Unmanned Marine Vehicles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

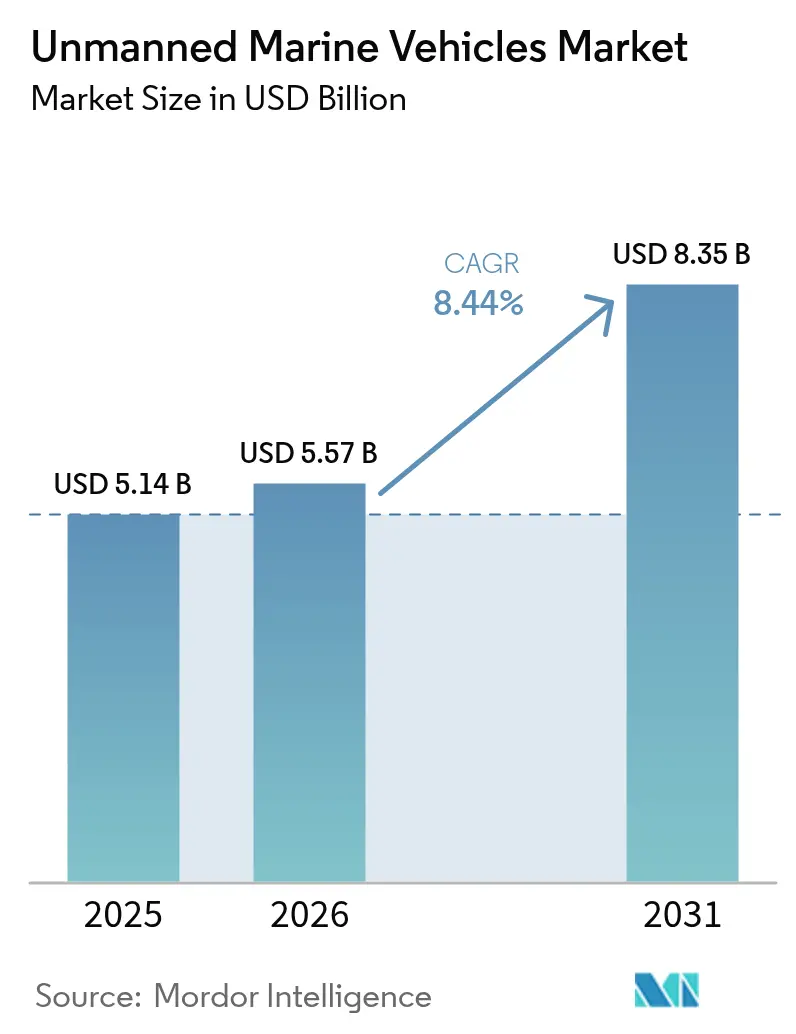

| Market Size (2026) | USD 5.57 Billion |

| Market Size (2031) | USD 8.35 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unmanned Marine Vehicles Market Analysis by Mordor Intelligence

The unmanned marine vehicles market size was valued at USD 5.14 billion in 2025 and estimated to grow from USD 5.57 billion in 2026 to reach USD 8.35 billion by 2031, at a CAGR of 8.44% during the forecast period (2026-2031). Heightened naval modernization programs, an expanding offshore energy footprint, and surging demand for persistent ocean-data collection underpin this growth trajectory. Uncrewed platforms are shifting from experimental tools to indispensable assets that extend the reach of defense forces, lower inspection costs for oil, gas, and wind operators, and widen the scope of long-duration climate missions. Intensifying geopolitical flashpoints spur procurement of stealthy undersea systems, while sustainability mandates accelerate the pivot toward low-emission powertrains. Venture-capital-backed start-ups inject rapid-iteration culture into a field dominated by defense primes, enabling faster prototype cycles and driving double-digit order books for smaller, swarm-capable craft. Ecosystem participants increasingly view software—autonomy algorithms and data-fusion engines as the decisive differentiator for next-generation fleets.

Key Report Takeaways

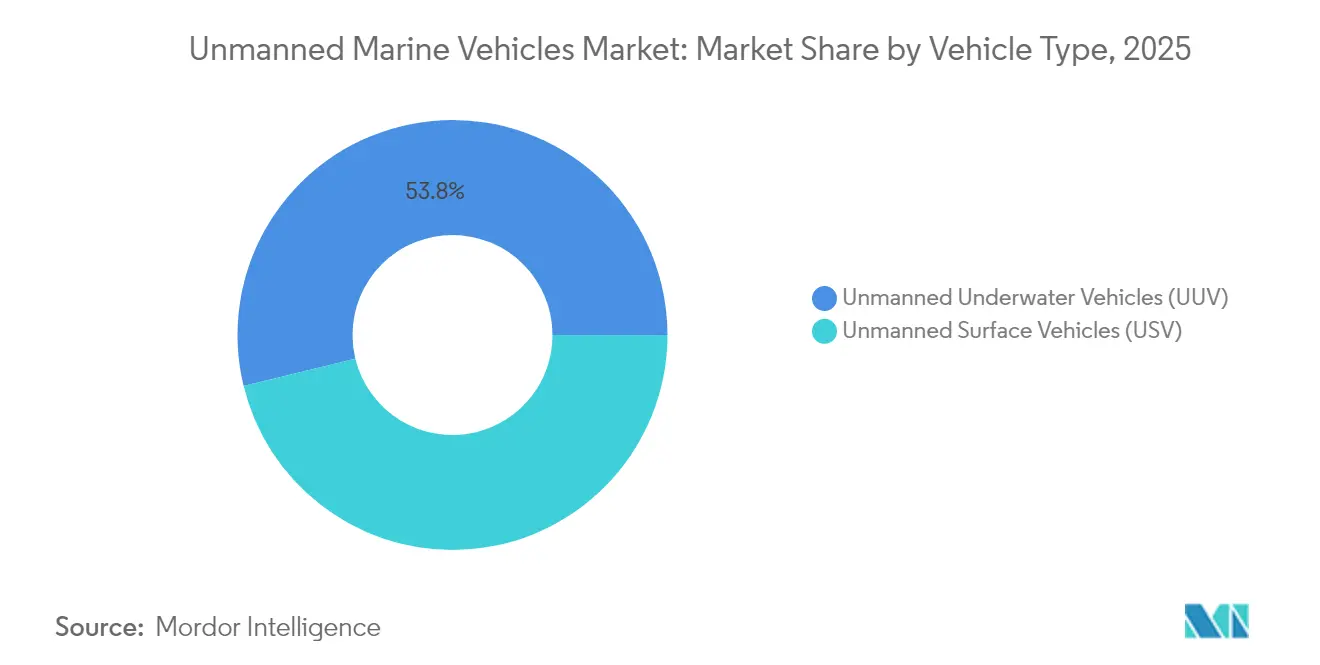

- By vehicle type, unmanned underwater vehicles captured 53.81% of the unmanned marine vehicles market share in 2025; the same segment is forecasted to expand at 11.03% CAGR through 2031.

- By vehicle size, medium craft commanded a 31.02% share of the unmanned marine vehicles market size in 2025, while micro vehicles are expected to hold the highest CAGR at 9.86% during the forecast period.

- By propulsion, electric systems held 31.95% of 2025 revenue; solar propulsion is expected to grow at a 10.65% CAGR to 2031.

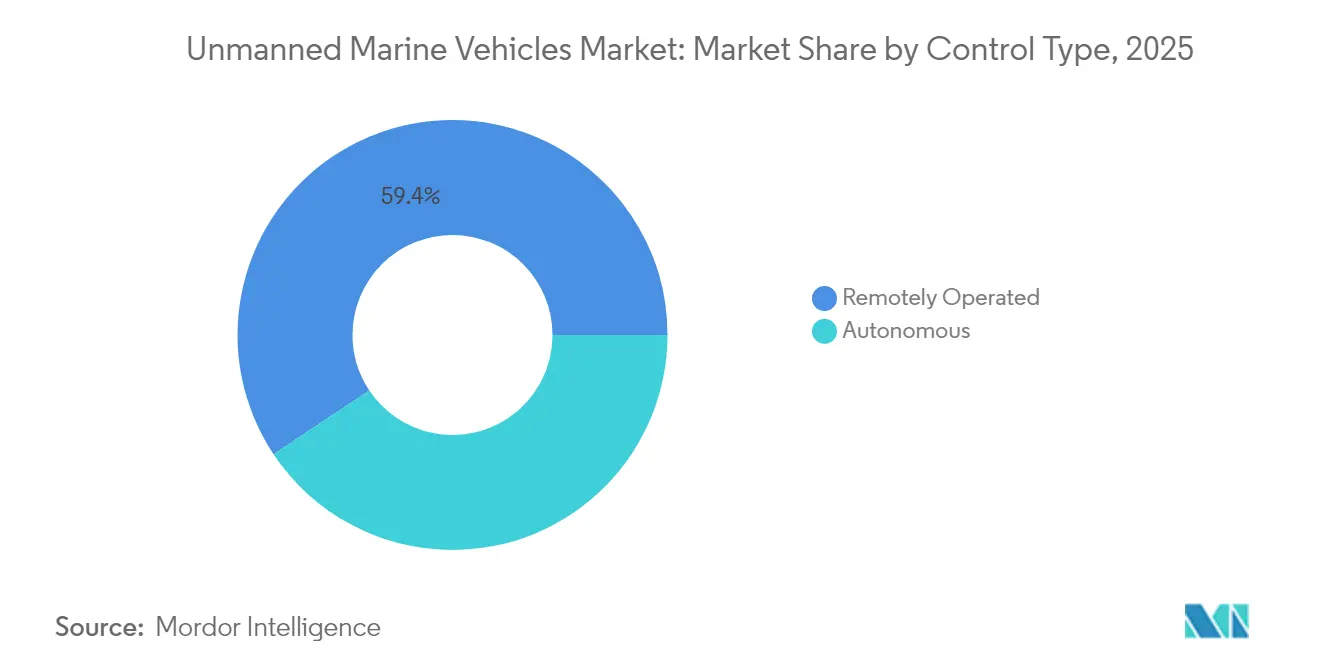

- By control type, remotely operated platforms accounted for 59.35% of 2025 sales, yet autonomous systems are advancing at 11.56% CAGR to 2031.

- By application, defense and security led with 46.10% of 2025 revenue; commercial use cases are poised to rise at 9.31% CAGR over the forecast window.

- By geography, North America led with 32.97% revenue share in 2025; Asia-Pacific is forecasted to post a 10.28% CAGR, the highest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Unmanned Marine Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased defense investments in ISR and anti-submarine warfare capabilities | +2.1% | North America, Europe, spillover to APAC | Medium term (2-4 years) |

| Growing utilization of UMVs for offshore oil and gas inspection and maintenance | +1.8% | North Sea, Gulf of Mexico, Asia-Pacific | Short term (≤ 2 years) |

| Expanding use of autonomous systems in oceanographic and climate research | +1.2% | Global, polar regions, deep ocean | Long term (≥ 4 years) |

| Emerging role of UMVs in offshore renewable energy operations and maintenance | +1.5% | Europe, North America, expanding to APAC | Medium term (2-4 years) |

| Proliferation of subscription-based ocean data services enabled by UMV fleets | +0.9% | Developed maritime economies | Long term (≥ 4 years) |

| Emergence of ocean data-as-a-service subscription model | +0.7% | Global maritime data hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Defense Investments in ISR and Anti-Submarine Warfare Capabilities

Escalating maritime tensions drive navies to bankroll sophisticated unmanned fleets that plug coverage gaps in contested waters. The US Navy budgeted USD 177.3 million for uncrewed systems in fiscal 2025, with the Replicator initiative targeting mass production of autonomous undersea craft. Anduril’s Rhode Island plant can now roll out more than 200 Dive-LD vehicles annually. Parallel programs such as Australia’s Ghost Shark and India’s XLUUV tender reinforce a multi-regional procurement wave. European alignment is visible in France’s Naval Group drone demonstrators, underpinning future cooperative under-ice operations. Combat success stories from the Black Sea validate operational concepts and compress acquisition timelines, while Taiwan and Norway expand indigenous production to address local threat matrices.

Growing Utilization of UMVs for Offshore Oil and Gas Inspection and Maintenance

Energy majors now deploy autonomous underwater vehicles (AUVs) that slice inspection outlays by up to 55% compared with tethered ROVs.[1]Terradepth, “Survey Services,” TERRADEPTH.COM TotalEnergies’ pilot of remotely controlled robots illustrates the shift toward onshore command hubs that cut offshore headcount. AUVs accelerate anomaly detection, shorten dry-dock intervals, and halve environmental footprints, prompting Gulf operators and North Sea contractors to retrofit digital twins for predictive maintenance. Renewable-powered uncrewed surface vessels in the UAE merge decarbonization goals with automation efficiencies. Conceptual studies such as DNV’s Solitude envisage fully unmanned floating LNG units realizing 20% operating-cost savings.

Expanding Use of Autonomous Systems in Oceanographic and Climate Research

Research agencies demand multi-month endurance to capture fine-grained data on carbon fluxes, polar melt rates, and deep-ocean currents. Seaglider platforms transmit live readings over satellite links for seasons at a time.[2]University of Washington, “Seaglider Autonomous Underwater Vehicle,” APL.UW.EDU Australia’s IMOS network logs seabed imagery with centimeter precision, feeding data to open portals for global modeling efforts. European operators, led by Cyprus Subsea, maintain large fleets of M1 Seagliders for ecosystem monitoring. MIT’s bio-inspired glider designs promise step-change energy efficiency, which is essential for polar traverses. Emerging swarm deployments, illustrated by Cyprus’s reef-monitoring EONIOS project, democratize high-resolution mapping while trimming vessel charter budgets.

Emerging Role of UMVs in Offshore Renewable Energy Operations and Maintenance

With technician logistics absorbing more than 80% of lifetime costs for distant wind farms, operators are fielding uncrewed platforms for blade-tip scans and cable-lay surveys. The US Bureau of Safety and Environmental Enforcement records 35-80% cost reductions when drones replace rope-access teams. Innovate-UK-funded HydroSurv trials electrical USVs for seagrass baseline surveys that underpin environmental approvals. Australia’s Hydrus AUV cut deep-water exploration spend by 75% by eliminating divers and large support vessels. Machine-learning-powered digital twins improve anomaly forecasting and schedule service runs during fair-weather windows, securing yield targets as turbines migrate into 60-meter-plus depths.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant capital expenditure and operational cost burdens | -1.4% | Global, pronounced in developing markets | Short term (≤ 2 years) |

| Lack of harmonized regulatory and classification frameworks | -0.8% | International operators | Medium term (2-4 years) |

| Emerging cybersecurity vulnerabilities in underwater communication networks | -0.6% | Global defense and commercial fleets | Long term (≥ 4 years) |

| Limited endurance and payload constraints in compact UMV platforms | -0.5% | All regions and applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Significant Capital Expenditure and Operational Cost Burdens

Price tags for large uncrewed surface vehicles reach USD 250 million per hull, while the US Navy’s XLUUV program alone will draw USD 21.5 million in FY 2025. Hydrogen-fuel-cell AUV concepts eliminate emissions but demand bespoke bunkering and inflate upfront budgets. Nauticus Robotics posted a USD 50.7 million loss in 2023, underscoring the protracted payback period for breakthrough subsea morphing platforms. Venture rounds such as Blue Water Autonomy’s USD 14 million seed highlight the steep capital ladder that early-stage innovators must climb before first revenue.

Lack of Harmonized Regulatory and Classification Frameworks

The IMO’s draft MASS Code will not reach adoption before 2030, extending uncertainty for commercial fleet managers. Europe’s AI Act imposes new validation layers for autonomous logic, adding complexity to approval pipelines. Interim class guidance from ABS provides navigation lanes yet forces builders to juggle divergent rulebooks across flag states. The US Coast Guard’s roadmap acknowledges the gap, but timelines remain fluid. Legal ambiguities around liability and salvage rights impede insurance underwriting for transoceanic ventures. Absence of unified test protocols inflates compliance costs and stalls cross-border commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Underwater Dominance Drives Innovation

Unmanned underwater vehicles (UUVs) retained 53.81% of the unmanned marine vehicles market share in 2025 while also logging the highest 11.03% CAGR through 2031, cementing their role as the sector’s dual growth and revenue engine. Demand springs from anti-submarine warfare upgrades and deep-water infrastructure inspection, with China’s typhoon-proof Blue Whale illustrating 30-day submerged endurance benchmarks.

Surface vehicles absorb the balance of the unmanned marine vehicles market but gain traction for coastal surveillance, mine countermeasures, and logistics. The United States’ hybrid fleet model exploits persistent surface patrols to complement covert undersea assets. Convergence trends show submarine-launched UAVs and joint surface-subsurface tasking that rewrite traditional mission doctrines.

By Vehicle Size: Micro Platforms Challenge Conventional Scaling

Medium craft secured 31.02% of 2025 revenue thanks to balanced payload-endurance profiles, yet micro vehicles sprint ahead at 9.86% CAGR, propelled by swarm robotics and barrier-free launch requirements. Compact nodes enable blanket coverage of littoral zones while minimizing attrition risk.

The modular design allows a scale-agnostic chassis where mission packs swap in at sea, blurring size boundaries. Soft-material thrusters and piezoelectric actuation sharpen maneuverability in confined pipelines and reef crevices. Swarm-based artificial reef monitoring in Cyprus validates month-long untended deployments, expanding biodiversity insights without research-vessel charters.

By Propulsion: Solar Innovation Disrupts Electric Leadership

Electric drives commanded 31.95% of 2025 sales, anchoring most inspection, research, and patrol profiles. Solar solutions, backed by net-zero mandates, are eyeing a 10.65% growth pace to 2031. Multi-source hybrids knit solar, wave, and battery packs to extend station-keeping into multi-month windows.

Fuel-cell demonstrators from Norway reveal 24-hour submerged endurance with silent signatures prized for ISR, yet supply-chain resilience for membranes and catalysts remains pivotal. Diesel retains relevance for high-power sprint legs, but AI-managed energy-mix controllers quickly become the default architecture across hull sizes.

By Control Type: Autonomous Systems Reshape Operational Paradigms

Remotely piloted craft formed 59.35% of 2025 deployments; nonetheless, autonomous modes outpace them with an 11.56% forecast CAGR as navies and surveyors cut tether latency and radio-link exposure.

Machine-learning route planners now optimize waypoints on the fly to dodge adverse currents and dense shipping lanes. MIT’s AI-tuned hydrodynamic forms achieve energy savings unattainable through manual hull-form iteration. Classification societies progressively codify fault-tolerant logic, allowing fully crewless vessels to transit restricted straits.

By Application: Commercial Growth Outpaces Defense Dominance

Defense and security captured 46.10% of 2025 turnover, driven by escalating undersea rivalry and mine-clearance imperatives, whereas commercial missions are slated to accelerate at 9.31% through 2031.

Renewable developers tap autonomous inspection to keep capacity factors high amid deeper-water turbine rollouts, and oil majors leverage big-data fusion to shrink downtime during brown-field rejuvenations. Dual-use payload bays facilitate rapid shifts from mine counter-measures to pipeline cathodic-protection surveys, smoothing asset utilization curves across budget cycles.

Geography Analysis

North America held 32.97% of 2025 revenue, underpinned by the Pentagon’s multi-billion-dollar fleet recapitalization and venture-financed scale-ups such as Saronic’s Louisiana shipyard producing 150-foot Marauder drones. Canada’s Arctic programs and Mexico’s deep-water Campeche inspections add incremental demand loops. The region benefits from a mature defense industrial base, AI talent pools, and early-adopter regulatory sandboxing.

Asia-Pacific registers the steepest 10.28% CAGR through 2031 thanks to China’s fleet buildup, Australia’s AUKUS-linked Ghost Shark prototypes, and India’s tender for 12 XLUUVs that extend maritime domain awareness. Collaborative projects, including Norway’s decision to co-produce USVs in Ukraine, signal rising technology dispersion throughout the wider Indo-Pacific quadrant.

Europe leverages integrated shipbuilding clusters and cohesive R&D funding to sustain a robust pipeline of autonomous trials. The EU AI Act sets harmonization precedents that may translate into first-mover regulatory advantages. The United Kingdom evaluates Kongsberg Vanguard motherships for mine-hunting packages, while France’s Naval Group anchors continental expertise in large-diameter hull forms.

Competitive Landscape

The unmanned marine vehicles market features a moderate fragmentation profile where blue-chip defense primes intersect with venture-backed disruptors. L3Harris Technologies, Inc., Thales Group, and BAE Systems plc wield legacy program-of-record credentials, ensuring steady backlog streams. Anduril Industries deploys agile sprints that compress prototype cycles from years to months. Saronic’s USD 850 million raise at a USD 4 billion valuation epitomizes the capital magnetism surrounding autonomy-first shipyards.

Consolidation remains brisk: BlueHalo absorbed VideoRay to marry micro-ROV know-how with counter-UUV kill chains, and L3Harris Technologies, Inc. integrated ASV Global to broaden surface-hull portfolios.[4]Marine Technology News, “BlueHalo Acquires VideoRay,” MARINETECHNOLOGYNEWS.COM Certification muscle becomes a differentiator as ABS and equivalent bodies harden test matrices, favoring vertically integrated vendors that can shoulder documentation overheads.

White-space revenue models emerge around subscription ocean-data services: Terradepth’s Absolute Ocean platform offers pay-per-gigabyte bathymetry feeds, while Oceaneering signs on as anchor customer to leverage cross-asset benchmarks. Competitive intensity will continue to sharpen around high-density energy systems, containerized command modules, and off-the-shelf AI inference stacks.

Unmanned Marine Vehicles Industry Leaders

L3Harris Technologies, Inc.

Kongsberg Gruppen ASA

Teledyne Technologies Incorporated

Thales Group

Saab AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: HII secured an order from Hitachi, Ltd. for over a dozen REMUS 300 small uncrewed undersea vehicles (SUUVs), part of a multi-year delivery program.

- April 2025: HII delivered the first two Lionfish small uncrewed undersea vehicles (SUUVs) to the US Navy. This delivery is part of a program that has the potential to expand to 200 vehicles, backed by a contract valued at over USD 347 million.

- April 2025: HD Hyundai Heavy Industries (HD HHI) received a contract from the Republic of Korea (ROK) Navy to develop the concept design for a combat USV program. Through this collaboration, the company will expand the naval combat USV to enhance maritime warfare capabilities.

Global Unmanned Marine Vehicles Market Report Scope

The unmanned marine vehicles market includes autonomous underwater vehicles, remotely operated vehicles, semi-submersibles, and unmanned surface craft. The defense sector is increasingly adopting, in addition to commercial sectors, to map and monitor the conditions of the sea or ocean and explore various oil and gas sites.

The study covers unmanned marine vehicles that include surface vehicles and underwater vehicles. Unmanned vehicles that operate completely on the surface are part of surface vehicles (USV). Subsurface and underwater vehicles are part of the underwater vehicle segment (UUV). Further, the study covers the applications of unmanned marine vehicles that include defense, commercial, and research.

| Unmanned Surface Vehicles (USV) |

| Unmanned Underwater Vehicles (UUV) |

| Micro |

| Small |

| Medium |

| Large |

| Diesel |

| Electric |

| Hybrid |

| Solar |

| Remotely Operated |

| Autonomous |

| Defense and Security | Anti-Submarine Warfare (ASW) |

| Intelligence, Surveillance, and Reconnaissance (ISR) | |

| Mine Counter-Measures | |

| Commercial | Offshore Oil and Gas |

| Offshore Wind and Renewables | |

| Port and Infrastructure Inspection | |

| Scientific Research and Exploration | |

| Search and Rescue (SAR) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Vehicle Type | Unmanned Surface Vehicles (USV) | ||

| Unmanned Underwater Vehicles (UUV) | |||

| By Vehicle Size | Micro | ||

| Small | |||

| Medium | |||

| Large | |||

| By Propulsion | Diesel | ||

| Electric | |||

| Hybrid | |||

| Solar | |||

| By Control Type | Remotely Operated | ||

| Autonomous | |||

| By Application | Defense and Security | Anti-Submarine Warfare (ASW) | |

| Intelligence, Surveillance, and Reconnaissance (ISR) | |||

| Mine Counter-Measures | |||

| Commercial | Offshore Oil and Gas | ||

| Offshore Wind and Renewables | |||

| Port and Infrastructure Inspection | |||

| Scientific Research and Exploration | |||

| Search and Rescue (SAR) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the unmanned marine vehicles market in 2031?

The unmanned marine vehicles market size is forecasted to reach USD 8.35 billion by 2031.

Which segment leads revenue and growth simultaneously?

Unmanned underwater vehicles hold 53.81% revenue share and are expanding at 11.03% CAGR through 2031.

How fast is the Asia-Pacific region growing?

Asia-Pacific is set to record a 10.28% CAGR, the fastest among all regions.

Which propulsion technology shows the highest growth potential?

Solar based propulsion technology are projected to grow at 10.65% CAGR to 2031.

What recent milestone demonstrates submarine-launched drone capability?

In June 2025 the US Navy completed the first launch and recovery of a UUV from a nuclear submarine, proving covert deployment feasibility.

Which new business model is gaining traction in this sector?

Subscription-based ocean-data services, where operators lease fleets and sell data rather than hardware, are rapidly emerging.

Page last updated on: