Disposable Thermometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 288.40 Million |

| Market Size (2031) | USD 420.20 Million |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

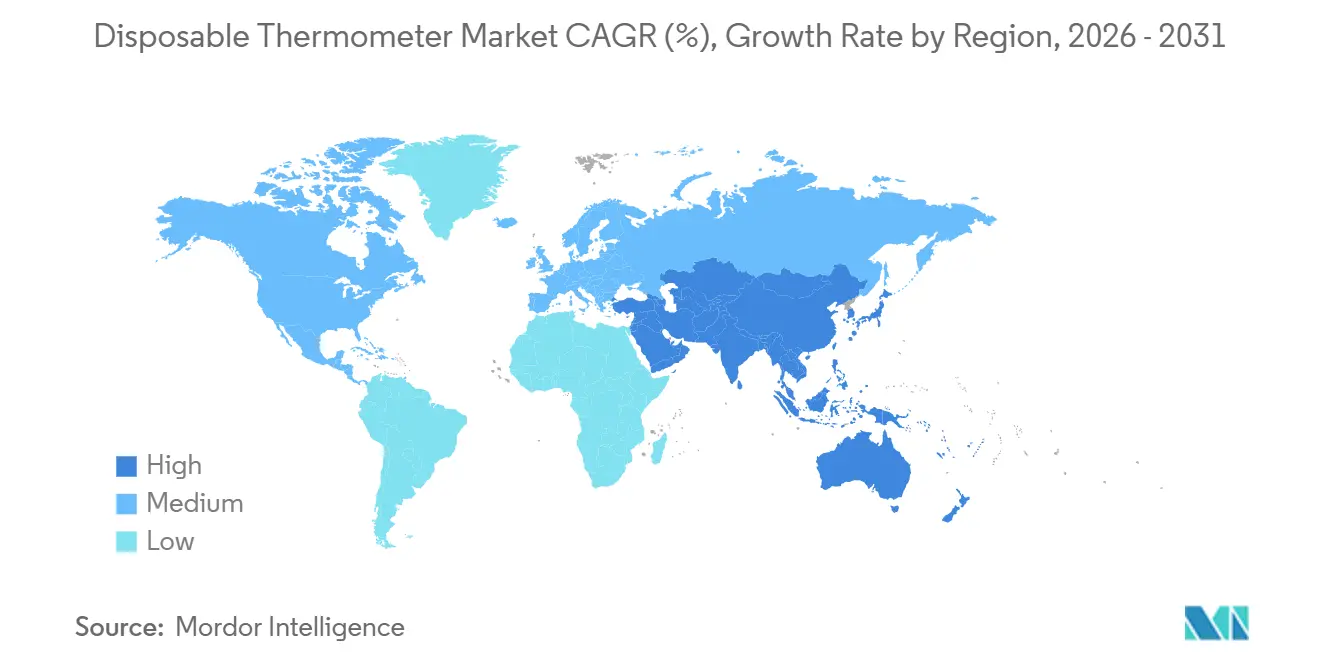

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Thermometer Market Analysis by Mordor Intelligence

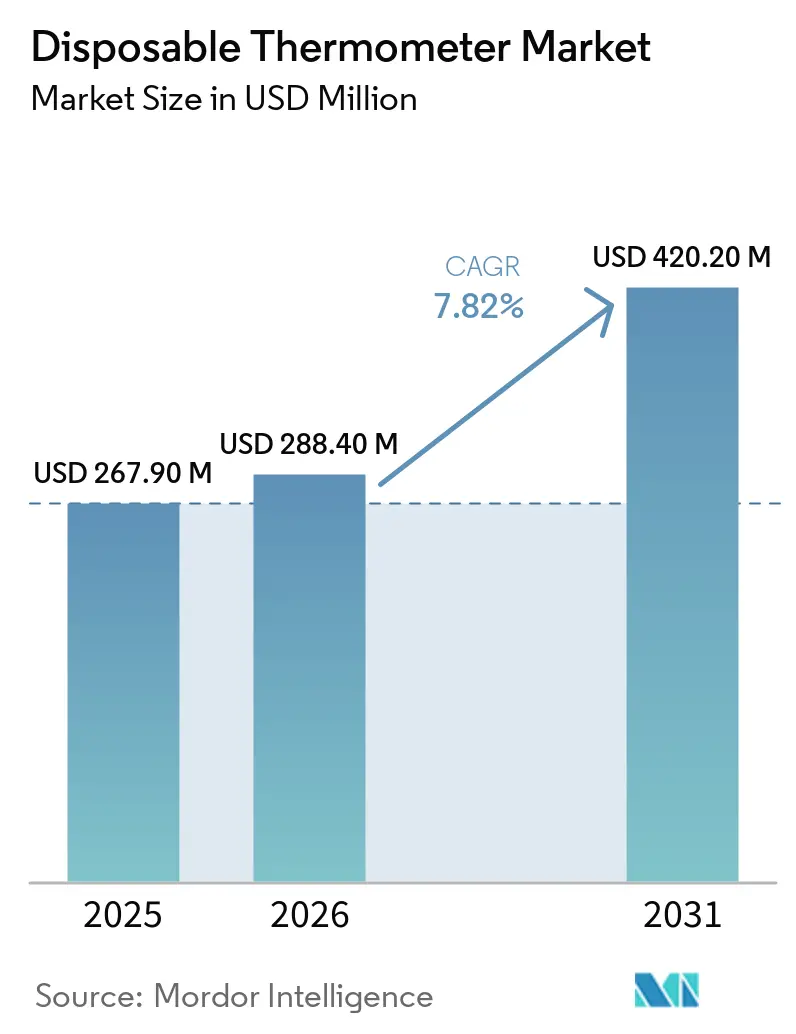

The Disposable Thermometer Market size is projected to expand from USD 267.90 million in 2025 and USD 288.40 million in 2026 to USD 420.20 million by 2031, registering a CAGR of 7.82% between 2026 to 2031.

Adoption rises where infection-prevention targets, mercury-elimination rules, and private-label contracting converge, giving hospitals and ambulatory surgery centers a low-friction route to mercury-free, single-patient devices [1]China Dialogue, “China Bans Mercury Thermometer Production,” chinadialogue.net. Group purchasing organizations bundle disposables into formularies at negotiated prices that undercut the total cost of reprocessing reusable probes, which requires labor, documentation, and autoclave cycles. Asia-Pacific procurement momentum accelerated after China shut down its 180-million-unit mercury-thermometer base, while North America remains ahead in revenue because accreditation bodies link reimbursement to healthcare-associated infection metrics. Sustainability mandates present a counterweight, as the United Kingdom’s National Health Service Evergreen program now scores suppliers on carbon disclosures, nudging net-zero hospitals toward reusable infrared devices when clinical protocols allow.

Key Report Takeaways

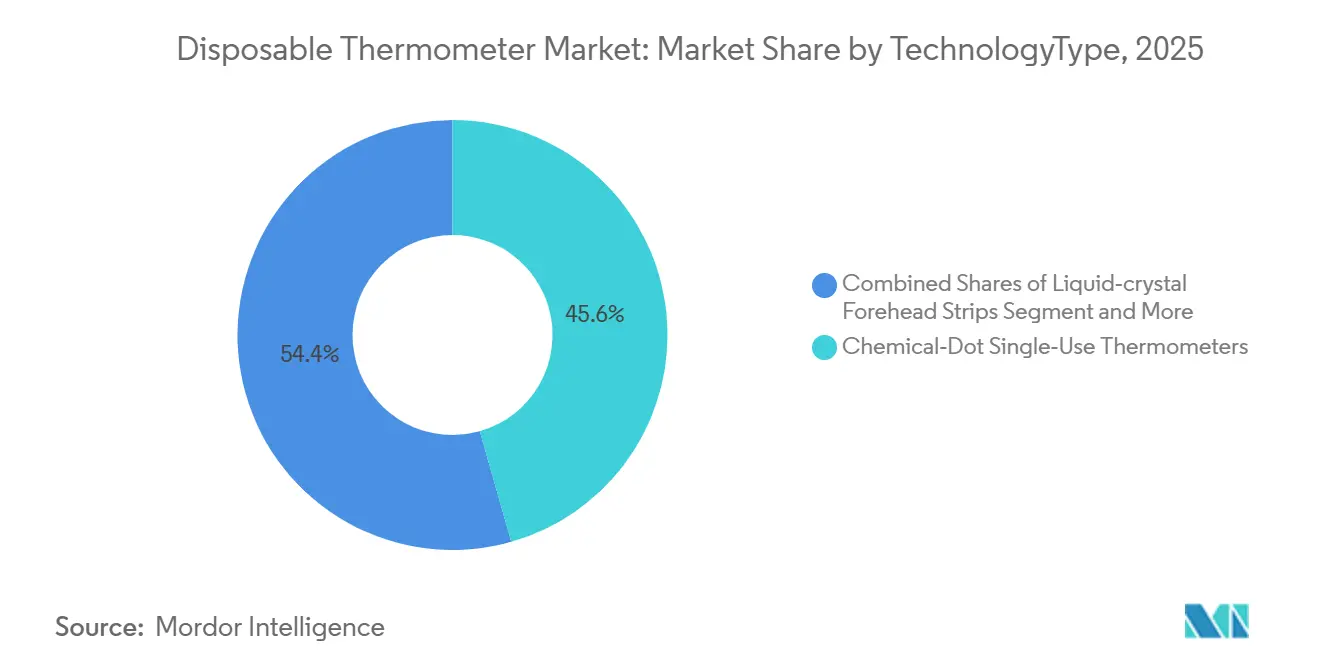

- By technology, chemical-dot single-use thermometers captured 45.60% of 2025 revenue, while single-patient digital variants advance at an 8.35% CAGR through 2031.

- By site of measurement, oral measurement retained a 48.15% share in 2025; forehead and skin formats are growing at an 8.29% CAGR, driven by the trend toward perioperative adhesive demand indicators.

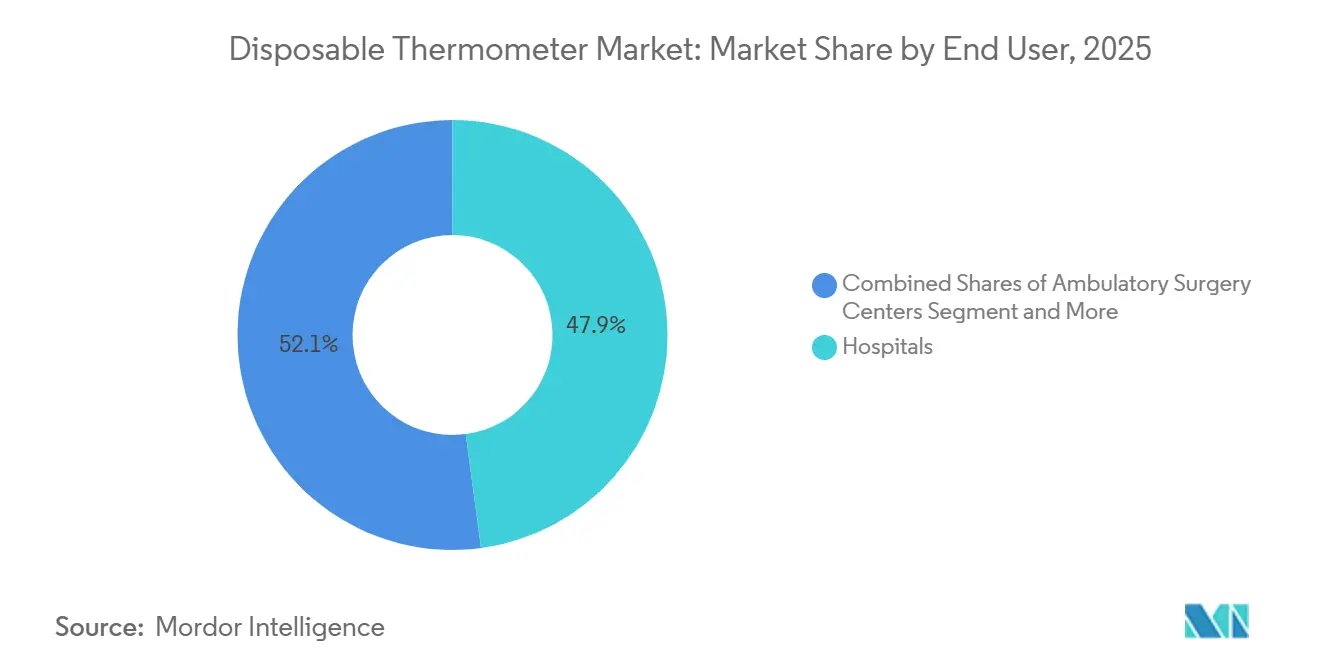

- By end user, Hospitals accounted for 47.89% of 2025 end-user revenue, whereas ambulatory surgery centers are expanding at an 8.3% CAGR as Medicare’s covered-procedures list broadens.

- By geography, North America accounted for 38.18% of 2025 sales, while Asia-Pacific is growing at an 8.48% CAGR as mercury phase-outs drive mercury-free procurement in China, India, and Southeast Asia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Disposable Thermometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection prevention mandates favor single-use to curb cross-contamination | +1.8% | Global, with strongest enforcement in North America & EU | Medium term (2-4 years) |

| Mercury-elimination policies accelerate mercury-free thermometer adoption | +1.5% | APAC core (China, India, Southeast Asia), spill-over to MEA | Short term (≤ 2 years) |

| Perioperative/ICU trend monitoring demand for low-cost adhesive indicators | +1.2% | North America & EU (ASC expansion, OR protocols) | Medium term (2-4 years) |

| Lower total cost-of-ownership versus reusable probes in high-throughput settings | +1.0% | Global, concentrated in large hospital systems | Long term (≥ 4 years) |

| GPO/distributor private-labels expand institutional reach | +0.8% | North America (Premier, McKesson-Provista networks) | Medium term (2-4 years) |

| Low-resource settings adopt disposables to offset poor reprocessing | +0.7% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection Prevention Mandates Favor Single-Use to Curb Cross-Contamination

Centers for Disease Control and Prevention guidelines and Joint Commission accreditation standards hard-wire temperature monitoring into infection-control scorecards [2]Centers for Disease Control and Prevention, “Core Infection Prevention Practices,” cdc.gov. Single-patient thermometers remove probe-sharing risks that persist despite compliant reprocessing routines, an issue underscored by a 2024 Department of Veterans Affairs directive banning reprocessed single-use devices in all VA facilities. The Association for Professionals in Infection Control and Epidemiology explicitly recommends dedicated or disposable devices for non-critical equipment, steering committees toward chemical-dot strips in emergency departments and isolation units. Saudi Arabia’s Ministry of Health applies similar logic, ruling that single-use devices cannot be reprocessed without committee approval. Facilities in litigious markets view disposables as insurance against costly cross-contamination events.

Mercury-Elimination Policies Accelerate Mercury-Free Thermometer Adoption

China’s January 1, 2026, production ban erased the world’s largest mercury-thermometer base, prompting immediate substitution with liquid-crystal strips and digital disposables. The Global Environment Facility mobilized USD 16 million in grants and USD 112 million in co-financing to help India, Vietnam, and Indonesia convert to mercury-free devices [3]Global Environment Facility, “Mercury-Free Thermometer Adoption,” thegef.org. Europe’s revised Mercury Regulation, in force since July 2024, further narrows the window for mercury-added medical products. Under the Minamata Convention, 148 parties must complete the phase-out by 2027, making compliance a near-term procurement priority. Asia-Pacific, therefore, records the steepest unit swing, replacing legacy mercury stock with chemical-dot and single-patient digital options.

Perioperative and ICU Trend Monitoring Demand for Low-Cost Adhesive Indicators

Operating-room hypothermia affects the majority of surgical patients despite ambient climate rules, so clinicians welcome forehead strips that show temperature drift without tying up a nurse’s hands. The Centers for Medicare & Medicaid Services added 573 procedures to the ambulatory-surgery-center list in 2026, broadening outpatient orthopedics and ophthalmology, both of which require intraoperative monitoring. Adhesive liquid-crystal strips cost a fraction of esophageal or bladder probes and fit ASC budgets as the U.S. ASC market heads toward USD 55.3 billion by 2029. Peer-reviewed evidence shows that local wound-temperature monitoring can flag surgical-site infections early, suggesting new applications for disposable indicators in post-acute care. States such as Maryland, with 36 ASCs per 100,000 Medicare beneficiaries, offer dense pockets of demand that private-label distributors target efficiently.

Cost Advantages and Distribution Leverage Sustain Long-Run Adoption

Medical Indicators calculates most of the cost savings once labor and autoclave cycles are factored into ownership expenses, an advantage that is magnified in emergency departments that process hundreds of patients daily. ECRI Institute confirms the break-even tilts toward disposables in high-throughput settings when reprocessing delays tie up beds. Medicare already saves USD 2.3 billion annually by migrating procedures to ASCs, creating headroom for infection-control consumables. Premier and McKesson embed private-label strips into formularies, widening reach while shielding hospitals from capital outlays. In low-resource regions where autoclave infrastructure is patchy, pre-sterilized disposables provide a practical infection-mitigation path.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy limits of liquid-crystal/strip formats versus core temperature | -0.5% | Global, most acute in critical-care and pediatric settings | Short term (≤ 2 years) |

| Competition from reusable non-contact IR devices in sustainability-focused systems | -0.4% | EU & North America (net-zero health systems) | Medium term (2-4 years) |

| Net-zero procurement discourages single-use plastics in hospitals | -0.3% | EU (NHS Evergreen), North America (CHARME collaborative) | Medium term (2-4 years) |

| Rx/professional-only distribution constrains some channels | -0.2% | North America, select EU markets with pharmacy-only rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accuracy Limits of Liquid-Crystal and Strip Formats Versus Core Temperature

An anesthesia study reported a 14% failure rate for liquid-crystal thermometers, while chemical-dot units varied by ±0.4 °C in critically ill cohorts, margins too wide for sepsis or therapeutic-hypothermia protocols. Zero-heat-flux adhesive sensors achieve 94%–96% accuracy within ±0.5 °C but carry higher unit costs, limiting use to reimbursed perioperative or ICU settings. Pediatric reliability problems arise when forehead strips misread febrile infants because of ambient interference. Hospitals, therefore, confine chemical-dot disposables to triage, leaving precision-critical cases to reusable digital or infrared tools.

Competition From Reusable Non-Contact Infrared Devices in Sustainability-Focused Systems

TriMedika’s TRITEMP delivers instant, probe-cover-free readings and generates less plastic waste than single-use strips, aligning with NHS Scope 3 carbon-cutting targets. A BMJ life-cycle study found reusable devices can emit two-to-five times less CO₂ than disposables when cleaning is optimized, data now cited by purchasing units seeking emissions reduction. The NHS Evergreen Sustainable Supplier Assessment requires vendors to file carbon disclosures, and the CHARME collaborative’s 40 health systems collectively prefer durable products, thereby shifting procurement bias toward reusable infrared formats. Suppliers without recycled-content formulations or take-back schemes may face contract erosion as net-zero targets mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Digital Variants Outpace Chemical-Dot Incumbents

Digital single-patient thermometers are advancing at an 8.35% CAGR, outstripping the disposable thermometer market average as pharmacies and formularies integrate battery-powered units that sync with smartphones. Chemical-dot formats still accounted for 45.60% of 2025 sales, underpinning the disposable thermometer market's leadership in size, as unit prices remain below USD 1 in high-volume emergency departments. Connectivity differentiates the next wave: Medical Indicators’ NexTemp App and Smart Meter’s iDigiTemp feed readings straight to electronic records, while FDA-cleared Bluetooth disposables from Guangdong Genial Technology extend monitoring beyond discharge. Price compression stems from private-label programs that place identical chemistry under distributor brands, yet the disposable thermometer market share remains concentrated in strips and dots for now.

Zero-heat-flux patches and multi-sensor devices, such as Withings’ BeamO bundle, thermometry with ECG and oximetry, create premium options for telehealth and ICU care. Hospitals evaluating lifecycle emissions may migrate volume from chemical-dot to reusable infrared for screening, but high-acuity workflows still favor disposable sensors that meet sterility rules without downtime. Product managers therefore chase biodegradable substrates that could reconcile infection control with net-zero goals.

By Site of Measurement: Forehead/Skin Applications Gain on Perioperative Demand

Forehead and skin formats are growing at a 8.29% CAGR, as anesthesiologists favor adhesive indicators that comply with operating-room temperature standards while leaving hands free for core tasks. Oral strips retained 48.15% of 2025 revenue, anchoring the disposable thermometer market size baseline, though their role skews toward triage rather than intraoperative trend tracking. Axillary measurement remains popular in pediatrics, but ±0.4 °C variance limits adoption where sepsis protocols demand tighter margins.

SpotSee’s FeverScan strips and CliniTemp monitors demonstrate forehead temperature accuracy, offering color-shift visuals that nurses can interpret instantly. Rapid ASC expansion—12,294 U.S. centers by Q2 2025—magnifies strip demand, particularly in high-volume markets such as California, Florida, and Texas. Regulatory barriers also factor in: Saudi Arabia’s infection-control rules steer procurement toward skin formats that avoid probe sharing.

By End User: ASCs Outpace Hospitals on Site-Neutral Payment Shifts

Hospitals still delivered 47.89% of 2025 revenue, but ambulatory surgery centers are climbing at an 8.3% CAGR as Medicare’s payment parity drives joint replacements, cataracts, and spine cases into lower-cost venues. The disposable thermometer market share widens in ASCs that choose forehead strips to minimize turnover time and avoid sterilizer bottlenecks.

Physician offices and retail clinics adopt disposables to eliminate the need for autoclaves, though lower throughput tempers the economic advantages. Health-system consolidators such as HCA and Tenet advance ASC portfolios, concentrating procurement clout and deepening reliance on GPO private-label supply chains. Over-the-counter growth also accelerates after Medical Indicators embeds app connectivity for caregiver trend logging.

Geography Analysis

North America led with 38.18% revenue in 2025 as CDC guidelines, Joint Commission metrics, and a VA ban on reprocessed disposables made single-patient thermometers a compliance default. Medicare’s 573-procedure ASC expansion further boosts strip uptake for outpatient orthopedics and ophthalmology. Large health systems use Premier and McKesson private-label frameworks to lock in discounted pricing and automatic replenishment.

Asia-Pacific posts the fastest 8.48% CAGR, catalyzed by China’s mercury-thermometer shutdown and Global Environment Facility grants that finance mercury-free adoption in India, Vietnam, and Indonesia. Low-resource centers lacking reliable sterilization shift directly to chemical-dot disposables, as demonstrated by Dr. Temp distributing NexTemp strips across Sub-Saharan Africa to bypass autoclave gaps.

Europe faces mixed signals: the EU’s tighter Mercury Regulation curtails the use of mercury devices, but NHS Evergreen and CHARME push procurement toward reusable infrared devices or take-back schemes. Hospitals that commit to net-zero often pilot recycled-content strips yet retain reusable options for routine vitals. Import Alert 89-08 reminds offshore suppliers that missing 510(k) will stall customs clearance, a hurdle particularly for new Asian entrants.

Competitive Landscape

Market fragmentation persists. Medical Indicators ships more than 100 million units annually and claims 70% cost savings versus reusable probes, yet private-label programs dilute brand share. Premier’s Healthcare Procurement Solutions and McKesson’s PSMA Connect route house-label strips directly into hospital formularies, compressing average selling prices. Tempagenix offers white-label capacity so regional distributors can market the same chemical-dot chemistry under local brands, keeping margins inside the channel.

Product differentiation now gravitates to connectivity and sustainability. Withings’ BeamO blends ECG, oximetry, and thermometry in a single, FDA-cleared unit for telehealth, while zero-heat-flux patches target high-acuity accuracy thresholds. The CHARME collaborative rewards suppliers that launch recycled-content formulations or closed-loop take-back programs, signaling future bidding advantages. Regulatory posture shapes entry. FDA Import Alert 89-08 detains thermometers without 510(k) clearance, affecting Chinese firms such as Contec and Shenzhen Beierkang, whereas Guangdong Genial Technology and Famidoc received clearances for Bluetooth and cellular-enabled disposables, unlocking hospital and home-care channels.

Disposable Thermometer Industry Leaders

Medical Indicators, Inc

Medline Industries, Inc

Cardinal Health, Inc

McKesson Corporation

Tempagenix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medline Industries signed a supply agreement with Better Life Medical & Surgical Supply to provide a comprehensive portfolio of medical products, including thermometers, across Florida.

- November 2025: FDA cleared Withings’ BeamO multi-sensor handheld combining temperature, ECG, and oximetry.

- March 2025: Cardinal Health launched a new line of disposable thermometers through a partnership with a major hospital network to streamline patient monitoring workflows.

Global Disposable Thermometer Market Report Scope

As per the scope of the report, disposable thermometers are thin, single-use medical devices typically made of plastic strips or "dot matrix" pads that utilize phase-change technology to measure body temperature. These devices contain heat-sensitive chemicals that undergo a precise color change at a specific temperature, allowing for a digital-like reading without electronic components.

The disposable thermometers market is segmented by technology, site of measurement, end user, and geography. Based on technology, the market is segmented into chemical‑dot single‑use thermometers (oral/axillary/rectal), liquid‑crystal forehead strips (reversible), moving‑line trend indicators for anesthesia (forehead), and single‑patient‑use digital contact thermometers (OTC/institutional). By site of measurement, the market is segmented into oral, axillary, rectal, and forehead/skin. Based on end user, the market is segmented into hospitals, ambulatory surgery centers (ASCs), clinics/physician offices, and others.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Chemical‑Dot Single‑Use Thermometers |

| Liquid‑Crystal Forehead Strips |

| Moving‑Line Trend Indicators for Anesthesia |

| Single‑Patient‑Use Digital Contact Thermometers |

| Oral |

| Axillary |

| Rectal |

| Forehead/Skin |

| Hospitals |

| Ambulatory Surgery Centers (ASCs) |

| Clinics/Physician Offices |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Chemical‑Dot Single‑Use Thermometers | |

| Liquid‑Crystal Forehead Strips | ||

| Moving‑Line Trend Indicators for Anesthesia | ||

| Single‑Patient‑Use Digital Contact Thermometers | ||

| By Site of Measurement | Oral | |

| Axillary | ||

| Rectal | ||

| Forehead/Skin | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers (ASCs) | ||

| Clinics/Physician Offices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is global demand for disposable thermometers growing toward 2031?

The disposable thermometer market is expanding at a 7.82% CAGR, moving from USD 288.4 million in 2026 to USD 420.2 million by 2031.

Which technology leads current sales?

Chemical-dot single-use thermometers generated 45.60% of 2025 revenue, the largest share among available formats.

Where is regional growth strongest over the forecast horizon?

Asia-Pacific posts the fastest CAGR of 8.48% as mercury phase-out policies and reprocessing gaps accelerate the procurement of mercury-free disposables.

Why are ambulatory surgery centers a high-growth end-user group?

ASC volumes expand as Medicare adds 573 covered procedures, boosting disposable thermometer uptake because single-patient strips fit rapid-turnover workflows.

Page last updated on: