Tremfya Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.43 Billion |

| Market Size (2031) | USD 10.18 Billion |

| Growth Rate (2026 - 2031) | 9.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tremfya Drug Market Analysis by Mordor Intelligence

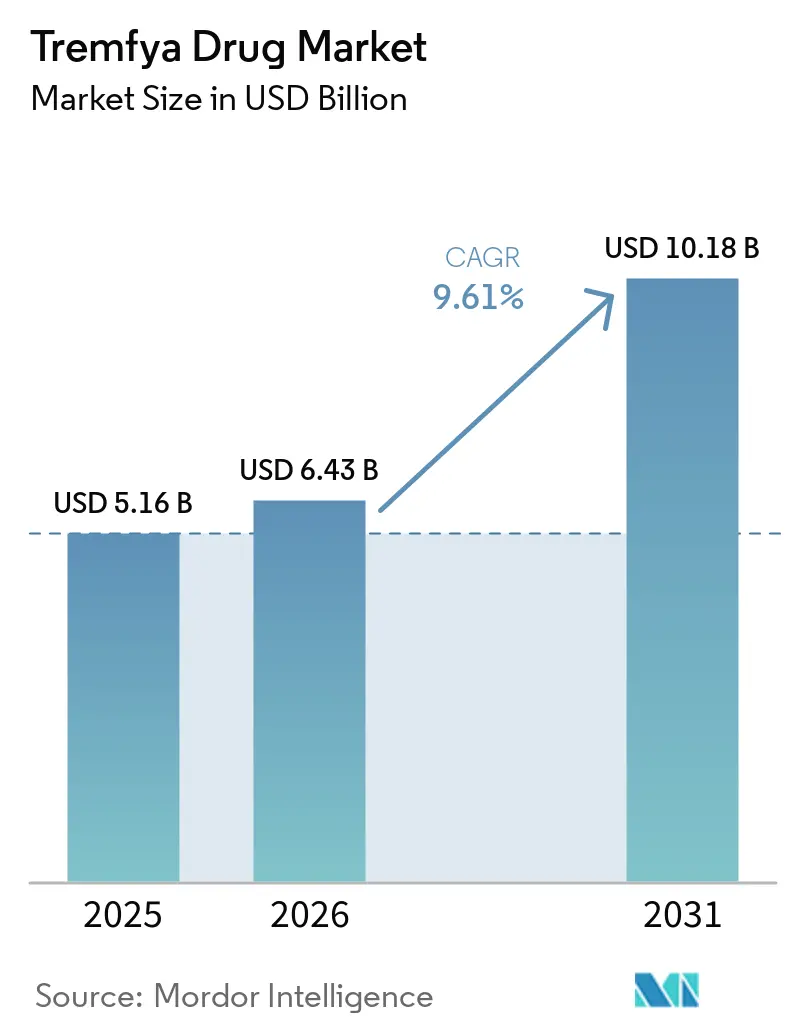

The Tremfya Drug Market size is projected to be USD 5.16 billion in 2025, USD 6.43 billion in 2026, and reach USD 10.18 billion by 2031, growing at a CAGR of 9.61% from 2026 to 2031.

The growth path of the Tremfya drug market reflects a clear expansion from a dermatology and rheumatology base into gastroenterology after the FDA approved ulcerative colitis in September 2024 and Crohn's disease in March 2025. Its profile remains distinct because guselkumab is the only approved fully human monoclonal antibody that blocks the IL-23 p19 subunit and also binds CD64 on IL-23-producing cells, which keeps the Tremfya drug market clinically differentiated within the IL-23 class. The Tremfya drug market is also benefiting from a wider site-of-care model because fully subcutaneous induction through maintenance in ulcerative colitis and Crohn's disease lowers dependence on infusion capacity and can support treatment persistence in routine care. Competitive pressure remains active as the Tremfya drug market now sits beside other IL-23 therapies in IBD and psoriasis and also beside a newly approved oral IL-23 receptor antagonist, which broadens treatment choice and raises the importance of differentiation in label depth and sequencing. At the same time, the pediatric approvals granted in September 2025 and the May 2026 label expansion for structural joint damage inhibition in active psoriatic arthritis extend the branded lifecycle of the Tremfya drug market and support use across a wider chronic-care continuum.

Key Report Takeaways

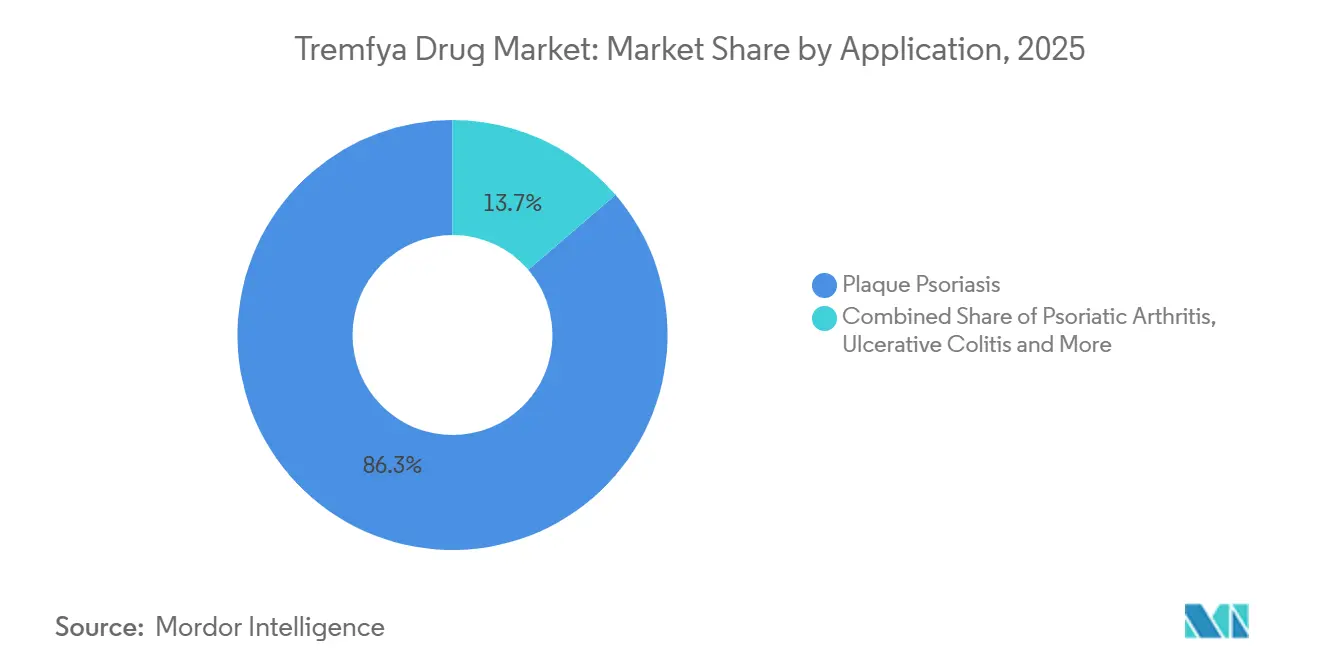

- By application, plaque psoriasis held 86.31% of the Tremfya drug market share in 2025, while Crohn's disease is projected to expand at an 11.38% CAGR through 2031.

- By route of administration, subcutaneous injection accounted for 65.24% of revenue in 2025, while intravenous infusion is expected to record the highest growth at a 10.52% CAGR during 2026-2031.

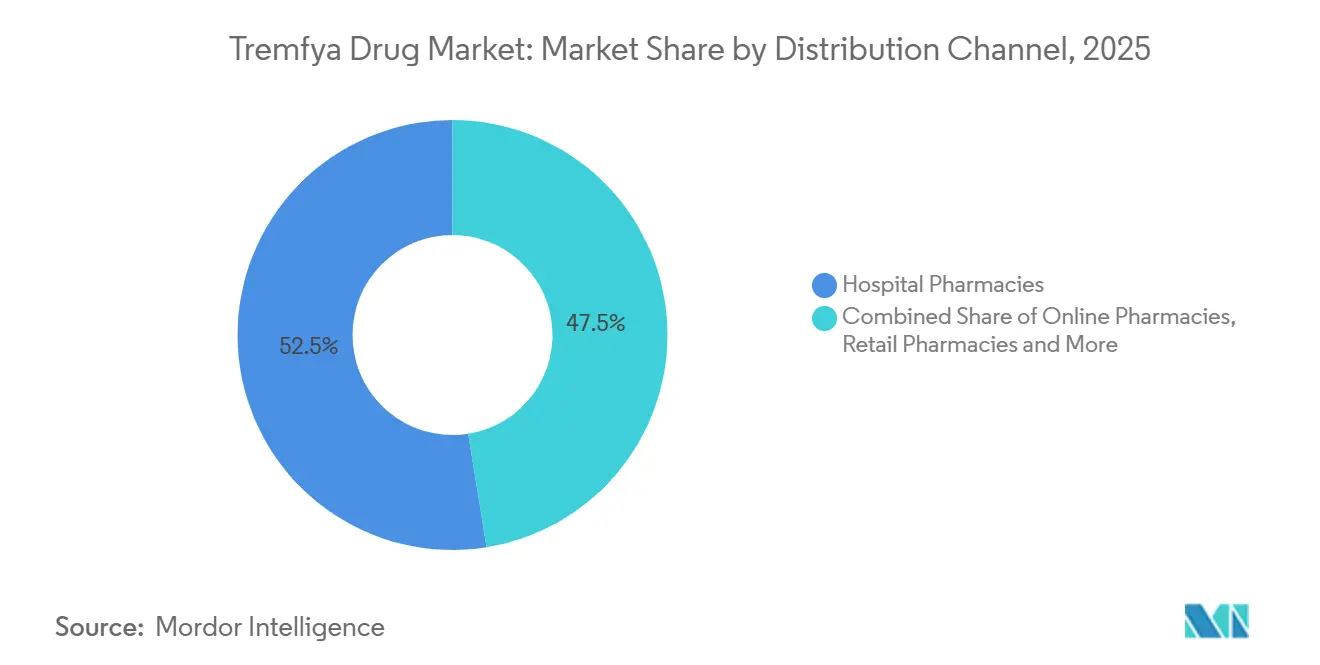

- By distribution channel, hospital pharmacies held 52.52% of the Tremfya drug market size in 2025, while online pharmacies are forecast to grow at an 11.25% CAGR through 2031.

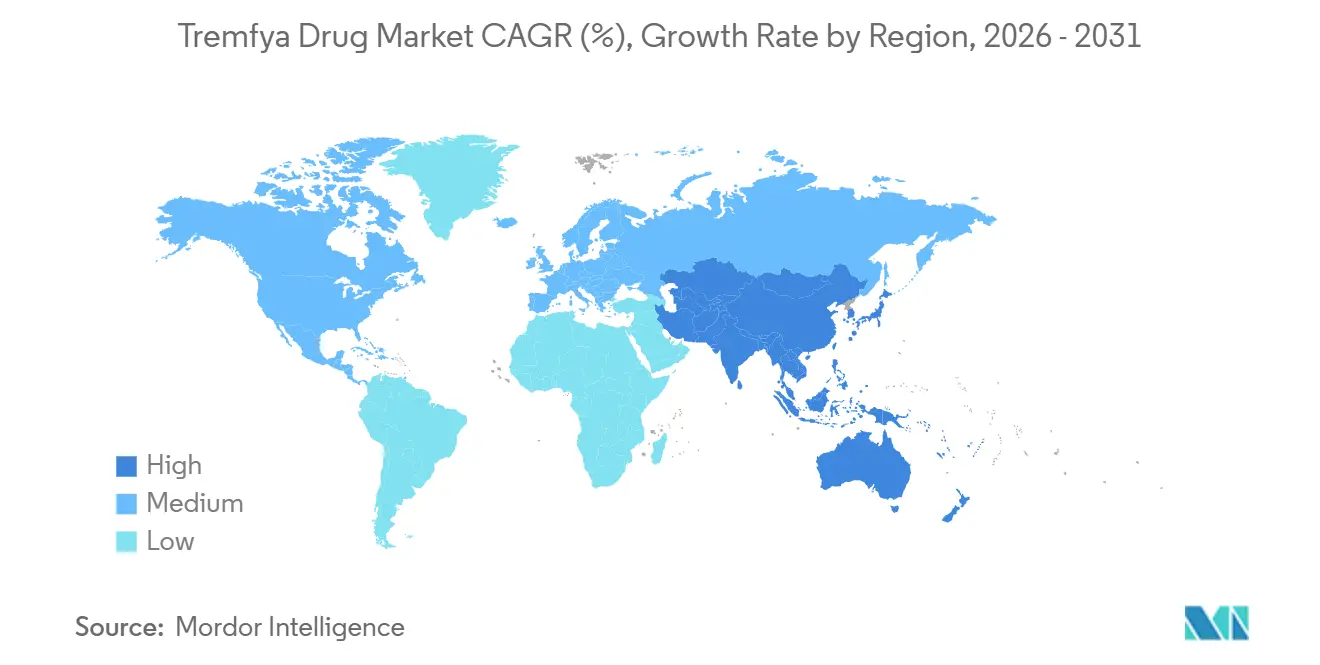

- By geography, North America held 42.22% of the Tremfya drug market share in 2025, while Asia-Pacific is expected to expand at a 10.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tremfya Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Label Into Inflammatory Bowel Disease | +2.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Durable IL-23 Differentiation Versus Legacy Biologics | +1.5% | Global | Medium term (2-4 years) |

| Pediatric and Multi-Label Expansion Supports Longer Lifecycle | +1.0% | North America, Europe | Medium term (2-4 years), Long term (≥ 4 years) |

| Site-of-Care Flexibility Improves Access and Persistence | +0.9% | Global | Short term (≤ 2 years) |

| Rising Demand for Endoscopic Remission in Biologic Sequencing | +0.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Specialty Pharmacy and Patient Support Programs Improve Uptake | +0.5% | North America (primary), Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Label Into Inflammatory Bowel Disease

The Tremfya drug market gained a wider clinical base when the FDA approved ulcerative colitis in September 2024 and Crohn's disease in March 2025, which moved guselkumab from a narrower immunology profile into a broader cross-specialty biologic position[1]Johnson & Johnson, “TREMFYA Receives U.S. FDA Approval for Adults with Moderately to Severely Active Ulcerative Colitis,” Johnson & Johnson Investor Relations, investor.jnj.com. The Tremfya drug market then gained support from the GALAXI-2 and GALAXI-3 Phase 3 results, which showed superiority versus ustekinumab across clinical remission, endoscopic response, and endoscopic remission at week 48 in Crohn's disease. That evidence matters because the Tremfya drug market is no longer competing only on class familiarity, and it now carries a head-to-head efficacy message in a setting where treatment sequencing often follows prior biologic exposure. The Tremfya drug market also benefits from the maintenance-phase pattern highlighted in the Crohn's disease positioning literature, where more than 90% of patients meeting primary endpoints did so without steroid dependence, a metric that aligns with the shift toward deeper disease control in gastroenterology. European approvals for ulcerative colitis in April 2025 and for Crohn's disease in May 2025 reduced the gap between the United States and Europe and supported a more synchronized international rollout of the Tremfya drug market. As a result, the Tremfya drug market is moving toward a revenue base that is less tied to plaque psoriasis alone and more balanced across chronic gastrointestinal use, where treatment duration and specialist follow-up are both structurally high.

Durable IL-23 Differentiation Versus Legacy Biologics

The Tremfya drug market retains a differentiated profile because guselkumab selectively inhibits the IL-23 p19 subunit and also binds CD64, which sets it apart from broader IL-12/23 and TNF-targeting biologics. The Tremfya drug market also carries the benefit of a longer commercial and clinical history in psoriasis, which gives prescribers years of familiarity in safety, persistence, and switching behavior. In moderate psoriasis with high-impact site involvement, the Phase 3b SPECTREM study showed that 74.2% of adults reached IGA 0/1 clearance on guselkumab versus 12.4% on placebo, which opens use earlier in the disease course for patients who were often left on repeated topical escalation. That earlier entry point matters because the Tremfya drug market can extend beyond severe cases and address patients whose disease burden is driven by location and daily impact rather than only by body surface area. The May 2026 FDA label expansion adds another clinical distinction because guselkumab is now the only IL-23 inhibitor with evidence of structural joint damage inhibition in active psoriatic arthritis. This keeps the Tremfya drug market relevant in rheumatology as well as dermatology, where prevention of radiographic progression carries long-term weight in treatment choice.

Pediatric and Multi-Label Expansion Supports Longer Lifecycle

The Tremfya drug market widened its lifecycle profile in September 2025 when the FDA approved guselkumab for children aged 6 years and older with moderate-to-severe plaque psoriasis and active psoriatic arthritis, marking the first pediatric indication for any IL-23 inhibitor. The European regulatory path continued in the same direction, as Johnson & Johnson submitted the EMA application in February 2025 and the European Commission later extended pediatric plaque psoriasis approval in December 2025. The Tremfya drug market gains durability from pediatric use because treatment tends to continue for longer periods in chronic immune diseases and approved alternatives are more limited in younger patients. Ongoing Phase 3 work in pediatric Crohn's disease and ulcerative colitis also supports a pathway where the Tremfya drug market could eventually span pediatric and adult IBD care within one mechanism and one brand family. The Tremfya drug market also benefits from referral continuity because a patient treated by a rheumatologist or dermatologist can remain on the same therapy if comorbid gastrointestinal disease later becomes part of care. That continuity lowers switching friction and gives the brand a broader role in long-term specialist management across immune-mediated disease.

Site-of-Care Flexibility Improves Access and Persistence

The Tremfya drug market stands out because guselkumab is the only IL-23 inhibitor with both subcutaneous and intravenous induction options in adult Crohn's disease, and that removes a historical access barrier tied to infusion-only starts. The GRAVITI study supported this advantage, with 56.1% of patients reaching clinical remission at week 12 versus 21.4% on placebo and 66.1% of the 200 mg SC every-4-weeks group reaching clinical remission at week 48 versus 17.1% on placebo. The Tremfya drug market saw the same pattern strengthen in ulcerative colitis when the ASTRO trial supported subcutaneous induction through 24 weeks and the FDA approved that option in September 2025. This matters operationally because the Tremfya drug market can reach patients who lack regular infusion-center access and can also fit provider settings without in-house infusion capacity. A wider subcutaneous pathway also changes channel economics in the Tremfya drug market because more prescriptions can move through specialty pharmacy workflows and home-delivery support rather than through hospital infusion billing. Over time, that flexibility should support initiation, adherence, and persistence across both academic and community care settings where infusion resources are uneven.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Biologic Pricing and Payer Prior Authorization Pressure | -1.8% | North America (primary), European markets with QALY-based reimbursement | Short term (≤ 2 years), Medium term (2-4 years) |

| Intensifying Competition From IL-23, IL-17, and TYK2 Therapies | -2.1% | Global | Short term (≤ 2 years), Medium term (2-4 years) |

| Complex Induction and Administration Pathways Create Adoption Friction | -0.8% | Emerging markets, community hospital settings | Medium term (2-4 years) |

| Long-Term Biosimilar and Formulary Erosion Risk After Patent Cliff | -1.2% | Global, concentrated in North America and Europe post-2031 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Biologic Pricing and Payer Prior Authorization Pressure

The Tremfya drug market still faces access friction because guselkumab sits in the specialty biologic category, and coverage rules in that category are shaped by utilization controls and formal review pathways. In ulcerative colitis, UnitedHealthcare's commercial policy requires documented inadequate response to conventional therapy and or prior biologic or JAK inhibitor therapy before coverage is approved, which shows how restrictive entry can be even after label expansion. The Tremfya drug market therefore depends not only on physician preference but also on how quickly clinics can gather records, submit authorizations, and respond to follow-up payer requests. That burden is heavier in community practices than in large academic centers, so the Tremfya drug market can see slower real-world starts than trial data alone would suggest[2]UnitedHealthcare, “Commercial and Individual Exchange Medical Benefit Drug Policy, Tremfya (Guselkumab),” UnitedHealthcare, uhcprovider.com. These delays matter because treatment initiation and persistence are closely linked in chronic immune disease, especially when patients are moving across prior therapies and complex benefit designs. As a result, payer management remains one of the clearest near-term limits on how quickly the Tremfya drug market can convert new approvals into realized prescribing volume.

Intensifying Competition From IL-23, IL-17, and TYK2 Therapies

The Tremfya drug market operates in a crowded immune-mediated treatment setting where competing IL-23 products are already established in psoriasis and IBD, and that keeps new patient capture contested across specialties. The launch environment changed again in March 2026 when icotrokinra became the first oral IL-23 receptor antagonist approved for psoriasis, giving prescribers an oral option within the same broader pathway focus. The Tremfya drug market is therefore exposed to a substitution risk in moderate plaque psoriasis, where convenience and route preference can influence early prescribing patterns even when biologic efficacy remains strong. Competition also extends beyond IL-23 because IL-17 and TYK2 therapies continue to shape formulary discussions and sequencing decisions in dermatology, which limits how much of the Tremfya drug market can be won through class presence alone. In IBD, the Tremfya drug market still needs to earn share in a multi-product prescribing environment, so strong clinical differentiation does not automatically translate into unrestricted first-line use. This leaves the Tremfya drug market in a position where brand growth is likely to depend on label depth, route flexibility, and sequencing relevance rather than on mechanism novelty alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: IBD Expansion Rebalances the Revenue Mix

Plaque psoriasis accounted for 86.31% of the Tremfya drug market in 2025, which shows how strongly the brand was still anchored in dermatology before the newer gastrointestinal approvals began to scale. That concentration was supported by long-standing formulary familiarity, broad specialist use, and guideline recognition in psoriasis care, which gave the Tremfya drug market a durable base before IBD started contributing meaningful incremental volume. Psoriatic arthritis remained the second-largest application and gained added importance in May 2026, when the FDA label was expanded to include structural joint damage inhibition in active disease. That label depth matters for rheumatologists because long-term management is shaped not only by symptom control but also by protection against irreversible radiographic progression. Crohn's disease is the fastest-growing application and is forecast to expand at an 11.38% CAGR through 2026-2031, supported by the March 2025 FDA approval, the May 2025 European Commission authorization, and the week 48 GALAXI results against ustekinumab.

Ulcerative colitis remains the third application by current revenue contribution, and its profile strengthened after the FDA first approved IV induction in September 2024 and later approved the subcutaneous induction option in September 2025. Long-term support for that application is visible in the QUASAR extension, where maintenance regimens sustained symptomatic, endoscopic, and histologic efficacy through week 92, which helps the Tremfya drug industry build confidence beyond the induction window. Other approved uses, including palmoplantar pustulosis and erythrodermic psoriasis in Japan, continue to add a smaller but stable revenue layer to the Tremfya drug market. Over the forecast period, the Tremfya drug market is likely to show a lower dependence on plaque psoriasis alone as Crohn's disease and ulcerative colitis move from early specialist adoption into broader community gastroenterology practice. That mix shift supports volume growth, but it also exposes the brand to a more step-therapy-intensive payer environment and a different balance between medical-benefit and pharmacy-benefit reimbursement.

By Route of Administration: SC Dominates, IV Gaining in IBD Induction

Subcutaneous injection held 65.24% of the Tremfya drug market in 2025, reflecting its established role in maintenance therapy across indications and its dominant position in plaque psoriasis and psoriatic arthritis care. The route has practical advantages because prefilled syringes, the TREMFYA PEN, and the One-Press injector all support home use and reduce the need for repeated clinic visits in long-term treatment. That convenience keeps the Tremfya drug market aligned with patient preference in chronic dermatology and rheumatology management, where continuity and self-administration often matter as much as efficacy. Intravenous infusion remains the smaller route today, but it is the fastest-growing segment at a 10.52% CAGR through 2026-2031 because induction in IBD still begins in hospital-linked infusion settings for many moderate-to-severe patients. The Tremfya drug market therefore shows a two-speed route structure, where mature skin and joint indications support subcutaneous volume while new IBD use lifts intravenous growth.

A key structural change is the move from IV-only initiation toward IV-or-SC induction in ulcerative colitis and Crohn's disease, which widens the clinical settings where the Tremfya drug market can be started. The FDA approved SC induction for ulcerative colitis in September 2025, and the European Commission followed in October 2025, which gives community physicians a clearer path when infusion capacity is limited. The GRAVITI data also support fully subcutaneous induction and maintenance in Crohn's disease, which should gradually shift more of the Tremfya drug market toward home-based care in appropriate patients. Even so, intravenous induction is likely to retain a durable role in tertiary IBD centers, where complex patients and prior biologic failures still favor closely supervised initiation. This means the Tremfya drug market is likely to remain mixed by route even as the subcutaneous share rises over time.

By Distribution Channel: Hospital Anchor Meets Rising Digital Access

Hospital pharmacies held 52.52% of the Tremfya drug market in 2025, which reflects the importance of IV induction in IBD and the continued role of specialty-care settings in biologic prescribing. Their position is reinforced by bundled services such as prior authorization coordination, patient monitoring, infusion scheduling, and case management, which makes the Tremfya drug market operationally sticky in hospital-linked systems. Retail pharmacies remained the second-largest channel because subcutaneous maintenance in psoriasis and psoriatic arthritis shifts dispensing closer to the patient's home after the initial prescribing pathway is established. Online pharmacies are the fastest-growing distribution channel and are expected to expand at an 11.25% CAGR during 2026-2031 as home-delivery logistics and adherence support become more central to chronic biologic use. This shift means the Tremfya drug market is moving from a hospital-centered model toward a more distributed fulfillment pattern, especially as subcutaneous induction adds volume outside infusion-heavy settings.

In the United States, the Tremfya drug market already operates through a contracted Specialty Pharmacy Enhanced Services Network that includes AcariaHealth, Walgreens Specialty Pharmacy, BioPlus, and other partners that support adherence, reimbursement, and transfer requirements. That structure gives the brand a ready-made platform for pharmacy-benefit dispensing as more patients receive subcutaneous maintenance and, increasingly, subcutaneous induction. The Tremfya drug industry also reflects a dual-benefit architecture, because IV induction is tied more closely to the medical benefit while SC treatment is more likely to move through the pharmacy benefit. As SC induction grows, a larger share of the Tremfya drug market is expected to move toward specialty pharmacy channels, which raises the importance of formulary placement and payer contracting. Other distribution pathways remain smaller, but they still matter in markets where access depends on centralized procurement or government formulary listing rather than on open commercial dispensing.

Geography Analysis

North America retained 42.22% of the Tremfya drug market in 2025, and the region remains the largest geographic contributor because the United States secured early approvals across indications and has the deepest specialty pharmacy infrastructure in routine use[3]Johnson & Johnson, “Johnson & Johnson 2025 Annual Report,” Johnson & Johnson, jnj.com. The regional position of the Tremfya drug market is also supported by the TREMFYA withMe support model, which helps patients navigate affordability, onboarding, and adherence across chronic treatment cycles. Johnson & Johnson's 2025 annual report shows that Tremfya contributed materially to company revenue, which underlines how central the United States is to the global scale of the Tremfya drug market. Canada benefits from the brand's established psoriasis and psoriatic arthritis presence, while Mexico remains smaller because biologic penetration is still constrained by infrastructure and funding patterns. This leaves North America with the broadest commercial base in the Tremfya drug market, but it also leaves the region most exposed to prior authorization intensity and benefit-design complexity.

Europe is the second-largest regional block in the Tremfya drug market, and its position improved after the European Commission approved ulcerative colitis in April 2025, Crohn's disease in May 2025, SC induction in ulcerative colitis in October 2025, and pediatric plaque psoriasis in December 2025. The United Kingdom added a separate post-Brexit path when the MHRA approved guselkumab for Crohn's disease and ulcerative colitis in May 2025. The Tremfya drug market still faces a slower revenue conversion cycle in Europe because national HTA bodies and price negotiations can delay broad reimbursement even after regulatory approval. Even with that friction, Europe remains important because treatment goals in gastroenterology increasingly emphasize endoscopic remission, which fits the way the Tremfya drug market is being positioned in IBD.

Asia-Pacific is the fastest-growing geography in the Tremfya drug market and is forecast to expand at a 10.65% CAGR during 2026-2031 as recent approval milestones widen use beyond psoriasis into IBD. Japan is central to that pattern because it approved guselkumab for ulcerative colitis in March 2025, Crohn's disease in June 2025, and SC induction for ulcerative colitis in February 2026, which gives the Tremfya drug market a more complete route and indication profile in a major high-income market. China adds scale potential because guselkumab already has approval breadth across plaque psoriasis and IBD-related use, which supports longer-term expansion of the Tremfya drug market in a large treated population base. The Middle East and Africa remain early in adoption, with higher-income Gulf markets leading use while the rest of the region contributes limited volume. South America also remains smaller, but Brazil stands out in the Tremfya drug market because approvals in ulcerative colitis and Crohn's disease create a base for biologic use in gastroenterology. Taken together, these patterns show a market that is still led by North America, well supported by Europe, and most rapidly widened by Asia-Pacific.

Competitive Landscape

The Tremfya drug market is structurally concentrated around a single originator product because guselkumab is manufactured by Janssen Biotech. Even so, competition inside the Tremfya drug market is strong at the indication level because prescribing decisions in psoriasis, psoriatic arthritis, ulcerative colitis, and Crohn's disease are shaped by several mechanism-adjacent options. The Tremfya drug market therefore competes less on ownership of the product itself and more on how well guselkumab can defend its place against other IL-23, IL-17, and TYK2 pathways in each specialty setting. The GALAXI week 48 superiority data against ustekinumab strengthen the clinical narrative of the Tremfya drug market in Crohn's disease, but prescriber choice still depends heavily on local practice habits and prior sequencing patterns. That makes the Tremfya drug market clinically differentiated, but not insulated.

Therapeutic sequencing remains one of the more important competitive levers in the Tremfya drug market because real-world German claims data show that advanced IBD care often depends on sustained efficacy after prior anti-TNF exposure. Guselkumab fits that sequencing logic because the GALAXI program included biologic-naive and biologic-experienced patients, which supports use in later treatment lines as well as in newer starts. That is commercially relevant because the Tremfya drug market often has to work through payer step-therapy rules before a specialist biologic receives approval. In psoriasis, route of administration is becoming a sharper point of differentiation because oral IL-23 receptor antagonism is now available with icotrokinra, which changes the way some patients and prescribers may think about early-line treatment. The Tremfya drug market therefore sits in a competitive field where efficacy, route flexibility, and reimbursement access have to work together rather than as separate strengths.

Johnson & Johnson has responded with a series of strategic moves that deepen the Tremfya drug market rather than relying on the original psoriasis base alone. The March 2025 Crohn's disease approval gave guselkumab both SC and IV induction options, and the September 2025 ulcerative colitis update extended that same flexibility into another large IBD population. The September 2025 pediatric approvals and the May 2026 label expansion in psoriatic arthritis further widened the clinical reach of the Tremfya drug market across age groups and specialist priorities. At the portfolio level, Johnson & Johnson and Protagonist also opened an adjacent oral IL-23 channel with icotrokinra in 2026, which suggests the company is shaping multiple access points around the same pathway rather than relying on a single format. This keeps the Tremfya drug market well defended, but it also confirms that future growth will come from careful positioning, not from a lack of competition.

Tremfya Drug Industry Leaders

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The FDA approved a supplemental BLA to include evidence of structural joint damage inhibition in the guselkumab label for active PsA, establishing it as the only IL-23 inhibitor with this claim. The update was supported by data from the APEX trial, which enrolled more than 1,000 biologic-naïve PsA adults and demonstrated significantly lower radiographic progression versus placebo at 24 weeks, providing a durable product differentiation in the rheumatology prescribing setting.

- February 2026: Japan's PMDA approved the SC induction regimen of guselkumab for adults with moderately to severely active UC, extending the fully subcutaneous treatment option to Japan and making it the first IL-23 inhibitor in Japan to offer SC induction.

Global Tremfya Drug Market Report Scope

As per the scope of the report, Tremfya (guselkumab) is a prescription medication used to treat certain autoimmune conditions. It is a biologic drug that belongs to the class of monoclonal antibodies.

The segmentation of the Tremfya drug market is categorized by application, route of administration, distribution channel, and geography. By application, the market includes plaque psoriasis, psoriatic arthritis, ulcerative colitis, Crohn’s disease, and other applications. By route of administration, it is segmented into subcutaneous injection and intravenous infusion. By distribution channel, the market is divided into hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. By geography, the market covers North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Plaque Psoriasis |

| Psoriatic Arthritis |

| Ulcerative Colitis |

| Crohn's Disease |

| Other Applications |

| Subcutaneous Injection |

| Intravenous Infusion |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Plaque Psoriasis | |

| Psoriatic Arthritis | ||

| Ulcerative Colitis | ||

| Crohn's Disease | ||

| Other Applications | ||

| By Route of Administration | Subcutaneous Injection | |

| Intravenous Infusion | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in Tremfya sales through 2031?

Growth is being driven mainly by label expansion into ulcerative colitis and Crohn's disease, route flexibility across SC and IV induction, and broader use beyond dermatology into gastroenterology.

Which indication contributes the most to Tremfya revenue?

Plaque psoriasis remains the largest application and accounted for 86.31% of revenue in 2025, showing that dermatology still anchors current sales even as IBD use rises.

Which Tremfya route of administration is growing the fastest?

Intravenous infusion is the fastest-growing route with a 10.52% CAGR through 2031 because IBD induction still relies heavily on supervised hospital-based starts.

Why is North America leading Tremfya revenue?

North America held 42.22% in 2025 because of early approvals, strong specialty pharmacy infrastructure, and well-developed patient support and reimbursement pathways.

What is the main access barrier for Tremfya in the United States?

Prior authorization remains the clearest barrier, especially in ulcerative colitis, where coverage policies can require failure on earlier therapies before approval.

How is Johnson & Johnson defending Tremfya against newer IL-23 options?

The company is widening label depth with pediatric approvals, structural joint damage data in PsA, and flexible SC and IV induction, while also building a broader IL-23 portfolio through the oral agent icotrokinra.

Page last updated on: