United States Rystiggo Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

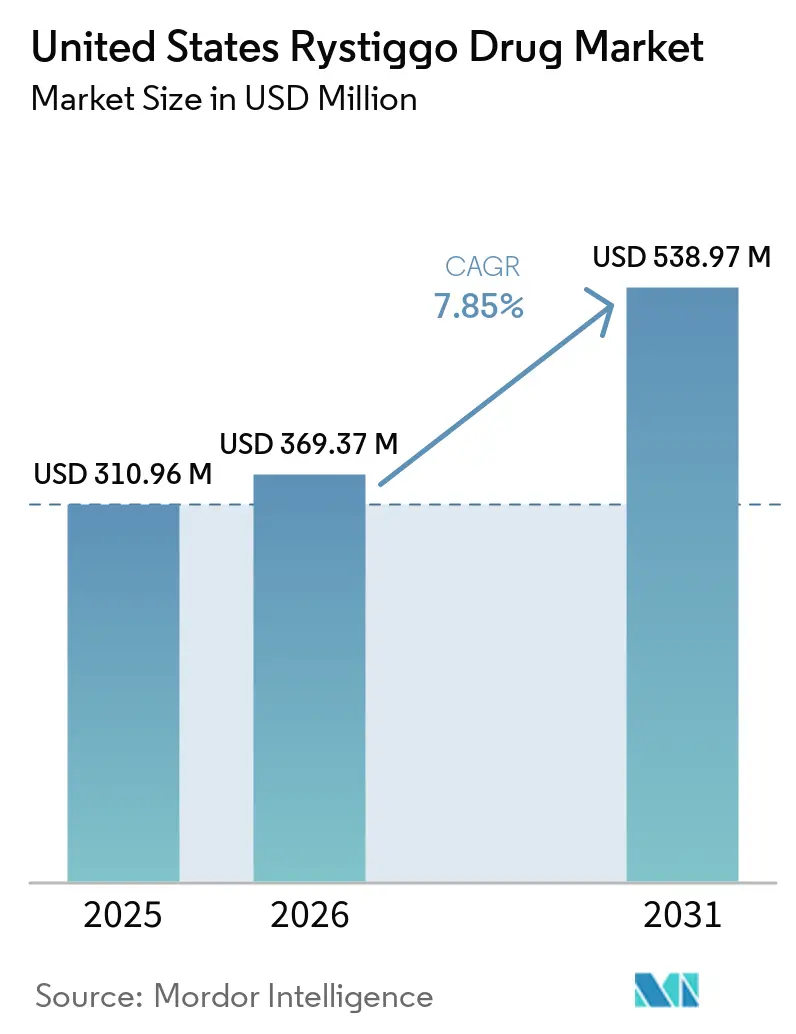

| Base Year Market Size (2025) | USD 310.96 Million |

| Market Size (2026) | USD 369.37 Million |

| Market Size (2031) | USD 538.97 Million |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

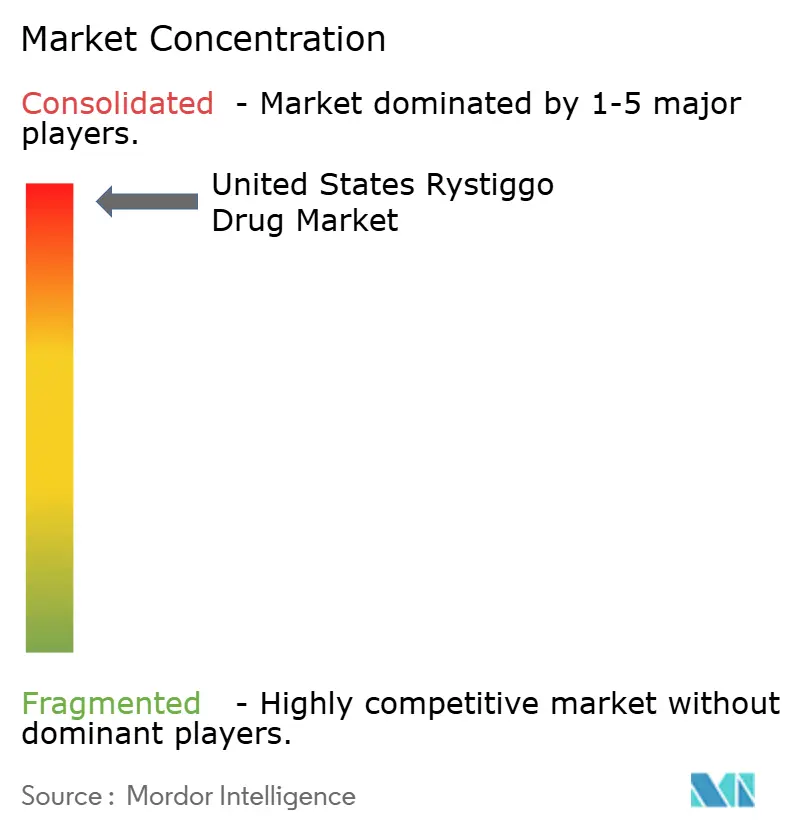

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Rystiggo Drug Market Analysis by Mordor Intelligence

The United States Rystiggo Drug Market size is expected to increase from USD 310.96 million in 2025 to USD 369.37 million in 2026 and reach USD 538.97 million by 2031, growing at a CAGR of 7.85% over 2026-2031.

The market is expanding on the back of steady physician uptake after the drug established a clear position in generalized myasthenia gravis through its coverage of both anti-acetylcholine receptor and anti-muscle-specific kinase antibody-positive disease. The drug also reached more than 2,400 patients globally by the end of 2025, compared with nearly 1,200 by the end of 2024, which shows that adoption widened materially as specialists gained more comfort with repeat-cycle use. The United States Rystiggo drug market is also being supported by stronger disease awareness, broader specialty neurology access, and payer interest in orphan biologics that can build a more durable real-world evidence base over time. Class competition is rising after the April 2025 approval of IMAAVY, but Rystiggo still benefits from orphan drug exclusivity through June 26, 2030, which helps protect early forecast-period pricing and limits near-term biosimilar risk in the United States Rystiggo drug market.

Key Report Takeaways

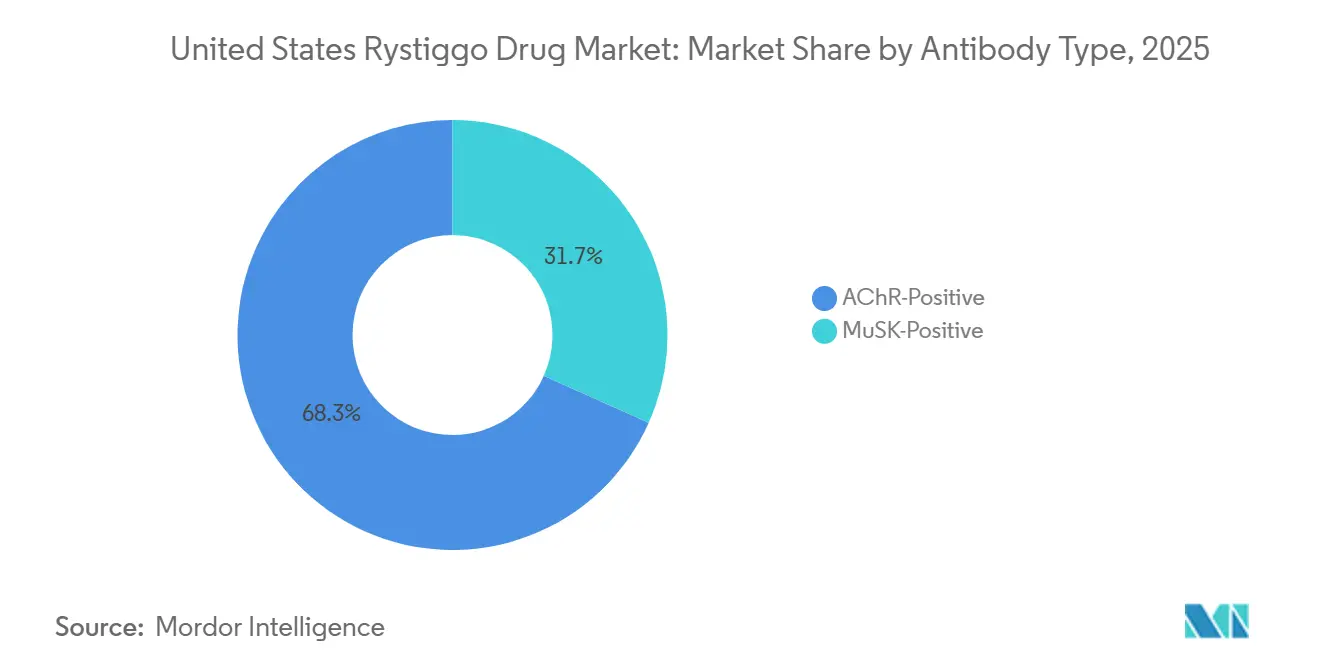

- By antibody type, AChR-positive patients held 68.31% of the United States Rystiggo drug market share in 2025, while MuSK-positive patients are projected to expand at a 9.38% CAGR through 2031.

- By dosage strength, the 560 mg/4 mL vial held a 39.24% share in 2025, while the 840 mg/6 mL vial is forecast to grow at a 9.52% CAGR through 2031.

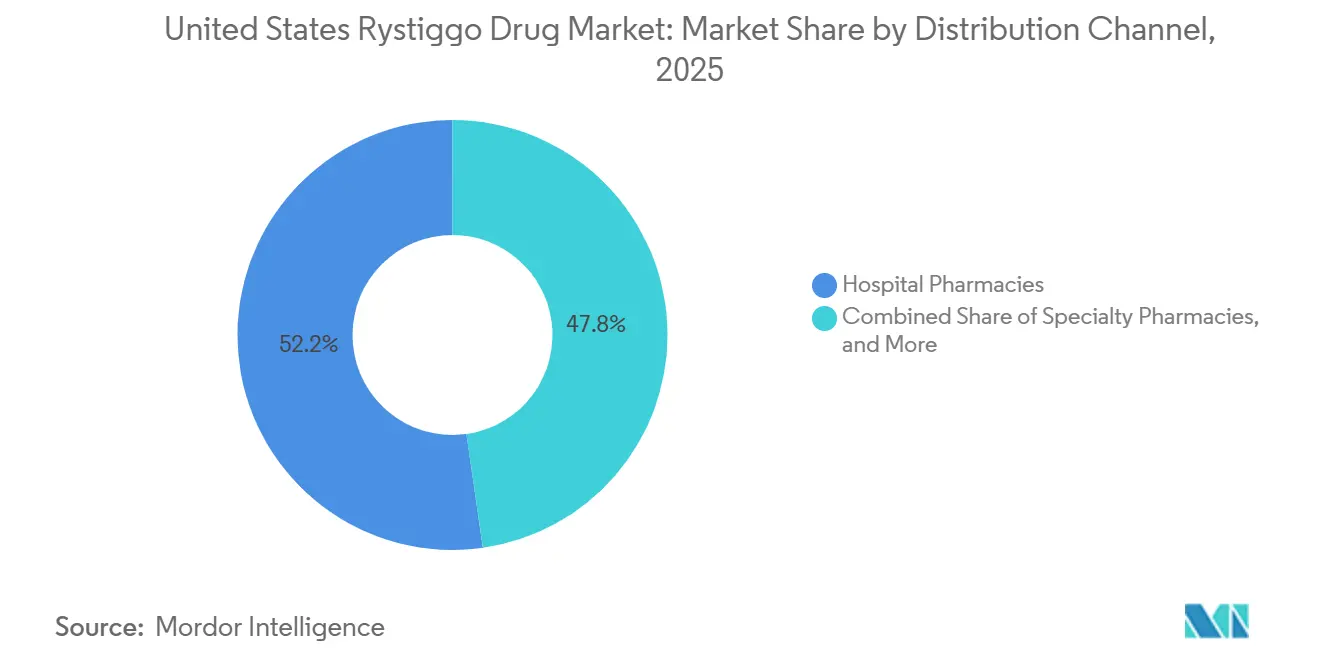

- By distribution channel, hospital pharmacies led with 52.24% share in 2025, while specialty pharmacies are projected to grow at an 8.25% CAGR through 2031.

- By end user, hospitals accounted for 52.52% share in 2025, while home care settings are forecast to expand at a 10.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Rystiggo Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid uptake of FcRn-targeted biologics in specialty neurology | +2.5% | National, with early gains in high-volume MG centers in the Northeast, Mid-Atlantic, and West Coast | Medium term (2-4 years) |

| Broad AChR and MuSK label expands treatable population | +2.2% | National, with specific upside in academic centers managing seronegative workup and MuSK confirmation | Short term (≤ 2 years) |

| Self-administered or clinic-light dosing supports adherence and site-of-care shift | +1.4% | National, with acute impact in patient populations distant from specialty infusion centers | Medium term (2-4 years) |

| Orphan neurology reimbursement pathways support early access | +0.9% | National, with the clearest benefit in Medicaid and Medicare Advantage populations | Short term (≤ 2 years) |

| Real-world evidence generation strengthens formulary conversion | +0.6% | National, with longer-term influence in commercial and managed Medicaid segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of FcRn-Targeted Biologics in Specialty Neurology

The FcRn inhibitor class changed how neurologists approached generalized myasthenia gravis, because treatment focus moved away from broad immunosuppression toward targeted reduction of pathogenic autoantibodies in the United States Rystiggo drug market. Rozanolixizumab works by blocking FcRn recycling and lowering circulating IgG, including pathogenic AChR and MuSK autoantibodies, which separates it mechanistically from acetylcholinesterase inhibitors and non-specific steroids[1]Springer Nature, “Myasthenia Gravis in 2025: Five New Things and Four Hopes for the Future,” Journal of Neurology, springer.com. Published systematic review and meta-analysis evidence across 8 randomized controlled trials and 873 patients showed that FcRn inhibitors improved MG-ADL, QMG, and MGC scores versus placebo, which supported growing class confidence among neurologists. That prior class familiarity mattered because physicians who had already used FcRn therapy in practice were more prepared to adopt Rystiggo for patients with incomplete response to intravenous alternatives in the United States Rystiggo drug market. UCB also presented long-term evidence from the MG0004 and MG0007 open-label extension studies in 2025, which reinforced tolerability and retreatment efficacy across repeated symptom-driven cycles. Those data supported payer renewals and physician confidence, and they helped the United States Rystiggo drug market move closer to a chronic management model instead of a one-time rescue pattern.

Broad AChR and MuSK Label Expands Treatable Population

Rystiggo’s dual approval for both AChR-positive and MuSK-positive disease remains commercially important because it reaches a broader treated pool than agents limited to AChR-positive labeling[2]ARUP Consult, “Myasthenia Gravis – Choose the Right Test,” ARUP Consult, arupconsult.com. MuSK-positive patients accounted for only a small portion of all myasthenia gravis cases, but they represented a larger share of refractory and treatment-resistant disease, which made this label breadth more meaningful than headline prevalence numbers suggested. U.S. prevalence estimates ranged from nearly 116,000 diagnosed patients to 135,000 when broader claims coverage was considered, and that created a defined addressable pool for targeted therapy in the United States Rystiggo drug market. Within that group, MuSK-positive disease represented 6% to 8% of cases and nearly 40% of AChR-seronegative patients, which kept Rystiggo relevant for a niche that historically relied on off-label management. The April 2025 approval of IMAAVY narrowed Rystiggo’s label advantage because Johnson & Johnson entered the same AChR-positive and MuSK-positive space with an intravenous FcRn blocker. Even so, Rystiggo preserved a practical convenience edge through its subcutaneous route and established access setup, which kept the United States Rystiggo drug market well positioned as site-of-care economics became more important to payers.

Self-Administered or Clinic-Light Dosing Supports Adherence and Site-of-Care Shift

Phase 3 MG0020 data showed that 100% of evaluable patients successfully self-administered rozanolixizumab through both syringe driver and manual push methods after a structured 6-week training period. The same study found that 63.6% of patients preferred self-administration over healthcare professional administration, and 74.5% preferred home-based dosing, which showed that convenience was not a marginal benefit. Median administration time was 5 minutes with manual push versus 12 minutes with the infusion pump, which reduced routine treatment burden for patients, caregivers, and clinic staff. That operating simplicity supports the fastest-growing home care end-user pattern in the United States Rystiggo drug market because therapy becomes less tied to major infusion centers and large metropolitan neurology programs. It also supports faster growth of specialty pharmacy dispensing, because payers have a clear incentive to push care away from hospital outpatient settings and toward lower-cost home administration. As a result, the United States Rystiggo drug market is gradually shifting from a center-based initiation model toward a more flexible care pathway that can sustain repeat use without adding equivalent infrastructure cost.

Orphan Neurology Reimbursement Pathways Support Early Access

Rystiggo’s orphan exclusivity runs through June 26, 2030, and that protection remains a direct support for the United States Rystiggo drug market because it limits near-term biosimilar pressure. That regulatory protection also helps sustain pricing stability during the core forecast window, which matters in a rare-disease setting where commercial access decisions depend on long-duration budget visibility. UCB’s ONWARD support program reported that more than 97% of commercially insured patients and more than 98% of Medicare supplemental patients had a defined access pathway, which reduced friction at treatment start. The same program stated that eligible Medicare supplement patients could pay USD 0 out of pocket per dose, which strengthened practical affordability even when gross therapy cost remained high. Medicaid access also remained relatively protected, with typical patient monthly out-of-pocket cost reported at USD 5.15 to USD 10.30, which removed a common access barrier seen in other rare-disease biologics. These reimbursement supports matter because they give specialty neurology centers a clearer pathway to start treatment and maintain follow-up in the United States Rystiggo drug market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High annual therapy cost and prior authorization friction | -2.0% | National, most pronounced in commercial insurance segments without specialty carve-outs | Medium term (2-4 years) |

| Safety monitoring burden, infection risk, and vaccine restrictions | -0.8% | National, acute in community neurology and primary care referral channels | Medium term (2-4 years) |

| Class competition from Vyvgart, IMAAVY, Soliris, Ultomiris, and Zilbrysq | -2.5% | National, concentrated in AChR-positive patient decisions at academic medical centers | Long term (≥ 4 years) |

| Limited eligible pool and diagnostic uncertainty outside specialty centers | -1.4% | National, with the greatest effect in rural and community hospital-served geographies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Annual Therapy Cost and Prior Authorization Friction

Rystiggo’s U.S. list price was USD 3,155.37 per mL, and a single 6-week treatment cycle for heavier patients could reach USD 75,000 to USD 90,000 at the vial level. That cost places the therapy among the highest-priced specialty neurology biologics per episode of care, which naturally tightens payer scrutiny in the United States Rystiggo drug market. Major commercial payers required prior authorization and often asked for confirmed MGFA Class II to IVa disease plus prior exposure to conventional immunosuppressive therapy before approval. Initial approvals commonly ran for 6 months and renewals then required additional response documentation, which turned access into a repeated administrative process rather than a one-time review. That matters because Rystiggo uses symptom-driven treatment cycles, and even responding patients can face delays if payer documentation thresholds are not met consistently across renewals. UCB’s support structure eases part of that burden, but the cost and authorization barrier remains one of the clearest limits on the near-term growth pace of the United States Rystiggo drug market.

Safety Monitoring Burden, Infection Risk, and Vaccine Restrictions

Rystiggo lowers total circulating IgG, so its mechanism creates a built-in immunosuppressive effect that requires more monitoring than simpler symptomatic therapies. In controlled studies, the prescribing information listed sinusitis in 23.4% of treated patients, COVID-19 in 21.8%, and urinary tract infection in 6.9%, which keeps infection surveillance central in routine care. Vaccine timing adds another logistical challenge because live and live-attenuated vaccines are contraindicated during active treatment and broader vaccination timing must be planned around dosing cycles. The product information states that vaccines should be given at least 4 weeks before treatment starts and at least 2 weeks after the final dose of a cycle, which complicates scheduling for older patients who need recurring adult immunizations. These steps are harder for community neurology practices that do not have dedicated rare-disease coordinators, because monitoring, vaccine review, and follow-up all add staff time. As a result, the United States Rystiggo drug market still faces a practical adoption ceiling outside major specialty centers even when physician interest in FcRn biology remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Antibody Type: AChR Dominance Supports Revenue While MuSK Expands Faster

AChR-positive patients held 68.31% of the United States Rystiggo drug market share in 2025, which kept them as the core treated population inside the antibody-type split FDA.GOV. This lead reflected the simple fact that AChR antibodies are present in the majority of adult generalized myasthenia gravis cases, so neurologists naturally focused first on that broader diagnosed base. In practice, these patients formed the main prescribing target when physicians moved beyond pyridostigmine, corticosteroids, or non-steroidal immunosuppressants and stepped into FcRn therapy. The pivotal MycarinG study supported that use pattern because it showed clinically meaningful improvement in MG-ADL and QMG scores by Day 43 across the antibody groups studied. That broad efficacy base anchored the antibody segment structure of the United States Rystiggo drug market, because it gave prescribers confidence that the drug could serve more than one immunologic profile.

MuSK-positive patients are projected to grow at a 9.38% CAGR through 2031, making them the fastest-growing antibody sub-segment in the United States Rystiggo drug market size outlook. MuSK antibodies were found in nearly 6% of all myasthenia gravis cases and in nearly 40% of AChR-seronegative patients, which made diagnostic improvement especially important for this subpopulation. These patients often showed more severe bulbar and facial involvement and had weaker response to cholinesterase inhibitors, so clinical demand for a targeted approved option remained high. Before 2025, the lack of approved alternatives gave Rystiggo a very favorable position in this niche, and that early foothold still matters even after the arrival of IMAAVY. The growth outlook therefore reflects both a real unmet-need base and rising physician attention to antibody subtype testing, which should keep MuSK treatment volumes expanding faster than the broader United States Rystiggo drug market.

By Dosage Strength: Mid-Weight Vials Lead While Higher-Strength Use Rises

The 560 mg/4 mL vial held 39.24% of the dosage-strength segment in 2025, which made it the leading presentation in the United States Rystiggo drug market. That position fits the weight-tiered dosing structure, because patients treated at nearly 7 mg/kg in the 70 kg to 80 kg range often align naturally with this configuration. Rystiggo is supplied in 280 mg/2 mL, 420 mg/3 mL, 560 mg/4 mL, and 840 mg/6 mL single-dose vials, and that portfolio lets pharmacies match dosing more closely to body weight. The 280 mg/2 mL and 420 mg/3 mL formats continue to serve lighter patients and combination-fill needs, but they do not appear to sit at the center of routine dispensing volume. The leading share of the 560 mg/4 mL vial therefore reflects the modal treated patient profile rather than a simple packaging preference inside the United States Rystiggo drug market.

The 840 mg/6 mL vial is forecast to grow at a 9.52% CAGR through 2031, which makes it the fastest-expanding strength format. This pattern points to broader use among heavier patients and among patients maintained on the 10 mg/kg tier across repeated treatment cycles. Open-label extension work from MG0007 and MG0004, which UCB highlighted in 2025, supported continued use across multiple symptom-driven cycles in patients with more persistent disease burden. The 840 mg/6 mL presentation also offers operational advantages because a single-unit fill can reduce dispensing complexity for specialty pharmacies and hospital pharmacies handling higher-weight patients. That shift does not change the current leadership of the 560 mg/4 mL vial, but it shows that treated-patient mix in the United States Rystiggo drug market is broadening in a way that favors stronger single-vial presentations.

By Distribution Channel: Hospital Pharmacies Lead While Specialty Dispensing Gains Pace

Hospital pharmacies held 52.24% share in 2025, which made them the largest distribution channel in the United States Rystiggo drug market. That lead reflected the initial treatment path for many patients, because diagnosis confirmation, antibody testing, first-cycle supervision, and reimbursement setup were concentrated inside hospitals and academic medical centers. Hospital settings also remained important for patients presenting with severe symptoms or complicated care histories, where structured monitoring mattered more than dispensing convenience. The United States Rystiggo drug market therefore started from a channel base shaped by institutional neurology, not by direct home dispensing. That historical setup explains why hospital pharmacies still led even as patient preference gradually moved toward more flexible administration models.

Specialty pharmacies are projected to grow at an 8.25% CAGR through 2031, which makes them the fastest-moving channel in the United States Rystiggo drug market. The strongest reason is the self-administration evidence base, because patients who can reliably dose at home no longer need the same level of repeated hospital involvement. Payers also have a clear incentive to steer treatment away from hospital outpatient billing when specialty pharmacy fulfillment and home-based administration can lower total cost of care. UCB’s access and patient support setup supports this shift by helping patients navigate reimbursement and ongoing care coordination outside the hospital setting. The channel mix is therefore likely to keep tilting toward specialty dispensing even if hospitals remain central for diagnosis, first-cycle oversight, and complex patient management in the United States Rystiggo drug market.

By End User: Hospitals Hold the Base While Home Care Reshapes Delivery

Hospitals accounted for 52.52% share in 2025, which left them as the leading end-user setting in the United States Rystiggo drug market. That outcome was tied to their role in diagnosis confirmation, antibody subtype testing, treatment initiation, and early-cycle safety monitoring for new generalized myasthenia gravis patients. Hospitals also remained the natural setting for patients with acute exacerbation or greater risk during initial dosing, because monitoring capacity is broader and care escalation can happen immediately if needed. Specialty neurology clinics sat between hospital initiation and long-term cycle management, especially in academic outpatient departments with dedicated myasthenia gravis programs. This structure means hospitals still anchor the end-user pattern of the United States Rystiggo drug market even as actual maintenance delivery becomes more flexible over time.

Home care settings are projected to grow at a 10.25% CAGR through 2031, which makes them the fastest-growing end-user in the United States Rystiggo drug market size outlook. The Phase 3 MG0020 study directly supports that shift, because 100% of evaluable patients self-administered successfully and 74.5% preferred home dosing over clinic administration. Manual push delivery also reduced median administration time to 5 minutes versus 12 minutes with the pump, which made routine treatment more manageable at home. UCB’s HumaMG digital adherence app and related data presentations in 2025 added another layer of support by giving providers a remote monitoring tool for follow-up outside conventional infusion settings. Together, those factors are gradually changing the care pathway from institution-heavy delivery toward a more patient-centered model without removing hospitals from the early care process of the United States Rystiggo drug market.

Geography Analysis

The United States Rystiggo drug market geographic footprint remains concentrated in regions with dense specialty neurology infrastructure rather than evenly distributed across the country. Early prescribing has been concentrated in academic medical centers across the Northeast corridor, major West Coast metropolitan areas, and large Midwest research institutions that handle complex neuromuscular disease. This concentration reflects referral patterns more than simple population density, because high-volume centers are better equipped to confirm generalized myasthenia gravis and subtype antibody status before biologic initiation. U.S. prevalence estimates ranged from nearly 116,000 patients to 135,000 depending on the claims base used, which suggests that national demand exists well beyond the current concentration of prescribing centers[3]Neurology, “Incidence and Prevalence of Myasthenia Gravis: Analysis of a US Commercial Insurance Claims Database,” Neurology, neurology.org. The age-standardized incidence was nearly 68.48 per million person-years in commercially insured or Medicare-insured populations, which supports steady, rather than sudden, expansion of the addressable pool in the United States Rystiggo drug market.

A major structural limit is the gap between where patients first present and where definitive diagnosis is made, because electromyography, repetitive nerve stimulation, and antibody testing are still more reliable in specialized centers. That means the effective treatment pool is constrained less by disease prevalence and more by the ability of the referral system to confirm eligibility and start targeted therapy. Rural and community-served geographies in the South, Mountain West, and rural Midwest tend to face the longest referral-to-treatment timelines, which slows prescribing spread beyond major urban clusters. This diagnostic concentration issue is especially important for MuSK-positive and seronegative workups, because those patients often require more specialized evaluation before treatment selection becomes clear. UCB’s ONWARD support program helps once the diagnosis is established, but it cannot fully remove the upstream shortage of specialty neurology access in the United States Rystiggo drug market.

Geographic concentration should ease over time as home-based administration becomes more common and specialty pharmacies expand remote training support. The 10-year Vitaccess Real MG Registry, which was actively recruiting 600 patients across U.S. and European sites as of July 2024, should add longer-term safety and outcomes evidence that can reassure less specialized providers. That broader post-approval evidence base may gradually reduce the need for every first-cycle decision to stay inside a top academic center, especially for repeat-cycle patients with stable follow-up pathways. The United States Rystiggo drug market also benefits from orphan exclusivity through June 2030, which removes one pricing uncertainty that might otherwise slow broader payer adoption across different regional care systems.

Competitive Landscape

The United States Rystiggo drug market is consolidated around a small group of targeted biologic therapies that compete through mechanism, label breadth, route of administration, and practical site-of-care economics. UCB holds a distinctive position because it participates in both the FcRn pathway through Rystiggo and the complement pathway through Zilbrysq, which gives it broader relevance across antibody-defined treatment decisions. Rystiggo’s strongest differentiation has been its ability to cover both AChR-positive and MuSK-positive adult generalized myasthenia gravis through a subcutaneous route that supports flexible care delivery. Competing therapies still matter sharply, especially in AChR-positive disease, where neurologists can choose among several targeted mechanisms and route options.

The most important recent competitive move was Johnson & Johnson’s April 2025 approval of IMAAVY, because nipocalimab entered with the same AChR-positive and MuSK-positive label reach and also added a pediatric indication for patients aged 12 years and older. That approval narrowed one of Rystiggo’s clearest class advantages, particularly in MuSK-positive disease, even though route and patient convenience still differentiate the two products. argenx’s Vyvgart franchise remained a meaningful FcRn competitor because of accumulated physician familiarity. AstraZeneca’s Soliris and Ultomiris also continue to compete in AChR-positive disease, but their intravenous delivery and narrower immunologic positioning limit direct overlap with Rystiggo’s broader adult label in the United States Rystiggo drug market. This means competition is real and rising, but it is still shaped by patient subtype, delivery preference, and care-setting logistics rather than by one simple price-driven hierarchy.

UCB’s main strategic response has been to deepen evidence rather than rely only on first-launch positioning in the United States Rystiggo drug market. The company funded and became the first subscriber to the Vitaccess Real MG Registry, which is a 10-year longitudinal dataset intended to build large-scale real-world evidence for payers and specialists. UCB also moved into label expansion by registering the MyVision Phase 3 program in ocular myasthenia gravis in March 2026, which could extend Rystiggo beyond its current adult generalized myasthenia gravis focus. Another strategic move came through claims-based switching data presented in 2026, which supported Rystiggo as a second-line FcRn option for patients with inadequate response to a competing FcRn therapy. Those steps suggest that competitive standing in the United States Rystiggo drug market will depend not only on label breadth, but also on who can build the most credible long-term evidence and the most workable care pathway for repeat-cycle use.

United States Rystiggo Drug Industry Leaders

UCB S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: UCB registered Phase 3 trials NCT07463521 (MyVision, placebo-controlled efficacy study) and NCT07465289 (open-label long-term extension) for rozanolixizumab in ocular myasthenia gravis (oMG), with estimated enrollment start in May–July 2026 and completion estimated in 2031. The oMG indication could expand Rystiggo's addressable patient population beyond the current adult gMG-only label.

- January 2026: KORU Medical Systems, Inc. received U.S. Food and Drug Administration (FDA) clearance for its FreedomEDGE infusion system. This approval allows the system to deliver RYSTIGGO (rozanolixizumab-noli), a therapy developed and marketed globally by UCB.

United States Rystiggo Drug Market Report Scope

As per the scope of the report, Rystiggo (rozanolixizumab-noli) is a prescription medication developed by UCB to treat generalized myasthenia gravis (gMG), a rare and chronic autoimmune disease that causes severe muscle weakness and fatigue.

The segmentation of the United States Rystiggo drug market is categorized by antibody type, dosage strength, distribution channel, and end user. By antibody type, the market is divided into AChR-positive and MuSK-positive. By dosage strength, it includes 280 mg / 2 mL, 420 mg / 3 mL, 560 mg / 4 mL, and 840 mg / 6 mL. By distribution channel, the segmentation comprises specialty pharmacies, hospital pharmacies, and other distribution channels. By end user, the market is segmented into hospitals, specialty neurology clinics, and home care settings. For each segment, the market size and forecast are provided in terms of value (USD).

| AChR-Positive |

| MuSK-Positive |

| 280 mg / 2 mL |

| 420 mg / 3 mL |

| 560 mg / 4 mL |

| 840 mg / 6 mL |

| Specialty Pharmacies |

| Hospital Pharmacies |

| Other Distribution Channels |

| Hospitals |

| Specialty Neurology Clinics |

| Home Care Settings |

| By Antibody Type | AChR-Positive |

| MuSK-Positive | |

| By Dosage Strength | 280 mg / 2 mL |

| 420 mg / 3 mL | |

| 560 mg / 4 mL | |

| 840 mg / 6 mL | |

| By Distribution Channel | Specialty Pharmacies |

| Hospital Pharmacies | |

| Other Distribution Channels | |

| By End User | Hospitals |

| Specialty Neurology Clinics | |

| Home Care Settings |

Key Questions Answered in the Report

What is driving growth in the United States Rystiggo drug market?

Growth is being supported by wider FcRn class adoption, Rystiggo's AChR-positive and MuSK-positive label coverage, and a growing shift toward home-friendly administration pathways.

How large is the United States Rystiggo drug market by 2031?

The United States Rystiggo drug market is expected to reach USD 538.97 million by 2031 from USD 369.37 million in 2026, at a CAGR of 7.85%.

Which patient group contributes the most revenue for Rystiggo in the United States?

AChR-positive patients contributed the largest share at 68.31% in 2025 because they represent the largest diagnosed antibody-defined population in generalized myasthenia gravis.

Which part of the care pathway is expanding fastest for Rystiggo use?

Home care settings are growing fastest at a 10.25% CAGR through 2031, supported by 100% successful self-administration in the MG0020 study and strong patient preference for home dosing.

What is the biggest barrier to wider use of Rystiggo?

High treatment cost and repeated prior authorization remain the main barriers, because a single 6-week cycle can reach USD 75,000 to USD 90,000 and renewals require continuing clinical documentation.

How strong is the competitive pressure around Rystiggo in generalized myasthenia gravis?

Competitive pressure is increasing after Johnson & Johnson's April 2025 approval of IMAAVY, but Rystiggo still benefits from adult dual-antibody positioning, subcutaneous administration, and orphan exclusivity through June 2030.

Page last updated on: