Medical Thermometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

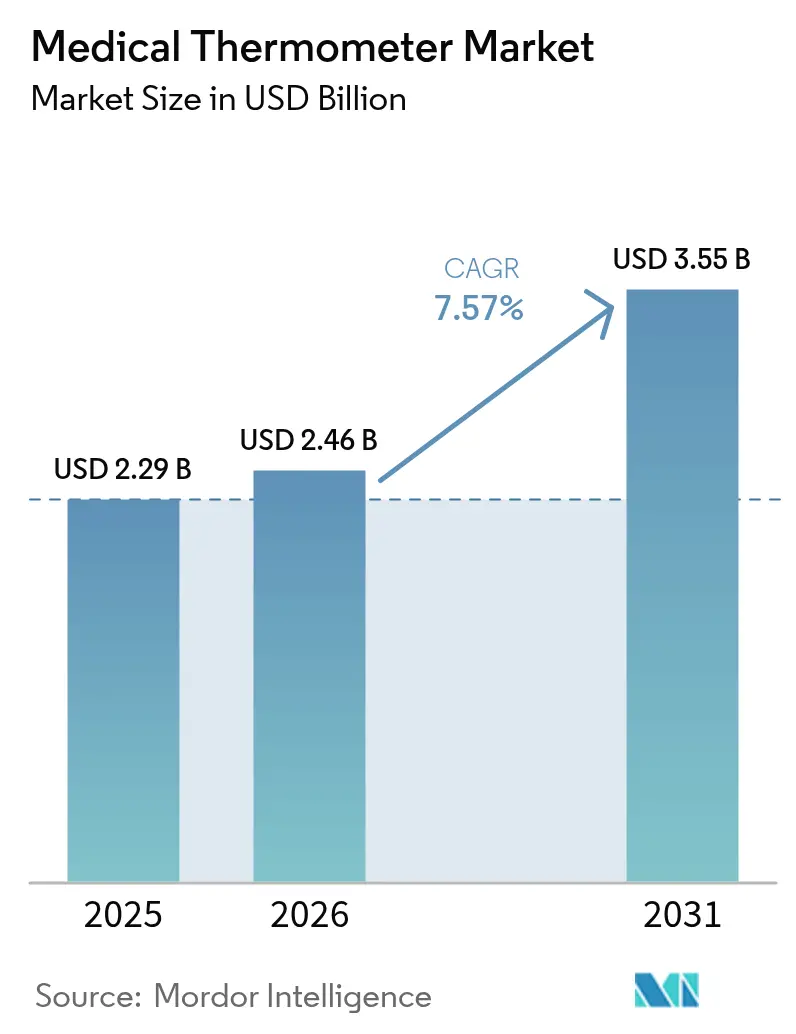

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 7.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Thermometer Market Analysis by Mordor Intelligence

The medical thermometer market size is expected to grow from USD 2.29 billion in 2025 to USD 2.46 billion in 2026 and is forecast to reach USD 3.55 billion by 2031 at 7.57% CAGR over 2026-2031. Sustained demand comes from healthcare digitization, regulatory moves that remove mercury devices, and growing use of AI-enabled temperature monitoring. The FDA’s June 2025 decision to exempt Class II clinical electronic thermometers from 510(k) review lowers compliance costs and encourages rapid innovation[1]Food and Drug Administration, “Exemption of Class II Clinical Electronic Thermometers from Premarket Notification Requirements,” fda.gov, while the European Union’s mercury ban continues to accelerate product substitution. Hospitals and home-care providers expand connected-care programs that bundle temperature sensors with other vital-sign modules, and semiconductor supply challenges are pushing manufacturers toward vertical integration strategies to safeguard production.

Key Report Takeaways

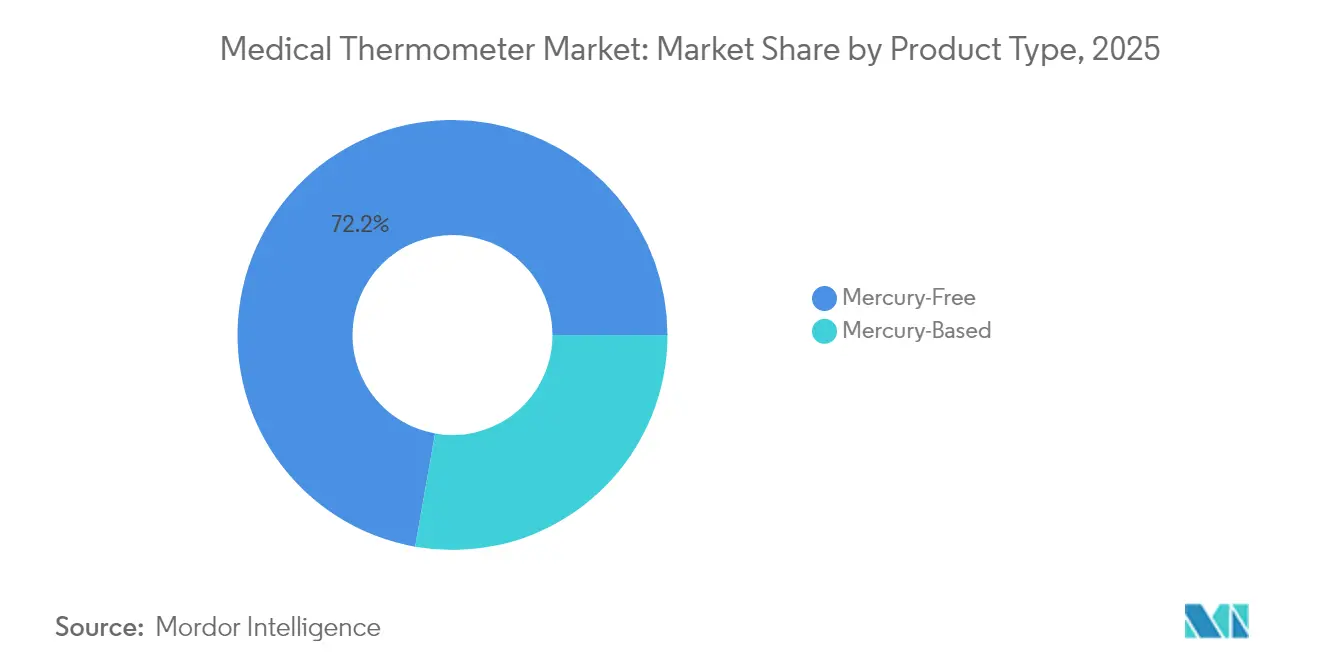

- By product type, mercury-free devices led with 72.22% of medical thermometer market share in 2025 and are advancing at an 8.29% CAGR to 2031.

- By measurement point, oral/axillary captured 62.90% revenue in 2025, whereas forehead thermometers record the highest 8.06% CAGR through 2031.

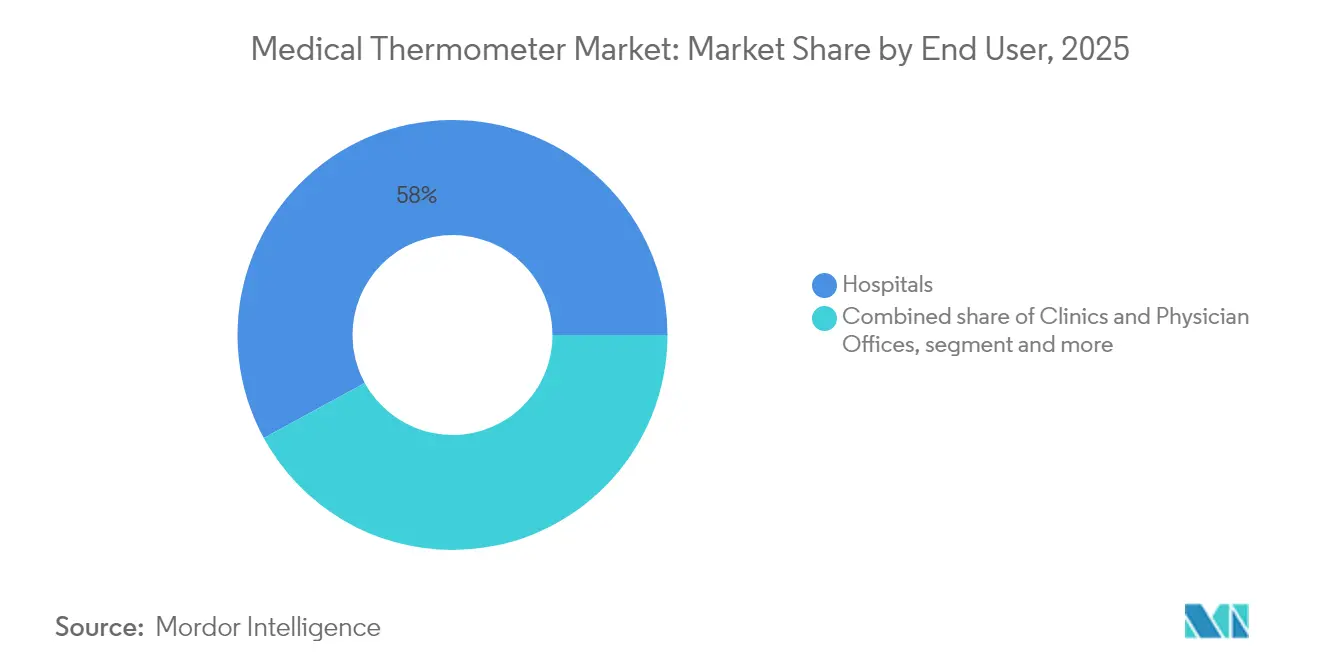

- By end user, hospitals held 57.95% of the medical thermometer market size in 2025; home-care settings post the fastest 8.74% CAGR to 2031.

- By patient age group, adult users commanded 68.10% share in 2025, but pediatric demand is rising at an 7.98% CAGR through 2031.

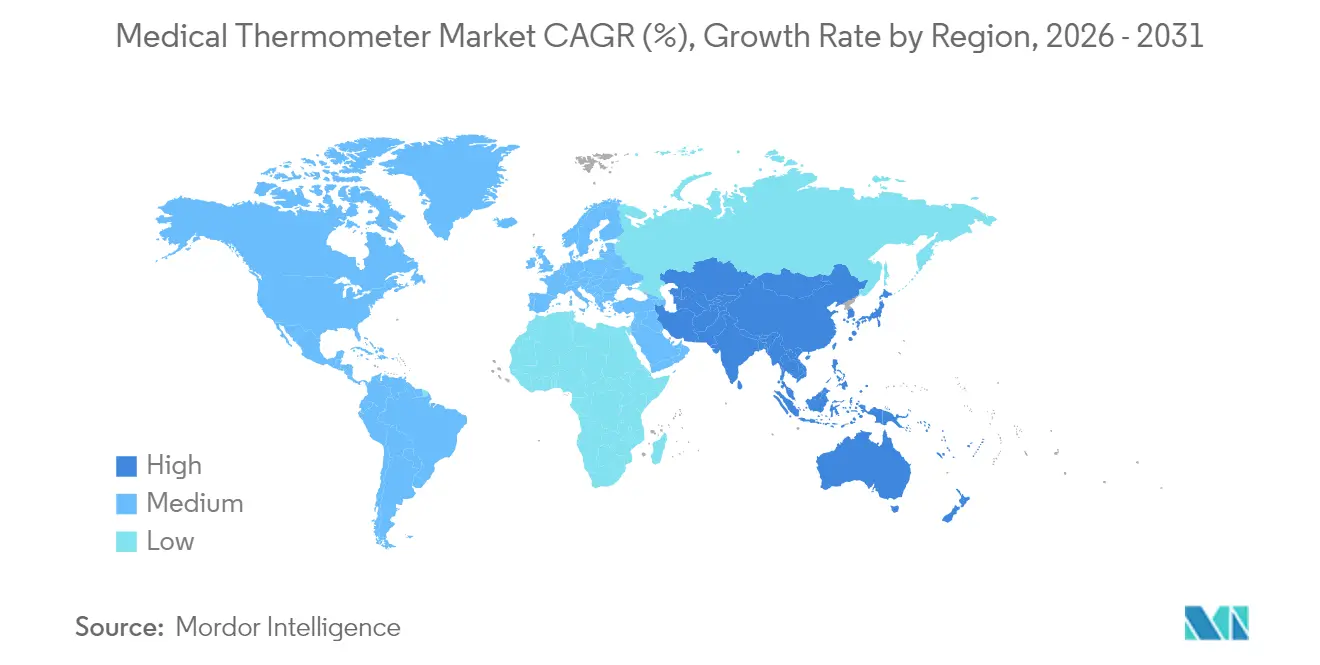

- By region, North America contributed 36.60% of 2025 revenue, while Asia-Pacific is expanding at 9.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Thermometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of home-use digital & smart thermometry post-COVID | +1.8% | Global, highest in North America & Europe | Medium term (2-4 years) |

| Hospital infection-control protocols favouring contact-less devices | +1.2% | Global, led by developed markets | Short term (≤ 2 years) |

| Growing pediatric & geriatric populations needing frequent monitoring | +0.9% | APAC core, spill-over to MEA & LatAm | Long term (≥ 4 years) |

| Integrated vital-sign platforms bundling temperature sensors | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-powered fever-prediction algorithms in wearables | +0.6% | Early adoption in North America & EU | Long term (≥ 4 years) |

| Climate-change-induced disease surveillance programs | +0.4% | Tropical & subtropical regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of home-use digital & smart thermometry post-COVID

Remote-care reimbursement now spans Medicare, and 81% of clinicians integrate temperature tracking into RPM protocols, lifting consumer demand for connected devices that feed data directly into telehealth dashboards. Smart-thermometer fleets exceeding 3 million units provide anonymized datasets used to forecast regional fever spikes, illustrating how the medical thermometer market increasingly overlaps with public-health analytics. Household adoption remains highest in North America, yet Asia-Pacific growth accelerates as mobile-health ecosystems mature and price points fall to mass-market levels. Data-driven platforms encourage repeat sales because firmware and algorithm upgrades extend device lifecycles. Device makers now bundle temperature probes with pulse-ox and blood-pressure modules, creating multi-parameter kits that anchor patient engagement.

Hospital infection-control protocols favoring contact-less devices

Clinical workflows prioritize non-contact thermometry to cut disinfection-time and cross-infection risks. National guidelines in Canada and Australia highlight infrared or single-use solutions in triage and aged-care settings.[2]Australian Commission on Safety and Quality in Health Care, “Infection Prevention and Control Guidelines,” safetyandquality.gov.au Procurement teams embed non-contact requirements in tenders, pushing vendors to refine sensor accuracy through emissivity-compensation algorithms. Although peer-reviewed studies still flag sub-0.8 correlation with core temperature, suppliers counter by integrating dual-sensor arrays and calibration certificates for each batch. Growth is further supported by thermal-screening gates deployed in airports and large venues that were repurposed for routine hospital entry points.

Growing pediatric & geriatric populations needing frequent monitoring

Asia-Pacific adds over 30 million people aged 65+ each year, while birth cohorts remain substantial, creating parallel demand for painless and precise thermometry. Wrist-based sensors validated in Swiss clinical trials demonstrate continuous monitoring without disturbing infants or elderly patients. In pediatric wards, non-contact infrared units reduce anxiety and enable rapid throughput during infection outbreaks. Continuous-data streams integrate into early-warning-score algorithms that spot subtle deviations before fever manifests, improving outcomes for vulnerable groups.

Integrated vital-sign platforms bundling temperature sensors

Hospitals shift budgets from standalone thermometers to platform plays where temperature is one data layer. Omron’s 2024 health-data strategy targets JPY 100 billion in sales from cloud services that pool temperature, blood pressure and activity metrics. API-first designs allow EHR vendors to pull readings in real time, eliminating manual charting. This convergence strengthens switching costs and helps incumbents defend margins against low-cost imports. Investors view these platforms as recurring-revenue models rather than pure hardware sales, raising the medical thermometer market’s profile among digital-health portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory moves to ban mercury thermometers in emerging markets | -0.6% | APAC, MEA & LatAm | Medium term (2-4 years) |

| Accuracy & calibration variability across low-cost imports | -0.8% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Rising cybersecurity concerns around connected thermometers | -0.5% | North America & EU | Medium term (2-4 years) |

| Sensor-grade semiconductor shortages disrupting supply | -0.7% | Global, acute in APAC hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accuracy & calibration variability across low-cost imports

Intra-class correlation coefficients below 0.8 for many budget infrared units undermine clinician trust and can delay febrile-illness diagnosis. Larger providers now demand NIST-traceable calibration reports, increasing compliance costs for suppliers without in-house metrology labs. The FDA’s forthcoming Quality Management System Regulation, aligned with ISO 13485:2016, may exclude non-certified importers, reshaping the competitive field.

Rising cybersecurity concerns around connected thermometers

Pen-tests revealed credential-exposure flaws in several Wi-Fi thermometers, exposing hospitals to ransomware or falsified temperature data. New IEEE standards 2621 and 2933-2024 require encrypted firmware updates and authenticated command channels, adding development overhead. IT departments often isolate medical IoT on dedicated VLANs, complicating rollout in resource-constrained clinics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mercury-Free Devices Cement Regulatory Leadership

Mercury-free thermometers represented USD 1.65 billion of the 2025 medical thermometer market size and continue to expand at 8.29% CAGR, buoyed by sweeping prohibitions on mercury under EU Regulation 2017/852. Digital stick thermometers dominate volume sales because caregivers value their sub-20-second readouts and absence of hazardous materials. Infrared guns and advanced ear probes reinforce infection-control strategies in crowded triage zones. Smart mercury-free units that sync with mobile apps are the fastest-growing niche, aided by cloud dashboards that convert raw temperature into longitudinal health trends.

Since transportation rules classify mercury devices as hazardous goods, distributors increasingly purge legacy stock in favor of mercury-free portfolios. Early movers such as Microlife leveraged R&D scale to certify products under the EU Medical Device Regulation, gaining a price premium over generic brands. Semiconductor shortages challenge smaller players lacking long-term supplier contracts, yet vertically integrated giants secure priority allocations, protecting output during demand spikes. As environmental-health frameworks tighten in Latin America and parts of Africa, the medical thermometer market faces virtually irreversible migration toward mercury-free solutions.

By Measurement Point: Forehead Devices Capture Non-Contact Momentum

Oral/axillary modalities delivered USD 1.44 billion revenue in 2025, or 62.90% of the medical thermometer market, reflecting routine ward protocols and reimbursement familiarity. However, forehead scanners notch an 8.06% CAGR because they minimize surface-contact and accelerate triage. Recent sensor-fusion algorithms adjust for emissivity and ambient drift, pulling root-mean-square error below 0.2 °C in controlled studies, narrowing the gap with oral probes.

Regulators in Australia and Canada now list non-contact screening as preferred practice in aged-care infection-control manuals. Clinical buyers appreciate the ability to read dozens of patients per minute without probe covers, cutting consumable expense. Meanwhile, tympanic devices retain relevance in pediatrics thanks to minimal discomfort and stable ear-canal core-temperature correlation. Innovations such as thermochromic masks that change color above 37.5 °C illustrate how forehead-centric solutions extend beyond handheld form factors. Manufacturers that reconcile speed, hygiene and accuracy are best placed to win tenders in the evolving medical thermometer market.

By End User: Home-Care Uptake Surges with Remote Patient Monitoring

Hospitals still generated 57.95% of 2025 revenue, yet home-care purchases rise 8.74% annually as RPM reimbursements widen across the United States and parts of Europe. Medicare now pays for at-home temperature surveillance within chronic-disease bundles, incentivizing providers to deploy kits that include cloud-linked thermometers. Start-ups exploit this shift by bundling software subscriptions with each unit, creating annuity streams beyond hardware margins.

Consumer channels increasingly favor app-enabled models that store multi-user profiles, aiding parents managing sick children and caregivers supporting seniors. Clinics and physician offices sit between hospital and home segments, seeking rugged devices that balance price with Professional-Grade ISO 80601-2-56 accuracy. As value-based care contracts penalize readmissions, providers integrate thermometer data with blood pressure, glucose and ECG feeds to trigger early interventions, elevating the medical thermometer market’s strategic importance inside population-health programs.

By Patient Age Group: Pediatric Devices Lead Growth Curve

Adults comprised 68.10% of units sold in 2025, but pediatric use cases post an 7.98% CAGR as technology adapts to child-specific needs. Studies from Oxford’s Horizon Scanning Centre confirm that calibrated non-contact sensors maintain suitable accuracy in children, reducing distress compared with rectal probes. Manufacturers apply gamification—LED smiley faces, mobile-app rewards—to improve compliance. Neonatal intensive-care units pioneer patch sensors with ±0.1 °C precision, essential for detecting sepsis risk within minutes.

Geriatric patients present distinct thermoregulation patterns, often lacking classic fever spikes. Continuous wrist sensors, validated in post-vaccination cohorts, provide 24/7 trendlines that flag subtle deviations sooner than spot checks. Dual-market designs that switch between adult and pediatric modes appeal to multigenerational households in emerging economies, broadening addressable demand and deepening the medical thermometer industry’s value proposition.

Geography Analysis

North America delivered USD 838 million of the 2025 medical thermometer market, holding 36.60% share on the back of robust RPM reimbursement, hospital digitization and regulatory clarity. The region’s providers increasingly mandate cybersecurity certifications, creating barriers for low-cost importers but supporting premium ASPs. Growth remains healthy at 6.58% CAGR as home-based chronic-care programs scale nationwide.

Asia-Pacific, valued at USD 654 million in 2025, records the fastest 9.11% CAGR to 2031, underpinned by China’s hospital-digitization subsidies and India’s Ayushman Bharat insurance rollout. Although medtech investment fell from 2021 peaks, consolidation allows established thermometer makers to buy distressed sensor firms and capture local distribution networks. Japan’s rapidly aging population favors continuous monitoring wearables, while Southeast Asian clinics leapfrog straight to mobile-linked devices due to smartphone ubiquity.

Europe holds a steady 23.80% revenue slice as the Medical Device Regulation tightens post-market surveillance, prompting smaller brands to exit rather than re-certify. Mercury prohibitions remain a decisive tailwind and keep the medical thermometer market aligned with sustainability mandates. Middle East and Africa show double-digit expansion from a low base, propelled by infection-surveillance grants and private-hospital projects, yet logistical hurdles and currency volatility temper near-term uptake. Latin America’s public-sector tenders favor budget models, but private insurers increasingly reimburse connected devices, gradually shifting the mix toward higher-value smart thermometers.

Competitive Landscape

The top five companies hold significant share of market creating a moderately concentrated medical thermometer market where brand trust and regulatory compliance matter as much as price. Terumo leverages a century-old thermometer legacy plus JPY 1,036.2 billion global revenue to maintain flagship status in hospitals. Cardinal Health, with USD 226.8 billion total sales, reinforces its Global Medical Products arm through the USD 1.2 billion acquisition of Specialty Networks, broadening therapeutic integration opportunities.

Technology differentiation centers on AI-powered fever-prediction algorithms embedded in wearables, as seen in Withings’ ScanWatch 2 which uses Greenteg’s CALERA sensor for 24/7 core-temperature tracking. Vendors pursue vertical integration to mitigate chip shortages, signing multi-year wafer contracts or acquiring MEMS-sensor startups. Platform economics become decisive: Omron’s cloud-based VitalSight program locks providers into subscription dashboards, raising switching costs and recurring revenue.

Regulatory shifts also reshape rivalry. The FDA’s 2025 510(k) exemption could commoditize entry-level digital sticks, spurring incumbents to migrate consumers toward premium smart models that add SaaS layers. Meanwhile, EU MDR compliance weeds out smaller brands unable to fund post-market surveillance, nudging the competitive balance toward scaled enterprises. Environmental pressure accelerates the mercury-free transition, giving early adopters of sustainable production processes a marketing edge in public-sector tenders.

Medical Thermometer Industry Leaders

American Diagnostic Corporation

Exergen Corporation

Actherm Medical Corp.

A&D Company Limited

CITIZEN SYSTEMS JAPAN CO. LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA exempts Class II clinical electronic thermometers from 510(k) review while retaining quality-system obligations.

- March 2025: Healthy Together acquires Kinsa Health, integrating 3 million smart thermometers to expand AI-driven illness forecasting.

- October 2024: Omron Healthcare unveils a data-solutions strategy aiming for JPY 100 billion sales by FY 2027, blending temperature sensors with population-health analytics.

- May 2023: Greenteg and University Hospital of Basel demonstrate continuous fever-tracking accuracy in wrist-worn sensors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical thermometer market as all factory-built devices dedicated to measuring human core or surface body temperature in clinical, home-care, and remote-monitoring settings, whether contact or contact-less, single-use or reusable, digital, infrared, or mercury-based.

Scope Exclusion: Industrial, veterinary, and process thermometers remain outside the study.

Segmentation Overview

- By Product Type

- Mercury-Based

- Mercury-Free

- Infrared (Contact-less)

- Digital (Contact)

- Smart / Connected

- By Measurement Point

- Forehead

- Ear (Tympanic)

- Oral/Axillary

- Rectal

- By End User

- Hospitals

- Clinics and Physician Offices

- Home-care Settings

- Others

- By Patient Age Group

- Neonatal

- Pediatric

- Adult

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed manufacturing engineers in the United States and China, hospital procurement heads across six regions, and community pharmacists in emerging markets to validate usage intensity, channel mark-ups, and migration toward non-contact devices. Expert calls also tested our early CAGR assumptions and confirmed price-erosion rates in bulk tenders.

Desk Research

We began with publicly available datasets from the World Health Organization, the United States FDA recall files, Eurostat's medical-device trade tables, and UN Comtrade export codes for HS 9025, which reveal global thermometer flows. Company 10-K filings, recent device approvals, and Association for the Advancement of Medical Instrumentation guidance helped us size installed bases and average selling prices.

Subscription platforms such as D&B Hoovers and Dow Jones Factiva supplied revenue splits, while Questel patent counts highlighted innovation pockets that signal demand shifts. Many other vetted secondary sources supported gap filling and cross-checks; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction from country-level import plus domestic production values for HS 9025 established the 2025 revenue pool, and one bottom-up pass using sampled unit sales multiplied by average selling price from leading suppliers allowed us to fine-tune outliers. Variables that feed the model include neonatal birth counts, fever-clinic visit volumes, penetration of infrared units within hospital wards, global mercury-phase-out progress, and e-commerce share for home devices. Forecasts to 2030 rely on multivariate regression blended with scenario analysis, using GDP per capita, healthcare spending, infection-incidence indices, and device-replacement cycles as drivers. Gap areas where supplier roll-ups were thin were interpolated with peer-country proxies that carry similar import dependence.

Data Validation & Update Cycle

Outputs pass a three-layer review that compares results with independent shipment tallies and retail scanner data. Variances beyond five percent trigger additional calls before sign-off. Our models refresh each year, and material recalls or pandemic waves prompt interim updates and a fresh analyst sweep before delivery.

Why Our Medical Thermometer Baseline Commands Reliability

Published estimates often diverge because firms choose distinct scope lines, price bases, and refresh cadences.

Key gap drivers here include whether non-clinical infrared guns are counted, the choice of factory-gate versus retail prices, and the treatment of disposable probe covers, which some studies bundle as thermometer revenue.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.29 B (2025) | Mordor Intelligence | - |

| USD 1.97 B (2025) | Global Consultancy A | Excludes smart Bluetooth units sold via online retail, uses only 2024 exchange rates |

| USD 2.98 B (2025) | Trade Journal B | Adds industrial safety thermometers and counts projected pandemic stockpiles |

| USD 2.30 B (2023) | Regional Consultancy C | Limited to North America and Europe, inflates global total by straight extrapolation |

The comparison shows that once scope misalignments and currency treatments are removed, Mordor Intelligence provides a balanced figure grounded in observable trade data and validated field insight, giving decision-makers a dependable starting point.

Key Questions Answered in the Report

What is the current size and growth outlook for the medical thermometer market?

The market totals USD 2.46 billion in 2026 and is projected to hit USD 3.55 billion by 2031, reflecting a 7.57% CAGR.

Why do mercury-free thermometers dominate sales?

Mercury-free models already hold 72.22% share because global bans such as the EU’s Regulation 2017/852 restrict mercury devices and push hospitals and consumers toward safer digital alternatives.

Which end-user segment is expanding the fastest?

Home-care environments show the highest growth at 8.74% CAGR through 2031 as remote-patient-monitoring programs gain reimbursement support and clinicians integrate temperature checks into telehealth workflows.

Which geographic region offers the strongest growth potential?

Asia-Pacific is advancing at a 9.11% CAGR thanks to large aging populations, expanding healthcare infrastructure and national digitization initiatives that favor connected thermometry.

Page last updated on: