Urinary Incontinence Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.97 Billion |

| Market Size (2031) | USD 7.06 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urinary Incontinence Therapeutics Market Analysis by Mordor Intelligence

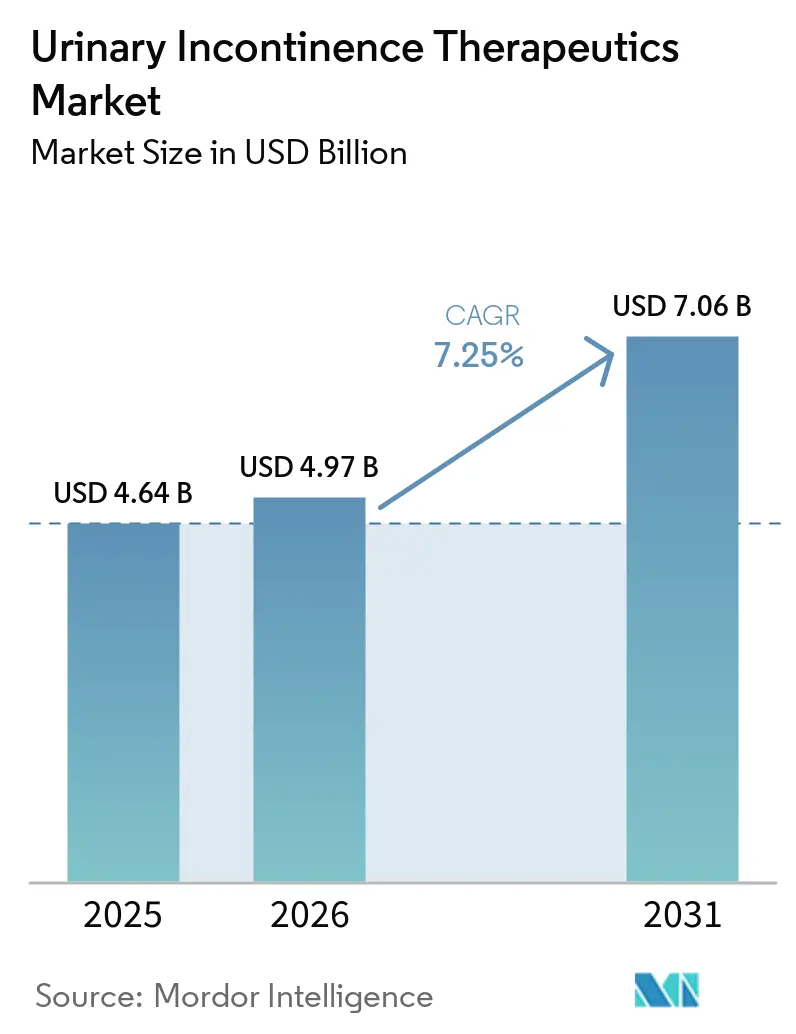

The Urinary Incontinence Therapeutics Market size is projected to expand from USD 4.64 billion in 2025 and USD 4.97 billion in 2026 to USD 7.06 billion by 2031, registering a CAGR of 7.25% between 2026 to 2031.

The urinary incontinence therapeutics market is supported by a large and growing patient base, with over 423 million adults aged 20 and above affected by urinary incontinence. This burden continues to rise due to the increasing prevalence of aging, obesity, diabetes, and neurological conditions. The market is also benefiting from improved diagnostics and stronger referral pathways, particularly in urban centers across Asia-Pacific and Latin America, where access to urology services through primary care is improving. Competitive activity in the market focuses on label expansion, life cycle management, managing generic entries, and promoting newer therapies with better tolerability. Additionally, telehealth-led prescribing, discreet pharmacy fulfillment, and enhanced patient engagement are reducing treatment hesitancy associated with stigma. These factors are driving steady market growth, with opportunities for further expansion in underdiagnosed populations, male patients, and digitally enabled treatment models.

Key Report Takeaways

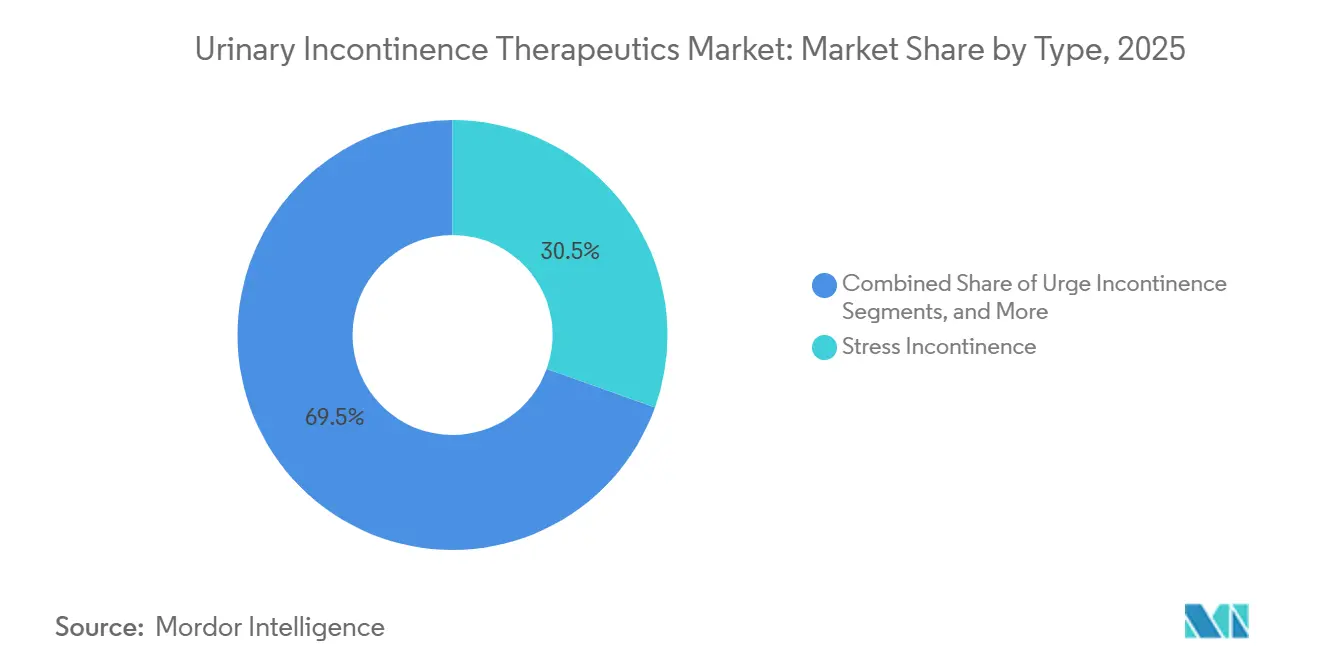

- By type, stress incontinence held 30.45% revenue share in 2025, while urge incontinence is projected to expand at a 7.66% CAGR through 2031.

- By drug class, anticholinergics accounted for 34.67% share in 2025, while beta-3 adrenoceptor agonists are projected to grow at an 8.12% CAGR through 2031.

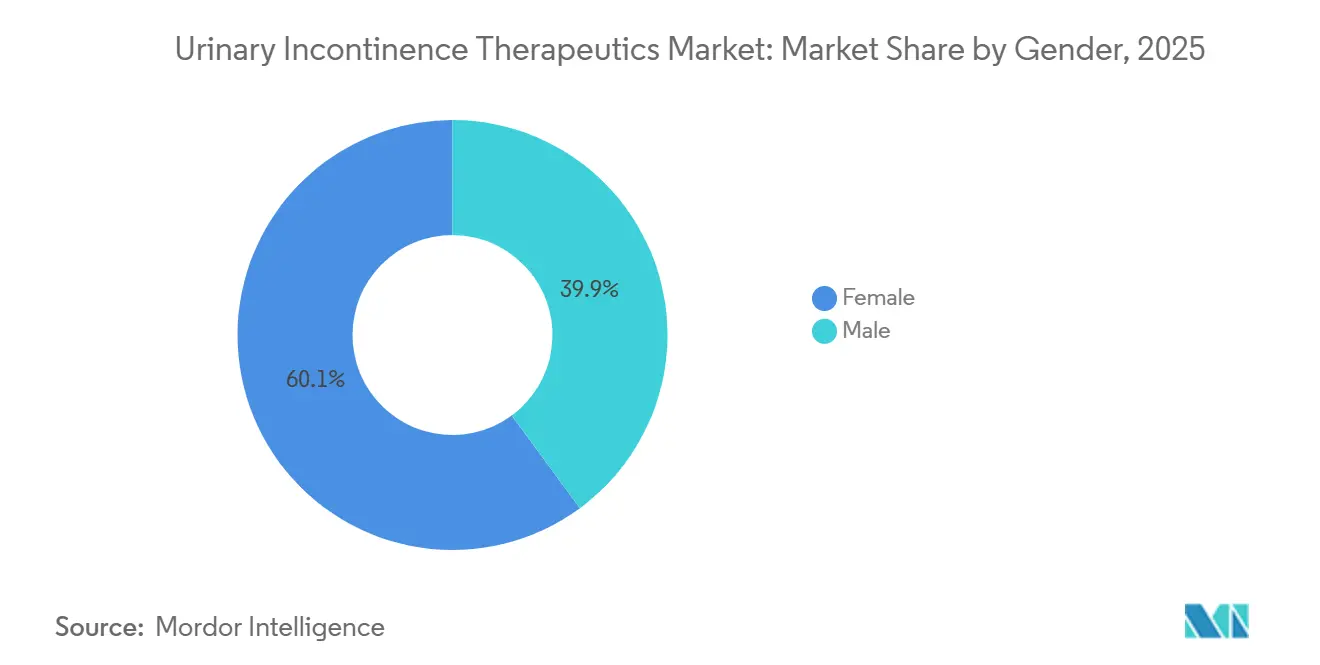

- By gender, female patients represented 60.11% share in 2025, while the male segment is expected to record the fastest CAGR at 8.75% through 2031.

- By distribution channel, retail pharmacies captured 44.93% share in 2025, while online pharmacies are projected to advance at a 7.90% CAGR through 2031.

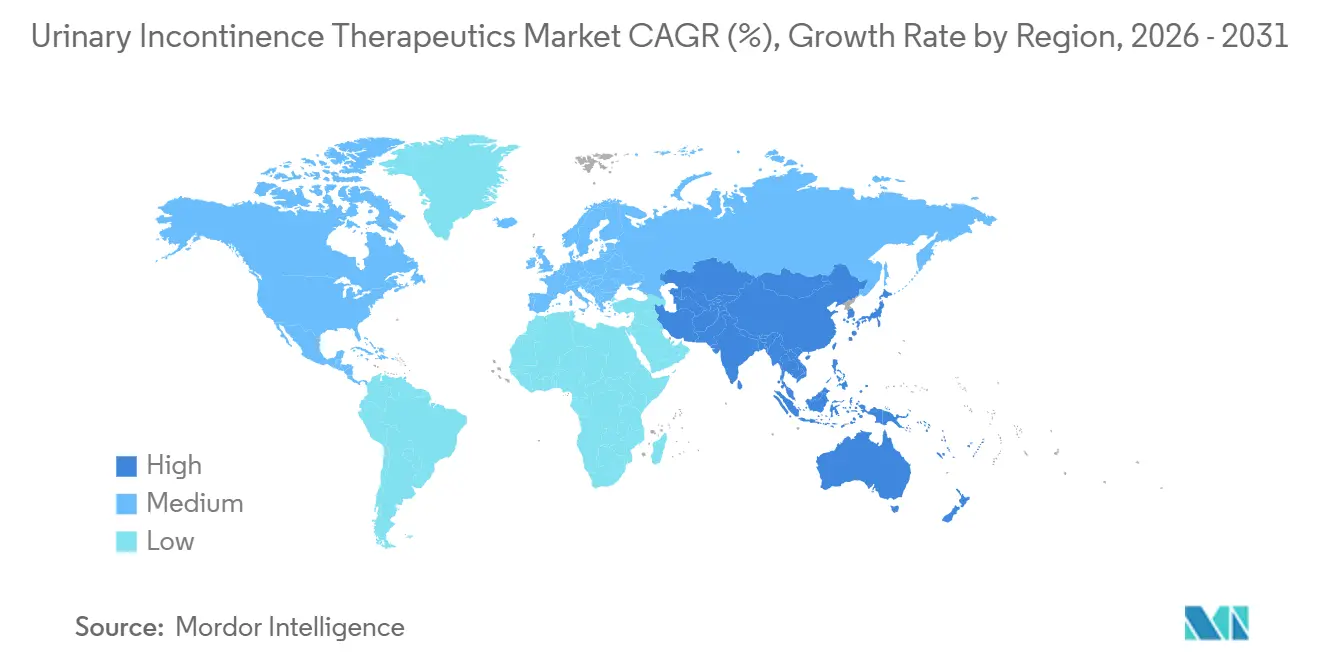

- By geography, North America held 40.08% share in 2025, while Asia-Pacific is projected to expand at an 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Urinary Incontinence Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence in aging and comorbid populations | +2.0% | Global, with highest concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Expanding female patient pool after pregnancy and postpartum care recognition | +1.5% | Global, highest uptake in North America and Europe | Medium term (2-4 years) |

| Growing uptake of minimally invasive and novel drug delivery approaches | +1.2% | North America and Europe, early traction in Asia-Pacific | Medium term (2-4 years) |

| Wider use of beta-3 agonists and combination pharmacotherapy regimens | +1.0% | North America, Europe, and Japan | Medium term (2-4 years) |

| Underdiagnosis to treatment conversion fueled by awareness campaigns | +0.8% | Asia-Pacific core, spillover to Middle East, Africa, and South America | Long term (≥ 4 years) |

| Treatment adoption driven by care setting expansion and digital health integration | +0.5% | Global, with strong momentum in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Urinary Incontinence in Aging and Comorbid Populations

With over 423 million adults aged 20 and above affected by urinary incontinence, as reported by the International Continence Society, the market for urinary incontinence therapeutics is witnessing significant growth.[1]International Continence Society, “ICS-EUS 2025 Abstract #256: Prevalence of Female Urinary Incontinence in the Developing World,” ICS Annual Meeting, ics.org Aging plays a pivotal role, as bladder function, pelvic support, and neurological control tend to weaken with age, leading to increased instances of urinary incontinence. Furthermore, as obesity, diabetes, and neurological disorders become more prevalent, they contribute to the rising burden of urinary incontinence. This dual influence from demographic aging and chronic diseases bolsters demand in primary care, urology, and urogynecology settings. Importantly, the market isn't merely generating demand; it's adeptly converting a visible and expanding patient pool into diagnosed and treated cases.

Expanding Female Patient Pool After Pregnancy and Postpartum Care Recognition

The urinary incontinence therapeutics market is increasingly recognizing the significant number of women experiencing symptoms post-pregnancy and childbirth. Up to 33% of women face postpartum urinary incontinence after a vaginal delivery, highlighting a treatment gap that is now garnering clinical attention. As pelvic floor care becomes integral to maternity follow-ups, women are being referred for urogynecology evaluations earlier than before. This is a notable shift, considering many patients previously navigated fragmented care pathways and delayed therapy for years. Backing this movement, the American Urogynecologic Society has advocated for consistent counseling during initial clinical contacts, facilitating timely discussions on symptoms and treatment planning. Consequently, the market is benefiting from a more defined treatment pathway for women, especially in health systems with structured postpartum care.

Growing Uptake of Minimally Invasive and Novel Drug Delivery Approaches

The urinary incontinence therapeutics market is witnessing a trend towards therapies that prioritize convenience and address tolerability concerns. Approaches like transdermal delivery are gaining traction, as they mitigate side effects associated with some oral treatments and enhance adherence, especially for patients on multiple medications. This shift is advantageous for the market, as reformulated products can rejuvenate older molecules, sidestepping the reliance on low-cost generics. Moreover, clinical developments are expanding the treatment demographic, encompassing younger patients and those requiring tailored pathways. Innovative methods, such as implantable and office-based neuromodulation, are bolstering specialist care pathways, ensuring continuity in prescription reviews and follow-ups. This evolution allows the market to capture value not just from new prescriptions but also from sustained long-term treatment.

Wider Use of Beta-3 Agonists and Combination Pharmacotherapy Regimens

The urinary incontinence therapeutics market is witnessing a pronounced shift towards beta-3 agonists and combination therapy regimens. This trend gained momentum with the December 2024 FDA nod to vibegron, specifically for men grappling with overactive bladder symptoms and undergoing pharmacological therapy for benign prostatic hyperplasia. This endorsement unlocked access to a clinically significant patient demographic, previously less tapped for beta-3 agonist treatments. Furthermore, physicians are increasingly at ease integrating newer agents with established urology medications, provided the symptom profile aligns. This evolution diminishes the default preference for older antimuscarinics, enhancing the market's quality mix as newer agents carve out a more substantial share of therapy initiations and specialist endorsements.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent underreporting due to social stigma and embarrassment | -1.0% | Global, most pronounced in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Adherence challenges linked to dry mouth, constipation, and cognitive side effects | -0.8% | Global | Medium term (2-4 years) |

| Reimbursement friction for brand only and patented therapies | -0.6% | Europe, Asia-Pacific, and South America | Medium term (2-4 years) |

| Limited real world differentiation across competing drug classes | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Underreporting Due to Social Stigma

The urinary incontinence therapeutics market faces challenges due to underreporting and delayed diagnoses. The European Association of Urology reported that in the UK, fewer than one-third of women with moderate to severe urinary incontinence sought health or social services support. Stigma prevents many patients from accessing formal care, with some opting for pads, lifestyle changes, or self-management over prescription treatments. This issue persists even in urban and educated populations, where embarrassment deters disclosure. Inconsistent screening efforts across national health systems further limit market growth, as symptom reporting remains uncommon in primary care and women’s health visits.

Adherence Challenges Linked to Dry Mouth, Constipation, and Cognitive Side Effects

Adherence remains a key challenge in the urinary incontinence therapeutics market, particularly with older anticholinergic therapies. A 2025 study found that patients on anticholinergic drugs for overactive bladder had a 28% higher risk of dementia compared to those on mirabegron. The AUA and SUFU guidelines now recommend that clinicians discuss potential cognitive risks with patients on chronic antimuscarinic therapy.[2]PubMed, “Systematic Review and Meta-Analysis on Anticholinergic Drugs and Dementia Risk in Overactive Bladder,” National Library of Medicine, pubmed.ncbi.nlm.nih.gov This has led to a gradual shift away from older, high-volume agents toward newer therapies. However, challenges such as reimbursement issues, patient habits, and physician preferences hinder seamless transitions. Concerns about tolerability and long-term safety continue to impact drug adherence and persistence across classes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stress Incontinence Holds the Largest Base While Urge Incontinence Builds Faster Prescription Momentum

In 2025, stress incontinence accounted for 30.45% of the urinary incontinence therapeutics market, maintaining its leading position. This dominance stems from the high prevalence of sphincter weakness and pelvic floor dysfunction, particularly among women post-pregnancy and during hormonal transitions. Clinicians continue to manage a significant patient pool in this segment, supported by established care pathways. While initial treatments focus on behavioral and pelvic floor support, pharmacologic interventions remain essential for persistent or disruptive symptoms. Consistent prescribing patterns ensure the segment's stability, even as newer therapies gain traction.

Stress incontinence benefits from frequent consultations with gynecology, primary care, and urogynecology services, creating opportunities for treatment discussions. The segment is a reliable volume driver due to its association with life events like childbirth and menopause. Mixed and overflow presentations are less common and more complex, often requiring multi-mechanism treatments. Functional incontinence remains reliant on neurological or structural management, limiting its drug revenue potential. Urge incontinence, however, is projected to grow at a 7.66% CAGR through 2031, driven by therapies like beta-3 agonists and improved pharmacotherapy follow-ups.

By Drug Class: Anticholinergics Still Lead, but Beta-3 Agonists Are Redefining Therapy Mix

Anticholinergics held 34.67% of the urinary incontinence therapeutics market in 2025, maintaining their position as the largest drug class. Their dominance is supported by widely used medications such as oxybutynin, tolterodine, and solifenacin, along with their cost-effectiveness and broad formulary presence. Physicians' familiarity with this class also slows the transition to newer options, despite growing safety concerns. However, while anticholinergics lead in market share, they lag in growth momentum.

Beta-3 adrenoceptor agonists are forecast to grow at an 8.12% CAGR through 2031, making them the fastest-growing drug class. Their rise is attributed to better tolerability, increased physician confidence, and recent label expansions. The December 2024 FDA approval for vibegron in men with benign prostatic hyperplasia has further strengthened their adoption. Other drug classes, including estrogen, desmopressin, alpha blockers, tricyclic antidepressants, and botulinum toxin, continue to play niche but important roles, ensuring diversity in therapeutic mechanisms.

By Gender: Female Patients Dominate Demand While Male Uptake Accelerates

In 2025, women accounted for 60.11% of the urinary incontinence therapeutics market, driven by factors such as pregnancy, childbirth, menopause, and lower urethral resistance. The market benefits from a well-established care pathway for women, with strong links to gynecology and women's health screenings. This maturity supports higher treatment volumes and continuity, ensuring women remain the primary demand base despite growing opportunities in the male segment.

The male segment is projected to grow at an 8.75% CAGR through 2031, driven by increased awareness of post-prostatectomy incontinence, overactive bladder treatment, and therapies for benign prostatic hyperplasia. The December 2024 vibegron label expansion has opened new treatment avenues for men. Additionally, reduced stigma around male urinary incontinence is encouraging more consultations and follow-ups, contributing to a broader gender mix in the market.

By Distribution Channel: Retail Pharmacies Lead, While Online Pharmacies Gain Refill and Access Momentum

Retail pharmacies held 44.93% of the urinary incontinence therapeutics market in 2025, maintaining their leading position. Their dominance is attributed to convenience, pharmacist interaction, and established insurance reimbursement pathways for prescriptions. Hospital pharmacies remain relevant for specialist-managed cases, particularly those involving inpatient care or complex conditions. However, routine oral therapies primarily flow through retail pharmacy networks, ensuring their central role in adherence and refill continuity.

Online pharmacies are projected to grow at a 7.90% CAGR through 2031, driven by telehealth normalization, discreet ordering, and patient preference for privacy. The extension of telemedicine flexibilities for prescription medications through December 2026 has further supported this channel. As subscription deliveries and remote follow-ups reduce therapy interruptions, online pharmacies are expected to gain momentum. Despite this growth, retail pharmacies are likely to remain the largest distribution channel due to their alignment with patient and prescriber habits.

Geography Analysis

In 2025, North America accounted for 40.08% of the urinary incontinence therapeutics market, making it the largest regional contributor. High diagnosis rates, extensive insurance coverage, and strong referral systems between primary care and urology drive this dominance. The U.S. remains the primary revenue center due to established prescribing pathways and better patient access to specialist care. The FDA approval of vibegron in December 2024 for men with overactive bladder symptoms linked to benign prostatic hyperplasia is expected to boost prescriptions. Additionally, the region benefits from a competitive generic market, sustaining treatment volumes despite evolving branded competition.

Europe remains a significant market, with Germany, the UK, and France leading in prescription volumes. The European Association of Urology has emphasized the socioeconomic burden of the condition and the need for early intervention. Access to newer therapies, including vibegron, has improved following European Commission marketing authorization in 2024, enhancing the competitive treatment landscape. However, reimbursement policies and country-specific access pathways continue to influence the transition from older anticholinergics to newer options.

Asia-Pacific is projected to grow at a CAGR of 8.95% through 2031, making it the fastest-growing regional segment. Japan's aging population drives demand, with a shift toward modern oral therapies. China and India contribute to growth as diagnosis pathways, specialist access, and pharmacy infrastructure improve in urban areas. Increased awareness and a growing willingness to seek treatment for previously unmanaged symptoms further support market expansion. While the Middle East, Africa, and South America represent smaller segments, their developing private clinic networks, awareness initiatives, and access models highlight their potential for future growth.

Competitive Landscape

The urinary incontinence therapeutics market features a mix of branded innovators and generic manufacturers competing across therapy classes, pricing tiers, and reimbursement scenarios. Key branded players include Astellas Pharma, Sumitomo Pharma, Pfizer, AbbVie, and Ferring, while generic competitors include Lupin, Teva, Dr. Reddy’s, Viatris, and Zydus Lifesciences. This competitive landscape prevents any single company from dominating the treatment spectrum, which spans oral agents, specialist therapies, and niche indications. Branded companies focus on label expansions, evidence generation, and strategic agreements, while generics emphasize pricing, accessibility, and formulary presence. The market's dynamics highlight the importance of therapy class strength alongside brand recognition.

In April 2026, Astellas secured a USD 75 million upfront payment from MSN Pharmaceuticals under a revised mirabegron license agreement, showcasing a structured approach to managing generic competition. Similarly, in December 2024, Sumitomo Pharma received FDA approval for GEMTESA, expanding its use to men with overactive bladder symptoms associated with benign prostatic hyperplasia. In Europe, Pierre Fabre strengthened its position in 2024 with marketing authorization for OBGEMSA, enhancing access to vibegron across EU markets. These developments reflect the market's evolution driven by regulatory advancements and disciplined life cycle management.

Urinary Incontinence Therapeutics Industry Leaders

AbbVie Inc.

Astellas Pharma Inc.

Bayer AG

Pfizer Inc.

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Urovant Sciences, a subsidiary of Sumitomo Pharma, announced positive Phase III trial results for vibegron, targeting incontinence associated with overactive bladder. This achievement positions the company for an expanded FDA submission later this year.

- December 2025: Versameb AG advanced its RNA-based therapy, VMB-100, into Phase II trials, focusing on addressing stress urinary incontinence through a novel regenerative mechanism.

- July 2025: Eisai Co., Ltd. in partnership with KYORIN Pharmaceutical Co., Ltd. announced the launch of Beova Tablets (vibegron) for overactive bladder treatment and urinary incontinence in Thailand through their subsidiary, Eisai (Thailand) Marketing Co., Ltd.

- February 2025: EG 427 initiated a Phase I/II clinical trial for its gene therapy candidate, EG-110, aimed at restoring bladder control by modulating nerve signaling.

Global Urinary Incontinence Therapeutics Market Report Scope

As per the scope of the report, urinary incontinence therapeutics are the treatments used to manage or cure the loss of bladder control, which causes accidental urine leakage. These treatments range from daily lifestyle changes and muscle training to advanced surgeries.

The urinary incontinence therapeutics market is segmented by type, drug class, gender, distribution channel, and geography. By type, the market includes stress incontinence, urge incontinence, overflow incontinence, functional incontinence, and mixed incontinence. By drug class, the market is segmented into anticholinergics, beta-3 adrenoceptor agonists, alpha blockers, estrogen, desmopressin, tricyclic antidepressants, and other drug classes. By gender, the market is categorized into female and male. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Stress Incontinence |

| Urge Incontinence |

| Overflow Incontinence |

| Functional Incontinence |

| Mixed Incontinence |

| Anticholinergics |

| Beta-3 Adrenoceptor Agonists |

| Alpha Blockers |

| Estrogen |

| Desmopressin |

| Tricyclic Antidepressants |

| Other Drug Classes |

| Female |

| Male |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Stress Incontinence | |

| Urge Incontinence | ||

| Overflow Incontinence | ||

| Functional Incontinence | ||

| Mixed Incontinence | ||

| By Drug Class | Anticholinergics | |

| Beta-3 Adrenoceptor Agonists | ||

| Alpha Blockers | ||

| Estrogen | ||

| Desmopressin | ||

| Tricyclic Antidepressants | ||

| Other Drug Classes | ||

| By Gender | Female | |

| Male | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the urinary incontinence therapeutics market?

The urinary incontinence therapeutics market stands at USD 4.97 billion in 2026 and is projected to reach USD 7.06 billion by 2031, growing at a CAGR of 7.25% during the forecast period.

Which region leads urinary incontinence therapeutics revenue?

North America led the urinary incontinence therapeutics market with a 40.08% share in 2025, supported by high diagnosis rates, insurance coverage, and a well-established specialist referral system.

Which region is growing the fastest in urinary incontinence therapeutics?

Asia-Pacific is the fastest-growing region in the urinary incontinence therapeutics market, with an 8.95% CAGR over 2026-2031, supported by aging demographics and improving care access.

Which drug class is expanding the fastest?

Beta-3 adrenoceptor agonists are the fastest-growing drug class in the urinary incontinence therapeutics market, with an 8.12% CAGR through 2031, reflecting a shift toward better tolerated therapies.

Which patient group offers the strongest growth opportunity?

Male patients are the fastest-growing gender segment in the urinary incontinence therapeutics market, with an 8.75% CAGR through 2031, helped by broader prescribing options in patients with overactive bladder and benign prostatic hyperplasia.

Which sales channel is changing the market structure the most?

Online pharmacies are changing refill and access patterns in the urinary incontinence therapeutics market, with a projected 7.90% CAGR through 2031 as telehealth and privacy-led purchasing become more common.

Page last updated on: