Temperature Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.33 Billion |

| Market Size (2031) | USD 4.03 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

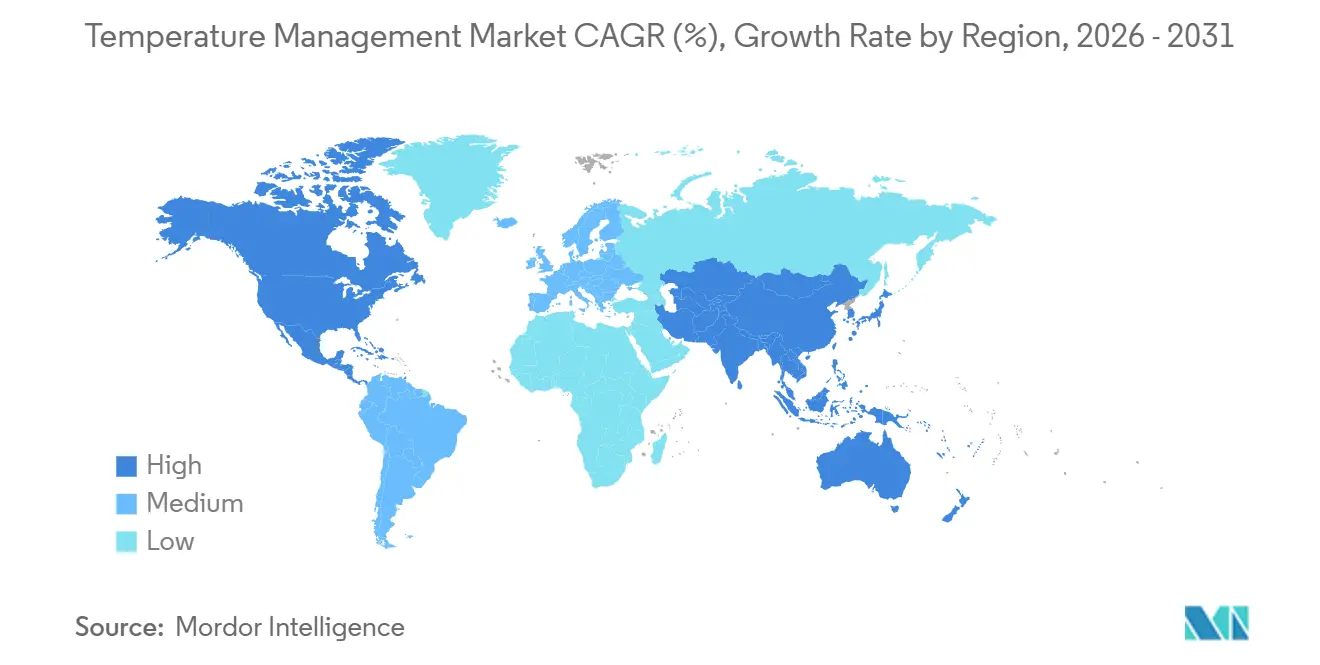

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Temperature Management Market Analysis by Mordor Intelligence

The temperature management market size is expected to increase from USD 3.20 billion in 2025 to USD 3.33 billion in 2026 and reach USD 4.03 billion by 2031, growing at a CAGR of 3.89% over 2026-2031. The steady headline growth conceals fast-moving shifts: artificial-intelligence (AI) algorithms that predict core temperature deviations, a resurgence of forced-air warming in outpatient surgery, and rising procurement of portable cooling systems for heat emergencies are redrawing competitive boundaries across the temperature management market. Hospitals are modernizing fleets to comply with updated Joint Commission perioperative-normothermia standards, while tariff shocks on Chinese components are prompting manufacturers to reshore supply chains. Simultaneously, Class I and II recalls have undermined confidence in older devices and opened opportunities for dual-mode intravascular-surface platforms that promise tighter control, faster ramp rates, and closed-loop automation.

Key Report Takeaways

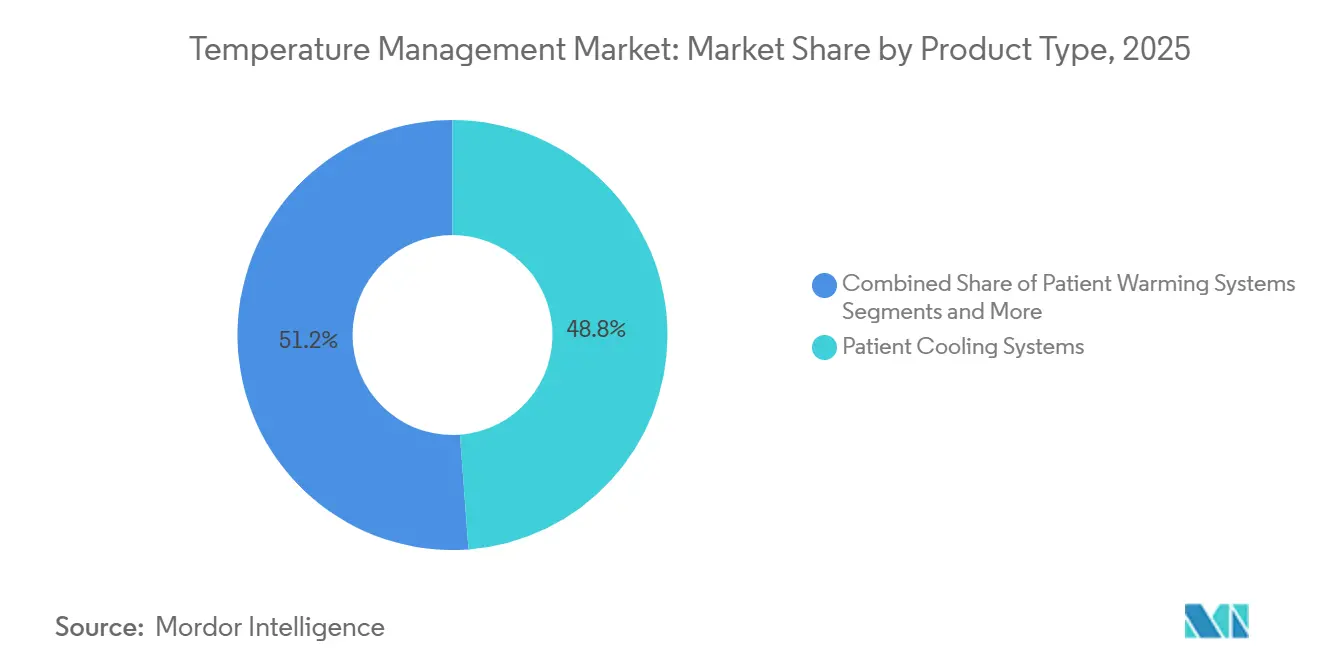

- By product type, Patient Cooling Systems held 48.81% of temperature management market share in 2025, yet Patient Warming Systems are forecast to expand at a 5.12% CAGR through 2031.

- By application, Perioperative Care accounted for 41.45% of the temperature management market size in 2025, while Neonatal and Pediatric Care is projected to grow at a 5.21% CAGR to 2031.

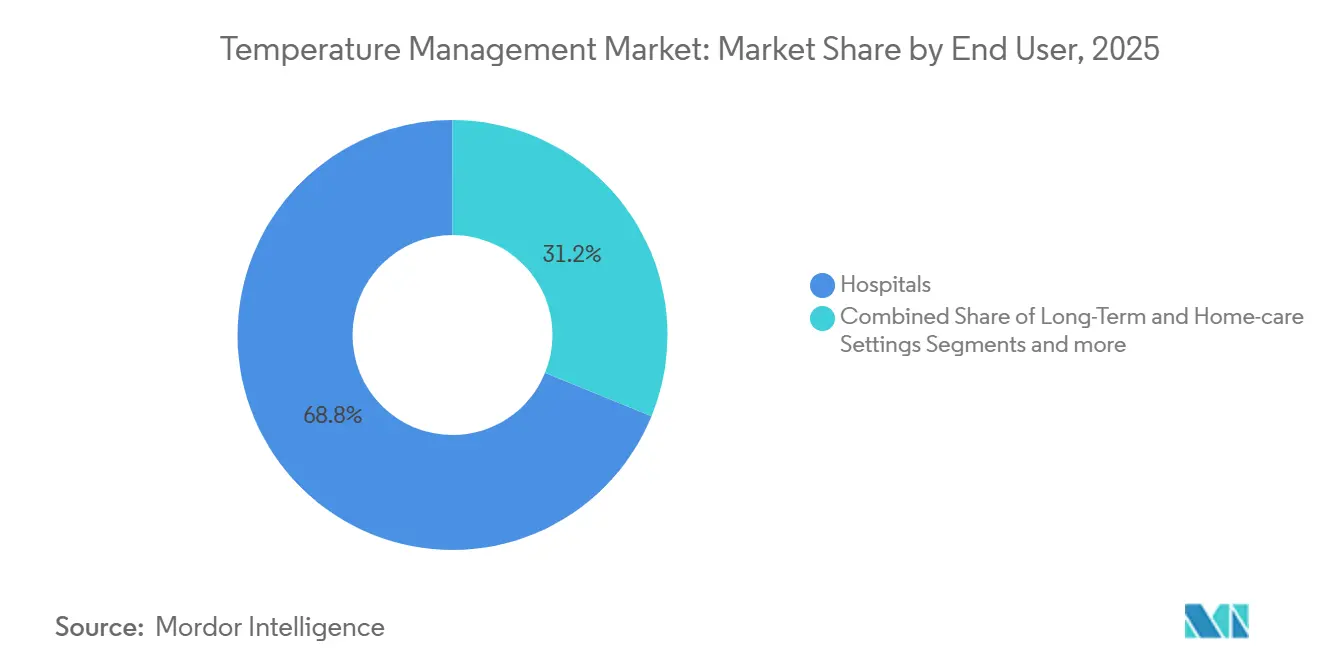

- By end user, Hospitals led with 68.83% of temperature management market share in 2025; Long-Term and Home-care Settings are expected to record the fastest CAGR at 4.98% through 2031.

- By geography, North America captured 41.45% revenue share in 2025, whereas Asia-Pacific is anticipated to post the highest CAGR at 5.05% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Temperature Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic & acute conditions requiring temperature control | +1.2% | Global, with concentration in North America and Europe due to aging populations | Medium term (2-4 years) |

| Growing global surgical volumes | +0.9% | Asia-Pacific core, spill-over to Middle East and South America | Short term (≤ 2 years) |

| Technological advances in intravascular & surface systems | +0.8% | North America & EU (early adoption), APAC (diffusion phase) | Long term (≥ 4 years) |

| AI-driven predictive thermoregulation adoption in ICUs | +0.5% | North America, select EU markets (Germany, UK), pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Climate-change-induced surge in heat-illness emergencies | +0.4% | Global, acute in Southern U.S., Mediterranean Europe, Middle East, South Asia | Short term (≤ 2 years) |

| Portable TTM devices for pre-hospital / battlefield care | +0.3% | North America (EMS, military), EU (emergency services), emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Acute Conditions Requiring Temperature Control

Cardiovascular disease, stroke, and sepsis together prompted more than 30 million OECD hospitalizations in 2025, and all three benefit from precise temperature modulation to curtail neurological damage, coagulopathy, or organ failure. American Heart Association guidelines updated in 2024 require 32-36 °C cooling for 24 hours after cardiac arrest to reduce neurological sequelae.[1]American Heart Association, “2024 Guidelines for Post-Cardiac Arrest Care,” ahajournals.org CDC data show 1.7 million U.S. sepsis hospitalizations in 2024; controlled normothermia lowers mortality by up to 12% in randomized trials.[2]Centers for Disease Control and Prevention, “Sepsis Hospitalizations 2024,” cdc.gov Asia-Pacific now records 13 million new strokes yearly, and early cooling within 6 hours improves 90-day outcomes, driving hospitals to expand device fleets. This epidemiological wave is expanding the temperature management market, particularly in neurocritical-care and cardiac-arrest units that demand rapid, servo-controlled systems. Procurement committees weigh evidence of shorter intensive-care stays and lower ventilator days when proactive temperature control is implemented.

Growing Global Surgical Volumes

Worldwide surgical procedures rebounded to roughly 400 million in 2024, exceeding pre-pandemic levels. Perioperative hypothermia below 36 °C occurs in up to 70% of patients under general anesthesia and heightens infection risk, transfusion requirements, and recovery times. The American Society of Anesthesiologists mandated active warming for procedures lasting more than 30 minutes in its 2024 advisory. Asia-Pacific leads growth: China performed 60 million inpatient surgeries in 2024 and India expanded capacity 12% year-over-year as district-level theaters opened. U.S. ambulatory surgical centers logged 28 million cases in 2024, adopting forced-air and conductive devices to meet Joint Commission norms. The temperature management market gains momentum as bariatric, robotic, and minimally invasive surgeries extend operative time and diminish endogenous heat production.

Technological Advances in Intravascular & Surface Systems

Intravascular temperature management circulates chilled or warmed saline through central venous catheters, achieving ±0.2 °C precision and reducing shivering versus surface pads. ZOLL’s Thermogard XP, cleared by the FDA in January 2024, unites intravascular and surface modalities and runs closed-loop algorithms tied to esophageal or bladder probes. Hydrogel surface pads now conform to complex anatomy, eliminating forced-air contamination concerns. A 2024 Journal of Neurosurgery trial found intravascular cooling cut time-to-target temperature by 40% in traumatic brain injury, improving discharge Glasgow scores. Hybrid operating rooms prefer dual-mode platforms that swap warming and cooling during cardiothoracic repairs or extracorporeal-membrane-oxygenation (ECMO) explantation. Forward-looking suppliers market energy-efficient compressors and quieter pumps to win capital-equipment tenders that increasingly score on total cost of ownership.

AI-Driven Predictive Thermoregulation Adoption in ICUs

Machine-learning models digest real-time bedside data to forecast core temperature 60 minutes ahead with ≤0.2 °C error, empowering nurses to intervene early. A 2024 Critical Care Medicine study across six hospitals cut fever spikes >38.5 °C by 30% in septic-shock patients via automated alerts. Transformer networks extended prediction to 4 hours in post-operative ICUs, lowering hypothermic episodes 22% in 2025 trials. Implementation hurdles persist: legacy monitors lack Health-Level 7 Fast Healthcare Interoperability Resources (HL7-FHIR) connectors, and the FDA has yet to issue tailored guidance specific to AI temperature-prediction software. Hospitals with interoperable infrastructure nonetheless view predictive algorithms as a path to lower ventilator days and shorter ICU length of stay, supporting incremental investment in supportive hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & maintenance costs | -0.6% | Global, acute in emerging markets and smaller ASCs | Short term (≤ 2 years) |

| Product recalls & device failures | -0.4% | North America & EU (stringent reporting), ripple effect in APAC | Medium term (2-4 years) |

| Tariff-driven component price volatility | -0.3% | Global supply chains, manufacturers sourcing from China | Short term (≤ 2 years) |

| Infection-control litigation slowing forced-air adoption | -0.2% | North America (litigation-prone), EU (regulatory scrutiny) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Maintenance Costs

Advanced intravascular units list between USD 25,000 and USD 40,000, and disposable catheters cost USD 800–1,200 per patient, pressuring budgets under value-based payment. The American Hospital Association reported 62% of U.S. hospitals deferred capital purchases in 2024, placing temperature devices among the top-10 delayed categories. Ambulatory centers favor USD 10–15 forced-air blankets over high-capex alternatives to preserve margins. Service contracts add 8–12% of purchase price annually, covering calibration and software patches. Import duties and currency swings elevate landed costs in emerging markets; an Indian hospital buying a USD 30,000 system pays up to 30% extra in tariffs and logistics, lifting final outlay above USD 38,000. Such economics elongate replacement cycles and impede penetration in mid-tier facilities.[3]American Hospital Association, “Annual Survey 2024,” aha.org

Product Recalls & Device Failures

The FDA’s MAUDE database logged 200-plus adverse-event reports in 2024–2025 concerning temperature devices, citing overheating, sensor drift, and software crashes. Augustine Surgical recalled Hot Dog mattresses in December 2024 after three burn cases; ZOLL recalled its Arctic Sun 5000 in June 2024 over unintended rewarming in 12 patients. Recalls foster clinician skepticism, trigger procurement moratoria, and expose manufacturers to liability. A class-action lawsuit filed in 2024 alleges forced-air systems compromise sterile fields, though discovery continues. Procurement teams now diversify vendor panels and favor dual-mode systems with built-in redundancy, reshaping competitive share in the temperature management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Warming Systems Outpace Cooling Despite Smaller Base**

Patient Warming Systems, propelled by the perioperative rebound and updated ASA mandates, are forecast to increase at a 5.12% CAGR from 2026 to 2031. Forced-Air Warming maintains leadership due to USD 10–15 disposables and rapid deployment, yet infection-control concerns in orthopedic and cardiac theaters nurture conductive-blanket uptake. Blood and IV-Fluid Warmers gain momentum in trauma centers where rapid transfusion of cold blood risks coagulopathy. The temperature management market size for warming devices is projected to reach USD 1.95 billion by 2031, yet dual-mode innovators threaten forced-air incumbents with integrated precision and reduced airborne-particle load. Accessories and disposables dominate recurring revenue, locking institutions into single-supplier service contracts that enhance lifetime value.

Patient Cooling Systems continue to hold 48.81% of 2025 revenue but face headwinds from recent recalls and capital-budget scrutiny. Surface gel-pad systems remain ICU staples for fever management, whereas intravascular catheters capture neurology and cardiac-arrest protocols demanding ±0.2 °C control. The temperature management market share for surface cooling is expected to erode 2 percentage points by 2031 as dual-mode platforms proliferate. Evaporative units see renewed interest as emergency-department stock for heat-stroke spikes documented by the CDC. Integrated dual-mode designs, such as Thermogard XP, are carving niches in hybrid rooms where aortic arch repair alternates between deep hypothermia and rapid rewarming.

By Application: Neonatal Care Surges on WHO Mandate

Neonatal and Pediatric Care leads growth at a 5.21% CAGR on the strength of WHO 2024 guidelines promoting 33.5 °C cooling for hypoxic-ischemic encephalopathy within 6 hours of birth. Cochrane evidence indicates a 75% drop in mortality or severe disability, compelling hospitals to install servo-controlled blankets and caps. The temperature management market size for neonatal applications is forecast to climb from USD 420 million in 2026 to USD 540 million in 2031. Emerging markets add incremental volume as philanthropic funding equips district hospitals. Specialized disposables sized for low birth weight infants contribute attractive margins.

Perioperative Care, with 41.45% share in 2025, remains the largest application by installed base. Implementation of Joint Commission audits pushes facilities to document core temperatures every 15 minutes, ensuring active warming adoption remains high. Cardiac Arrest & Critical Care is stable, yet adoption of intravascular cooling spreads from tertiary centers to regional hospitals as evidence of neurological benefit matures. Neurology & Stroke applications grow in Asia-Pacific, leveraging national subsidies for stroke centers. The “Others” bucket—burn units, transplant teams, military trauma—expands modestly, particularly as portable warming blankets become standard in mass-casualty kits.

By End User: Home Care Gains as Reimbursement Shifts

Hospitals commanded 68.83% of 2025 revenue, but value-based care incentives accelerate transfers to step-down units and home recovery. Ambulatory Surgical Centers, performing 28 million U.S. procedures in 2024, adopt low-cost forced-air blankets to maintain competitiveness. Long-Term and Home-care Settings grow fastest at a 4.98% CAGR; Medicare Advantage plans reimburse disposable conductive blankets paired with cloud-linked sensors that alert clinicians to hypothermia. The temperature management market share for home settings is expected to double from 3% to 6% of global revenue by 2031. Military and disaster-response users add incremental growth through contracts for ruggedized, battery-operated coolers and warmers.

Remote monitoring pilots in 2024 proved 18% fewer 30-day readmissions for orthopedic patients discharged with wearable warmers and Bluetooth thermometers. FDA draft guidance for home-use Software-as-a-Medical-Device eased regulatory pathways in late 2024, sparking start-up interest in app-based platforms. Long-term-care facilities deploy conductive blankets to offset elderly thermoregulatory deficits and reduce hypothermia-related falls, supporting steady demand.

Geography Analysis

North America retained 41.45% of 2025 revenue, bolstered by 50 million surgical procedures and early AI adoption in academic ICUs. The CDC heat-illness surge has pushed emergency departments to secure portable cooling devices, enlarging the temperature management market. Device recalls have forced procurement diversification, benefitting mid-tier vendors and spurring hospitals to negotiate dual-source contracts. Canada funds therapeutic hypothermia under provincial budgets, while Mexico’s private chains add dual-mode systems to new hybrid theaters.

Asia-Pacific posts the highest regional CAGR at 5.05% for 2026–2031. China’s CNY 1.55 trillion healthcare spend earmarks 1,000 county hospitals for surgical upgrades, each stipulating perioperative temperature control equipment. India’s district-hospital expansion fuels forced-air blanket purchases, and private chains invest in intravascular cooling for neurocritical hubs. Japan’s aging demographic elevates stroke-cooling demand, aided by 2024 reimbursement codes. South Korea leverages subsidies for domestic startups developing AI-integrated platforms. Australia’s bushfire seasons heighten procurement of portable cooling units for emergency-department surge capacity.

Europe maintains significant share despite Medical Device Regulation (MDR) transition costs. Germany’s Diagnosis-Related-Group codes incentivize therapeutic hypothermia post-cardiac arrest. NHS England’s net-zero procurement policy favors energy-efficient conductive devices, nudging market share away from high-wattage forced-air systems. Heat-wave mortality in Italy and Spain catalyzes bulk orders for mobile cooling. Compliance hurdles under MDR have delayed small-firm launches, consolidating share among MDR-ready incumbents.

The Middle East & Africa benefit from mega-hospital projects under Saudi Vision 2030 and UAE Health Strategy 2025, each ICU bed budgeted with integrated temperature management systems. Field hospitals in Gulf nations now include industrial evaporative coolers for heat-stroke mass-casualty events. South Africa issues neonatal cooling tenders to cut birth-asphyxia deaths. South America records steady growth as Brazil’s SUS funds perioperative warming upgrades and Argentina’s private network chases accreditation.

Regulatory Landscape

Temperature management devices are regulated primarily as medical devices using risk-based pathways that cover electrical safety, software validation, and clinical performance evidence. Postmarket expectations are also expanding in response to recent adverse-event and recall activity in the category. In the United States, the FDA implemented the Quality Management System Regulation (QMSR) in February 2026, aligning quality-system requirements more closely with ISO 13485:2016 and increasing the emphasis on lifecycle controls for design changes and software updates that are common in closed-loop temperature platforms.

Device-specific classification and standards recognition continue to tighten the compliance baseline. In April 2026, the FDA finalized classification of brain temperature measurement systems as Class II devices under 21 CFR 882.1565 with special controls covering in vivo performance testing, electrical and thermal safety testing, and software algorithm validation, reinforcing the broader shift toward more explicit evidence packages for novel temperature-related systems. Separately, the FDA updated 21 CFR 880.2910 in June 2025 to clarify exemption conditions for certain clinical electronic thermometers while pointing manufacturers to recognized standards (for example, ISO 80601-2-56 and ASTM E1965/E1112). The agency continues to recognize IEC 80601-2-59 (Edition 2.1) for febrile temperature screening thermographs, with a transition timeline extending to 2028. In Europe, EU MDR 2017/745 remains the governing framework, and Team-NB updated technical documentation guidance in April 2025, raising the documentation and ongoing benefit-risk evaluation burden that smaller suppliers cite as a barrier to maintaining or expanding CE-marked portfolios.

Value Chain Analysis

The value chain in temperature management spans component and sensor suppliers (thermal sensors, control electronics, compressors or thermoelectric elements, catheter and pad materials), device OEMs (patient warming systems, cooling systems, and integrated dual-mode platforms), sterilization and packaging partners, and downstream distribution via direct hospital sales teams and specialized medical-device distributors serving hospitals, ambulatory surgical centers, and emergency services. Accessories and disposables (blankets, pads, probes, tubing sets, and intravascular catheters) form a large recurring revenue layer. Vendor qualification, clinical protocols, and service agreements create switching frictions and concentrate purchasing through contracted supply channels.

Operational performance is shaped by quality and traceability requirements and by supply continuity for specialized parts. Regulatory-driven quality management updates, including the FDA QMSR implementation in 2026 and ongoing EU MDR audits, increase documentation and supplier oversight across design, manufacturing, and postmarket change control. Recent recall activity in the category has also encouraged providers to diversify approved vendors and tighten incoming inspection and software-update governance. On logistics, broader medical supply-chain fragility themes described by organizations such as the OECD, including just-in-time purchasing exposure and limited stockpiling capacity, reinforce the need for resilient inventories of disposables and critical spare parts to limit OR and ICU downtime when shortages occur.

Competitive Landscape

Medtronic bundles warming blankets with patient monitors, while ZOLL positions Thermogard XP as a dual-mode premium alternative. Gentherm’s 2016 purchase of Cincinnati Sub-Zero integrated Blanketrol coolers into a broader lineup, and ICU Medical’s USD 2.4 billion Smiths Medical buy added level-1 warmers and temperature probes. Emerging firms like Belmont Medical and The 37Company challenge incumbents with modular systems priced 15-20% lower and backed by cloud-analytics dashboards.

Regulatory dynamics shape strategy. EU MDR compliance expenses push smaller players to partner or exit Europe. U.S. tariff hikes on Chinese parts drive nearshore production. Energy-efficiency scoring in UK NHS tenders favors conductive solutions, prompting redesign of forced-air blowers. AI-driven predictive modules represent white space; no device maker yet markets an FDA-cleared forecasting algorithm despite promising trials. Recalls of forced-air and cooling systems tilt preference toward conductive blankets and intravascular catheters, altering purchase criteria in favor of proven safety records.

Supply-chain resilience features prominently in 2025-2026 roadmaps. ZOLL expanded a Texas PCB facility to hedge tariff risk, while Gentherm invested in an Ohio catheter plant. Vendors pursue ecosystem lock-in: capital equipment discounted upfront, balanced by higher-margin disposables under multiyear agreements. Hospitals weigh interoperability, lifecycle cost, and energy footprint alongside precision, cementing a nuanced competitive chessboard.

Temperature Management Industry Leaders

Becton, Dickinson and Company

Medtronic PLC

Stryker Corporation

Drägerwerk AG & Co. KGaA

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is opening around portability and earlier initiation of cooling, particularly for neuroprotection where minutes matter in out-of-hospital cardiac arrest and emergency care. Clinical research in 2026 supported this direction: the PRINCESS2 randomized pilot trial reported on portable trans-nasal evaporative cooling used on-scene for selective brain cooling in out-of-hospital cardiac arrest, and a first-in-human study evaluated a non-invasive intranasal temperature modulation device in awake volunteers, demonstrating core cooling without shivering or sedation in a small cohort. These proof points point to commercial differentiation for manufacturers that can package compact systems with simple workflows, battery operation, and robust training and service models for EMS and emergency departments.

A second opportunity track is closed-loop automation that reduces manual temperature checks and helps mitigate perioperative hypothermia, aligning with tighter hospital norms around documentation and protocol compliance. In March 2026, clinical results were reported for intelligent closed-loop warming systems that integrate wireless sensors with heating devices and improved prevention of perioperative hypothermia versus conventional methods in video-assisted thoracoscopic surgery, reinforcing demand for integrated monitoring and device-control capabilities. Regulatory structure also shapes the development roadmap: FDA product classification for thermal regulating systems (for example, Class II under product code NZE) and expanding software validation expectations, reinforced by the FDA Class II classification of brain temperature measurement systems in April 2026, raise the bar for algorithm-driven platforms. That creates room for suppliers able to industrialize software lifecycle processes under QMSR and maintain MDR-ready technical documentation for global deployments.

Recent Industry Developments

- February 2026: TSC Life received FDA clearance for pediatric use of its Fluido Compact blood and fluid warmer in the United States and Canada. The expanded label strengthens the companys position in pediatric perioperative and critical-care warming workflows, where validated performance and safety claims influence formulary access and tender outcomes.

- July 2025: 3T Medical Systems completed the acquisition of the Altrix Precision Temperature Management System product line from Stryker. The deal consolidated ownership of an established platform under a specialist player, reshaping competitive positioning and giving 3T Medical Systems a faster path to scale through an acquired installed base and product roadmap.

- January 2025: TSC Life assumed direct management and sales of its Mistral-Air portfolio in the United States, transitioning away from Stryker as its distribution partner. Moving to a direct commercial model increased control over pricing, service responsiveness, and customer relationships in a segment where service contracts and disposable pull-through materially affect lifetime account value.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the temperature management market covers medical devices and related consumables used to warm or cool patients in clinical care, so body temperature can be maintained or deliberately adjusted during treatment.

Scope exclusions: Non-medical thermal control used in automotive, electronics, building HVAC, cold chain logistics, and industrial process temperature control is excluded.

Segmentation Overview

- By Product Type

- Patient Warming Systems

- Forced-air Warming Devices

- Conductive / Resistive Warming Devices

- Blood & IV-Fluid Warmers

- Integrated Dual-Mode Systems

- Patient Cooling Systems

- Surface Cooling Devices

- Intravascular Cooling Systems

- Evaporative / Air Cooling Systems

- Accessories & Disposables

- Patient Warming Systems

- By Application

- Perioperative Care

- Cardiac Arrest & Critical Care

- Neurology & Stroke

- Neonatal and Pediatric Care

- Others

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Long-Term and Home-care Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean fact base on procedure volumes, care settings, and device adoption signals that shape warming and cooling demand. We typically use public sources such as the US CDC for hospital and clinical statistics, the US FDA databases for device clearances and safety communications, WHO health datasets for system-level indicators, and OECD health statistics for utilization context.

To keep the model grounded, we also review company filings and investor presentations for product mix language, plus medical society and hospital association publications for practice patterns around perioperative warming and critical care cooling. In a few places, we supplement with paid subscriptions that help with company financials and intelligence, plus patent databases to track where innovation is concentrated. The sources listed here are illustrative, and other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to confirm how products are actually used in operating rooms, ICUs, and neonatal care, and to pressure-test assumptions on average selling prices, disposable attachment rates, and replacement cycles. We spoke with a mix of manufacturers, distributors, and hospital-side stakeholders across major regions, so regional practice differences and procurement realities could be reflected in the final view.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 45% |

| Mid tier: 49% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 14% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is first constructed using a top-down approach, where procedure and patient-volume signals are translated into an addressable demand pool for warming and cooling across key hospital departments. The model then uses selective bottom-up approximations, like sampled pricing by product category, typical accessory and disposable usage per case, and channel feedback on mix, and the totals are adjusted when the numbers do not line up.

Inputs used in the market model include indicators such as surgical and perioperative case volumes, critical care and post-cardiac arrest treatment intensity, neonatal ICU activity, installed base replacement timing, and observed pricing movement for capital equipment and consumables. Forecasts are built using scenario analysis, because adoption and utilization can shift with hospital budget cycles and changes in clinical practice, and these scenarios are aligned to what interviewees expect by region. Where direct volume signals are thin, gaps are filled using proxy utilization rates that are checked against procurement behavior and the expected split between warming systems, cooling systems, and related disposables.

Data Validation & Update Cycle

Outputs are checked against independent demand signals, including whether implied unit volumes make sense versus procedure counts and whether price assumptions remain consistent with recent procurement feedback. Variances are reviewed in more than one step, and when a region or category shows an unusual jump, we re-check the drivers and, if needed, re-contact sources to confirm what changed.

The report is refreshed annually, and interim adjustments are made when material events occur, such as major regulatory actions, product recalls, or sharp changes in hospital capital spending. Before delivery, a final analyst pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Temperature Management Market Size Compared Against Other Published Estimates

Published market sizes for temperature management often vary, even when the topic sounds identical, because analysts do not always count the same products, care settings, and revenue components. Differences also come from how procedure volumes are converted into device demand, how consumables are treated, and how currency timing and inflation are handled.

Procedure-volume checks and cross-validation to operating room, ICU, and neonatal care usage are the evidence that keeps Mordor Intelligence's estimate anchored to patient warming systems, patient cooling systems, and accessories and disposables used in hospital care. Another common gap driver is revenue scope, since some sources add services or monitoring revenues, and others apply faster adoption without matching it to replacement cycles and disposable attachment rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.33 B (2026) | |

| Global Market Report A | USD 3.02 B (2025) | Uses a factory-gate revenue view and can include related services and monitoring revenue, which shifts totals relative to a device-and-consumables demand build tied to hospital utilization. |

| Market Analytics Firm B | USD 3.11 B (2024) | Uses an earlier base year and a higher growth path, with limited visibility on how procedure volumes, replacement timing, and disposable attachment rates constrain near-term expansion. |

Across the three numbers, the spread is mostly explained by scope differences and how demand is converted into value, not by arithmetic. When the product set, care-setting coverage, and price and volume inputs are made explicit, the market size becomes easier to audit and refresh year to year.

Key Questions Answered in the Report

How large is the global temperature management market in 2026?

The temperature management market size reached USD 3.33 billion in 2026 and is forecast to grow at a 3.89% CAGR to 2031.

Which product segment is growing fastest through 2031?

Patient Warming Systems lead growth with a projected 5.12% CAGR, reflecting renewed perioperative volumes and stricter normothermia guidelines.

Why is neonatal temperature management gaining attention?

WHO 2024 guidance mandates therapeutic hypothermia for moderate-to-severe neonatal encephalopathy, boosting demand for servo-controlled blankets and caps and driving a 5.21% CAGR in neonatal and pediatric applications.

Which region will post the highest growth rate?

Asia-Pacific is projected to register a 5.05% CAGR, propelled by China’s healthcare infrastructure investments and India’s expanding surgical capacity.

What is driving demand for portable cooling devices?

Intensifying heatwaves have escalated heat-stroke emergencies, prompting emergency departments and field hospitals to procure rapid cooling systems that can lower core temperature below 39 °C within 30 minutes.

How concentrated is the supplier landscape?

The top five players hold about 45-50% of revenue, indicating moderate concentration with room for regional specialists and AI-centric entrants.

Page last updated on: