Market Overview

| Study Period | 2020 - 2031 |

|---|---|

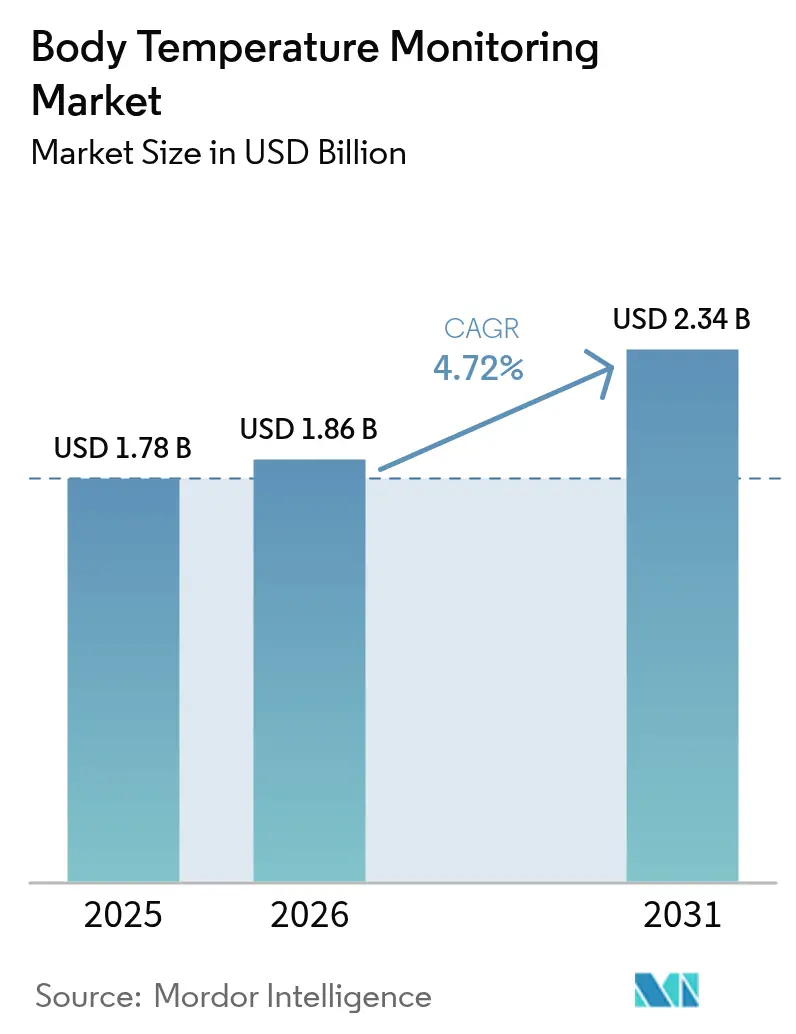

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

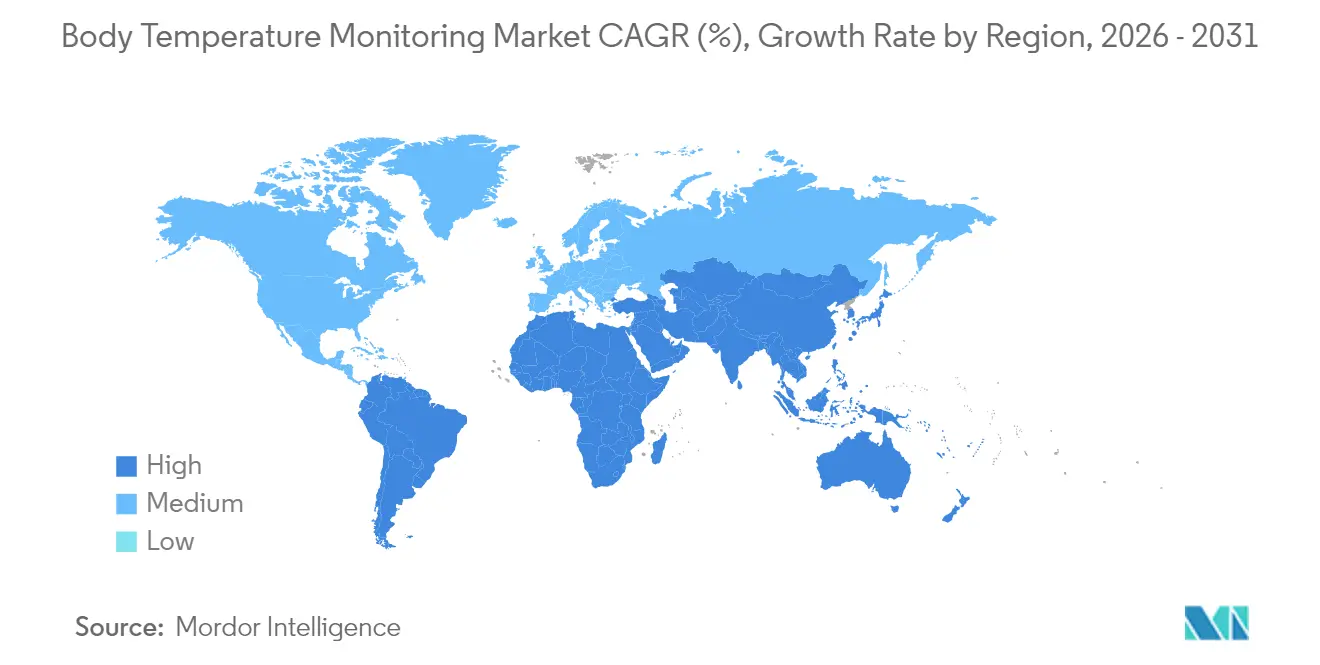

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Temperature Monitoring Market Analysis by Mordor Intelligence

body temperature monitoring market size in 2026 is estimated at USD 1.86 billion, growing from 2025 value of USD 1.78 billion with 2031 projections showing USD 2.34 billion, growing at 4.72% CAGR over 2026-2031. The healthy growth reflects a transformation from episodic thermometry toward always-on, IoT-enabled ecosystems that fuse temperature with hemodynamic and respiratory data. Pandemic-era screening routines, an aging global population, and regulatory incentives that phase out mercury devices all continue to stimulate demand. Contact devices retain clinical trust because of accuracy, but non-contact infrared (IR) systems and wearables expand quickly as hospitals, workplaces, and households embrace hygienic, touch-free workflows. Manufacturers accelerate vertical integration and software partnerships, aiming to bundle sensors, analytics, and cloud dashboards into one platform.

Key Report Takeaways

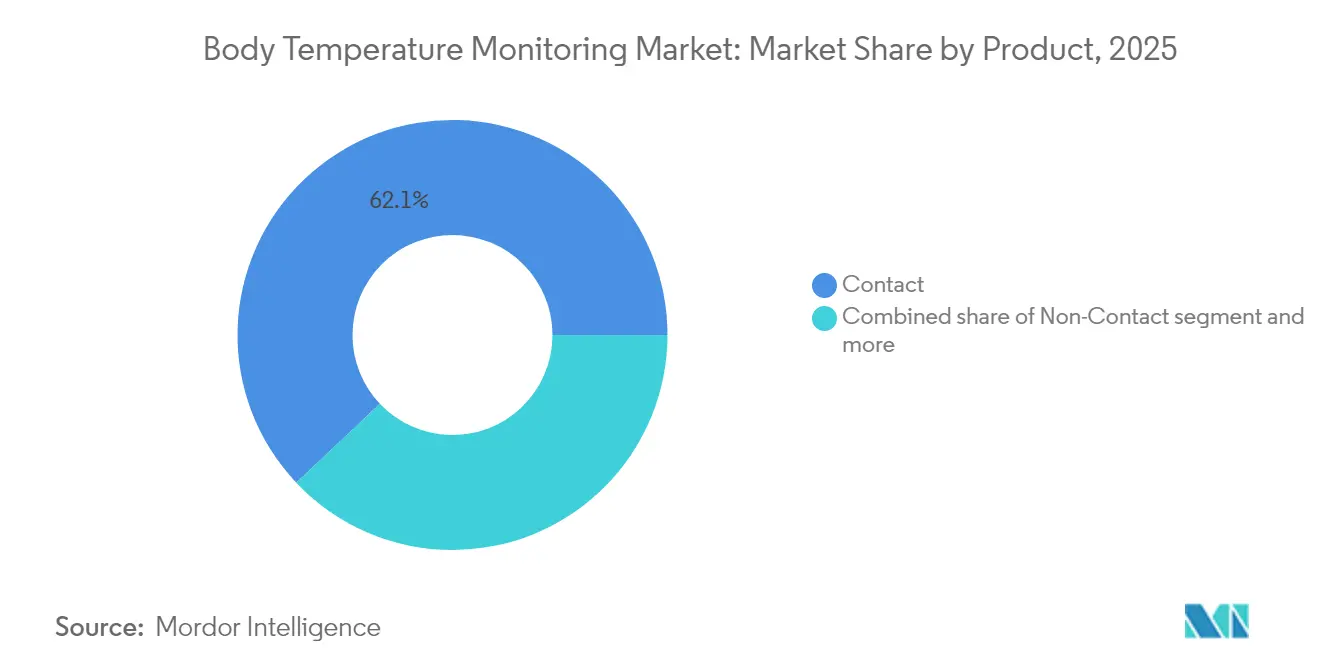

- By product type, contact devices led with 62.05% of body temperature monitoring market share in 2025, while non-contact IR systems record the highest projected CAGR through 2031.

- By distribution channel, the offline segment held 70.88% of the body temperature monitoring market size in 2025, whereas online platforms are set to post the fastest CAGR to 2031.

- By application, oral cavity measurement captured 35.05% revenue share in 2025; wearable and other emerging sites are projected to grow at the quickest pace over the forecast horizon.

- By end-user, hospitals accounted for 53.10% of demand in 2025, yet home-care environments are expanding at the strongest CAGR to 2031.

- By geography, North America commanded 41.10% of 2025 revenue, while Asia-Pacific is forecast to grow at 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Body Temperature Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infectious-disease outbreaks elevate screening demand | +1.2% | Global, higher in APAC and MEA | Short term (≤ 2 years) |

| Digital and wearable sensor innovation lowers ownership cost | +1.1% | North America and EU lead, APAC follows | Medium term (2-4 years) |

| Hygiene-focused shift to non-contact IR thermometers | +0.9% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Expanding pediatric and geriatric cohorts require frequent checks | +0.8% | Global, highest in North America and Europe | Long term (≥ 4 years) |

| Smart-hospital IoT integration of temperature data | +0.7% | North America and EU core, spill-over to APAC | Long term (≥ 4 years) |

| Fertility-tracking wearables using wrist-skin temperature | +0.4% | Global, highest penetration in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Infectious-Disease Outbreaks Drive Screening Demand

Temperature checks moved from ad-hoc crisis responses to permanent daily routines in hospitals, schools, and corporate campuses. The United States Food and Drug Administration issued performance recommendations for mass thermal screening systems, signaling regulatory acceptance of non-contact public venue deployment. AI-enhanced calibration and sensor fusion—linking thermal images with heart-rate or SpO₂ inputs—now address the false-negative risk exhibited in early pandemic devices.

Digital & Wearable Sensor Innovations Lower Ownership Cost

Miniaturized thermistors, better power management, and relaxed regulatory pathways have pushed continuous temperature tracking into consumer wearables. Withings integrated greenteg’s CALERA sensor into ScanWatch 2[1]greenteg AG, “Introducing ScanWatch 2 by Withings: 24/7 core body temperature tracking with CALERA,” greenteg.com, enabling 24/7 core body temperature logging in a mass-market smartwatch. In June 2025 the US FDA exempted select Class II clinical electronic thermometers[2]U.S. Federal Register, “Medical Devices; Exemptions From Premarket Notification—Class II Devices: Clinical Electronic Thermometers,” federalregister.gov from premarket notification, shortening launch cycles and lowering compliance cost.

Hygiene-Focused Shift to Non-Contact IR Thermometers

COVID-19 hygiene protocols gave IR thermometers a permanent foothold in healthcare and public safety. Clinical literature still flags measurement drift and environmental sensitivity, but manufacturers now use computer-vision alignment, dual-sensor averaging, and adaptive emissivity algorithms to hit tighter accuracy bands. Regulatory advisories caution against overreliance, yet facility managers accept the trade-off between absolute accuracy and infection-control convenience.

Expanding Pediatric & Geriatric Cohorts Needing Frequent Checks

Aging societies and higher neonatal survival rates increase daily monitoring events. The University of Washington’s smart thermal earring[3]Stefan Milne, “UW-Developed Smart Earrings Can Monitor a Person’s Temperature,” UW News, washington.edu achieved closer agreement with ingestible core temperature capsules than leading smartwatches, offering a painless option for children anxious about traditional probes. Geriatric home-care programs add continuous sensors to reduce emergency readmissions and support predictive analytics that flag infection earlier.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy and user-error concerns with IR devices | -0.6% | Global, higher impact in regulated markets | Short term (≤ 2 years) |

| Privacy pushback on continuous wearable data capture | -0.4% | North America and EU, emerging in developed APAC | Medium term (2-4 years) |

| Mercury-device bans squeeze low-income markets | -0.3% | Developing regions in Africa and Asia | Medium term (2-4 years) |

| False-security risk from mass thermal imaging | -0.2% | Global, especially high-traffic institutional settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accuracy & User-Error Concerns with IR Devices

Peer-reviewed evaluations show several forehead IR thermometers deviating by ±1 °C or more in uncontrolled environments, below clinical fever-screening thresholds. Variability from ambient temperature, humidity, and user alignment drives recall events and additional hospital protocol layers, tempering adoption pace. Suppliers invest in training, auto-distance targeting, and multi-spectral modules, yet fundamental physics of surface emissivity still limits error reduction in low-cost hardware.

Mercury-Based Device Bans Squeezing Low-Income Markets

WHO’s USD 134 million project across Albania, Burkina Faso, India, Montenegro, and Uganda accelerates mercury thermometer removal[4]World Health Organization, “Nations unite to eliminate mercury-containing medical devices,” who.int to reduce 23,350 kg of spill risk, but replacement units cost multiples of legacy glass models. Budget-constrained clinics delay upgrades, shrinking near-term unit volumes before donor financing and local low-cost digital substitutes fill the gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Contact Devices Maintain Commanding Lead

The contact segment accounted for 62.05% of the body temperature monitoring market in 2025 thanks to proven accuracy and decades-long clinician familiarity. Ear probes, digital stick thermometers, and ingestible pills anchor intensive-care protocols, especially where medication dosing or sepsis surveillance requires sub-0.2 °C precision. Non-contact IR devices are forecast to be the fastest-growing sub-category through 2031, propelled by infection-control guidelines and workplace deployment mandates. Continuous wearables, such as FDA-cleared Radius Tº and skin patches used in oncology trials, illustrate a shift toward persistent measurement that bridges hospital discharge and home recovery. Device makers now position hybrid portfolios, pairing disposable contact probes for invasive procedures with cloud-connected IR kiosks for visitor screening, allowing each care setting to select the optimal workflow.

The contact segment’s breadth supports innovation beyond simple sticks. High-acuity wards increasingly automate readings via cable-free oral probes docked in central nursing dashboards. Algorithm-ready data streams enable early sepsis detection models and medication titration engines. Meanwhile, non-contact system improvements in optics, distance-to-spot ratio, and ambient compensation have narrowed the accuracy gap to ±0.4 °C in some premium SKUs. Suppliers layer AI on board to flag poor aiming or excessive environmental drift, reinforcing user confidence and expanding addressable clinical cases.

By Distribution Channel: Offline Procurement Still Dominates

Hospitals and large clinics rely on vetted distributors, generating 70.88% of 2025 revenue through the offline channel. Group purchasing organizations bundle thermometers with infusion pumps and monitors, favoring suppliers that offer clinical evidence and technical service contracts. Despite offline strength, the body temperature monitoring market witnesses rapid e-commerce uptake as small practices and households order direct from brand sites or marketplaces. Online sales surged during COVID-19 lockdowns and sustained momentum as consumers accepted self-care roles. Emerging direct-to-consumer brands leverage data dashboards, app-based coaching, and firmware updates to differentiate beyond price.

Distributors respond by digitizing catalogues and enabling click-and-collect models that preserve fulfillment control. Manufacturers experiment with subscription-based firmware analytics, creating recurring revenue on top of device shipments. Regulation continues to anchor a sizable offline base because many institutional buyers need calibration certificates and technical in-service training not yet matched by pure-play e-commerce storefronts.

By Application: Oral Cavity Remains Familiar but New Sites Surge

Oral thermometry captured 35.05% revenue in 2025 due to comfort, ease of cleaning, and proximity to core blood flow. Nevertheless, segments such as the temporal artery, wrist, and ear are expanding fastest. Wearables harness thin-film thermistors on the radial artery, continuous power management, and Bluetooth Low-Energy links to deliver clinical-grade trends without manual intervention. Research from the University of Washington demonstrated that a jewelry-style thermal earring beats smartwatch accuracy during rest, pointing to product diversification aimed at children and lifestyle users.

Rectal routes remain niche but indispensable for neonatal and post-anesthesia accuracy. The application spectrum thus spans single-use probe covers to AI-enabled biosensor patches, challenging suppliers to optimize calibration algorithms for different skin regions, sweat profiles, and motion artefacts. Rapid growth in fertility tracking platforms keeps wrist and skin-patch technologies in focus, supported by sensors that detect luteal-phase shifts as small as 0.1 °C.

By End-User: Hospital Demand Evolving Toward Home Settings

Hospitals delivered 53.10% of global revenue in 2025, driven by bundled procurement of multi-parameter monitoring pods that incorporate temperature channels. Intensive care and emergency departments require minute-to-minute data resolution to guide antimicrobial stewardship and fluid therapy. Yet cost-pressure and value-based reimbursement steer convalescence to home environments where lower-cost wearables continue the continuity of care. The home-care segment is projected to record the fastest CAGR to 2031.

Device designs now prioritize intuitive placement, smartphone visualization, and automatic clinician alerts to suit lay caregivers. Pharmacies and telehealth portals supply starter kits with disposable patches and connected tablets. Schools, offices, and travel hubs represent emerging institutional end-users, embedding thermal imaging gates within broader access-control systems. The diversification strands revenue resilience across public health, consumer wellness, and professional care niches.

Geography Analysis

North America delivered the largest regional share at 41.10% in 2025, benefiting from mature reimbursement environments, hospital digitization programs, and early adoption of AI-enabled analytics. Integration partnerships between academic medical centers and OEMs fast-track pilots for multi-sensor platforms that combine temperature, blood oxygen, and motion data to predict deterioration events. The region’s stable 4.31% CAGR is underwritten by chronic disease prevalence and an expanding remote-care ecosystem that reimburses continuous monitoring hardware.

Asia-Pacific is the fastest-growing territory at 5.52% CAGR, linked to rising middle-class healthcare expectations and government stimulus for smart hospitals. China’s domestic manufacturers leverage scale and component verticalization to ship economical IR thermometers into export and domestic channels. Japan’s super-aged society drives home-care wearable uptake. India’s digital-health policy encourages remote vital sign kits in rural clinics, broadening the body temperature monitoring market footprint beyond urban tertiary centers. High smartphone penetration simplifies user onboarding for app-centric devices, while multinational brands form joint ventures to navigate heterogeneous regulatory schemes.

Europe maintains a robust trajectory with a 4.68% CAGR to 2031. Stringent data-protection rules catalyze on-device encryption and local gateway storage solutions, improving patient trust. Mercury device bans progress under the Minamata Convention alignment, triggering accelerated replacement cycles for digital and IR units. The Middle East and Africa, growing at 5.29% CAGR, channels oil revenues into tertiary healthcare clusters and public screening infrastructure. Mass events such as pilgrimages amplify demand for rapid, non-contact screening portals. South America progresses at 5.03% CAGR as public insurers upgrade basic equipment and private hospitals install connected monitoring suites. Currency swings and import tariffs continue to influence price positioning, rewarding value engineering and local assembly strategies.

Regulatory Landscape

Regulation of body temperature monitoring devices is tightening around performance validation while streamlining pathways for lower-risk products. In the United States, the FDA published a final order in June 2025 exempting specified Class II clinical electronic thermometers from 510(k) premarket notification, while keeping devices with telethermographic or continuous measurement functions under closer scrutiny. The FDA classification framework for clinical electronic thermometers under 21 CFR 880.2910 remained an active reference point, with the regulation text updated in the eCFR as of April 20, 2026.

In Europe, the Medical Device Regulation (EU) 2017/745 continues to raise documentation, clinical evaluation, and post-market surveillance requirements, with transitional provisions for certain legacy devices still phasing out under defined conditions. China is also updating compliance benchmarks: YY 9706.256-2023 for clinical thermometer safety and performance took effect on May 1, 2026, superseding YY 0785-2010. Internationally, ISO 12487:2026 (published May 21, 2026) adds a dedicated clinical-investigation framework for medical electrical thermometers used in indirect measurement mode, increasing the emphasis on evidence generation and harmonized test methods for suppliers operating across regions.

Value Chain Analysis

The value chain for body temperature monitoring devices starts with upstream component and material supply, including thermistors and infrared thermopile sensors, microcontrollers for signal conditioning, displays, batteries, and molded medical-grade plastic housings. Manufacturing typically combines automated SMT electronics assembly with precision injection molding, followed by calibration against reference sources and functional testing. These steps become more demanding for non-contact IR and connected devices, where alignment, ambient compensation, and software algorithms shape measured output.

Midstream players include OEM assemblers and specialized module suppliers, along with tooling and molding vendors that support scalable production of housings and probe parts. Downstream, regulated distribution remains central for clinical channels because hospitals often require calibration documentation, service support, and compliance-ready labeling, while consumer devices increasingly move through e-commerce and direct-to-consumer storefronts. Regulatory requirements also affect how value is captured across the chain: the June 2025 FDA action narrowed 510(k) exemption eligibility by device function, reinforcing the need for design controls, standards-based testing (for example, ISO 80601-2-56 and related ASTM methods used in clinical thermometer verification), and post-market quality systems for suppliers serving institutional buyers.

Competitive Landscape

More than 75 active manufacturers generate a moderately fragmented competitive field. Tier-one firms such as Philips, Omron, and Baxter provide broad device portfolios, global distribution, and strong regulatory dossiers. Mid-tier specialists like Blue Spark Technologies and Kinsa Health focus on connected consumer or patch solutions, differentiating through cloud analytics and epidemiological data dashboards.

Technology stacking defines competitive advantage. Vendors embed Bluetooth Low-Energy or Wi-Fi to push data into hospital EMRs or consumer wellness apps. AI layers deliver early-warning scores or fertility predictions, turning raw temperature into actionable insight. Component sourcing shifts toward CMOS-based microbolometers and high-density thermistor arrays, lowering the bill of materials while raising resolution. Service wrap-arounds, such as calibration-as-service and predictive maintenance, strengthen recurring revenue.

Regulatory agility becomes a second differentiator. FDA deregulation of low-risk digital sticks shortens release cycles, favoring agile firms. European IVDR compliance boosts entry barriers, encouraging outsourcing of technical documentation to speciality consultancies. Sustainability credentials emerge as a purchase criterion, with hospitals selecting mercury-free, low-plastic packaging to align with net-zero goals. Companies able to balance accuracy, cost, connectivity, and ESG attributes inch ahead in tenders.

Body Temperature Monitoring Industry Leaders

Baxter International

Helen of Troy Limited

Koninklijke Philips N.V.

Microlife Corporation

Omron Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in body temperature monitoring are clustering around continuous measurement, workflow integration, and improved robustness in non-contact screening. FDA actions in June 2025 that exempted specified clinical electronic thermometers from 510(k) premarket notification reduce friction for iterative updates in low-risk, spot-measurement devices, supporting portfolio refresh cycles and faster software-driven feature upgrades where allowed. At the same time, higher scrutiny for continuous and telethermographic functions creates room for manufacturers that can provide standards-aligned validation packages and interoperable data outputs that fit into hospital monitoring stacks.

A second whitespace is emerging at the edge of core-temperature accuracy without adding invasive burden. In June 2026, research reported by MIT and published in Nature Electronics described a miniaturized ingestible temperature sensor (6 mm x 4 mm) demonstrated in swine models, pointing to a pathway for internal temperature monitoring in perioperative and other controlled clinical scenarios once translated into human-validated, regulated products. In parallel, the role of IEC 80601-2-59 for febrile screening thermographs and the growing use of connected patient-monitoring ecosystems create scope for hybrid systems that fuse temperature with additional physiological signals (such as heart rate or SpO2) to reduce user error and environmental drift in real-world settings.

Recent Industry Developments

- June 2026: Philips launched the IntelliVue Patient Monitor 6000 Series, positioned around flexible deployment and compatibility with existing IntelliVue MX supplies. The shared consumables and standardized configurations help hospitals scale temperature-inclusive monitoring while simplifying training and inventory management.

- September 2025: Baxter launched the Welch Allyn Connex 360 Vital Signs Monitor, which includes body temperature among the captured vital signs for adult, pediatric, and neonatal use. The system emphasizes connected workflows, including automated documentation into electronic medical records, aligning spot temperature capture with broader vital-signs integration.

- April 2024: Philips partnered with smartQare to automate and simplify continuous patient monitoring in and out of the hospital. The collaboration highlights the shift toward continuous sensing and digital workflows that reduce manual burden and extend monitoring beyond traditional bedside settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices and systems used to measure and monitor human body temperature for screening, diagnosis support, and ongoing patient monitoring across clinical and non-clinical settings, and then valued based on equipment sales and related usage in the study period.

Scope exclusions: We exclude industrial and laboratory temperature instruments that are not intended for human body temperature measurement.

Segmentation Overview

- By Product

- Contact

- Digital Thermometers

- Infrared Ear Thermometers

- Other Contact Products

- Non-Contact

- Non-contact Infrared Thermometers

- Thermal Scanners

- Wearable & Continuous-Monitoring Devices

- Contact

- By Distribution Channel

- Offline

- Online

- By Application

- Oral Cavity

- Rectum

- Ear

- Other Applications

- By End-User

- Hospitals

- Clinics

- Home-care Settings

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To set market boundaries and starting assumptions, we review public health and device guidance, plus utilization signals that indicate where temperature monitoring is used most. Sources that help here include US FDA device safety communications, CDC clinical guidance, WHO technical guidance, and OECD health statistics, and these are then combined with published clinical evidence from peer-reviewed journals.

We also review publicly available company filings, investor presentations, product brochures, and hospital procurement notes to identify shifts in product mix, for example, contact versus non-contact use. Where helpful, we reference paid subscriptions for company financials and news, and we use a patent database to understand sensor and wearable innovation direction. The sources listed are illustrative only, and many other public and paid references were checked to collect data, validate assumptions, and clarify uncertainties.

Primary Interviews and Surveys

Primary calls and surveys were used to pressure-test adoption patterns for contact thermometers, non-contact infrared devices, and continuous monitoring wearables across hospitals, clinics, and home care use. We spoke with a mix of manufacturers, distributors, clinical users, and procurement-focused respondents across APAC, EMEA, and the Americas to reduce gaps from desk research and confirm assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 14% | Managers: 51% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up blended logic. From the top-down side, we reconstruct demand pools using healthcare delivery and screening intensity signals, then translate them into device volumes by applying realistic penetration and replacement cycles for each main device class.

The model uses indicators such as hospital and clinic throughput, home care monitoring adoption, the mix shift between contact and non-contact measurement, average selling price ranges by device type, replacement and calibration cycles, and infection seasonality that temporarily lifts screening demand. Where public data is thin, gaps are handled using interview-backed ranges, followed by conservative mid-points that are stress-tested against observed channel behavior.

To corroborate totals, selective bottom-up checks are run using sampled supplier revenue splits, channel markups, and estimated unit shipments inferred from product positioning and distribution coverage. For forecasting, we run scenario analysis supported by expert expectations around care-at-home expansion, procurement normalization after peak screening periods, and the pace of adoption for wearable continuous temperature monitoring.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as regional healthcare spending direction, device import and export patterns where visible, and the expected share split across major care settings. When an output looks inconsistent, we revisit assumptions tied to pricing, replacement timing, or adoption rates, then trigger clarifying outreach with the most relevant respondent types.

Before sign-off, the work is reviewed in multiple steps so calculation links, year alignment, and currency conversion timing stay consistent across tables. Reports are refreshed annually, and interim updates are added when material events occur, after which a final pre-delivery review pass is completed so clients receive the latest view.

Mordor Intelligence's Global Body Temperature Monitoring Market Market Estimate Compared With Other Published Estimates

It is normal to see different market values for body temperature monitoring because teams draw the market boundary differently and use different price and volume logic. Differences also come from how fast older product types are assumed to phase down, and whether wearables are counted as a core temperature monitoring device or as a broader remote monitoring add-on.

By checking device-type level adoption, ASP progression, and replacement cycles with annual refresh rules, Mordor Intelligence keeps the modeled total tied to contact and non-contact temperature monitoring demand rather than letting adjacent patient monitoring categories inflate the number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.86 B (2026) | |

| Global Consultancy A | USD 1.77 B (2024) | Uses an earlier base year and typically blends medical and wellness use without fully separating one-time screening spikes from ongoing monitoring, which can shift the starting point downward while keeping a higher long-run growth path. |

| Industry Publisher B | USD 2.09 B (2025) | Includes a wider basket of thermometer types and tends to treat some remote monitoring wearables as fully in-scope temperature monitoring, which can raise the counted revenue even when temperature is a secondary measured signal. |

Overall, the spread in published values is mainly explained by year selection, how wearables are treated, and how pricing is normalized across clinical and home settings. With clear inclusion rules and cross-checks that link demand indicators to unit and price math, the estimate stays traceable and repeatable when new data points are added.

Key Questions Answered in the Report

What is driving the rapid uptake of non-contact thermometers in clinical settings?

Stricter infection-control protocols established after COVID-19 have made touch-free infrared and thermal imaging devices a preferred choice for routine patient screening and visitor triage.

How are wearable sensors changing body-temperature monitoring practices?

Continuous skin-patches and smartwatches stream temperature data to cloud dashboards, enabling early detection of infection and allowing clinicians to track trends without manual spot checks.

Why are hospitals integrating temperature data into broader patient-monitoring platforms?

Connecting temperature with hemodynamic and respiratory metrics in a single interface supports earlier sepsis alerts and reduces the workload associated with independent device management.

What role do mercury-elimination initiatives play in product development?

Global bans on mercury instruments compel manufacturers to design low-cost digital alternatives that match the affordability of legacy glass thermometers while eliminating hazardous waste.

How is regulatory policy affecting innovation speed in this industry?

Recent FDA exemptions for certain low-risk electronic thermometers shorten approval timelines, encouraging companies to release software-enabled upgrades and iterate hardware more quickly.

What competitive strategy is most common among leading vendors today?

Established device makers are acquiring AI and IoT startups to bundle advanced analytics with traditional hardware, positioning themselves as end-to-end remote patient-monitoring providers.

Page last updated on: