United States Lawn Mowers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

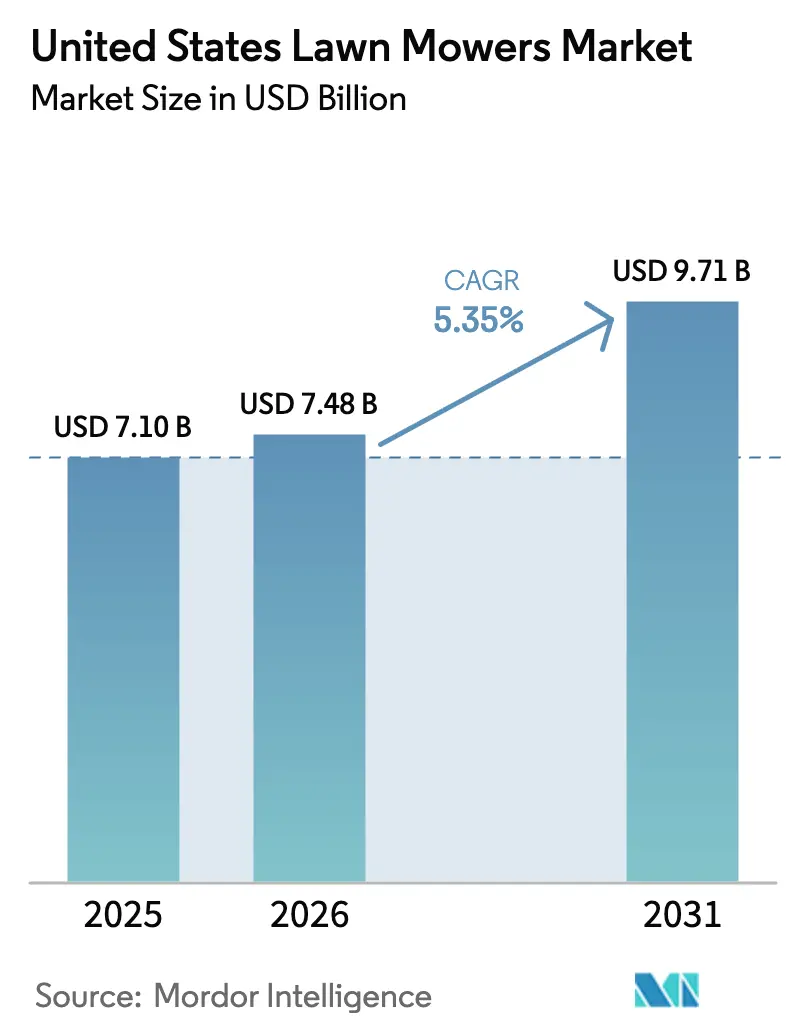

| Base Year Market Size (2025) | USD 7.1 Billion |

| Market Size (2026) | USD 7.48 Billion |

| Market Size (2031) | USD 9.71 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Lawn Mowers Market Analysis by Mordor Intelligence

The United States lawn mowers market size was valued at USD 7.1 billion in 2025 and estimated to grow from USD 7.48 billion in 2026 to reach USD 9.71 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031). California’s 2024 ban on new gasoline-powered small off-road engines, approved by the Environmental Protection Agency (EPA) in January 2025, forces manufacturers to accelerate investment in battery platforms even though gasoline models still dominated demand in 2024. Lithium-ion pack prices falling below USD 100 per kilowatt-hour during 2024 removes a long-standing cost barrier, allowing battery-electric units to close the total-cost-of-ownership gap with gasoline models within two years of purchase. Professional landscapers coping with a 12% labor vacancy rate are shifting to robotic and zero-turn electric machines that reduce fuel logistics and operator fatigue, while municipalities are piloting subscription fleets that convert one-time equipment purchases into recurring service contracts. Ongoing dealer channel strength and growing direct-to-consumer e-commerce sales illustrate how distribution models are fragmenting as incumbents race to defend share against battery specialists.

Key Report Takeaways

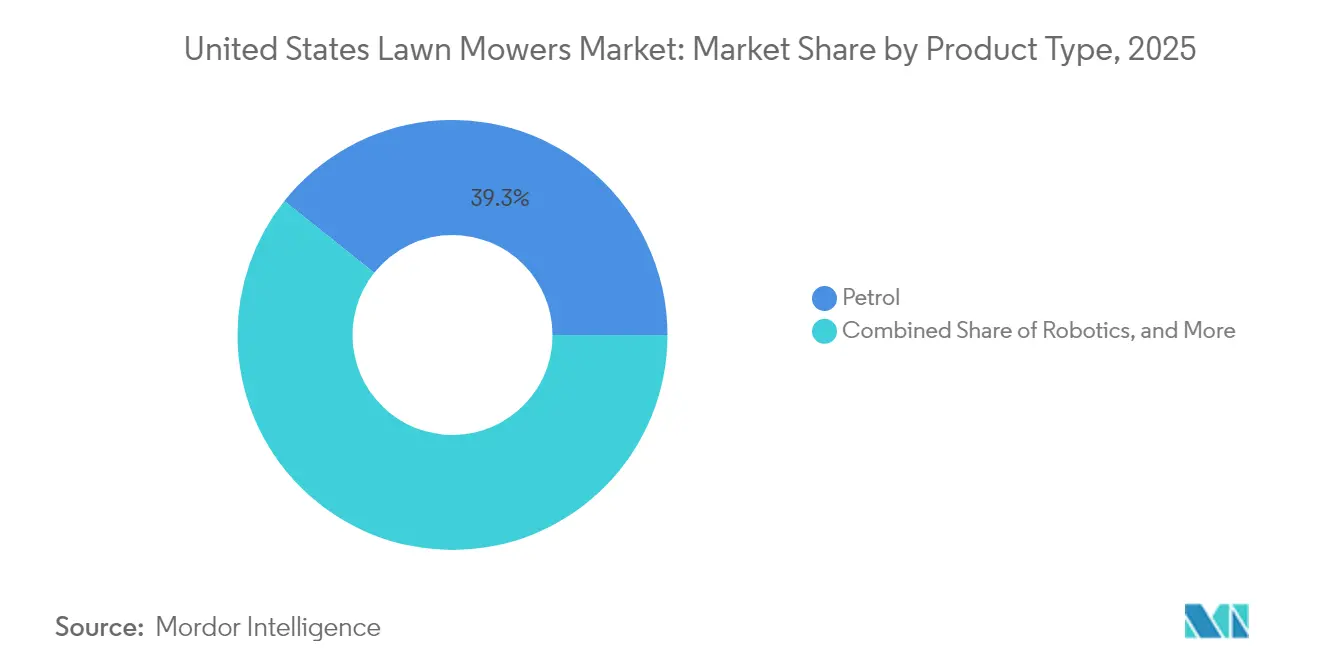

- By product type, petrol holds the largest share, accounting for 39.30% of the United States lawn mowers market size in 2025, whereas robotic are forecast to post the fastest 18.4% CAGR through 2031.

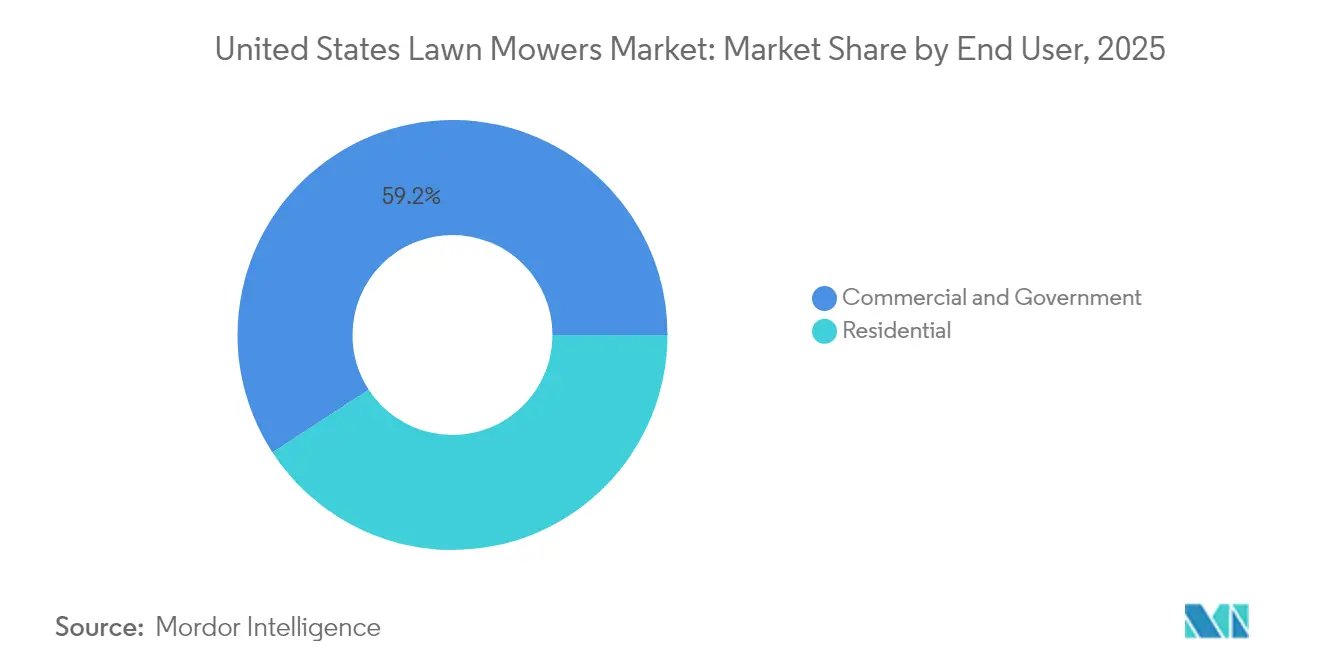

- By end user, commercial buyers captured 59.20% of the United States lawn mower market size in 2025, while residential users are projected to grow at a 5.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Lawn Mowers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for landscaped residential yards | +1.2% | National, strongest in the South and the West | Long term (≥ 4 years) |

| State-level bans on new small-off-road gas engines | +1.8% | West and Northeast | Short term (≤ 2 years) |

| Accelerating adoption of battery-powered platforms by major OEMs | +1.4% | National, led by West Coast and the Northeast | Medium term (2-4 years) |

| Rapid cost declines in lithium-ion packs | +0.9% | National | Medium term (2-4 years) |

| Subscription-based autonomous mower fleets for municipalities | +0.5% | Urban municipalities in the West and the Northeast | Long term (≥ 4 years) |

| Turf-analytics platforms boosting mower replacement cycles | +0.3% | Commercial landscaping nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Landscaped Residential Yards

Homeownership rates stabilized near 66% in 2024, sustaining baseline demand for lawn maintenance equipment across single-family properties. The strategic implication lies in the shift toward larger-lot suburban development in Sun Belt markets, where median yard sizes exceed 0.25 acres and require ride-on or zero-turn platforms rather than walk-behind units. This geographic skew elevates average selling prices and favors Original Equipment Manufacturer (OEMs) with strong dealer networks in Texas, Florida, and Arizona. Curb appeal remains a key driver of resale value, with landscaped properties commanding premiums of 5% to 10% in competitive housing markets, ensuring replacement cycles continue even during economic uncertainty. The Environmental Protection Agency's (EPA) WaterSense partnership is promoting drought-tolerant turf alternatives, which could reduce mowing frequency in arid regions.

State-Level Bans on New Small Off-Road Gas Engines

In 2024, California's Air Resources Board finalized regulations prohibiting the sale of new gasoline-powered small off-road engines starting with model year 2024 equipment, with full enforcement planned for 2026. In January 2025, the Environmental Protection Agency (EPA) granted California a Clean Air Act waiver, allowing the state to implement stricter standards than those mandated by federal regulations[1]Source: U.S. Environmental Protection Agency, “EPA Grants California Waiver for Small Off-Road Engine Regulations,” epa.gov. This waiver allows other states to adopt California's framework without requiring separate federal approval. States such as Oregon and Washington, as well as several in the Northeast, are considering similar measures. The impact of these regulations is significant. Original Equipment Manufacturers (OEMs) are unlikely to sustain dual production lines due to economic constraints, effectively making California's rules a national standard for equipment sold after 2026. Additionally, compliance extends beyond emissions to noise regulations. Battery-powered mowers, which operate at 60 to 70 decibels compared to over 90 decibels for gasoline models, enable mowing during early-morning and late-evening hours in municipalities with noise restrictions.

Accelerating Adoption of Battery-Powered Platforms by Major OEMs

Deere and Company, The Toro Company, and Husqvarna Group have collectively invested over USD 500 million in battery platform development between 2023 and 2024, as reported in their annual reports and investor presentations. Deere introduced the Z370R electric zero-turn mower in 2024, offering runtime comparable to gas-powered models, capable of mowing up to 2.5 acres per charge for commercial operators. Toro expanded its 60-volt battery product range across both residential and commercial markets, while Husqvarna's CEORA autonomous mower gained popularity in municipal and golf-course applications. This strategic shift underscores the recognition that battery technology has now met the performance requirements for professional use, addressing the primary concerns that previously hindered its adoption. Charging infrastructure remains a challenge, as commercial fleets require 240-volt Level 2 chargers to reduce downtime, and suburban electrical panels often lack the capacity to support multiple simultaneous charges without expensive service upgrades.

Rapid Cost Declines in Lithium-Ion Packs

In 2024, lithium-ion battery pack prices averaged USD 95 per kilowatt-hour, a significant decrease from USD 153 per kilowatt-hour in 2022. This decline was driven by increased manufacturing scale in the automotive industry and advancements in cell chemistry. The cost reduction has directly influenced the economics of lawn mowers. For instance, a 5-kilowatt-hour battery pack used in premium zero-turn mowers cost approximately USD 765 in 2022 but dropped to USD 475 in 2024, reducing the price disparity with gasoline-powered models. Total cost of ownership calculations now favor battery-powered units for commercial operators using equipment for over 500 hours annually. Savings in fuel and maintenance costs offset the higher initial investment within 18 to 24 months. This shift is significant as it transitions purchasing decisions from early adopters to mainstream buyers, who prioritize return on investment over environmental considerations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled landscaping labor inflating service costs | -0.7% | National, most acute in metropolitan areas | Short term (≤ 2 years) |

| High upfront price of robotic and commercial zero-turn units | -0.9% | Nationwide, weighs on residential and small commercial buyers | Medium term (2-4 years) |

| Grid-capacity limits for large charging depots in suburbs | -0.4% | South and West suburbs with aging transformers | Long term (≥ 4 years) |

| Theft and vandalism risk for unattended robotic mowers | -0.3% | Urban corridors and dense suburbs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Landscaping Labor Inflating Service Costs

The landscaping services market experienced a 12% vacancy rate in 2024, marking the highest level in a decade. This shortage was driven by immigration restrictions and demographic changes that reduced the available workforce. In response, operators increased hourly service rates, which ranged from USD 50 to USD 75 per hour in metropolitan areas, compared to USD 40 to USD 60 in 2022 [2]Source: U.S. Bureau of Labor Statistics, “Landscaping Services Labor Market Analysis,” bls.gov . Rising labor costs have prompted residential customers to shift toward do-it-yourself lawn care, thereby expanding the market for consumer-grade mowers. Professional landscapers face compressed margins as they are unable to fully pass on cost increases to price-sensitive clients. The labor shortage has also heightened interest in autonomous and zero-turn electric mowers, which help reduce operator fatigue and allow a single worker to cover larger areas. Despite this, adoption remains limited due to capital constraints faced by small and mid-sized landscaping firms.

High Upfront Price of Robotic and Commercial Zero-Turn Units

Robotic lawn mowers are priced between USD 1,200 and USD 4,500 for residential models, while commercial-grade autonomous units cost over USD 15,000. In comparison, gasoline push mowers are priced between USD 300 and USD 800, and gas-powered zero-turn models range from USD 3,000 to USD 8,000. This significant price difference limits adoption among cost-conscious homeowners and small landscaping businesses operating with narrow profit margins. Although financing options and leasing programs are becoming available to address affordability, they introduce additional complexity and interest costs, which can discourage buyers unfamiliar with equipment financing. This challenge is particularly pronounced in the residential segment, where discretionary spending on lawn care competes with other home improvement priorities. Additionally, homeowners often focus on upfront costs rather than evaluating the total cost of ownership over multiple years, further hindering adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robotic Units Gain Commercial Traction

Petrol holds the largest share, accounting for 39.30% of the United States lawn mower market size in 2025, reflecting its entrenched position in residential and small commercial applications. Replacement demand is shifting toward battery-electric alternatives as California's 2024 ban on new gasoline-powered vehicles takes effect. Petrol mowers face the steepest headwinds, as state-level emission bans and noise ordinances erode their value proposition, yet they remain the lowest-cost option for budget-conscious buyers in states without regulatory pressure.

Robotic lawn mowers are forecast to grow at a 18.4% CAGR through 2031, the fastest expansion across all product categories, driven by municipal fleet adoptions and commercial landscaping trials. The robotic lawn mower segment is experiencing remarkable growth, emerging as the fastest-growing category in the market. This impressive growth is driven by rapid technological advancements in artificial intelligence, the Internet of Things (IoT), and machine learning capabilities.

By End User: Commercial Segment Drives Growth

Commercial buyers captured 59.20% of the United States lawn mower market size in 2025. The commercial segment's faster growth reflects structural drivers: landscaping companies operating equipment for more than 500 hours annually achieve total cost of ownership savings with battery-electric units within 18 to 24 months, as the higher upfront costs are offset by fuel and maintenance expenses. Residential buyers, by contrast, prioritize initial purchase price and are slower to adopt premium battery platforms absent regulatory mandates.

Residential users are projected to grow at a 5.3% CAGR through 2031, reflecting the large installed base of single-family homeowners. Their purchasing decisions are increasingly influenced by noise ordinances and emission regulations that favor battery-electric models. Government and municipal buyers represent a smaller but strategically important segment, piloting subscription-based robotic fleets to reduce operating expenses and meet emissions targets without upfront capital outlays.

Geography Analysis

The South region holds the largest share of the United States lawn mower demand in 2025, driven by year-round growing seasons, larger average yard sizes, and high single-family homeownership rates in Texas, Florida, and Georgia. The West region is forecast to grow at the fastest rate from 2026 to 2031, driven by California's 2024 ban on new petrol small off-road engines and state incentive programs that subsidize the purchase of battery-electric equipment.

The Midwest region maintains steady demand, anchored by residential and agricultural applications, while the Northeast faces slower growth due to shorter growing seasons and higher population density, which reduces average yard sizes. California's Air Resources Board regulations, authorized by the Environmental Protection Agency (EPA) in January 2025, effectively set a national standard, as OEMs cannot economically maintain dual production lines for compliant and non-compliant states.

The South's dominance reflects not only climate and yard size but also cultural preferences for landscaped properties as markers of homeownership success, sustaining replacement cycles even during economic uncertainty. The West's regulatory environment is accelerating a structural shift: California's ban, combined with Oregon and Washington's evaluations of similar measures, creates a de facto regional standard that pressures OEMs to prioritize battery platform development over petrol product refreshes.

Competitive Landscape

The United States lawn mower market exhibits high concentration, with the top five players including Deere & Company, The Toro Company, Husqvarna AB, Stanley Black & Decker Outdoor (MTD), and American Honda Motor Co., Inc. This oligopoly structure limits price competition but creates strategic vulnerability as smaller battery-specialist brands like Mean Green Products and Greenworks Tools capture commercial fleet contracts by offering lower total cost of ownership and faster charging solutions.

Opportunities exist in the mid-tier battery-electric zero-turn mower segment, priced between USD 5,000 and USD 8,000. This segment remains underserved, as incumbents primarily focus on premium commercial units and entry-level residential models. Emerging disruptors are utilizing direct-to-consumer sales channels to avoid dealer markups and offer competitive pricing. These disruptors often lack the service networks required by professional landscapers for equipment priced at USD 10,000 or more.

Technology adoption within the market is inconsistent. Products like Husqvarna's CEORA autonomous mower and Toro's Lynx turf-management platform highlight the growing importance of connectivity and data analytics as competitive differentiators. Despite this, many OEMs continue to treat these capabilities as aftermarket add-ons rather than integrating them as core product features. Additionally, the EPA's authorization of California's Clean Air Act waiver in January 2025 is accelerating industry changes. OEMs that delayed battery platform development now face a compressed timeline to meet 2026 compliance deadlines, potentially requiring dual production lines to address regulatory requirements.

United States Lawn Mowers Industry Leaders

Deere & Company

The Toro Company

Husqvarna AB

Stanley Black & Decker Outdoor (MTD)

American Honda Motor Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: John Deere expands its residential zero-turn mower lineup with the introduction of its first model to feature removable battery technology. The Z370RS Electric ZTra Mower was developed in collaboration with EGO, a leader in battery-powered outdoor equipment. Featuring the EGO 56V ARC Lithium removable battery system, the Z370RS Electric delivers enhanced flexibility and convenience for homeowners. The removable batteries can be used across the entire suite of EGO products, providing a seamless outdoor lawn-cleanup experience.

- September 2023: John Deere has a partnership with EGO and parent company Chervon, a leading global provider to the Outdoor Power Equipment (OPE) and Power Tool industries. The agreement will enable the brands to offer homeowners EGO battery-powered lawn care solutions through John Deere dealers.

- May 2023: Ariens, a brand of AriensCo, introduced the IKON ONYX, a custom zero-turn lawnmower with a 52-inch deck, equipped with a 23-horsepower Kawasaki FR691V engine, in the United States.

United States Lawn Mowers Market Report Scope

A lawn mower, also known as a grass cutter, is a machine used to cut grass in agriculture, gardening, landscaping, and horticulture. This machine has one or more revolving blades to cut the grass. The United States lawn mowers market is segmented by product type and end user. By product type, the market has been segmented into manual, electric, petrol, robotics, and other product types. By end user, the market has been bifurcated into residential and commercial/government. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Manual |

| Electric |

| Petrol |

| Robotics |

| Other Product Types |

| Residential |

| Commercial or Government |

| Product Type | Manual |

| Electric | |

| Petrol | |

| Robotics | |

| Other Product Types | |

| End User | Residential |

| Commercial or Government |

Key Questions Answered in the Report

How large is the United States lawn mowers market in 2026?

It is valued at USD 7.48 billion, with a forecast to reach USD 9.71 billion by 2031.

Which product type is growing the fastest?

Robotic mowers lead with a projected 18.4% CAGR through 2031, driven by commercial and municipal pilots.

Why are battery-electric mowers gaining share?

Lithium-ion pack prices below USD 100/kWh and state bans on gasoline engines make battery models cost-competitive within two years of purchase.

What limits rapid electrification for commercial fleets?

Suburban grid capacity constraints and the cost of installing multiple Level 2 chargers slow large-scale fleet rollouts.

Page last updated on: