Robotic Lawn Mower Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

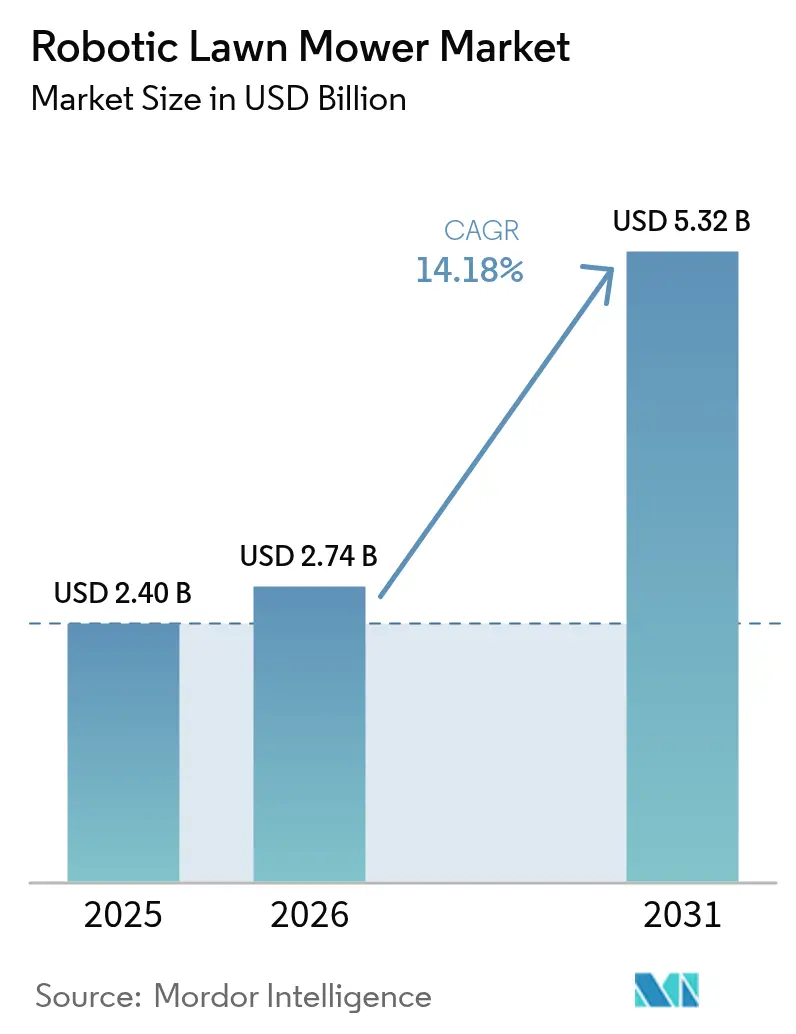

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 5.32 Billion |

| Growth Rate (2026 - 2031) | 14.18% CAGR |

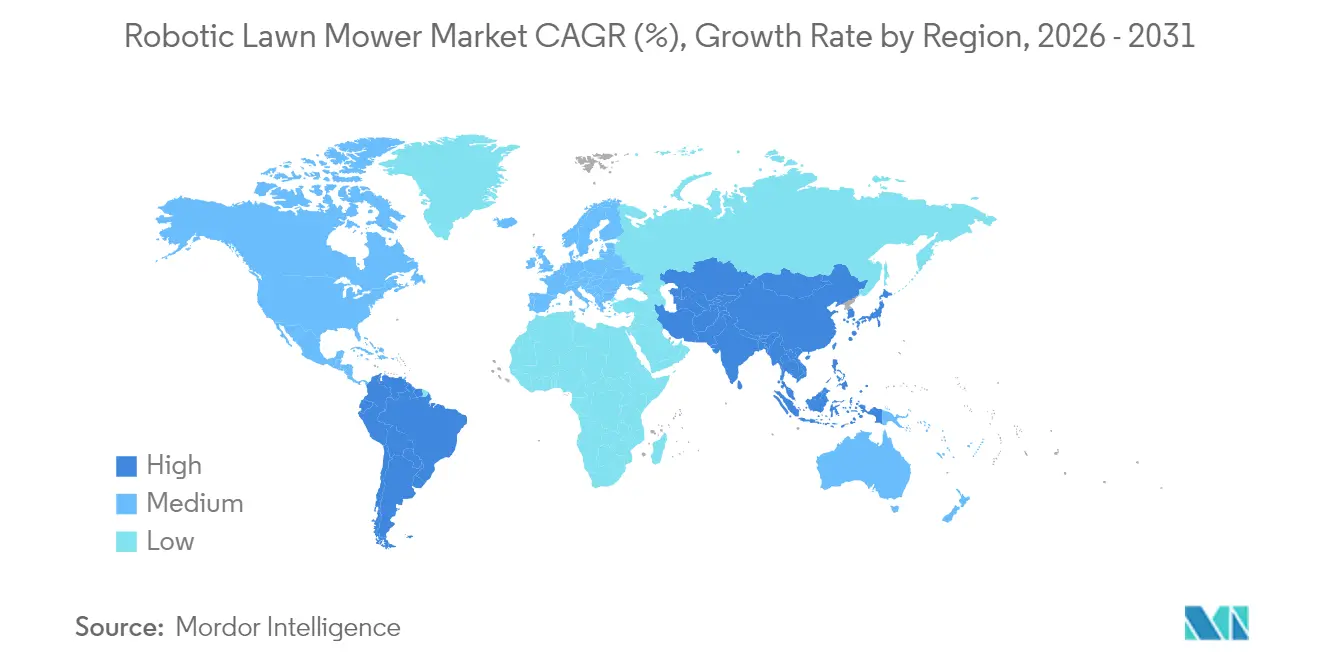

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Lawn Mower Market Analysis by Mordor Intelligence

The robotic lawn mower market size is expected to grow from USD 2.4 billion in 2025 to USD 2.74 billion in 2026 and is forecast to reach USD 5.32 billion by 2031 at 14.18% CAGR over 2026-2031. The increasing adoption of battery-powered autonomous mowing systems drives this growth. The market expansion is supported by labor shortages in the landscaping industry, enhanced environmental regulations, improvements in charging technology, and advanced vision-based navigation systems that eliminate the need for boundary wires. Manufacturers are strengthening their revenue streams through subscription services and remote software updates for existing equipment. The market benefits from retailers' focus on smart-home devices with higher profit margins, while homeowners increasingly opt for automated mowing services. The commercial segment, particularly sports field managers and facility maintenance contractors, is increasing investments in robotic mowers to address workforce shortages and maintain consistent mowing quality across extensive areas.

Key Report Takeaways

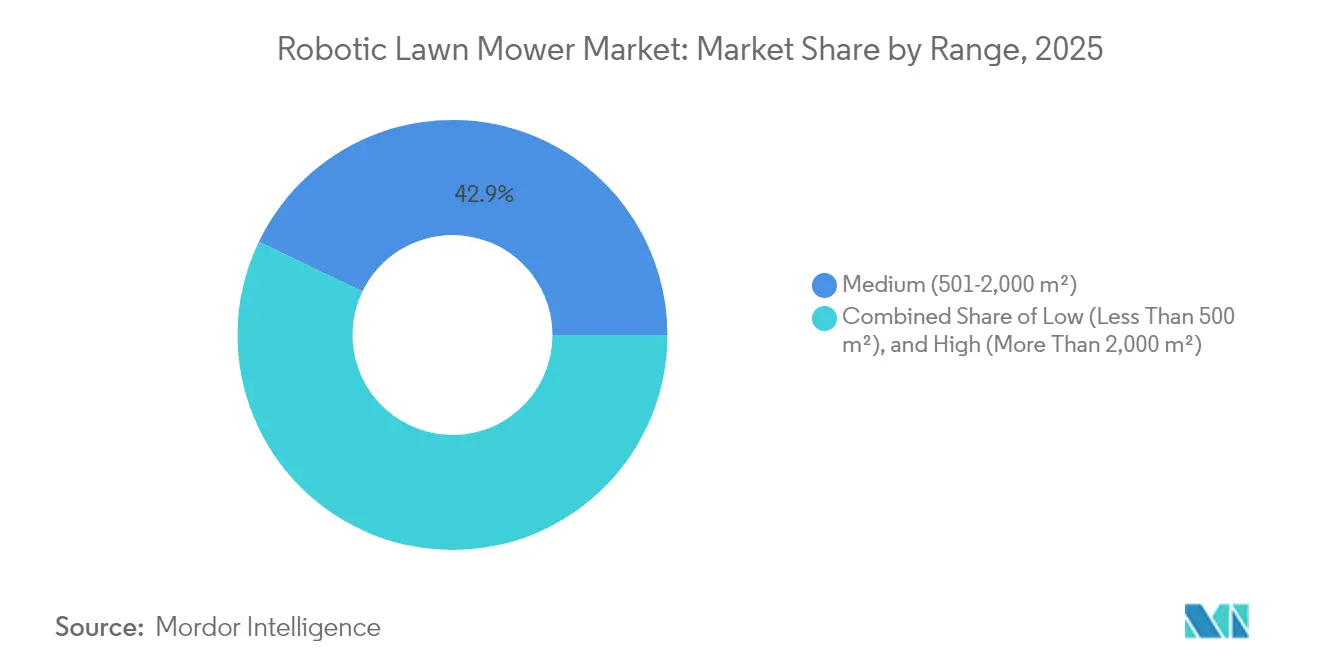

- By range, the medium 501–2,000 m² class accounted for 42.85% of the robotic lawn mower market size in 2025, while the high-range segment is projected to grow at 17.1% CAGR through 2031.

- By navigation technology, boundary-wire units held 64.75% of the market share in 2025, yet vision/camera-based systems are advancing at a 18.9% CAGR to 2031.

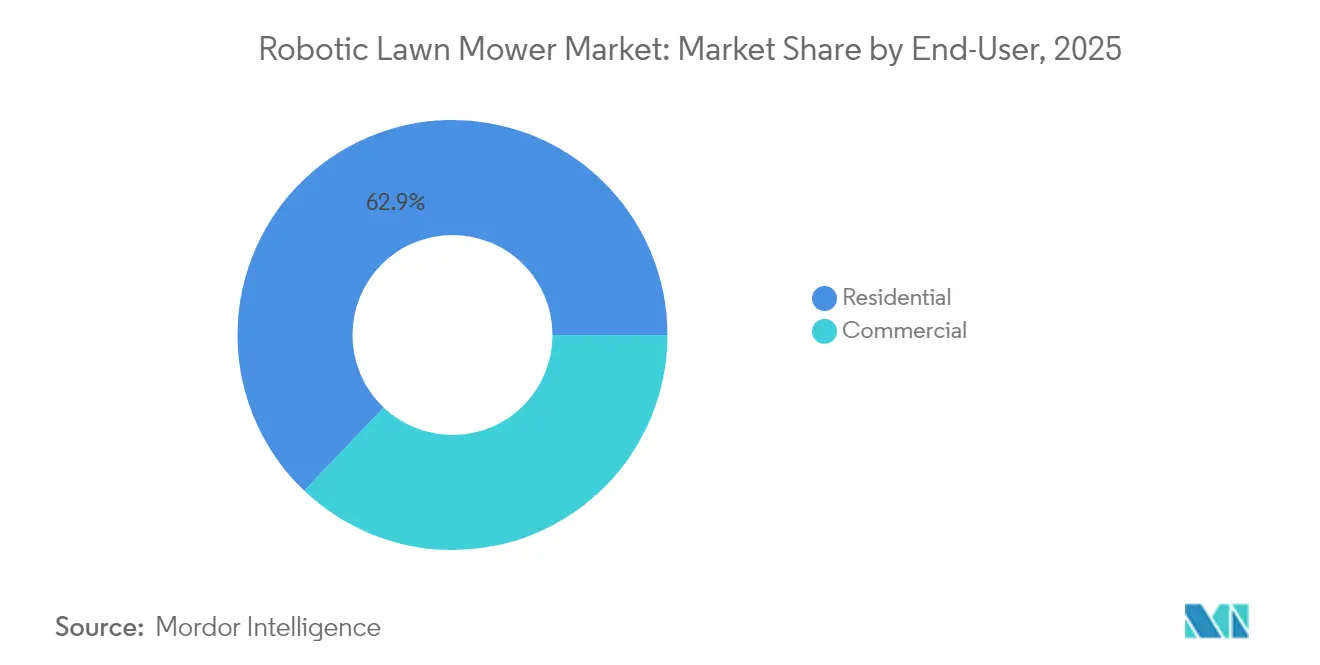

- By end-user, residential customers provided 62.90% revenue in 2025, and the commercial installations are set to expand at a 16.6% CAGR through 2031.

- By distribution channel, offline DIY stores and specialty dealers captured 70.40% sales in 2025, and the online channels are climbing at a 17.0% CAGR to 2031.

- By geography, Europe led with a 44.80% share in 2025, and Asia-Pacific is forecast to post a 13.2% CAGR to 2031.

- The market maintains a moderate consolidated structure, as the top five companies - Husqvarna AB, ANDREAS STIHL AG & Co. KG, Robert Bosch GmbH, Honda Motor Co., Ltd., and Deere & Company- account for 75.20% of the market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotic Lawn Mower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential lawn-care outsourcing | +2.6% | North America and Europe, spreading globally | Medium term (2 – 4 years) |

| Shift toward battery-electric outdoor equipment | +3.0% | Europe and North America leadership, global adoption | Long term (≥ 4 years) |

| Labor shortages in landscaping services | +2.0% | North America and Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Retailer push for high-margin smart-home SKUs | +1.7% | North America and Europe, expanding Asia-Pacific | Medium term (2 – 4 years) |

| Advent of vision-based, perimeter-free navigation | +2.5% | Developed markets worldwide | Medium term (2 – 4 years) |

| Original equipment manufacturer subscription models for autonomous mowing | +1.6% | North America and Europe pilots, Asia-Pacific rollouts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Lawn-Care Outsourcing

The residential lawn care market shows increasing preference for professional services over self-maintenance, driven by dual-income households prioritizing leisure time and an aging population less inclined toward physical labor. Landscape companies address persistent labor shortages by implementing robotic mowing fleets to maintain service schedules without increasing workforce. This automation enables crews to focus on higher-margin services such as landscape design and hardscaping. The robotic mowers operate nightly, increasing the number of properties serviced per route while ensuring uniform cutting heights independent of labor constraints. The frequent, precise mowing patterns improve lawn health and reduce fertilizer requirements, enhancing the return on investment for service providers. This trend of outsourced lawn maintenance accelerates adoption across North American suburbs and Western European markets, where single-family homes predominate and household income levels support professional service fees.

Shift Toward Battery-Electric Outdoor Equipment

Government restrictions on gasoline-powered handheld equipment in California and the European Union accelerate the transition to battery-powered products, establishing electric propulsion as a standard rather than an optional upgrade. STIHL reported that battery-powered units comprised 24% of its 2023 sales and aims to reach 35% by 2027, demonstrating the industry's shift toward electrification. The reduced noise and vibration of robotic units enable overnight operation, maximizing daily mowing cycles without disrupting residents while leaving daylight hours available for watering or recreational activities[1]Source: UL Solutions, “Robotic Lawn Mower Safety Testing and Certification,” ul.com. Improvements in battery energy density now enable mid-range robots to operate for over 150 minutes per charge, while rapid charging capabilities reduce downtime to less than 20% of the operational cycle. Government incentives, such as Germany's EUR 200 (USD 215) rebate on zero-emission garden equipment, reduce the investment recovery period and maintain steady demand during economic fluctuations.

Labor Shortages in Landscaping Services

Labor shortages in the landscaping industry, driven by seasonal visa restrictions and competition from other sectors, are pushing operators to invest in automation equipment. Commercial robotic mowers, with a capacity of 50,000 m², can replace three conventional ride-on mowers, reducing annual labor costs across sports facilities. Automated mowing systems maintain consistent turf maintenance schedules during peak seasons, eliminating the need for costly emergency contractors. The Asia-Pacific region, particularly in urban areas of Japan and Australia, faces comparable labor cost pressures, indicating continued global demand for automated solutions.

Retailer Push for High-Margin Smart-Home SKUs

Major retail chains prioritize shelf space for connected outdoor equipment due to higher gross margins compared to traditional gas-powered walk-behind mowers. Store employees receive incentives for selling smart device bundles, including irrigation controllers and security lighting, which increase average transaction value. E-commerce platforms expand market reach through customer reviews and installation guides, reducing barriers for new buyers and increasing online sales. Data shows that coordinated marketing with smart home devices increases unit sales by 8 weeks post-campaign, demonstrating the effectiveness of connected device messaging. These retail strategies expand the robotic lawn mower market by attracting technology-oriented homeowners who previously used manual mowers due to price sensitivity or perceived complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus conventional mowers | -2.4% | Global, acute in price-sensitive regions | Short term (≤ 2 years) |

| Limited performance on uneven and tall-grass terrains | -1.8% | Regions with complex topography | Medium term (2 – 4 years) |

| Cyber-security and data-privacy concerns | -1.3% | Markets with strict data laws | Long term (≥ 4 years) |

| Fire-risk recalls of Li-ion garden equipment | -1.1% | North America and Europe focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost versus Conventional Mowers

The cost of robotic lawn mowers ranges from USD 800 to USD 5,000, significantly higher than gas-powered push mowers priced between USD 300 and USD 800. Professional installation costs of USD 500 create barriers for first-time buyers, particularly in emerging economies[2]Source: Yarbo, “How Much Should I Pay for a Good Lawn Mower in 2025?” yarbo.com. In developed markets, homeowners compare the three to five-year payback period against shorter financing terms available for riding tractors. While retail financing and subscription models reduce initial costs, these options are primarily available for premium brands, limiting sales volume in entry-level segments. In South America, currency depreciation increases dollar-denominated import prices, causing consumers to opt for used gas-powered units. Although battery cost reductions and local assembly may eventually reduce the price difference, current market growth remains constrained by affordability challenges.

Fire-Risk Recalls of Li-ion Garden Equipment

The recall of 217,500 RYOBI cordless mowers in February 2025, caused by connector-related fires, increased concerns about charging batteries in garages and sheds[3]Source: U.S. Consumer Product Safety Commission, “TTI Outdoor Power Equipment Recalls RYOBI Mowers,” cpsc.gov. Insurance companies began evaluating policy surcharges for properties storing large battery packs, which increased the total cost of ownership and reduced market adoption. Regulatory authorities implemented stricter thermal-runaway testing requirements, which extended certification periods for new models and increased demands on engineering teams. While robotic mowers use smaller batteries than walk-behind models, media coverage intensified consumer safety concerns. Despite manufacturers implementing additional safety features like redundant temperature sensors and UL 2595-compliant battery packs, safety concerns continued to impact sales growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: Medium-Sized Properties Drive Market Foundation

Medium units covering 501-2,000 m² accounted for 42.85% of the robotic lawn mower market in 2025. This dominance reflects the typical suburban lot sizes in Europe and North America. These models offer an optimal balance of price, coverage area, and battery life, meeting average residential yard requirements while requiring minimal storage space. The segment's growth continues as manufacturers implement systematic cutting patterns, improving grass cutting uniformity compared to random navigation systems. The segment's stability is evident in reduced return rates, indicating these models meet consumer performance expectations.

High-range models covering areas above 2,000 m² demonstrate the highest growth rate at 17.1% CAGR. This growth stems from increased adoption by golf courses, sports facilities, and educational institutions seeking to reduce labor costs. The implementation of wire-free navigation systems reduces installation costs for large areas, while centralized control systems enable management of multiple units through single-device interfaces. Low-range robots covering under 500 m² maintain market presence in dense urban areas of Japan and the United Kingdom. Declining prices affect profit margins, leading manufacturers to include additional features like patio-edge trimming capabilities. The industry focus has shifted from hardware innovations to software enhancements, such as irrigation-synchronized scheduling systems, to strengthen customer retention.

By Navigation Technology: Vision Systems Reshape Market Dynamics

Boundary-wire guidance maintained a 64.75% market share in robotic lawn mowers in 2025, as installers and homeowners value its consistent performance during rainy conditions and heavy debris seasons. The established wire infrastructure supports replacement sales through brand loyalty, though yard renovation and repair expenses motivate some users to explore alternative technologies.

Vision/camera-based platforms are projected to grow at a 18.9% CAGR through 2031. These systems eliminate trenching requirements and enable quick deployment across multiple locations, particularly benefiting commercial contractors managing multiple properties. Hybrid systems combine RTK-GPS for broad positioning with optical edge detection for precise navigation near flower beds, delivering centimeter-level accuracy for sports facilities. While Global Navigation Satellite System (GNSS) only units perform well in open areas with clear sky views, their effectiveness decreases in suburban environments with dense tree coverage due to signal interference. Manufacturers continue to enhance AI algorithms to improve the detection of common yard obstacles, including trampolines, driveways, and outdoor furniture, indicating increased focus on software development.

By End-User: Commercial Segment Drives Premium Growth

The residential segment accounted for 62.90% of the robotic lawn mower market size in 2025, driven by homeowners seeking efficient and quiet lawn maintenance solutions. Declining prices, mobile application controls, and voice assistant integration have simplified robot mower adoption. The ability to operate at night allows homeowners to use their lawns during daytime hours. Residential developers are incorporating charging pad infrastructure in premium housing developments, positioning robotic mowers as standard home automation features.

The commercial segment is experiencing rapid growth at a CAGR of 16.6%, primarily driven by contractors servicing golf courses and public parks. The automation allows maintenance teams to focus on specialized services such as edging, pruning, and chemical treatment, which generate higher margins. Commercial-grade units demonstrate high utilization rates, resulting in investment recovery periods of less than two years for large properties. The integration with cloud-based management systems provides operational and energy consumption data, supporting environmental, social, and governance (ESG) reporting requirements for corporate and educational institutions.

By Distribution Channel: Online Growth Challenges Traditional Retail

Offline channels, including DIY stores and specialty dealers, account for 70.40% of the robotic lawn mower market share in 2025. These retailers provide showroom demonstrations and installation packages that build confidence among first-time buyers. Dealers also operate service centers essential for battery diagnostics and firmware updates. The channel benefits from volume discounts, enabling prominent display of flagship models during peak lawn season.

Online channels demonstrate a 17.0% CAGR, driven by product comparison tools, unboxing videos, and influencer reviews. E-commerce platforms reduce costs by eliminating dealer margins, enabling emerging Asian brands to offer competitive prices while providing optional remote support services. Manufacturers implement hybrid distribution strategies where customers configure units online and connect with local partners for installation, combining digital accessibility with in-person expertise. The industry may expand to include click-and-collect lockers for battery exchanges, similar to developments in the cordless power tool market.

Geography Analysis

Europe held 44.80% of the robotic lawn mower market share in 2025, driven by established gardening practices, high labor costs, and emissions regulations that support robotic lawn mower adoption. Germany, the United Kingdom, and France maintain extensive dealer networks, while Scandinavian markets show high penetration in detached housing segments. European machinery regulations streamline safety certification processes, facilitating cross-border product launches and enabling consolidated marketing across multiple regions. Manufacturers leverage regional supply chains to avoid U.S.–China tariffs, providing a competitive advantage for North American exports.

Asia-Pacific demonstrates 13.2% growth through 2031, supported by China's RMB 73.755 billion (USD 10.4 billion) service-robot industry in 2024, which provides domestic lithium-ion cells and camera modules at scale. Japan's declining workforce and South Korea's concentrated urban lawns increase demand for compact models operating below 60 dB. Australian municipalities test robots in public spaces to address wage inflation, positioning Oceania as an evaluation ground for commercial fleet operations.

North America shows lower penetration compared to Europe despite extensive lawn areas, while trade dynamics favor European imports over Chinese products, affecting market share distribution. The Inflation Reduction Act's proposed consumer rebate on electric outdoor equipment may increase robotic mower adoption if implemented in 2026. South America, the Middle East, and Africa currently represent single-digit market shares, though increasing middle-class wealth in Mexico and Gulf nations indicates future opportunities for premium models designed for high temperatures and sand exposure.

Mordor Intelligence provides coverage of the robotic lawn mower market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Robotic lawn mowers are governed by electrical safety standards for household appliances, with ANSI/OPEI 60335-2-107-2020 widely used in the United States as a voluntary safety specification and recognized in the Consumer Product Safety Commission (CPSC) standards landscape for mowers.

In Canada, CSA C22.2 No. 60335-2-107:2020 was updated with an effective date of 1 December 2024, adding markings and sensor-related provisions that affect product design and certification timelines. In the European Union, Machinery Regulation (EU) 2023/1230 is adopted and will apply from 20 January 2027, expanding focus to risks linked to digital technologies, robotics, and autonomous functions. That shift increases the importance of cybersecurity-by-design and functional safety considerations for connected, wire-free navigation platforms.

Competitive Landscape

The robotic lawn mower market shows a moderate concentration, with five companies - Husqvarna AB, ANDREAS STIHL AG & Co. KG, Robert Bosch GmbH, Honda Motor Co., Ltd., and Deere & Company - accounting for 76% of market share in 2024. Husqvarna AB maintains market leadership, generating SEK 7.2 billion (USD 1.01 billion) in robotic sales during 2024. The company's position stems from its 30-year industry experience and manufacturing partnership with Flex for improved cost efficiency. Husqvarna AB's planned 2025 release of 13 wire-free models demonstrates its focus on AI navigation technology.

ANDREAS STIHL AG & Co. KG and Robert Bosch GmbH maintain significant market positions by utilizing their battery technology expertise from their handheld tools and automotive electronics divisions. STIHL's strategy includes an 80% battery product mix target by 2035. Robert Bosch GmbH focuses on developing cloud-based garden systems that integrate sensors, irrigation, and robotics. The market sees new competition from Deere & Company, which is developing autonomous zero-turn mowers, bringing its agricultural and construction equipment expertise to the residential sector.

Asian manufacturers, including Segway Inc. (Ninebot Ltd.) and Shenzhen Mammotion Technologies Co., Ltd., compete through competitive pricing and rapid product updates, supported by regional camera supply chains and direct consumer sales channels. The United States tariffs on Chinese machinery restrict unbranded import distribution through retail channels, benefiting European manufacturers. Market differentiation increasingly depends on AI object recognition capabilities, predictive maintenance analytics, and subscription-based service contracts rather than traditional features like cutting width.

Robotic Lawn Mower Industry Leaders

Husqvarna AB

ANDREAS STIHL AG & Co. KG

Robert Bosch GmbH

Honda Motor Co., Ltd.

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wire-free navigation is creating replacement and first-time adoption whitespace by reducing installation complexity and enabling faster deployment for multi-site users. In 2026, the direction toward fusion navigation stacks (AI vision, RTK, and LiDAR) is becoming more visible: Worx presented the Landroid Vision Cloud at CES 2026 with Vision AI and RTK Cloud positioning, and ANTHBOT launched the M9 Pro with HoloSense Quad-Fusion Navigation, combining LiDAR, RTK, and dual AI vision. This technology direction supports attach opportunities for OEMs and channel partners, including paid setup, mapping, remote monitoring, and over-the-air feature upgrades, consistent with the market shifts toward subscription services and remote software updates outlined in the context.

Commercial grounds maintenance and managed services also offer a clearer path to higher-utilization deployments, where fleet management and uptime are central procurement criteria. In the UK, Mitie and Kress announced a partnership to deploy 24 autonomous Kress Voyager mowbots across customer sites, reflecting facilities-management-led buying rather than single-unit consumer adoption. Crossover demand beyond residential lawns is also apparent, with XAG launching the RM80 unmanned electric mower in Guangzhou for orchard management and land reclamation tasks.

Recent Industry Developments

- April 2026: Husqvarna launched the Automower 560 EPOS professional robotic lawn mower. The release reinforces Husqvarna's position in higher-duty commercial applications where perimeter-wire-free operation and precise navigation support multi-site deployments and contractor workflows.

- October 2025: Husqvarna announced its 2026 robotic mower lineup featuring AI Vision technology, including night-time IR cameras and expanded professional offerings such as the Automower 540 EPOS. The announcement pointed to a product roadmap centered on camera-led autonomy and improved obstacle detection, sharpening competitive emphasis on wire-free navigation capabilities.

- February 2025: Mitie and Kress announced a partnership to deploy 24 autonomous Kress Voyager mowbots across customer sites in the United Kingdom. The contract expands institutional adoption of autonomous mowing in facilities management and highlights scale for enterprise deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue generated from robotic lawn mowers sold for grass cutting in residential and commercial lawns, counted at the manufacturer selling price (including standard software and charging accessories shipped with the unit).

Scope exclusions: We exclude manual and ride-on mowers, non-robotic electric mowers, and garden tools that do not perform autonomous mowing.

Segmentation Overview

- By Range

- Low (Less Than 500 m2)

- Medium (501-2,000 m2)

- High (More Than 2,000 m2)

- By Navigation Technology

- Boundary-Wire

- Vision / Camera

- GNSS / RTK-GPS

- By End-User

- Residential

- Commercial

- By Distribution Channel

- Online (Direct, Marketplaces)

- Offline (DIY Stores, Specialty Dealers)

- By Geography

- North America

- United States

- Canada

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Iran

- Oman

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the demand pool using public statistics and category signals that show where mowing equipment adoption is realistic. Useful sources include government trade and production statistics such as UN Comtrade, USITC DataWeb, and Eurostat, along with labor and wage series from sources such as the US Bureau of Labor Statistics to capture landscaping cost pressure.

To keep the model grounded, we also track product and safety context through references to IEC standards, patent databases for navigation and battery innovations, and peer-reviewed papers that discuss outdoor robotics performance limits. Company annual reports, investor presentations, and reputable press coverage are used to understand product launches, pricing bands, and channel shifts. For cross-checking company scale and shipment indicators, we reference paid subscriptions for company financials and intelligence, and import or export shipment level databases when available. The sources listed here are illustrative and many other public and paid references were also used for data collection and clarification.

Primary Interviews and Surveys

Our primary work focused on validating what drives unit shipments and realized prices, since retail pricing can differ from factory level revenue. We spoke with a mix of manufacturers, component ecosystem participants, distributors and dealers, and commercial landscaping users across major regions, then used follow-up checks to close gaps around adoption barriers (boundary wire versus wireless), battery life expectations, and replacement cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 48% |

| Mid tier: 53% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 14% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs demand using mowing-equipment trade flows, installed base signals, and the share of lawns that can practically adopt robotic mowing given yard size and typical landscaping practices. Once that demand pool is shaped, we apply penetration ranges and region-specific price bands to estimate value, then check totals against selective bottom-up approximations like sampled model lineups, dealer feedback on unit volumes, and an ASP times unit sanity check.

A few inputs that mattered in this market were average selling price progression by feature set (wired versus wireless navigation), battery pack cost trends that influence entry price points, labor cost pressure in landscaping, seasonal selling patterns in temperate climates, and the pace of smart home integration that improves perceived ease of use. Where bottom-up details are missing in smaller countries, we use proxy pricing and adoption ranges anchored to similar climate and income profiles, followed by a second validation step.

For forecasting, we rely on scenario analysis supported by a simple multivariate view of drivers such as battery cost direction, new product cycles, and regional landscaping labor constraints. The final forecast is then adjusted using expert feedback on regulatory noise restrictions and the speed at which wireless boundary systems are replacing older wired setups.

Data Validation & Update Cycle

We validate outputs by triangulating across independent signals, then running variance checks at the region level so outliers get flagged early. If implied unit volumes or ASPs drift away from what interviews, trade statistics, and product price bands suggest, the assumptions are revisited and the relevant experts are re-contacted.

Before sign-off, the model goes through multi-step analyst reviews that check math logic, currency conversion timing, and year-on-year continuity. Reports are refreshed annually, and interim updates are made when material events occur, such as major product launches or policy changes affecting outdoor power equipment. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Robotic Lawn Mower Market Size Measured Against Other Published Estimates

Published market values for robotic lawn mowers can differ because analysts do not always use the same demand signals, pricing level, or timing for currency conversion. Differences also come from what is counted as a robotic mower versus adjacent lawn equipment, and how quickly newer wireless navigation models are assumed to scale.

Import and export unit trends, retail model counts by region, and interview-backed ASP bands are the checks that keep Mordor Intelligence's 2025 estimate tied to realistic shipment volumes and factory-level pricing, instead of list prices or mixed outdoor equipment categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.4 B (2025) | |

| Trade Publisher A | USD 1.94 B (2024) | Uses a different base year and appears to lean more on production and consumption splits with broader type definitions, which can undercount premium models and newer wireless segments when revenue is normalized. |

| Industry Research Group B | USD 2.4 B (2025) | The 2025 value is close, but the lower 2031 projection suggests more conservative assumptions on penetration growth and ASP uplift from wireless navigation and feature upgrades over the forecast window. |

The spread mainly comes from scope edges and how pricing is treated, especially whether factory-level revenue is separated cleanly from retail tags and adjacent mower categories. By tying the build to unit signals and repeatable price bands, the resulting number stays transparent and easier to re-check when new model launches or adoption data changes.

Key Questions Answered in the Report

What is the projected CAGR for robotic lawn mowers between 2026 and 2031?

The market is forecast to climb at a 14.18% compound annual growth rate, moving from USD 2.74 billion in 2026 to USD 5.32 billion by 2031.

Which region currently purchases the most robotic lawn mowers?

Europe leads with 44.80% of 2025 global revenue thanks to strong gardening culture, high labor costs, and supportive emissions rules.

Why are commercial landscaping firms turning to robotic mowers?

Robots offset labor shortages and let crews focus on higher-margin tasks, giving professional users a 16.6% CAGR and payback periods near two years.

What safety standards regulate autonomous mowers in 2025?

IEC 60335-2-107 and the EU’s Regulation 2023/1230 mandate blade-stop controls, battery safeguards, and cybersecurity measures for connected outdoor robots.

Page last updated on: