Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 12.87 Billion |

| Market Size (2031) | USD 16.08 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Yogurt Market Analysis by Mordor Intelligence

The United States yogurt market size is estimated to be valued at USD 12.87 billion in 2026 and is projected to reach USD 16.08 billion by 2031, advancing at a 4.55% CAGR during the forecast period. Growth is supported by consumers shifting breakfast and snacking habits toward higher-protein formats, an accelerating pivot into plant-based alternatives, and distribution gains for shelf-stable drinkable products. Price-tier segmentation is also widening, with premium Greek, Icelandic, and oat-based SKUs co-existing alongside value multipacks. Leading companies are expanding portfolios through vertical integration, aseptic processing, and proprietary probiotic strains, while regional dairies protect share by emphasizing local sourcing. Regulatory pressure around added sugar disclosures and volatile milk input costs continues to rationalize low-margin flavored lines, yet the strongest brands leverage reformulation agility to maintain shelf space.

Key Report Takeaways

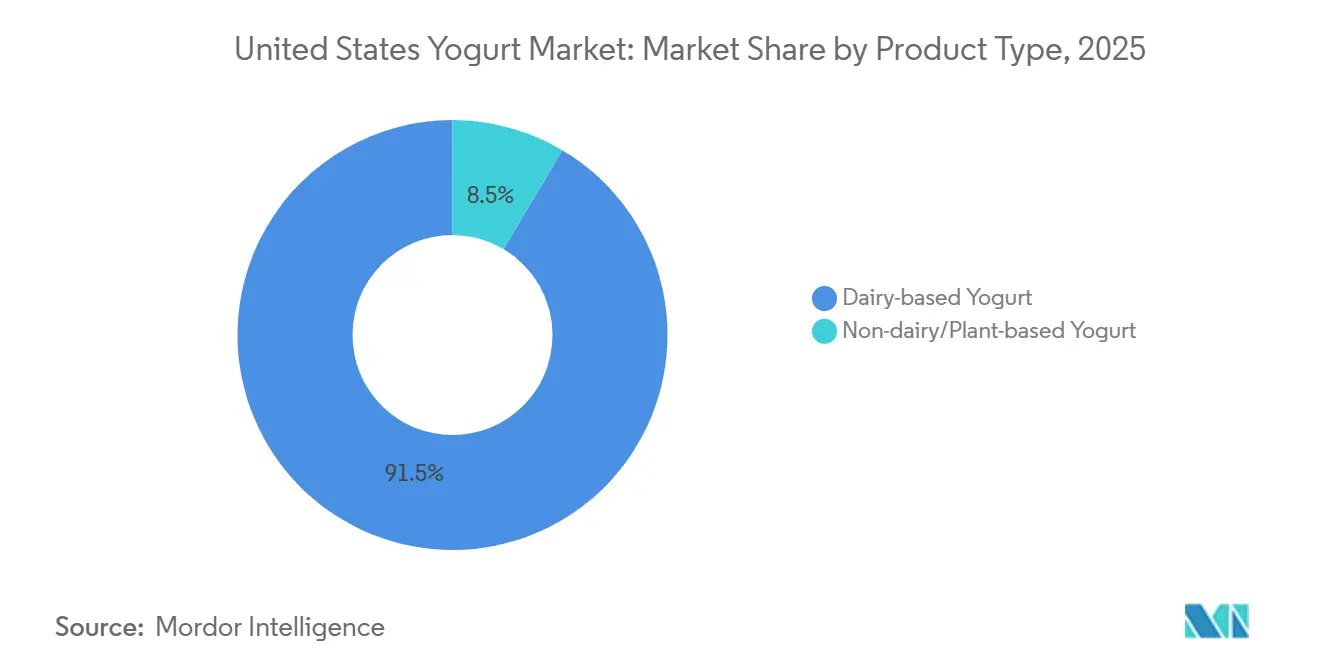

- By product type, dairy-based yogurt accounted for 91.47% of the United States yogurt market share in 2025, whereas non-dairy alternatives are expected to expand at a 6.63% CAGR through 2031.

- By product form, spoonable yogurt retained 80.72% revenue share in 2025, while drinkable formats are forecast to grow at a 5.56% CAGR through 2031.

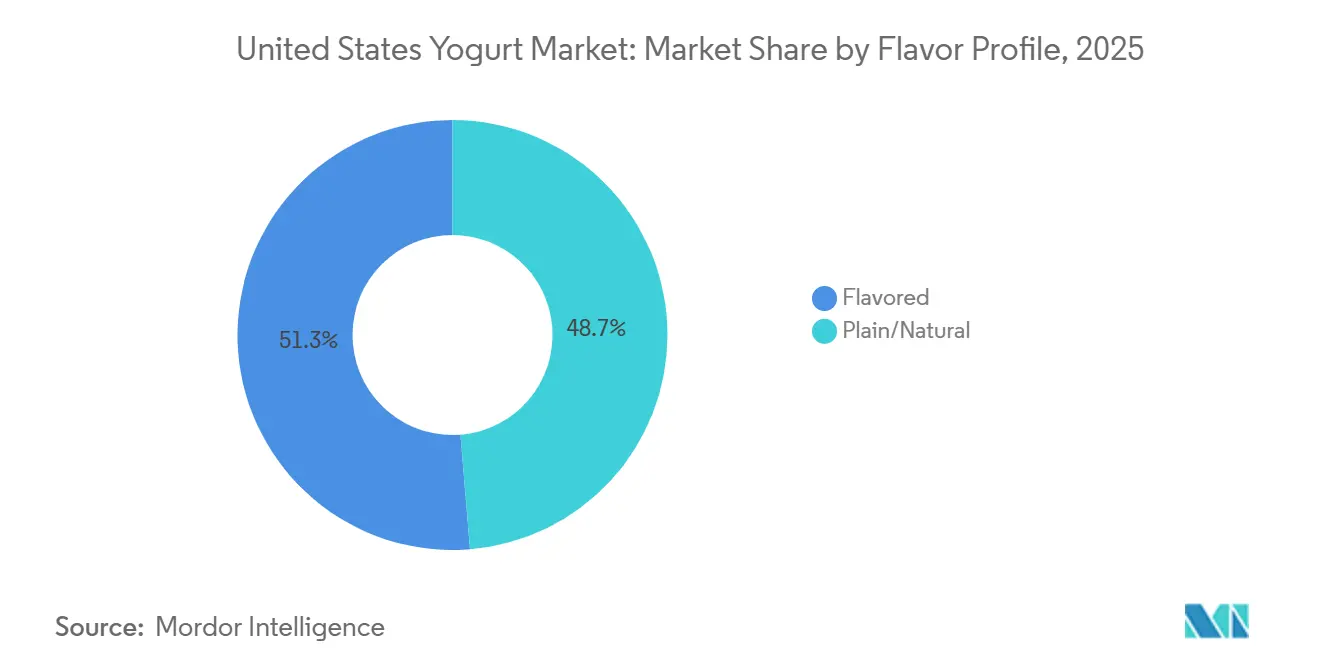

- By flavor profile, flavored varieties led with 51.29% share in 2025; plain and natural yogurt is advancing at a 4.81% CAGR through 2031.

- By packaging type, cups, containers, and tubs held a 65.13% share in 2025; tetra packs and pouches exhibit the fastest growth at a 6.48% CAGR through 2031.

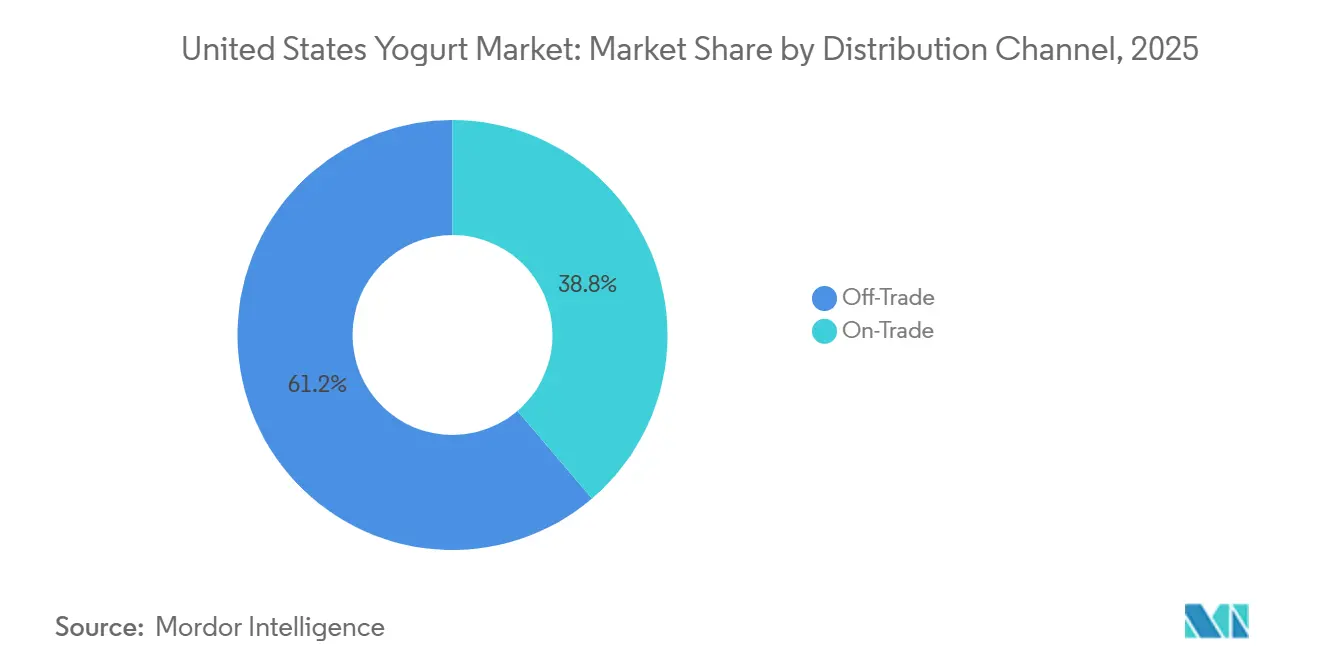

- By distribution channel, off-trade accounted for 61.24% of 2025 sales, but on-trade outlets are anticipated to post a 6.46% CAGR through 2031.

- By geography, the South captured 31.38% of nationwide volume in 2025, while the Northeast is the fastest-growing region at a 4.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Yogurt Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing market demand for high-protein Greek yogurt among millennials | +1.0% | National, with concentration in Northeast and West Coast urban centers (New York, Boston, San Francisco, Los Angeles) | Medium term (2-4 years) |

| Leveraging local fruit-based flavor innovations to drive yogurt sales | +0.6% | Regional focus in West (California, Oregon, Washington) and Northeast (New York, Vermont, Massachusetts), with spillover to Midwest berry-growing states | Medium term (2-4 years) |

| On-the-go breakfast trends supporting growth in drinkable yogurt products | +0.9% | National, strongest in metropolitan areas with average commute times exceeding 30 minutes; concentrated in Northeast corridor and West Coast | Short term (≤ 2 years) |

| Increased consumer interest in lactose-free and digestive health claims driving non-dairy yogurt alternatives | +1.4% | West Coast leadership (California 14% non-dairy share), expanding to Northeast urban markets and progressive Midwest cities | Long term (≥ 4 years) |

| Focus on clean-label and locally sourced ingredients to meet sustainability goals | +0.7% | National, with premium positioning in Northeast and West Coast; strongest in organic-certified retail channels | Long term (≥ 4 years) |

| Probiotic and immunity-focused fortification leading new product development | +0.8% | National, with premium positioning in Northeast and California; accelerated by post-pandemic health consciousness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing market demand for high-protein Greek yogurt among millennials

Millennials are a significant driver of growth for high-protein Greek yogurt, combining strong health and protein-seeking behaviors with a preference for convenient, flavorful, and ethically positioned products. Brands are actively innovating and tailoring their messaging to appeal to this demographic. According to the United States Census Bureau and related demographic estimates, Millennials were the largest generational group in the United States in 2024, accounting for approximately 21.81% of the population [1]Source: United States Census Bureau, "Population and Housing Unit Estimates", census.gov . This demographic influence positions Millennials as a primary target for Greek yogurt, which is increasingly marketed as an everyday high-protein snack rather than a niche fitness product. The rising adoption of high-protein diets and interest in satiety and muscle recovery have shifted consumer preferences toward products with higher protein content. Greek yogurt, with its naturally higher protein density compared to regular yogurt, aligns well with these wellness priorities. Brands like Chobani have normalized Greek yogurt as a mainstream, lower-sugar, high-protein option in breakfast and snacking routines, reinforcing its perception as a functional and convenient nutritional choice. To maintain engagement, brands focus on flavor innovation and textural variety, as seen in Danone’s Oikos line, which has refreshed recipes, textures, and packaging to enhance its appeal. Digital-first, omnichannel marketing strategies, such as Oikos’ campaigns across social media, influencer partnerships, and online video platforms, effectively reach Millennials, strengthening the association between Greek yogurt and aspirational, lifestyle-driven branding. Sustainability and quality cues, such as non-GMO ingredients and "cleaner" ingredient narratives, further resonate with Millennials' values-based consumption patterns, positioning Greek yogurt as a premium yet accessible choice and a key driver of growth in the United States yogurt market.

Leveraging local fruit-based flavor innovations to drive yogurt sales

Local fruit-based flavor innovations are a significant driver of yogurt sales, aligning health-focused attributes with taste-driven, regionally relevant experiences that encourage both trial and repeat purchases. Incorporating locally familiar and seasonal fruits enables brands to differentiate in a competitive chilled aisle. Traditional flavors such as strawberry, blueberry, and peach remain central to the segment while creating opportunities for localized or creative variations that cater to regional tastes. As taste is a critical factor for health-conscious consumers, developing fruit-forward recipes using recognizable United States fruit crops positions yogurt as a permissible indulgence, combining nutrition with authentic fruit flavors. For example, Chobani has expanded its offerings with fruit-centric and dessert-inspired flavors like strawberry, peach, mocha tiramisu, and apple pie a la mode variants, demonstrating how American fruit cues can be integrated into Greek and traditional yogurt formats to maintain category dynamism. This focus on local fruits also supports premiumization, as recipes featuring "real fruit" and carefully crafted pairings justify higher price points while signaling quality and freshness to consumers. Similarly, Noosa emphasizes fruit-rich profiles such as raspberry and strawberry-rhubarb, combining thick whole-milk yogurt with generous fruit preparations to reinforce an artisanal, farm-style positioning that appeals to consumers seeking both comfort and novelty in familiar fruit flavors. By introducing limited-time or regionally inspired fruit flavors, brands create urgency and discovery, encouraging consumers to explore different options within a portfolio rather than remaining loyal to a single SKU. These innovations enhance consumer engagement, strengthen brand identity, and drive volume and value growth by aligning yogurt consumption with everyday American fruit preferences and evolving flavor trends.

Increased consumer interest in lactose-free and digestive health claims driving non-dairy yogurt alternatives

Consumer interest in lactose-free and digestive health claims is driving the growth of non-dairy yogurt alternatives, as these products address lactose intolerance challenges and cater to the increasing focus on gut health through plant-based, probiotic-rich formulations. With digestive sensitivities on the rise, highlighted by the Centers for Disease Control and Prevention (CDC) estimates that 2.4 to 3.1 million Americans will be living with inflammatory bowel disease (Crohn’s disease and ulcerative colitis) in 2024, there is a growing need for accessible options that support gut health without dairy-related discomfort [2]Source: Centers for Disease Control and Prevention (CDC), "IBD Facts and Stats", cdc.gov . Lactose-free positioning eliminates a key barrier for consumers who value yogurt’s probiotic benefits but experience issues with traditional dairy, while non-dairy bases such as cashew, coconut, and almond provide the creamy texture and live cultures essential for digestive health. Forager Project exemplifies this trend with its organic, dairy-free cashew-coconut yogurts fermented with six strains of live active probiotics, including L. Plantarum and Bifidus, specifically designed to promote gut health. Prebiotic and probiotic fortifications further enhance the appeal, as consumers increasingly associate these attributes with improved gut microbiome balance, immunity, and regular digestion. Silk’s almond milk dairy-free yogurt alternative also supports this trend by offering a smooth, lactose-free option that integrates seamlessly into health-focused routines, appealing to those prioritizing allergen avoidance and digestive comfort. Clean label and plant-based attributes, including vegan, gluten-free, and additive-free claims, strengthen consumer trust, enabling non-dairy yogurts to compete directly with traditional dairy products. The convergence of rising digestive health concerns, lactose intolerance needs, and demand for bioavailable probiotics positions non-dairy yogurt alternatives as a high-growth segment, expanding access to gut health solutions for a broader consumer base.

Focus on clean-label and locally sourced ingredients to meet sustainability goals

Clean-label and locally sourced ingredients are increasingly aligning with sustainability objectives by promoting transparency and reducing environmental impact. This approach leverages minimal, recognizable components and shorter supply chains to appeal to label-conscious consumers. According to the National Science Foundation, in 2024, 83% of American consumers read food labels before making purchase decisions, with 64% paying more attention to labels compared to five years ago. Among these consumers, 79% prioritize the ingredients list, 78% look for health claims, and 77% check the allergen warnings [3]Source: National Science Foundation (NSF), "NSF Research Shows Americans Demand Greater Clarity and Standardization in Food Labeling", nsf.org . This growing scrutiny positions clean-label yogurts with simple, locally sourced ingredients as a trusted choice over additive-heavy alternatives. Locally sourced milk, fruits, and cultures reduce carbon emissions associated with transportation while signaling freshness and ethical farming practices, creating a narrative of environmental responsibility that resonates with eco-conscious shoppers. Siggi’s exemplifies this approach with its low-fat Skyr yogurts, made using real fruit, simple ingredients, no preservatives or artificial sweeteners, and milk sourced from regional United States farms, emphasizing clean composition alongside lower-impact sourcing. Local sourcing also enhances clean-label appeal by enabling "made nearby" narratives, reducing packaging needs, supporting community agriculture, and positioning yogurt as a sustainable, everyday product. These ingredients further improve allergen transparency and provide non-GMO assurances, linking label readability with broader wellness and environmental goals, which drives interest among families and premium buyers. Stonyfield Organic reinforces this trend by using USDA organic, grass-fed milk from United States family farms without unnecessary additives, connecting clean-label simplicity with regenerative farming practices that improve soil health and biodiversity. The synergy of heightened label attention, clean formulations, and local sourcing positions yogurt brands as sustainability leaders, fostering growth through consumer-aligned values.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| United States milk price volatility exerting margin pressure on dairy yogurt producers | -0.7% | National, most acute in Midwest and Northeast dairy-producing regions (Wisconsin, Minnesota, New York, Pennsylvania); affects regional dairies disproportionately | Short term (≤ 2 years) |

| Rising input costs for SMEs driven by import tariffs on probiotic cultures | -0.4% | National impact on small and medium enterprises lacking domestic fermentation capacity; concentrated among brands sourcing cultures from Europe and Asia | Medium term (2-4 years) |

| Elevated cold-chain logistics expenses constraining e-commerce profitability | -0.3% | National, with highest impact in rural and low-density markets; affects direct-to-consumer brands and online-exclusive SKUs disproportionately | Short term (≤ 2 years) |

| FDA added-sugar labeling regulations restricting formulation options for flavored yogurt SKUs | -0.5% | National enforcement; compliance costs concentrated among smaller manufacturers with limited research and development budgets; institutional channel (schools, hospitals) most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

United States milk price volatility exerting margin pressure on dairy yogurt producers

Milk price volatility has created significant challenges for dairy yogurt producers, disrupting pricing strategies and profitability. Between 2024 and 2025, milk prices paid to farmers fluctuated between USD 18.50 and USD 24.20 per hundredweight, a 31% variation driven by feed-cost inflation, drought in the Southwest, and export demand volatility, according to the USDA National Agricultural Statistics Service. These fluctuations directly impact producers, who face difficulties in passing on cost increases without risking consumer resistance or losing market share to plant-based competitors. Feed-cost inflation further compounds the issue by increasing overall production expenses, forcing manufacturers to either absorb losses or reformulate products with more expensive alternatives, which strains relationships with cooperatives and suppliers already managing herd-related challenges under volatile conditions. Companies like Chobani, heavily reliant on domestic dairy sourcing, encounter amplified difficulties as milk price swings erode the cost advantages of scale, prompting tighter inventory controls and hedging strategies that fail to fully offset financial pressures during peak drought periods. Drought conditions in the Southwest further restrict regional milk supplies, intensifying competition for high-quality fluid milk and raising logistics costs for cross-country transportation. Export demand volatility adds complexity, as milk is diverted to international markets during high-price periods, leaving domestic processors to contend with shortages or elevated spot market prices, undermining long-term margin stability. Smaller producers, lacking the bargaining power to secure fixed-price contracts, are particularly vulnerable, limiting their ability to invest in innovation within a category already under pressure from non-dairy alternatives. These interconnected factors constrain producers’ agility, limit growth potential, and drive a shift toward more resilient product formulations.

Rising input costs for SMEs driven by import tariffs on probiotic cultures

Import tariffs on probiotic cultures have significantly increased input costs for small and medium-sized enterprises (SMEs), creating substantial challenges in the yogurt industry. These tariffs disproportionately impact smaller producers, who lack the scale to absorb or negotiate the higher costs of essential live culture imports. The increased tariffs raise the price of specialized probiotic strains, often sourced from Europe or Asia, leading to higher formulation expenses. SMEs are frequently compelled to either increase retail prices, risking shelf-space loss to larger competitors, or compromise product quality by opting for cheaper domestic alternatives with lower efficacy. This cost pressure is compounded by supply chain vulnerabilities, as smaller producers rely on consistent culture availability to ensure fermentation consistency. Tariff-induced delays or shortages disrupt production schedules and batch reliability, further straining operations. For instance, Maple Hill Creamery, a smaller producer specializing in 100% grass-fed organic dairy yogurt, faces rising probiotic sourcing costs that erode its premium clean-label margins, forcing tighter cost controls amid competition from larger, tariff-resilient players. Without the ability to leverage bulk purchasing or hedging strategies, SMEs struggle to maintain the probiotic potency claims that differentiate their products in a health-conscious market, widening the competitive gap with larger brands benefiting from favorable import terms. Tariff volatility also discourages innovation in functional probiotic blends, as SMEs hesitate to invest in research and development for advanced strains due to unpredictable costs, slowing advancements in the category. These challenges, combined with margin pressures from other inputs like milk, push smaller producers toward consolidation or niche strategies, while larger players strengthen their dominance through diversified supply networks that mitigate tariff impacts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Dominance Masks Plant-Based Velocity

Dairy-based yogurt maintains a dominant position in the yogurt market and accounted for 91.47% of the market share in 2025. This dominance is attributed to established consumer preferences, a mature cold-chain infrastructure, and cost advantages over non-dairy alternatives. In 2025, dairy yogurt was expected to average USD 0.85 per pound, significantly lower than the USD 2.10 per pound for plant-based options. These cost efficiencies enable dairy brands to adopt competitive pricing strategies and sustain high household penetration. Additionally, milk’s natural compatibility with probiotic fermentation supports the growth of cultures like Lactobacillus without extensive fortification, reinforcing its digestive health benefits at a lower production cost. Greek yogurt leads the dairy segment, offering a thick, strained texture and high protein content that aligns with consumer preferences for satiety and fitness-oriented diets. Icelandic skyr further enhances the premium dairy segment, with brands like Siggi’s and Icelandic Provisions emphasizing higher protein density and lower sugar content, appealing to health-conscious consumers. Together, these subcategories, regular, Greek, and skyr, create a competitive hierarchy within the dairy segment.

Non-dairy yogurt, while representing a smaller share, is expanding rapidly with a projected CAGR of 6.63% through 2031. Growth is driven by oat, almond, and coconut-based formulations targeting lactose-intolerant consumers, vegans, and flexitarian shoppers. Plant-based matrices require fortification with Lactobacillus strains and stabilizers to achieve comparable texture and colony-forming unit (CFU) levels, contributing to higher production costs. However, advancements in oat and almond processing are narrowing the cost gap, enabling more competitive pricing. Brands such as Silk and Forager Project exemplify this growth, offering plant-based yogurts with added live cultures to replicate dairy’s probiotic benefits while addressing allergen and ethical concerns. Although non-dairy yogurt has not displaced dairy’s dominance, it is reshaping shelf space allocation as retailers dedicate more facings to plant-based lines to meet rising demand. The market reflects a stable dairy foundation alongside the rapid growth of non-dairy alternatives, positioning both segments to coexist and compete for health-conscious and sustainability-focused consumers.

By Product Form: Drinkable Formats Capture Convenience Premium

Spoonable yogurt accounted for 80.72% of the yogurt market share in 2025, supported by its role in established breakfast and snack routines. Its adaptable texture makes it suitable for mixing with toppings or consuming on its own. Single-serve cups, typically sized between 5.3 and 6 ounces, dominate this category due to their portion control and convenience, appealing to consumers with busy lifestyles who prefer mess-free options. Multi-serve tubs, ranging from 24 to 32 ounces, cater to households that incorporate yogurt into cooking or daily meals, offering bulk value for meal preparation and versatile use. However, family-size containers exceeding 48 ounces are declining in popularity, reflecting the trend of smaller household sizes and the rise of single-person homes, which favor smaller formats to minimize waste and align with reduced consumption needs. Brands such as Chobani maintain their leadership in this segment by offering single-serve Greek yogurt cups that emphasize protein-rich convenience, while larger tubs support home-based consumption with clean-label attributes. This segmentation ensures a balanced portfolio that sustains market stability despite competition from alternative formats.

Drinkable yogurt formats are projected to grow at a 5.56% CAGR through 2031, driven by their portability and suitability for on-the-go consumption. Single-serve bottles, typically sized between 8 and 12 ounces, are designed to fit into vehicle cup holders and remain stable for 2-3 hours without refrigeration after opening, making them ideal for commuters and gym-goers. Although packaging costs for bottles (12-15 cents per unit) are higher compared to cups (6-8 cents per unit), brands offset these costs through 20-30% price premiums. This allows drinkable yogurt to be marketed as a functional beverage, emphasizing added nutritional benefits such as probiotics, and competing with smoothies and protein shakes. Danone’s Oikos drinkable line exemplifies this trend by offering high-protein shakes in portable bottles, targeting active consumers and blending the familiarity of yogurt with the convenience of a shake. Drinkable yogurt formats are gradually capturing market share by addressing unmet convenience needs, fostering a dual-format ecosystem where both spoonable and drinkable options coexist to expand overall yogurt consumption occasions.

By Flavor Profile: Plain Gains as Culinary Use Expands

Flavored yogurt accounted for 51.29% of the market share in 2025, driven by enduring consumer preferences for flavors such as strawberry, blueberry, and vanilla. These options appeal to everyday snacking habits with their familiar and indulgent taste profiles. Blended formats dominate this segment due to their convenience and consistent flavor distribution, eliminating the need for stirring and aligning with fast-paced lifestyles. However, fruit-on-the-bottom varieties have experienced a decline in popularity following the FDA's January 2025 added-sugar labeling rules, which reclassified fruit compote sugars as "added," highlighting higher sugar content that deters health-conscious consumers. Mix-in formats, while offering customization and interactive appeal, remain smaller in scale compared to blended options. Brands like Noosa exemplify success in this category with their thick, fruit-rich blended yogurts, such as raspberry and strawberry-rhubarb, which combine real fruit layers with the convenience that consumers prioritize. Despite its leadership, the flavored yogurt segment faces increasing scrutiny over sugar content.

Plain and natural yogurt is projected to grow at a compound annual growth rate (CAGR) of 4.81% through 2031, driven by its versatility in culinary applications such as marinades, sauces, and baking. It also offers customization opportunities when paired with fresh fruit or granola, catering to consumers seeking tailored nutrition. The shift toward clean-label products has further accelerated plain yogurt's growth, particularly following the FDA's January 2025 labeling rules, which revealed that a 6-ounce flavored yogurt cup often contains 12-18 grams of added sugar. This transparency has prompted many consumers to switch to unsweetened options. Plain yogurt’s neutral profile enhances its versatility in cooking and supports at-home personalization, avoiding the added sweetness flagged on labels. Siggi’s has capitalized on this trend with its high-protein skyr in natural form, appealing to consumers prioritizing lower-sugar, clean-ingredient options. This growth trajectory is gradually reshaping market dynamics, shifting focus toward functional, unsweetened products that empower consumers to make informed dietary choices.

By Packaging Type: Shelf-Stable Formats Unlock New Channels

Cups, containers, and tubs accounted for 65.13% of the packaging share in 2025, driven by their established role in household storage and spoonable consumption. These formats benefit from mature filling lines and strong consumer familiarity, making them a reliable choice for daily breakfast and snack routines. Single-serve cups provide portioned convenience, while larger tubs cater to family meal preparation and ingredient use, ensuring versatility and retail stability. Bottles, primarily used for drinkable yogurt, maintain a notable share through 8-12 ounce single-serve PET designs that offer resealability and portability for on-the-go consumption. Sustainability efforts are also shaping the market, with Chobani committing to 100% recyclable cups and Stonyfield transitioning to plant-based Polylactic Acid (PLA) cups, which reduce carbon footprints while maintaining the structural integrity required for chilled dairy transport. However, multi-material designs, such as foil lids on plastic cups, continue to hinder recycling efforts, with yogurt packaging recycling rates remaining low in 2025 despite technical recyclability.

Tetra packs and pouches are gaining traction, with a projected CAGR of 6.48% through 2031, supported by shelf-stable innovations that expand distribution beyond cold-chain limitations. Tetra Pak's aseptic processing technology enables yogurt to remain unrefrigerated for 6-9 months, reducing logistics costs and facilitating broader distribution in e-commerce, dollar stores, and gas stations. Pouches are particularly popular in the children's snack segment, with products like Go-Gurt and Stonyfield YoKids offering squeezable, spoon-free formats that prioritize convenience for parents and mess-free fun for children. Tetra packs also achieve higher recycling rates, up to 70% in municipalities equipped for paperboard recycling, outpacing multi-material cups. By combining portability with extended shelf life, these formats allow brands to explore new consumption occasions without cannibalizing core refrigerated sales, driving market growth, and aligning with sustainability trends.

By Distribution Channel: On-Trade Recovery Accelerates

Off-trade channels accounted for 61.24% of yogurt sales in 2025, with supermarkets and hypermarkets leading due to high purchase frequency. On average, households purchase yogurt 18 times annually, supported by promotional efforts, where 38% of volume is sold on deals. These factors enable a wide product assortment and strategic endcap displays, positioning yogurt as a staple item. Convenience stores complement this by capturing impulse and on-the-go purchases, with drinkable yogurt formats driving sales among commuters seeking quick protein options. Online retail contributes to volume growth through subscription models like Thrive Market and Amazon Subscribe and Save, favoring multi-packs of 12-24 units to address cold-chain shipping challenges. Shelf-stable tetra packs also capture a share of e-commerce demand. Specialty stores and direct-to-consumer channels hold a smaller market share, but premium brands such as Arethusa Farm and La Fermière command higher price points, ranging from USD 3-4 per cup, through local delivery and artisanal appeal.

On-trade channels are anticipated to grow at a CAGR of 6.46% through 2031, driven by increased yogurt integration in hotels, cafés, and quick-service restaurants. Hotels have resumed breakfast services featuring yogurt stations with customizable toppings, while cafés offer layered parfaits that combine convenience with perceived freshness. Quick-service restaurants, such as Panera, include yogurt in health-focused menus, catering to consumers seeking portable, nutritious alternatives to carbohydrate-heavy options. Brands like Oikos support this growth by providing portioned, high-protein yogurt cups for grab-and-go consumption, aligning with retail protein trends. This expansion broadens yogurt consumption occasions beyond home use, balancing off-trade saturation and enhancing the overall market footprint.

Geography Analysis

The South region accounted for 31.38% of the yogurt market share in 2025, driven by a well-established dairy infrastructure in states such as Texas, Georgia, and North Carolina. Cooperatives like Dairy Farmers of America operate large-scale processing plants in the region, supplying major retailers including Walmart and Kroger. These facilities ensure a consistent supply of family-size formats and flavored yogurt varieties, which align with the region's strong breakfast and snack traditions. The focus remains on value-oriented multipacks rather than premium single-serve options. However, the region's heat and humidity increase cold-chain logistics costs by 8-12% compared to northern areas, impacting margins and slowing the adoption of temperature-sensitive probiotic-enhanced yogurts that require precise refrigeration. This logistical challenge reinforces the popularity of durable, flavored yogurt staples that withstand distribution demands while maintaining consumer loyalty. Brands like Fage utilize Southern production facilities to efficiently distribute Greek yogurt, which aligns with regional snacking preferences without the challenges associated with probiotics.

The West region, led by California, is recognized for its leadership in plant-based yogurt, driven by an early adoption of alternative proteins and a sustainability-focused consumer base favoring oat and almond-based products. The region's ethnic diversity fosters flavor innovation, with options like mango, coconut, and matcha gaining popularity in states such as California and Washington. These flavors expand beyond traditional fruit profiles, catering to multicultural tastes. However, rural cold-chain gaps and high labor costs challenge local dairies, prompting a reliance on scalable plant-based innovations that mitigate milk price volatility. This combination of cultural diversity and cost pressures accelerates the growth of non-dairy yogurt, linking consumer preferences to resilient supply chains. Forager Project exemplifies this trend with its cashew-coconut yogurts tailored to West Coast tastes, reflecting the region's momentum in plant-based products and flavor experimentation.

The Midwest sustains steady growth, supported by its strong dairy heritage in states like Wisconsin, Minnesota, and Michigan. Cooperatives such as Tillamook and regional brands like Anderson Erickson achieve high household penetration through trusted, locally rooted production. This foundation supports consistent demand for spoonable and family-size yogurt formats, which align with the region's traditional routines. The focus remains on whole-milk and low-fat staples rather than trend-driven innovations. The scale of cooperatives enables competitive pricing and widespread distribution, fostering consumer loyalty in a region less influenced by coastal trends like plant-based alternatives. Heritage branding, combined with everyday practicality, sustains volume without relying on fleeting fads. Tillamook exemplifies this approach with its creamery-fresh yogurts that emphasize Midwest milk quality, appealing to families who prioritize authenticity over novelty.

Competitive Landscape

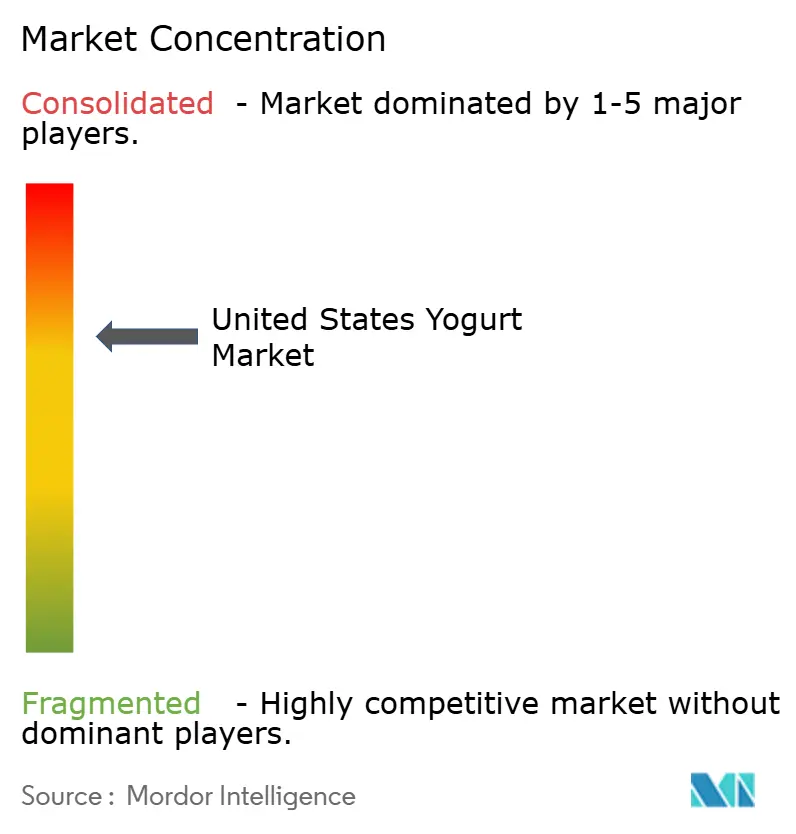

The yogurt market in the United States demonstrates moderate consolidation, with the top five companies, Danone, Chobani, Lactalis, FAGE, and Dairy Farmers of America, accounting for a major share of the market. This structure enables major players to leverage scale efficiencies and broad distribution networks to shape category trends. At the same time, smaller entities focus on niche segments with tailored offerings to avoid direct price competition. Danone employs a multi-brand strategy, including mass-market Dannon, premium Greek Oikos, and digestive health-focused Activia, to address diverse consumer needs while optimizing shared manufacturing infrastructure. Chobani capitalizes on vertical integration at its New York and Idaho facilities, achieving cost advantages and accelerating product launches, such as limited-edition flavors introduced within 90 days. Smaller brands like Siggi's differentiate themselves by targeting sugar-conscious consumers with products containing just 4-9 grams of total sugar per serving, contributing to a dynamic market environment.

Regional dairies and plant-based entrants sustain competitiveness by targeting niche markets and prioritizing premium pricing over high-volume strategies. Forager Project, for instance, caters to organic-certified plant-based consumers with cashew-coconut blends, addressing vegan and lactose-free demand without competing in mass-market channels. Similarly, La Fermière appeals to luxury-oriented consumers with French-style ceramic packaging and whole-milk indulgence, commanding a price of USD 3.50 per cup. These disruptors complement category growth by expanding plant-based and high-end indulgence segments, while avoiding direct competition with larger players. Siggi's sharpens its focus on low-sugar skyr, aligning with clean-label trends and drawing market share from traditional flavored yogurt lines, ensuring that specialization coexists with the dominance of top-tier players.

Technological advancements are a key differentiator among competitors. Leading companies utilize ultra-filtration to enhance protein concentration without heat damage, preserving nutritional integrity in dairy and blended formats. Aseptic processing facilitates shelf-stable tetra packs, reducing cold-chain dependency and expanding distribution opportunities for products like Danone's Activia drinks. Fermentation-control systems ensure consistent probiotic CFU counts, supporting health claims that justify premium pricing amid rising interest in digestive wellness. These technologies work synergistically; ultra-filtration improves spoonable yogurt, aseptic processing enhances drinkable formats, and fermentation controls stabilize probiotics, creating a robust foundation for competitive advantage. Chobani integrates these systems to maintain consistent Greek yogurt thickness and accelerate flavor innovation, reinforcing its market position. Investments in technology solidify the competitive hierarchy, driving efficiency and credibility in a market where formulation precision is essential.

United States Yogurt Industry Leaders

-

Chobani LLC

-

Danone S.A

-

Lactalis Groupe

-

FAGE International S.A.

-

Dairy Farmers of America Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Little Spoon, Inc. expanded its product portfolio with the introduction of the YoGos yogurt line. These snacks were made with whole milk Greek yogurt, providing 4 grams of protein, along with fruit, vegetables, and probiotics. The yogurt snacks were available in four flavors with no added sugar: Strawberry Bananza, Apple Berry Blast, Peachy Pearadise, and Tropical Mango Twist. They were packaged in pouches featuring resealable caps for convenience.

- October 2024: Chobani introduced a Greek yogurt line with a focus on high protein content. The yogurt cups provided 20 grams of protein, while the drink options included 15 grams, 20 grams, and 30 grams of protein per serving. The Greek yogurt cups were offered in flavors such as vanilla, strawberry kiwi, mango, raspberry lemon, and cherry berry, packaged in 6.7-oz cups priced at USD 1.99 each. The 15-gram protein drinks were available in strawberries and cream and tropical punch flavors, packaged in 7-oz bottles for USD 1.99 each.

- October 2024: Chobani launched Chobani Creations Greek Yogurt, a new range of dessert-inspired snacks. Each 5.3-ounce single-serving container contained fewer than 200 calories, 10 grams of protein, 9 essential amino acids, and billions of probiotics. The initial flavors included mocha tiramisu, apple pie a la mode, cherry cheesecake, orange cream pop, banana foster, and caramel sundae.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the United States yogurt market covers all spoonable, drinkable, frozen, and plant-based yogurts sold in retail and food-service channels, valued at the invoice price to first-level distributors. Fermented milk drinks whose primary cultures are S. thermophilus and L. bulgaricus anchor the definition, while new dairy-free recipes are mapped under the same taxonomy.

Scope Exclusions: products where yogurt is less than 50% of the final formulation (e.g., parfaits, dips) are left out.

Segmentation Overview

-

By Product Type

- Dairy-based Yogurt

- Non-dairy/Plant-based Yogurt

-

By Product Form

- Spoonable/Set Yogurt

- Drinkable Yogurt

-

By Flavor Profile

- Plain/Natural

- Flavored

-

By Packaging Type

- Cups, Containers and Tubs

- Bottles

- Tetra Packs and Pouches

- Others

-

By Distribution Channel

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

- On-Trade

-

Off-Trade

-

By Geography

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Our team conducts semi-structured interviews with dairy processors, packaging converters, retail buyers, and nutritionists across the South, Midwest, West, and Northeast to validate consumption seasons, average selling prices, plant-based penetration, and private-label momentum. Short online surveys with urban shoppers further gauge flavor switching and willingness to pay.

Desk Research

We start with structured pulls from public datasets such as USDA Dairy Products, U.S. Census trade codes, and the National Health & Nutrition Examination Survey, followed by trade association briefs from IDFA, American Dairy Science Association, and Mintel GNPD for launch counts. Company 10-Ks, investor decks, Nielsen open summaries, and reputable newspapers help us capture pricing corridors, channel shifts, and competitive moves.

Mordor analysts then enrich these facts with license-based resources like D&B Hoovers for brand revenues, Dow Jones Factiva for M&A traces, and Questel for live patent themes around plant proteins and fermentation strains. This list is illustrative; many additional records are mined, cross-compared, and archived for traceability.

Market-Sizing & Forecasting

A top-down supply and demand reconstruction converts USDA raw milk output into yogurt-grade solids, deducts export flows, and multiplies by verified yield factors. Results are stress tested through selective bottom-up rolls of processor volumes and sampled ASP × unit checks. Key variables like milk class I prices, per capita yogurt intake, retail shelf inflation, probiotic launch counts, and plant-based share drive our multivariate regression and ARIMA blend that projects 2025-2030 values. Gaps in individual processor data are bridged with weighted channel averages agreed upon during expert calls.

Data Validation & Update Cycle

Every dataset passes a three-layer review: automated variance scans, analyst peer checks, and a senior sign-off. Reports refresh annually, while interim updates are triggered when milk price swings exceed 7% or when a top-three brand alters portfolio scope.

Why Mordor's US Yogurt Baseline Commands Confidence

Public estimates often diverge because firms pick different product baskets, pricing points, and refresh cadences. Our disciplined scope setting and dual-path modeling deliver a balanced reference that clients can reproduce with public inputs.

Key gap drivers include whether non-dairy drinks are folded in, how probiotic beverages are grouped, and if food-service cups are blended with retail scans. Currency year alignment and inflation treatment also widen spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.30 B (2025) | Mordor Intelligence | - |

| USD 8.59 B (2024) | Regional Consultancy A | Omits yogurt drinks and plant-based lines; heavy retail scan reliance |

| USD 9.12 B (2023) | Global Consultancy B | Combines probiotic beverages with yogurt; uniform ASP assumption |

| USD 31.59 B (2024) | Industry Analysis C | Adds cultured desserts and in-store food service; broader channel mix |

Taken together, the comparison shows that Mordor's scoped-in product list, channel normalization, and annual refresh cadence yield a dependable midpoint for strategic planning, avoiding both conservative undercounts and inflated aggregates.

Key Questions Answered in the Report

How large is the United States yogurt market in 2026?

The United States yogurt market size stands at USD 12.87 billion in 2026 and is projected to reach USD 16.08 billion by 2031.

Which segment is growing fastest within U.S. yogurt?

Non-dairy yogurt leads growth, registering a 6.63% CAGR through 2031, driven primarily by oat-based and almond-based launches.

What drives the popularity of drinkable yogurt in the United States?

Rising on-the-go breakfast occasions and convenience-store placement underpin the 5.56% CAGR forecast for drinkable formats.

Which U.S. region purchases the most yogurt?

The South holds the largest volume share at 31.38%, though the Northeast is currently the fastest-expanding region.

Page last updated on: