Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

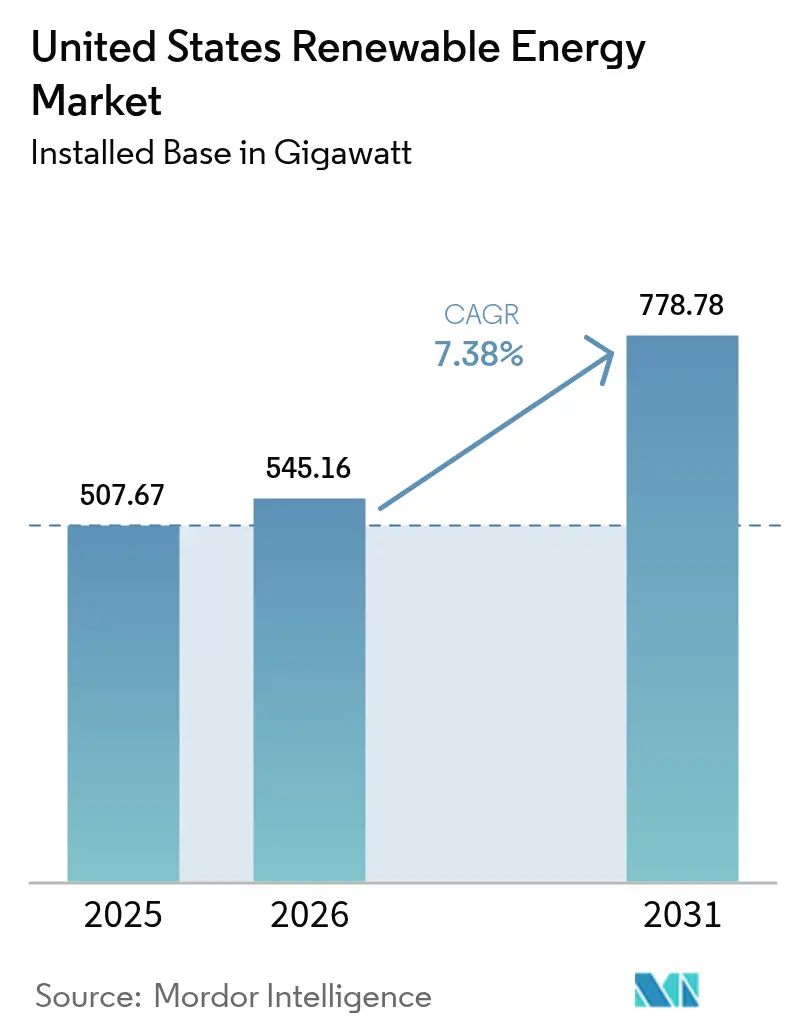

| Base Year Market Size (2025) | 507.67 gigawatt |

| Market Volume (2026) | 545.16 gigawatt |

| Market Volume (2031) | 778.78 gigawatt |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Renewable Energy Market Analysis by Mordor Intelligence

The United States Renewable Energy Market size was valued at 507.67 gigawatt in 2025 and estimated to grow from 545.16 gigawatt in 2026 to reach 778.78 gigawatt by 2031, at a CAGR of 7.38% during the forecast period (2026-2031).

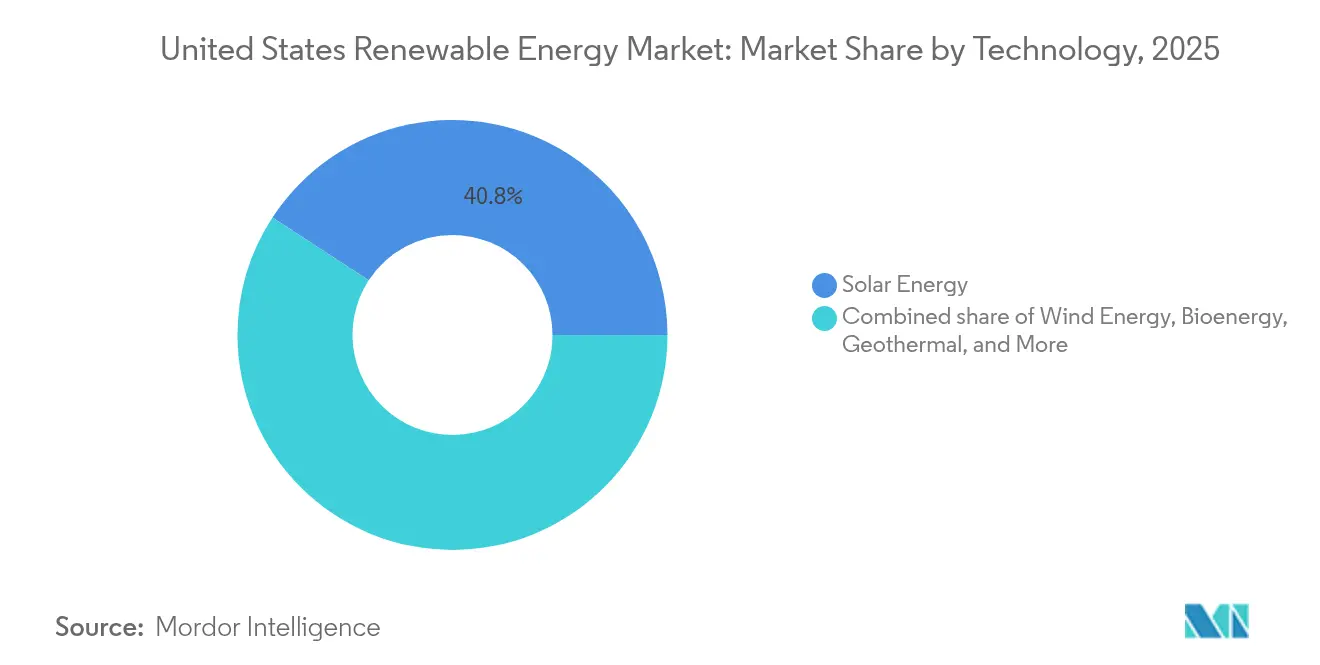

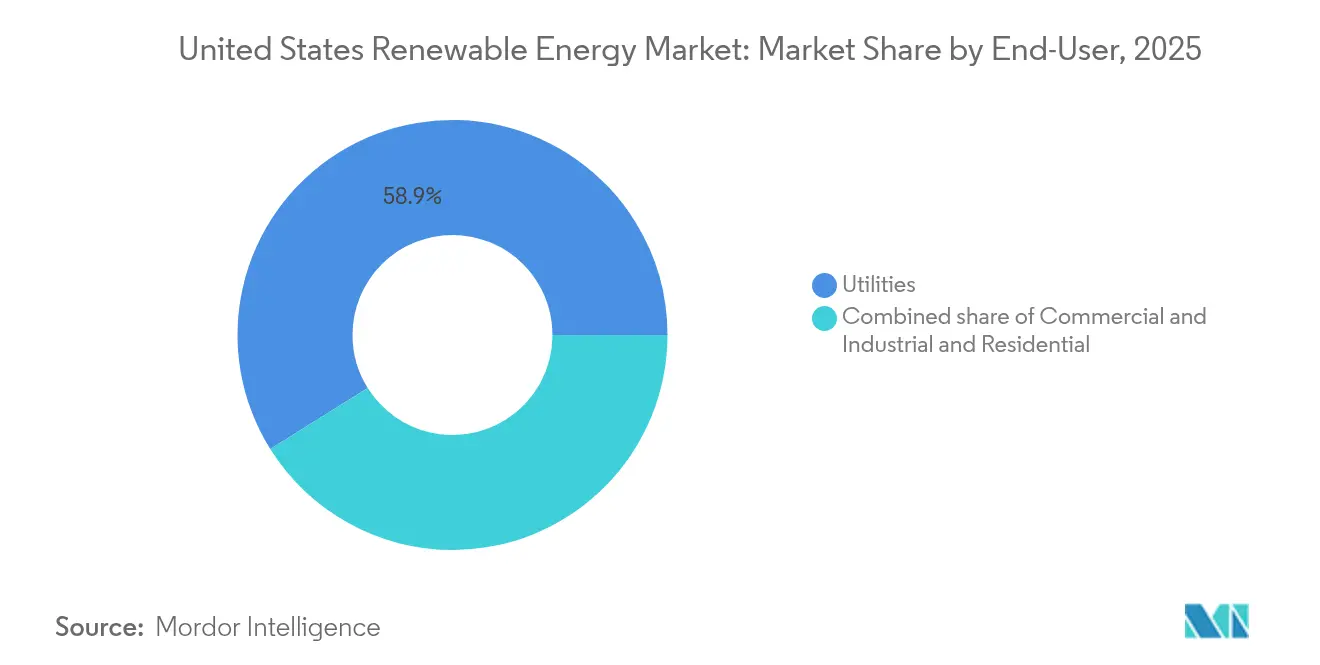

Federal incentives under the Inflation Reduction Act, steep cost declines in solar photovoltaic and wind equipment, and record-high corporate clean-electricity commitments are driving an investment cycle that no longer depends solely on subsidies. Transmission reforms, battery-plus-renewable project structures, and domestic manufacturing expansion further strengthen the economics of the US renewable energy market. Solar holds the leading 41.2% technology share, while wind remains a foundational resource, and storage solutions accelerate grid flexibility. Utilities still dominate installed capacity, yet distributed resources in homes and businesses grow quickly, reshaping revenue models and spurring service innovation across the US renewable energy market.

Key Report Takeaways

- By technology, solar commanded 40.80% of the US renewable energy market share in 2025 and is projected to grow at a 12.05% CAGR through 2031.

- By end-user, utilities held a 58.90% revenue share of the US renewable energy market size in 2025, while the residential segment is expected to advance at a 13.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extension of Federal Investment & Production Tax Credits | +1.20% | National, with concentrated benefits in high-solar states | Medium term (2-4 years) |

| Rapid Decline in Solar-PV & Wind LCOE | +1.60% | National, with regional variations based on resource quality | Long term (≥ 4 years) |

| Corporate Net-Zero & RE100 Procurement Targets | +1.40% | National, concentrated in corporate headquarters regions | Medium term (2-4 years) |

| Inflation Reduction Act–linked Manufacturing Upswing | +0.90% | Regional, focused on manufacturing hub states | Long term (≥ 4 years) |

| Grid-enhancing Technologies enabling higher renewable penetration | +0.80% | National, with priority in high-renewable penetration states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extension of Federal Investment & Production Tax Credits

Long-term certainty through 2032 for the 30% investment tax credit on solar and USD 26 per MWh production tax credit for wind keeps the US renewable energy market on a steady build schedule, avoiding the historical boom-bust pattern.(1)U.S. Department of Energy, “Inflation Reduction Act 2022 Resources for Solar,” energy.govDomestic-content bonuses lift effective credits by 10 percentage points and have already encouraged a 40% increase in US solar panel output during 2024. Layered manufacturing credits, worth up to USD 0.07 per watt for solar cells, further improve project economics and anchor new factories in traditional industrial states, broadening the tax base benefits of the US renewable energy market.

Rapid Decline in Solar-PV & Wind LCOE

Utility-scale solar reached USD 0.048 per kWh and onshore wind USD 0.033 per kWh in 2024, both undercutting combined-cycle gas prices without subsidies.(2)National Renewable Energy Laboratory, “2024 Annual Technology Baseline,” nrel.gov Larger turbines, high-density cell architectures, and supply-chain optimization compress capital costs, while energy storage attachments convert variable output into dispatchable power. Corporate buyers treat these falling prices as a hedge against fossil-fuel volatility, adding momentum to the US renewable energy market’s project pipeline and creating predictable revenue streams for investors.

Corporate Net-Zero & RE100 Procurement Targets

Corporate contracts totaled 23.7 GW in 2024 as more than 400 companies adopted net-zero or RE100 pledges. Technology firms, Amazon, Meta, and Google, signed agreements for over 8 GW, pioneering 24/7 carbon-free supply models. Virtual power purchase agreements now dominate transaction structures, allowing off-take buyers to acquire new capacity anywhere on the grid and amplifying diversity in the US renewable energy market’s customer mix.

Inflation Reduction Act-linked Manufacturing Upswing

Since 2022, announced clean-energy factory investments have exceeded USD 110 billion, doubling domestic solar panel capability to 15 GW and adding five nacelle assembly plants for wind technology.(3)Solar Energy Industries Association, “Solar Industry Research Data,” seia.org Battery gigafactory announcements covering 1,000 GWh per year reinforce local content requirements and shorten supply chains. These capital-intensive projects expand the skilled labor pool and reduce import dependencies, thereby reinforcing price stability across the US renewable energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission Bottlenecks & Interconnection Queues | -0.60% | National, concentrated in high-renewable resource regions | Short term (≤ 2 years) |

| Volatility in Commodity Prices for Turbines & Panels | -0.50% | National, with supply chain concentration risks | Medium term (2-4 years) |

| Community Opposition to Utility-Scale Projects | -0.30% | Regional, focused on rural development areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transmission Bottlenecks & Interconnection Queues

The interconnection backlog hit 2.6 TW by 2024, quadrupling 2020 levels and delaying projects by 4-5 years. Although FERC Order 2023 imposes cluster-study rules and commercial readiness screens, most pending applications still face network upgrades valued at more than USD 1 million per MW. The Great Plains, rich in wind, sees development stymied without conduits to load centers, resulting in trimmed near-term additions in the US renewable energy market.

Volatility in Commodity Prices for Turbines & Panels

Polysilicon price swings of up to 300% between 2020 and 2024, along with steel cost fluctuations of 15-25%, add to financing uncertainty. Supply-chain concentration poses geopolitical risks, while spikes in copper and rare-earth metals weigh on offshore wind foundations and permanent-magnet generators. Domestic content rules mitigate exposure, but the US renewable energy market anticipates another three years before a fully localized supply meets volume demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Dominance Accelerates Grid Integration

Solar technology accounted for 40.80% of the US renewable energy market share in 2025 and is projected to grow at the fastest rate, with a 12.05% CAGR, to 2031. Pairing with batteries means that 85% of new utility solar installations include storage, turning midday generation into peaking capacity and raising revenue certainty. Agrivoltaics blends crop production and photovoltaics, easing land constraints while improving farmer economics. Wind still anchors many portfolios and benefits from taller towers and larger rotors that expand viable terrain. Offshore wind gains momentum through federal lease auctions and state solicitations totaling 15 GW. Hydropower and geothermal energy offer dependable capacity, yet resource limitations and higher upfront costs slow their relative advancement. Technology mix decisions now reflect grid-service value in addition to kilowatt-hour prices, reshaping investment logic inside the US renewable energy market.

The US renewable energy market size for solar alone is expected to reach 326.4 GW by 2031, while onshore wind is projected to expand to 253.1 GW amid regional transmission upgrades. Emerging resources, such as enhanced geothermal systems and marine energy, exhibit modest baselines, but pilot projects reveal scalability once costs are optimized. In aggregate, technology diversification cushions weather-related output swings and strengthens reliability as penetration rises beyond 50% in leading states.

By End-User: Residential Segment Disrupts Traditional Utility Model

Utilities still account for 58.90% of installed capacity in 2025, yet the residential slice is projected to grow at a 13.95% CAGR through 2031, marking the quickest ascent within the US renewable energy market. Residential rooftops are increasingly bundling batteries; 40% of 2024 installations did so, enabling homeowners to shift consumption and provide grid services. Community solar expands access for renters and properties unsuitable for traditional solar panels, adding 4 GW of subscriptions in 2024 alone. These trends shift the load away from utilities, prompting tariff redesigns and demand flexibility programs.

Commercial and industrial buyers secure long-dated contracts that lock in energy costs and hedge carbon exposure, collectively adding stability to the US renewable energy market size. Behind-the-meter systems cut peak-demand charges, while microgrid deployments enhance energy resilience. Utilities retain an advantage in large-scale procurement economics but must adapt to distributed asset orchestration and performance-based regulatory models that reward system-wide efficiency.

Geography Analysis

Regional performance highlights the diversity of resources across the US renewable energy market. Texas leads with more than 40 GW of combined wind and solar capacity, supported by competitive ERCOT market pricing and abundant land.Generation surpluses attract hydrogen pilot projects aiming to turn curtailed power into stored fuel. California generates 33% of its electricity from renewable sources and has installed 5 GW of utility-scale storage, demonstrating the high-penetration feasibility of this approach. Its experience shapes grid-planning norms nationwide as other states race toward similar targets.

The Southeast registers rapid gains as corporate procurement and solar economics converge. Florida utilities ordered 6 GW of new solar in 2024, and North Carolina’s favorable interconnection rules fostered 1.2 GW of customer-sited projects. In the Great Plains, resource-rich states like Kansas and Oklahoma wait on transmission corridors to export power eastward, while grid-enhancing technologies deliver interim relief. Federal infrastructure grants seed multi-state line proposals aimed at unlocking 30 GW of latent wind energy by 2030.

Offshore wind is concentrated in the Northeast and Mid-Atlantic, where lease areas and load centers coincide. The Bureau of Ocean Energy Management authorized the first commercial project, the 132 MW South Fork Wind, in 2024, establishing operational proof-points. State-mandated solicitations exceed 25 GW through 2035, but supply-chain maturity and community outreach will determine pacing. Elsewhere, the Pacific Coast studies floating-turbine arrays that exploit deep-water wind, adding another growth frontier for the US renewable energy market.

Regulatory Landscape

Federal policy continues to anchor renewable project economics through long-dated tax incentives under the Inflation Reduction Act framework, including Investment and Production Tax Credit structures referenced in the report context (certainty through 2032). Grid integration policy also remains a binding factor, since FERC has been active on reliability and interconnection issues, with June 2026 remarks and actions aimed at multiple RTOs and ISOs in response to rapid large-load growth. That focus reinforces how transmission planning, queue management, and connection rules shape whether new renewable and storage additions can move from planning to operation.

On the federal demand and facilities side, the Department of Energy (DOE) has managed compliance timing for federal building clean-energy performance requirements by staying the compliance date until May 1, 2026, and then further staying it to September 1, 2026. DOE also issued a May 2026 final rule to rescind the Renewable Energy Production Incentives (REPI) program regulations (10 CFR part 451), effective at the end of FY 2026, while its FY 2026 budget request emphasizes R&D across geothermal, hydropower, biofuels, and advanced manufacturing, including support for the National Renewable Energy Laboratory and the EMAPS facility.

Competitive Landscape

The US renewable energy market shows moderate concentration as utilities, developers, and manufacturers blend roles to capture margin layers. NextEra Energy leads capacity ownership and leverages its regulated subsidiaries for stable cash flows, while deploying merchant assets to capture upside. Invenergy, Pattern Energy, and Clearway Energy specialize in project origination and long-duration contracts with corporate off-takers, demonstrating portfolio agility. Equipment makers such as First Solar expand into project development to secure panel demand, and Enphase Energy’s inverter data platforms enter the distributed asset aggregation market.

Partnership density grows, especially offshore. Ørsted collaborates with turbine maker GE Vernova and installation firm DEME to manage construction risk. Joint ventures streamline financing for multibillion-dollar arrays and resolve supply bottlenecks. Storage integrators now vie for hybrid bids, and software providers offer dispatch optimization as a competitive differentiator in the US renewable energy market.

M&A remains active. Brookfield Renewable bought 500 MW of operating solar assets from Trina Solar, and General Electric acquired LM Wind Power blades, shoring up domestic supply. Credit-rating upgrades for pure-play renewables, such as Pattern Energy’s 2024 jump to investment grade, lower borrowing costs, and widen institutional capital pools. Players capable of delivering grid services, navigating FERC reforms, and aligning with state clean energy standards gain a durable advantage.

United States Renewable Energy Industry Leaders

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy S.A.

First Solar Inc.

Sunrun Inc.

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Utility-scale build activity and the storage attach-rate point to clear whitespace in dispatchable renewable supply. Across the United States, 2025 utility-scale capacity additions reached 50.3 GW, with renewables and storage accounting for 90.5% of new capacity, and developer plans for 2026 follow the same direction (86 GW planned, led by solar and battery storage). This is creating demand for hybrid solar-plus-storage offerings, battery integration services, and grid-flexibility software that can capture value from capacity and ancillary services, particularly where interconnection queues and transmission upgrades compress time-to-power.

A second opportunity set is domestic manufacturing and supply-chain localization tied to federal incentives and corporate procurement structures. The report context notes more than USD 110 billion in announced clean-energy factory investments since 2022 and expanding US module and component capacity, while corporate contracting remains a major route-to-market (23.7 GW of corporate contracts in 2024). These factors support growth in bankable, long-duration offtake products, including 24/7 matching structures, alongside factory-linked demand for US-made modules, inverters, and balance-of-system components as developers and buyers manage commodity volatility and domestic-content provisions.

Recent Industry Developments

- July 2026: Sunrun launched a distributed compute pilot that places compute nodes in homes alongside distributed energy assets. The effort links data center and AI load growth to distributed resource orchestration, supporting the business case for residential solar-plus-storage and aggregation platforms.

- November 2025: First Solar announced a USD 330 million investment in a new 3.7 GW manufacturing facility in Gaffney, South Carolina. The added domestic module capacity supports IRA-linked supply-chain localization and improves procurement options for utility-scale developers seeking US-made equipment.

- December 2024: Orsted completed the 132 MW South Fork Wind project off Long Island, the first commercial-scale offshore wind installation in US federal waters. Operational delivery provided a reference point for permitting, construction logistics, and offtake structures for subsequent East Coast offshore wind projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market refers to renewable power capacity in the United States, counted as installed base that is connected to the grid and available to generate electricity from renewable sources.

Scope exclusions: This sizing does not count fossil-based generation, nuclear generation, or behind-the-meter assets that are not recorded in national capacity totals.

Segmentation Overview

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

Data Sources, Market Sizing, and Validation

Desk Research

We started by building a consistent fact base on US renewable electricity capacity, additions, and operating fleet because these are the inputs that are hardest to change later. Public datasets and filings were used to anchor the time series, then aligned to the same unit definition before any forecasting was attempted.

Key references included public sources such as the US Energy Information Administration, NREL publications, US Department of Energy program updates, FERC and ISO interconnection and queue disclosures, and US Census or trade statistics where equipment shipment patterns help explain build rates. We also used company annual reports, project announcements, and investor presentations, plus reputable press, to cross-check commissioning timing and the technology mix. For hard-to-find company financials, major project pipelines, and patent activity signals, we used a paid subscription database category that supports company intelligence and patent lookups. The desk research sources listed here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Our team validated the desk findings through expert interviews and structured surveys with developers, EPC and O&M participants, utility and C&I buyers, and domain specialists who track grid connections and permitting. Coverage was kept national, with input reflecting the main build hubs across APAC-linked supply chains, EMEA-linked financing and OEM footprints, and demand and policy signals across the Americas. When assumptions looked weak, such as commissioning delays or curtailment pressure, we re-contacted sources to confirm the most realistic range for the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | |

| Mid tier: 45% | Functional/Unit leaders: 41% | |

| Smaller Players: 16% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where national installed capacity series, technology additions, and retirements were reconstructed year by year, then converted into a single market total that stays consistent across sources. To keep the total realistic, we also ran selective bottom-up checks, including sampled project capacity rollups from pipelines and channel checks on commissioning cadence, and adjusted totals when gaps were repeatedly observed.

A few inputs mattered most, including annual capacity additions by technology, interconnection queue conversion rates, project COD slippage patterns, policy and incentive timelines, and grid constraints that can slow new builds. These indicators helped us decide when growth should be steady and when it should step up or cool down. For forecasting, scenario analysis was used, supported by expert views on permitting speed, supply chain tightness, and transmission availability, and then the final trajectory was chosen based on the most repeatable assumptions. Where bottom-up lists were incomplete, missing projects were handled through capacity-to-queue ratios and historical completion shares rather than forcing a full project-by-project build.

Data Validation & Update Cycle

We validated results by comparing the modeled capacity totals against independent signals, including publicly reported national capacity, annual build additions, and technology share trends, and then investigating any large year-to-year jumps that did not match observed project activity. Variance checks were done across unit definitions, commissioning timing, and technology classification so the totals did not mix incompatible series.

Before sign-off, a second analyst review is completed, followed by targeted re-checks when a data point is inconsistent with multiple sources. Reports are refreshed annually, and interim updates are made when material policy changes, major commissioning delays, or large pipeline shifts occur. Right before delivery, we scan the latest public releases again so the output reflects the most current view available.

Mordor Intelligence's United States Renewable Energy Market Estimate Compared With Other Published Estimates

It is common to see different market sizes for US renewable energy because publishers may measure different things, including installed capacity, electricity value, or investment and revenue tied to equipment and services. Timing also drives gaps, since the same year can look different if commissioning cutoffs, currency conversion dates, or inflation assumptions are handled differently.

Some published figures are value-based and may blend generation value, equipment sales, and related services into one total. In the Mordor Intelligence approach, the market size shown on the report page is expressed in installed capacity (GW) and is counted only for grid-connected renewable generation assets included in national capacity tallies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 507.67 B (2025) | |

| Global Consultancy A | USD 94.86 B (2024) | Uses USD value sizing that can reflect revenue or economic value across multiple renewable categories, so pricing, inflation, and what is monetized can shift the total away from a capacity-based count. |

| Industry Publisher B | USD 137.14 B (2024) | Reports a USD market value with a broader monetization lens and longer-horizon assumptions, which can embed aggressive price progression and include adjacent spend beyond installed generation capacity. |

The spread mainly comes from the unit of measurement and what is being monetized, not from disagreement that renewables are growing. When the goal is to track build-out, capacity in GW stays closely tied to measurable additions and retirements, which makes the steps easier to repeat and audit year to year.

Key Questions Answered in the Report

How large is the US renewable energy market in 2026?

Installed capacity is 545.16 GW in 2026 and tracking toward 778.78 GW by 2031, implying continued growth in 2026.

Which technology leads new capacity additions?

Solar accounts for 40.80% share and is expanding fastest at 12.05% CAGR through 2031.

What slows project completion timelines?

Transmission bottlenecks and a 2.6 TW interconnection queue add 4-5 years to schedules.

How do federal tax credits influence project economics?

Through 2032, 30% investment tax credits and USD 26 per MWh production credits cut upfront costs and raise returns.

Why are corporations signing renewable PPAs?

Long-term price certainty and net-zero commitments drove 23.7 GW of corporate contracts in 2024.

Is domestic manufacturing keeping pace with demand?

USD 110 billion of announced factories have doubled solar panel capacity to 15 GW and added new wind component plants.

Page last updated on: