Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.61 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

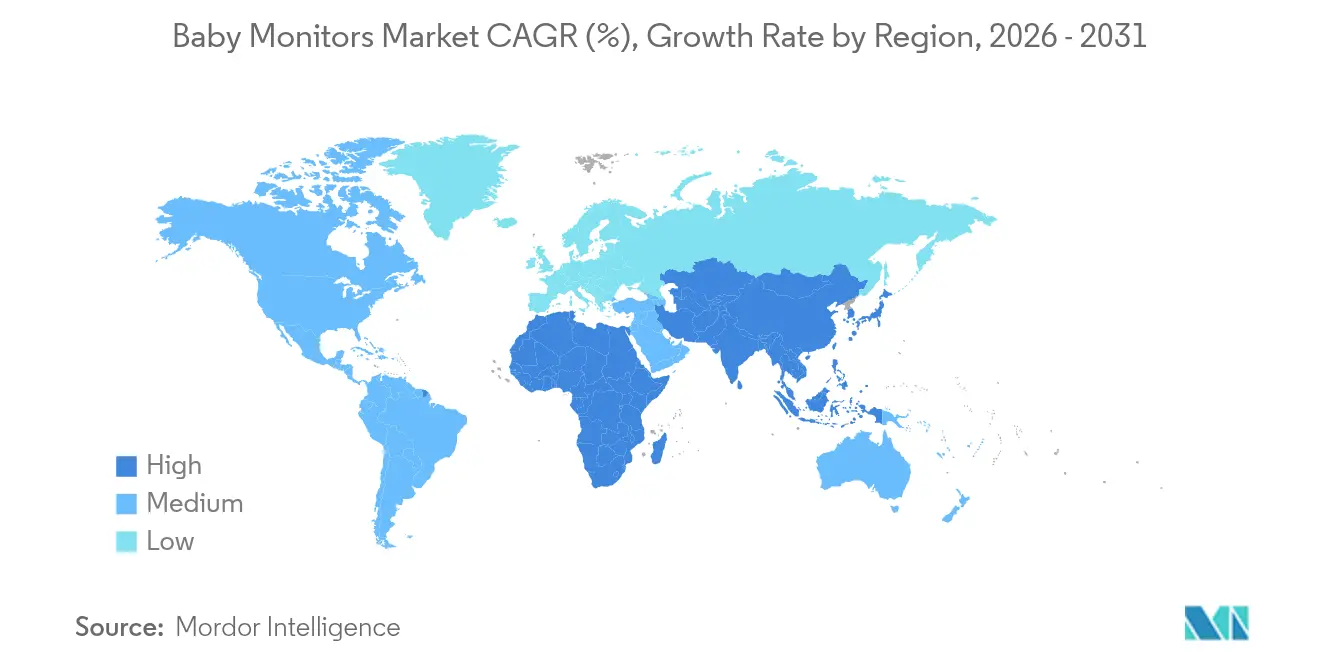

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

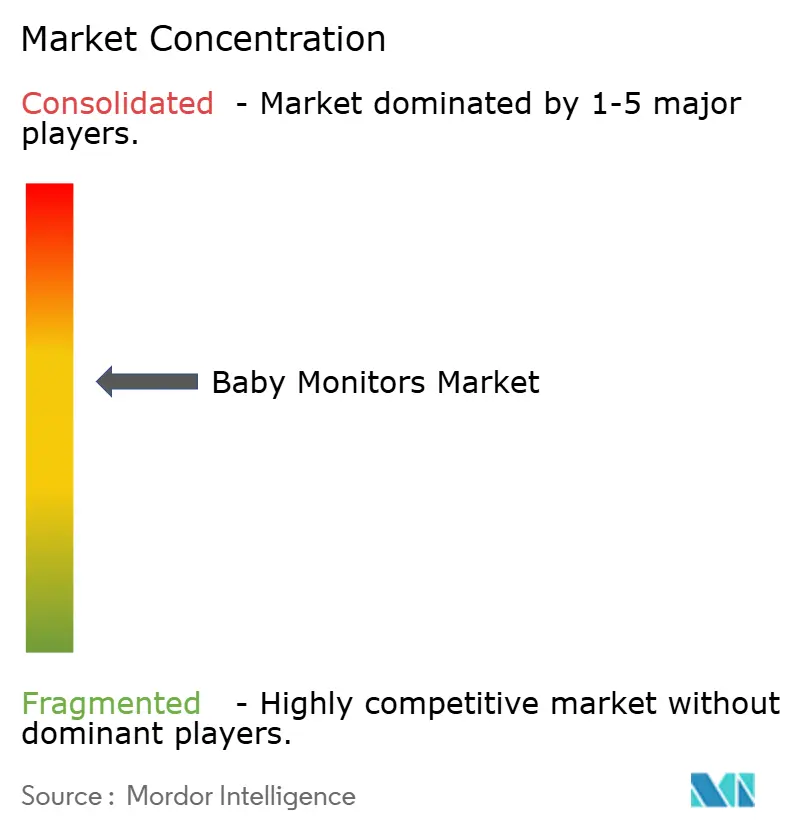

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Monitors Market Analysis by Mordor Intelligence

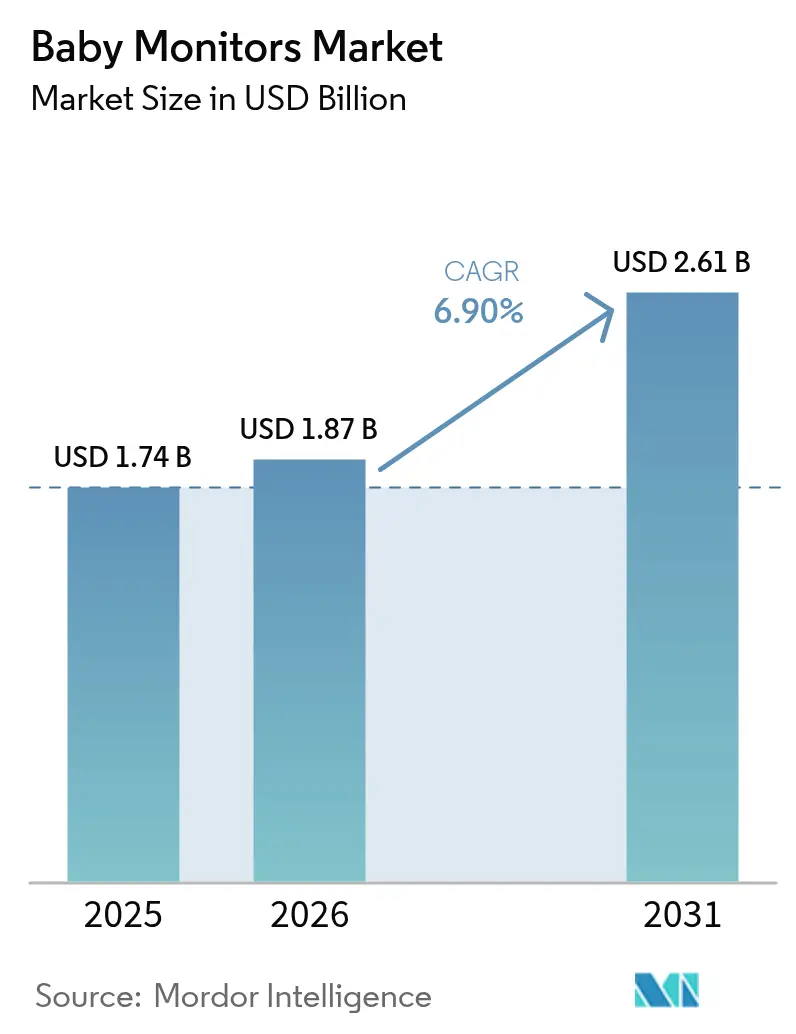

The baby monitors market size is expected to grow from USD 1.74 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.61 billion by 2031 at a 6.9% CAGR over 2026-2031. In the near term, dual-income households and hybrid work patterns are sustaining demand for connected nursery devices that let parents supervise infants without leaving the home office. Motion-sensor models that track breathing and sleep position are taking share from traditional video units as caregivers look for clinical-grade insights rather than simple visual reassurance. Wireless and Wi-Fi-enabled designs dominate retail shelves because of their seamless smartphone pairing and cloud analytics that transform a basic monitor into a data-rich parenting tool. At the same time, regulators on both sides of the Atlantic have begun to treat insecure monitors as potential attack surfaces, making third-party cybersecurity certifications a new purchase criterion. Competitive intensity is rising as consumer-electronics giants, infant-care start-ups, and medical-device manufacturers converge on premium segments of the baby monitors market.

Key Report Takeaways

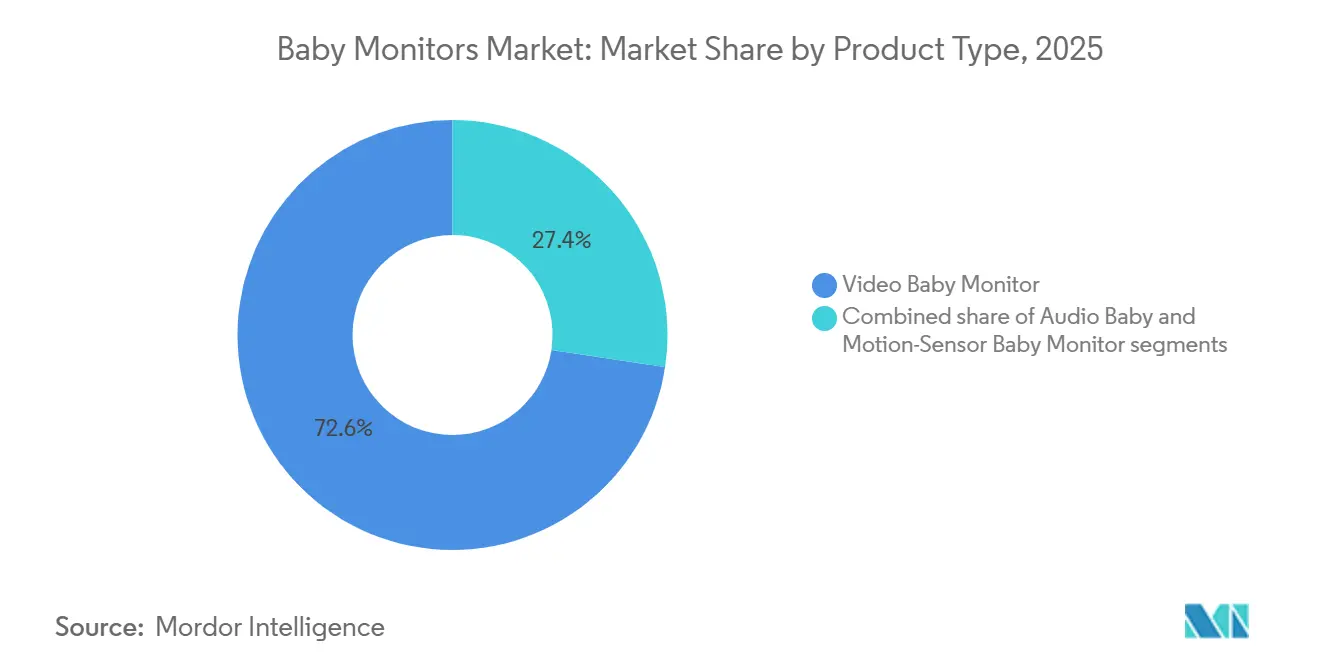

- By product type, video baby monitors led with 72.62% of baby monitors market share in 2025, while motion-sensor variants are advancing at a 7.5% CAGR to 2031.

- By mode of communication, wireless and Wi-Fi-enabled devices held 89.74% of the baby monitors market in 2025, and the same segment is forecast to expand at a 7.91% CAGR through 2031.

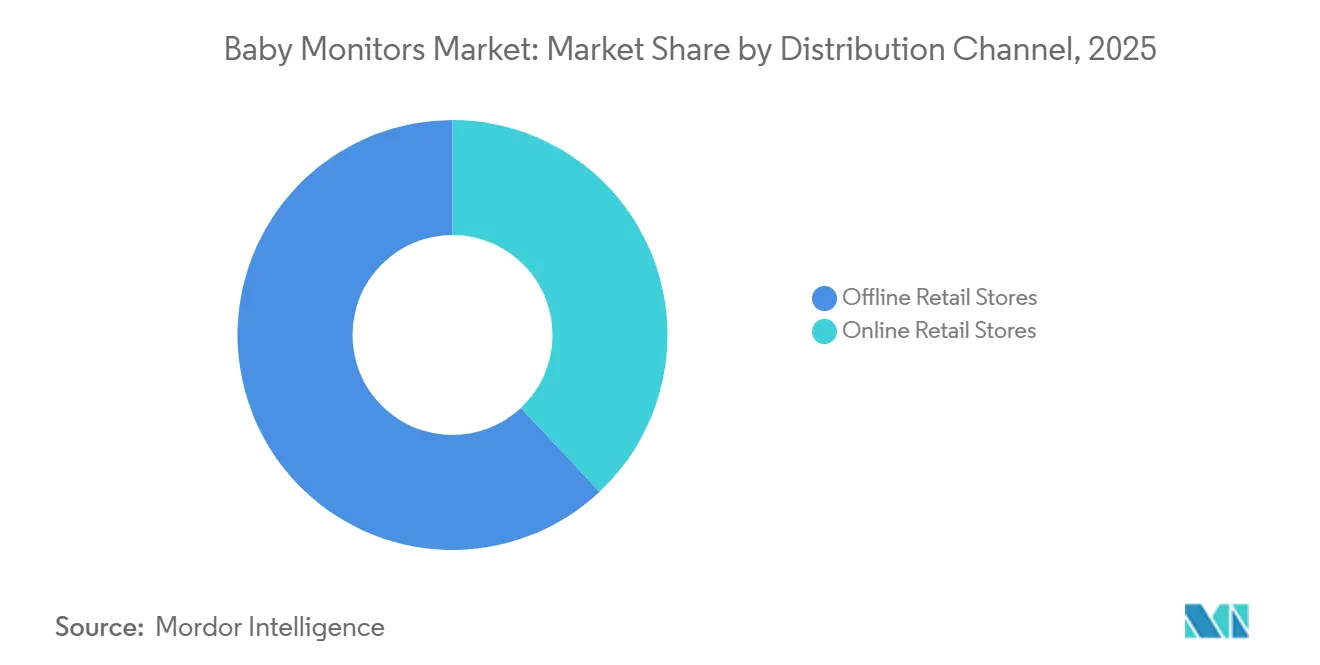

- By distribution channel, offline stores accounted for 62.62% of sales in 2025; online retail is projected to grow at a 7.12% CAGR to 2031.

- By region, North America captured 38.43% revenue share in 2025, whereas Asia-Pacific is on track to register the fastest 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baby Monitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of working parents requiring remote child supervision | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of smart home technology and smartphone integration | +1.5% | North America and Europe lead; the Asia-Pacific core is accelerating | Short term (≤ 2 years) |

| Swift uptake of wireless/IoT-enabled monitors | +1.3% | Global, with the strongest momentum in the Asia-Pacific and North America | Short term (≤ 2 years) |

| Pediatric tele-health finds its niche | +0.9% | North America and Europe, early pilots in urban Asia-Pacific | Medium term (2-4 years) |

| Increasing awareness and focus on infant safety and well-being | +0.8% | Global | Long term (≥ 4 years) |

| Select EU states offer insurance subsidies | +0.4% | Europe, concentrated in Germany, the Netherlands, and Belgium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising number of working parents requiring remote child supervision

Dual-income households now constitute the majority of families with infants in developed economies, creating structural demand for real-time nursery oversight that extends beyond traditional audio alerts. In the United Kingdom, 73% of mothers with children aged 0-4 years participated in the workforce in 2024, reflecting tighter labor markets and expanded parental leave policies that encourage earlier return to work, according to the UK Department for Education[1Source: UK Department for Education, “Economic Activity of Mothers with Young Children 2024,” education.gov.uk]. This demographic shift intersects with hybrid work models that keep parents physically proximate yet cognitively occupied, driving adoption of video monitors with smartphone alerts that minimize interruption costs. The Family Online Safety Institute reported in 2025 that 68% of parents allow children under 5 to use tablets, suggesting comfort with digital parenting tools that extend naturally to connected nursery devices. Vendors are responding by embedding scheduling features that sync with calendar apps, enabling automated monitoring intensity adjustments during conference calls or deep-work blocks, a capability that transforms monitors from passive sensors into active productivity enablers.

Growing adoption of smart home technology and smartphone integration

In 2024, US households increasingly embraced smart home security devices. Baby monitors, once standalone gadgets, are now pivotal in expansive home automation networks. Manufacturers are integrating these monitors with platforms like Amazon Alexa, Google Home, and Apple HomeKit. This allows parents to check on their nursery via voice commands and adjust lighting based on their baby's sleep patterns. Such integrations simplify the transition to smart homes, especially for parents who prioritize nursery safety. Philips, in October 2024, unveiled its Avent Premium Connected Baby Monitor. This device merges SenseIQ breathing tracking with Zoundream's cry-translation algorithms, alerting parents via smartphone notifications to their baby's needs, be it hunger, discomfort, or fatigue. Priced at INR 14,995 (USD 180), the monitor is positioned as a premium product, emphasizing its clinical utility over mere hardware features. This approach strikes a chord with millennial parents, who increasingly rely on data-driven insights in their parenting journey.

Swift uptake of wireless/IoT-enabled monitors

Wireless and Wi-Fi-enabled baby monitors captured 89.74% of the market in 2025 and are forecast to grow at a 7.91% CAGR through 2031, outpacing wired alternatives that now serve primarily as budget options or backup systems. The Federal Communications Commission launched its voluntary IoT Cybersecurity Label program in March 2024 (FCC 24-26), introducing the Cyber Trust Mark for wireless consumer devices that meet baseline security standards, including baby monitors. Owlet capitalized on this regulatory momentum by securing SGS Cybersecurity Mark certification for its Dream Sight monitor in September 2025, becoming the first baby monitor brand to achieve third-party security validation. The USD 99.99 device integrates with Owlet's FDA-cleared Dream Sock wearable, creating a closed-loop monitoring system that appeals to parents concerned about both functionality and data privacy. This certification-driven differentiation is likely to fragment the market into security-validated premium tiers and uncertified budget segments, with the former capturing a disproportionate share of revenue growth.

Pediatric tele-health finds its niche

Baby monitors are slowly integrating with telehealth platforms, marking a promising use case that's commanding premium prices and recurring subscription revenues. Masimo's Stork baby monitor, launched commercially in August 2023, boasts features like hospital-grade pulse oximetry and temperature tracking, firmly establishing it as a medical device rather than just another consumer gadget. Priced between USD 249-549, the device's cost reflects its clinical roots. Yet, its adoption faces hurdles: insurance reimbursement gaps and pediatricians' reluctance to trust parent-operated sensors for diagnostics. Nonetheless, the American Academy of Pediatrics' 2024 endorsement of remote monitoring for high-risk infants lends credibility to home-based vital sign tracking. This endorsement paves the way for medical-grade monitors to evolve from niche offerings to essential tools for premature infants and those with chronic respiratory issues. With this regulatory boost, baby monitors are poised to become the gateway for pediatric remote monitoring. McKinsey projects this market could balloon to USD 4 billion by 2030, contingent on evolving reimbursement models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over cybersecurity and privacy | -1.2% | Global, with heightened sensitivity in Europe and North America | Short term (≤ 2 years) |

| The high cost of advanced smart baby monitors is limiting affordability | -0.9% | The Asia-Pacific, South America, and Middle East and Africa; price-sensitive segments in developed markets | Medium term (2-4 years) |

| Limited awareness and adoption in developing regions | -0.6% | South America, the Middle East and Africa, and rural Asia-Pacific | Long term (≥ 4 years) |

| Technical issues such as connectivity problems and battery life concerns | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concerns over cyber-security and privacy

Cybersecurity breaches have shifted from mere theoretical concerns to real threats, particularly with baby monitors, undermining consumer trust and prompting regulatory scrutiny. In 2025, Bitdefender unveiled a severe flaw in the iBaby Monitor M6S, allowing hackers to hijack video feeds and access recordings without any authentication. This revelation led to a global firmware recall, impacting thousands of units. Such breaches have not gone unnoticed, leading to regulatory actions. The European Union's Cyber Resilience Act (Regulation 2024/2847) now categorizes baby monitors as Class I products[2]Source: European Parliament, “Regulation 2024/2847 Cyber Resilience Act,” europarl.europa.eu. Starting September 2026, these devices will be mandated to disclose vulnerabilities, commit to software updates, and undergo conformity assessments. However, the compliance costs associated with this regulation pose a significant challenge, especially for smaller manufacturers. This financial strain could push the market towards consolidation, favoring brands equipped with specialized security engineering teams. Highlighting the pervasive nature of these challenges, Australia's Office of the Australian Information Commissioner revealed that in 2024, 60% of data breaches were due to malicious attacks, with a staggering 68% of those linked to phishing or credential compromises[3]Source: OAIC, “Australian Data Breach Report 2024,” oaic.gov.au .

High cost of advanced smart baby monitors limiting affordability

Middle-income families in emerging markets and price-sensitive segments in developed economies find themselves priced out of premium baby monitors. These high-end devices, boasting AI-driven analytics, medical-grade sensors, and subscription-based cloud storage, come with hefty price tags. Take, for example, Philips' Avent Premium Connected Baby Monitor, priced at INR 14,995 (USD 180), and Masimo's Stork, which ranges from USD 249 to 549. While these monitors sit firmly in the premium tier, median household incomes in countries like India and Brazil treat them as discretionary luxuries rather than essential buys. The challenge is heightened by the lack of insurance subsidies in most regions. Only select European markets, such as Germany, the Netherlands, and Belgium, offer a silver lining, providing partial reimbursements for baby monitors. These are prescribed specifically for infants grappling with respiratory issues. The market's split between high-end AI-enabled devices and basic audio/video monitors poses a dilemma for manufacturers. They face a tug-of-war: while economies of scale in sensor production demand high volume, premium pricing limits that very volume. In a bid to navigate this landscape, brands are toying with tiered subscription models. These models aim to reduce the initial hardware costs but come with the caveat of ongoing fees for cloud storage and advanced analytics. However, the broader acceptance of such subscription-based tools in parenting remains an open question.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Motion Sensors Challenge Video Dominance

In 2025, video baby monitors led the market with a 72.62% share, driven by parents' preference for visual assurance of infant safety and declining HD camera module costs. Motion-sensor baby monitors, supported by clinical validation of contactless respiratory monitoring and integration with FDA-approved wearables, are projected to grow at a 7.50% CAGR through 2031, the fastest among product types. In 2025, Nanit secured patents for camera-based breathing-detection algorithms using computer vision to track chest movements, eliminating the need for wearable sensors. This innovation addresses a key issue in motion-sensor adoption: false alarms caused by blanket shifts or pet movements. By leveraging machine learning models trained on nursery footage, Nanit's technology distinguishes respiratory motion from environmental noise. Audio baby monitors, once dominant, now serve a shrinking niche of budget-conscious parents and grandparents seeking simple, smartphone-free solutions. Their market share has declined as the price gap for video monitors narrowed to under USD 30, reducing the appeal of audio-only devices.

The shift toward motion sensors reflects a move from passive monitoring to proactive diagnostics, as parents seek actionable insights to prevent health issues. In September 2025, Owlet launched "Dream Sight" at USD 99.99, integrating with its FDA-approved Dream Sock pulse oximeter to form a dual-sensor system. This system links video-based sleep position analysis with real-time oxygen saturation and heart rate data. The convergence of video and biometric monitoring blurs traditional product boundaries, with vendors bundling multiple sensor types into unified platforms that command premium pricing through clinical utility. The FDA's 2024 draft guidance, "General Wellness: Policy for Low Risk Devices," requires baby monitors with health claims to undergo premarket review, favoring established medical device manufacturers over consumer electronics startups.

By Mode of Communication: Wireless Dominance Masks DECT Resilience

In 2025, wireless and Wi-Fi-enabled baby monitors dominated the market, capturing 89.74% of the market share. These monitors are projected to grow at a 7.91% CAGR through 2031, driven by demand for smartphone integration and cloud-based remote access. The FCC's IoT Cybersecurity Label program (FCC 24-26), launched in March 2024, is differentiating the wireless segment as brands pursue Cyber Trust Mark certification. Owlet’s SGS Cybersecurity Mark certification for its Dream Sight monitor in September 2025 set a competitive precedent, as parents increasingly prioritize data privacy. This certification race is raising security standards, with manufacturers adopting encryption, two-factor authentication, and automatic firmware updates to meet regulatory expectations.

Wired baby monitors, with a 10.26% market share in 2025, remain relevant as backup systems and for privacy-conscious buyers avoiding cloud storage. A subset of wireless monitors using DECT (Digital Enhanced Cordless Telecommunications) technology occupies a niche by offering long-range transmission without Wi-Fi or the internet. These monitors appeal to rural parents with unreliable broadband and urban buyers concerned about Wi-Fi radiation or hacking risks. DECT monitors operate on dedicated frequency bands (1.9 GHz in North America, 1.88-1.9 GHz in Europe), minimizing Wi-Fi interference and providing encrypted transmission over 1,000 feet in open spaces. Brands like VTech and Philips offer DECT product lines at a premium, reflecting stable demand for privacy-focused, long-range solutions over cloud-based analytics.

By Distribution Channel: E-commerce Gains Despite Offline Majority

In 2025, offline retail stores dominated baby monitor sales, capturing 62.62% of the market. This trend was bolstered by parents' valuing in-store demonstrations and the trustworthiness of established baby specialty retailers. Online retail channels, however, are projected to grow at a 7.12% CAGR through 2031, driven by direct-to-consumer brands bypassing traditional retail markups. Amazon's dominance in baby products e-commerce has enabled smaller brands to reach national audiences without the capital requirements of retail distribution. Owlet's September 2025 launch of the Dream Sight monitor as a direct-to-consumer exclusive exemplifies this strategy, allowing the company to control pricing, customer data, and post-purchase engagement.

Asia-Pacific is witnessing a rapid e-commerce evolution due to mobile-first shopping habits and limited physical retail infrastructure in tier-2 and tier-3 cities. From 2024 to 2025, China's baby products e-commerce market grew at double-digit rates, driven by platforms like Tmall and JD.com offering same-day delivery in major metropolitan areas. Traditional retailers are adopting omnichannel strategies, with brands like Philips and VTech introducing "buy online, pick up in-store" options. This approach preserves retail relationships while catering to digital-first consumer preferences. Generational differences also influence the distribution channel split, as millennial and Gen-Z parents prefer online purchases, while older generations favor physical retail for its emphasis on packaging and brand presentation.

Geography Analysis

In 2025, North America holds a commanding 38.43% market share, buoyed by its high disposable incomes, swift adoption of technology, and a well-established childcare infrastructure that champions premium monitoring solutions. Cultural nuances play a pivotal role in the region's market dominance. Factors such as the prevalence of dual-income households, the geographic dispersion of extended families (which diminishes informal childcare support), and regulatory frameworks that incentivize safety technology adoption through insurance perks and tax benefits underscore this leadership. Both the Canadian and the United States markets exhibit parallel adoption trends. Urban locales gravitate towards smart monitors, while rural areas, hampered by internet connectivity issues and cost sensitivities, lean towards basic audio-video solutions.

Asia-Pacific is set to be the fastest-growing region, boasting a 7.52% CAGR through 2031. This surge is largely fueled by the burgeoning middle-class populations in China, India, and Southeast Asia. As these nations witness rising disposable incomes, there's a marked prioritization of infant safety technology. The region's growth narrative is shaped by demographic shifts: declining birth rates lead to heightened per-child investments, urbanization trends fragment extended families (diminishing informal childcare support), and advancements in technology infrastructure pave the way for sophisticated monitoring solutions. Notably, government actions, like Hong Kong's February 2025 update to children's product safety standards, not only bolster market expansion but also emphasize stringent product safety compliance .

Europe stands as a seasoned market, witnessing steady growth. This momentum is largely attributed to regulatory harmonization, stringent privacy protection standards, and insurance subsidy programs in select nations. These initiatives collectively lower the barriers to adopting premium monitoring solutions. However, the landscape is not without its challenges. The European Union's stringent cybersecurity regulations, highlighted by the Cyber Resilience Act set to take effect in December 2024, present a dual-edged sword. While they escalate compliance costs, they also hold the promise of bolstering consumer trust in connected monitoring devices. Meanwhile, regions like South America and the Middle East and Africa are on the cusp of growth. Urbanization, bolstered healthcare infrastructures, and a heightened awareness of infant safety technology drive this momentum. Yet, economic constraints and sparse distribution networks in rural locales temper the adoption rates.

Competitive Landscape

The baby monitors market demonstrates a moderately concentrated competitive landscape, with prominent consumer electronics companies such as Samsung, Panasonic, and Philips competing alongside specialized manufacturers like Owlet, Infant Optics, and Angelcare. This mix of established players and niche innovators creates a dynamic environment where scale and innovation coexist. Market leaders leverage their extensive distribution networks, global reach, and strong brand equity to maintain their competitive edge. These companies focus on delivering reliable and widely accessible products, ensuring their dominance in the market. Meanwhile, specialized players bring agility and innovation to the forefront, targeting specific consumer needs and preferences to carve out their market share effectively.

Specialized manufacturers differentiate themselves through cutting-edge technological advancements, particularly in areas such as artificial intelligence (AI) integration, advanced sensing technologies, and partnerships with healthcare providers. These innovations have transformed baby monitors from basic surveillance tools into comprehensive infant wellness platforms. For instance, AI-powered features enable predictive analytics and real-time alerts, while advanced sensors monitor vital signs like heart rate and oxygen levels. Collaborations with healthcare organizations further enhance the credibility and functionality of these products, appealing to health-conscious parents seeking more than just traditional monitoring solutions. This focus on innovation allows specialized players to address evolving consumer demands and establish a strong foothold in the market.

The competitive intensity in the market is further amplified by the growing demand for smart home integration. Companies are striving to ensure their products are compatible with leading platforms such as Amazon Alexa, Google Home, and Apple HomeKit. This compatibility allows baby monitors to seamlessly integrate into the broader ecosystem of connected households, catering to tech-savvy consumers who prioritize convenience and interoperability. As the adoption of smart home technologies continues to rise, the race to capture this segment has become a critical focus for both established players and emerging innovators in the baby monitors market. The ability to offer products that align with the smart home trend is increasingly becoming a key differentiator in this competitive landscape.

Baby Monitors Industry Leaders

Lenovo Group Limited

Panasonic Holdings Corporation

VTech Communications Inc.

Kids 2, Inc. (Summer Infant, Inc.)

Dorel Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Owlet launched the Dream Sight baby monitor at USD 99.99, becoming the first brand to achieve the SGS Cybersecurity Mark, which validates end-to-end encryption and secure firmware update protocols. The device integrates with Owlet's FDA-cleared Dream Sock wearable to provide correlated video and biometric monitoring, positioning it as a clinical-grade consumer product.

- October 2024: Philips, a global leader in health technology and innovation, launched the Philips Avent Connected Baby Monitor with a mobile app. This monitor introduces advanced features to enhance child safety and well-being. With high-definition video streaming, two-way communication, clear audio transmission, and motion detection, it provides parents a comprehensive view of their child's environment, even in low-light conditions.

- February 2024: Harbor, a US-based infant-care start-up, secured USD 3.7m in seed funding, gearing up to unveil its innovative baby monitor. This smart device boasts the ability to stream both with and without internet connectivity. Key features of Harbor's monitor include: local and remote streaming access, a high-quality 2k camera, robust data privacy assurances, split-screen functionality for monitoring up to four children, and an advanced Smart Audio alerting system.

- January 2024: Dorel Industries Inc.'s flagship baby gear brand, Maxi-Cosi, unveiled its latest innovation: the See Pro 360° Baby Monitor. This cutting-edge monitor is set to transform parental engagement, boasting the pioneering CryAssist™ technology. Harnessing the power of AI, CryAssist™ decodes a baby's cries, offering parents insights into their child's needs, whether they're sleepy, fussy, gassy, agitated, or hungry.

Global Baby Monitors Market Report Scope

An electronic device consists of a one-way radio or video transmitter and a portable receiver for remotely listening to or viewing an otherwise unaccompanied child. The baby monitors market is segmented by product type, mode of communication, distribution channel, and geography. Based on product type, the market is segmented into audio baby monitors, video baby monitors, and motion sensor baby monitors. Based on the mode of communication, the market is segmented into wired and wireless/Wi-Fi. Based on the distribution channel, the market is segmented into online retail stores, supermarkets/hypermarkets, specialty stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecast have been done based on value (USD million).

Product Type

| Audio Baby Monitors |

| Video Baby Monitors |

| Motion-Sensor Baby Monitors |

Mode of Communication

| Wired |

| Wireless/Wi-Fi |

Distribution Channel

| Offline Retail Stores |

| Online Retail Stores |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| Product Type | Audio Baby Monitors | |

| Video Baby Monitors | ||

| Motion-Sensor Baby Monitors | ||

| Mode of Communication | Wired | |

| Wireless/Wi-Fi | ||

| Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the baby monitors market be by 2031?

The baby monitors market is projected to reach USD 2.61 billion by 2031 based on a 6.9% CAGR from 2026-2031.

Which product segment is growing fastest?

Motion-sensor monitors will record the highest 7.5% CAGR through 2031 as parents seek contactless respiratory tracking.

Why are cybersecurity labels important for baby monitors?

Labels such as the FCC Cyber Trust Mark assure buyers that devices use encryption and receive timely patches, reducing hacking risks.

Which region offers the strongest future growth?

Asia-Pacific is expected to grow at a 7.52% CAGR as rising middle-class incomes and mobile-first shopping lift adoption.

Page last updated on: