Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

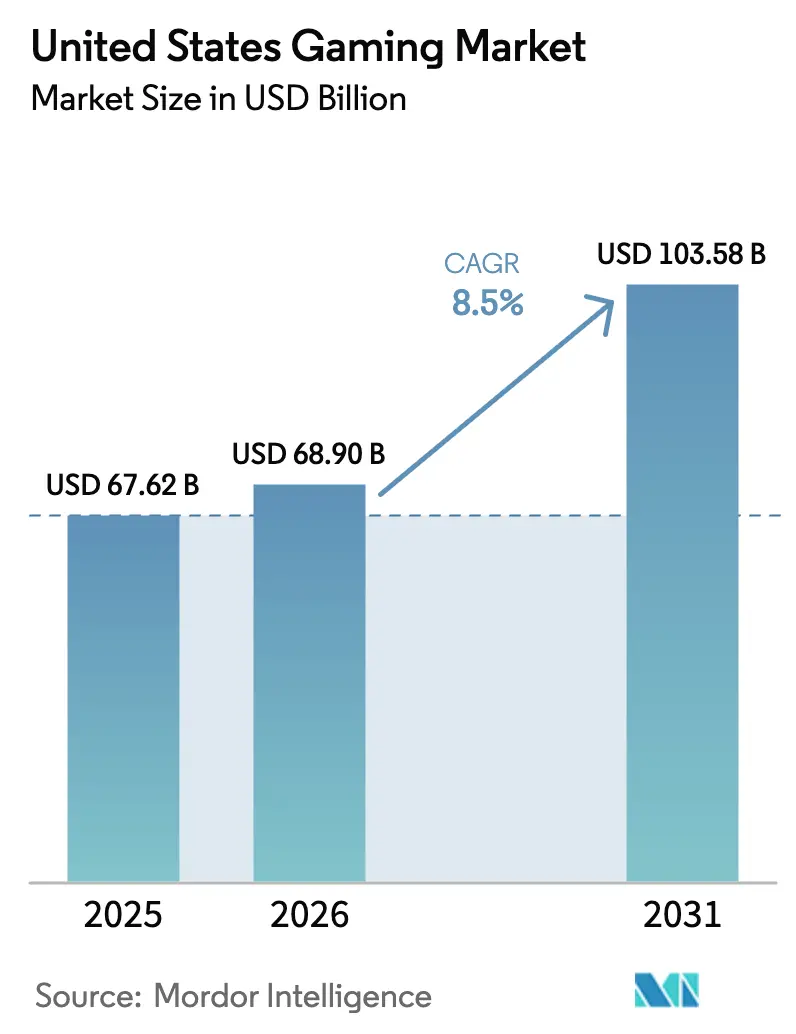

| Base Year Market Size (2025) | USD 67.62 Billion |

| Market Size (2026) | USD 68.90 Billion |

| Market Size (2031) | USD 103.58 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Gaming Market Analysis by Mordor Intelligence

The United States gaming market size was valued at USD 67.62 billion in 2025 and estimated to grow from USD 68.90 billion in 2026 to reach USD 103.58 billion by 2031, at a CAGR of 8.5% during the forecast period (2026-2031). Smartphone penetration above 85% and the rapid rollout of 5G fixed wireless have expanded the reach of the audience while lowering latency thresholds for cloud gaming. Subscription bundles, led by Xbox Game Pass and PlayStation Plus, are steering consumer spending toward recurring-revenue models and compressing the pay-to-own channel. Federal Trade Commission guidance on micro-transactions is nudging publishers to adopt transparent monetization, while also removing regulatory overhang and clarifying compliance costs. Rising capital requirements-AAA budgets now exceed USD 200 million per title-are reinforcing the dominance of deep-pocketed publishers and accelerating studio consolidation.

Key Report Takeaways

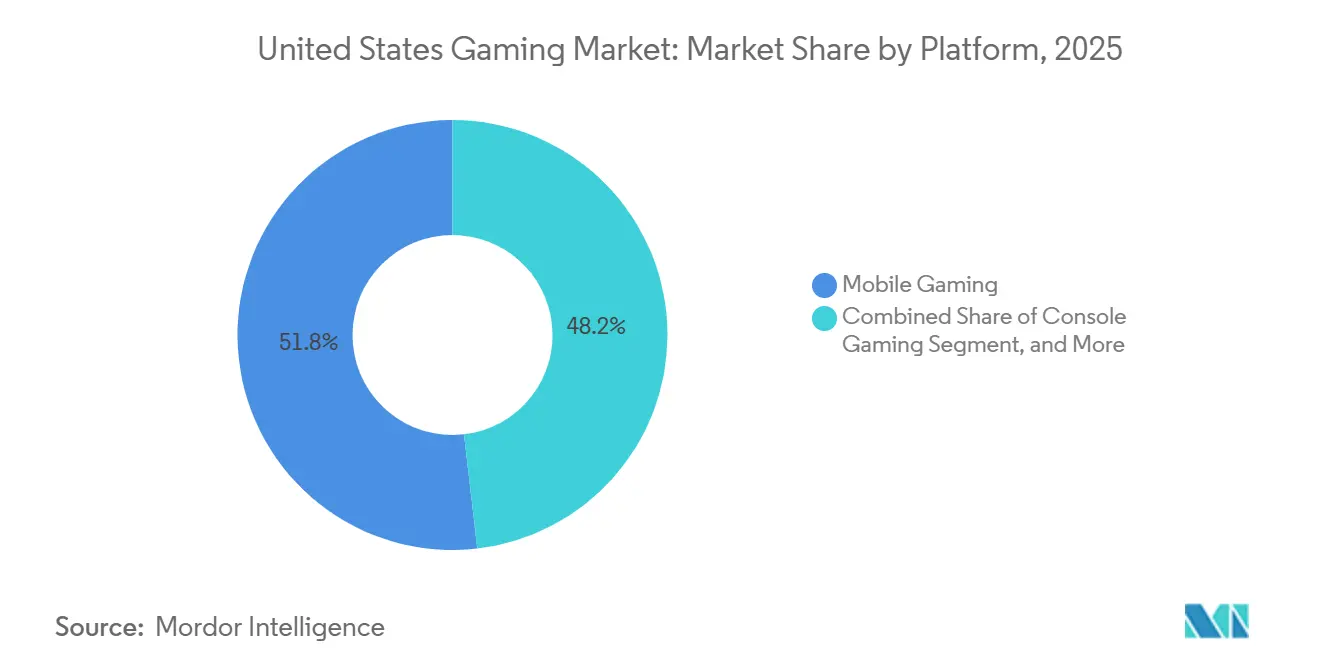

- By platform, mobile gaming led with 51.83% of United States gaming market share in 2025, while cloud and streaming gaming is projected to expand at a 9.16% CAGR through 2031.

- By revenue model, in-app purchases captured 62.66% share of the United States gaming market size in 2025, whereas subscription passes are forecast to advance at an 8.74% CAGR to 2031.

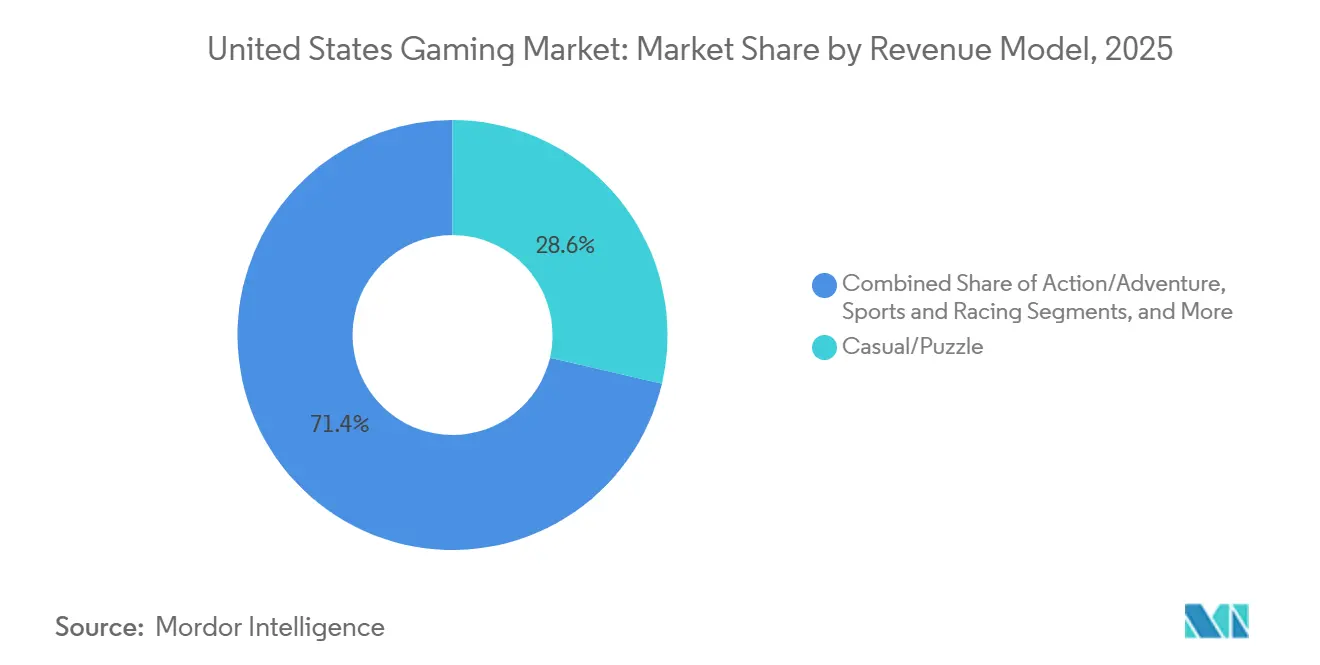

- By genre, casual and puzzle titles accounted for 28.64% share of the United States gaming market size in 2025 and sports and racing is anticipated to register the fastest 9.02% CAGR over 2026-2031.

- By gamer demographic, the 18-34 cohort held 44.71% of the United States gaming market share in 2025 and the 45-plus segment is expanding at an 8.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cloud-gaming subscriptions | +1.2% | National, with concentrated adoption in urban and suburban areas served by 5G fixed-wireless | Medium term (2-4 years) |

| Rising mobile-gamer base and smartphone penetration | +1.8% | National, with highest penetration in metropolitan statistical areas and among 18-44 age cohorts | Long term (≥ 4 years) |

| Esports media-rights monetization boom | +0.9% | National, with premium valuations in coastal markets and university towns | Medium term (2-4 years) |

| AI-driven in-game personalization lifts ARPU | +1.1% | National, led by studios in California, Washington, and Texas technology corridors | Short term (≤ 2 years) |

| FTC micro-transaction guidance clarity | +0.4% | National, with compliance frameworks enforced federally and supplemented by state-level consumer-protection statutes | Short term (≤ 2 years) |

| 5G fixed-wireless roll-out lowers latency | +0.6% | National, with early gains in T-Mobile and Verizon coverage zones; AT&T expanding rapidly | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud-Gaming Subscriptions

Xbox Game Pass surpassed 35-37 million subscribers by mid-2025, generating roughly USD 5 billion in annual revenue, after Microsoft inked more than 150 content deals in the same year.[1]Microsoft Corporation, “Investor Relations,” microsoft.com Subscriber spending across all gaming platforms climbed 24% year-over-year in December 2025, confirming consumer appetite for bundled day-one access. Reduced hardware requirements and cross-device continuity are projected to propel global cloud-gaming revenue from USD 1.4 billion in 2025 to USD 18.3 billion by 2030. Platform holders use “all-you-can-play” libraries to smooth revenue volatility and shift titles toward live-service design. This raises barriers for mid-tier publishers that lack back catalogs large enough to anchor a subscription proposition.

Rising Mobile-Gamer Base and Smartphone Penetration

Mobile gaming represented 51.83% of the United States gaming market in 2025, supported by USD 52 billion in mobile in-app-purchase revenue during 2024, up 16% year-over-year.[2]Sensor Tower, “Mobile Gaming Market Intelligence,” sensortower.comiOS captured 55% of that spend despite Android’s larger install base, highlighting Apple’s monetization edge. 5G devices now deliver sub-20-millisecond latencies that enable competitive play previously confined to console and PC. Affordable mid-tier handsets with 120-hertz displays are democratizing premium experiences for older demographics that value short session lengths. Publishers are therefore prioritizing one-hand controls and portrait orientations to widen reach.

Esports Media-Rights Monetization Boom

The National Basketball Association’s USD 76 billion domestic broadcast renewal in 2025 underscored the premium valuations attached to live content and raised expectations for esports rights packages. United States esports viewership hit 805 million hours in Q3 2025, narrowing the gap with traditional sports ratings. Sponsorship and ad revenue tied to esports climbed 18% year-over-year, fuelled by in-broadcast product integrations that bypass ad-blockers. Collegiate leagues are formalizing franchising structures, granting media partners multi-year visibility. Bundled subscriptions that mix live sports and esports on the same streaming platforms are reducing churn.

AI-Driven In-Game Personalization Lifts ARPU

Studios deploying machine-learning bid engines have reported ARPU gains above 180% by tailoring offers and difficulty curves in real time. Fifty-two percent of developers already employ generative AI for prototyping and asset creation, compressing production schedules by up to 30%. Investors reward AI-enabled publishers with valuation multiples two to three times higher than peers because scalable content pipelines reduce hit-risk. Nonetheless, 30% of creators worry about IP leakage and energy usage, indicating an emerging governance challenge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating AAA development and marketing costs | -1.4% | National, with highest concentration in California, Washington, and Texas studio clusters | Long term (≥ 4 years) |

| Regulatory scrutiny on loot-box mechanics | -0.8% | National, with federal enforcement supplemented by state-level consumer-protection statutes | Medium term (2-4 years) |

| Senior real-time-engine talent shortage | -0.6% | National, with acute shortages in Unreal Engine and Unity specialists in technology hubs | Medium term (2-4 years) |

| Energy-intensive data centers raise OPEX | -0.5% | National, with highest impact in Virginia, California, and Texas data-center corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating AAA Development and Marketing Costs

Take-Two capitalized USD 2.145 billion in development costs by June 30 2025, primarily for Grand Theft Auto VI, illustrating ballooning spending profiles.[3]Take-Two Interactive Software Inc., “Form 10-K 2025,” sec.gov Ray-tracing consumes 30-40% of modern AAA budgets and motion-capture plus voice talent can exceed USD 25 million per release. Development cycles now stretch five to seven years, requiring teams of up to 1,000 employees with six-figure salaries, shrinking margins. Publishers answer by canceling mid-tier titles and doubling down on live-service franchises to amortize investment.

Regulatory Scrutiny on Loot-Box Mechanics

The FTC levied USD 520 million in relief against Epic Games through June 2025 and fined Cognosphere USD 20 million in January 2025, establishing federal precedent on random-reward monetization. Compliance expenses-from age-verification to parental-consent workflows-are climbing, prompting some publishers to excise loot-boxes from youth-oriented releases. The Entertainment Software Rating Board’s “random items” label, combined with state privacy acts, adds further disclosure obligations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Dominance Meets Cloud Disruption

Mobile contributed 51.83% of United States gaming market share in 2025, led by USD 52 billion in IAP revenue. Cloud play, although only a low-single-digit contributor today, is poised to grow at a 9.16% CAGR, outpacing the overall United States gaming market.Console gaming experienced a resurgence in 2025, with hardware sales climbing 20 percent year-to-date through August to USD 2.9 billion, propelled by Nintendo Switch 2's record-breaking launch that sold more than 2.4 million units in the United States within three months, outpacing PlayStation 4's debut by approximately 5 percent.

Market concentration is intensifying, as the top 10 games on Steam captured 61 percent of revenue and the top 100 accounted for 91 percent, indicating winner-take-most dynamics that favor established franchises and live-service titles. Forward momentum stems from 5G fixed-wireless that already covers 10.3 million households combined across T-Mobile and Verizon, enabling sub-10 millisecond round-trip latencies. Console hardware price hikes-Xbox Series X at USD 599 and PlayStation 5 at USD 549-are nudging budget-sensitive users toward streaming alternatives.

By Revenue Model: In-App Purchases Lead, Subscriptions Accelerate

In-app purchases delivered 62.66% of value in 2025, underpinning the largest pool within the United States gaming market size. Subscription passes, on the other hand, are projected to record an 8.74% CAGR to 2031. Premium pay-to-own titles faced headwinds as new releases accounted for only 12 percent of total playtime in 2024, with players gravitating toward established live-service games that offer continuous content updates and social engagement.

Xbox Game Pass alone added more than 150 titles during 2025 and pushed console content revenue up 65.9% after catalog integration. Hybrid models that mix IAP, advertising and subscriptions achieve steadier cash flows and hedge against whale-spend volatility. Fifty-eight percent of marketers planned to increase connected-TV spending in the second half of 2025, with addressability, measurability, and first-party data cited as top priorities, positioning gaming as a distinct ad channel with positive year-over-year growth.

By Genre: Casual Puzzle Anchors Share, Sports Racing Surges

Casual and puzzle games held 28.64% of United States gaming market share in 2025 thanks to older-age mobile adoption. Sports and racing franchises, however, are expected to expand at a 9.02% CAGR as live-service updates and cross-platform play deepen engagement.Shooter games remain a cornerstone of the market, with Call of Duty: Black Ops 6 generating USD 1 billion in its first three weeks post-launch in October 2024, marking the fastest-selling entry in franchise history, while the broader Call of Duty franchise surpassed 500 million lifetime players.

Role-playing and massively multiplayer online games maintain dedicated audiences, with Sony's Bungie studio accelerating Marathon's launch by March 2026 under tighter corporate oversight following restructuring in August 2025. Electronic Arts generated USD 1.9 billion in quarterly sports revenue in fiscal Q3 2025, with EA Sports FC 25 attracting 22 million unique players in its first three months. Annualized content drops sustain monetization well into subsequent release cycles.

By Gamer Demographic: Young Adults Dominate, Older Cohorts Accelerate

Gamers aged 18-34 comprised 44.71% of players in 2025, anchoring premium console and competitive shooter demand. The 45-plus segment, expanding at an 8.96% CAGR, uses mobile interfaces and health gamification to reinforce daily routines. AARP reported 52.4 million gamers aged 50 and older in the United States in 2024, while the Entertainment Software Association found that 26 percent of gamers are 55 or older, and the average gamer age reached 36 years.

Mobile gaming serves as the primary entry point for older demographics, with casual and puzzle genres offering low-friction onboarding and shorter session lengths that fit into daily routines. Cross-generational play is rising as family subscription plans gain popularity. This dynamic creates incremental revenue opportunities through cosmetics that appeal across age divides.

Geography Analysis

Regional revenue reached USD 52.7 billion in 2025, accounting for the largest share globally. Coastal metropolitan areas boast faster broadband, greater ad budgets and higher disposable incomes than rural zones. Regional variations within the United States reflect infrastructure disparities, with 5G fixed-wireless adoption concentrated in urban and suburban zones served by T-Mobile's 6.1 million and Verizon's 4.2 million fixed-wireless access customers as of Q3 2024, while rural areas lag due to limited fiber availability affecting 25 percent of United States households.

Urban clusters in California, Washington and Texas host the majority of studio headcount and cloud data-center racks, benefiting from talent density and venture capital access. Virginia’s “Data Center Alley” leads electricity consumption, compelling operators to sign renewable power-purchase agreements as GPU servers exceed 5 kW per unit.

5G fixed-wireless adoption remains strongest in the 10 largest MSAs, yet 25% of households in rural counties still lack fiber-grade connectivity, limiting cloud-gaming uptake. The Federal Trade Commission and state-level consumer-protection agencies enforce compliance frameworks that shape monetization practices nationwide, with California's Consumer Privacy Act and Children's Online Privacy Protection Act setting de facto national standards that publishers adopt to avoid fragmented compliance regimes.

Competitive Landscape

Platform holders Microsoft, Sony Interactive Entertainment and Nintendo act as gatekeepers by bundling exclusive intellectual property with hardware and services. Microsoft finalized its USD 68.7 billion Activision Blizzard acquisition in 2023, folding Call of Duty into Game Pass and nudging subscribers past the 35 million mark by mid-2025.

Electronic Arts accepted a USD 55 billion privatization offer in October 2025, signaling that private-equity capital values predictable live-service cash flows. Epic Games’ partnership with Unity will let Unity-built titles run inside Fortnite from 2026, positioning Fortnite as an alternative distribution layer that retains 88% of creator revenue.

Smaller studios deploying generative AI can now build prototype levels in days, yet 41% of developers reported layoffs in 2025 as publishers prune overlapping roles after M&A waves. Market power is therefore tilting toward conglomerates able to fund ballooning budgets and negotiate prime cloud contracts.

United States Gaming Industry Leaders

Activision Blizzard, Inc.

Electronic Arts Inc.

Take-Two Interactive Software Inc.

Microsoft Corporation

Sony Interactive Entertainment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: U.S. lawmakers requested an FTC review of Electronic Arts’ USD 55 billion buyout, citing national-security concerns over foreign data ownership.

- January 2026: Microsoft confirmed simultaneous Fable and Kiln launches on PlayStation 5 to maximize software reach.

- December 2025: Netflix unveiled an USD 82.7 billion deal to acquire Warner Bros. Discovery’s gaming assets, pending regulatory approval

- December 2025: Fortnite Creative map “Steal the Brainrot” exceeded 1 million concurrent players, netting USD 13.8 million in a single day.

United States Gaming Market Report Scope

As per the scope of the report, gaming is defined as playing electronic games through a variety of means, such as computers, mobile phones, consoles, or other mediums altogether. There is an increasing prevalence of high-speed internet connections, especially in emerging economies, which has made online gaming practical for more people in recent years.

The United States Gaming Market Report is Segmented by Platform (Mobile Gaming, Console Gaming, PC Gaming, and Cloud/Streaming Gaming), Revenue Model (In-App Purchases, Premium (Pay-to-Own), Subscription Passes, and Advertising-Supported), Genre (Action/Adventure, Shooter, Sports and Racing, Role-Playing and MMO, Casual/Puzzle, Strategy and Card, and Other Genres), and Gamer Demographic (Less Than 18 Years, 18-34 Years, 35-44 Years, and 45+ Years). The Market Forecasts are Provided in Terms of Value (USD).

By Platform

| Mobile Gaming |

| Console Gaming |

| PC Gaming (Client and Browser) |

| Cloud / Streaming Gaming |

By Revenue Model

| In-App Purchases (IAP) |

| Premium (Pay-to-Own) |

| Subscription Passes |

| Advertising-Supported |

By Genre

| Action / Adventure |

| Shooter |

| Sports and Racing |

| Role-Playing and MMO |

| Casual / Puzzle |

| Strategy and Card |

| Other Genres |

By Gamer Demographic

| Less Than 18 Years |

| 18 -34 Years |

| 35 -44 Years |

| 45+ Years |

| By Platform | Mobile Gaming |

| Console Gaming | |

| PC Gaming (Client and Browser) | |

| Cloud / Streaming Gaming | |

| By Revenue Model | In-App Purchases (IAP) |

| Premium (Pay-to-Own) | |

| Subscription Passes | |

| Advertising-Supported | |

| By Genre | Action / Adventure |

| Shooter | |

| Sports and Racing | |

| Role-Playing and MMO | |

| Casual / Puzzle | |

| Strategy and Card | |

| Other Genres | |

| By Gamer Demographic | Less Than 18 Years |

| 18 -34 Years | |

| 35 -44 Years | |

| 45+ Years |

Key Questions Answered in the Report

How big is the United States gaming market in 2026?

The United States gaming market size reached USD 68.9 billion in 2026.

Which platform leads spending?

Mobile Gaming led with 55.88% of United States gaming market share in 2025.

What is the forecast growth rate through 2031?

Overall revenue is projected to rise at a 8.75% CAGR between 2026 and 2031.

Which revenue model is expanding fastest?

Subscription Passes are forecast to post a 10.18% CAGR through 2031.

What demographic spends the most on games?

Players aged 18-34 represent the largest and fastest-growing spending cohort at 39.35% share.

Page last updated on: