United States Maple Syrup Urine Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

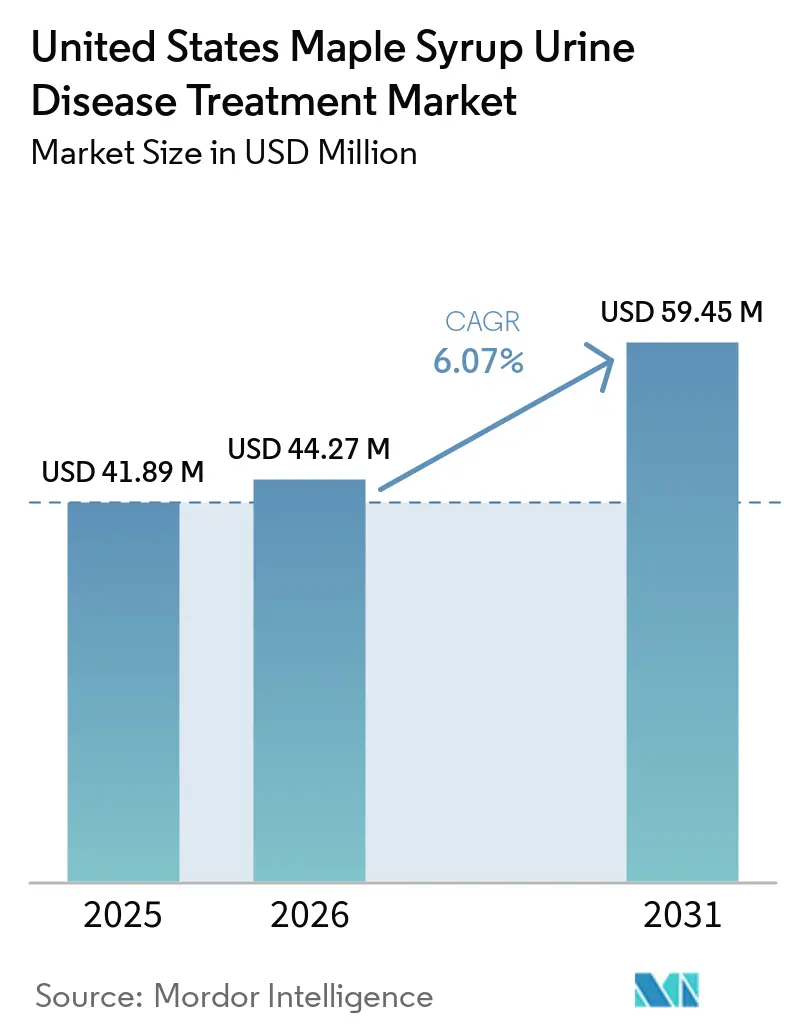

| Market Size (2026) | USD 44.27 Million |

| Market Size (2031) | USD 59.45 Million |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

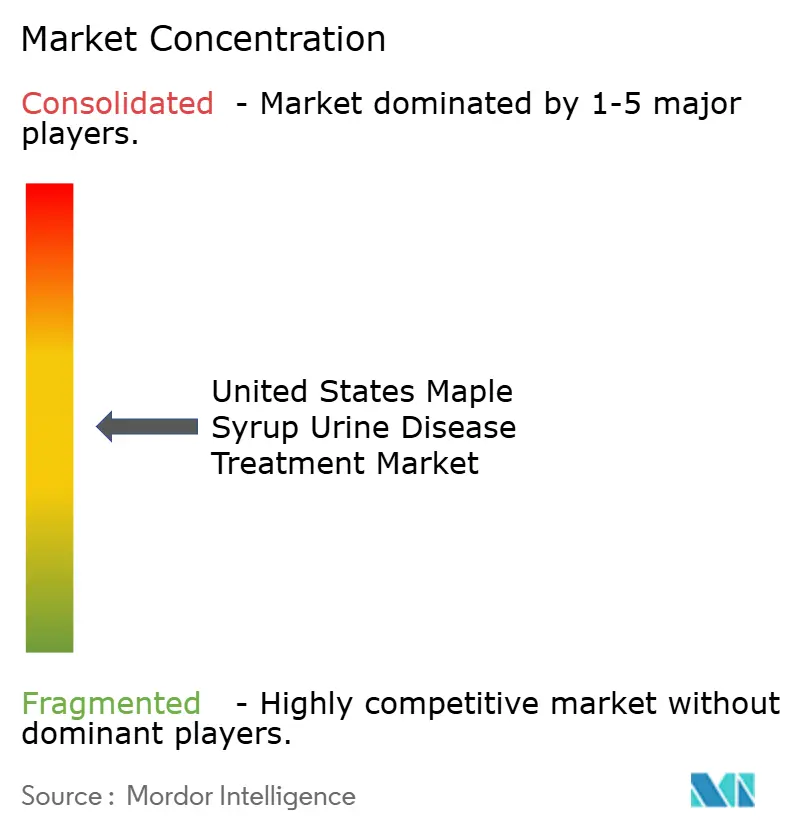

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Maple Syrup Urine Disease Treatment Market Analysis by Mordor Intelligence

The United States Maple Syrup Urine Disease Treatment Market size was valued at USD 41.89 million in 2025 and is estimated to grow from USD 44.27 million in 2026 to reach USD 59.45 million by 2031, at a CAGR of 6.07% during the forecast period (2026-2031).

Universal newborn screening mandates, ongoing orphan-drug incentives, and a first wave of curative gene-therapy assets are reshaping care pathways, underwriting a steady expansion of the United States Maple Syrup Urine Disease treatment market. Pipeline visibility around dual-vector AAV9 and lipid-nanoparticle mRNA platforms is widening investor appetite even as formula vendors defend share through ready-to-drink blends and bone-health fortification. Specialty pharmacies continue to dominate distribution, but telemedicine-enabled e-commerce is pulling new households online, lifting adherence while lowering travel burdens. Rising survival after living-donor liver transplantation is swelling the adult patient pool and stimulating demand for long-term neurological follow-up services.

Key Report Takeaways

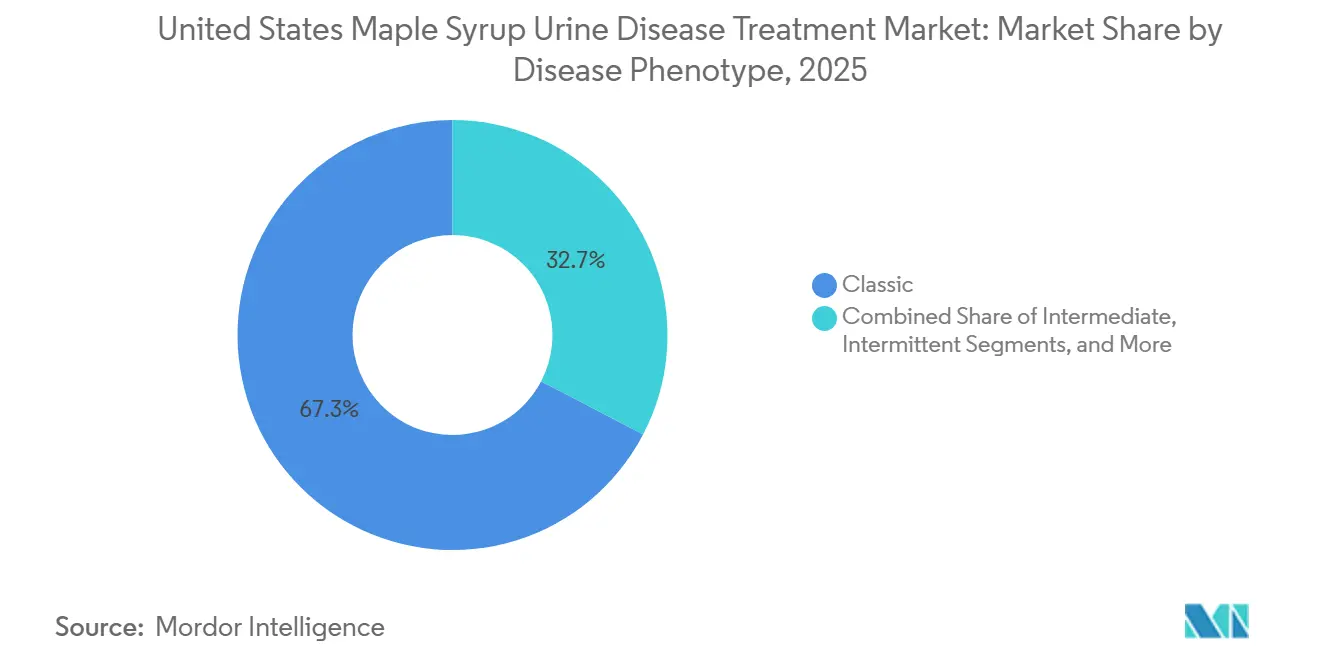

- By disease phenotype, classic cases led with 67.34% revenue share in 2025, while thiamine-responsive cases are forecast to expand at a 7.77% CAGR through 2031.

- By age group, pediatric patients accounted for 41.36% of the United States Maple Syrup Urine Disease treatment market size in 2025, but neonatal and infant cases are advancing at a 6.59% CAGR to 2031.

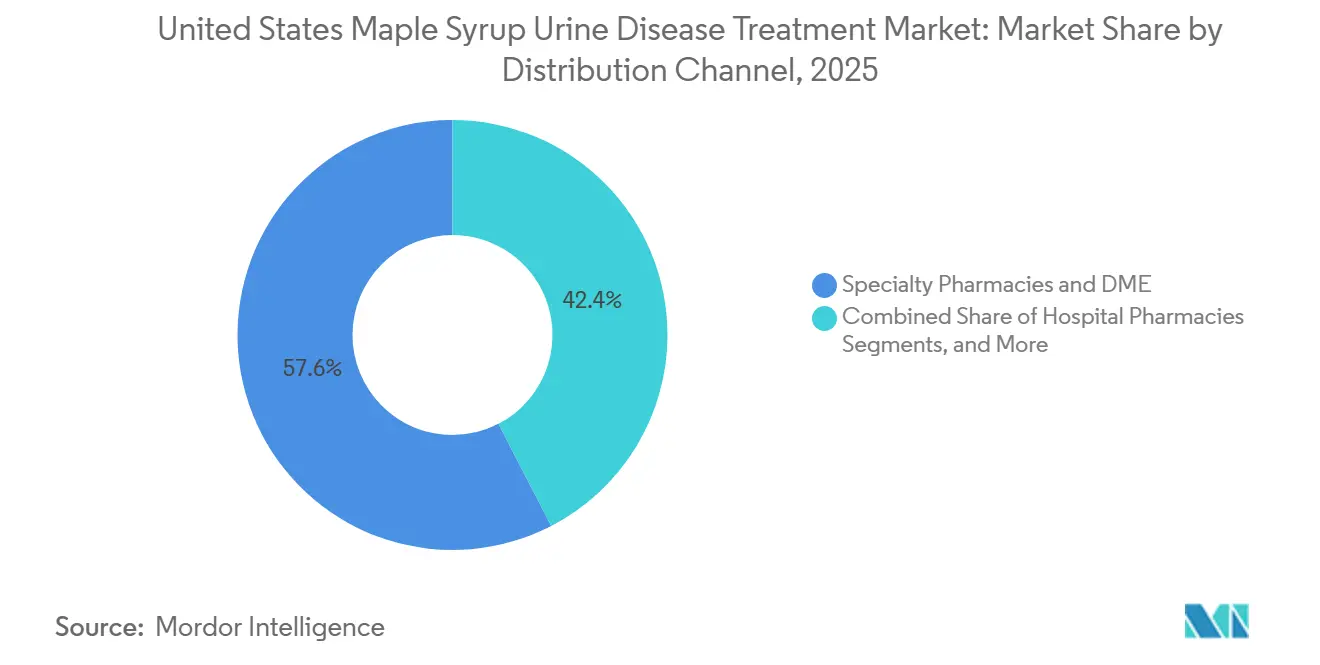

- By distribution channel, specialty pharmacies held 57.59% share of the United States Maple Syrup Urine Disease treatment market size in 2025, whereas direct-to-consumer e-commerce is rising at a 7.41% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global United States Maple Syrup Urine Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Newborn-screening-led rise in diagnosed MSUD cases | +1.2% | Nationwide (54 of 56 state programs) | Short term (≤ 2 years) |

| Improved survival rates post living-donor liver transplantation | +0.9% | Academic transplant centers | Medium term (2-4 years) |

| Orphan-drug incentives and payer coverage expansions | +1.4% | State-level Medicaid variability | Medium term (2-4 years) |

| Clinical pipeline of BCKDH mRNA and enzyme-replacement therapies | +1.8% | Contingent on FDA pathway | Long term (≥ 4 years) |

| Next-generation BCAA-free medical-food technologies | +0.6% | Driven by palatability gains | Short term (≤ 2 years) |

| Growing awareness on rare metabolic diseases | +1.4% | State-level Medicaid variability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Newborn Screening Boosts MSUD Diagnoses

Mandatory tandem mass spectrometry panels now identify elevated leucine levels within 24 to 48 hours of birth across 54 U.S. jurisdictions, transforming MSUD from a late-crisis diagnosis to a routinely detected condition.[1]Science Translational Medicine Editors, “Dual AAV9 Gene Therapy Corrects MSUD in Large Animals,” scitranslmed.org Early detection enables the prompt initiation of intravenous dextrose and BCAA-free formulas, preventing irreversible neurological damage, reducing historical mortality rates, and increasing the number of patients requiring lifelong management. Louisiana's registry from 2005 to 2024 reported four cases among 1.2 million births, consistent with the national incidence rate of 1 in 185,000, demonstrating the program's effectiveness.[2]Louisiana Department of Health, “Newborn Screening Annual Report 2024,” ldh.la.gov While longer survival rates are filling adolescent and adult clinics, 80% of adult patients still receive care in pediatric centers, creating additional pressure on metabolic teams. Although telemedicine, at-home leucine meters, and cross-state licensure waivers are improving access, workforce shortages remain a significant challenge.

Living-Donor Liver Transplantation Sees Surge in Survival Rates

Recent data from U.S. single-center cohorts indicate a 100% survival rate following living-donor liver transplantation, enabling classic-phenotype patients to discontinue lifelong emergency dietary restrictions. The use of heterozygous parental donors has expanded the donor pool without introducing metabolic risks, effectively reducing wait-list times. While leucine levels stabilize post-transplant, occasional crises triggered by sepsis suggest potential limitations in muscle and kidney BCKDH activity during stress. An increasing number of transplant-eligible families are temporarily relocating to academic centers, driving demand for housing assistance and long-term follow-up coordination.

Orphan Drug Incentives and Expanded Payer Coverage

Incentives such as seven-year market exclusivity, trial-cost tax credits, and waived FDA user fees are attracting biotech companies to address the limited U.S. patient pool for Maple Syrup Urine Disease. ACER-001, a sodium phenylbutyrate formulation, received U.S. orphan status in 2014 and European designation in 2022, with Phase 2a enrollment expected in late 2026.[3] Health Resources & Services Administration, “Newborn Screening Data and Quality Measures,” hrsa.gov Advocacy groups are successfully pushing Medicaid agencies to include BCAA-free formulas under pharmacy benefits, removing prior authorization barriers. However, clinics continue to face coverage denials for valine and isoleucine capsules, exacerbating geographic disparities and complicating manufacturer forecasts.

BCKDH mRNA and Enzyme-Replacement Therapies in the Clinical Pipeline

Preclinical data from February 2025 revealed that Dual Adeno-Associated Virus 9 vectors encoding BCKDHA and BCKDHB achieved 100% survival and unrestricted diets in murine and calf models, prompting ASC Therapeutics to finalize Phase I/II trial designs with regulatory authorities. Researchers at the University of Pennsylvania and Moderna Therapeutics demonstrated that lipid-nanoparticle mRNA administration reduced plasma leucine levels and extended lifespans in mice, enabling repeat dosing without triggering AAV immunogenicity. Academic institutions in Paris, London, and Philadelphia are simultaneously advancing AAV strategies targeting liver, muscle, and brain, intensifying the competition to achieve first-in-human proof.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High lifetime cost and adherence burden of dietary therapy | -1.1% | States lacking full Medicaid coverage | Medium term (2-4 years) |

| Small patient pool limiting commercial ROI | -0.8% | Nationwide, impacts pharma investment | Long term (≥ 4 years) |

| Volatile supply of pharma-grade BCAA-free amino-acid inputs | -0.5% | Global supply-chain dependencies | Short term (≤ 2 years) |

| Ultra rare nature of the disease | -0.8% | Nationwide, impacts pharma investment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs and Adherence Challenges of Dietary Therapy

Annual formula expenses often exceed USD 13,320, excluding supplements and emergency admissions. A single shipment lasting 2.5 months is priced at nearly USD 2,775. While insurers occasionally cover leucine-free blends, they frequently deny coverage for valine and isoleucine capsules, leading families to incur out-of-pocket expenses exceeding USD 100 monthly. The prior-authorization process delays deliveries and increases the risk of lapses. Hospitalizations during metabolic crises can cost over USD 50,000, particularly when dialysis is required to reduce plasma leucine levels below 1,100 µmol/L. Cognitive challenges, including attention-deficit disorder and executive-function delays, affect 45.7% of pediatric patients, further complicating dietary adherence.

Limited Patient Pool Restricts Commercial Returns

With an incidence rate of 1 in 185,000 births, MSUD results in approximately 30 new cases annually in the U.S., with a total patient population of fewer than 5,000. In Louisiana, only four cases were recorded over two decades from 1.2 million births, highlighting the rarity of the condition even in comprehensive registries. A gene therapy priced between USD 2–3 million requires durable outcomes and payer acceptance to justify its cost. Formula manufacturers catering to this ultra-orphan group often cross-subsidize MSUD-specific products with phenylketonuria volumes to maintain their specialized amino-acid product lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Phenotype: Classic Dominance Masks Thiamine-Responsive Opportunity

Classic phenotype, driven by near-zero residual BCKD activity and a mandatory life-long formula reliance, accounted for 67.34% of 2025 revenue. In the U.S., the treatment market for classic patients with Maple Syrup Urine Disease (MSUD) remains a cornerstone for manufacturers. These patients consume nearly 90% of their protein as BCAA-free mixtures and require monthly plasma monitoring. On the other hand, intermediate and intermittent phenotypes, with milder enzymatic deficits, can either take limited intact-protein or use episodic formulas during illness. This not only reduces their annual product demand but also leads to heightened emergency-room billings during times of catabolic stress.

Thiamine-responsive MSUD, though currently a minor segment, is witnessing a growth spurt at a 7.77% CAGR. This surge is attributed to enhanced genotype-phenotype mapping, which identifies DBT variants responsive to daily thiamine doses ranging from 10 to 1,000 mg. Looking ahead, the market share for thiamine-responsive MSUD in the U.S. is poised to expand, especially as precision-dosing protocols and whole-exome sequencing gain traction in regional clinics. Companies are also developing low-valine modular powders tailored for partial protein liberalization, hinting at potential growth, even if it might cannibalize some high-volume classic formulations.

By Age Group: Neonatal Surge Reflects Screening Success

Neonatal and infant segments are on a growth trajectory, expanding at a 6.59% CAGR through 2031. This growth mirrors the success of universal newborn screenings, which can detect elevated leucine levels within 48 hours. With feeding volumes of 120–150 mL/kg/day, there's a notable uptick in per-capita formula consumption. Additionally, weekly plasma assays during the first year bolster laboratory revenues. Currently, pediatric patients account for 41.36% of the U.S. treatment market for MSUD. However, as these patients transition into adolescence, there's a concerning rise in non-adherence, heightening the risk of crisis hospitalizations.

While adult patients constitute the smallest segment of the market, they represent a rapidly growing demographic, thanks in part to improved post-transplant survival rates. Due to workforce shortages, a significant 80% of these adults still find themselves in pediatric units. This has spurred telehealth initiatives aimed at addressing metabolic oversight gaps. In response, the industry is rolling out adult-friendly ready-to-drink shakes and apps focused on executive-function coaching, aiding in independent diet management.

By Distribution Channel: E-Commerce Gains From Telemedicine Integration

In 2025, specialty pharmacies and durable-medical-equipment distributors commanded 57.59% of channel revenue. They achieved this by utilizing end-to-end prior-authorization and drop-shipment workflows, which are particularly favored by metabolic clinics. The integration of insurance billing with on-call dietitian services creates significant switching costs for families. While hospital pharmacies play a crucial role in acute-crisis scenarios, their contribution to chronic-formula volumes remains limited.

Direct-to-consumer e-commerce, growing at a 7.41% CAGR, is leveraging telemedicine follow-ups. These follow-ups often bundle video consultations with home leucine meters that are sensor-enabled. A pilot program in the Midwest demonstrated a 40% reduction in in-person appointments, leading to improved compliance and decreased travel expenses. Manufacturers are also innovating, offering subscription boxes that not only contain high-protein bars for caregivers but also feature QR codes for mixing instructions.

Geography Analysis

Regional disparities arise from variations in state Medicaid policies, population founder effects, and the concentration of academic centers. States with significant Mennonite or Amish populations, such as Pennsylvania, Ohio, and Indiana, report incidences as high as 1 in 380 births. This has driven localized increases in formula demand and transplant referrals. In contrast, sparsely populated Mountain West states often lack in-state metabolic specialists, prompting families to travel to major hubs like Seattle Children’s Hospital for urgent care.

Medicaid coverage differs significantly across states. Several Northeastern states classify BCAA-free products as pharmacy benefits with minimal copays, while others treat them as over-the-counter supplements, resulting in substantial out-of-pocket expenses. A 2024 clinic survey indicated that families in states without coverage were three times more likely to ration formula themselves, increasing the risk of decompensation. As a result, the U.S. Maple Syrup Urine Disease treatment market's e-commerce share is highest in regions where public coverage gaps overlap with extensive broadband access and employer-sponsored insurance.

Competitive Landscape

Abbott, Nutricia North America, Vitaflo USA, and Ajinomoto Cambrooke lead a moderately fragmented formula segment, competing on taste, micronutrient depth, and age-specific product lines. Nutricia’s Complex MSD Essential, supported by a decade of real-world outcome data, is widely utilized by clinics to standardize protocols. Abbott is piloting resealable, ready-to-drink pouches for school cafeterias, aiming to reduce lunchtime stigma and enhance daytime adherence. Meanwhile, Vitaflo’s app-linked refill reminders are gaining popularity among tech-savvy caregivers.

ASC Therapeutics is driving innovation in the emerging gene-therapy field, reporting a 100% survival rate in dual AAV9-treated calves and preparing for an Investigational New Drug filing with enrollment planned for late 2026. The University of Pennsylvania and Moderna are positioning themselves as strong competitors with their repeat-dosed mRNA alternative, particularly if challenges with AAV readministration persist. Various academic consortia, including the Imagine Institute and University College London, are developing liver-sparing vectors targeting muscle or brain, offering diversified approaches to organ-specific corrections.

If a one-time curative therapy succeeds, the U.S. Maple Syrup Urine Disease treatment market is expected to bifurcate into a pre-therapy cohort requiring lifelong formula and a post-therapy cohort with minimal dietary oversight. In anticipation of this shift, formula manufacturers are prototyping sachets for intermittent or thiamine-responsive cases and exploring mergers to consolidate R&D budgets. Strategic initiatives, such as licensing university intellectual property or acquiring home monitoring startups, could accelerate value creation as the therapeutic landscape evolves.

United States Maple Syrup Urine Disease Treatment Industry Leaders

Homology Medicines Inc.

Nutricia North America, Inc.

Abbott Laboratories.

Ajinomoto Cambrooke, Inc..

Astellas Pharma Inc..

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: : Plowshare Therapies licensed an AAV-vector MSUD program from UMass Chan Medical School, advancing the asset toward IND-enabling studies.

- August 2025: Evogene and Tel Aviv University launched a collaboration to model metabolite-driven self-assembly in ultra-rare disorders including Maple Syrup Urine Disease, leveraging AI-guided peptide design.

- February 2025: UMass Chan Medical School and ASC Therapeutics reported 100% survival and normalized growth in calf MSUD models treated with dual AAV9 gene therapy, prompting FDA discussion for Phase I/II trial design.

Global United States Maple Syrup Urine Disease Treatment Market Report Scope

As per the scope of the report, Maple Syrup Urine Disease (MSUD) is a rare, inherited metabolic disorder where the body cannot break down certain amino acids (leucine, isoleucine, and valine), leading to a toxic buildup and a sweet-smelling urine odor. Treatment in the US involves lifelong, strict low-protein diets, specialized formula, frequent blood monitoring, and prompt, emergency management of metabolic crises.

The United States Maple Syrup Urine Disease Treatment Market is segmented by disease phenotype, age group, and distribution channel. By disease phenotype, the market includes classic, intermediate, intermittent, and thiamine-responsive types. By age group, the market is segmented into neonates/infants, pediatrics, and adults. By distribution channel, the market is categorized into specialty pharmacies & DME, hospital pharmacies, and direct-to-consumer e-commerce. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Classic |

| Intermediate |

| Intermittent |

| Thiamine-responsive |

| Neonates / Infants |

| Pediatrics |

| Adults |

| Specialty Pharmacies & DME |

| Hospital Pharmacies |

| Direct-to-Consumer E-Commerce |

| By Disease Phenotype | Classic |

| Intermediate | |

| Intermittent | |

| Thiamine-responsive | |

| By Age Group | Neonates / Infants |

| Pediatrics | |

| Adults | |

| By Distribution Channel | Specialty Pharmacies & DME |

| Hospital Pharmacies | |

| Direct-to-Consumer E-Commerce |

Key Questions Answered in the Report

How large will the United States Maple Syrup Urine Disease treatment market be in 2031?

It is forecast to reach USD 59.45 million, advancing at a 6.07% CAGR from 2026 to 2031.

Which phenotype generates most revenue today?

Classic MSUD accounts for 67.34% of 2025 spending, reflecting near-total BCKD deficiency and continual formula use.

What is the fastest-growing segment by phenotype?

Thiamine-responsive cases are projected to grow at 7.77% CAGR through 2031 as genotype-guided dosing expands.

How are distribution channels shifting?

Direct-to-consumer e-commerce is rising at 7.41% CAGR thanks to telemedicine and home leucine monitoring, although specialty pharmacies still hold majority share.

Could gene therapy replace dietary management?

Preclinical AAV9 and mRNA platforms show curative potential, and first-in-human trials may begin by 2027; long-term durability and payer reimbursement will determine uptake.

Why does geographic location affect patient costs?

Medicaid rules on formula reimbursement differ by state, so families in non-coverage states face higher out-of-pocket spending, influencing adherence and outcomes.

Page last updated on: