United States Tahini Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

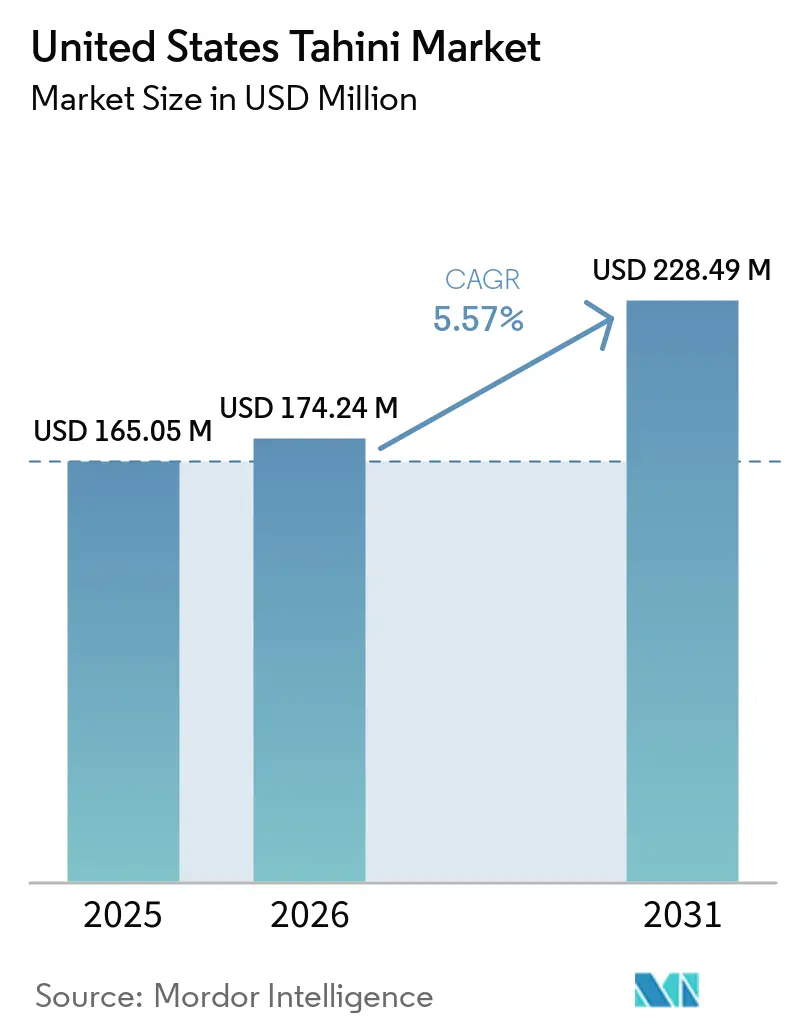

| Base Year Market Size (2025) | USD 165.05 Million |

| Market Size (2026) | USD 174.24 Million |

| Market Size (2031) | USD 228.49 Million |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

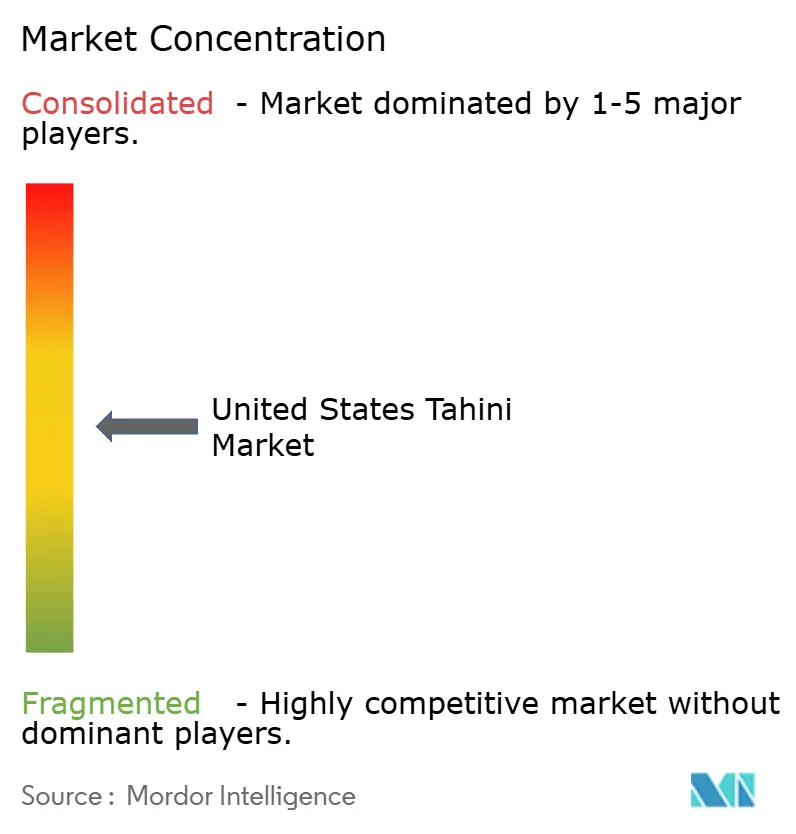

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Tahini Market Analysis by Mordor Intelligence

The United States tahini market size was valued at USD 165.1 million in 2025 and estimated to grow from USD 174.2 million in 2026 to reach USD 228.5 million by 2031, at a CAGR of 5.57% during the forecast period 2026-2031. The United States tahini market is evolving from its niche roots, now vying for prominence alongside peanut and almond butter on mainstream retail shelves. This transition is largely fueled by a surge in clean-label demand; tahini's appeal lies in its concise ingredient list and recognizable whole-food essence. Additionally, the rising popularity of plant-based proteins, nutrient-rich spreads, and Mediterranean cuisine suitable for both home cooking and foodservice bolsters tahini's market position. Innovations in packaging, expanded distribution through natural channels, and a robust online presence are making tahini more accessible, even to households that once found it challenging to incorporate. However, the landscape is not without challenges: sesame sourcing risks, allergen regulations, and potential recalls are steering competition towards suppliers adept at ensuring consistent quality and reliability[1]Source: Agricultural & Applied Economics Association, " Unintended Consequences of Allergen Food Labeling", choicesmagazine.org. As a result, companies that can effectively address these challenges are better positioned to capture market share and build consumer trust.

Key Report Takeaways

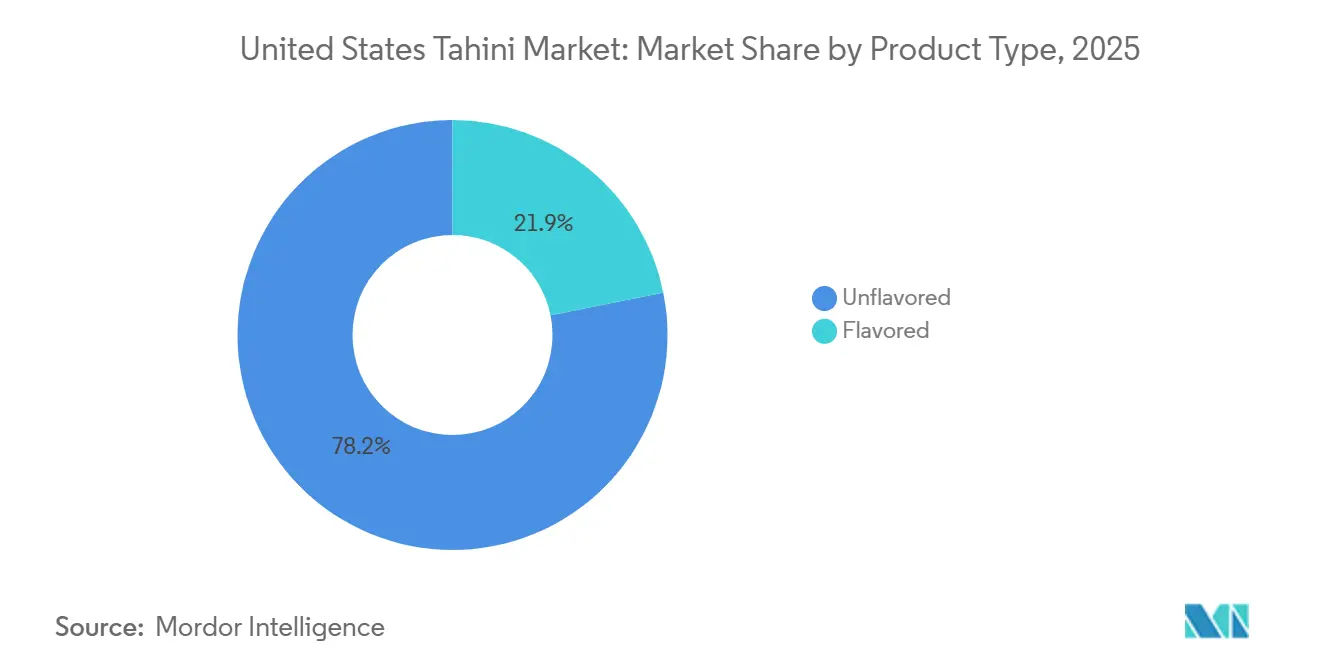

- By product type, unflavored tahini held 78.2% share in 2025, while flavored tahini is projected to grow at 6.1% CAGR from 2026 to 2031.

- By nature, conventional tahini accounted for 74.3% share in 2025, while organic tahini is forecast to expand at 6.8% CAGR from 2026 to 2031.

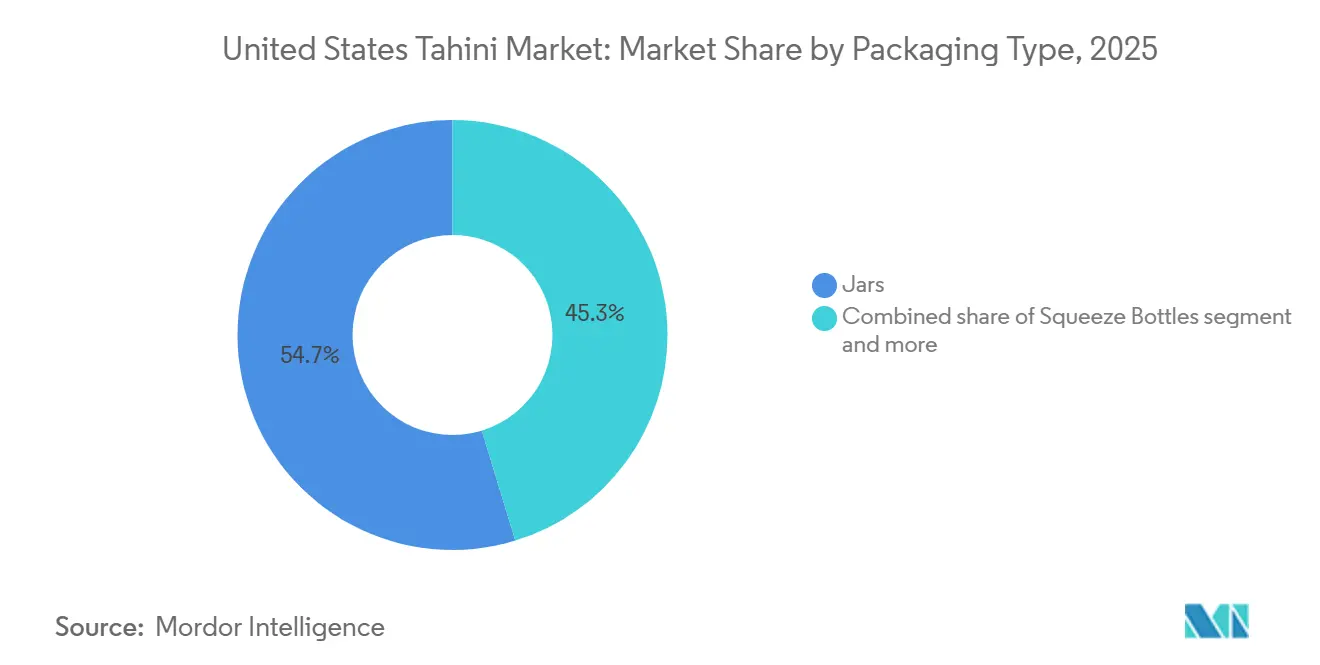

- By packaging type, jars captured 54.7% share in 2025, while squeeze bottles are expected to grow at 6.3% CAGR from 2026 to 2031.

- By distribution channel, supermarkets and hypermarkets held 39.5% share in 2025, while online retail is projected to advance at 7.0% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Tahini Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plant-based and clean-label spread adoption | +1.4% | Global, with highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Mainstreaming of Mediterranean and Middle Eastern menus | +1.2% | North America core, with spillover to Europe and Australia | Medium term (2-4 years) |

| E-commerce and natural-channel retail expansion | +0.9% | North America and Europe core, with emerging adoption in APAC | Short term (≤ 2 years) |

| Premiumization through organic and single-origin tahini | +0.8% | North America and Europe, with early adoption in GCC | Long term (≥ 4 years) |

| Squeeze-bottle convenience widening household usage occasions | +0.6% | North America primary, Europe secondary | Short term (≤ 2 years) |

| Foodservice sauce-platform adoption beyond hummus | +0.5% | North America campus and quick-service dining, with growing use in European hospitality | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Plant-based and clean-label spread adoption

In the U.S., the tahini market is expanding its reach, thanks to the growing popularity of plant-based diets. Tahini enjoys a prime spot in this trend, boasting a clean ingredient list that aligns with the rising demand for transparency in food labeling. A recent study published in the journal Foods highlighted sesame meal as a top-tier plant protein, emphasizing its digestibility and amino acid profile[2]Source: National Center for Biotechnology Information, "Sesame Seed Meal as a Sustainable Source of High-Quality Plant-Based Proteins: Delineating Recent Advances in the Preparation, Composition, Techno-Functionalities, and Food Industry Applications", pubmed.ncbi.nlm.nih.gov. This bolsters the nutritional reputation of sesame-based foods, setting them apart from many heavily processed alternatives. Such distinctions resonate with consumers seeking plant-based choices that are both simple and minimally processed. Furthermore, this newfound versatility is allowing tahini to break free from its traditional confines, finding its way into breakfast dishes, snacks, and sauces. Consequently, tahini is carving out a niche for itself, not just in natural food stores but also in mainstream grocery aisles, where it's now being evaluated alongside other popular pantry spreads.

Mainstreaming of mediterranean and middle eastern menus

As foodservice expands, the U.S. tahini market sees new opportunities. Mediterranean and Middle Eastern dishes are increasingly featured in university and workplace dining, as well as quick-service outlets. This trend introduces first-time diners to tahini-based sauces and dressings. Such exposure is crucial; consumers are more inclined to buy tahini at retail after sampling it in a flavorful dish. Beyond its traditional use in hummus, tahini's versatility shines in wraps, grain bowls, salads, roasted veggies, and sandwiches. As foodservice operators increasingly adopt these dishes, tahini transitions from a specialty item to a staple sauce, stabilizing its demand. This shift benefits both branded suppliers and private-label processors, ensuring they can consistently meet institutional demand.

E-commerce and natural-channel retail expansion

Digital commerce is shining a spotlight on the tahini market in the United States. Online platforms allow sellers to delve deeper into product details like origin, texture, organic status, and production methods than traditional shelf tags permit. This added context is crucial in a market where consumers often grapple with taste, use cases, and quality distinctions. Additionally, the convenience of online shopping enables consumers to access a wider variety of premium tahini products that may not be available in local stores. Furthermore, the U.S. tahini market is reaping rewards from natural and specialty retail channels, which allocate more shelf space to artisanal, organic, and single-origin products compared to conventional grocers. Soom Foods, adopting a chef-led strategy, has seamlessly transitioned into major retail accounts after establishing product credibility. This approach has also allowed the brand to build a loyal customer base that values high-quality, differentiated products. This blend of foodservice trust, digital clarity, and availability in natural channels is elevating the premium tahini segment, pushing boundaries beyond just entry-level sales.

Premiumization through organic and single-origin tahini

In the United States, the tahini market is witnessing a shift towards premium positioning. Brands are leveraging organic certifications, single-origin sourcing, and clearer provenance claims to transition from competing on price to emphasizing quality. This trend is particularly evident in natural and specialty retail outlets, where consumers are already opting for premium products in related categories like nut butters and olive oil. In 2026, Once Again Nut Butter Collective underscored its longstanding Oregon Tilth organic certification. Such continuity is significant; it not only highlights a commitment to process discipline and consistent sourcing but also distinguishes the brand from fleeting premium trends. This same principle bolsters the appeal of single-origin tahini, as origin narratives provide brands with a distinct avenue to articulate differences in flavor, texture, and processing. As this trend continues, it's poised to drive value growth at a pace that outstrips volume growth, even amidst a moderately fragmented base category.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sesame seed import dependence and raw-material volatility | -0.9% | Global supply chain, with acute exposure in North America | Medium term (2-4 years) |

| Taste familiarity ceiling outside core ethnic and health cohorts | -0.7% | North America and Europe mainstream consumer base | Long term (≥ 4 years) |

| Sesame allergen labeling burden after FASTER Act | -0.4% | United States, under FDA compliance rules | Short term (≤ 2 years) |

| Recall and microbial-risk pressure on quality assurance and working capital | -0.3% | North America, especially FDA-regulated supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sesame seed import dependence and raw-material volatility

Import dependence poses a significant challenge for the U.S. tahini market. With domestic sesame production falling short of processing demands, manufacturers find themselves vulnerable to global crop fluctuations, shipping costs, currency shifts, and documentation challenges. This vulnerability is heightened in tahini, as sesame sourcing is limited to a few external origins. Even with steady finished demand, fluctuations in raw material supply can squeeze margins and postpone price recovery for mid-sized processors. Consequently, the U.S. tahini market favors companies that diversify their sourcing across various countries and adopt robust inventory planning. Companies that fail to adapt to these dynamics risk losing market share and profitability. This shift underscores the evolving perception of supply-chain resilience, now seen as a competitive edge rather than merely a procurement task.

Taste familiarity ceiling outside core ethnic and health cohorts

In the United States, the tahini market grapples with consumer education hurdles, limiting its expansion within the broader pantry category. Many newcomers to tahini remain uncertain about its taste, proper stirring techniques, and uses beyond hummus, dips, or dressings. Additionally, natural texture variations and oil separation can deter households accustomed to a more consistent spread. While these challenges haven't halted category growth, they have dampened repeat purchases among those unfamiliar with tahini. As a result, clear recipe communication, packaging guidance, and ready-to-use flavored formats have gained prominence in driving category development. Educating consumers about tahini's versatility and nutritional benefits could further enhance its appeal. Brands that simplify preparation and clarify usage stand to retain new buyers more effectively than those relying solely on shelf visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unflavored Products Keep The Base Strong While Flavored Lines Build New Usage

Unflavored tahini has solidified its position as the cornerstone of the U.S. tahini market, catering to a diverse clientele spanning retail, food manufacturing, and foodservice sectors. In 2025, unflavored tahini commanded a substantial 78.2% share of the U.S. tahini market, underscoring its pivotal role as the go-to base for hummus producers, bakers, and operators seeking a neutral flavor and consistent texture. This leading position is poised to endure, as high-volume users favor products versatile enough to adapt across various applications without necessitating changes in formulation or back-of-house processes. Furthermore, the U.S. tahini market reaps benefits from the alignment of unflavored products with private-label programs, where simplicity and scalability take precedence over novelty. For numerous institutional buyers, this segment offers a dependable means to manage costs and maintain menu consistency, stabilizing the category's entry point even as premium sub-segments emerge around it.

Flavored tahini is rapidly gaining traction, introducing fresh retail opportunities for the U.S. tahini market. Forecasted to expand at a 6.1% CAGR through 2031, the segment is buoyed by enticing flavor profiles like harissa, roasted garlic, and sweet variants, which effectively lower the barrier for first-time buyers. Brands are increasingly positioning tahini not just as a cooking base, but as a finishing sauce, sandwich spread, or snack ingredient. A testament to this trend, Soom Foods broadened its flavored squeeze-bottle line in 2026, highlighting suppliers' efforts to merge flavor variety with user convenience in a single launch. Similarly, Roland Foods showcases a diverse array of tahini formats and flavor profiles, indicating a growing supplier-level assortment as tahini's usage expands. While the surge in flavored products doesn't jeopardize the supremacy of unflavored tahini, it undeniably enhances the overall value mix and deepens its penetration in households.

By Nature: Conventional Products Lead On Scale While Organic Products Advance Faster

In the U.S. tahini market, conventional tahini dominated, aligning with the purchasing priorities of bulk buyers. In 2025, this segment commanded a 74.3% share, bolstered by institutional accounts and private-label programs that primarily emphasized affordability and a reliable supply. This conventional foundation enables the category to cater to supermarkets, club stores, and foodservice outlets, without being solely dependent on premium retail demand. Additionally, the segment enjoys greater sourcing flexibility, as building a conventional supply at scale is more feasible than for certified organic. This advantage is crucial in a market where reliance on imports can lead to time and cost challenges. Consequently, while premium values are on the rise, conventional tahini still establishes the baseline for category throughput.

Organic tahini is emerging as the fastest-growing segment in the U.S. tahini market, with projections indicating a 6.8% CAGR growth through 2031. This growth trajectory is bolstered by consumers who, having embraced organic products in other pantry staples, now seek those same organic standards in spreads, oils, and seeds. The significance of USDA organic standards is underscored by their role as a trust signal in a market where ingredient simplicity doesn't always set products apart. For instance, Once Again Nut Butter Collective highlights the importance of long-term organic certification, suggesting that consistency can bolster trust in this segment. The rapid ascent of organic tahini underscores a shift in the U.S. tahini market's premiumization trend, linking it more to verified sourcing and process credibility than mere branding.

By Packaging Type: Jars Hold Category Scale While Squeeze Bottles Improve Repeat Usage

In the United States tahini market, jars have consistently led as the preferred packaging choice, adeptly catering to both premium shelf displays and bulk handling demands. In 2025, jars commanded a notable 54.7% share of the U.S. tahini market, bolstered by their strong foothold in retail and enduring significance in larger foodservice packs. Glass jars, with their visual appeal, play a pivotal role in specialty and natural retail settings, where texture and color heavily influence purchasing decisions. The U.S. tahini sector continues to favor jars, not only for their compatibility with thicker formulations but also due to ingrained consumer habits. Familiar to buyers who incorporate tahini into their recipes, jars meet the expectation of easy stirring and portioning at home. Thus, even as alternative packaging formats gain traction, jars steadfastly anchor the category's volume.

Squeeze bottles are rapidly emerging as the preferred packaging choice in the U.S. tahini market, projected to grow at a robust 6.3% CAGR through 2031. Their rising popularity stems from their ability to minimize mess, reduce the need for stirring, and facilitate quick use as a topping or sauce. Mighty Sesame Co., a key player, has strategically centered its brand identity around squeeze packaging, underscoring the potential of packaging as a brand differentiator in this evolving market. On the technical front, delivering fluid tahini via squeeze bottles demands precise formulation and processing expertise, presenting a modest entry barrier for smaller brands[3]Source: Food and Drug Administration, " FDA Draft Guidance Could Result in Safer Food Options for People with Allergies to Sesame, Other Food Allergens", fda.gov. This positions the burgeoning squeeze format as not just a convenience but also a catalyst for product innovation and a testament to manufacturing prowess. Moving forward, while squeeze bottles are set to increase their usage frequency, they may not entirely supplant jars.

By Distribution Channel: Supermarkets And Hypermarkets Lead Volume While Online Retail Raises The Premium Mix

In the United States, supermarkets and hypermarkets have solidified their position as the dominant distribution channel for tahini, underscoring their pivotal role in mainstreaming the product. In 2025, this channel commanded a 39.5% market share, signaling tahini's evolution from a niche specialty to a recognized pantry staple. This trend indicates that tahini's popularity is expanding beyond just ethnic grocers and natural-food outlets. Large-format retailers empower both established brands and private-label suppliers, providing them with the volume necessary to maintain competitive shelf prices. Moreover, these retailers introduce tahini to households alongside familiar spreads and global condiments, rather than as a standalone item. Such visibility is crucial for turning consumer awareness into regular purchases.

Online retail is emerging as the fastest-growing channel for tahini in the U.S., with projections indicating a 7.0% CAGR surge through 2031. From 2026 to 2031, the U.S. tahini market anticipates a 7.0% CAGR growth in online retail, bolstered by enhanced product assortments, clearer educational content, and improved access to premium organic offerings. E-commerce proves advantageous for tahini brands, allowing them to elaborate on aspects like origin, texture, and certifications, thereby alleviating potential buyer hesitations. Furthermore, it provides smaller brands an avenue to tap into national demand without incurring the hefty slotting and shelf-access fees typical of physical retail. Brands like Soom Foods have adeptly leveraged a foodservice-first strategy, establishing credibility before expanding their retail footprint, a move that aligns seamlessly with online discovery and repeat purchases. Consequently, this online surge not only boosts channel volume but also tilts the value spectrum towards premium offerings.

Geography Analysis

In 2025, the Northeast and the West Coast emerged as the dominant hubs for tahini demand in the U.S., despite the absence of a regional share breakdown in the source draft. These regions boast vibrant Middle Eastern and Mediterranean communities, a robust specialty grocery framework, and a more seasoned consumer base familiar with tahini. Furthermore, they host a diverse array of establishments, from restaurants and delis to natural grocers and upscale supermarkets, catering to both mainstream and niche tahini varieties. This unique blend solidifies their status as the primary centers for tahini demand in the U.S.

The Sunbelt and various secondary metropolitan areas are witnessing the most rapid growth in the U.S. tahini market. Here, the rise of Mediterranean dining establishments and the expansion of natural food retailers are broadening household exposure to tahini. While specific CAGR figures for these regions weren't provided, the trend is unmistakable: demand is infiltrating areas previously unfamiliar with the product. In these locales, university and workplace dining, along with casual Mediterranean eateries, play a pivotal role. They introduce tahini through prepared dishes, paving the way for subsequent retail purchases. As a result, while these secondary cities may have a smaller sales base than the Northeast and West Coast, they possess a more pronounced growth trajectory.

The U.S. tahini market presents a landscape of expanding demand juxtaposed with supply challenges. Demand is shifting from coastal hubs to a broader national audience, facilitated by foodservice, e-commerce, and enhanced retail distribution. Conversely, U.S. processors' heavy reliance on imported sesame links domestic tahini performance to global sourcing dynamics, rather than solely local demand. This underscores the significance of origin diversification and quality control across all regions, even those with the strongest consumer demand. Thus, while consumption patterns are becoming more nationwide, the risks associated with sourcing remain global. This scenario positions well-equipped suppliers advantageously over smaller competitors who may lack depth in sourcing and testing capabilities.

Competitive Landscape

The United States tahini market remains moderately fragmented, with branded specialists, international suppliers, and private-label participants all active across different customer groups. Competition hinges more on product uniqueness, packaging, sourcing narratives, and foodservice ties than sheer scale. While Soom Foods and Mighty Sesame Co. shine in the premium branded segment, Prince Tahina and Halwani Bros. leverage their rich manufacturing legacies and regional clout. This dynamic curtails pricing power at the category level, allowing multiple players to flourish through unique channel strategies.

In the U.S. tahini market, strategic moves focus on packaging innovation, channel growth, and credible sourcing. In 2026, Soom Foods tapped into the trend by introducing flavored squeeze-bottle products, aligning with the category's rapid growth in both packaging and flavor. Meanwhile, Mighty Sesame Co. has carved a niche with its squeeze-format, positioning packaging as a cornerstone of its brand identity rather than just a line extension. Once Again Nut Butter Collective underscores the importance of certification continuity, bolstering trust in the organic segment and highlighting how disciplined processes can serve as a competitive edge.

In the U.S. tahini market, food safety and compliance have risen to prominence, rivaling traditional branding efforts. Recent FDA recalls of tahini and sesame products spotlighted the importance of microbial control. This scrutiny likely benefits producers with robust testing and documentation systems. Similarly, sesame allergen labeling compliance is crucial; missteps can tarnish consumer trust and strain retail ties. Sesajal's investment in a U.S. facility underscores a strategic pivot towards shorter supply chains and tighter operational oversight, even in a fragmented market. Firms that merge reliable sourcing with credible quality assurance stand a better chance of securing coveted foodservice and retail partnerships. As the competition evolves, operational resilience may prove as vital as product innovation.

United States Tahini Industry Leaders

-

Soom Foods

-

Joyva Corp.

-

Sunshine International Foods, Inc.

-

Mighty Sesame Co.

-

Seed + Mill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sesajal, a Mexican manufacturer specializing in sesame products, announced a USD 30 million investment in a new manufacturing facility in the U.S. The company has chosen Temple, Texas, for its 50,000-square-foot production and warehousing site. Construction is expected to begin in mid-2026, with operations employing 54 full-time staff by mid-2027. This investment signifies a pivotal shift for Sesajal, moving from being solely an exporter to establishing itself as a domestic processing supplier in the U.S. market.

- February 2026: Soom Foods has unveiled a new line of flavored tahini in squeeze bottles. By introducing these flavored variants, the company aims to cater to both retail households and foodservice operators, offering a convenient, ready-to-use tahini sauce.

- September 2025: Roland Foods, a New York-based specialty foods importer and a major tahini distributor, completed a 112,000-square-foot distribution expansion in Plant City, Florida. The company secured a long-term lease at Lakeside Logistics II, consolidating and broadening its operations in the Southeast U.S.

United States Tahini Market Report Scope

Tahini is a condiment made from toasted ground hulled sesame seeds, oil, and sometimes salt, particularly famous in the Middle East.

The United States Tahini market is segmented by product type into flavored and unflavored. Based on the nature, the market is segmented into conventional and organic. By packaging type, the market is segmented into jars, squeeze bottles, sachets, and pouches. Based on distribution channel, the market is segmented into supermarkets, convenience stores, online retail stores, and other distribution channels.

| Flavored |

| Unflavored |

| Conventional |

| Organic |

| Jars |

| Squeeze Bottles |

| Sachets and Pouches |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Retail Stores |

| By Product Type | Flavored |

| Unflavored | |

| By Nature | Conventional |

| Organic | |

| By Packaging Type | Jars |

| Squeeze Bottles | |

| Sachets and Pouches | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Stores |

Key Questions Answered in the Report

What is the current size of tahini demand in the United States

The United States tahini market is valued at USD 174.2 million in 2026 and is projected to reach USD 228.5 million by 2031 at a 5.6% CAGR.

Which product type leads tahini sales in the United States

Unflavored tahini remains the largest product type, with 78.2% share in 2025 because it serves retail, food manufacturing, and foodservice needs.

Which segment is growing the fastest in this category

Organic tahini is the fastest-growing segment across the report at a 6.8% CAGR from 2026 to 2031, reflecting stronger demand for verified clean-label sourcing.

Why are squeeze bottles becoming more important for tahini brands

Squeeze bottles are forecast to grow at 6.3% CAGR because they reduce handling friction and make tahini easier to use as a topping, sauce, or quick meal ingredient.

Page last updated on: