Electric Lawn Mowers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.20 Billion |

| Market Size (2031) | USD 11.40 Billion |

| Growth Rate (2026 - 2031) | 12.95% CAGR |

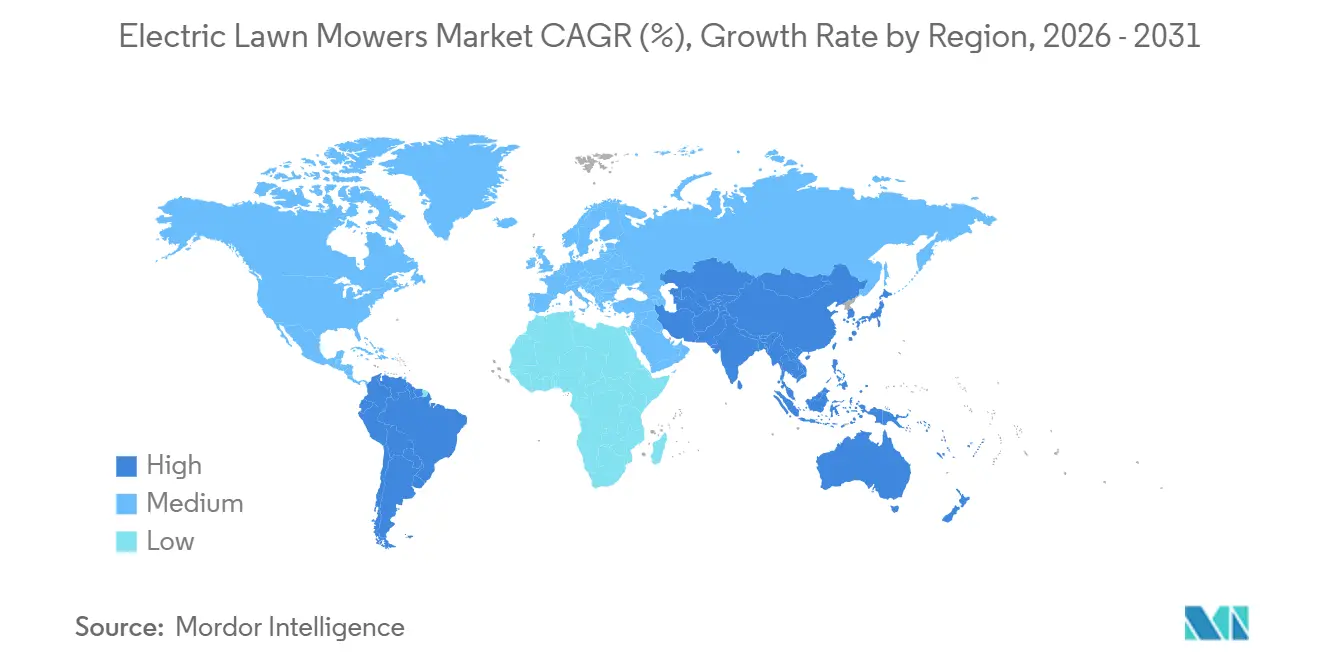

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

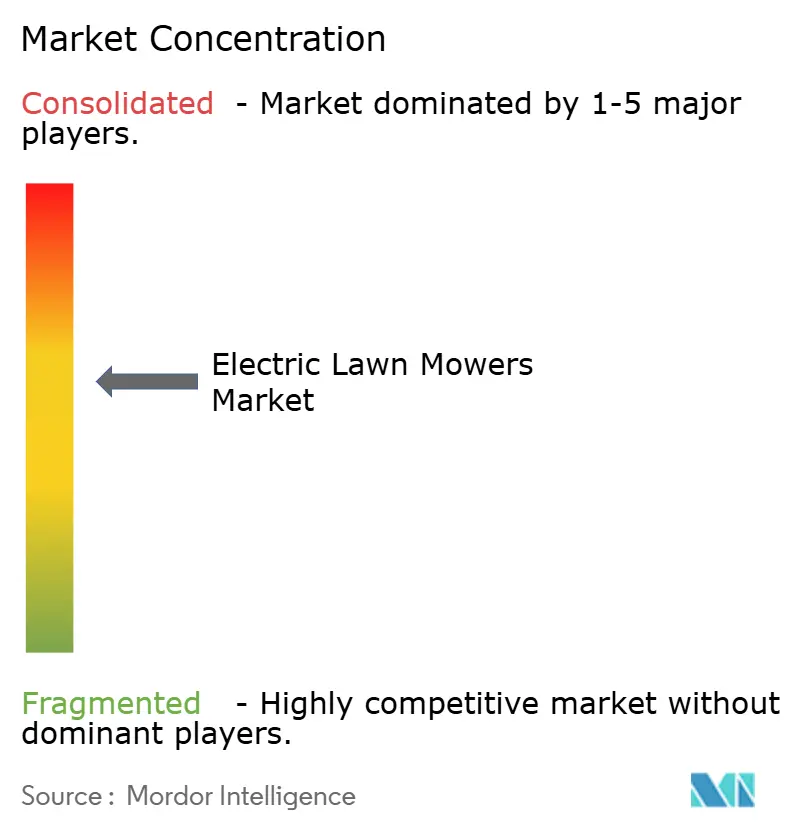

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Lawn Mowers Market Analysis by Mordor Intelligence

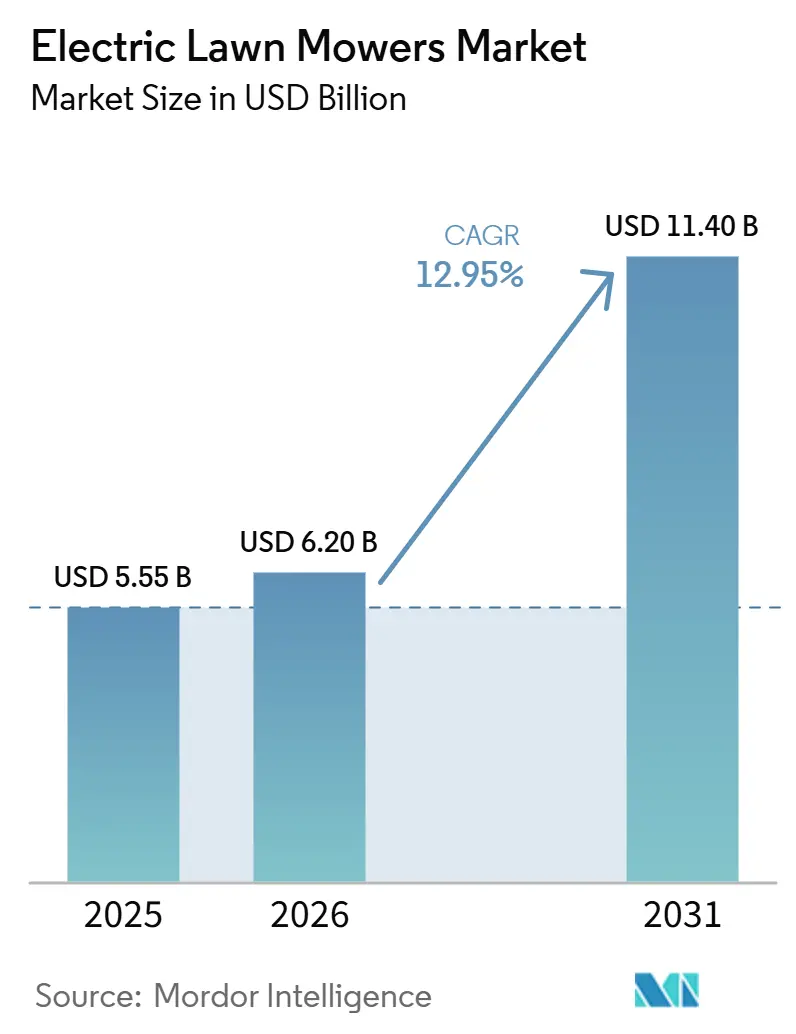

The electric lawn mower market size was valued at USD 5.55 billion in 2025 and is estimated to reach USD 6.20 billion in 2026, and is projected to reach USD 11.40 billion by 2031, registering a CAGR of 12.95% from 2026 to 2031. The market's growth is driven by a shift among consumers from gasoline-powered equipment to quieter, low-maintenance battery-powered alternatives. Regulatory measures in North America and various urban markets are supporting this transition, as new gasoline-powered options face stricter certification requirements or reduced appeal for residential and public use. Product advancements are also expanding the market, with robotic models evolving beyond boundary-wire installations and higher-voltage platforms offering extended runtimes for larger properties and commercial applications. Replacement demand is further bolstered by public procurement programs, changes in retailer assortments, and the integration of battery tool ecosystems across residential, municipal, and professional users. The market remains competitive, with leading brands aiming to secure customer loyalty through battery systems, dealer networks, and connected features, while emerging robotic specialists are rapidly entering regions traditionally dominated by established players.

Key Report Takeaways

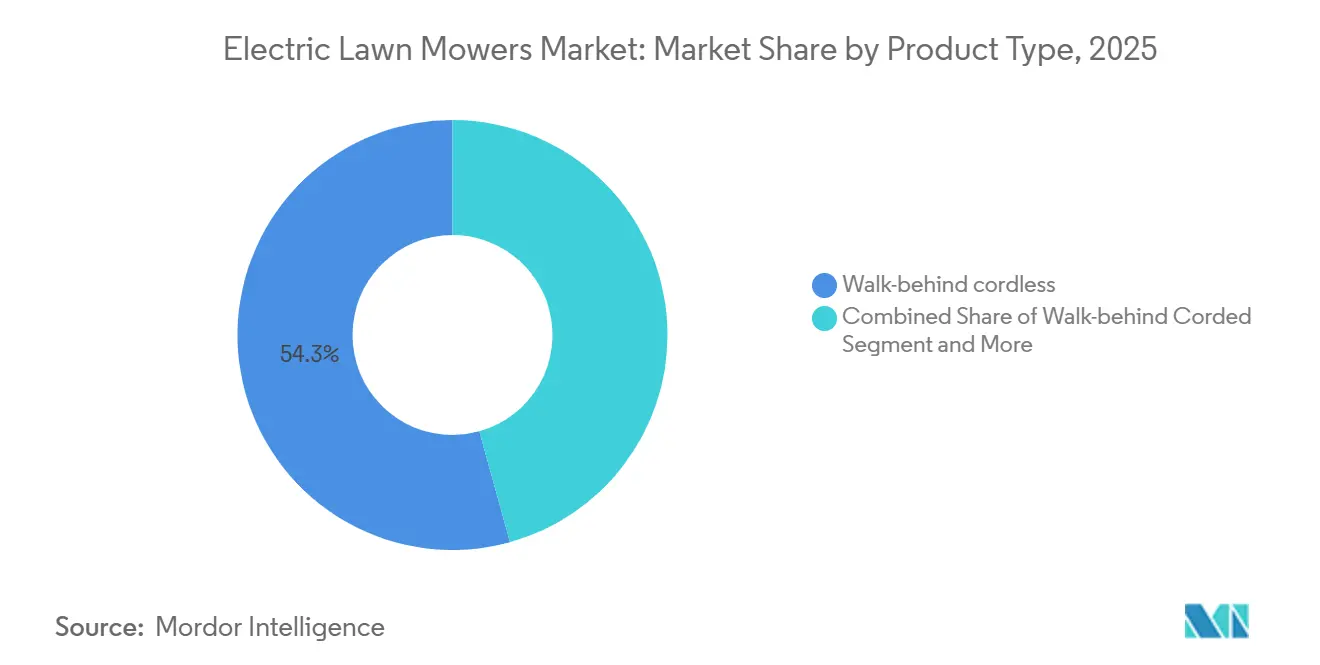

- By product type, walk-behind cordless models captured 54.3% of the electric lawn mowers market share in 2025, while robotic and autonomous mowers are set to grow at a 17.1% CAGR to 2031.

- By end user, residential DIY buyers accounted for 71.2% of revenue in 2025, while municipal and government use is forecast to expand at a 13.3% CAGR through 2031.

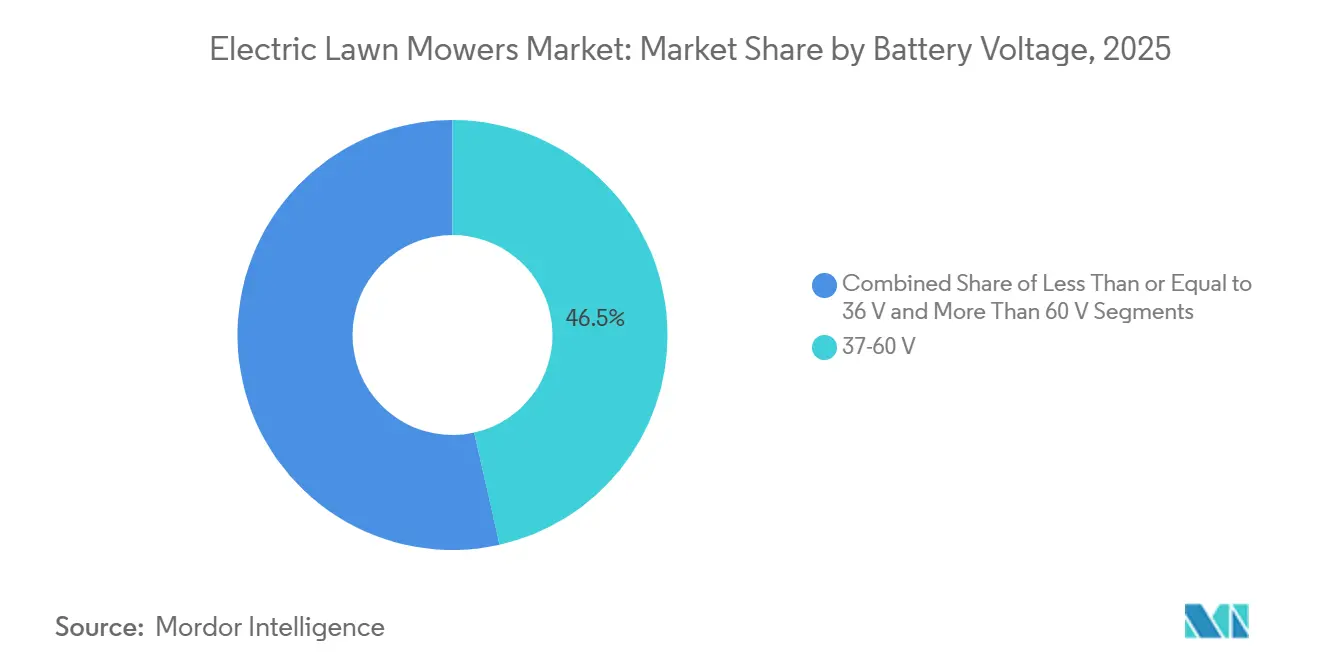

- By battery voltage, 37-to-60-volt platforms accounted for 46.5% of the electric lawn mowers market size in 2025, and systems above 60 volts are projected to post a 15.2% CAGR through 2031.

- By distribution channel, in-store retail accounted for 64.1% of sales in 2025, while online marketplaces were the fastest-growing route, with a 13.9% CAGR from 2026 to 2031.

- By geography, North America accounted for 30.2% market share in 2025, and the Asia-Pacific region is anticipated to record the fastest regional growth at a 16.8% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Lawn Mowers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery cost deflation and higher energy density | +2.8% | Global, strongest unit impact in North America and Europe | Short term (≤ 2 years) |

| Tightening emission and noise rules for small engines | +2.2% | North America, EU urban centers, select Asia-Pacific cities | Short term (≤ 2 years) |

| Lower maintenance and operating costs versus gas mowers | +1.9% | Global, concentrated in professional landscaping-intensive markets | Medium term (2-4 years) |

| AI-enabled robotic mowing reduces labor intensity | +1.4% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Retailer shelf-space shift toward battery outdoor power equipment | +1.1% | North America and Europe, with spillover to Asia-Pacific mass retail | Short term (≤ 2 years) |

| Public-sector zero-emission grounds equipment programs | +0.6% | North America, especially California, Colorado, and Utah, and EU municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Battery Cost Deflation and Higher Energy Density

Battery economics have moved the electric lawn mower market closer to broad replacement demand rather than niche adoption. Buyers are seeing better runtime without the weight penalties that older cordless models often carried. That matters most in the residential segment, where a mower needs to finish a typical suburban lawn on a single charge and remain easy to handle. Higher energy density is also helping brands offer self-propelled, larger-deck walk-behind products without making the machines feel too heavy for household use. A second benefit is an expanded product portfolio, as the same battery platform can now support mowers, trimmers, blowers, and riders with more consistent performance. That makes the purchase decision easier for households that already own cordless tools and want fewer engine-related service needs. It also helps manufacturers spread battery investment across more categories, strengthening pricing discipline and supporting the electric lawn mower market over the next few years.

Tightening Emission and Noise Rules for Small Engines

Regulation is one of the clearest structural supports for the electric lawn mower market. California’s small off-road engine rules, which the United States Environmental Protection Agency authorized in January 2025, make zero-emission equipment the practical route for new product compliance in a major U.S. state. That shift matters beyond California because manufacturers often prefer common product platforms rather than state-specific hardware[1]Source: California Air Resources Board, “Small Off-Road Engines,” arb.ca.gov. Local noise regulations are also shaping demand in dense residential areas, where electric mowing offers a clear operational advantage. Voucher and exchange programs in cities such as Menlo Park are reducing the upfront barrier and speeding the replacement of older gas units. The rule effect is strongest when it combines compliance pressure with consumer convenience, since quieter equipment is easier to use in neighborhoods with tighter time-of-day expectations. This is making the electric lawn mower market less dependent on voluntary green purchasing alone and more tied to lasting policy change.

Lower Maintenance and Operating Costs versus Gas Mowers

Lower maintenance is a practical driver across the electric lawn mower market, especially for users who run their equipment frequently and want fewer service interruptions. Gasoline mowers bring fuel handling, spark plug replacement, oil changes, winterization, and more frequent engine maintenance, while battery systems remove much of that burden. For commercial crews, those differences add up because downtime affects labor scheduling and route efficiency. California’s implementation review showed strong demand for zero-emission landscaping incentives, with more than 27,000 pieces of equipment funded by late 2023 under the CORE Professional Landscaping program using USD 30 million in state appropriations[2]Source: Environmental Protection Agency, “California State Nonroad Engine Pollution Control Standards, Small Off-Road Engines Regulations, Notice of Decision,” federalregister.gov. That pattern suggests users who tested battery equipment found enough operating value to keep buying into the format. Another benefit is easier handling of job-site logistics, since crews no longer need to carry and store gasoline. Insurance exposure, spill risk, and compliance tasks also become simpler, which supports wider fleet conversion in the electric lawn mower market.

AI-Enabled Robotic Mowing Reduces Labor Intensity

Automation is changing the electric lawn mower market from a simple equipment category into a labor-saving solution. Earlier robotic mowers often struggled to reach mainstream buyers because installation required perimeter wires and manual setup, which many users found inconvenient. Newer systems are reducing that friction with vision, LiDAR, and RTK-based navigation, allowing faster deployment and more flexible route planning. Husqvarna revealed AI Vision technology for its 2026 robotic lawnmowers, showing how leading brands are pushing robotic performance deeper into residential and professional applications. Mammotion’s 2026 LUBA 3 AWD also reflects the same shift, combining LiDAR, camera vision, and RTK in a single navigation stack for more precise movement across complex lawns. The value extends beyond replacing a manual mowing session, as robotic systems can reduce the need for skilled operator judgment in spaces with varied layouts. That creates a larger opening for commercial and institutional automation, lifting the long-term ceiling for the electric lawn mower market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher upfront purchase price | -2.0% | Emerging markets and price-sensitive residential segments globally | Short term (≤ 2 years) |

| Runtime and recharge constraints on larger properties | -1.5% | Rural North America, Australia, and Europe | Medium term (2-4 years) |

| Tariffs on imported batteries and battery components | -1.3% | North America, especially United States imports linked to China-origin batteries | Short term (≤ 2 years) |

| Battery-platform fragmentation across brands and voltages | -0.9% | Global including most acute in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Purchase Price

Upfront pricing remains one of the clearest barriers in the electric lawn mower market, especially outside premium residential and regulated commercial niches. The gap is modest in smaller walk-behind models, but it is still meaningful in larger riding and zero-turn categories, where battery pack size drives cost higher. Commercial battery zero-turn products can still sit well above gasoline alternatives, which makes payback harder to justify for buyers with limited financing flexibility. Incentive programs can narrow the gap in some locations, but those programs are not widely available, and their budgets are uneven across regions. Replacement battery costs also weigh on buyer confidence, as some users view battery replacement as a second capital event rather than routine maintenance. That concern is stronger in emerging markets and in rural areas where service networks are thinner. The result is that many price-sensitive buyers continue to delay switching even if they see long-term savings. This keeps a portion of the electric lawn mower market dependent on policy support, retailer financing, or rising fuel costs to close the value gap.

Tariffs on Imported Batteries and Battery Components

Trade policy is adding cost pressure to the electric lawn mower market at a time when the category is trying to broaden price accessibility. Many outdoor power equipment brands still rely on battery cells, modules, and components sourced from Asian supply chains, particularly China. When tariffs raise landed costs, brands must either absorb margin pressure or pass those costs through to dealers and buyers. That is especially difficult in mid-range segments where pricing comparisons against gasoline products remain tight. The impact is not uniform across all brands, as some companies have broader sourcing options or sufficient scale to manage procurement more effectively than smaller entrants. Still, tariffs can slow the benefits of manufacturing efficiency by dampening the final price reductions that end users expect. This matters more in North America, where policy changes can quickly affect channel pricing and reshape promotional calendars. As a result, trade-related cost inflation acts as a short-term brake on the electric lawn mower market even when product demand fundamentals remain favorable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Walk-Behind Leadership Holds While Robotics Grow Faster

Walk-behind cordless mowers accounted for 54.3% of the electric lawn mowers market share in 2025, giving them the largest share of the electric lawn mower market by product type. Their lead comes from a good fit with common residential lot sizes and broad product availability across mass retail and dealer channels. Major brands such as EGO, Greenworks, RYOBI, and Makita have kept this segment active through frequent model launches and support for their battery ecosystems. That has made walk-behind cordless equipment the most accessible entry point for households, replacing gasoline mowers.

Robotic and autonomous mowers are projected to expand at a 17.1% CAGR through 2031, making them the fastest-growing product format in the electric lawn mower market. Husqvarna’s AI Vision roadmap and broader push into wire-free robotics show how quickly the segment is moving beyond early adopters. Ride-on and zero-turn electric products are also gaining ground as higher-voltage platforms improve runtime for larger lawns and commercial use. Stand-on products such as AriensCo’s Arrow E series are targeting contractor and municipal buyers who want maneuverability around obstacles. Corded walk-behind models still hold a niche in parts of Europe, but their shelf presence is fading as cordless pricing improves. Within the electric lawn mower industry, the deeper shift is that automation is starting to redirect future spending away from repeat walk-behind replacement and toward managed robotic ownership.

By End User: Residential Demand Leads While Institutional Use Gains Pace

Residential do-it-yourself users accounted for 71.2% of the electric lawn mowers market size, making them the largest end-user segment in the electric lawn mower market. The segment reflects the large number of homeowners who manage lawns directly and increasingly replace aging gas models with battery equipment. Retail visibility and platform familiarity are helping that transition, especially for buyers who already own battery-powered outdoor tools. The channel effect is important because many residential purchases still begin in home centers, where demonstration and comparison matter.

Municipal and government users are forecast to grow at a 13.3% CAGR through 2031, making them the fastest-growing end-user group in the electric lawn mower market. Public fleet conversion is being pushed by procurement rules, emissions goals, and pressure to reduce noise around schools, hospitals, and public venues. Golf courses and sports facilities are also becoming more receptive as electric turf equipment improves, with John Deere’s 2775 E-Cut Electric Triplex Mower offering more than 22 greens per charge in the United States and Canada from August 2025. Professional landscaping remains a major commercial buyer group, though mid-day charging and crew battery management still matter in intensive-use settings. Larimer County’s grant-backed equipment transition shows how institutional replacement can move quickly once funding and policy align[3]. Across the electric lawn mower industry, this means demand is no longer driven only by homeowners, since public and managed landscapes are becoming a more dependable growth layer.

By Battery Voltage: Mid-Voltage Platforms Dominate While High Voltage Expands the Ceiling

The 37- to 60-volt mid-duty segment accounted for 46.5% of the electric lawn mowers market in 2025, driven by its balance of cost efficiency, lightweight design, and runtime performance for both residential and light commercial applications. At the same time, systems above 60 volts are projected to grow at a CAGR of 15.2% through 2031, supported by advancements in high-capacity battery packs that provide extended operating times and performance levels increasingly comparable to gasoline-powered equipment. As demand for longer runtimes and higher efficiency rises, lower-voltage products, particularly 36-volt systems, are gradually losing market traction.

Battery-platform compatibility has strengthened the position of 40-volt systems in residential applications, while 80-volt platforms continue to dominate commercial usage. However, market fragmentation persists as manufacturers maintain proprietary ecosystems to retain customer loyalty. Although industry organizations are encouraging greater interoperability and standardization, consolidation may progress gradually due to established brand ecosystems. Nevertheless, ongoing technological advancements in battery performance and system integration are anticipated to accelerate adoption across both mid- and high-voltage categories, further enhancing the competitiveness of electric lawn mowers compared to traditional gasoline-powered alternatives.

By Distribution Channel: Physical Retail Leads While Online Channels Gain Speed

In-store retail accounted for 64.1% of 2025 revenue, giving it the largest channel position in the electric lawn mower market. Home centers, mass retailers, and specialty dealers still matter because many buyers want to compare weight, deck size, battery fit, and handling in person before spending on a mower. That behavior is strongest in residential cordless products, but it also matters in premium robotic and commercial equipment, where service expectations influence the choice. The Home Depot’s stated goal to shift more than 85% of outdoor lawn equipment sales to battery-powered products by 2028 shows how physical retail is supporting category conversion.

Online marketplaces are projected to grow at a 13.9% CAGR through 2031, making them the fastest-growing route to market in the electric lawn mower market. The channel is gaining traction because direct-to-consumer robotic brands often rely on digital sales, app-led onboarding, and connected-feature subscriptions. Brand websites are also becoming more important as manufacturers bundle battery warranties, firmware support, and service plans that are easier to explain in owned digital channels. Chervon’s first EGO flagship store in Germany also showed how the line between direct brand control and physical retail is becoming less rigid. Specialty dealers keep a strong role in robotic installation, calibration, and commercial support. The result is a channel mix where stores still lead current revenue, but online pathways are gaining importance as the electric lawn mower market becomes more software-linked and platform-based.

Geography Analysis

North America accounted for 30.2% of 2025 revenue, making it the largest regional market. The United States remains the core driver because regulation, retail breadth, and homeowner adoption are all moving in the same direction. California’s small off-road engine standards are the single most important policy change shaping regional product mix, since the U.S. Environmental Protection Agency authorized the state’s request in January 2025. Local voucher programs are widening the impact beyond California, including Salt Lake City’s FY2024-25 exchange support for landscaping equipment. Canada is also becoming an active market for early commercial and homeowner conversion, supported by Honda’s July 2025 launch of its battery walk-behind lineup in the country.

Asia-Pacific is forecast to grow at a 16.8% CAGR through 2031, making it the fastest-expanding region in the electric lawn mower market. China’s battery manufacturing scale supports price competitiveness across cordless equipment, which helps both domestic sales and export positioning. Japan’s high urban density and stricter noise regulations also support robotic and low-noise electric formats, especially in residential areas where operational convenience matters. South Korea and Australia add to regional momentum through sustainability-led procurement and professional landscaping demand. India and the rest of Asia-Pacific are still early adopters, but commercial horticulture and premium residential projects are creating a foundation for broader growth. In regional terms, the Asia-Pacific is growing, even though North America still leads the electric lawn mower market share at present.

Europe remained the second-largest regional market in 2025, supported by strong robotic mower penetration and tighter noise regulations. Germany stands out as the largest country market in the region and a major base for manufacturing and product development. The region’s mature acceptance of robotic mowing gives it a different demand mix from North America, with automation already normalized in several countries. The Middle East is still small, but large-lot residential development and green-city projects are creating early commercial demand. Africa remains constrained by infrastructure and purchasing power, though resorts and sports venues offer limited premium opportunities. South America is a mid-term opportunity, but currency volatility and supply chain constraints for batteries continue to slow near-term expansion of the electric lawn mower market.

Regulatory Landscape

Emissions and noise requirements continue to shift demand away from gasoline small off-road engines toward corded and battery electric mowers. In the United States, U.S. EPA small nonroad spark-ignition engine requirements under 40 CFR Part 1054 apply to internal-combustion engines (generally below 19 kW) rather than electric mowers, while California Air Resources Board (CARB) requirements for small off-road engines point buyers toward zero-emission equipment, consistent with the state-level pathway culminating in a 2028 ban on sales of new gasoline-powered lawn mowers referenced in the report context.

For product safety and conformity, the U.S. Consumer Product Safety Commission (CPSC) safety standard for walk-behind power lawn mowers (16 CFR Part 1205) underpins certification and labeling practices across major brands and private-label lines. Internationally, IEC 62841-4-3:2025 consolidates safety requirements for pedestrian-controlled walk-behind lawn mowers (with scope exclusions such as robotic and ride-on), supporting harmonization of electrical safety and guarding expectations across markets. In Europe, Regulation (EU) 2025/14 (adopted December 2024) expands technical and administrative requirements for non-road mobile machinery intended for public road circulation, explicitly covering electric and hybrid machinery and adding compliance considerations for manufacturers supplying municipal and contractor fleets that transport equipment between sites.

Competitive Landscape

The electric lawn mower market remains moderately consolidated among leading players, while it is significantly fragmented among smaller manufacturers. Major companies, including Husqvarna Group, Deere & Company, The Toro Company, Robert Bosch GmbH, and Techtronic Industries, collectively accounted for a significant share of market revenue in 2025. Their scale advantages in battery platform development, dealer networks, and product innovation continue to strengthen market positioning, while smaller players are finding growth opportunities in specialized and robotic mower segments.

Competition in the market is increasingly shifting beyond traditional hardware performance toward automation, ecosystem integration, and battery-platform compatibility. Husqvarna accelerated its robotic mower expansion through wire-free technologies and AI-enabled product launches, while Deere expanded into removable-battery zero-turn equipment with its Z370RS Electric ZTrak platform. Similarly, Honda introduced advanced battery-powered and autonomous riding mower solutions, highlighting the industry’s growing emphasis on connected ecosystems, automation capabilities, and commercial uptime efficiency.

At the same time, emerging companies such as Mammotion and Segway Navimow are intensifying competition through wire-free robotic solutions designed to simplify installation and improve user convenience. Manufacturers are also focusing heavily on battery safety, product reliability, and intelligent design as key differentiators, particularly as core battery performance becomes increasingly standardized across the industry. As a result, the competitive landscape of the electric lawn mower market is evolving toward ecosystem strength, robotic intelligence, service support, and consumer trust rather than price competition alone.

Electric Lawn Mowers Industry Leaders

Deere & Company

Husqvarna Group

The Toro Company

Techtronic Industries Co. Ltd.

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial and municipal fleet conversion is creating near-term opportunities in higher-voltage platforms, charging logistics, and fleet software, as runtime and downtime constraints continue to shape purchasing decisions for crews on continuous routes. Recent product and platform moves indicate room for progress in faster charging and higher cycle-life batteries: in May 2026, STIHL introduced the ALLPRO battery system with a 3000-cycle service life and mobile fast-charging capability (80% charge in nine minutes under stated conditions), directly addressing professional uptime needs. Solutions that bundle batteries, chargers, and energy management also support battery-as-a-service models, which retailers and OEMs have been testing, particularly where lifecycle-cost procurement rules influence buying choices.

Battery platform standardization and cross-brand compatibility are also emerging levers for expanding adoption in professional channels that run mixed equipment fleets. In July 2026, Karcher and STIHL announced a battery alliance around the STIHL ALLPRO system for professional equipment, pointing to demand for shared infrastructure across contractor and facilities segments. At the equipment level, manufacturers are adding modular battery configurations to sustain longer duty cycles: STIGA launched the ePark Pro front mower in March 2026 using its 56V ePower Pro system, with configurations up to six batteries for extended runtime. Together, these developments support opportunities for OEMs and channel partners to differentiate through ecosystem breadth (multi-tool battery platforms), mobile charging and storage, and robotic autonomy packages that reduce labor inputs in golf courses, sports facilities, and municipal applications described in the report context.

Recent Industry Developments

- March 2026: STIGA Group launched the ePark Pro electric front mower using its modular 56V ePower Pro battery system, supporting configurations of up to six batteries for longer operating time. The move expands electrification beyond walk-behind categories into professional-grade front mowers, where runtime and duty-cycle requirements are higher. It also reinforces the role of battery modularity as a competitive lever for contractors and facilities buyers.

- October 2025: Husqvarna Group launched seven robotic lawnmowers featuring AI Vision and night-time IR cameras, including professional-oriented models such as the Automower 540 EPOS. This release accelerated the shift to wire-free, sensor-rich robotic platforms that reduce installation friction and expand use in larger commercial and institutional sites. It also places greater emphasis on the software and perception stack as differentiation versus conventional cordless walk-behind products.

- October 2024: Honda Power Sports and Products introduced battery-powered versions of its HRX, HRN, and HRC walk-behind mowers and unveiled a new battery-powered ZTR model for the North American market at Equip Exposition 2024. The portfolio update signaled a clearer transition from gasoline lineups toward battery platforms in core mower categories. It also increased competitive pressure in big-box and dealer channels as more established engine brands bring electric alternatives into their mainstream ranges.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers sales value of new electric lawn mowers used to cut and maintain turf, where the cutting system is powered by corded electricity or a rechargeable battery. It includes walk-behind units, ride-on units, and robotic mowers sold for residential and commercial use.

Scope exclusions: The sizing excludes gasoline and propane models, manual reel mowers, retrofit electrification kits or conversion parts, and any aftermarket parts, servicing, or repair revenue.

Segmentation Overview

- By Product Type

- Walk-behind - Corded

- Walk-behind - Cordless

- Ride-on - Lawn Tractor

- Ride-on - Zero-Turn

- Stand-on

- Robotic/Autonomous

- By End User

- Residential DIY

- Professional Landscaping Services

- Golf Courses and Sports Facilities

- Municipal and Government

- By Battery Voltage

- Less than or equal to 36 V(Light-Duty)

- 37-60 V(Mid-Duty)

- More than 60 V (Commercial-Grade)

- By Distribution Channel

- In-store Retail

- Specialty

- Online Marketplaces

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to anchor it to observable signals that track outdoor power equipment demand. We reviewed public sources such as the US International Trade Commission trade statistics, UN Comtrade, Eurostat, and relevant national statistical offices to understand equipment trade flows, consumer spending direction, and seasonal purchase patterns.

We also referenced sources such as US EPA and European Commission policy pages to track tightening rules on emissions and noise that indirectly support battery adoption, along with patent databases to monitor activity around batteries, charging, and autonomous mowing. Company filings, investor presentations, and reputable press were used to confirm product launches, channel focus, and regional exposure. Paid subscriptions for company financials, news, and shipment-level trade were used selectively to validate data points where public series were not granular enough. These examples are illustrative only, and many other public documents and datasets were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with a mix of manufacturers, component and battery ecosystem participants, distributors and retailers, and commercial landscaping buyers, so key demand and channel views could be cross-checked. For a global market like this, inputs were validated across APAC, EMEA, and the Americas, and the conversations emphasized confirming price moves, cordless versus corded shifts, and the pace of robotic adoption in purchase decisions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 46% |

| Mid tier: 55% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 14% | Managers: 48% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where outdoor power equipment demand is reconstructed using consumption signals, trade flows, and adoption splits between corded, cordless, and robotic electric formats, and then converted into value using reasonable pricing bands. Once that total is formed, it is corroborated with selective bottom-up approximations, such as sampled model pricing by region, channel checks, and supplier and distributor feedback on unit movement, which are then used to fine-tune the totals.

Key inputs used in the model include battery pack cost trends and typical replacement cycles, average selling price movement by product format (corded, cordless, and robotic), seasonal selling patterns, residential versus commercial purchase mix, and the pace of policy-driven switching away from internal combustion equipment in certain metros. Where unit-level information is not consistently available for a country, gaps are handled using proxy indicators like import intensity, comparable lawn and garden spending, and peer-market penetration levels, before results are reviewed against interview feedback.

For forecasting, scenario analysis is used to reflect different adoption speeds for cordless and robotic mowers. The scenarios are anchored to expert consensus on battery pricing, feature-driven upgrades, and the rate at which commercial users electrify their fleets. Growth rates are not pushed mechanically, and the final trajectory is adjusted so it remains consistent with the underlying demand pool and the pricing logic used in the base year.

Data Validation & Update Cycle

Outputs are checked through multiple steps so results are not driven by one data series or one assumption. We compare totals against independent signals like trade direction, publicly visible product pricing, and the implied unit volumes that the model suggests, and then large variances are reworked until they can be explained clearly.

Before sign-off, anomalies are reviewed by another analyst, and follow-up outreach is triggered when a key assumption changes, such as battery cost moves, new regulations, or a major shift in robotic mower availability. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so the numbers reflect the latest validated view.

Mordor Intelligence's Electric Lawn Mowers Market Size Versus Other Published Estimates

Published market numbers for electric lawn mowers can differ by a wide margin because the market can be framed in several reasonable ways, and each choice changes the final total. The biggest differences usually come from what product formats are counted, which year is used as the starting point, and whether the estimate treats equipment value as separate from service and parts.

In this study, the spread is mainly explained by whether robotic mowers are included, how corded units are treated in the demand pool, and how pricing is trended as lithium-ion costs change over time. Another common gap comes from the forecast window itself, because a longer horizon can amplify adoption assumptions if they are not checked against trade, pricing, and channel signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.55 B (2025) | |

| Global Consultancy A | USD 9.10 B (2022) | Uses an earlier base year and a broader revenue interpretation, which can lift totals when historical ranges and category mapping are not aligned to current electric-only mower definitions. |

| Industry Publisher B | USD 5.29 B (2025) | Applies a different product-coverage cut, and the split between robotic, ride-on, and walk-behind formats is treated differently, which shifts the total even when the same year is referenced. |

The table shows that year selection and scope choices create most of the variance, especially around robotic inclusion and how equipment-only revenue is separated from adjacent categories. By keeping the count limited to new electric mower equipment sales (including robotic) and cross-checking implied units against price bands and trade signals, the estimate stays traceable to practical inputs, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is driving demand for electric lawn mowers worldwide?

Demand is being supported by regulation against small gasoline engines, stronger battery performance, lower maintenance needs, retailer support for battery tools, and rising public-sector purchases. The category is projected to grow from USD 5.55 billion in 2025 to USD 11.40 billion by 2031 at a 12.95% CAGR.

Which product category leads sales today?

Walk-behind cordless mowers led revenue with a 54.3% share in 2025 because they fit the largest residential use case and are widely available across retail channels.

Which product category is growing the fastest?

Robotic and autonomous mowers are forecast to grow the fastest at a 17.1% CAGR through 2031 as wire-free navigation and AI vision reduce installation barriers.

Which region is currently the largest?

North America held the largest regional share at 30.2% in 2025, supported by strong retail availability and policy actions such as California’s zero-emission standards for small off-road engines.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow the fastest at a 16.8% CAGR through 2031, supported by China’s battery manufacturing base and rising demand for quieter and more automated solutions in markets such as Japan.

How concentrated is competition among manufacturers?

The top 5 companies held majority share of revenue in 2025, which indicates meaningful scale at the top but still leaves substantial room for smaller players and robotic specialists to expand.

Page last updated on: