United States Healthcare Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

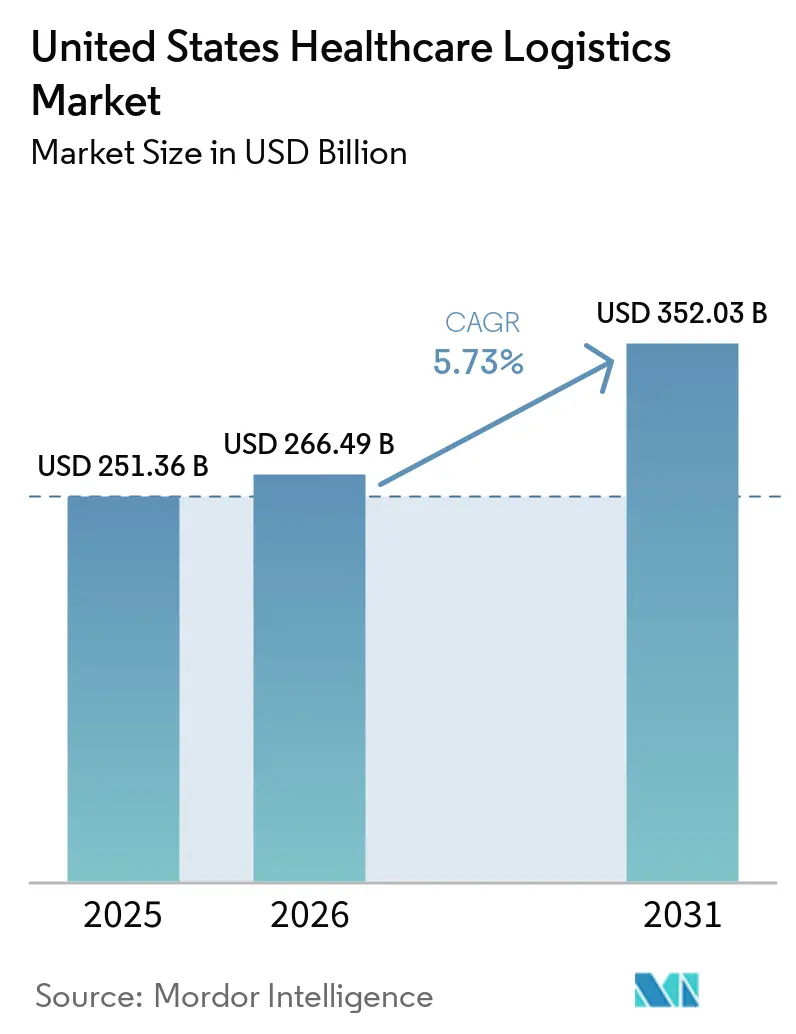

| Base Year Market Size (2025) | USD 251.36 Billion |

| Market Size (2026) | USD 266.49 Billion |

| Market Size (2031) | USD 352.03 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Healthcare Logistics Market Analysis by Mordor Intelligence

The United States healthcare logistics market size was valued at USD 251.36 billion in 2025 and is estimated to grow from USD 266.49 billion in 2026 to reach USD 352.03 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031).

Growth is being shaped by specialty pharmaceuticals, cell and gene therapies, and decentralized care delivery, which are shifting spending toward cold chain capacity, last-mile execution, and stronger chain-of-custody controls across the market. DSCSA requirements are also pushing distributors and logistics providers toward package-level traceability and interoperable electronic processes, which raises the value of compliant transport and warehousing partners. Buyer expectations around visibility and redundancy remain higher than they were before 2020, so contracts now place more weight on service continuity and auditable handling. Large integrators and pharmaceutical distributors are responding with acquisitions, network expansion, and capability-led partnerships, which is narrowing room for mid-tier providers that lack validated cold chain or specialty fulfillment assets. Domestic flows still anchor the market, but new opportunities are opening in cryogenic handling, direct-to-patient distribution, and distributed support for care outside traditional inpatient settings.

Key Report Takeaways

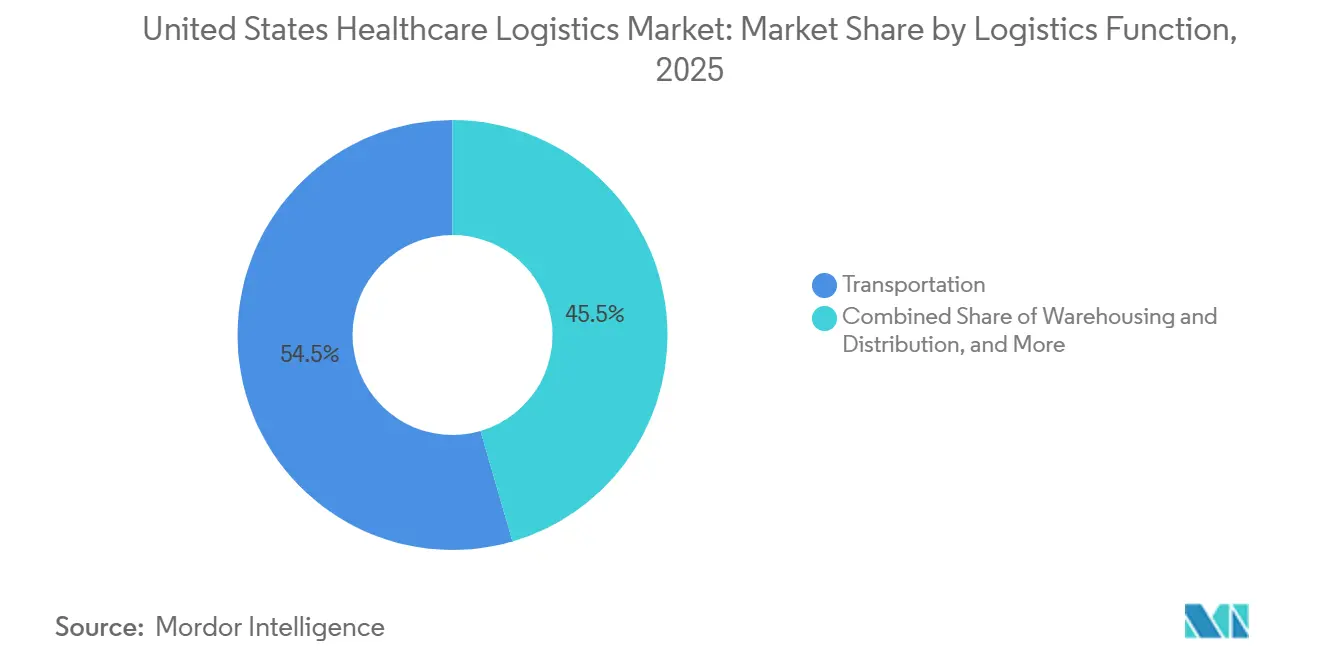

- By logistics function, transportation held 54.50% of the United States healthcare logistics market share in 2025, while warehousing and distribution is projected to grow at 7.49% CAGR through 2031.

- By temperature type, non-temperature controlled logistics accounted for 82.14% of the United States healthcare logistics market size in 2025, while temperature-controlled logistics is projected to expand at 7.63% CAGR through 2031.

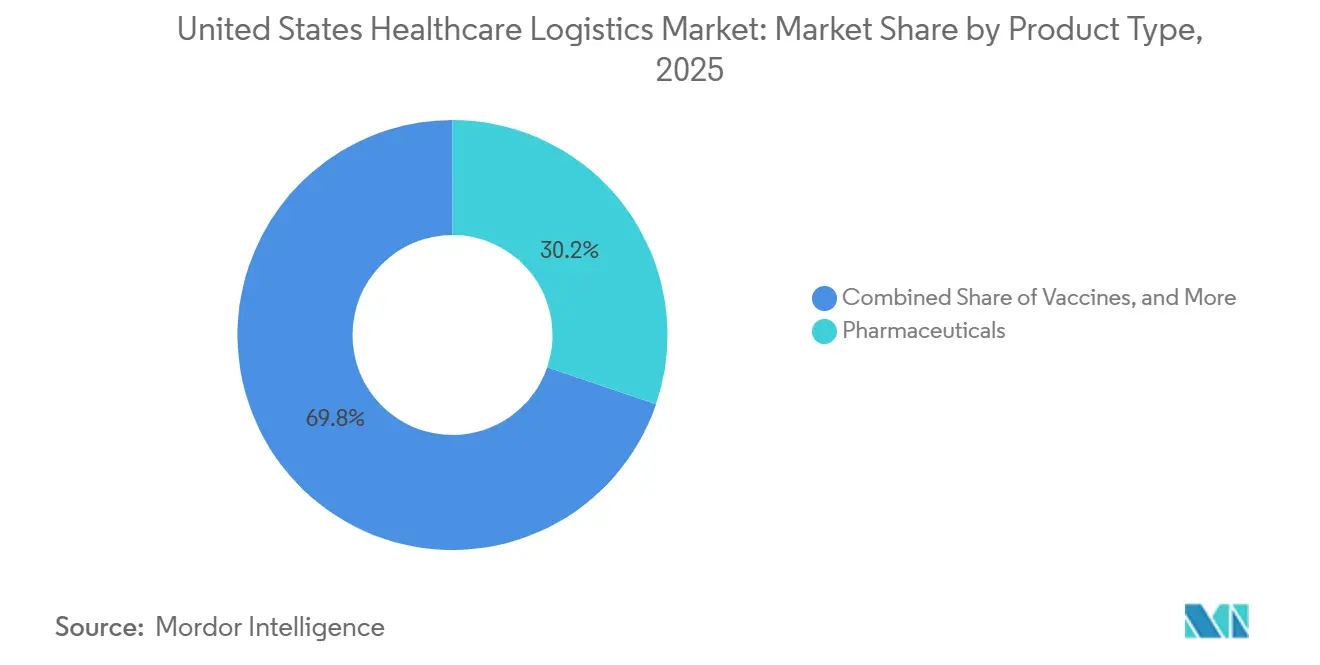

- By product type, pharmaceuticals led with a 30.22% of the United States healthcare logistics market share in 2025, while cell and gene therapies are forecast to grow at 11.79% CAGR through 2031.

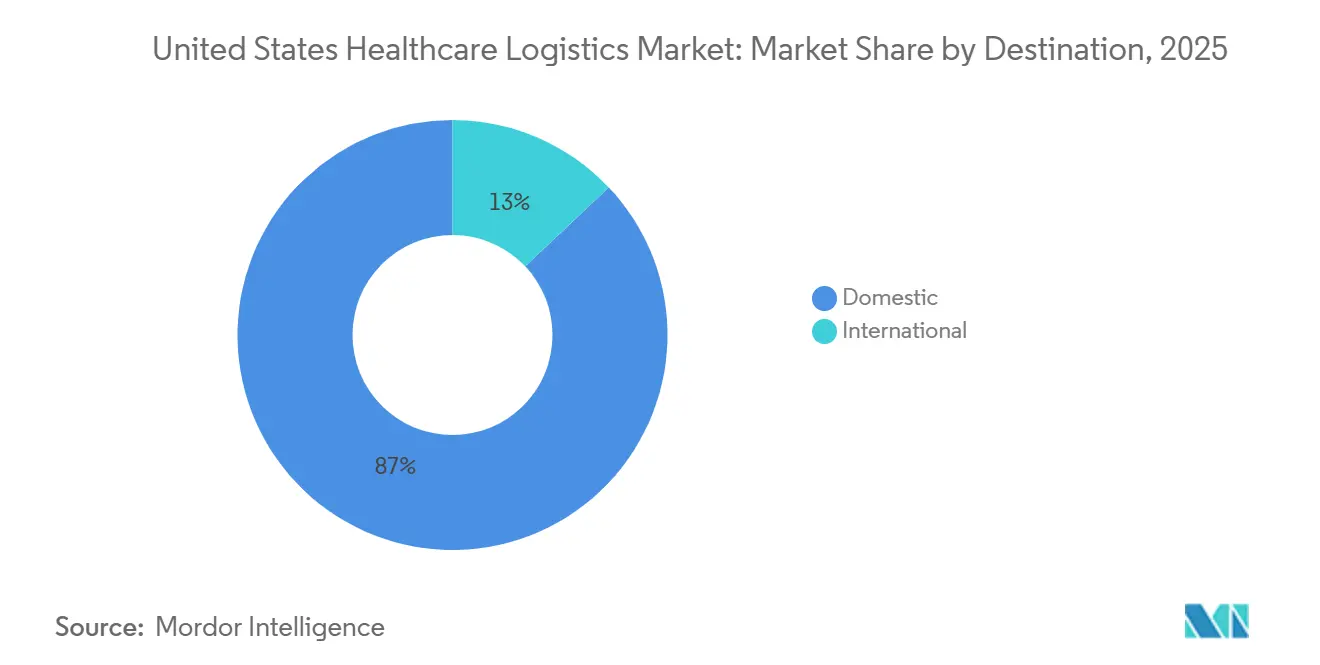

- By destination, domestic shipments held 87.04% of the United States healthcare logistics market share in 2025, while international shipments are projected to advance at 6.79% CAGR through 2031.

- By end user, pharmaceutical manufacturers accounted for 32.77% of the United States healthcare logistics market size in 2025, while hospitals and clinics are projected to grow at 8.37% CAGR through 2031.

- By geography, the Northeast led with a 26.14% of the United States healthcare logistics market share in 2025, while the West is projected to grow at 7.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Healthcare Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Direct-to-Patient Specialty Pharmacy Fulfillment | +1.10% | National, with concentrated demand in Northeast, Southeast, and West | Short term (≤ 2 years) |

| Expansion of Cell and Gene Therapy Cold Chain Lanes | +0.90% | National, with early gains in Northeast, Mid-Atlantic, and California biopharma clusters | Medium term (2-4 years) |

| Rising Serialization, Track-and-Trace, and Chain-of-Custody Demands | +0.50% | National, driven by FDA DSCSA full enforcement effective 2025-2026 | Short term (≤ 2 years) |

| Adoption of Predictive Control Towers and IoT Monitoring | +0.40% | Global networks with United States domestic distribution hubs as primary nodes | Medium term (2-4 years) |

| Growth of Hospital-at-Home and Home Infusion Delivery Models | +0.70% | National, with accelerated adoption in Northeast, Southeast, and West metro areas | Short term (≤ 2 years) |

| Sustainability Pressure on Temperature-Controlled Packaging and Transport | +0.30% | National, with regulatory influence from California, Colorado, Maine, and Oregon EPR frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Direct-to-Patient Specialty Pharmacy Fulfillment

Direct-to-patient fulfillment has moved from an emerging channel to a mainstream operating model for specialty pharmaceuticals. A larger therapy mix now carries handling, reimbursement, and patient support needs that do not fit well with traditional wholesale distribution. Payers and pharmacy benefit managers are redirecting more high-cost biologics, GLP-1 products, and oncology treatments toward mail-order and hub-and-spoke fulfillment. That shift requires logistics providers to manage temperature assurance, delivery scheduling, adherence support, and nurse coordination in one operating flow. Providers that cannot combine delivery with service visibility are losing ground in the United States healthcare logistics market to integrated specialty pharmacy and purpose-built direct-to-patient platforms.

Expansion of Cell and Gene Therapy Cold Chain Lanes

FDA-regulated cellular and gene therapy products are now established commercial products, and that is changing lane design, packaging, and exception management in the United States healthcare logistics market. Each autologous treatment follows a chain-of-identity flow from collection to manufacturing to cryogenic shipment to final infusion, so the logistics process becomes part of the treatment pathway. This structure requires cryogenic handling at or below -150 °C for some therapies, energy-redundant storage, and auditable chain-of-custody records. Manufacturing investment is filling future logistics pipelines, especially near established biopharma clusters in the Northeast and Pennsylvania. The high capital threshold is concentrating this part of the United States healthcare logistics market among operators that already run validated cryogenic networks.

Rising Serialization, Track-and-Trace, and Chain-of-Custody Demands

DSCSA has established package-level traceability and electronic interoperability requirements for certain prescription drugs in the United States, which is raising compliance standards across the United States healthcare logistics market. Wholesale distributors and third-party logistics providers now face tighter expectations around product identification, data exchange, and rapid handling of illegitimate product notifications. The operational effect is that logistics partners must connect physical handling with accurate digital records on both inbound and outbound flows. That change is reshaping commercial relationships because manufacturers increasingly view non-compliant operators as a risk rather than a backup option. The same visibility layer also supports stronger temperature monitoring and exception management when paired with connected tracking tools[1]"Drug Supply Chain Security Act (DSCSA)." FDA, fda.gov.

Growth of Hospital-at-Home and Home Infusion Delivery Models

Care delivery outside traditional inpatient settings is creating a new service layer in the United States healthcare logistics market. Hospital-at-home and home infusion programs depend on predictable delivery windows, secure handling, and rapid replenishment of therapy supplies and consumables. That demand favors distributed warehousing, purpose-built medical courier capability, and tighter coordination between logistics teams and care teams. It also raises the importance of last-mile execution because service failure now affects treatment continuity in the home rather than only shelf availability in a facility. Operators that can combine delivery reliability with route visibility and patient support are better placed to win this part of the market[2]"Hospital-at-Home." American Hospital Association, aha.org/hospitalathome .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver Shortages in Time-Critical Road Freight | -0.50% | National, with acute impacts in Sun Belt corridors, Midwest pharmaceutical hubs, and Northeast distribution-dense markets | Short term (≤ 2 years) |

| High Cost of Ultra-Low Temperature Infrastructure | -0.40% | National, disproportionately affecting markets outside major biopharma clusters | Medium term (2-4 years) |

| Refrigeration Failure and Excursion Liability Risk | -0.30% | National, with concentrated risk at air cargo ground-handling nodes and last-mile touchpoints | Short term (≤ 2 years) |

| Fragmented Compliance Across Multi-State and Cross-Border Flows | -0.30% | National, with heightened complexity for 3PLs operating in 15 or more states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortages in Time-Critical Road Freight

The road freight market entered 2026 with a tighter driver base, which is a meaningful constraint on the United States healthcare logistics market. The shortage states that a rule change affecting non-domiciled commercial driver eligibility removed 50,000 drivers from active service in the near term. It also states that the broader truck driver shortfall stood at around 82,000 drivers, leaving healthcare freight exposed because road transport still handles the bulk of pharmaceutical replenishment and last-mile movement. That pressure is particularly serious for organs, blood products, cell therapies, and urgent pharmaceutical deliveries, as those shipments offer little or no transit flexibility. Carriers that can still provide healthcare-grade service are gaining pricing power as reefer and time-critical capacity tighten.

High Cost of Ultra-Low Temperature Infrastructure

Ultra-low-temperature infrastructure remains one of the most expensive parts of the United States healthcare logistics market to build and operate. The higher cost states that purpose-built pharmaceutical facilities can exceed USD 4,305.56 per square meter in construction cost, before adding validated refrigeration, monitoring, HVAC redundancy, and compliance layers. In addition, a standard -80 °C laboratory freezer consumes 10.00 to 12.00 kWh per day, which pushes operating costs well above those of standard cold chain sites. The result is a split market, with a small number of specialists serving cryogenic and deep-frozen therapies, while the broader field remains focused on chilled and frozen ranges. That concentration reduces redundancy and raises single-point-of-failure risk during periods of capacity stress[3]"ENERGY STAR Certified Lab Grade Refrigerators & Freezers." ENERGY STAR, energystar.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Warehousing Infrastructure Reshapes Competitive Positioning

Transportation held 54.50% of the United States healthcare logistics market share in 2025, while warehousing and distribution is forecast to advance at 7.49% CAGR through 2031. That leading share reflects the central role of road, air, and intermodal movement in pharmaceutical distribution, where timing and compliant handling remain critical service requirements. Air freight serves the premium end of the network because cryogenic therapies and urgent biologics depend on validated lanes and tightly managed handoffs. Road networks still carry the volume base of the United States healthcare logistics industry because they connect manufacturers, distributors, hospitals, pharmacies, and regional distribution points at national scale. This keeps transportation at the center of contract value even as the service mix becomes more specialized[4]"Economic Impact of Healthcare Distributors in the United States." Healthcare Distributors Association, getmga.com.

Warehousing and distribution is growing faster because manufacturers are moving toward outsourced models that combine storage, fulfillment, and temperature management under one provider. That change is tied to the rise of distributed care because home-based therapy and acute-care-at-home programs need inventory positioned closer to patients and care teams. The value-added layer is also expanding as providers take on kitting, labeling, cold packing, and reverse logistics alongside core storage. Providers with GDP and cGMP compliant sites are holding a structural advantage because regulated pharmaceutical products cannot easily be moved through non-certified environments. Over time, this is shifting competitive positioning within the United States healthcare logistics market from basic transport reach toward integrated warehousing capability and validated operating discipline.

By Temperature Type: Cold Chain Investment Outpaces The Broader Market

Non-temperature-controlled logistics accounted for 82.14% of the United States healthcare logistics market size in 2025, while temperature-controlled logistics are projected to grow at 7.63% CAGR through 2031. Ambient flows remain dominant because a large volume of pharmaceuticals, devices, and healthcare supplies can move without active temperature control. This wide ambient base supports national scale and cost efficiency, making it essential for routine replenishment and broad healthcare distribution. Even so, the mix is slowly shifting because new therapies are placing greater weight on refrigerated, frozen, and deep-frozen handling. That is moving investment toward monitoring, qualified packaging, and tighter exception management in the United States healthcare logistics market.

The chilled 2 °C to 8 °C range serves much of the refrigerated pharmaceutical base, while frozen ranges support mRNA vaccines and selected biologics, and deeper frozen ranges support advanced therapy flows. Also, refrigerant regulations are affecting construction economics for new cold storage facilities in 2026, adding another planning variable to network expansion. At the same time, validated cold-chain capacity continues to command a premium because the service is harder to replicate, more capital-intensive, and more compliance-sensitive. This also states that cold-chain rates can run 150% to 200% above ambient alternatives, which shows how sharply pricing separates the two service tiers. That widening gap suggests that temperature-controlled capacity will remain one of the strongest value pools in the United States healthcare logistics industry.

By Product Type: Specialty Complexity Redefines The Pharmaceutical Logistics Baseline

Pharmaceuticals held the leading product share at 30.22% of the United States healthcare logistics market size in 2025, while cell and gene therapies are set to expand at 11.79% CAGR through 2031. The pharmaceutical base remains large because prescription drug distribution continues to run through high-volume wholesale networks and established pharmacy relationships. At the same time, the advanced therapy segment is changing operating standards, as each commercial cell or gene therapy shipment requires tight chain-of-identity controls and specialized thermal protection. FDA oversight of cellular and gene therapy products supports the commercial reality that these therapies now require regulated handling across collection, manufacturing, transport, and infusion. This makes advanced therapies a strategic growth area within the United States healthcare logistics market, even when their starting volume is lower than that of conventional pharmaceuticals.

Biopharmaceuticals, vaccines, and clinical trial materials each add their own storage, handling, and regulatory demands, so the product mix is becoming more tiered and specialized. This highlights Cencora's 2026 work with Gilead on CAR-T therapies, which shows how distributors are building operational depth around commercially approved advanced therapies. Medical devices, veterinary products, blood and plasma components, and diagnostic products continue to fill the remaining product basket and support broader network utilization. Diagnostic and laboratory products are also benefiting from more distributed testing and point-of-care activity outside traditional centralized settings. As a result, product complexity in the United States healthcare logistics market is rising faster than overall volume growth.

By Destination: Domestic Concentration Masks International Complexity

Domestic shipments held 87.04% of the United States healthcare logistics market share in 2025, while international flows are projected to grow at 6.79% CAGR through 2031. The domestic lead reflects the largely self-contained structure of the United States pharmaceutical supply chain, where most products move within national lanes between manufacturers, distributors, and care sites. That broad internal network helps support resilience because most finished product flows do not depend on cross-border movement. It also gives large domestic operators an advantage because they can scale route density, service consistency, and compliance oversight more efficiently. This domestic concentration remains one of the defining features of the United States healthcare logistics market.

The international segment is smaller but growing faster because pharmaceutical imports, clinical trial movements, and specialized sourcing still require more cross-border handling. This highlights growing import exposure to manufacturing hubs such as India and Ireland, which add documentation, temperature verification, and chain-of-custody demands that are less intense in domestic flows. Border scrutiny and product safety programs also make international execution more sensitive to the quality of paperwork and shipment visibility. That means international healthcare logistics can deliver attractive growth, but it also brings a higher compliance burden and less room for operating error. Over time, the gap between domestic scale and international complexity will remain a key organizing pattern in the United States healthcare logistics market.

By End User: Pharmaceutical Manufacturers Drive Volume, Hospitals Drive Service Complexity

Pharmaceutical manufacturers accounted for 32.77% of the United States healthcare logistics market share in 2025, while hospitals and clinics are projected to grow at 8.37% CAGR through 2031. Manufacturers remain the largest customer group because they originate distribution demand and set many of the network standards for handling, compliance, and delivery performance. Their needs range from ambient distribution to cryogenic movement, and from domestic lanes to international flows, making them the most operationally complex accounts to serve. This position gives them strong leverage in carrier selection, outsourcing models, and preferred-partner structures across the United States healthcare logistics market. It also helps explain why large logistics providers are investing in capabilities rather than only in network scale.

Hospitals and clinics are growing faster because care is moving outside traditional inpatient settings, and service models now require more direct and time-sensitive replenishment. This links the shift to hospital-at-home expansion, which is raising demand for coordinated last-mile delivery and distributed inventory support. Cardinal Health's Velocare model illustrates how providers are responding with dedicated platforms for medical supply movement tied to home-based care pathways. Distributors, wholesalers, retail pharmacies, and other users still make up a large share of the end-user base, but consolidation is compressing the middle tier of that group. This leaves the United States healthcare logistics market increasingly shaped by a large-volume manufacturer base and a faster-growing care-delivery segment that demands greater service precision.

Geography Analysis

The Northeast held 26.14% of the United States healthcare logistics market share in 2025, while the West is projected to expand at 7.03% CAGR through 2031. The Northeast leads because the Boston-to-Washington corridor combines academic medical centers, specialty hospital systems, pharmaceutical headquarters, and dense distribution activity in one connected region. New York remains a major pharmaceutical import gateway, and the surrounding concentration of biopharmaceutical operations in New Jersey and Connecticut supports a high level of origination and destination activity. DSCSA execution is especially important in this region because multi-site hospital systems and large pharmacy networks operate in complex, high-volume settings. The West is growing faster because California is expanding its biopharmaceutical manufacturing base and because Pacific states are seeing wider adoption of hospital-at-home service models.

The Cencora's planned 39,948.31-square-meter distribution center in Fontana, California, shows how the West is adding automated capacity to support future growth. The Southeast and Midwest also account for a major share of volume because manufacturing and wholesale activity remain strong in North Carolina, Indiana, Ohio, and nearby states. Cardinal Health's 32,516.06 square meter logistics center in Groveport, Ohio, and Cencora's planned 49,238.61 square meter national distribution center in Harrison, Ohio, reinforce the Midwest's role as a core wholesale distribution base. GEODIS also opened a 7,246.44 square meter cold chain cross-dock facility near Chicago with a 483.10 square meter temperature-controlled addition, which strengthens the region's role in pharmaceutical air and ocean handling. In the Southeast, Cencora's planned Dothan expansion points to stronger refrigerated and frozen storage capacity, which supports more specialized healthcare flows.

The Southwest is growing with its population centers, especially in Texas, where it was planned a 46,451.52 square meter 3PL facility for future operation. That region's large geography and dispersed demand base make last-mile execution harder, which increases the value of strategically placed pharmaceutical nodes. Taken together, regional patterns show that the United States healthcare logistics market combines a dense, compliance-heavy Northeast base with faster western growth and broad central distribution strength. Geography in the United States healthcare logistics market therefore remains less about simple volume concentration and more about how network density, therapy mix, and care delivery models vary from one region to another.

Competitive Landscape

The United States healthcare logistics market is moderately consolidated at the top tier, with UPS Healthcare, DHL Supply Chain, FedEx Healthcare Solutions, McKesson, Cencora, and Cardinal Health controlling a large share of high-value pharmaceutical logistics activity. These companies are competing on validated cold chain capability, distribution scale, compliance execution, and direct-to-patient reach rather than on freight movement alone. The strongest players are also extending deeper into specialty logistics, clinical trial handling, and advanced therapy support, which raises the capability threshold for new entrants. That is making the United States healthcare logistics market more selective because customers increasingly want a smaller number of partners that can support transport, warehousing, visibility, and regulated handling in one network. Mid-tier providers still have room in niche services, but the gap is widening between specialist leaders and general logistics operators.

UPS has used acquisitions to expand cold chain reach, including Andlauer Healthcare Group and the earlier Frigo-Trans and BPL transactions, which add specialized distribution and temperature-controlled capability. DHL has moved on a similar track through CRYOPDP and SDS Rx, pairing clinical trial and cell and gene therapy strength with final-mile pharmaceutical delivery. FedEx has leaned more toward organic investment, using quality programs and visibility tools such as SenseAware and Surround to strengthen service governance and shipment monitoring. This difference in strategy shows that the United States healthcare logistics market still offers more than one path to scale, but every viable path now depends on regulated service depth. C.H. Robinson's report of more than USD 1.00 billion in healthcare revenue over the prior 12 months also shows that large orchestration players can compete when they combine control towers, carrier reach, and healthcare-grade quality systems.

Specialists such as Marken, AIT Worldwide Logistics, and World Courier continue to hold defensible positions in clinical trial and specialty therapy movement because deep regulatory knowledge still matters. Compliance has become a sharper dividing line as DSCSA traceability requirements and advanced therapy handling expectations push customers toward proven operators. The main whitespace remains in fully integrated cryogenic logistics, direct-to-patient rare disease fulfillment, and predictive control tower execution at national scale. Even with strong top-tier players, the United States healthcare logistics market still has no single operator that fully dominates every high-complexity lane and service layer.

United States Healthcare Logistics Industry Leaders

-

United Parcel Service of America, Inc. (UPS)

-

FedEx

-

DHL Group

-

Cencora

-

McKesson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Cencora and Gilead Sciences bolstered their distribution partnership, enhancing access to Gilead's CAR-T cell therapies, Yescarta and Tecartus. These therapies are now available at an expanding number of authorized treatment centers across the United States, including both health systems and community oncology practices. By leveraging Cencora's distribution infrastructure and order management capabilities, the agreement aims to alleviate the administrative burdens faced by these authorized treatment sites. This move underscores the increasing significance of major pharmaceutical distributors in navigating the operational complexities associated with commercially approved cell therapies.

- June 2026: McKesson finalized Apollo Funds' minority investment in its Medical-Surgical Solutions (MMS) business on June 1, 2026. Apollo Funds injected USD 1.25 billion in convertible preferred equity, securing an approximate 13% stake and valuing MMS at a total enterprise valuation of around USD 13 billion. This deal serves as a precursor to a prospective MMS IPO, with McKesson poised to maintain both operational control and majority ownership.

- May 2026: Americold Realty Trust and EQT unveiled a USD 1.3 billion joint venture in North America's cold storage sector. The venture encompasses 12 United States cold storage warehouses, boasting a combined temperature-controlled capacity of roughly 124 million cubic feet. EQT took a commanding 70% stake, while Americold retained the remaining 30% and oversight of daily operations. With net cash proceeds of USD 1.1 billion allocated for debt repayment, the venture anticipated to finalize in Q3 2026 stands as one of North America's largest cold storage transactions. It also highlights the surging interest from institutional investors in the healthcare and food cold chain infrastructure.

- April 2026: GEODIS inaugurated its inaugural dedicated healthcare cold chain cross-dock facility in the Americas, situated in Chicago, Illinois. Spanning 78,000 sq ft, the facility is strategically located near O'Hare International Airport. It boasts a 5,200 sq ft temperature-controlled segment, featuring deep cold (15–25 °C) and refrigerated (2–8 °C) storage zones. These zones cater exclusively to pharmaceutical air and ocean exports and imports. Holding both CEIV Pharma and Certified Cargo Screening Facility (CCSF) certifications, this facility marks GEODIS's debut in the United States cold chain storage arena. It further extends GEODIS's global network, which already encompasses pharmaceutical cold chain nodes in France, the United Kingdom, the Netherlands, and Germany.

United States Healthcare Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Temperature Controlled | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (less than -20 °C) | |

| Non-Temperature Controlled |

| Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | |

| Biopharmaceuticals (Biologics and Biosimilars) | |

| Vaccines | |

| Clinical Trial Materials | |

| Cell and Gene Therapies | |

| Medical Devices | |

| Veterinary Medicine | |

| Blood, Plasma and Blood Components | |

| Diagnostic and Laboratory Products | |

| Organs and Human Tissues | |

| Others |

| Domestics |

| International |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Hospitals and Clinics |

| Hospitals and Retail Pharmacies |

| Healthcare Distributors and Wholesalers |

| Others |

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Temperature Type | Temperature Controlled | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than -20 °C) | ||

| Non-Temperature Controlled | ||

| By Product Type | Pharmaceuticals | Prescription and Specialty Drugs |

| OTC Drugs | ||

| Biopharmaceuticals (Biologics and Biosimilars) | ||

| Vaccines | ||

| Clinical Trial Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices | ||

| Veterinary Medicine | ||

| Blood, Plasma and Blood Components | ||

| Diagnostic and Laboratory Products | ||

| Organs and Human Tissues | ||

| Others | ||

| By Destination | Domestics | |

| International | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Hospitals and Clinics | ||

| Hospitals and Retail Pharmacies | ||

| Healthcare Distributors and Wholesalers | ||

| Others | ||

| By Region | Northeast | |

| Southeast | ||

| Midwest | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is the 2026 value of the United States healthcare logistics sector?

The United States healthcare logistics market reached USD 266.49 billion in 2026 and is projected to reach USD 352.03 billion by 2031, growing at a 5.73% CAGR over 2026-2031.

Which logistics function is the largest in 2025?

Transportation led with 54.50% of revenue in 2025, reflecting the central role of road, air, and intermodal movement in pharmaceutical distribution.

Which part of the service mix is growing fastest?

Warehousing and distribution is projected to grow at 7.49% CAGR through 2031, supported by outsourced storage, fulfillment, and distributed care delivery needs.

Why is cold chain becoming more important in healthcare distribution?

Temperature-controlled logistics is projected to grow at 7.63% CAGR through 2031 because biologics, vaccines, and advanced therapies require tighter thermal protection and stronger chain-of-custody controls.

Which product category is expanding the fastest?

Cell and gene therapies are forecast to grow at 11.79% CAGR through 2031, even though pharmaceuticals remained the largest product category with a 30.22% share in 2025.

Which end-user group is changing service requirements the most?

Hospitals and clinics are projected to grow at 8.37% CAGR through 2031, driven by hospital-at-home and more time-sensitive replenishment needs outside traditional inpatient settings.

Page last updated on: