Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

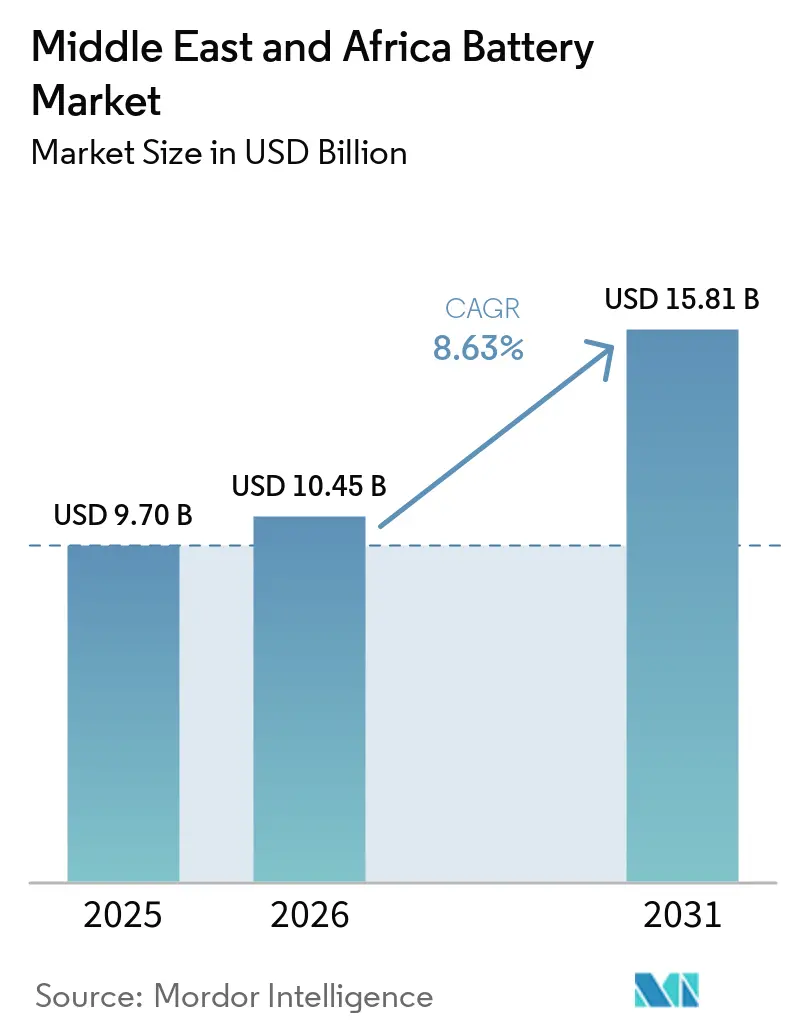

| Base Year Market Size (2025) | USD 9.70 Billion |

| Market Size (2026) | USD 10.45 Billion |

| Market Size (2031) | USD 15.81 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Battery Market Analysis by Mordor Intelligence

The Middle East and Africa Battery Market size is projected to expand from USD 9.70 billion in 2025 and USD 10.45 billion in 2026 to USD 15.81 billion by 2031, registering a CAGR of 8.63% between 2026 and 2031. Today, ambitious utility-scale storage procurements in the Gulf Cooperation Council and mini-grid programs across sub-Saharan Africa are accelerating demand, while gigafactory announcements in Saudi Arabia and Morocco signal the region’s transition from importer to producer.[1]Anu Bhambhani, “Middle East & Africa Solar PV News Snippets: ‘Record’ Energy Storage Costs At $73–75/kWh & More,” TaiyangNews, taiyangnews.info Falling lithium-ion pack prices, mounting grid-stability needs, and electric-vehicle (EV) uptake underpin near-term growth. At the same time, donor-backed concessional finance is de-risking early storage deployments in Egypt, Kenya, and Nigeria, and record-low installed costs of USD 73-75 per kilowatt-hour in Saudi tenders show that the Middle East and Africa battery market is approaching global cost benchmarks. Competitive pressure from Chinese cell makers and localization policies from Gulf sovereign wealth funds continue to compress margins but accelerate technology transfer.

Key Report Takeaways

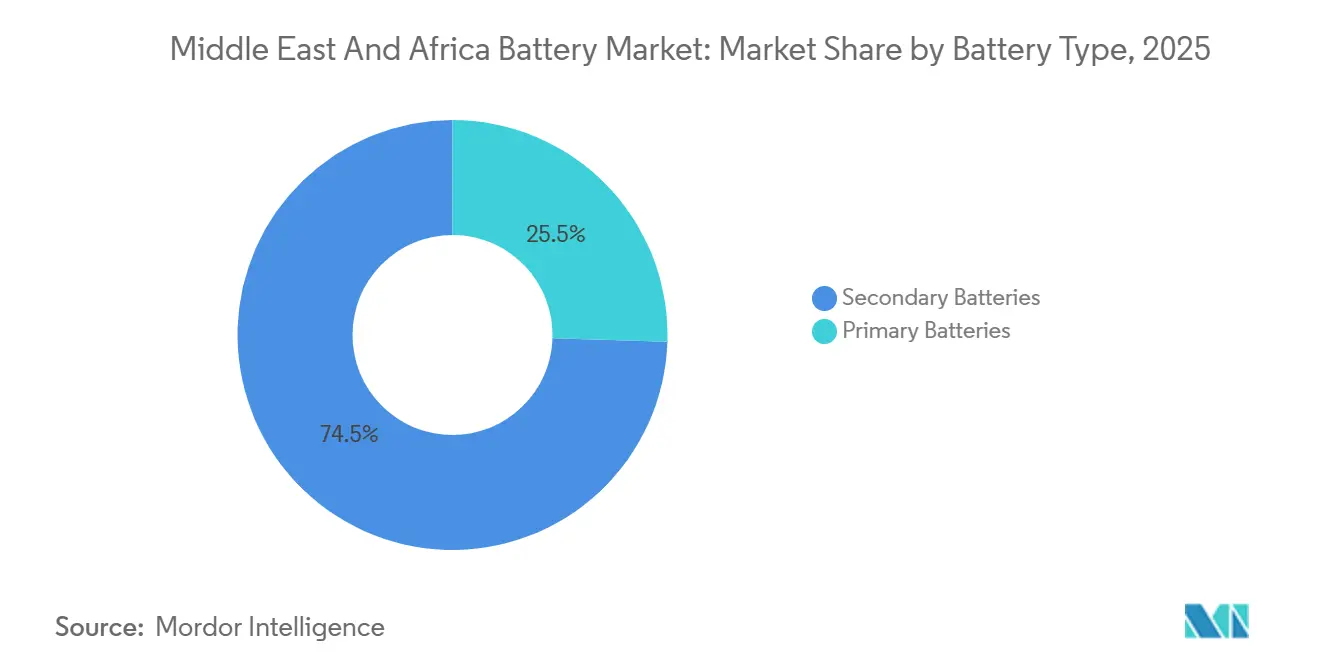

- By battery type, secondary batteries held 74.5% of the Middle East and Africa battery market share in 2025. Secondary batteries are forecast to expand at a 15.8% CAGR through 2031.

- By technology, lithium-ion captured 34.9% revenue share of the Middle East and Africa battery market size in 2025. Solid-state batteries are projected to grow at a 22.4% CAGR between 2026-2031.

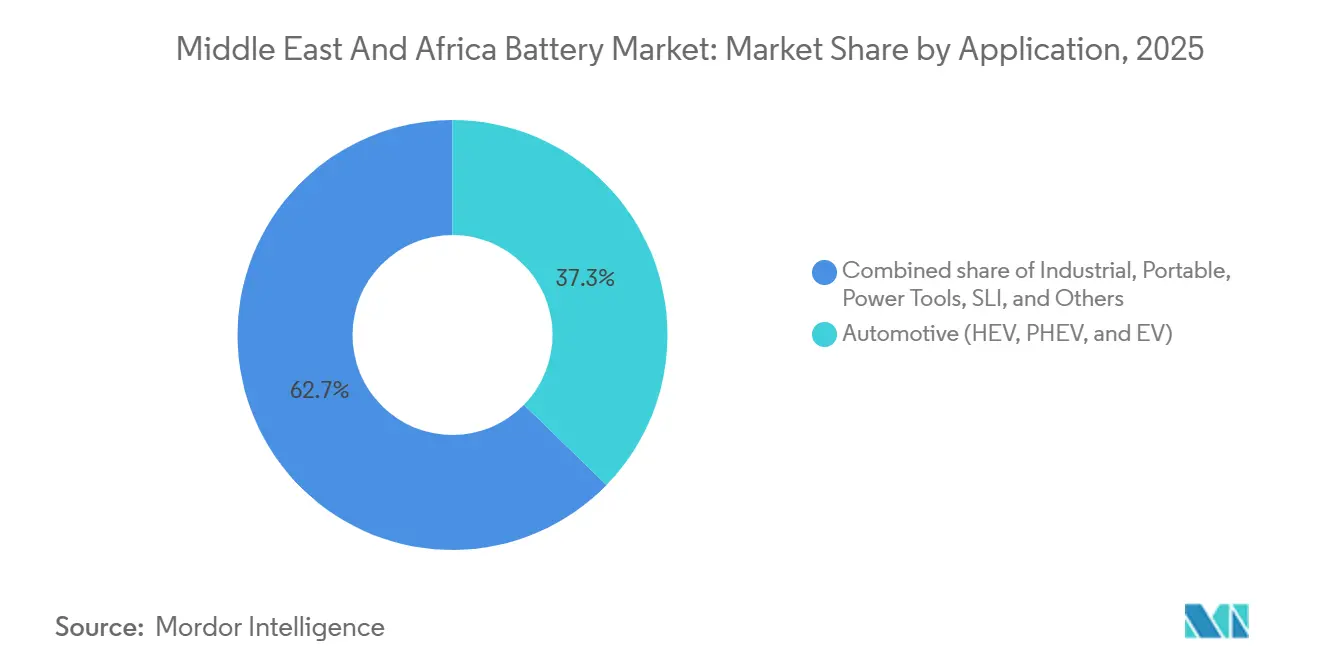

- By application, automotive batteries accounted for 37.3% of the Middle East and Africa battery market share in 2025. Industrial battery applications are set to post a 10.6% CAGR to 2031.

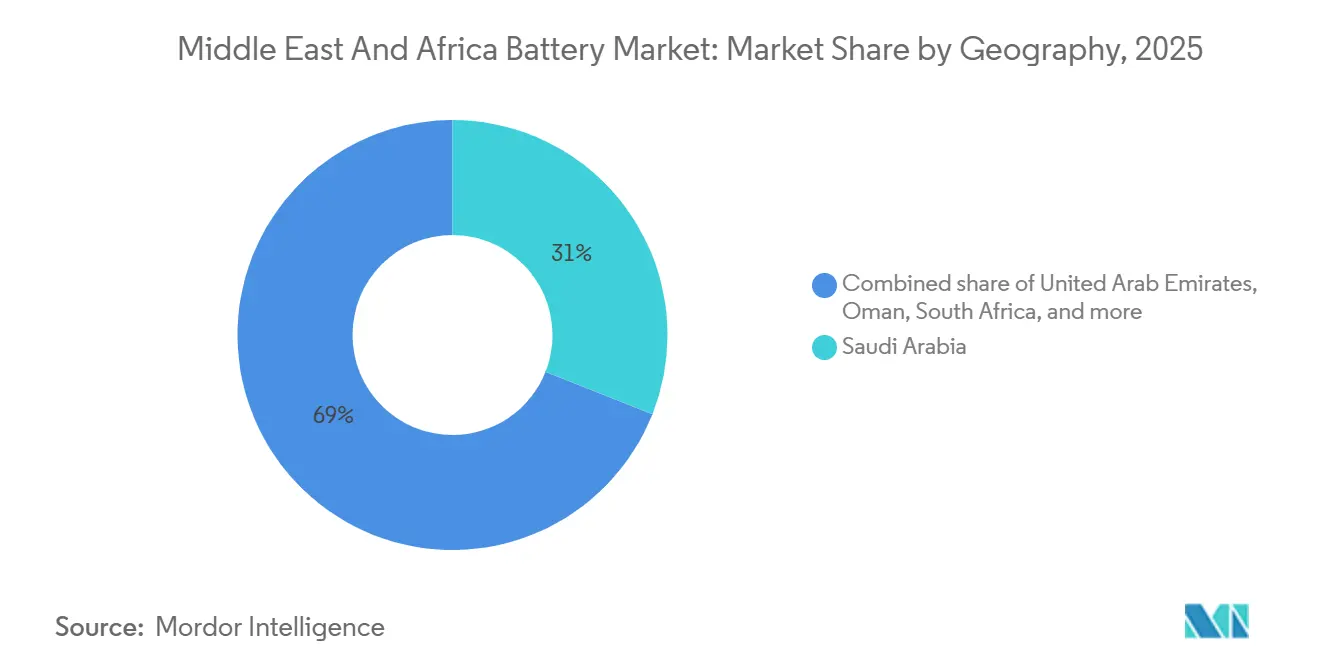

- By geography, Saudi Arabia led with 31.0% revenue share of the Middle East and Africa battery market in 2025. Oman is expected to register the fastest 14.7% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery prices | 2.10% | GCC, South Africa, pan-regional tenders | Short term (≤ 2 years) |

| Rapid EV adoption and GCC electrification targets | 1.80% | Saudi Arabia, UAE, Qatar, Egypt, Morocco | Medium term (2-4 years) |

| Distributed solar + storage uptake in off-grid Africa | 1.50% | Nigeria, Kenya, Ethiopia | Medium term (2-4 years) |

| Localization of cell and pack gigafactories | 1.30% | Saudi Arabia, Morocco | Long term (≥ 4 years) |

| Telecom-tower lithium retrofits | 0.90% | Nigeria, Kenya, South Africa, Egypt | Short term (≤ 2 years) |

| Grid unreliability driving lead-acid replacement | 0.70% | Nigeria, Egypt, Kenya, South Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Prices

Lithium-ion pack prices slid to USD 108 per kilowatt-hour in December 2025, down from USD 139 in 2023, narrowing the cost gap with lead-acid batteries and improving total-cost-of-ownership for telecom backup and four-hour utility storage.[2]BloombergNEF, “Battery Pack Prices in 2025,” about.bnef.com Saudi Arabia’s Tabuk and Hail projects set a regional record at USD 73-75 per kilowatt-hour by deploying HiTHIUM’s 1,175 Ah lithium-iron-phosphate (LFP) cells, underscoring how volume procurement and Chinese supply-chain scale pass through to buyers. Transparent tenders in GCC states and South Africa capture these savings immediately, while import duties and forex volatility moderate benefits in Kenya and Nigeria. Egypt’s 1.1 GW Obelisk solar-plus-storage project, financed by multilateral lenders, shows that LCOE parity with natural-gas peakers is within reach in high-insolation markets.[3]Sam Peters, “Solar and batteries could help Egypt beat its blackouts,” CNN, cnn.com Overall, falling pack costs reinforce the Middle East and Africa battery market’s path to scale, especially where subsidies or concessional debt further cut financing costs.

Rapid EV Adoption & GCC Electrification Targets

Saudi Arabia’s EV Green Initiative aims for 30% EV penetration in Riyadh by 2030, catalyzed by Ceer Motors and a Saudi Aramco-BYD manufacturing MoU. The United Arab Emirates targets a 20% EV share in Dubai and 10% in Abu Dhabi, with more than 740 public chargers already installed by late 2024. These mandates diversify oil economies and anchor new industrial value chains, lifting battery demand and prompting recycling investments. Qatar, Oman, and Egypt replicate the model on a smaller scale, while Morocco’s USD 346 million sovereign investment into Gotion’s Kenitra gigafactory underpins export-oriented battery output. EV growth, therefore, pulls forward local cell production, shortens supply lines to European OEMs, and embeds the Middle East and Africa battery market in global automotive platforms.

Distributed Solar + Storage Uptake in Off-Grid Africa

Nigeria’s Energy Transition Plan calls for 5 GW solar and 2.5 GW battery additions, backed by USD 3.6 billion raised so far and structured around mini-grids and solar-home-systems. Ethiopia’s DREAM program, funded by the African Development Bank, supports solar mini-grid irrigation with battery storage for 300,000 rural beneficiaries. Kenya’s World Bank-backed 100 MWh BESS due in 2026 complements geothermal and wind. These distributed models bypass transmission build-outs, delivering electricity within 18 months and unlocking productive evening loads. Affordability remains a hurdle, off-grid systems cost USD 225-400 per household versus willingness-to-pay below USD 150, but results-based financing and carbon-credit revenues close gaps. As cost curves decline, the Middle East and Africa battery market sees rising volumes from pay-as-you-go solar companies and donor-funded utilities.

Localization of Cell & Pack Gigafactories (KSA, Morocco)

Gotion High-Tech’s USD 1.3 billion first-phase gigafactory in Kenitra targets 20 GWh annual output from 2026, scaling to 100 GWh on a USD 6.5 billion budget. The project integrates cathode and anode lines, creates 17,000 jobs, and runs on dedicated wind power coupled with a 2 GWh storage plant. Saudi Arabia leverages a 2.5 GW/10 GWh tender pipeline to attract BYD and potential Aramco joint ventures, embedding manufacturing and R&D within its Vision 2030 framework. Localization locks in supply security, drives down landed costs, and positions the Middle East and Africa battery market as a hedge against tariff risks in Europe and North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material supply constraints (Li, Co) | -1.20% | Global, DRC cobalt focus | Medium term (2-4 years) |

| High upfront cost in price-sensitive African markets | -0.90% | Nigeria, Kenya, Ethiopia | Short term (≤ 2 years) |

| Weak recycling ecosystem and lead regulations | -0.60% | Region-wide | Long term (≥ 4 years) |

| Policy-incentive fragmentation | -0.50% | GCC, North Africa, sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Supply Constraints (Li, Co)

Lithium carbonate spot prices collapsed from USD 80,000 per ton in 2022 to USD 10,000 in 2024, then rebounded to USD 11,500 in early 2025, upsetting contract negotiations and squeezing manufacturer margins. Cobalt remains 70% concentrated in the Democratic Republic of Congo, raising ESG compliance costs under EU and U.S. battery rules. OEMs respond by pivoting to cobalt-free LFP chemistries, while Morocco leverages phosphate reserves for cathode precursors. Saudi Arabia and Oman explore lithium recovery from oil-field brines. Supply volatility, therefore, tempers but does not derail the Middle East and Africa battery market’s growth trajectory.

High Upfront Cost in Price-Sensitive African Markets

Per-capita GDP of USD 2,200 in Nigeria and USD 1,100 in Ethiopia limits commercial uptake beyond donor-backed or corporate use cases. Ethiopia’s National Electrification Program pegs off-grid system costs at USD 225-400 per household versus sub-USD 150 willingness-to-pay, requiring subsidy tenders. Concessional debt at 1.25% over 30 years allowed Kenya to finance its 100 MWh BESS; commercial rates above 12% would render similar projects uneconomic. Therefore, affordability remains a brake on the Middle East and Africa battery market outside sovereign-backed GCC programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Cells Extend their Lead

Secondary batteries controlled 74.5% of the Middle East and Africa battery market share in 2025, reflecting soaring telecom retrofits and EV uptake. The segment is forecast to post a 15.8% CAGR through 2031, pushing the Middle East and Africa battery market size for rechargeables well above USD 12 billion by the end of the period. Rising cycle-life, declining pack costs, and growing financing options underpin penetration into UPS, mini-grid, and motive-power niches.

Primary batteries now occupy specialized roles in defense and remote sensing. Although they offer high energy density, tightening waste regulations and improving rechargeable economics erode their relative appeal. Lead-acid units lose share each year as tower-cos and C&I customers upgrade to lithium-ion, enabled by pay-as-you-save contracts. Over the forecast horizon, rechargeable penetration rises further as donor-funded electrification schemes specify minimum 2,000-cycle batteries for community systems.

By Technology: Lithium-Ion Dominates, Solid-State on the Horizon

Lithium-ion variants held 34.9% of the Middle East and Africa battery market in 2025, and the segment benefits from supply-chain localization and diverse chemistries covering automotive, stationary, and motive-power needs. Within lithium-ion, LFP outperforms nickel-manganese-cobalt in stationary storage thanks to thermal stability.

Solid-state batteries rise from pilot runs to commercial output after 2027, expanding at 22.4% CAGR. Early volumes flow to premium EVs imported into GCC markets, while cost declines determine mid-2030s mass-market penetration. Flow batteries and sodium-sulfur systems remain niche, serving long-duration industrial microgrids. Emerging sodium-ion technologies could undercut lithium costs, but require demonstration of 3,000-cycle durability in desert climates before broad uptake.

By Application: Industrial Storage Surges Ahead

Automotive batteries provided 37.3% of 2025 revenue in the Middle East and Africa battery market, anchored by 34,970 EVs on UAE roads and Riyadh’s 30% penetration goal.[4]PwC Middle East, “UAE EV Market Update 2025,” pwc.com Yet industrial uses, including telecom, UPS, and grid-scale storage, are projected to eclipse automotive growth with a 10.6% CAGR. The Middle East and Africa battery market size for grid-connected projects increases sharply as South Africa’s BESIPPPP and Egypt’s IPP programs clear more megawatt-hour capacity.

Portable electronics and power tools form a mature segment with modest single-digit growth. Starting-lighting-ignition demand declines as EV sales rise, but legacy vehicle fleets sustain replacement volumes through the late 2020s. All told, industrial storage becomes the revenue growth engine, while automotive underwrites manufacturing scale and technology transfer.

Geography Analysis

Saudi Arabia commanded 31.0% of the Middle East and Africa battery market in 2025, leveraging a 48 GWh-by-2030 target and a 2.5 GW/10 GWh tender pipeline valued at SAR 6.73 billion (USD 1.8 billion). BYD’s 12.5 GWh contract and Sungrow’s 7.8 GWh installed base make the kingdom the region’s largest single buyer. The United Arab Emirates follows with Abu Dhabi’s 19 GWh Masdar project and a dense charging-station network that supports the fastest regional EV per-capita uptake.

Oman’s 14.7% projected CAGR stems from a 20 GW renewables plan and green-hydrogen export ambitions needing multi-hour storage buffers. Qatar, Kuwait, and Bahrain proceed more cautiously, yet policy roadmaps now reference battery tenders after observing Saudi and Emirati cost declines.

North Africa’s momentum is export-driven. Morocco’s Kenitra gigafactory captures European demand under free-trade deals, while Egypt’s Vision 2030 renewables target lifts utility-scale deployments financed by the European Bank for Reconstruction and Development and the African Development Bank. South Africa’s load-shedding crisis and BESIPPPP awards anchor commercial opportunity for integrators. In contrast, sub-Saharan Africa relies on donor-funded mini-grids: Nigeria’s 5 GW solar-plus-2.5 GW storage pledge, Kenya’s 400 MWh target, and Ethiopia’s DREAM program illustrate how concessional capital channels storage to energy-access projects.

Competitive Landscape

Global cell makers converge on GCC tenders, giving the Middle East and Africa battery market a moderately concentrated profile. Contemporary Amperex Technology landed Abu Dhabi’s 19 GWh order, while BYD secured Saudi Arabia’s 12.5 GWh contract, using price leadership to lock in multi-year offtake. LG Energy Solution and Samsung SDI remain active but have not yet matched Chinese bids on cost.

Regional champions emerge through localization. Gotion High-Tech’s Kenitra plant embeds upstream cathode lines and benefits from Moroccan wind power at USD 0.03 per kWh. In Saudi Arabia, potential BYD-Aramco alliances leverage petrochemical know-how and sovereign financing. Local assemblers such as Middle East Battery Company retrofit telecom towers, drawing on established lead-acid channels to pivot into lithium.

Market differentiation centers on cell format and duration. HiTHIUM’s 1,175 Ah LFP cell reduced rack count and thermal-management complexity, enabling record GCC price points. ESS Inc. positions iron-flow units for Nigerian IPPs seeking 8-hour runtime and unlimited cycle life. Certification to IEC and ITU standards is now a prerequisite, raising barriers for smaller entrants.

Middle East and Africa Battery Industry Leaders

Exide Industries Ltd

First National Battery Pty Ltd

Middle East Battery Company (MEBCO)

EnerSys

Amara Raja Batteries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Masdar, a renewable energy developer from the UAE, inked a deal with Sungrow. The agreement entails the supply of 7.5 GWh of battery energy storage systems (BESS) for a significant renewable energy initiative in Abu Dhabi. This project plays a pivotal role in bolstering large-scale renewable integration and ensuring grid stability across the UAE.

- September 2025: Saudi Electricity Company awarded 4.9 GWh of BESS contracts for Tabuk and Hail at USD 73-75 per kWh, with HiTHIUM as supplier.

- July 2025: The African Development Bank granted USD 1.2 million for Nigeria’s national BESS feasibility study.

- June 2024: Gotion High-Tech began groundwork on Morocco’s Kenitra gigafactory, phase one valued at USD 1.3 billion.

- May 2024: ESS Inc. received a 1 MW/8 MWh iron-flow battery order from Nigerian IPP Sapele, supported by U.S. EXIM financing.

Middle East and Africa Battery Market Report Scope

A battery stores energy and discharges it by converting chemical energy into electricity. Typical batteries most often produce electricity by chemical means through the use of one or more electrochemical cells.

The Middle East and Africa Battery Market Report is Segmented by Battery Type (Primary, Secondary), Technology (Lead-acid, Li-ion, Nickel-metal hydride, Nickel-cadmium, Sodium-sulfur, Solid-state, Flow Battery, Emerging chemistries), Application (Automotive, Industrial, Portable, Power Tools, SLI, Other Applications), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Rest of Middle East, South Africa, Egypt, Kenya, Nigeria, Morocco, Ethiopia, Rest of Africa). Market Forecasts are Provided in Terms of Value (USD).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Kenya | |

| Nigeria | |

| Morocco | |

| Ethiopia | |

| Rest of Africa |

| By Battery Type | Primary Batteries | |

| Secondary Batteries | ||

| By Technology | Lead-acid | |

| Li-ion | ||

| Nickel-metal hydride | ||

| Nickel-cadmium | ||

| Sodium-sulfur | ||

| Solid-state | ||

| Flow Battery | ||

| Emerging chemistries | ||

| By Application | Automotive (HEV, PHEV, and EV) | |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | ||

| Portable (Consumer Electronics, etc.) | ||

| Power Tools | ||

| SLI | ||

| Other Applications | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Kenya | ||

| Nigeria | ||

| Morocco | ||

| Ethiopia | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa battery market today and what is its expected growth?

The market stood at USD 10.45 billion in 2026 and is forecast to reach USD 15.81 billion by 2031, posting an 8.63% CAGR.

Which battery type dominates regional demand?

Secondary (rechargeable) batteries held 74.5% share in 2025 and are projected to grow at 15.8% CAGR through 2031.

What drives utility-scale storage procurement in Gulf states?

Record-low installed costs near USD 73 per kWh and sovereign diversification agendas spur multi-gigawatt tenders in Saudi Arabia and the UAE.

Why are telecom-tower lithium retrofits accelerating?

Lithium-iron-phosphate cuts diesel runtime by up to 70% and provides under-three-year paybacks for tower operators in Nigeria, Kenya, and South Africa.

Which geography is growing fastest?

Oman leads growth with a projected 14.7% CAGR, driven by its 20 GW renewables and green-hydrogen roadmap.

What role do gigafactories play in the region?

Morocco's and Saudi Arabia's gigafactory plans localize cell production, reduce supply risk, and position the region to serve European and African EV demand.

Page last updated on: