Unmanned Sea Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

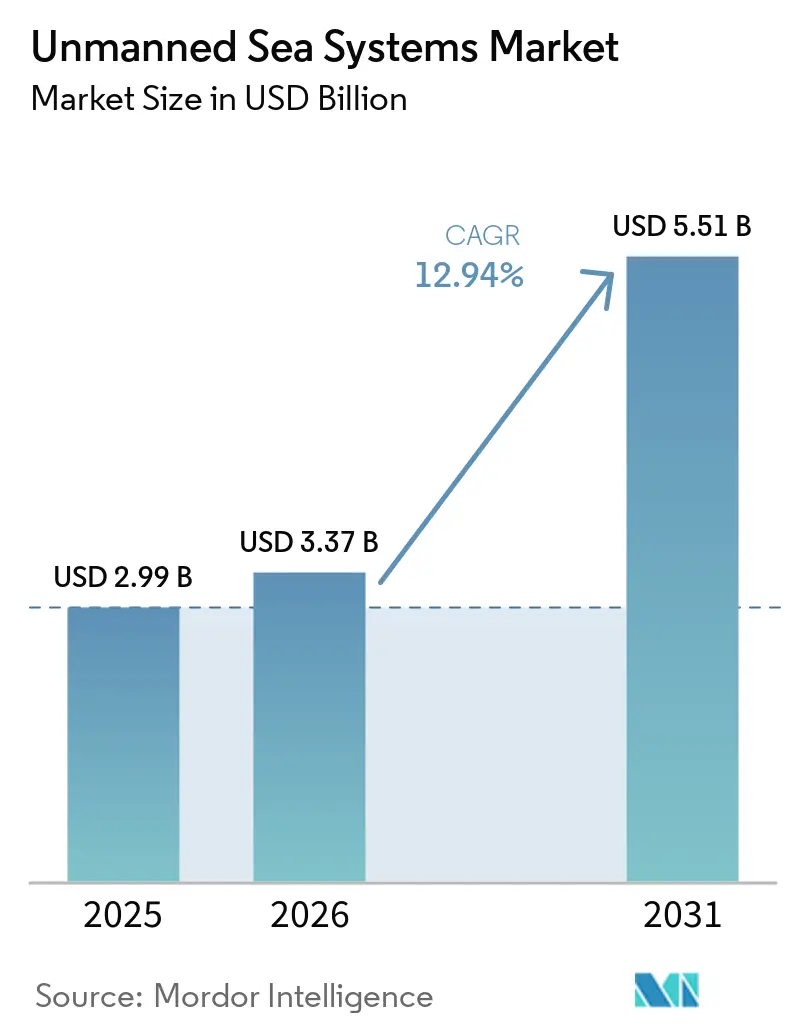

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 12.94% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unmanned Sea Systems Market Analysis by Mordor Intelligence

The unmanned sea systems market size is expected to grow from USD 2.99 billion in 2025 to USD 3.37 billion in 2026 and is forecast to reach USD 5.51 billion by 2031 at a 12.94% CAGR over 2026-2031. The growth profile is shaped by simultaneous defense and commercial priorities that reward persistence, safety, and lower operating costs at sea. Defense buyers are rebalancing spending toward low-signature, long-endurance capabilities that can operate from contested littorals to deep ocean theaters. At the same time, energy and infrastructure operators scale remote inspection to reduce emissions and weather downtime. Advancements in modular autonomy stacks and premium sonar payloads are shifting value to software and sensors, even as hull formats remain standardized for logistics and certification. Regulatory signals are clear in selected countries, driving firm demand for zero-crew and zero-emission deployments in specific corridors.

Key Report Takeaways

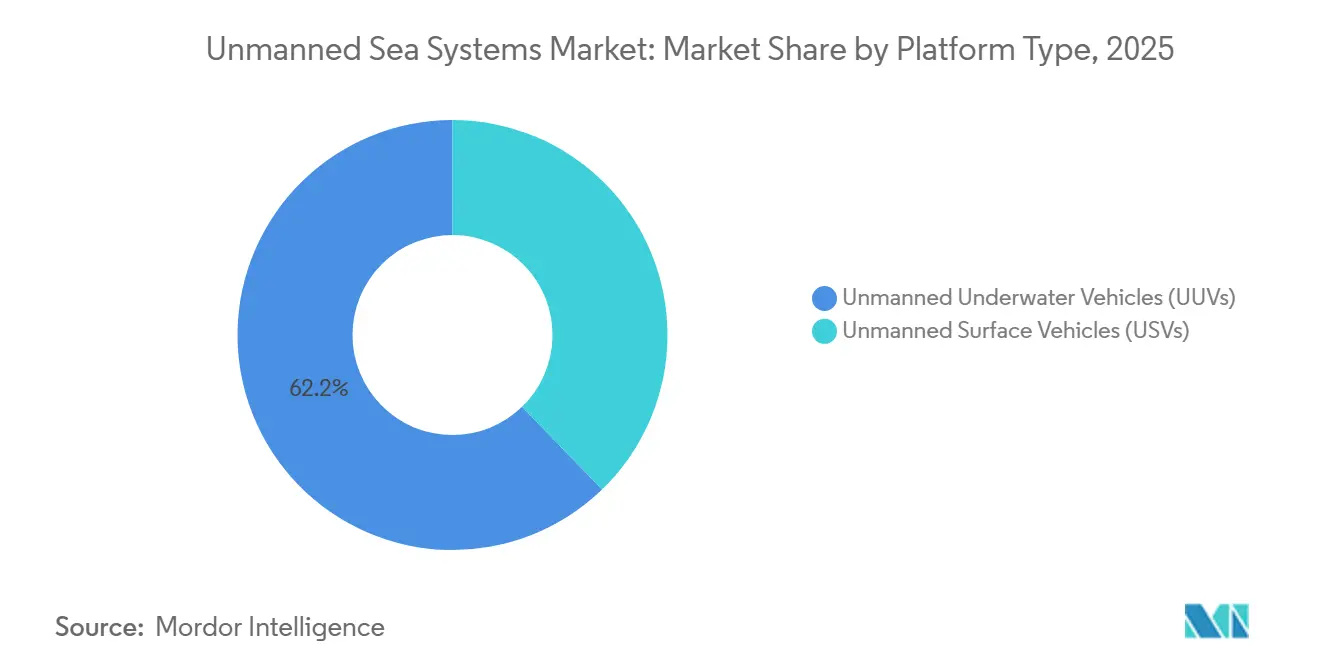

- By platform type, unmanned underwater vehicles (UUVs) led the unmanned sea systems market with 62.24% market share in 2025, while unmanned surface vehicles (USVs) posted the highest projected CAGR of 13.99% through 2031.

- By vehicle size, small-class formats captured a 49.20% share of the unmanned sea systems market in 2025 and are projected to expand at a 13.40% CAGR through 2031.

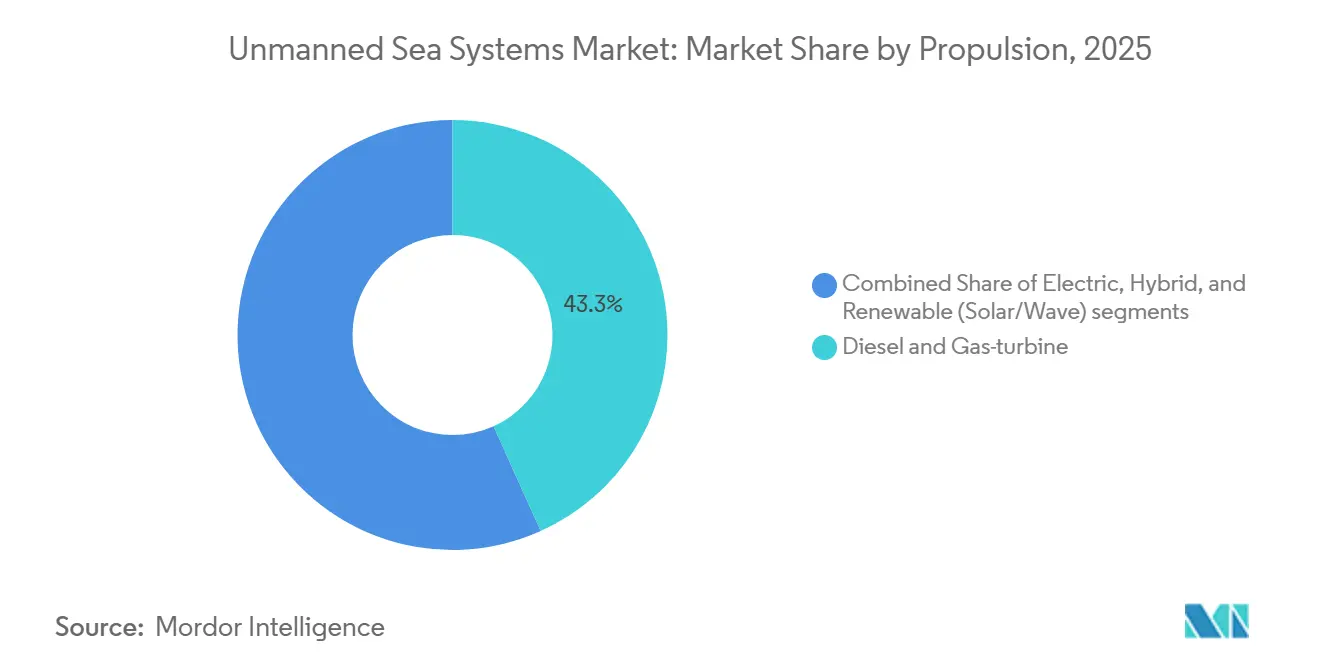

- By propulsion, diesel and gas-turbine systems held a 43.27% share of the unmanned sea systems market in 2025, while renewable hybrids are forecasted to grow the fastest at 14.89% CAGR through 2031.

- By application, the military accounted for a 52.59% share in 2025 and is advancing at a 13.16% CAGR through 2031.

- By component type, propulsion and power systems accounted for 32.60% of revenue in 2025, while the sensors suite segment is projected to record the fastest 14.10% CAGR through 2031.

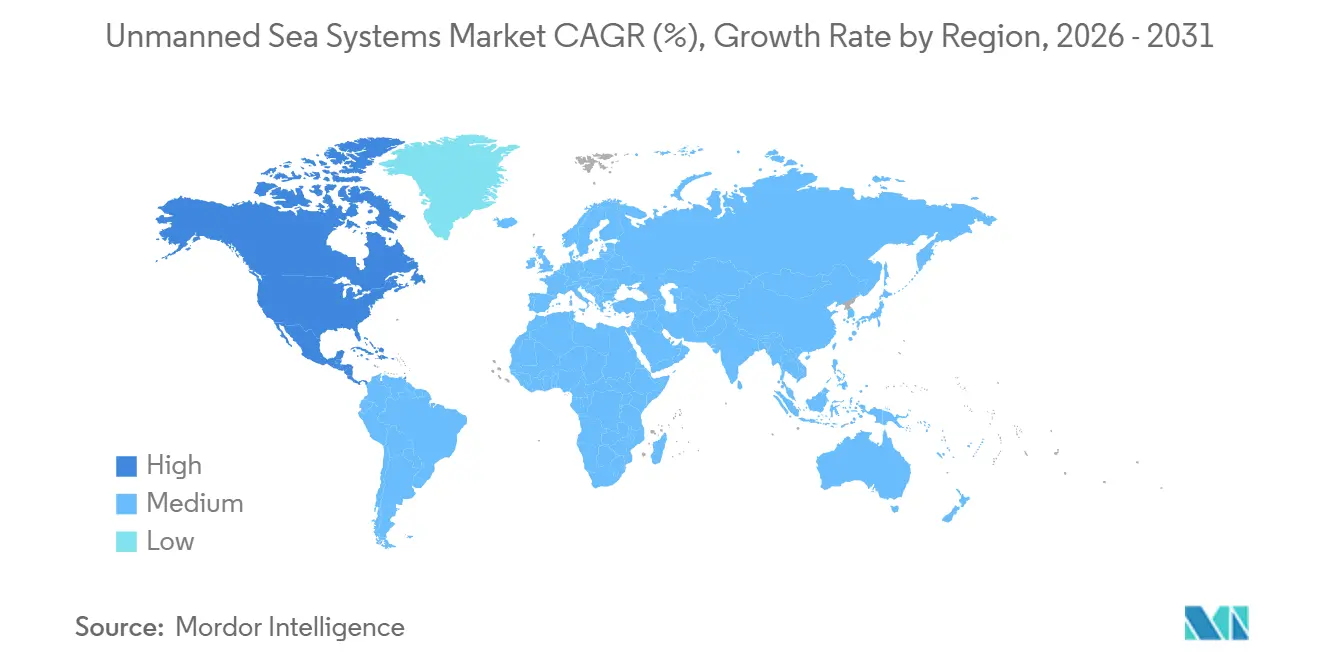

- By geography, North America held a 38.36% share of the unmanned sea systems market in 2025 and posted the highest regional CAGR of 14.09% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unmanned Sea Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global naval modernization and force transformation programs | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising demand for offshore wind farm inspection and seabed survey missions | +2.1% | Europe, Asia-Pacific, North America | Short term (≤ 2 years) |

| Declining cost per sea mile compared to crewed surface vessels | +1.9% | Global | Short term (≤ 2 years) |

| Increased adoption of swarm-capable USVs for MCM operations | +1.7% | North America, Europe, Middle East | Medium term (2-4 years) |

| ESG-linked insurance discounts for zero-crew craft | +1.2% | Europe, North America | Long term (≥ 4 years) |

| Defense offset policies promoting domestic integration of USS | +1.1% | Asia-Pacific, Middle East, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Naval Modernization and Force Transformation Programs

Defense procurement emphasizes autonomous platforms as force multipliers for operational efficiency in contested maritime environments. Newly introduced programs and prototypes highlight navies' progression from experimental phases to operational integration of mine warfare, ISR capabilities, and distributed undersea effectors in fleet planning. Lockheed Martin Corporation introduced the Lamprey Multi‑Mission Autonomous Undersea Vehicle in February 2026 as a modular submersible with a reconfigurable payload bay to support ISR, electronic warfare, and kinetic missions. Saab AB advances large undersea vehicles under national contracts, focusing on long-range deterrence and seabed defense, through formal European programs supporting strategic defense objectives. NATO is formalizing interoperability through standards and frameworks, reducing integration challenges for multinational task groups. These measures accelerate deployment timelines for autonomous assets and standardize modular payload updates, enhancing operational efficiency across allied fleets.

Rising Demand for Offshore Wind Farm Inspection and Seabed Survey Missions

Autonomous inspection is critical as offshore wind operators expand operations, balancing limited O&M budgets with stringent ESG compliance requirements. In April 2023, Fugro conducted the first fully remote offshore wind farm inspection using its Blue Essence USV and Blue Volta eROV. European wind‑farm stakeholders are introducing autonomy to reduce crew transfers and expand inspection windows, with field deployments that reveal strong operating cost and uptime benefits for persistent monitoring.[1]Cabinet Office of Japan, “AUV Strategy and Demonstration Projects,” Cabinet Office Japan, cao.go.jp These initiatives enhance zero-crew concepts by mitigating weather-related downtime, transitioning labor from sea to shore, and streamlining inspection payback. This establishes a dependable pipeline for unmanned platforms, underpinned by resilient O&M contracts across multiple wind basins.

Declining Cost per Sea Mile Compared to Crewed Surface Vessels

Regulatory approvals for uncrewed operations and the rise of certified remote operations centers are reshaping cost structures. In October 2025, the Norwegian Maritime Authority permitted Reach Remote 1 to operate uncrewed in the North Sea without a dedicated support vessel, signaling a replicable authorization path that removes a major operating expense for survey and inspection tasks. Shore-based, certified master supervisors overseeing multiple vessels enable a centralized expertise model, reducing reliance on distributed crews. Manufacturers of hybrid or fully electric designs benefit from increased adoption, driven by compounded energy and labor savings over extended mission durations, enhancing operational efficiency and cost-effectiveness.

Increased Adoption of Swarm-Capable USVs for MCM Operations

Navies are shifting mine countermeasures from sequential single‑platform clearance to coordinated, distributed action through swarms. The US Navy’s Unmanned Campaign Framework and the Belgian-Dutch rMCM program focus on standardizing swarm control software and inter-vessel communication protocols to enhance collaborative mine countermeasure operations. Industry efforts are advancing autonomy systems to coordinate multiple assets with shared sensing and tasking in complex near-shore environments. These initiatives integrate surface nodes with towed or hull-mounted sonar for classification and cueing, ensuring neutralization platforms operate effectively while keeping crewed ships at safer stand-off distances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export control regulations and ITAR restrictions limiting global sales | -1.4% | Middle East, Asia-Pacific, South America | Medium term (2-4 years) |

| High vulnerability to GNSS denial in contested maritime environments | -1.1% | Taiwan Strait, South China Sea, Baltic, Black Sea, Red Sea | Short term (≤ 2 years) |

| Limited availability of certified maritime AI-assurance and testing ranges | -0.9% | Global | Long term (≥ 4 years) |

| Disruptions in lithium-titanate battery supply impacting endurance-focused platforms | -0.7% | Supply concentrated in China, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export Control Regulations and ITAR Restrictions Limiting Global Sales

Licensing regulations and defense article classifications extend transaction cycles for autonomous vehicles and payloads, prompting vendors to localize production, customize configurations, or prioritize sales within regions aligned with shared compliance frameworks. Companies that deliver modular architectures can advance capability through payload upgrades that avoid fresh platform certifications, a method that can reduce the compliance burden on subsequent tranches. These dynamics collectively favor incumbents with established compliance teams and documented quality systems and can nudge market share toward geographies with clearer regulatory pathways.

High Vulnerability to GNSS Denial in Contested Maritime Environments

Intentional jamming and spoofing disrupt satellite-reliant autonomous navigation systems, increasing operational uncertainty and challenges in contested environments. Industry suppliers address this gap through sensor fusion, integrating Doppler velocity logs, inertial sensors, and terrain-reference methods to ensure reliable navigation performance when satellite signals are unavailable. Operators in coastal terrain have employed line-of-sight workarounds using shore-based transponders and managed corridors, but these are unsuitable for blue-water operations. This has driven efforts toward multi-sensor navigation, certified autonomy logic, and mission profiles with redundant positioning methods, ensuring operational reliability in high-risk maritime environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Subsurface Primacy Meets Surface Disruption

Unmanned Underwater Vehicles (UUVs) accounted for 62.24% of 2025 revenue, as customers prioritized stealth, endurance, and low-observable signatures for ISR and mine warfare in high‑risk zones. Within subsurface fleets, ROVs hold a larger installed base for manipulation and inspection tasks, while AUVs are scaling faster as route planning, classification, and autonomy improve for wide‑area survey. The market continues to anchor many of its premium programs on deep‑rated hulls with modular bays that support rapid payload swaps, which compresses upgrade timelines versus full platform replacement. On the surface, rising adoption is being driven by remote operations centers and regulatory green lights that support persistent, uncrewed inspection and patrol missions. USVs grow fastest at 13.99%, reinforced by wind‑farm inspection use cases, where uncrewed surface craft act as motherships for electric ROVs, enabling continuous operation through challenging weather. Platform makers that deliver plug‑and‑play payload suites gain flexibility to address both defense and commercial workflows without major hull redesigns.

Regulatory frameworks also differentiate the pathway to market for surface and subsurface systems. The International Maritime Organization is progressing the MASS Code, which provides the governance foundation for collision avoidance, remote operations qualifications, and cyber resilience for uncrewed surface vessels. Select national authorities have issued precedent‑setting permits for uncrewed offshore operations and are building licensing regimes for shore‑based masters, a move that signals durable operating models for commercial USVs. Subsurface platforms continue to follow classification rules that emphasize pressure safety, redundancy, and the validation of structured autonomy across specific mission profiles.[2]Source: DNV, “Autonomous and AI Certification Guidance,” DNV, dnv.com Growth on both vectors is strengthened by modular sensors and autonomy stacks that can migrate across platform types with limited integration overhead.

By Vehicle Size: Compact Swarms Versus Deep-Diving Leviathans

Small‑class vehicles captured 49.20% of the 2025 share and are set to deliver the fastest growth, 13.40% CAGR, as buyers favor hand‑deployable systems and multi‑asset control from shore. Training and expeditionary use cases benefit from vehicles that can be launched and recovered without the need for large ships, reducing charter costs and expanding deployment frequency. The unmanned sea systems market rewards these attributes with shorter budgeting cycles and mission-scheduling agility, thereby lifting utilization and total lifecycle value. Medium‑class formats balance payload and endurance with transport and deck‑handling practicalities, which make them well‑suited for survey firms and energy customers that rotate assets across projects. This class is the typical home for work-class ROVs and mid-depth AUVs that require robust navigation and power for longer missions. The most capital‑intensive large and extra‑large vehicles serve strategic, deep‑ocean, or long‑patrol missions where mission depth and duration justify higher unit costs.

Procurement preferences by mission profile influence which size bands scale fastest across defense and commercial fleets. Defense mine warfare teams and ISR operators lean toward small and medium classes for rapid deployment, distributed sensing, and high reusability across short cycles. Commercial O&M teams can justify both small units for turbine inspections and medium units for survey coverage, often in paired surface‑subsurface configurations. Unit economics favor small vehicles for high‑frequency tasks, while deep‑rated premium vehicles dominate applications such as seabed mapping and strategic undersea infrastructure monitoring. Across all sizes, software‑centric autonomy and swarm control are pushing more value into sensor fusion and command middleware that span fleets rather than single hulls.

By Propulsion: Electrification Accelerates as Diesel Retreats

Diesel and gas‑turbine systems retained a 43.27% share in 2025 for harsh‑environment reliability and sprint speed requirements, especially where temperature extremes challenge battery performance. The renewable (solar/wave) is projected to grow at a 14.89% CAGR through 2031. At the same time, growth tilts toward electric and hybrid architectures as operators opt for lower acoustic signatures, simpler maintenance, and alignment with zero‑emission mandates. The unmanned sea systems market size attributed to electric and hybrid options is also supported by modular powertrains, in which battery packs and fuel‑cell range extenders can be tailored to mission endurance and payload power requirements. Demonstrated hydrogen-fuel-cell AUV configurations achieve multi‑week autonomy within practical volume and weight envelopes, enabling longer missions without surfacing for recharge. Surface fleets in regulated corridors gain economic benefits from battery‑electric USVs as insurance pricing and permitting align with zero‑crew, zero‑emission deployments. Buyers operating near sensitive ecosystems also cite compliance with evolving underwater noise regulations as an added benefit of electric thrusters.

Technical trade-offs remain for burst performance, extreme cold, and high-power payloads, which preserve a role for hybrid and mechanical systems in select missions. Still, investment and policy signals support broader electrification through five to seven‑year planning windows. Remote operations centers keep utilization high for electric fleets by optimizing charging, maintenance, and mission scheduling across routes and seasons. The supply base is also moving toward standardized power and propulsion modules that reduce integration time when swapping between electric and hybrid configurations. As software‑defined power management improves, operators extract greater endurance from the same energy budget through smarter route planning, sensor duty cycling, and formation tactics that reduce aggregate drag. These collective trends reinforce the growth path for cleaner powertrains as operational familiarity and infrastructure mature.

By Application: Defense Supremacy Yields to Dual-Use Models

Military applications accounted for 52.59% of 2025 spend and are advancing at a 13.16% CAGR, supported by mine warfare, ISR, and distributed anti‑submarine tactics that favor the use of autonomous assets. Serial production programs and lab‑to‑fleet prototypes are now public across multiple primes, including newly unveiled multi‑mission AUVs designed for rapid payload swaps and submarine compatibility. Research findings also point to active adaptation in strategic undersea systems among peer competitors, which accelerates the shift to persistent, low‑signature surveillance and standoff effectors. Mine countermeasures funding highlights a sustained commitment to portable, modular systems that lower risk for crewed ships and can be deployed quickly in littoral bottlenecks. Training, test, and evaluation pipelines are normalizing swarm logic, mission handoffs, and human‑on‑the‑loop controls, which smooth the path to broader fleet use.

Commercial applications show faster adoption where autonomy translates into better uptime, lower emissions, and quicker payback periods. In Europe, field trials and deployments have validated surface‑subsurface pairings for 24/7 wind‑farm inspection with major reductions in fuel use and weather downtime. Japan’s public programs are building a bridge between demonstration and commercial use by seeding standards and export‑minded supply chains for ASV‑ROV linkages and future AUV integration. Environmental monitoring, hydrography, and infrastructure inspection are broadening the base for recurring service contracts, often with autonomous sampling, survey, and visual inspection at lower total ownership cost. The outcome is a market where both military and commercial buyers are strengthening demand for modular platforms and sensor suites that can pivot between roles with minimal refit.

By Component Type: Sensors Eclipse Hulls as Value Drivers

Propulsion and power systems accounted for 32.60% of revenue in 2025, reflecting the capital intensity of core drive and energy subsystems. Yet the fastest growth now lies in sensor suites growing at 14.10% CAGR, which are benefiting from AI‑enabled processing, synthetic aperture techniques, and miniaturization, enabling small vehicles to perform tasks once confined to larger platforms. The unmanned sea systems market has seen leading vendors demonstrate compact multibeam sonars and integrated navigation packages that reduce system weight and power consumption while increasing data quality and swath width. This capability mix raises the utility of commodity hulls and concentrates margin in payloads and autonomy rather than the platform chassis. Communications and navigation stacks are also evolving with higher‑throughput acoustic modems and hybrid architectures that store high‑resolution data on the vehicle and relay compressed summaries during missions. Advances in onboard processing further support real‑time decision-making and obstacle avoidance within the vehicle’s energy budget.

Classification frameworks and AI management standards continue to formalize documentation, testing, and risk management for autonomy software. This raises entry barriers and gives incumbents with compliance experience and internal toolchains mapped to notifier requirements an advantage. The unmanned sea systems market, driven by sensors and autonomy, is aided by shorter refresh cycles that enable frequent capability upgrades without platform changes. This model encourages navies and commercial operators to treat payloads as the primary lever for performance improvement when deploying platforms over longer lifespans. The result is a procurement and operations pattern that invests in smarter sensors, cleaner propulsion, and software roadmaps to expand mission reach.

Geography Analysis

North America accounted for 38.36% of 2025 revenue and is projected to register the fastest regional CAGR of 14.09% through 2031, supported by ongoing procurement and active prototype programs across mine warfare and ISR. New multi‑mission AUV introductions and test milestones underscore a maturing pipeline that blends submarine‑compatible vehicles and surface autonomy within larger fleet concepts. The unmanned sea systems market in the region also reflects serial deliveries of mine countermeasures that leverage lessons from contested theaters to deliver modular systems ready for rapid deployment. The US and Canadian suppliers reinforce leadership with vertically integrated payloads and autonomy stacks linked to established defense frameworks. Commercial activity is growing from offshore wind and environmental monitoring contracts, with approvals and infrastructure emerging to support uncrewed operations at scale.

Europe shows synchronized defense and commercial adoption, especially in the North Sea, Baltic, and Atlantic corridors. Scandinavian countries continue to pioneer uncrewed permitting, remote operations, and zero‑emission mandates that align with autonomous, battery‑electric deployments, which, in turn, catalyze commercial inspection and logistics use cases. European defense programs include large undersea vehicles and swarm projects that target seabed mapping, mine hunting, and infrastructure protection at depth. Commercial operators continue to validate 24/7 inspection workflows for wind assets using USVs paired with ROVs, with fuel and emissions benefits relative to crewed survey ships. This region’s policy environment and project density create durable demand for both platforms and sensors suited to high latitudes and variable sea states.

Asia‑Pacific demand is driven by defense modernization, offshore wind build‑out, and maritime domain awareness needs along complex coastlines. Regional research output highlights advancing capabilities in extra‑large UUVs across endurance, depth, and navigation resilience, pointing to a competitive technology race that drives aggregate procurement. South Korea and Singapore continue to integrate autonomy into maritime security and commercial operations through domestic programs and partnerships. At the same time, Australia’s ecosystem ties procurement to persistent Indo‑Pacific monitoring and deterrence. Across the region, swifter adoption is likely where national rules align with MASS‑style governance and where energy and port authorities enable zero‑crew operations in controlled corridors.

Competitive Landscape

The unmanned sea systems market features a set of leaders with vertically integrated portfolios and long‑cycle defense relationships, combined with specialist suppliers that compete through modular payloads and autonomy. Kongsberg Gruppen ASA is focused on maritime autonomy, AUV production, and integrated systems, and its recent strategic actions emphasize dedicated execution on these vectors. Teledyne continues to expand through acquisitions and product introductions that target compact, integrated navigation and sonar solutions for smaller vehicles, a shift that broadens the addressable base for micro‑AUVs and micro‑USVs. Saab AB advances under national defense contracts and joint programs that align with NATO interoperability and seabed defense priorities. L3Harris Technologies, Inc. expands multi‑domain autonomy with a portfolio spanning command software, USV platforms, and AUVs, enabling bundled offerings for navies and commercial fleets.

Strategic moves over the past two years have focused on consolidation, vertical integration, and dual‑use positioning. Lockheed Martin Corporation invested in a leading USV supplier and subsequently unveiled a multi‑mission AUV designed for rapid reconfiguration, linking sensing to strike options within a single platform family. BAE Systems plc entered a 10‑year exclusive agreement with Cellula Robotics to commercialize an extra‑large AUV, signaling stronger alignment between primes and innovation partners on modular, long‑endurance vehicles.[3]BAE Systems, “Herne XLAUV,” BAE Systems, baesystems.com These actions indicate a race to package hulls, autonomy, and sensors into turnkey solutions that can be procured and sustained under tighter budgets and accelerated timelines.

Open architectures, payload modularity, and certification pathways are the levers that shape competitive positioning. Vendors that demonstrate compliance with evolving autonomy and cybersecurity requirements facilitate procurement and shorten time-to-deployment for their customers. Companies that demonstrate compact, power‑efficient sensor fusion stacks on small vehicles unlock new missions that were historically impractical at lower weights and energy budgets. In parallel, remote operations centers and national permitting regimes are creating new operating models in which vendors partner with service providers to deliver inspection and survey outcomes rather than asset sales, which widens the field for recurring revenue models in the market.

Unmanned Sea Systems Industry Leaders

Kongsberg Gruppen ASA

L3Harris Technologies, Inc.

BAE Systems plc

Teledyne Technologies Incorporated

General Dynamics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Huntington Ingalls Industries Inc. was awarded a contract by the US Defense Innovation Unit (DIU) for its Torpedo Tube Launch and Recovery (TTLR) system, which facilitates the launch and recovery of REMUS unmanned underwater vehicles from a submarine's torpedo tubes. The DIU aims to hasten the US Department of War's integration of technologies pivotal for deterrence and victory in warfare.

- September 2025: Saab AB secured a contract with the Royal Australian Navy to deliver an extra AUV62-AT, an autonomous training target designed for ASW.

- July 2025: Exail Technologies SA received a contract to deliver five DriX H-8 USVs to an unnamed European nation. The agreement marks a significant advancement in deploying the standard DriX model for ISR operations. The DriX H-8 USV, initially developed for hydrographic missions, operates as a medium-range vessel suitable for shallow and deep-water environments.

- January 2025: Kongsberg Maritime delivered the first USV for Offshore Operations. The company completed the delivery of REACH REMOTE 1, a 24 m USV developed through collaboration between Kongsberg Maritime, REACH SUBSEA ASA, Massterly, and Trosvik Maritime. The ship represents an advancement in offshore operations technology.

Global Unmanned Sea Systems Market Report Scope

The unmanned sea systems market includes autonomous underwater vehicles, remotely operated vehicles, semi-submersibles, and unmanned surface craft. The defense sector, alongside commercial sectors, is increasingly adopting technologies to map and monitor ocean conditions and to explore various oil and gas sites.

The unmanned sea systems market is segmented based on platform type, vehicle size, propulsion, application, component type, and geography. By platform type, the market is segmented into unmanned underwater vehicles (UUVs) and unmanned surface vehicles (USVs). By vehicle size, the market is divided into small, medium, and large. By propulsion, the market is segmented into electric, hybrid, diesel and gas-turbine, and renewable (solar/wave). By application, the market is segmented into military and commercial. By component type, the market is segmented into hull, autonomy suite, communications and navigation, sensors suite, propulsion and power systems, and others (payload, launch/recovery systems). The report also covers the market sizes and forecasts for the unmanned sea systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Unmanned Underwater Vehicles (UUVs) | Remotely Operated Vehicles (ROVs) |

| Autonomous Underwater Vehicles (AUVs) | |

| Unmanned Surface Vehicles (USVs) | Remotely Operated Surface Vehicles (ROSVs) |

| Autonomous Surface Vehicles (ASVs) |

| Small |

| Medium |

| Large |

| Electric |

| Hybrid |

| Diesel and Gas-Turbine |

| Renewable (Solar/Wave) |

| Military | Intelligence, Surveillance, and Reconnaissance (ISR) |

| Mine Counter-Measures (MCM) | |

| Anti-Submarine Warfare (ASW) | |

| Logistics and Resupply | |

| Commercial | Environment Monitoring |

| Infrastructure Inspection | |

| Hydrographic Survey | |

| Others |

| Hull |

| Autonomy Suite |

| Communications and Navigation |

| Sensors Suite |

| Propulsion and Power Systems |

| Others (Payload, Launch/Recovery systems) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform Type | Unmanned Underwater Vehicles (UUVs) | Remotely Operated Vehicles (ROVs) | |

| Autonomous Underwater Vehicles (AUVs) | |||

| Unmanned Surface Vehicles (USVs) | Remotely Operated Surface Vehicles (ROSVs) | ||

| Autonomous Surface Vehicles (ASVs) | |||

| By Vehicle Size | Small | ||

| Medium | |||

| Large | |||

| By Propulsion | Electric | ||

| Hybrid | |||

| Diesel and Gas-Turbine | |||

| Renewable (Solar/Wave) | |||

| By Application | Military | Intelligence, Surveillance, and Reconnaissance (ISR) | |

| Mine Counter-Measures (MCM) | |||

| Anti-Submarine Warfare (ASW) | |||

| Logistics and Resupply | |||

| Commercial | Environment Monitoring | ||

| Infrastructure Inspection | |||

| Hydrographic Survey | |||

| Others | |||

| By Component Type | Hull | ||

| Autonomy Suite | |||

| Communications and Navigation | |||

| Sensors Suite | |||

| Propulsion and Power Systems | |||

| Others (Payload, Launch/Recovery systems) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the Unmanned Sea Systems market size and growth outlook through 2031?

The unmanned sea systems market size is projected to rise from USD 2.99 billion in 2025 to USD 5.51 billion by 2031 at a 12.94% CAGR, supported by defense modernization and remote offshore inspection demand.

Which platform type leads revenue in the Unmanned Sea Systems market?

Unmanned Underwater Vehicles (UUVs) lead with 62.24% of 2025 revenue, while Unmanned Surface Vehicles (USVs) are the fastest growing on the back of wind‑farm inspection and uncrewed operations approvals.

Which regions will grow the fastest in the Unmanned Sea Systems market?

North America combines the largest 2025 revenue share with the fastest projected regional CAGR at 14.09%, helped by active defense programs and permitting for uncrewed operations in commercial use cases.

What is the propulsion trend across new programs and commercial deployments?

Electrification and hybrid architectures are gaining share due to zero‑emission mandates, simpler maintenance, and lower acoustic signatures, while diesel and gas‑turbine remain in niche missions that require sprint speeds or extreme endurance.

Which components are driving the most value in current procurements?

Sensor suites and autonomy stacks are growing the fastest as AI‑enabled sonar, compact navigation, and onboard processing turn commodity hulls into differentiated platforms with shorter upgrade cycles.

What are the key risks that could slow adoption of unmanned sea systems?

Export controls can elongate international sales cycles and GNSS denial degrades autonomous navigation, which raises the need for multi‑sensor fusion and certified autonomy logic for contested waters.

Page last updated on: