomy Secures Preference Amid Regulatory Evolution

Large USVs commanded a 32.40% share in 2024, supplying ample deck space and power reserves for heavy sensors, mine-sweep gear, and weapons modules needed by blue-water fleets. However, small vessels will post a 31.10% CAGR to 2030, fueled by lean procurement budgets, minimal shore-side infrastructure needs, and a growing appetite for swarm tactics that distribute sensing across numerous low-cost nodes. Ocean Aero’s TRITON, integrating surface and subsurface propulsion, typifies multifunctional versatility that smaller agencies find financially accessible. High-volume, automated production lines shorten delivery cycles, while containerized shipping simplifies global deployment.

Medium platforms bridge mission gaps, supporting heavier payloads than small craft but retaining manageable logistics footprints suitable for commercial survey firms. Extra-large hulls remain niche, mostly experimental mother-ship concepts that launch aerial or underwater drones; their future adoption hinges on doctrinal shifts toward unmanned task groups. Overall, cost curves favor miniaturization, and advances in micro-electronics allow small hulls to house sensor suites once exclusive to destroyer-sized ships, propelling the USV market toward broader user communities.

By Size: Small Platforms Propel Fleet Proliferation

Large USVs commanded a 32.40% share in 2024, supplying ample deck space and power reserves for heavy sensors, mine-sweep gear, and weapons modules needed by blue-water fleets. However, small vessels will post a 31.10% CAGR to 2030, fueled by lean procurement budgets, minimal shore-side infrastructure needs, and a growing appetite for swarm tactics that distribute sensing across numerous low-cost nodes. Ocean Aero’s TRITON, integrating surface and subsurface propulsion, typifies multifunctional versatility that smaller agencies find financially accessible. High-volume, automated production lines shorten delivery cycles, while containerized shipping simplifies global deployment.

Medium platforms bridge mission gaps, supporting heavier payloads than small craft but retaining manageable logistics footprints suitable for commercial survey firms. Extra-large hulls remain niche, mostly experimental mother-ship concepts that launch aerial or underwater drones; their future adoption hinges on doctrinal shifts toward unmanned task groups. Overall, cost curves favor miniaturization, and advances in micro-electronics allow small hulls to house sensor suites once exclusive to destroyer-sized ships, propelling the USV market toward broader user communities.

By Propulsion System: Renewable Energy Challenges Diesel Supremacy

Diesel engines supplied dependable high-power thrust and held a 51.84% share in 2024, ensuring mission readiness across adverse sea states and enabling sprint speeds vital for security patrols. Yet, the solar segment will rise at 23.08% CAGR as panel efficiency improves and autonomous routing lets craft maximize isolation. Saildrone’s Pacific deployments clocked 12-month voyages without refuel stops, validating cost reductions tied to fuel-free endurance.

Hybrid diesel-electric configurations combine conventional reliability with silent electric mode, making them attractive for anti-submarine surveillance and wildlife studies where acoustic stealth matters. Battery advances, with 25% density gains in 2024, bring medium-duration electric missions within the financial reach of research institutes. Environmental legislation that caps maritime emissions in protected zones will likely uplift zero-emission propulsion adoption curves, gradually chipping away diesel’s historical dominance within the USV market.

By Payload: Sensor Integration Lifts Data-Driven Services

Chassis and electronic backbones formed 27.00% of 2024 revenue, as every hull relies on robust control, navigation, and power distribution frameworks. However, sensor suites are projected to climb at 16.40% CAGR through 2030 because data acquisition—not platform ownership—drives user value in maritime analytics. Demand spans electro-optical cameras for surface imaging, synthetic-aperture sonars for seabed mapping, and multi-spectral payloads that merge IR and radar for all-weather surveillance.

Modular open-system architectures let operators swap sensors between missions, accelerating fleet utilization rates. Weapon modules remain limited to defense customers but influence platform design, requiring resilient deck structures and secured data links. Communication payloads, including high-bandwidth Ka-band antennas, continue to evolve as value-add extensions that push live data ashore, cementing payload flexibility as a central purchasing criterion in the Unmanned surface vessels industry.

Geography Analysis

North America sustained 36.10% of 2024 revenue and is forecasted to rise at a 16.23% CAGR, reflecting the US Navy’s multi-year procurement push under its Distributed Maritime Operations framework and NOAA’s expanding climate-research charters that capitalize on long-endurance solar-hybrid hulls. Venture funding, typified by Saronic’s USD 600 million Series B round, also signals deep investor confidence in the region’s capacity to scale autonomous production lines. Canada complements US adoption with Arctic sovereignty patrols deploying solar-powered craft that operate in ice-choked passages long after conventional cutters withdraw for the season.

Europe ranks second, propelled by offshore wind build-outs and supportive regulatory stances that shorten permitting cycles for autonomous trials. Norway’s Maritime Authority allows commercial unmanned transits within demo corridors, attracting technology pilots from German, British, and French operators. The EU Green Deal intensifies environmental monitoring duties, bringing steady service contracts for data-as-a-service providers in the USV market. Concurrently, European navies, led by France and the United Kingdom, allocate budget lines for mine countermeasure USVs that mesh with NATO’s collective maritime domain-awareness goals.

Asia-Pacific records the fastest regional upswing outside North America due to maritime-security modernization in Japan, Australia, and South Korea, and strategic competition in the South China Sea, driving multi-country interest in distributed sensor fleets. Japan’s MSDF integrated USVs into fleet exercises during 2024 to bolster anti-submarine picket lines, while Australia’s BlueBottle contract highlights sovereign capability ambitions in persistent Indian-Ocean surveillance. Commercial shipping firms in Korea and Singapore test autonomous cargo vessel routes, indicating cross-industry diffusion beyond defense and energy. Infrastructure constraints and uneven policy alignment temper immediate uptake in South America and the Middle East & Africa, yet pilot projects focused on port security and offshore resource surveys foreshadow incremental market entries.

Competitive Landscape

Competition remains moderate with no single vendor exceeding 15% share, granting room for agile newcomers and specialized robotics firms to carve niches. Legacy defense primes such as L3Harris and Textron leverage established naval relationships and proven program-management frameworks to win multi-year contracts, while integrating advanced electronics from their broader portfolios enhances cross-platform economies of scale. Kongsberg and Saab’s 2024 partnership unites maritime control systems with electronic countermeasure expertise, mirroring a broader consolidation trend aimed at offering turnkey autonomous packages.

Emergent players like Saildrone, Sea Machines, and Saronic differentiate through software-centric stacks emphasizing AI decision engines, renewable-energy propulsion, and cloud-native data portals. Saronic’s Port Alpha facility targets 100 vessels annually, signaling confidence in production scalability that could shift the balance toward high-volume manufacturing. Patent filings for autonomy algorithms rose 45% in 2024, evidencing fierce intellectual-property competition as vendors race to lock in proprietary collision-avoidance, path-planning, and cyber-resilience techniques. Overall, the USV market tilts toward firms that blend rapid software iteration with reliable marine engineering, as end-users prioritize mission assurance and life-cycle cost over platform lineage.

Unmanned Surface Vehicle Industry Leaders

L3Harris Technologies, Inc.

Teledyne Technologies Incorporated

Textron Inc.

QinetiQ Group plc

Fugro N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Saildrone completed a demonstration for NATO's Task Force X Baltic initiative by operating four Voyager-class USVs.

- April 2025: The Republic of Korea Navy (RoKN) awarded HD Hyundai Heavy Industries (HD HHI) a contract to jointly develop a USV for autonomous reconnaissance and combat operations.

Global Unmanned Surface Vehicle Market Report Scope

| Defense | Intelligence, Surveillance, and Reconnaissance (ISR) |

| Mine Countermeasure (MCM) | |

| Anti-Submarine Warfare (ASW) | |

| Naval Warfare | |

| Others | |

| Commercial | Environment Monitoring |

| Infrastructure Inspection | |

| Hydrographic Survey | |

| Others |

| Autonomous |

| Remotely Operated |

| Small |

| Medium |

| Large |

| Extra-Large |

| Diesel |

| Hybrid (Diesel-Electric) |

| Electric/Battery |

| Solar |

| Sensors |

| Camera Systems |

| Sonar |

| Communication Systems |

| Weapon Systems |

| Chassis and Electronic Systems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Defense | Intelligence, Surveillance, and Reconnaissance (ISR) | |

| Mine Countermeasure (MCM) | |||

| Anti-Submarine Warfare (ASW) | |||

| Naval Warfare | |||

| Others | |||

| Commercial | Environment Monitoring | ||

| Infrastructure Inspection | |||

| Hydrographic Survey | |||

| Others | |||

| By Mode of Operation | Autonomous | ||

| Remotely Operated | |||

| By Size | Small | ||

| Medium | |||

| Large | |||

| Extra-Large | |||

| By Propulsion System | Diesel | ||

| Hybrid (Diesel-Electric) | |||

| Electric/Battery | |||

| Solar | |||

| By Payload | Sensors | ||

| Camera Systems | |||

| Sonar | |||

| Communication Systems | |||

| Weapon Systems | |||

| Chassis and Electronic Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Unmanned surface vehicle (USV) market?

The USV market size is USD 1.13 billion in 2025 with a forecasted to climb to USD 2.18 billion by 2030, registering a 13.98% CAGR.

Which application generates the most revenue for autonomous surface vessels?

Defense applications accounted for 52.21% of 2024 revenue, driven by ISR and MCM demand.

How fast are solar-powered USVs expected to grow?

Solar-propelled platforms are projected to register a 23.08% CAGR through 2030 due to fuel-free endurance advantages.

Which region leads in adopting unmanned surface vessels?

North America holds 36.10% of global revenue, propelled by substantial U.S. defense and NOAA investments.

What is the primary restraint affecting commercial deployment?

The absence of harmonized international regulations for autonomous ships introduces uncertainty, curbing rapid commercial rollout.

Who are the notable new entrants challenging established defense contractors?

Software-centric firms such as Saildrone, Sea Machines, and Saronic are gaining traction through AI-driven platforms and renewable-energy propulsion.

Page last updated on: