Tafamidis Drug Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.12 Billion |

| Market Size (2031) | USD 7.77 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tafamidis Drug Market Analysis by Mordor Intelligence

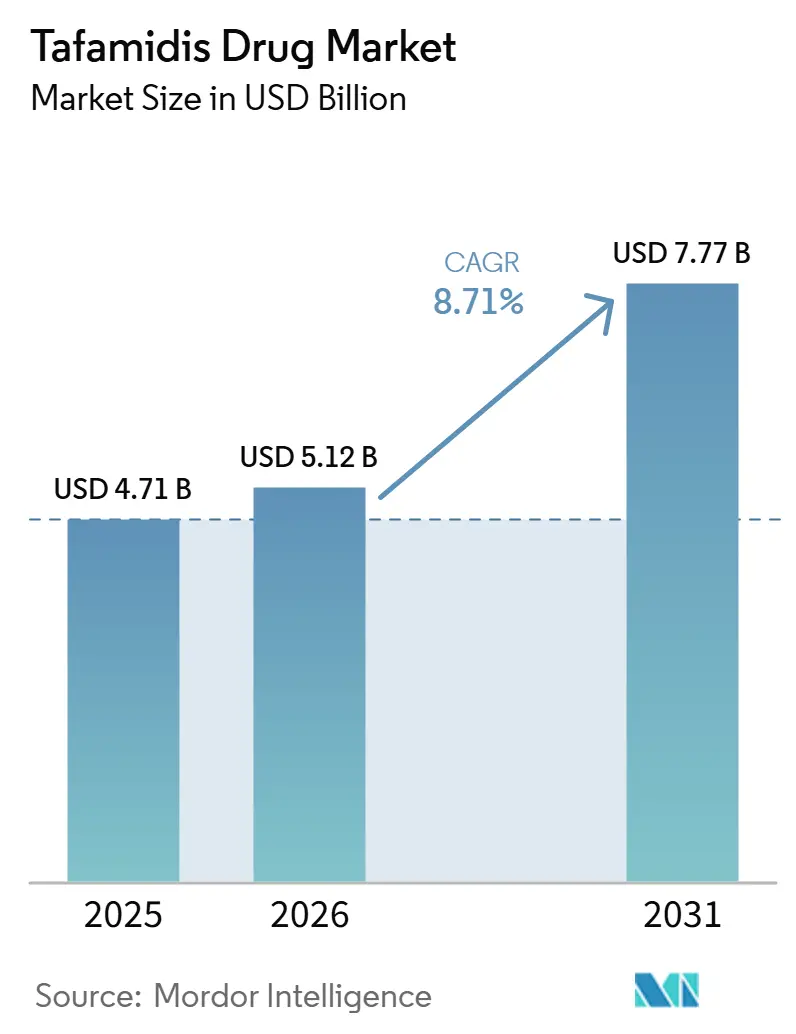

The Tafamidis Drug Market size is projected to expand from USD 4.71 billion in 2025 and USD 5.12 billion in 2026 to USD 7.77 billion by 2031, registering a CAGR of 8.71% between 2026 to 2031.

The tafamidis drug market is expanding because non-invasive diagnosis with technetium-99m pyrophosphate scintigraphy has widened the treated pool beyond hereditary disease and brought more older wild-type ATTR-CM patients into therapy pathways. Earlier identification is also pulling treatment initiation forward, which increases the time patients remain on therapy and supports steady prescription growth in the tafamidis drug market. The 2025 Medicare Part D redesign reduced patient out-of-pocket burden with a USD 2,000 annual cap, which improved access even though payer controls still shape the pace of uptake. Competitive pressure is now stronger as acoramidis and vutrisiran have entered ATTR-CM treatment, but Pfizer remains the scale leader and its April 2026 settlements keep effective U.S. patent protection for Vyndamax in place until June 1, 2031. The main limits on the tafamidis drug market remain the therapy’s high annual cost, strict prior authorization, rising competition from next-generation therapies, and expected price erosion after generic entry begins in mid-2031

Key Report Takeaways

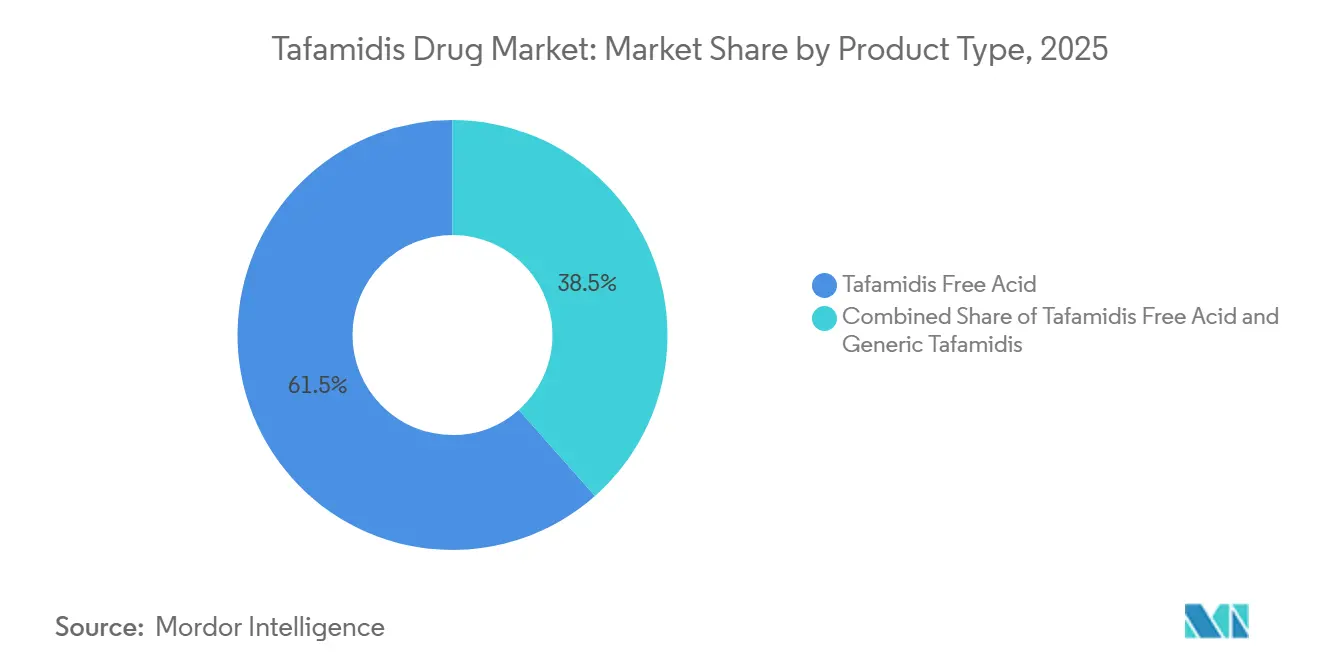

- By product type, tafamidis free acid held 61.53% of the tafamidis drug market share in 2025, while generic tafamidis is projected to expand at a 18.17% CAGR through 2031.

- By application, ATTR-CM accounted for 67.30% of the tafamidis drug market size in 2025, while mixed phenotype ATTR amyloidosis is forecast to grow at a 11.16% CAGR through 2031.

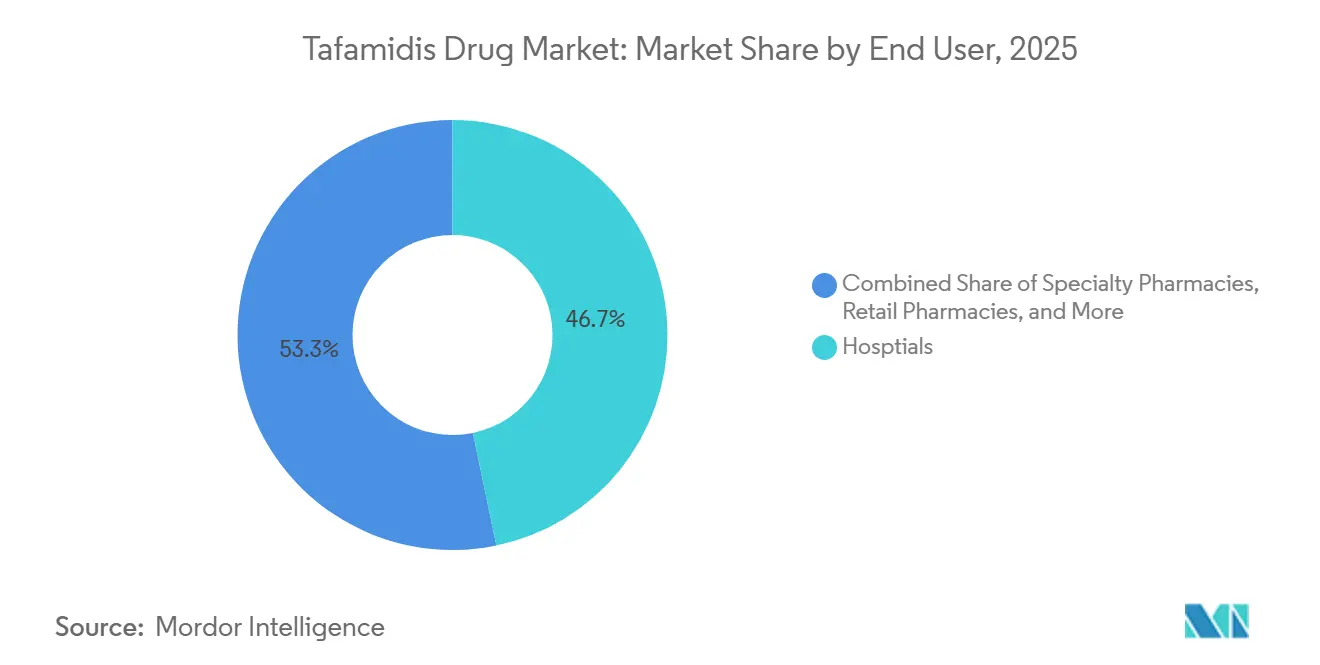

- By distribution channel, hospital pharmacies represented 46.73% of the tafamidis drug market in 2025, while specialty pharmacies are projected to advance at a 16.23% CAGR through 2031.

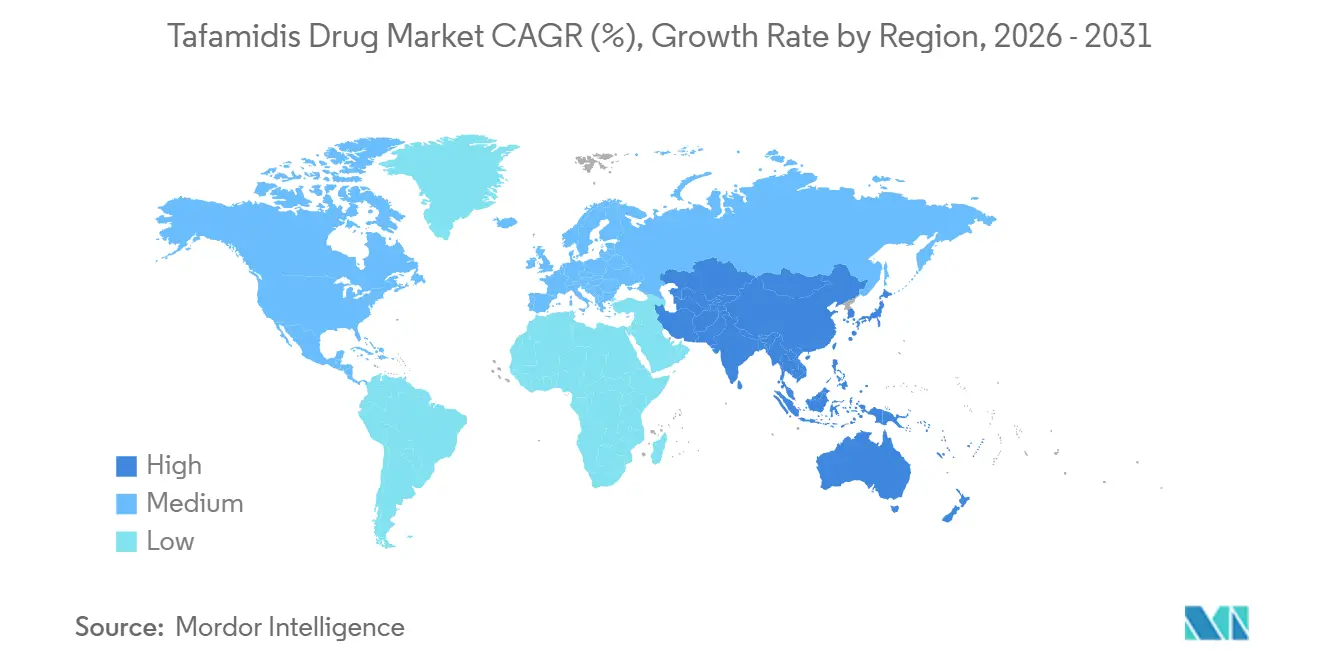

- By geography, North America held 39.37% of the tafamidis drug market in 2025, while Asia-Pacific is expected to register the fastest CAGR at 17.63% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tafamidis Drug Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diagnosis Of ATTR-CM Through Advanced Cardiac Imaging | +2.10% | Global, strongest in North America, Western Europe, and Japan | Short term (≤ 2 years) |

| Broader Cardiology Adoption Of Disease-Modifying Therapies | +1.80% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Aging Patient Pool And Higher ATTR-CM Prevalence In Older Populations | +1.50% | Global, concentrated in Japan, Germany, Italy, and South Korea | Long term (≥ 4 years) |

| Favorable Rare-Disease Access Pathways And Specialty Drug Programs | +1.00% | North America, with Medicare changes, and Europe under orphan drug frameworks | Short term (≤ 2 years) |

| Treatment Consolidation Around Once-Daily Oral Tafamidis | +0.90% | Global, strongest in high-income markets | Medium term (2-4 years) |

| Earlier Referral From Heart Failure Clinics To Amyloidosis Centers | +0.70% | North America and Europe, emerging in Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis Of ATTR-CM Through Advanced Cardiac Imaging

Non-invasive diagnosis using 99mTc-PYP and related bone scintigraphy has changed the way ATTR-CM is found in the tafamidis drug market. The 2025 epidemiology review showed rising incidence and prevalence across the United States and Europe, with especially strong growth among men older than 65 in countries with established scintigraphy use. U.S. incidence reached 44.3 per 100,000 person-years, which reflected better detection rather than a sudden change in underlying disease burden. This matters for the tafamidis drug market because imaging identifies more patients before advanced functional decline, which supports earlier treatment start. Earlier initiation tends to capture more NYHA Class I and II patients, and this group has been the clearest clinical fit for tafamidis use. The result is that the tafamidis drug market gains both a larger diagnosed base and a longer treatment window per patient.

Aging Patient Pool And Higher ATTR-CM Prevalence In Older Populations

The tafamidis drug market is closely tied to aging because wild-type ATTR-CM is concentrated in older adults[1]Source: Yun S. et al., “International Prevalence Of Transthyretin Amyloid Cardiomyopathy In High-Risk Patients With Heart Failure And Preserved Or Mildly Reduced Ejection Fraction,” Amyloid Journal of Protein Folding Disorders, openaccess.sgul.ac.uk. A 2024 international study showed that prevalence in high-risk HFpEF populations above age 85 reached or exceeded 40%, which confirms how strongly age drives case finding. Population aging across North America, Western Europe, and East Asia is therefore enlarging the diagnosis pool and sustaining demand for treatment. Japan stands out with documented ATTR-CM prevalence of 100 per million per year, and that disease burden has not yet been fully matched by prescription volumes because earlier eligibility rules were stricter. The 2025 revision of Japan’s Heart Failure Clinical Guidelines gave tafamidis a Class I, Evidence Level A recommendation for NYHA Class I and II ATTR-CM patients, which now supports wider use. This guideline shift should keep the tafamidis drug market on a firmer growth path in Japan over the medium term.

Broader Cardiology Adoption Of Disease-Modifying Therapies

Broader use by cardiologists is widening the prescribing base for the tafamidis drug market. HFpEF accounts for 50% of global heart failure cases, and ATTR-CM has been identified in 18% of high-risk HFpEF subgroups compared with 3% in unselected cohorts. This has pushed cardiologists to screen more routinely in patients with carpal tunnel history, bicuspid aortic stenosis, and unexplained concentric hypertrophy. The 2025 ACC concise clinical guidance placed TTR stabilizer therapy within standard management for confirmed ATTR-CM, which moved tafamidis further into mainstream cardiology protocols. Historical orphan-drug and breakthrough pathways also helped speed regulatory progress, while ongoing post-marketing monitoring continues to shape how manufacturers support distribution and access. As the referral barrier between general cardiology and specialist centers falls, the tafamidis drug market is reaching more patients without relying only on rare disease centers.

Earlier Referral From Heart Failure Clinics To Amyloidosis Centers

Earlier referral from heart failure clinics is shortening the path to treatment in the tafamidis drug market. Dedicated amyloidosis clinics now combine echocardiography, nuclear imaging, and genetic testing in a single care pathway, which reduces delays that used to occur in sequential workups. The Japanese claims study showed shorter diagnostic timelines when patients were managed at specialist centers with formal imaging protocols. Heart failure clinics are now acting as practical referral hubs for ATTR-CM cases that once might have remained misclassified in broader HFpEF populations. Patients often arrive at amyloidosis centers with preliminary imaging already completed, which allows a faster move from suspicion to prescription. That compression in time to therapy is supporting annual prescription growth in the tafamidis drug market, especially in tertiary hospitals and academic centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Annual Therapy Cost And Payer Prior Authorization Requirements | -1.50% | North America, strongest, and Europe to a lesser extent | Short term (≤ 2 years) |

| Generic Entry And Patent-Expiry Uncertainty | -1.20% | Global, concentrated in the United States after 2031 | Long term (≥ 4 years) |

| Diagnostic Delay And Misclassification Of ATTR-CM As Other Conditions | -0.70% | Global, acute in markets without scintigraphy infrastructure | Medium term (2-4 years) |

| Competitive Pressure From RNA-Silencing And Next-Generation Therapies | -1.10% | North America and Europe, expanding to Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Annual Therapy Cost And Payer Prior Authorization Requirements

High cost remains a direct limit on the tafamidis drug market even after recent access improvements. Tafamidis carries a U.S. list price of USD 234,900 per year, which places it among the most expensive cardiovascular therapies. Major payers require diagnosis confirmation, cardiology attestation, and functional assessment before they approve dispensing, and each plan has its own utilization rules. The 2025 Medicare Part D cap reduced patient financial burden, but some Medicare Advantage plans still placed Vyndamax in non-preferred specialty tiers, which kept plan-level friction in place. That means access barriers in the tafamidis drug market now come less from direct patient affordability and more from administrative delay, formulary placement, and documentation requirements. Appeals channels still exist for medically necessary treatment, but the prescriber burden remains significant and slows faster uptake.

Competitive Pressure From RNA-Silencing And Next-Generation Therapies

The tafamidis drug market is facing stronger competitive pressure from therapies that reduce TTR production rather than stabilize the protein. Alnylam’s Amvuttra received FDA approval for ATTR-CM in March 2025 and introduced a subcutaneous RNA interference therapy dosed every 3 months. In HELIOS-B, Amvuttra showed a 28% relative reduction in all-cause mortality and cardiovascular events versus placebo, which strengthened its case in ATTR-CM treatment. This creates a prescriber narrative that upstream TTR suppression may fit advanced disease or high amyloid burden better than stabilization alone. Next-generation RNAi candidates such as nucresiran are also being developed with twice-annual dosing and at least 95% TTR knockdown, which raises the competitive bar further. The pressure is strongest among new-to-therapy patients in the tafamidis drug market, where differentiation by mechanism, dosing frequency, and expected outcomes carries the most weight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tafamidis Free Acid Anchors Revenue as Generic Horizon Approaches

Tafamidis free acid held 61.53% of the tafamidis drug market share in 2025, which reflected the commercial strength of Pfizer’s once-daily Vyndamax and related brands in other countries. The single-capsule regimen offered a practical adherence advantage over the older four-capsule tafamidis meglumine presentation. Pfizer’s decision to discontinue Vyndaqel 20 mg in the U.S. by the end of 2025 further concentrated branded revenue around the free acid format. Tafamidis meglumine still retains relevance in markets where the free acid version has not secured local approval or where legacy patient cohorts remain established on older treatment protocols. A 2025 post-approval study in China showed that tafamidis free acid 61 mg delivered safety and efficacy findings consistent with international Phase 3 evidence, which supported confidence in markets absent from the original ATTR-ACT enrollment base[2]Springer Nature / Cardiology and Therapy. "Safety and Efficacy of Tafamidis in Chinese Patients with Transthyretin Amyloid Cardiomyopathy." 2025. https://link.springer.com/article/10.1007/s40119-025-00408-6.

The tafamidis drug market size for generic products is projected to expand at a 18.17% CAGR through 2031, making generic tafamidis the fastest-growing product segment. Indian manufacturers, including Dr. Reddy’s Laboratories, Aurobindo Pharma, Lupin, Torrent Pharmaceuticals, Sun Pharmaceutical Industries, and Zydus Lifesciences are building active pharmaceutical ingredient capabilities ahead of the June 2031 U.S. entry date tied to Pfizer’s settlements with Dexcel Pharma, Hikma Pharmaceuticals, and Cipla. Growth in this segment is expected to be uneven because some ex-U.S. markets can absorb generic tafamidis earlier under more favorable reimbursement settings, while the U.S. branded market remains protected until mid-2031. The molecule follows established organic chemistry routes, so price erosion after generic entry could be sharper than in rare-disease therapies with more complex manufacturing barriers. That outlook means the tafamidis drug market will likely see branded companies defend value through access execution, channel control, and clinical differentiation rather than formulation alone

By Application: ATTR-CM Dominates as Screening Expands Into Mainstream Cardiology

ATTR-CM accounted for 67.30% of the tafamidis drug market size in 2025, supported by broader recognition of wild-type disease in older cardiac patients. Non-invasive scintigraphy has made screening more practical in patients with HFpEF, carpal tunnel history, and unexplained ventricular thickening, which keeps ATTR-CM central to demand. The 2025 ACC clinical guidance reinforced tafamidis as a standard option in confirmed ATTR-CM management, which gives this segment a durable treatment anchor. Hereditary transthyretin amyloid polyneuropathy remains the second application segment because tafamidis had an earlier approval history in neuropathy than in cardiac disease across several markets. Familial amyloid polyneuropathy continues as a narrower niche in Portugal, Sweden, and Japan, where endemic TTR variants and long-standing registries sustain targeted use.

The tafamidis drug market size for mixed phenotype ATTR amyloidosis is forecast to expand at a 11.16% CAGR through 2031, making it the fastest-growing application segment. Current clinical literature places 24.5% of symptomatic ATTR patients in the mixed phenotype group, which means both cardiac and neurologic manifestations are present at the same time.. This subset has been underserved because treatment pathways often focused on either pure ATTR-CM or pure ATTR-PN rather than combined disease expression. Tafamidis aligns well with that need because systemic TTR stabilization can address both cardiac and peripheral manifestations within one therapeutic approach. As genetic sequencing and multimodal imaging sharpen phenotyping, the tafamidis drug market should see more newly identified mixed-phenotype patients enter treatment pathways.

By Distribution Channel: Hospital Pharmacies Lead While Specialty Channels Accelerate

Hospital pharmacies represented 46.73% of the tafamidis drug market in 2025 because diagnosis and treatment initiation were concentrated in tertiary hospitals, academic medical centers, and specialized amyloidosis programs. These sites handle the multidisciplinary workflow that typically includes cardiologists, neurologists, genetic counselors, and pharmacists, all of whom support documentation for payer approval. Hospital dispensing also fits renewal requirements because patients can be monitored more closely for hospitalization history, walking ability, and broader functional status. That operational fit keeps hospital pharmacies at the center of first-treatment use in the tafamidis drug market. Retail and online pharmacies still play a role, but most of that demand comes from stable maintenance patients who move out of hospital-based dispensing after treatment routines are established.

Specialty pharmacies are expected to record the fastest growth in the tafamidis drug market, at a 16.23% CAGR through 2031. Payer mandates for high-cost rare-disease drugs are a major reason, since many plans route dispensing through specialty pharmacy networks rather than general retail channels. These pharmacies also provide prior authorization support, adherence outreach, and patient assistance coordination, which directly reduces interruption risk. This channel is likely to become even more important as branded manufacturers prepare to defend retention and service quality in the years approaching generic competition. The others category remains relevant for institutional buyers, managed care direct-dispensing arrangements, and outpatient hospital programs that do not fit standard retail or specialty classifications.

Geography Analysis

North America held 39.37% of the tafamidis drug market share in 2025, making it the largest regional revenue base. The United States drove most of that demand because it has the deepest ATTR-CM diagnostic infrastructure, broad access to 99mTc-PYP scintigraphy, and the highest per-patient therapy spending. The 2025 Medicare Part D redesign improved patient affordability, but plan-level tiering still created friction in some Medicare Advantage settings. Canada and Mexico remain smaller contributors because reimbursement structures and specialist density are less favorable than in the United States. South America, led by Brazil and Argentina, supports demand through rare disease access programs and the presence of hereditary TTR variants in Portuguese-descended populations, which keep both ATTR-PN and ATTR-CM clinically relevant[3]Journal of the American Heart Association. "Temporal Trends in Incidence and Prevalence of Transthyretin Amyloid Cardiomyopathy in the United States." 2025. https://doi.org/10.1161/jaha.125.047135.

Europe remains the second-largest geography in the tafamidis drug market, with Germany, the United Kingdom, France, Italy, and Spain forming the core base. The European Commission approval of Beyonttra in February 2025 introduced direct TTR stabilizer competition, which will shape prescribing and pricing decisions more actively through 2031. Tafamidis still benefits from physician familiarity and from reimbursement frameworks that are already established with major health technology assessment bodies. Portugal and Sweden maintain a distinct neuropathy patient base linked to endemic TTR variants, while the rest of Europe offers incremental growth as diagnosis spreads beyond Western European specialist centers.

Asia-Pacific is the fastest-growing region in the tafamidis drug market and is forecast to expand at a 17.63% CAGR over 2026-2031. Japan has the highest documented ATTR-CM prevalence at 100 per million per year, and the 2025 guideline revision is now improving the path to broader Vynmac use in NYHA Class I and II patients. China is strengthening its position as a growth market because post-approval data in Chinese patients supported the safety and efficacy of tafamidis free acid 61 mg. India, Australia, and South Korea should grow from a smaller base as access improves, especially once pricing becomes more compatible with reimbursement expansion. The Middle East and Africa still represent a small share of the tafamidis drug market, with demand centered in GCC countries and broader regional growth dependent on stronger scintigraphy capacity and specialist diagnosis pathways

Competitive Landscape

The tafamidis drug market moved from effective single-company dominance to a more contested branded field between November 2024 and March 2025. Pfizer still led clearly, with USD 6.38 billion in Vyndaqel family revenue in 2025 and 75% of global ATTR-CM prescription volume. Pfizer also strengthened its near-term position through April 2026 settlements with Dexcel Pharma, Hikma Pharmaceuticals, and Cipla, which keep effective U.S. protection for Vyndamax in place until June 1, 2031. BridgeBio’s Attruby entered with a branded stabilizer that emphasized near-complete TTR stabilization of at least 90%, giving physicians a differentiated clinical story within the same broad mechanism class. Alnylam’s Amvuttra is competing on an upstream RNA interference mechanism, which broadens treatment choice and increases pressure on the tafamidis drug market among newly diagnosed patients.

Mixed-phenotype ATTR amyloidosis remains an important white space in the tafamidis drug market because it sits between cardiac-only and neuropathy-only treatment approaches. Another opening lies in patients who are already diagnosed but remain untreated because access, referral, or documentation barriers still slow initiation. Artificial intelligence-enabled electrocardiogram screening is emerging as a practical tool to identify more ATTR-CM candidates inside large cardiology networks, which could expand the diagnosed pool further. Generic manufacturers including Hikma, Cipla, Dexcel, Aurobindo, Sun Pharma, Lupin, Torrent, and Zydus are also preparing manufacturing and launch readiness, which sets up the main post-2031 competitive event. AstraZeneca and Ionis are expected to report Phase 3 CARDIO-TTRansform data in the second half of 2026, which could add an antisense option and push competition further toward outcomes, dosing frequency, and route of administration.

Pfizer’s main strategic move has been to simplify its branded portfolio around once-daily Vyndamax while defending exclusivity through patent settlements, which keeps commercial focus tight in the tafamidis drug market. BridgeBio’s strategic move has been to pair U.S. commercialization with European expansion through Bayer and Japanese commercialization through AstraZeneca Rare Disease, which broadens reach without duplicating infrastructure in every market. Alnylam’s strategic move has been to reinforce Amvuttra with updated HELIOS-B data and to outline the TRITON-CM Phase 3 path for nucresiran, which signals a longer pipeline push beyond a single product cycle. These moves show that the tafamidis drug market is no longer defined only by brand familiarity and now depends more on evidence, access execution, and channel strategy.

Tafamidis Drug Industry Leaders

-

Pfizer Inc.

-

BridgeBio Pharma, Inc.

-

Alnylam Pharmaceuticals, Inc.

-

Hikma Pharmaceuticals PLC

-

Cipla Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Adalvo is well-positioned for Day-1 launches of its generic Tafamidis 61 mg soft gel capsules, supported by a strong development and IP strategy. The company has been preparing for Day-1 launches in key European markets. It has navigated the CP and DCP submission process with precision, reflecting the exceptional quality of its Tafamidis dossier. With a robust IP strategy in place, Adalvo is among the few pharmaceutical companies with the technical capability and commercial readiness to deliver a partner-ready asset at launch.

- April 2026: Pfizer announced settlement agreements with Dexcel Pharma Technologies, Hikma Pharmaceuticals, and Cipla Ltd. regarding VYNDAMAX patent infringement litigation in the U.S. District Court for the District of Delaware. The settlements extend the effective U.S. patent expiry for VYNDAMAX to June 1, 2031. Pfizer now expects U.S. Vyndamax revenues to remain "relatively stable" from 2028 through mid-2031, revising earlier projections of significant revenue decline beginning in 2028-2029.

Global Tafamidis Drug Market Report Scope

As per the scope of the report, tafamidis is a transthyretin (TTR) stabilizer used for the treatment of transthyretin amyloidosis (ATTR amyloidosis), a rare progressive disease characterized by the misfolding and accumulation of transthyretin protein in tissues, particularly the heart and peripheral nerves. Tafamidis works by stabilizing the transthyretin tetramer, thereby preventing amyloid fibril formation and slowing disease progression.

The Tafamidis Drug Market is segmented by product type into Tafamidis Meglumine, Tafamidis Free Acid, and Generic Tafamidis; by application into Transthyretin Amyloid Cardiomyopathy (ATTR-CM), Hereditary Transthyretin Amyloid Polyneuropathy (ATTR-PN or hATTR-PN), Familial Amyloid Polyneuropathy (FAP), and Mixed Phenotype ATTR Amyloidosis; by distribution channel into Hospital Pharmacies, Specialty Pharmacies, Retail Pharmacies, and Online Pharmacies; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Tafamidis Meglumine |

| Tafamidis Free Acid |

| Generic Tafamidis |

| Transthyretin Amyloid Cardiomyopathy (ATTR-CM) |

| Hereditary Transthyretin Amyloid Polyneuropathy (ATTR-PN or hATTR-PN) |

| Familial Amyloid Polyneuropathy (FAP) |

| Mixed Phenotype ATTR Amyloidosis |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Tafamidis Meglumine | |

| Tafamidis Free Acid | ||

| Generic Tafamidis | ||

| By Application | Transthyretin Amyloid Cardiomyopathy (ATTR-CM) | |

| Hereditary Transthyretin Amyloid Polyneuropathy (ATTR-PN or hATTR-PN) | ||

| Familial Amyloid Polyneuropathy (FAP) | ||

| Mixed Phenotype ATTR Amyloidosis | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the tafamidis drug market?

The tafamidis drug market size is estimated at USD 5.12 billion in 2026 and is forecast to reach USD 7.77 billion by 2031 at a 8.71% CAGR.

Which application generates the most revenue for tafamidis?

ATTR-CM is the leading application, accounting for 67.30% of revenue in 2025 because diagnosis has expanded rapidly in cardiac care settings.

Which product type leads sales in tafamidis therapy?

Tafamidis free acid led with 61.53% revenue share in 2025, supported by the once-daily Vyndamax format and the shift away from the older meglumine version.

Which region is growing fastest for tafamidis treatment demand?

Asia-Pacific is the fastest-growing region, with a projected 17.63% CAGR through 2031, driven by Japan, China, and improving access in other regional markets.

Why are hospital and specialty pharmacies important in this space?

Hospital pharmacies led with 46.73% share in 2025 because initiation usually starts in specialist centers, while specialty pharmacies are growing fastest at 16.23% CAGR due to payer mandates and access support services.

What is the biggest competitive threat to tafamidis over the next few years?

The strongest pressure comes from RNA-silencing and next-generation therapies such as Amvuttra and nucresiran, along with generic entry expected after mid-2031.

Page last updated on: