United States Timber Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.67 Billion |

| Market Size (2026) | USD 18.31 Billion |

| Market Size (2031) | USD 21.56 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

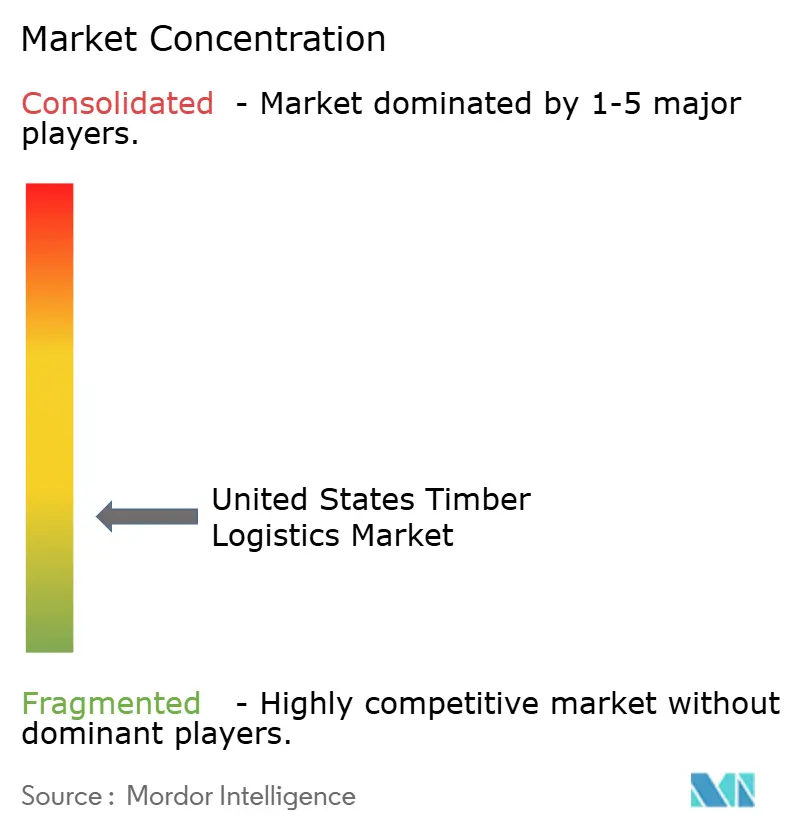

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Timber Logistics Market Analysis by Mordor Intelligence

The United States timber logistics market size was valued at USD 17.67 billion in 2025 and estimated to grow from USD 18.31 billion in 2026 to reach USD 21.56 billion by 2031, at a CAGR of 3.32% during the forecast period 2026-2031.

The United States timber logistics market is supported by a structural shift toward engineered wood and mass timber applications, a broader federal push to expand forest management, and the rising use of intermodal freight options in major timber corridors. The USDA committed USD 200 million under its National Active Forest Management Strategy and linked that effort to a target of 4 billion board feet annually by fiscal year 2028, which strengthens the long-run freight base tied to harvested and managed timber volumes[1]USDA Forest Service, “USDA Invests $200M to Expand Timber Production, Strengthen Rural Economies, Secure American Industry,” USDA, usda.gov. Intermodal adoption and southward sawmill investment are also shifting the operating center of the United States timber logistics market toward the Southeast, where fiber supply, mill additions, and inland port capacity are increasingly aligned. Driver shortages in specialized log hauling and seasonal road weight limits in northern corridors still disrupt capacity and delivery timing, especially during spring thaw periods. Chain-of-custody and due diligence costs remain a burden for smaller operators, yet policy support, regional mill growth, and specialized transport demand continue to provide a steady floor for the United States timber logistics market through 2031.

Key Report Takeaways

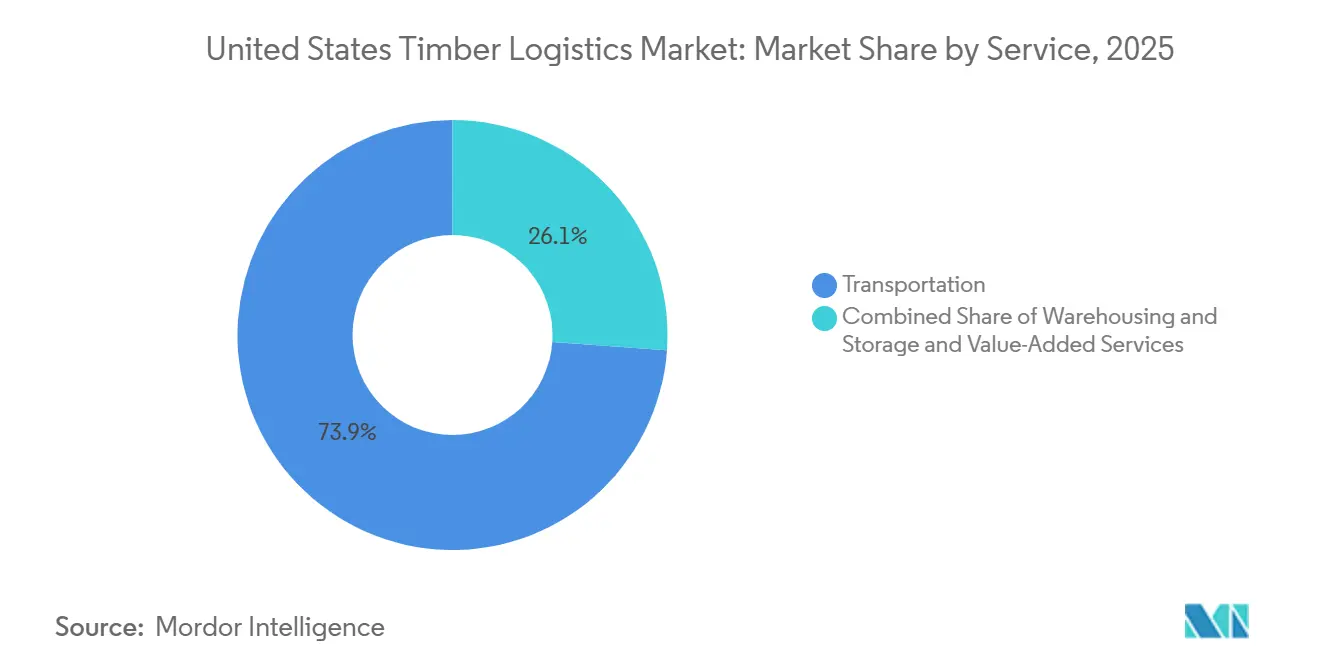

- By service, transportation held 73.87% of the United States timber logistics market share in 2025, while value-added services are projected to expand at a 4.52% CAGR through 2031.

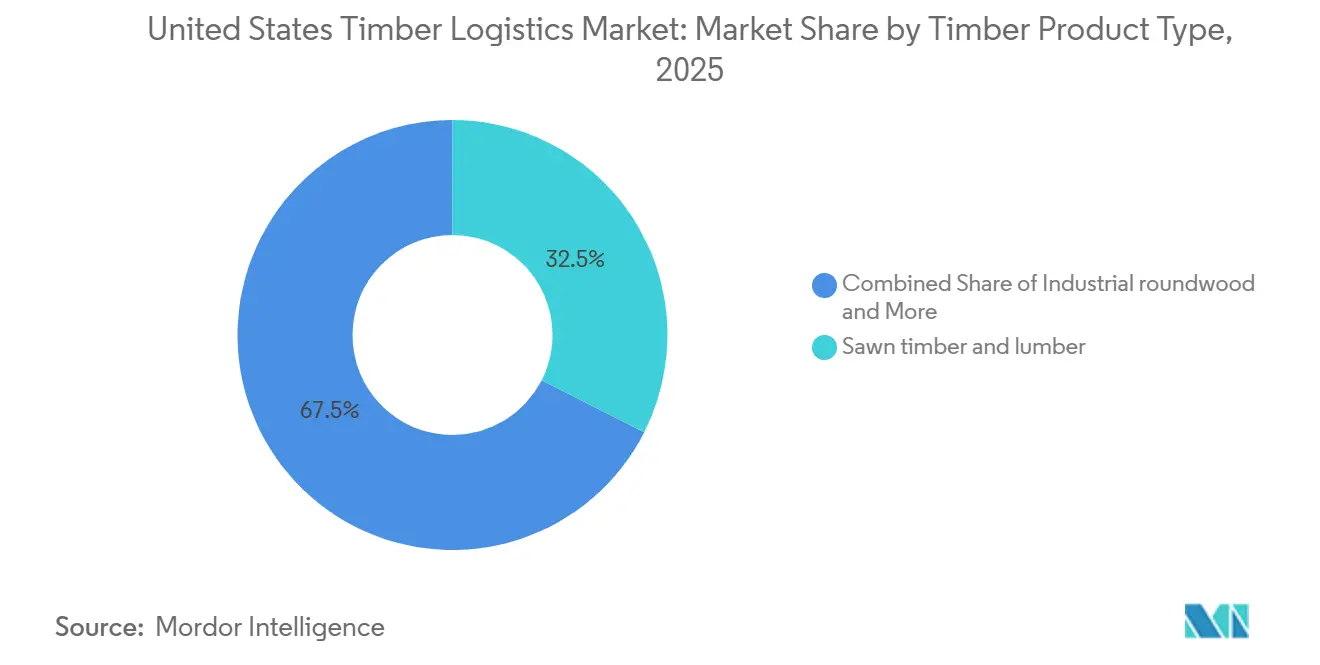

- By timber product type, sawn timber and lumber accounted for 32.48% of the United States timber logistics market size in 2025, while engineered wood products are forecast to grow at a 4.27% CAGR through 2031.

- By end-use industry, construction and infrastructure accounted for 54.20% of the United States timber logistics market size in 2025, while the energy and biomass segment is expected to record the fastest CAGR of 3.98% through 2031.

- By geography, the Southeast captured 37.32% of the United States timber logistics market share in 2025 and is also expected to post the fastest regional CAGR at 3.76% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Timber Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Mass Timber and Engineered Wood in Nonresidential Construction | +0.70% | National, concentrated in Southeast, Pacific Northwest, and urban Northeast | Medium term (2-4 years) |

| Higher Intermodal Reloading to Reduce Empty Miles and Product Damage | +0.50% | Southeast, Midwest intermodal corridors, Gulf Coast port hubs | Medium term (2-4 years) |

| Digital Chain-of-Custody Pressure From ESG-Sensitive Buyers and Public Procurement | +0.40% | National, with early adoption in Northeast and West Coast commercial buyers | Long term (≥ 4 years) |

| Wildfire-Driven Salvage Logging and Distressed Timber Recovery | +0.30% | West, Southeast post-hurricane zones, Mountain West | Short term (≤ 2 years) |

| Rail and Port Slot Optimization for Longer-Distance Inbound and Export Flows | +0.40% | Southeast, Gulf Coast, Pacific Northwest ports | Medium term (2-4 years) |

| Shorter Lead Times From Regionalized Sawmill and Distribution Networks | +0.50% | Southeast, South-Central United States, Appalachian corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Mass Timber and Engineered Wood in Nonresidential Construction

Mass timber is moving from a niche building choice to a more regular structural option in nonresidential construction, and that shift is changing freight planning in the United States timber logistics market. CLT and glulam panels do not travel like standard bundles of sawn lumber, so carriers need different flatbed setups, tighter load sequencing, and more precise unloading windows at jobsites. Construction projects using these products also depend on coordinated deliveries because oversized panels are harder to store on site, and delays can slow installation crews quickly. That makes scheduling discipline, cargo protection, and final-mile execution more important than in conventional timber hauling. As engineered wood volumes rise, carriers with specialized handling capability are gaining access to higher-value freight lanes within the United States timber logistics market.

Higher Intermodal Reloading to Reduce Empty Miles and Product Damage

Intermodal reloading is becoming a structural part of timber supply chains rather than a narrow cost tactic in the United States timber logistics market. C.H. Robinson reported that intermodal contract prices were up 3.5% year over year in its April 2025 freight update, reinforcing the push to redesign lanes to better utilize assets[2]C.H. Robinson, “North America Intermodal and Port Freight Market Update, April 2025,” C.H. Robinson, chrobinson.com. Timber operators are increasingly routing long-haul lumber and pulp traffic through inland port nodes to reduce drayage expense and cut empty miles on truck legs. The model also helps protect payload quality because rail-linked moves can reduce edge damage and moisture exposure over multi-day trips. Carriers that can combine rail and final-mile road movements within a single booking and visibility flow hold a stronger service position than truck-only operators.

Digital Chain-of-Custody Pressure From ESG-Sensitive Buyers and Public Procurement

Chain-of-custody requirements are becoming more demanding for buyers operating under ESG expectations or public procurement rules, turning documentation into a logistics capability issue in the United States timber logistics market. Large public projects already operate in an environment where supply chain transparency and recognized forest stewardship standards carry weight in sourcing decisions. Logistics providers that integrate geolocation data, species information, and custody handoffs into their transport systems are better positioned to support these requirements. The risk of failing those checks is not limited to administrative delay because it can also remove carriers from qualified bid lists for large contracts. That is why digital track-and-trace investment is moving from an optional add-on to a more durable selling point for carriers serving construction and pulp customers.

Wildfire-Driven Salvage Logging and Distressed Timber Recovery

Wildfire and storm salvage work is creating a separate demand stream that does not track normal housing or harvest cycles in the United States timber logistics market. The USDA Forest Service awarded USD 23 million in Hazardous Fuels Transportation Program grants in May 2025 to move dead and downed trees from national forests to processing facilities, which positioned hazardous fuels transport as an operating priority[3]USDA Forest Service, “USDA Acts to Boost Timber Production, Reduce Wildfire Risk,” USDA, usda.gov. Hurricane Helene also downed 800,000 acres of trees, including 187,000 acres in national forests, and the United States Army Corps of Engineers conducted salvage operations at several Southeastern sites during 2025. Salvage freight is harder to plan than routine harvest traffic because roads can be damaged, loads are uneven, and the recovery window is short when fire or decay risks are present. Operators that can deploy off-road support and short-notice flatbed capacity are better placed to win this recurring stream of government-backed work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver Shortages in Specialized Timber Haulage | -0.60% | National, most acute in Southeast and Midwest timber-producing corridors | Short term (≤ 2 years) |

| Seasonal Road Weight Restrictions and Weather Disruptions | -0.40% | Midwest, Northeast, Northern states spring thaw zones, with secondary impact in the Southeast after storms | Short term (≤ 2 years) |

| Tight Chain-of-Custody and Emissions Compliance Costs | -0.30% | National, concentrated in Northeast and West with ESG-mature buyer bases | Long term (≥ 4 years) |

| Fragmented Forest Access Roads and Loading Infrastructure | -0.30% | West, Southeast post-wildfire access corridors, rural Appalachian and Mountain West | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortages in Specialized Timber Haulage

The shortage of log truck drivers is more structural than cyclical, making it harder to fix than a typical freight capacity imbalance in the United States timber logistics market. A 2025 review from the University of Georgia Center for Forest Business and the USDA Forest Service found that most log truck drivers were over 40 and that very few workers under 30 were entering the field[4]University of Georgia Center for Forest Business, “Log Trucking vs. General Freight, What the Forest Industry Needs to Know,” University of Georgia Center for Forest Business, cfb.uga.edu. The same review noted that many operators run smaller, older fleets, which increases insurance and fuel costs and limits their ability to compete with general freight employers on pay. Transportation can account for up to 40% of delivered wood cost in the United States South, so any tightening in driver availability quickly affects mill procurement economics and carrier margins. The Forest Resources Association stated in September 2025 that CDL streamlining under the License Act of 2025 could help the sector, but relief would still take time because training and fleet renewal do not happen quickly. Carriers that can move some higher-volume freight into intermodal patterns are better positioned to reduce the direct driver pressure per load.

Seasonal Road Weight Restrictions and Weather Disruptions

Seasonal road rules continue to reduce truck productivity in the northern and Upper Midwest corridors, which are important to the United States timber logistics market. Michigan kept spring weight restrictions in place through May 9, 2025, with reductions of 25% to 35% below standard limits on state trunklines. Minnesota also adjusted spring load restrictions in 2025 and imposed 84,000-lb limits on 6-axle rigs in relevant zones, reducing effective payloads during thaw periods. South Dakota activated spring restrictions on multiple highway segments in early March 2025, adding another seasonal pinch point for carriers moving forest products across northern lanes. These restrictions often occur when construction demand is picking up, worsening delivery delays and equipment utilization. Weather-driven timber loss can compound the problem because storms can block access roads, flood loading sites, and redirect limited trucks toward cleanup work rather than planned commercial hauls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Redefine Margin Structure

Transportation services accounted for 73.87% of the United States timber logistics market size in 2025, confirming that core line-haul activity remains the largest revenue driver across the service mix. Road freight remains the dominant transport mode because log trucks still handle most harvest-to-mill and mill-to-distribution movements across the country. Rail has a larger role on long-distance lanes, especially on Southeast-to-Northeast lumber routes and Pacific Northwest export corridors. Waterway freight supports bulk biomass, wood chip, and log export activity through Gulf and Atlantic gateways. Multimodal offerings are expanding as inland terminals and port-linked rail nodes become more useful to timber shippers in the United States timber logistics market.

Value-added services are forecast to grow at a 4.52% CAGR from 2026 to 2031, making them the fastest-moving service category in the United States timber logistics industry. Growth reflects rising demand for kiln-drying coordination, remanufacturing sequencing, digital track-and-trace, cross-docking, and other handling steps that more complex timber flows now require. The USDA Forest Service's National Active Forest Management Strategy also supports a steadier pipeline of managed and salvage volumes that need customized handling rather than simple point-to-point hauling. That gives value-added providers a better chance to capture margin than pure-haul carriers that compete mainly on price.

By Timber Product Type: Engineered Wood Reshapes Flow Complexity

Sawn timber and lumber accounted for 32.48% of the United States timber logistics market share in 2025, making it the largest timber product segment by revenue. Its flow pattern is mature and widely distributed, with large volumes moving from Southern sawmills to regional distribution centers and then onward to dealer yards. Fuelwood and biomass shipments feed pellet export and energy channels, especially through Gulf Coast corridors. Pulpwood, chips, and fiber continue to move through dedicated rail and truck contracts tied to paper and packaging processors. Industrial roundwood and logs remain more geographically concentrated, with the Southeast and Pacific Northwest acting as the main harvest basins.

Engineered wood products are forecast to expand at a 4.27% CAGR through 2031, which is the fastest growth rate among product types in the United States timber logistics market. Demand is being supported by the broader use of CLT and glulam in nonresidential buildings, where project requirements favor precise staging and protected transport. These products create more complex freight conditions because oversized panels are sensitive to deflection and need different flatbed configurations than standard lumber loads. Carriers that can handle engineered wood reliably can command a service premium because the freight is harder to move and more sensitive to scheduling errors.

By End-Use Industry: Energy and Biomass Gains Pace Amid Construction's Scale

Construction and infrastructure accounted for 54.20% of the United States timber logistics market in 2025, keeping it well ahead of all other end-use categories. This scale reflects the broad role of timber in residential and nonresidential building activity, as well as sustained freight demand from institutional and infrastructure projects. Broader industrial freight demand stayed below mid-cycle norms, yet nonresidential and infrastructure channels remained more resilient and helped preserve timber logistics volumes. Pulp and paper continues to rely on dedicated contract logistics for the movement of wood chips and fiber from Southern timberlands to integrated mills. Furniture manufacturing and packaging are smaller in revenue terms, but they remain steady users of hardwood, lumber, and engineered panel distribution.

The energy and biomass segment is expected to grow at a 3.98% CAGR through 2031, which makes it the fastest-growing end-use segment in the United States timber logistics industry. Its growth is linked to biomass energy targets, continued pellet demand, and the USDA Forest Service's support for biomass as an outlet for hazardous fuels removed from forests. These flows require different equipment and handling practices, including chip vans, curtainsiders, moisture-sensitive storage, and pellet-ready packaging. That creates a more specialized service tier inside the broader timber freight base and gives the segment a more policy-backed demand profile than construction-led lanes.

Geography Analysis

The Southeast held 37.32% of the United States timber logistics market share in 2025 and is also projected to record the fastest regional CAGR at 3.76% through 2031. Southern softwood lumber mill capacity exceeded 28 billion board feet in 2025, a 35% increase since 2017, reinforcing the region's role as the main fiber and distribution hub. Norfolk Southern stated that the Gainesville Inland Port opened in May 2026 and expanded global market access for Northeast Georgia businesses through a new inland intermodal link. South Carolina Ports completed the Inland Port Greer expansion in March 2025, raising capacity and strengthening rail access for the Carolinas timber corridor. Logistics capital spending across Alabama and Tennessee also points to a denser support network for fleets serving the United States timber logistics market in the broader Southeast.

The West remains the second most significant geography for logs and engineered wood flows, supported by Pacific Northwest production and export-oriented port connections. Wildfires and salvage activity also keep the region important because they generate irregular but recurring movement of distressed timber from affected forest zones. The Northeast is a smaller production base but a major consumption corridor for sawn timber, engineered wood, and paper products from Southeast mills and Atlantic import channels. That concentration of demand in large urban markets supports specialized inbound freight planning, especially for engineered wood shipments moving into dense commercial construction locations.

The Midwest functions as a major intermodal bridge between Southeast timber production and northern consumption markets in the United States timber logistics market. Seasonal restrictions in Michigan, Minnesota, and South Dakota reduce allowable truck weights during thaw periods and create friction at the same time construction demand is improving. These seasonal windows favor carriers that can shift volumes to rail, manage permits carefully, or reposition equipment before restrictions tighten. The Southwest is smaller by timber volume, but it remains an important link between West Coast lumber supply and growing construction demand in Texas, Arizona, and Nevada.

Competitive Landscape

The United States timber logistics market is fragmented, with larger providers competing against a long tail of regional flatbed and specialized forest product operators. National multimodal firms are trying to win share through broader mode coverage, better visibility tools, and stronger dedicated contract networks rather than through simple spot-market pricing. Regional carriers still hold entrenched positions in harvest-to-mill and mill-to-yard corridors where local relationships, loading knowledge, and equipment fit matter more than national scale. As freight conditions tighten, consolidation is becoming a more visible strategy across the United States timber logistics market. Werner closed its USD 282.8 million acquisition of FirstFleet in January 2026, expanding its dedicated fleet by close to 50% and strengthening its position across the eastern United States.

TFI International also expanded its service footprint through TA Dedicated's acquisition of Triangle Warehouse, adding warehousing capacity and power units in the Upper Midwest. These moves show that transportation and storage are being bundled more closely as providers seek to capture a greater share of shipper spending in specialized freight categories. Technology is also becoming a clearer differentiator, with route optimization and cost discipline playing a larger role as capacity becomes less loose. ArcBest reported annualized operational savings of at least USD 15 million from city route optimization efforts already deployed across its network, which shows how digital execution can support margins even when freight markets are shifting.

A major white space remains in digital chain-of-custody integration because no carrier has yet established a widely accepted platform that links certification data, harvest origin, and transport records in one buyer-facing workflow. That gap leaves room for logistics technology firms and regional carriers to build compliance-led offerings around timber freight. Recent network investment by providers such as Ryder also shows that service competition is expanding through maintenance support and fleet access in fast-growing Southern corridors. The result is a market where scale matters in dedicated and multimodal contracts, but specialized regional capability still protects a meaningful share of freight from full national consolidation.

United States Timber Logistics Industry Leaders

J.B. Hunt Transport Services Inc.

Schneider National, Inc.

Knight-Swift Transportation Holdings Inc.

C.H. Robinson Worldwide, Inc.

XPO, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Saia Inc. opened two new LTL terminals in Marysville, Washington, and Edinburgh, Indiana, expanding its national network flexibility and reducing transit variability in key freight corridors that serve Midwest and Pacific Northwest timber distribution markets.

- April 2026: Ryder System opened a new 10,000-square-foot full-service commercial truck rental and maintenance facility in Huntsville, Alabama, to support high-growth manufacturing and logistics markets in one of Alabama's fastest-growing industrial corridors, as part of Ryder's broader Southeast expansion strategy.

- April 2026: TFI International's TA Dedicated acquired Triangle Warehouse, a Minneapolis-based operator, adding 900,000 square feet of warehousing and cold storage, and 150 power units, to expand TA Dedicated's Upper Midwest supply chain offerings.

- January 2026: Werner Enterprises closed its USD 282.8 million acquisition of FirstFleet, expanding its dedicated fleet by approximately 50% to nearly 7,365 dedicated trucks and positioning Werner as the fifth-largest dedicated carrier in the United States by power units, while strengthening its geographic footprint across the eastern United States.

United States Timber Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Waterway | |

| Multimodal | |

| Warehousing and Storage | |

| Value-Added Services |

| Industrial roundwood / logs |

| Fuelwood & biomass |

| Sawn timber & lumber |

| Engineered wood products |

| Pulpwood, chips, and fibre |

| Pellets and briquettes |

| Other Timber Types |

| Construction & Infrastructure |

| Pulp & Paper Industry |

| Furniture Manufacturing |

| Packaging Industry |

| Energy & Biomass Industry |

| Other End-Use Industries |

| Northeast |

| Southwest |

| West |

| Southeast |

| Midwest |

| By Service | Transportation | Road |

| Rail | ||

| Waterway | ||

| Multimodal | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By Timber Product Type | Industrial roundwood / logs | |

| Fuelwood & biomass | ||

| Sawn timber & lumber | ||

| Engineered wood products | ||

| Pulpwood, chips, and fibre | ||

| Pellets and briquettes | ||

| Other Timber Types | ||

| By End-Use Industry | Construction & Infrastructure | |

| Pulp & Paper Industry | ||

| Furniture Manufacturing | ||

| Packaging Industry | ||

| Energy & Biomass Industry | ||

| Other End-Use Industries | ||

| By Geography | Northeast | |

| Southwest | ||

| West | ||

| Southeast | ||

| Midwest |

Key Questions Answered in the Report

How large is the United States timber logistics market in 2026?

The United States timber logistics market stands at USD 18.31 billion in 2026 and is forecast to reach USD 21.56 billion by 2031 at a 3.32% CAGR.

What is driving growth in timber freight across the United States?

Growth is tied to wider use of engineered wood and mass timber, federal forest management support, salvage timber movement, and rising intermodal adoption in Southeast and Midwest corridors.

Which service category leads revenue and which one grows the fastest?

Transportation led with 73.87% of revenue in 2025, while value-added services is projected to grow the fastest at a 4.52% CAGR through 2031.

Which timber product category is expanding the fastest?

Engineered wood products is the fastest-growing product type with a 4.27% CAGR, while sawn timber and lumber remained the largest segment in 2025 with 32.48% revenue share.

Which region is strongest for timber logistics activity?

The Southeast is the leading region, with 37.32% of 2025 revenue and the fastest projected regional growth at 3.76% through 2031.

What are the main operating challenges for carriers in this space?

Driver shortages in specialized log hauling, seasonal road weight restrictions, and rising chain-of-custody compliance costs are the main constraints affecting service reliability and margins.

Page last updated on: