Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The United States Home Organizers and Storage Market Report is Segmented by Product (Storage Baskets, Storage Boxes, Storage Bags, and More), Application (Bedroom Closets, Laundry Rooms, Home Offices, and More), Distribution Channel (Hypermarkets and Supermarkets, Specialty Stores, Online, Other Distribution Channels), and Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

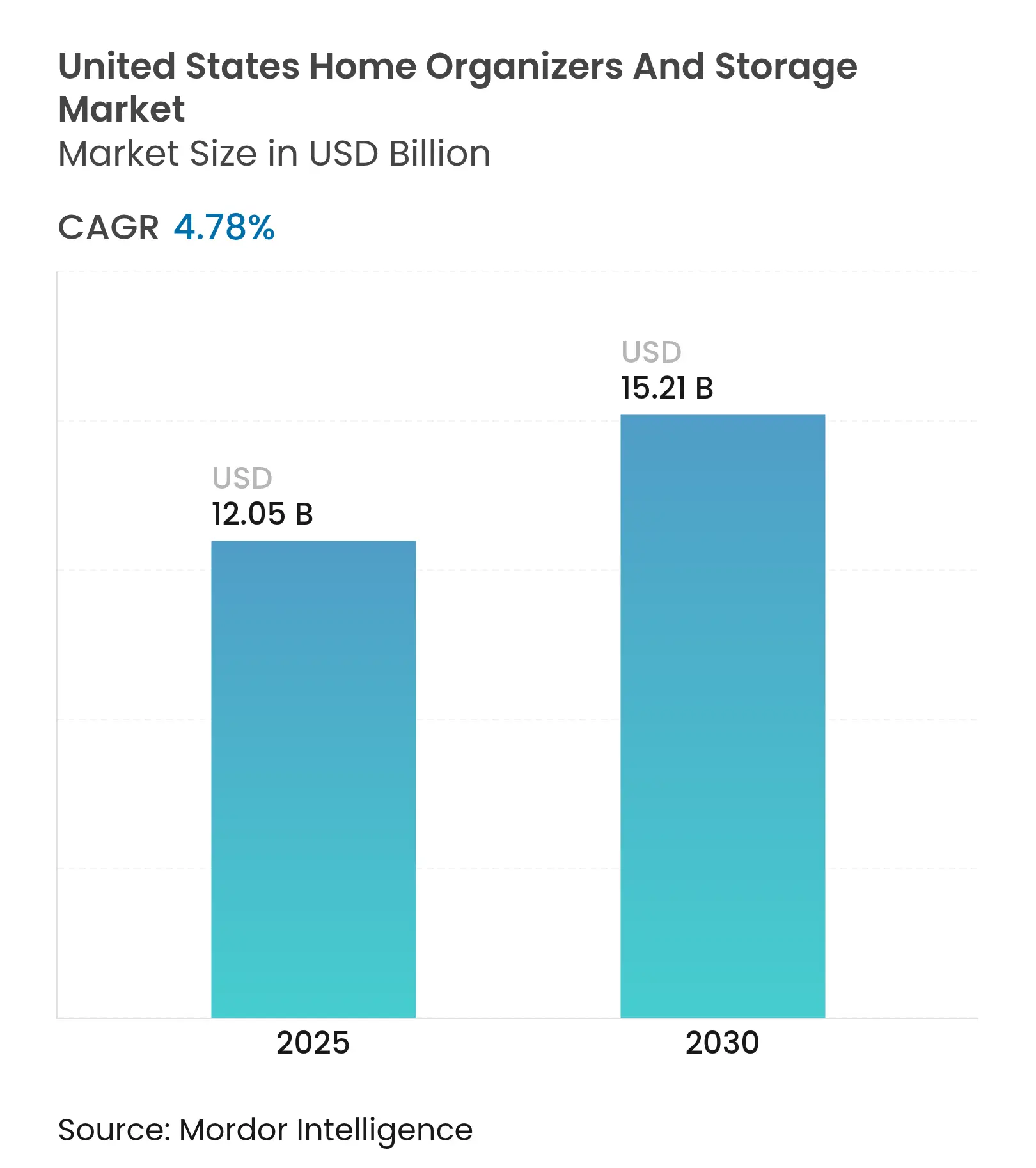

| Market Size (2025) | USD 12.05 Billion |

| Market Size (2030) | USD 15.21 Billion |

| Growth Rate (2025 - 2030) | 4.78 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The United States home organizers and storage market size is valued at USD 12.05 billion in 2025 and is forecast to reach USD 15.21 billion by 2030, expanding at a 4.78% CAGR during the period. Demographic shifts toward smaller households, persistent housing shortages that lengthen owner tenure, and a steady uptick in renovation spending keep demand resilient. Federal incentives under the Inflation Reduction Act funnel tax credits into retrofit projects that routinely bundle closet or pantry upgrades, while e-commerce penetration—now 29% of home-improvement transactions—broadens access to ready-to-assemble storage lines. At the same time, technology platforms offering AI-assisted design enable mass customization once reserved for luxury installations, lowering entry barriers for modular units. Competitive dynamics remain fragmented: big-box retailers still own critical shelf space, yet direct-to-consumer specialists leverage social commerce and influencer content to capture shoppers who equate decluttering with wellness.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

home-renovation expenditure

Rising

home-renovation expenditure

| +1.2% | National; strongest in South & West | Medium term (2–4 years) | (~) % Impact on

CAGR Forecast:

+1.2%

|

Geographic

Relevance

:

National; strongest

in South & West

|

Impact Timeline

:

Medium term (2–4

years)

|

Urbanization &

shrinking living spaces

Urbanization &

shrinking living spaces

| +0.9% | Northeast & West urban cores | Long term (≥ 4 years) | |||

DIY culture &

e-commerce availability

DIY culture &

e-commerce availability

| +0.8% | Nationwide; highest in West | Short term (≤ 2 years) | |||

Hybrid work-driven

home-office storage

Hybrid work-driven

home-office storage

| +0.7% | National; tech hubs concentrated | Medium term (2–4 years) | |||

Federal

energy-efficiency retrofit incentives

Federal

energy-efficiency retrofit incentives

| +0.4% | National; state-level variation | Medium term (2–4 years) | |||

AI-powered design

& mass-customized closets

AI-powered design

& mass-customized closets

| +0.3% | Urban markets; early West Coast uptake | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Home-Renovation Expenditure

Home-improvement outlays totalled USD 485 billion in 2024, reflecting owners who chose upgrades over moves amid elevated mortgage rates[1]Lila Argin, “Home Renovation Facts and Statistics,” Architectural Digest, architecturaldigest.com. Kitchen and bath projects climbed in median spend from USD 15,000 in 2020 to USD 18,000 in 2021, creating halo demand for pull-out pantries, drawer dividers, and laundry organizers. Realtors say 86% of clients feel motivated to renovate another room after a satisfactory first project, giving storage vendors multiple cross-sell points. Return-on-investment math also favours closet retrofits that recoup 83% of cost, a figure frequently promoted by installers to close premium jobs. The linkage between discretionary remodelling and organization systems keeps the United States home organizers and storage market on a predictable upswing, even as macro housing sales fluctuate.

Urbanization & Shrinking Living Spaces

Average new-build apartments in core metros now sit below 800 square feet, with Seattle registering just 661 square feet—the smallest among major U.S. metros. Zoning reforms in Arizona, Colorado, and Florida that legalize duplexes and accessory dwelling units further compress per-capita square footage[2]Abigail Wilford, “States Embrace Diverse Strategies to Ease Housing Supply Constraints,” The Pew Charitable Trusts, pewtrusts.org. As interior footprints shrink, residents turn to vertical shelving, under-bed bins, and multi-purpose organizers that capitalize on overlooked corners. Builders of microunits in Denver spend USD 123,000 per door versus USD 400,000 for a studio, yet still command rents of USD 850—proof that renters will pay for design efficiency when paired with adequate storage. Self-storage operators consequently experience a lift, reinforcing the mindset that optimized organization inside the home is a cost-saving alternative to renting an external unit.

DIY Culture & E-Commerce Availability

DIY project participation reached 55% of homeowners in Q3 2023, up eight points year-over-year, while online sales grabbed 22.3% of home-improvement dollar volume. Video tutorials and ratings drive 43% and 53% of digital decisions, respectively, making content marketing an indispensable lever for storage brands. Amazon’s March 2025 launch of 80 home-organization SKUs illustrates how marketplaces fast-track assortment breadth, particularly for stackable boxes and small-parts organizers that ship parcel-friendly[3]Lauren Taylor, “Amazon Launched 80 Home Essentials in March,” Better Homes & Gardens, bhg.com. Quick-click configuration tools are also lowering buyer hesitation for modular closets, letting consumers visualize layouts and generate parts lists in minutes. Ready-to-assemble formats lessen reliance on skilled installers, a benefit in markets where carpentry labor remains scarce.

Hybrid Work-Driven Home-Office Storage

Forty-three percent of 2025 homebuyers report that job location no longer dictates where they live, cementing hybrid work as a structural change. As spare bedrooms evolve into offices, demand rises for concealed filing, ergonomic shelving, and cable-management solutions that preserve aesthetic minimalism. The Container Store responded with nine “closet system in a box” configurations targeting pantries, flex rooms, and office nooks. Professional organizers rank home-office storage immediately behind kitchen upgrades for return on productivity, often emphasizing adjustable heights and modular add-ons. The result is an incremental revenue stream that grows in parallel with software-sector employment and the spread of full-time remote policies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Raw-material price

volatility

Raw-material price

volatility

| –0.8% | Nationwide; acute in manufacturing belts | Short term (≤ 2 years) | (~) % Impact on

CAGR Forecast:

–0.8%

|

Geographic

Relevance

:

Nationwide; acute in

manufacturing belts

|

Impact Timeline

:

Short term (≤ 2

years)

|

Supply-chain &

labor shortages

Supply-chain &

labor shortages

| –0.6% | National; severe in construction hubs | Medium term (2–4 years) | |||

Big-box shelf-space

saturation

Big-box shelf-space

saturation

| –0.4% | National; most pronounced in mature markets | Medium term (2–4 years) | |||

Digital-minimalist

lifestyle adoption

Digital-minimalist

lifestyle adoption

| –0.3% | Urban centers; millennial-dense areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Raw-Material Price Volatility

Lumber climbed 21% year-over-year to USD 545 per thousand board feet in March 2025 amid tariff clouds and logistical choke points[4]HBS Dealer Staff, “March 2025 Lumber Report: Tariff Confusion and Rising Prices,” hbsdealer.com. Polyurethane foam shortages linked to Gulf hurricanes bumped input costs for upholstered benches and ottomans that double as storage, while cabinet components now face 10% baseline import duties. Manufacturers walk a tightrope between holding inventory to shield against future spikes and over-committing capital. Retailers, in turn, battle consumer pushback when SKUs re-ticket multiple times within a season. The cumulative effect shaves margin headroom and can delay planned product launches inside the United States home organizers and storage market.

Supply-Chain & Labor Shortages

Home Depot shed 3.2 million square feet of warehouse capacity in 2024 as volume normalized, yet installers still report shortages of finish carpenters and plumbers needed for built-ins. Houzz data show 90% of trade professionals expect tariffs to elevate material costs into 2026. Specialty player The Container Store entered Chapter 11 in December 2024, citing disrupted inbound freight and reduced foot traffic. Delivery backlogs push some consumers toward flat-pack alternatives or postpone jobs altogether, moderating near-term sales for premium systems. Skilled-labor scarcity also restrains project throughput, especially in sunbelt metros where housing starts stay elevated.

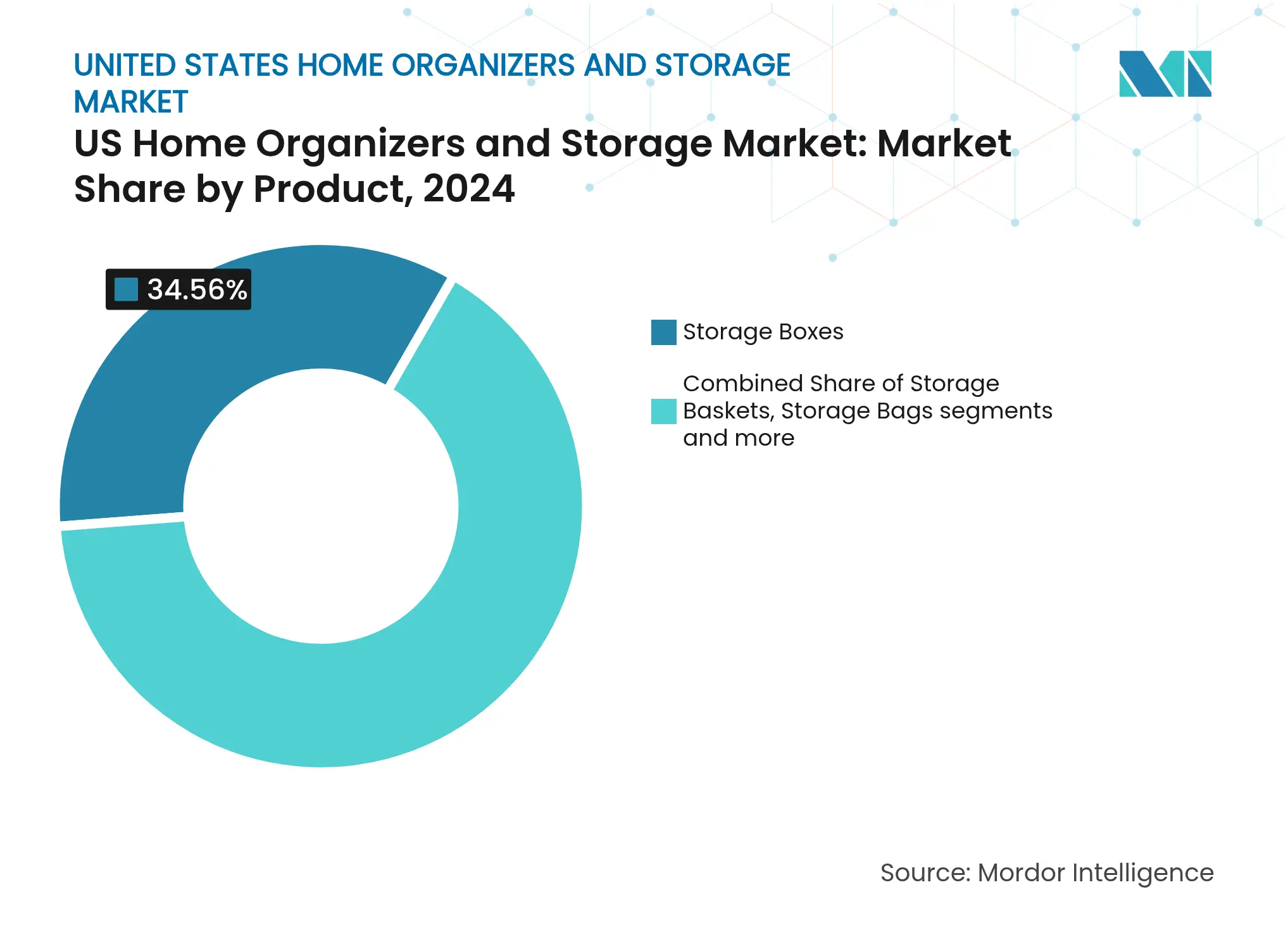

By Product: Modular Innovation Drives Premium Growth

Storage Boxes held 34.56% of the 2024 demand thanks to universal compatibility with closets, garages, and utility rooms. That dominance aligns with consumer preference for quick, low-cost fixes, yet Modular Units are charting a 5.91% CAGR through 2030 as AI-aided design tools ease customization. In value terms, the United States home organizers and storage market size for modular units is projected to rise from USD 2.15 billion in 2025 to USD 2.86 billion by 2030, underscoring how mass personalization converts higher average selling prices into outsized revenue. Storage Baskets retain traction in décor-driven zones such as living rooms, while gasket-sealed Storage Bags cater to seasonal wardrobe rotations. Hanging Storage appeals to renters unable to alter built-ins, and multipurpose organizers fulfil cross-room utility, especially in dorms and microunits. Travel-luggage organizers, a niche sub-segment, benefit from the uptick in work-from-anywhere travel habits, nudging suitcase accessory makers toward expandable cubes and compression technology.

Competitive energy in this segment emerges around patentable hinge systems, recycled material content, and click-fit connectors that simplify weekend installs. Sterilite’s 2025 five-shelf plastic unit combines UV additives with weight ratings that meet garage specs, illustrating how basic polymers can command a premium shelf price when performance is verified. Direct-to-consumer brand Modular Closets surpasses 100,000 closets sold by touting millwork-grade plywood over particleboard, a spec gamers and craft hobbyists scrutinize during online research. As more builders pre-wire closets for lighting and sensors, future-proofing through upgradeable modular panels offers another value lever. The innovation trajectory supports durable demand, ensuring the United States home organizers and storage market continues to tilt toward configurable systems.

Note: Segment shares of all individual segments available upon report purchase

By Application: Home Office Surge Reshapes Demand Patterns

Bedroom Closets captured 39.12% of 2024 sales, a metric reflecting both near-universal household necessity and the routine cadence of wardrobe refreshes. Architectural updates—barn-style doors, shoe sanctuaries, and integrated laundry hampers—push ticket values up without structural remodeling. Home Office storage, however, is growing faster at 6.23% CAGR, driven by households that repurpose spare bedrooms into offices or hybrid guest rooms. The United States home organizers and storage market size for home office solutions reached USD 1.75 billion in 2025 and is on course for USD 2.38 billion by 2030. Laundry-room cabinetry remains a stable, mid-ticket opportunity, especially in suburban builds where mudrooms merge with utility areas. Pantry and kitchen organizers ride meal-prep culture; pull-out spice racks and under-sink caddies migrate from high-end custom into mass retail SKUs. Garage storage—a realm of slatwalls, overhead racks, and climate-controlled cabinets—has grown into a lifestyle category tied to home gyms and maker spaces.

Across applications, retailers highlight quick-ROI talking points: a dedicated garage solution can add USD 6,000 to resale value, while a well-designed pantry cuts weekly grocery waste by 15% according to installer case studies. Specialty channels also note demographic nuance: Gen X homeowners gravitate toward walk-through laundry stations, while millennials want “invisible” desk set-ups that fold away after work hours. Overall, the diversification of storage touchpoints across the dwelling supports multi-category wallets, reinforcing revenue stickiness within the United States home organizers and storage market.

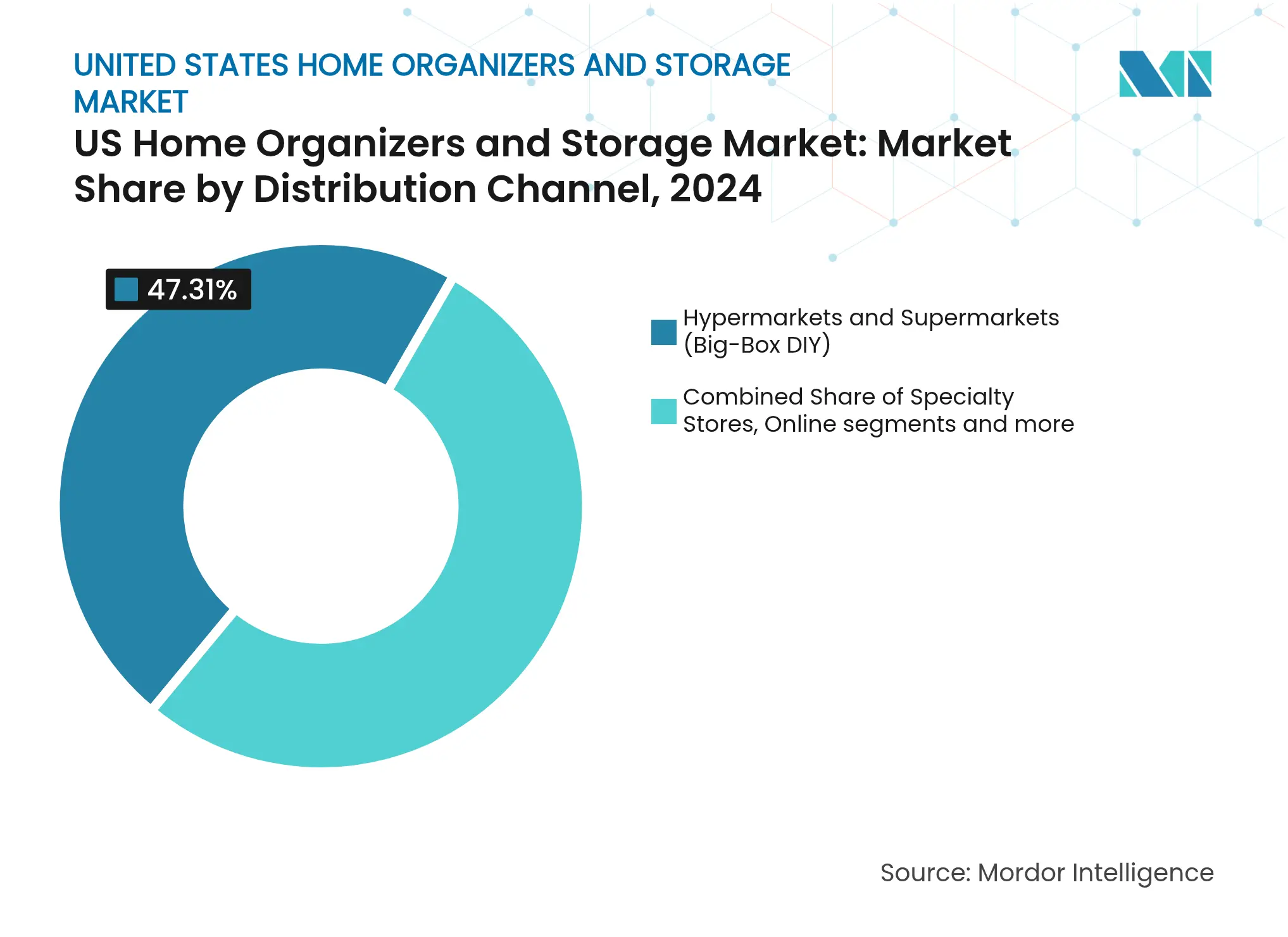

By Distribution Channel: Online Acceleration Reshapes Retail Landscape

Big-box and supermarket formats controlled 47.31% of 2024 revenue, underpinned by the tactile inspection consumers prefer for larger shelving systems. They strengthen lock-in through exclusive brand deals—Lowe’s 2025 tie-up with Masco for Home Options is a prime example. Yet online is the rocket, posting 7.24% CAGR, buoyed by high-definition imagery, AR fit tools, and next-day delivery thresholds that inch downward each quarter. With average basket sizes at USD 118 for storage items on major marketplaces, e-commerce now punches well above its store share in premium-per-unit terms. Specialty Stores, though smaller in footprint, carve out authority via on-staff designers and financed installs, enabling them to upsell motorized valet rods and lit display shelving.

Wayfair’s 150,000-square-foot Illinois store signals a hybrid trend where digital natives open showrooms to cut return rates for large items, pointing to an omnichannel future for the United States home organizers and storage market. Contractors and pro-dealers populate the “Other” bucket, a channel that gains importance as build-for-rent developers bulk-purchase mudroom kits and coat-closet inserts. As shelf-space wars intensify, suppliers with robust drop-ship programs win—retailers bear less inventory risk, and consumers accept elongated lead times for niche finishes. Data aggregation from online reviews also feeds into rapid SKU rationalization, helping brands retire underperformers in months, not seasons.

Note: Segment shares of all individual segments available upon report purchase

The South generated 29.12% of 2024 revenue, thanks to inbound migration and favorable tax regimes that keep disposable income high. States like Florida (+34.7% inventory) and Texas (+16.0% inventory) report robust move-in activity that sparks new closet installs during the first 12 months of ownership. Builders in Atlanta and Dallas embed walk-in pantries as a default spec, creating downstream opportunities for pull-out organizers and bulk-storage tubs. The United States home organizers and storage market size tied to the South is forecast to reach USD 4.5 billion by 2030, sustaining its seat as the volume powerhouse.

The West, while smaller in absolute terms, is projected for 6.03% CAGR—the fastest nationwide—driven by tech incomes, high real-estate values, and early uptake of AI-designed spaces. Seattle’s micro-apartment boom underscores how square-foot pressures increase per-unit spending on vertical storage. Californian municipalities mandate electrification and energy upgrades during major remodels, giving contractors a natural segue into closet or garage retrofits bundled with insulation projects. West Coast homeowners also lead in premium wood finishes, elevating average order values in the region well above national norms.

The Northeast benefits from the oldest housing stock; aging interiors spur consistent retrofit cycles even amid population outflows. NAHB shows a 9.1% uptick in regional housing starts during 2024, indicating fresh demand for built-ins that align with space-efficient brownstone layouts. Midwest consumers, meanwhile, value-shop but possess basements and attics uncommon on the coasts, favoring large-format shelving and moisture-resistant totes. Together, these two regions maintain a steady 40% slice of demand, providing ballast when high-growth sunbelt metros occasionally cool. Across all four regions, localized design palettes and climate considerations ensure no one-size-fits-all assortment, compelling brands to refine SKUs accordingly.

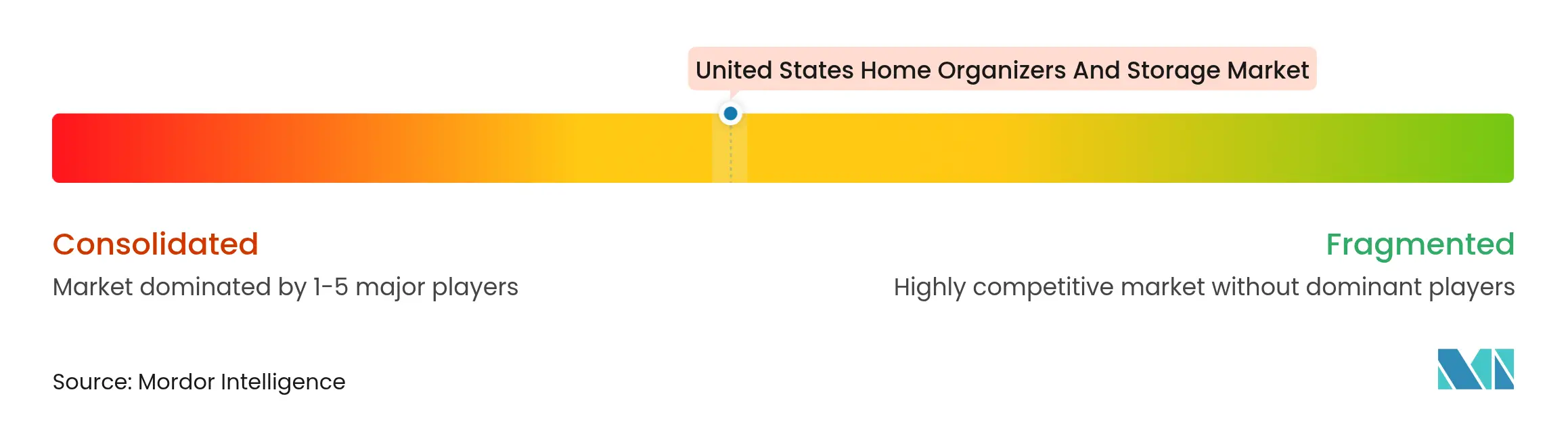

Market Concentration

The United States home organizers and storage market remains moderately fragmented despite the heft of big-box retailers. Home Depot and Lowe’s jointly command roughly 32% of national home-improvement sales, channel clout that translates into prime endcaps and private-label leverage for storage products. Specialty chain The Container Store still dominates high-touch consultation, yet its 2024 bankruptcy filing revealed vulnerability when foot traffic wanes. Wayfair’s entry into physical retail adds another contender able to cross-pollinate website data on search and conversion into in-store merchandising—a formidable loop small independents struggle to match.

Manufacturers likewise segment into commodity and premium cohorts. Sterilite and Rubbermaid control large-format plastic lines at sub-USD 15 price points; their moat lies in resin-molding capacity and truckload logistics efficiencies. At the premium end, American Woodmark and MasterBrand Cabinets integrate closet inserts into broader kitchen and bath packages, leveraging builder relationships to upsell complete storage ecosystems. Direct-to-consumer disruptors such as Modular Closets ride low overhead and viral social campaigns, claiming that factory-direct pricing undercuts traditional quotes by 30%. Organized Living focuses on the pro-builder segment with dealer programs and cloud-based Bid360, reflecting another path to scale without chasing mass retail.

Strategic activity over the past 18 months underscores portfolio realignment: Rev-A-Shelf consolidated multiple Kentucky facilities to raise throughput by 20%, Lowe’s locked an exclusive closet brand from Masco, and American Woodmark launched the mid-priced 1951 Cabinetry line to court distributors. M&A has been modest but purposeful—Karp Associates picked up Adjustable Shelving’s library line to diversify beyond residential niches. Overall, barriers to entry stay low in commodity bins yet escalate in AI-customized wood systems where design software, CNC routing, and color-matched touch-up kits become table stakes. This competitive mosaic supports sustained innovation and keeps pricing power diffused among numerous players instead of a single dominant firm.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

The report provides the scope of the market along with primary growth factors and offers major market insights. The US home organizers and storage market report covers a brief overview of the segments and sub-segmentations, including product types, applications, and companies. This report describes the market size by analyzing historical data and future forecasts.

The US home organizers and storage market is segmented by product (storage baskets, storage boxes, storage bags, hanging stores, multipurpose organizers, travel luggage organizers, modular units, and others), application (bedroom closets, laundry rooms, home offices, pantries and kitchen, garages, and others), and distribution channel (supermarkets and hypermarkets, specialty stores, online, others).

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.