Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

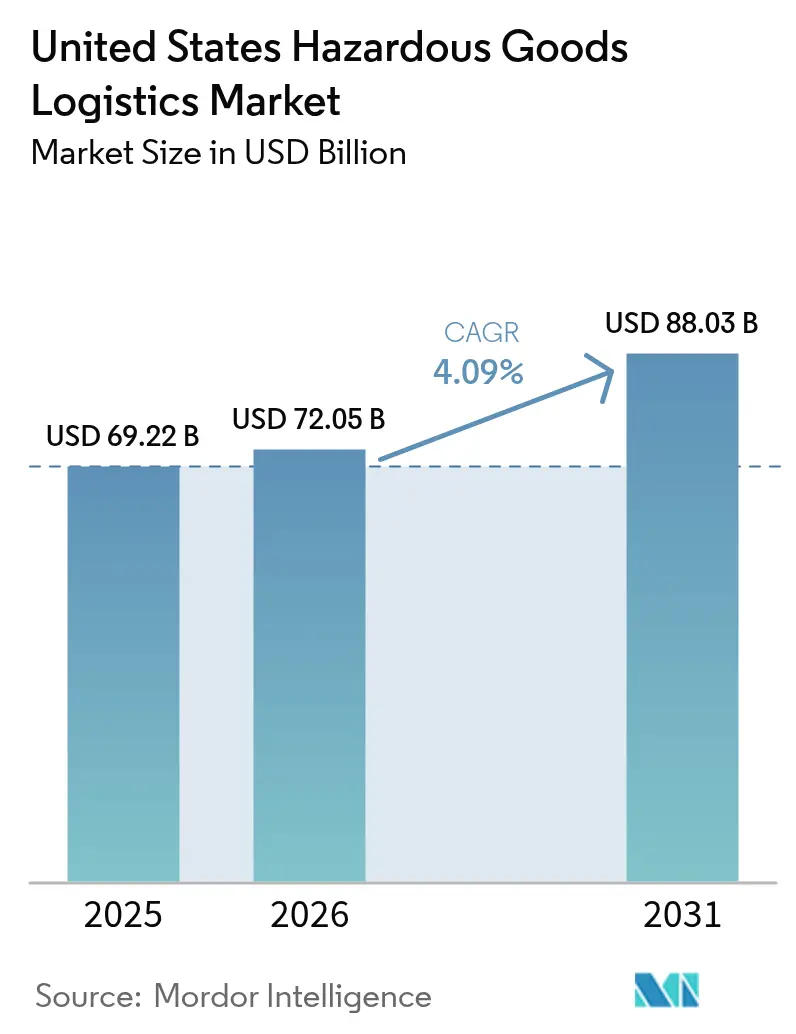

| Base Year Market Size (2025) | USD 69.22 Billion |

| Market Size (2026) | USD 72.05 Billion |

| Market Size (2031) | USD 88.03 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

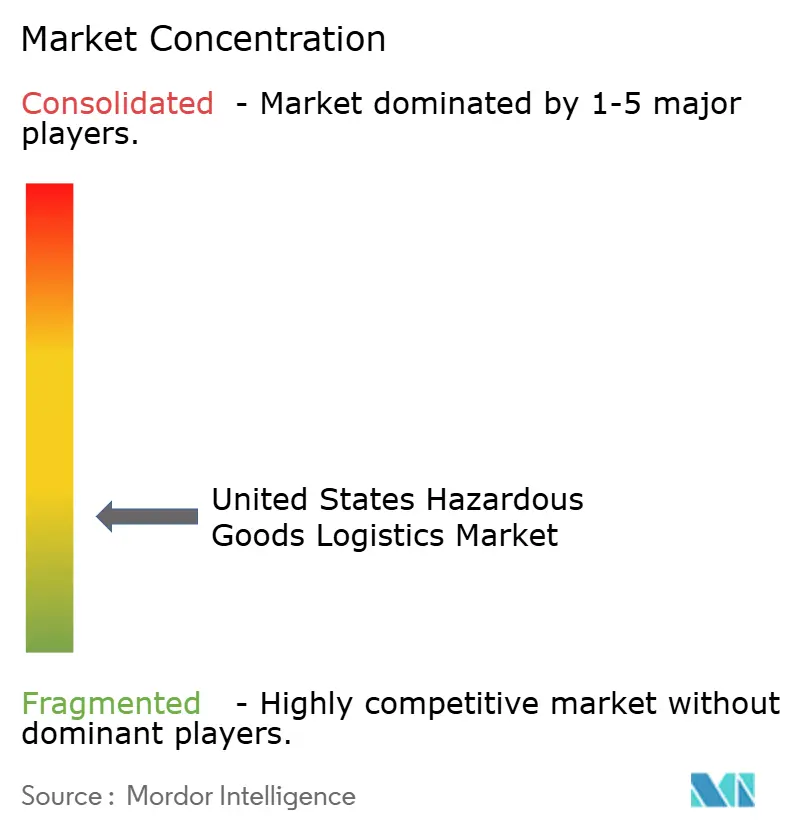

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Hazardous Goods Logistics Market Analysis by Mordor Intelligence

The United States Hazardous Goods Logistics Market size was valued at USD 69.22 billion in 2025 and estimated to grow from USD 72.05 billion in 2026 to reach USD 88.03 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031).

The steady trajectory reflects tightening OSHA and PHMSA oversight, increased petrochemical production, and a shift toward technology-enabled supply chains. Transportation maintains dominant value because most hazmat moves remain over-the-road or by rail, yet growth is spreading to value-added services such as real-time monitoring and compliance documentation. LNG export build-outs and hydrogen corridors are multiplying long-haul opportunities, while e-commerce volumes of ORM-D goods bring hazmat handling requirements into parcel networks. Investments in IoT sensor platforms and blockchain documentation are migrating from pilot programs to standard operating practice as shippers demand visibility and evidence of compliance. Digitization therefore evolves from optional feature to basic qualification for bids in the United States hazardous goods logistics market.

Key Report Takeaways

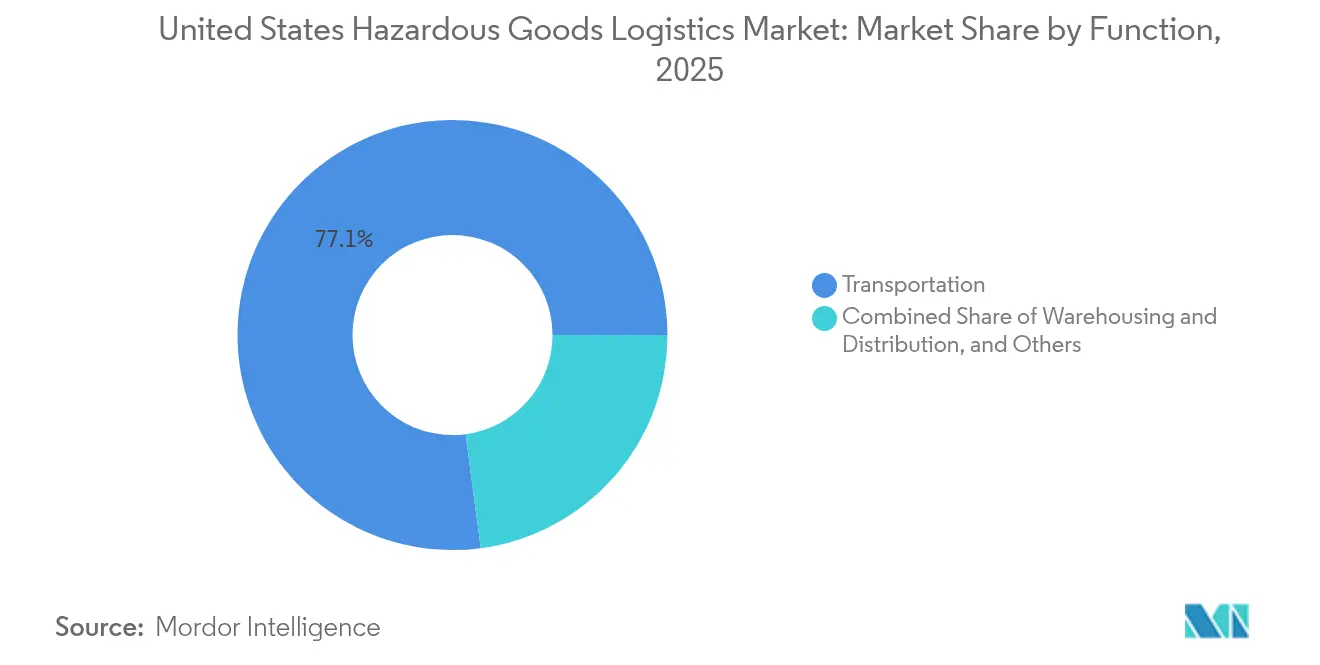

- By function, transportation commanded 77.10% of United States hazardous goods logistics market share in 2025; value-added services is forecast to post the fastest 3.72% CAGR through 2031.

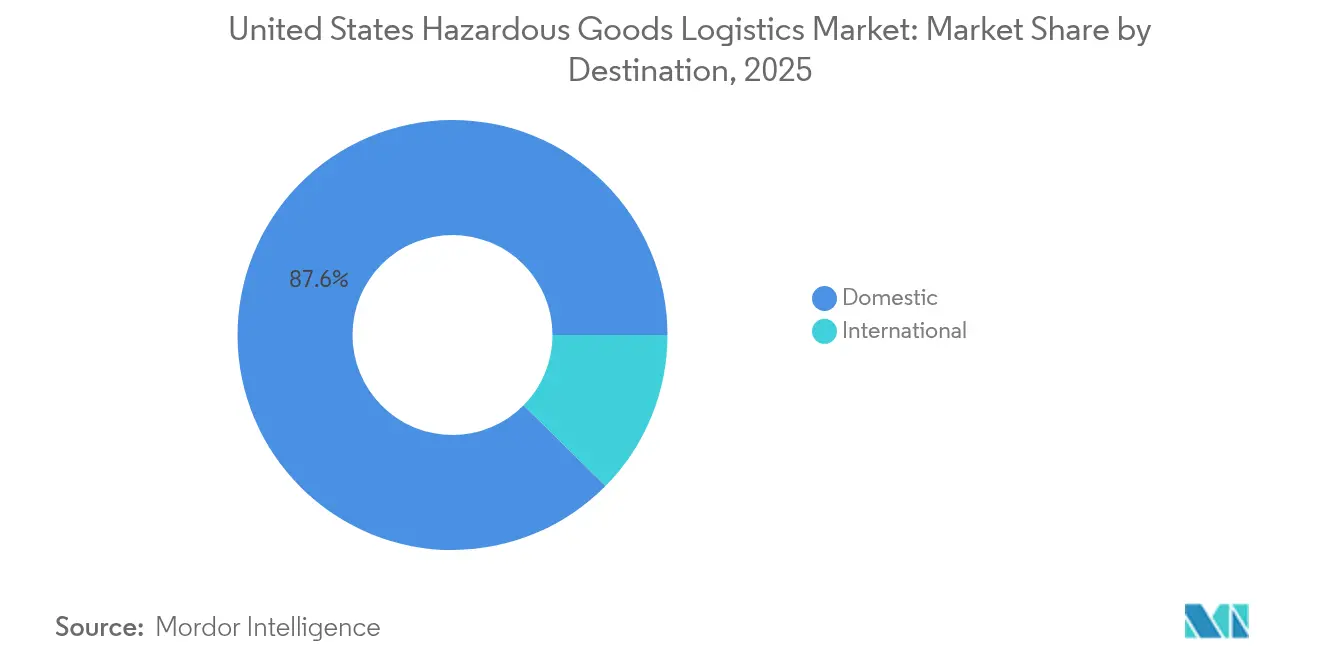

- By destination, domestic flows held 87.60% share of the United States hazardous goods logistics market size in 2025, while international shipments expand at a 4.28% CAGR to 2031.

- By end-use industry, chemicals & petrochemicals accounted for 34.60% share of the United States hazardous goods logistics market size in 2025; healthcare & pharmaceuticals advances at a 4.86% CAGR through 2031.

- By region, the South led with 30.70% of United States hazardous goods logistics market share in 2025; the West accelerates at 4.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Hazardous Goods Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust domestic petrochemical output growth | 1.2% | South, Midwest | Long term (≥ 4 years) |

| Rise in e-commerce shipment of ORM-D & consumer hazmat | 0.8% | Global, with concentration in West and Northeast | Medium term (2-4 years) |

| Expansion of LNG & hydrogen fuel supply chains | 0.9% | South, West | Long term (≥ 4 years) |

| Lithium-ion battery UN 3480/3481 volumes soaring | 0.7% | Global | Short term (≤ 2 years) |

| Tightening OSHA/PHMSA compliance enforcement | 0.4% | Global | Short term (≤ 2 years) |

| DoD modernization driving explosive class shipments | 0.3% | South, West | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Domestic Petrochemical Output Growth

Gulf Coast ethane crackers and propane dehydrogenation units continue to expand, securing low-cost feedstock that feeds new tank truck, rail, and pipeline demand. Terminal capacity projects around Houston and Louisiana reduce transfer bottlenecks yet require specialized equipment and driver endorsements. Strong regional production draws incremental railcars certified to DOT-117 standards, reinforcing long-haul demand between coastal refineries and inland chemical hubs. Hiring pressures persist because hazmat-endorsed drivers command wage premiums that smaller fleets cannot match. The pull from petrochemical shippers therefore anchors long-term volume in the United States hazardous goods logistics market[1]“Hazardous Materials: Enhanced Enforcement Summary,” U.S. Department of Transportation, transportation.gov.

Rise in E-commerce Shipment of ORM-D and Consumer Hazmat

Direct-to-consumer channels now move aerosols, household cleaners, and battery-powered devices once relegated to B2B lanes. Parcel integrators retrofit sorting centers with fire-suppression upgrades and implement carrier training that meets PHMSA’s 49 CFR Part 173 packaging rules. Lithium battery volumes intensify complexity because UN 3480 and UN 3481 shipments need dangerous-goods declarations, yet customer expectations remain next-day delivery. Logistics providers embedding hazmat modules within warehouse management systems gain share as omnichannel retailers outsource compliance tasks. The shift enlarges last-mile density, adding incremental stops but raising revenue per shipment across the United States hazardous goods logistics market[2]“Lithium Battery Advisory,” Pipeline and Hazardous Materials Safety Administration, phmsa.dot.gov.

Expansion of LNG and Hydrogen Fuel Supply Chains

New liquefaction trains on the Gulf Coast and Pacific Northwest spur cryogenic tank truck procurement and vessel retrofits. Hydrogen projects, financed through federal clean-energy credits, demand tube-trailers rated for 10,000 psi plus personnel trained in high-purity protocols. The Port of Oakland’s USD 50 million terminal upgrade demonstrates public-sector commitment to alternative fuel trade lanes. Equipment costs and engineering compliance elevate barriers to entry, rewarding carriers with scale and capital access. Over the horizon, domestic hydrogen offtake contracts are expected to create continuous backhauls that improve network utilization across the United States hazardous goods logistics market.

Lithium-ion Battery UN 3480/3481 Volumes Soaring

Consumer electronics, medical devices, and electric power tools drive surging battery shipments under IATA DGR Section II revisions. Recent PHMSA advisories on damaged or defective lithium batteries require route-specific risk assessments and thermal-shield packaging. Carriers install real-time temperature and g-force sensors that trigger exception reports before cells reach runaway thresholds, reducing claim severity and insurance premiums. Specialized facilities for segregation and fire-rating are springing up near West Coast import ports, facilitating trans-load into domestic networks. These investments align with the broader digitization wave reshaping the United States hazardous goods logistics market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver and equipment shortages | -1.1% | Global, acute in Midwest and South | Short term (≤ 2 years) |

| Escalating hazmat insurance premiums | -0.6% | Global | Medium term (2-4 years) |

| Limited public-sector bulk rail capacity | -0.4% | Midwest, Northeast | Long term (≥ 4 years) |

| Community opposition to hazmat corridors | -0.3% | West, Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver and Equipment Shortages

Hazmat-certified CDL drivers remain scarce as retirements outpace training-school throughput. The DOT-117 tank-car manufacturing backlog extends beyond two years, curbing bulk chemical rail growth. Fleets bid up wages and offer sign-on bonuses, yet pass-through to shippers raises landed cost, dampening volume. Shortages hit rural lanes hardest, forcing petrochemical shippers to reposition assets, which inflates deadhead miles in the United States hazardous goods logistics market.

Escalating Hazmat Insurance Premiums

Large-loss incidents and higher civil liability ceilings push insurance underwriters to hike hazmat premiums by double-digit percentages. Smaller operators exit long-haul sectors when umbrella coverage exceeds operating margin. Carriers seek differentiated pricing by installing telematics, lane-specific risk scoring, and automated emergency-response alerting. Premium burdens accelerate consolidation as well-capitalized firms absorb market share across the United States hazardous goods logistics market[3]“2024 Penalty Adjustments,” Occupational Safety and Health Administration, osha.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Transportation Remains Core While Services Scale Up

Transportation retained 77.10% United States hazardous goods logistics market share in 2025 as shippers relied on multi-modal road and rail assets to connect refineries, chemical plants, and distribution centers. Road fleets deliver flexibility for last-mile moves, whereas rail unit trains equipped with DOT-117 cars capture bulk lanes that demand lower per-ton cost and improved safety. Marine operators invest in pressurized barges for LNG and chemical exports, while air cargo remains a niche for medical isotopes and emergency supplies.

Value-added services register a 3.72% CAGR, the fastest among functions, as shippers outsource SDS authoring, labeling, and real-time cargo telemetry. Warehousing follows with steady growth because strategically located hazmat facilities shorten haul lengths and mitigate driver-hour constraints. IoT integrations such as vibration and temperature sensors lower insurance deductibles, propelling incremental revenue. These developments indicate the United States hazardous goods logistics market is maturing from pure transport toward integrated service offerings that monetize compliance expertise.

By Destination: Domestic Dominance with International Momentum

Domestic shipments delivered 87.60% of United States hazardous goods logistics market size in 2025, reflecting the breadth of inland production and consumption. Petrochemicals from the Gulf Coast move to Midwest plastics converters, fertilizers flow from central plants to Corn Belt farms, and ORM-D parcels reach households nationwide. Standardized regulatory frameworks reduce documentation friction, maintaining cost efficiency.

International volumes, holding 12.40% share, accelerate at 4.28% CAGR as LNG and hydrogen offtake contracts expand export lanes and cross-border e-commerce stimulates small-parcel hazmat demand. Carriers integrate multilingual documentation modules and partner with foreign forwarders versed in IMDG and ADR standards. The blend of domestic scale and global expansion diversifies revenue streams across the United States hazardous goods logistics market.

By End-Use Industry: Chemicals Lead, Healthcare Surges

Chemicals & petrochemicals accounted for 34.60% of United States hazardous goods logistics market size in 2025, supported by low-cost natural gas feedstocks and robust domestic plastics demand. Bulk tank-truck and rail tanker utilization remains high, and new terminal capacity absorbs incremental output.

Healthcare & pharmaceuticals records the quickest 4.86% CAGR through 2031 as lithium-ion batteries power medical devices, and biologics require temperature-controlled hazmat packaging. Waste management grows due to circular-economy rules that mandate closed-loop handling for solvent and pesticide residues. The diversification underscores how end-use shifts distribute growth vectors across the United States hazardous goods logistics market.

Geography Analysis

The South’s 30.70% share rests on integrated refinery-petrochemical clusters, multi-commodity pipelines, and LNG export piers that funnel large cargo volumes into specialized tanker networks. Ongoing investments in dock capacity, hurricane-resilient storage, and automated valve systems safeguard throughput even amid extreme weather. Federal infrastructure grants channel funds to dredging and levee upgrades, cementing regional dominance in the United States hazardous goods logistics market.

The West grows fastest at 4.08% CAGR as hydrogen fueling corridors and renewable-diesel projects converge with technology-sector demand for high-spec lithium batteries. Pacific ports pilot electronic hazmat pre-notification systems that accelerate Customs clearance and reduce yard dwell. However, zoning disputes over fuel terminals and pipeline extensions underscore the need for community outreach programs to safeguard project timelines. State incentives for zero-emission drayage fleets compound asset turnover, steering equipment investment toward alternative fuel compatibility.

The Northeast and Midwest log steady growth tied to pharmaceutical clusters, specialty chemical mixers, and agricultural input suppliers. Rail bridge upgrades near Chicago and New York unlock limited additional hazmat capacity, but yard congestion remains a constraint. Shippers therefore adopt modal splits that favor short-haul trucks feeding intermodal ramps, balancing cost with compliance. Network reliability improvements support export ambitions for niche chemicals, reinforcing the national footprint of the United States hazardous goods logistics market.

Competitive Landscape

Competition is moderately fragmented leaving significant share for regional specialists. Global integrators such as Kuehne + Nagel and DSV deploy multimodal platforms that blend brokerage, contract logistics, and digital visibility. XPO Logistics extended last-mile capability via its USD 87 million NLM purchase, targeting consumer hazmat segments that value same-day delivery. Kenan Advantage Group continues bolt-on acquisitions that add ISO tank depots and specialty trailers, boosting density in chemical corridors.

Technology deployment sets winners apart. Leading fleets install sensor suites that transmit temperature, pressure, and door status in real time, feeding machine-learning engines that flag anomaly patterns. Shippers use dashboards to audit compliance, granting premium revenue to carriers demonstrating zero-incident records. Corporate ESG mandates also favor providers investing in low-emission powertrains; early adopters of hydrogen or battery-electric tractors gain competitive differentiation within the United States hazardous goods logistics market.

Scale additionally aids insurance negotiation. Large carriers spread risk over bigger fleets and routes, securing lower deductibles and enabling rate advantages over smaller rivals squeezed by premium inflation. Consolidation momentum should persist because private equity funds seek platform plays that can be scaled through tuck-ins across regional lanes. The result is a gradually tightening concentration ratio, yet niche carriers remain viable by specializing in high-hazard classes or geographic verticals underserved by larger networks.

United States Hazardous Goods Logistics Industry Leaders

Deutsche Post DHL Group

Kuehne + Nagel

DSV

XPO Logistics

Landstar System Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kenan Advantage Group acquired MC Tank Transport, adding 8 terminals, 3 ISO depots, and 175 hazmat-qualified drivers, expanding chemical transport reach across the Southeast and Midwest.

- July 2025: Schneider implemented Bluetooth-enabled load sensors for a paper manufacturer’s black-liquor shipments, slashing loading time from 4 hours to 45 minutes and enhancing driver retention.

- June 2024: PHMSA finalized the Real-Time Train Consist Rule mandating electronic hazmat train consists accessible to emergency responders within minutes, enhancing incident transparency.

- April 2024: PHMSA distributed 1.9 million updated Emergency Response Guides, ensuring first responders nationwide possess current hazmat incident procedures.

United States Hazardous Goods Logistics Market Report Scope

The US hazardous goods logistics market is segmented by function and destination. The report also covers insights on the different classes of dangerous goods, regulations and rules governing transportation of hazardous goods, technology involved, and packaging of hazardous goods, among others.

By Function

| Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Warehousing and Distribution | |

| Value-added Services |

By Destination

| Domestic |

| International |

By End-Use Industry

| Chemicals and Petrochemicals |

| Oil and Gas |

| Healthcare and Pharmaceuticals |

| Agriculture and Fertilizers |

| Manufacturing and Industrial |

| Waste Management and Recycling |

| Mining |

| Others |

By US Region

| Northeast |

| Midwest |

| South |

| West |

| By Function | Transportation | Road |

| Rail | ||

| Sea | ||

| Air | ||

| Warehousing and Distribution | ||

| Value-added Services | ||

| By Destination | Domestic | |

| International | ||

| By End-Use Industry | Chemicals and Petrochemicals | |

| Oil and Gas | ||

| Healthcare and Pharmaceuticals | ||

| Agriculture and Fertilizers | ||

| Manufacturing and Industrial | ||

| Waste Management and Recycling | ||

| Mining | ||

| Others | ||

| By US Region | Northeast | |

| Midwest | ||

| South | ||

| West |

Key Questions Answered in the Report

What is the projected value of the United States hazardous goods logistics market in 2031?

The market is expected to reach USD 88.03 billion by 2031.

Which region currently leads U.S. hazmat logistics by value?

The South region leads with 30.70% share because of its energy and petrochemical clusters.

Which functional segment shows the fastest growth?

Value-added services, expanding at a 3.72% CAGR through 2031 by integrating compliance and monitoring solutions.

How fast are international hazmat shipments growing?

International lanes are forecast to rise at a 4.28% CAGR as LNG exports and cross-border e-commerce accelerate.

What driver most boosts long-term growth?

Robust domestic petrochemical capacity expansion adds an estimated +1.2% to overall market CAGR.

Why are insurance costs rising for hazmat carriers?

Higher claim severity and stricter OSHA and PHMSA penalties push underwriters to lift premiums by double digits.

Page last updated on: