Market Overview

| Study Period | 2020 - 2031 |

|---|---|

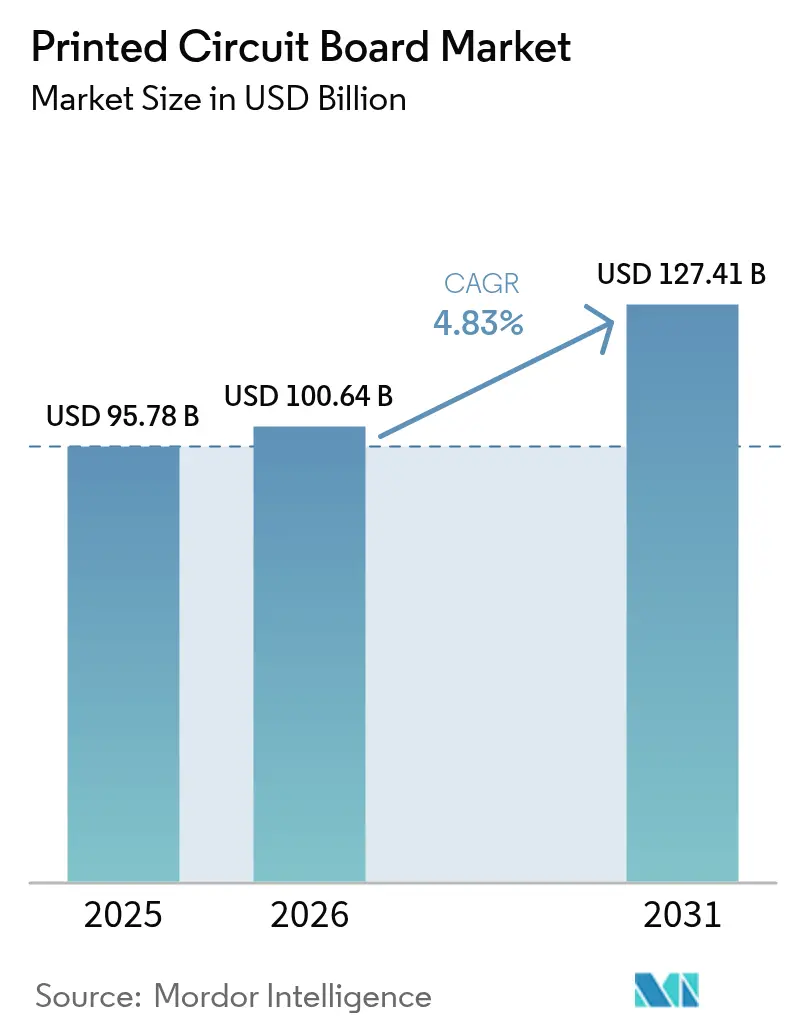

| Market Size (2026) | USD 100.64 Billion |

| Market Size (2031) | USD 127.41 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

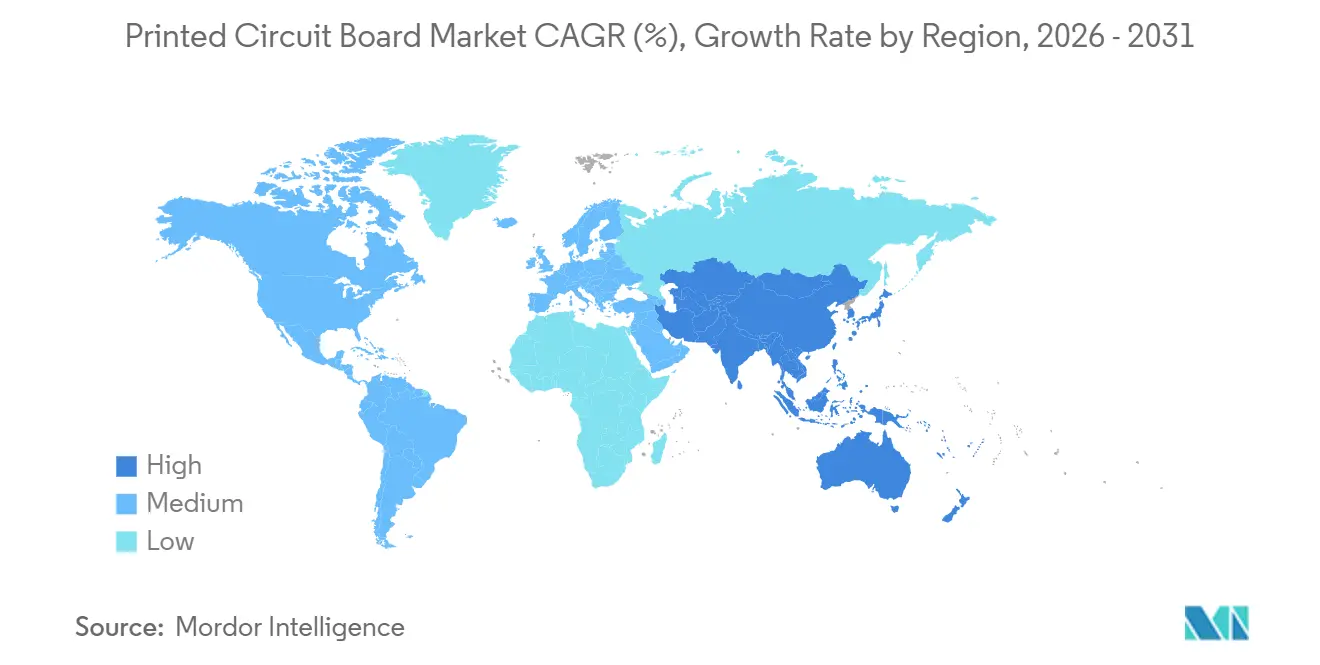

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printed Circuit Board Market Analysis by Mordor Intelligence

The printed circuit board market size is projected to be USD 95.78 billion in 2025, USD 100.64 billion in 2026, and reach USD 127.41 billion by 2031, translating to a 4.83% CAGR over the forecast period. Demand is shifting from legacy consumer devices toward higher-value deployments in artificial-intelligence servers, electric-vehicle power electronics, and next-generation telecom networks, each of which specifies boards with more layers, tighter tolerances, and premium dielectric materials. Hyperscale data-center operators upgrading to 112 Gbps per-lane signaling now order 40-plus-layer backplanes that carry selling prices nearly four times those of eight-layer smartphone boards. Regional policy, led by United States CHIPS and Science Act incentives and European sovereign-AI mandates, is encouraging new fabrication in North America and Central Europe while tempering Asia-Pacific’s historic scale advantage. Material substitution is another tail-wind, with ultra-low-loss substrates gaining share as hyperscalers shift to 800 Gbps and 1.6 Tbps optics. At the same time, raw-material volatility and tightening wastewater rules are thinning margins for commodity makers, prompting consolidation that should favor suppliers positioned in premium niches of the printed circuit board market.

Key Report Takeaways

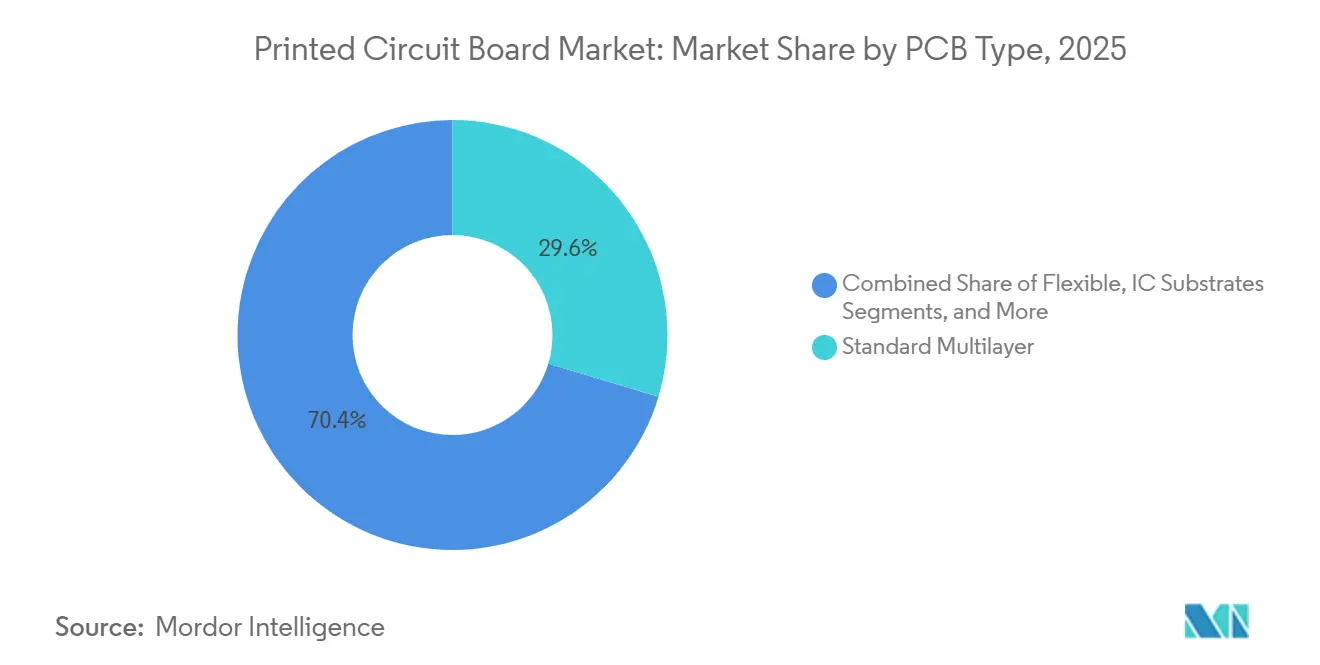

- By PCB type, standard multilayer boards held 29.64% of printed circuit board market share in 2025, while flexible circuits (FPC) are forecast to expand at a 5.39% CAGR through 2031.

- By substrate material, glass-epoxy (FR-4) laminates captured 44.29% of printed circuit board (PCB) market size in 2025, and high-speed and low-loss laminates are advancing at a 5.42% CAGR.

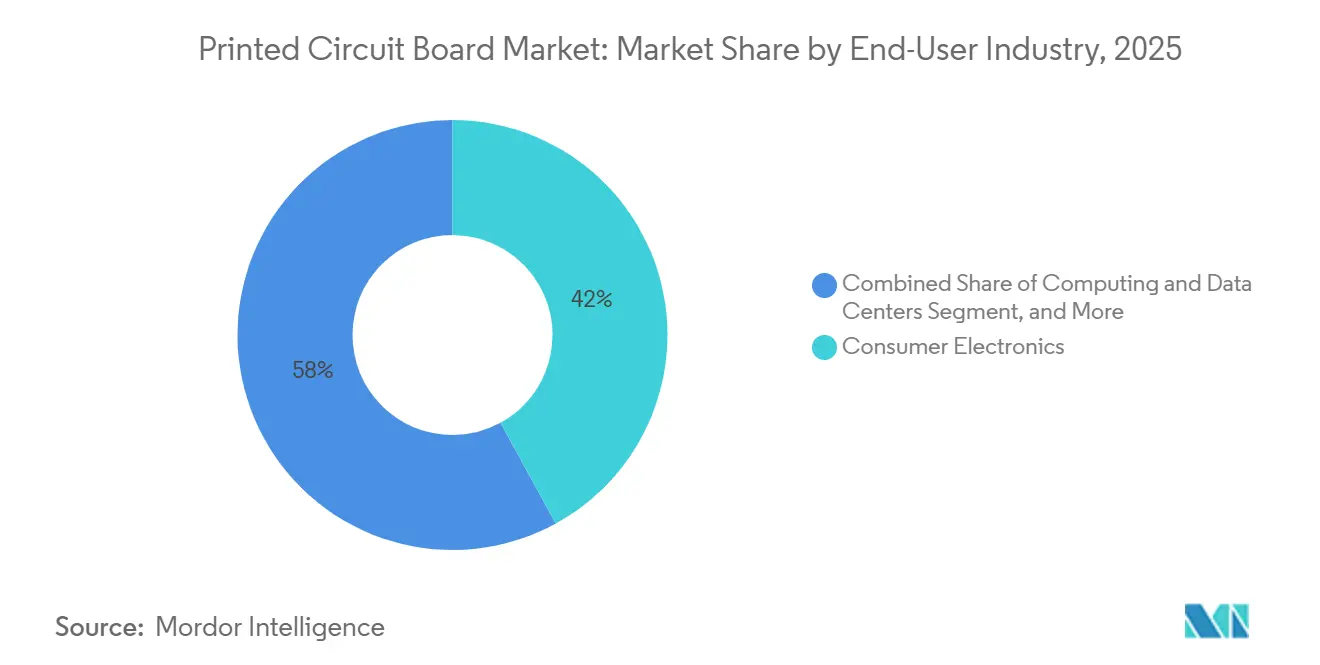

- By end-user industry, consumer electronics represented 42.03% of 2025 PCB market demand, whereas telecommunications and 5G infrastructure is growing fastest at 5.37% CAGR.

- By geography, Asia-Pacific produced 82.54% of global PCb market output in 2025; Asia-Pacifc is the fastest-growing region through 2031 at 4.86% CAGR under re-shoring incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI server and high-performance computing demand | +1.2% | Global, concentrated in North America and Asia-Pacific data-center hubs | Medium term (2-4 years) |

| Accelerated EV power electronics content | +0.9% | Asia-Pacific core, expanding to Europe and North America | Long term (≥ 4 years) |

| 5G and emerging 6G transition boosting HDI adoption | +0.8% | Global, with early gains in South Korea, China, Japan | Medium term (2-4 years) |

| Shift toward advanced IC substrates for chiplet integration | +0.7% | Taiwan, Japan, South Korea; spillover to Malaysia and Vietnam | Long term (≥ 4 years) |

| Re-shoring incentives in U.S. and EU for critical PCB supply chains | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Adoption of ultra-low-loss materials for 112-224 Gbps signaling | +0.6% | Global, led by North American and European hyperscalers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in AI Server and High-Performance Computing Demand

Hyperscale operators deployed roughly 1.2 million AI-optimized servers in 2025, each integrating 8-16 GPU accelerators that draw more than 1.0 kW per socket. These platforms specify 40-to-60-layer backplanes with microvias under 75 μm, laser-drilled stacked vias, and embedded thermal vias that dissipate heat from liquid-cooled cold plates.[1]NVIDIA Corporation, “Blackwell Architecture Whitepaper,” nvidia.com Unit pricing for such substrates exceeds USD 200 compared with USD 50 for legacy server boards, expanding gross margins for Taiwanese specialists able to meet the tolerance window. AMD’s Instinct MI350 program employs chiplet topologies that require embedded-trace substrates, driving incremental demand through 2026 and beyond.[2]Advanced Micro Devices, “Instinct MI350 Product Brief,” amd.com The printed circuit board market therefore captures a direct uplift from both higher layer counts and richer mixes of advanced substrates.

Accelerated EV Power Electronics Content

Battery-electric vehicles delivered in 2025 contained USD 150-200 worth of PCB content across inverters, chargers, and battery-management units, double that of internal-combustion models. Silicon-carbide power modules switching at 800 V create junction temperatures above 175 °C, forcing designers to adopt polyimide or ceramic boards with glass-transition values above 260 °C and thick copper foils up to 210 μm to carry 400 A.[3]IEEE, “Silicon Carbide Power Modules in EVs,” ieeexplore.ieee.org Automotive-grade validation under IATF 16949 narrows the supplier pool, increasing pricing power for incumbents and enlarging the PCB market in value terms.

5G and Emerging 6G Transition Boosting HDI Adoption

Operators installed 2.5 million 5G macro cells in 2025, each embedding 6-10 high-density interconnect boards to enable massive-MIMO beamforming. HDI technology uses microvias below 150 μm and 75 μm line-widths to compress radio units that must mount on urban structures, spurring steady volume in Asia and rapid growth in North America as Open RAN architectures gain momentum. Early 6G prototypes operating above 100 GHz rely on liquid-crystal-polymer laminates with dissipation factors below 0.002, a specification opening a future premium-priced tier inside the printed circuit board market.

Shift Toward Advanced IC Substrates for Chiplet Integration

Chiplet-based processors such as Intel Sapphire Rapids and AMD EPYC Genoa redistribute thousands of signals over organic substrates that combine ultra-fine 10 μm lines with ball-grid arrays on 0.4 mm pitch. The boom in Ajinomoto Build-up Film consumption forced Ibiden and Shinko Electric to invest JPY 50 billion (USD 0.32 billion) in new lines, keeping supply tight and sustaining a pricing premium that enlarges revenue for substrate makers. Embedded-die variants insert passives directly into the laminate, reducing assembly steps and future-proofing the printed circuit board market against further silicon disaggregation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged copper and epoxy-resin price volatility | -0.7% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Talent shortages in advanced PCB design and process engineering | -0.4% | North America and Europe, emerging in Taiwan and Japan | Medium term (2-4 years) |

| Escalating ESG compliance costs for wastewater and PFAS elimination | -0.5% | North America and Europe, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Geopolitical export controls limiting advanced-substrate equipment | -0.3% | China, with global spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Copper and Epoxy-Resin Price Volatility

Copper futures oscillated between USD 8,200 and USD 10,500 per metric ton during 2024-2025 as mine disruptions in Chile and Peru collided with speculative EV demand.[4]London Metal Exchange, “Copper Futures Historical Data,” lme.com Because copper foil can represent up to 40% of finished-board cost, spot spikes erode margins for smaller Asian fabricators lacking hedging programs. Epoxy-resin prices jumped after a 2025 Taiwanese precursor plant fire cut bisphenol-A output, leading laminate suppliers to invoke force-majeure clauses that delayed shipments to North America]. Such volatility complicates capital-investment models and dampens short-term growth in the PCB market.

Escalating ESG Compliance Costs for Wastewater and PFAS Elimination

The United States Environmental Protection Agency proposed classifying legacy PFAS surfactants as hazardous substances in 2024, triggering wastewater limits that could demand oxidation or filtration systems costing USD 10-20 million per facility.[5]United States Environmental Protection Agency, “PFAS Strategic Roadmap,” epa.gov European REACH rules are moving in parallel, forcing formulators to re-engineer resists and surface finishes. Smaller Western plants may close rather than invest, consolidating capacity and shifting volume toward Asia unless regulators impose carbon-adjustment mechanisms. Compliance costs therefore subtract an estimated 0.5 percentage-points from the sector CAGR yet favor larger firms that can amortize the upgrades across higher-value programs, subtly reshaping the printed circuit board market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Outpace Commodity Multilayers

Standard multilayer boards retained 29.64% printed circuit board market share in 2025, anchored by automotive body electronics and industrial drives. Flexible circuits, however, are set to expand at a 5.39% CAGR through 2031 as foldable smartphones, wearable health monitors, and thin automotive interior modules demand bend radii below 3 mm. Samsung’s Galaxy Z series alone shipped 10 million units in 2025, each carrying three or more polyimide flexes supplied by Nippon Mektron and Flexium. High-density interconnect designs have become the de facto choice for premium handsets because 75 µm line widths accommodate multi-camera arrays. IC substrates remain a small but lucrative niche, priced four to five times higher than eight-layer server boards because they require 0.4 mm ball-grid arrays and 10 µm traces.

Rigid-flex constructions are carving share in aerospace and implantable medical devices where vibration resistance and space savings justify a 30-50% cost premium. Metal-core and ceramic boards serve LED headlamps and automotive radar, benefiting from the move to solid-state lighting and advanced driver-assistance systems. Commodity four-layer product runs face margin compression as Shenzhen and Suzhou factories compete aggressively on price. Conversely, specialty fabricators that hold IPC-6012 Class 3 or MIL-PRF-55110 certifications enjoy insulated pricing because defense and medical customers will not switch to lower-grade suppliers. Overall, the printed circuit board market size gains value as the mix shifts toward flex, rigid-flex, and IC substrates even while commodity unit volumes level off.

By Substrate Material: Ultra-Low-Loss Laminates Capture Network Upgrades

Glass-epoxy FR-4 commanded 44.29% of 2025 revenue, sustained by cost-sensitive consumer and industrial applications. Yet high-speed, low-loss substrates are projected to grow 5.42 % annually through 2031 as hyperscalers transition to 800 Gbps and 1.6 Tbps switch ports that require dissipation factors below 0.005 at 10 GHz. Panasonic Megtron 8 and Rogers RO4000 series already appear on approved-vendor lists at Arista and Cisco. Polyimide films remain essential for flex boards but face supply concentration because DuPont and Kaneka dominate global capacity. Ajinomoto Build-up Film continues in structural shortage, extending lead times for AI-server substrates to as long as 20 weeks.

Emerging liquid-crystal-polymer laminates priced above USD 500 per square meter address 6G prototypes that must operate beyond 100 GHz, though volume production is unlikely before standardization. Heavy-copper variants, with foil weights up to 12 oz, support 48 V automotive platforms and grid-scale inverters. Regulatory frameworks such as RoHS and REACH are nudging FR-4 suppliers toward halogen-free flame retardants, fragmenting the legacy grade into multiple sub-categories with distinct thermal properties. Overall, substitution toward ultra-low-loss and high-temperature substrates lifts average selling prices, enlarging the printed circuit board market size even where total panel square-meter growth is moderate.

By End-User Industry: Telecoms and 5G Infrastructure Lead Growth

Telecommunications and 5G infrastructure is expanding at a 5.37% CAGR, the fastest among verticals, as each macro base station integrates 6-10 HDI boards for beamforming processors and millimeter-wave transceivers. Open RAN disaggregation adds additional server-class boards in edge data centers, deepening demand. Consumer electronics remained the largest bucket at 42.03% of 2025 revenue, yet replacement cycles stretching to 3.5 years temper volume growth. Premium foldables, multi-camera flagships, and true-wireless earbuds still require advanced rigid-flex or HDI, preventing an outright decline. Computing and data centers absorb high-layer-count backplanes and costly AI-package substrates, keeping average prices elevated.

Automotive and electric-vehicle electronics double PCB value per car versus internal-combustion models, climbing to USD 150-200 in 2025 as silicon-carbide inverters switch at 800 V. Industrial drives, renewable-energy inverters, and grid-tied storage systems adopt heavy-copper and metal-core boards, adding steady, margin-rich demand. Medical implants and aerospace avionics insist on IPC-6012 Class 3 traceability, confining supply to a handful of FDA-registered and ITAR-compliant plants. Defense spending in radar and unmanned platforms keeps specialty volumes firm despite modest overall size. Collectively, these shifts reinforce a tilt toward higher-complexity designs, cushioning the printed circuit board market against softness in commodity consumer segments.

Geography Analysis

Asia-Pacific accounted for 82.54% of global production in 2025 and is forecast to grow 4.86% annually, supported by integrated ecosystems in Guangdong, Jiangsu, and the Pearl River Delta where component sourcing, plating chemistry, and assembly lines co-locate. Taiwan anchors the advanced-substrate stack, with Unimicron, Nan Ya PCB, and Kinsus running semiconductor-grade clean rooms that feed both Intel and Taiwan Semiconductor Manufacturing Company. China’s Shennan Circuits and DSBJ dominate smartphone HDI volumes but face tooling bottlenecks under United States export controls. Japan’s Ibiden, Shinko Electric, and Meiko concentrate on high-reliability automotive and industrial boards, leveraging process patents in via fill and surface finish that command premium pricing. South Korean groups Samsung Electro-Mechanics and LG Innotek, historically captive to mobile phones, now channel capex toward automotive radar and data-center substrates.

North America captured roughly 8% printed circuit board market size in 2025 yet is scaling under United States CHIPS and Science Act tax credits and defense-offset clauses. TTM Technologies is investing USD 150 million in New York State for rigid-flex lines dedicated to avionics and radar.[6] TTM Technologies, “CHIPS Act Expansion Announcement,” ttm.com Defense primes stipulate domestic sourcing for mission-critical designs, raising utilization in smaller specialty shops across Arizona and California. Mexico leverages maquiladora status to assemble servers and telecom gear with imported boards, a conduit that keeps some volume inside the broader regional supply chain. Canada’s footprint remains limited to high-mix, low-volume industrial and aerospace prototypes.

Europe held about 6% of 2025 volume yet benefits from the EUR 43 billion (USD 50.7 billion) European Chips Act that subsidizes advanced substrates and encourages dual sourcing for automotive safety systems. AT&S’s Austrian and Malaysian split-site strategy aligns with German carmakers’ preference for diversified risk. Schweizer Electronic is evaluating a joint venture in Arizona, reflecting trans-Atlantic attempts to secure defense and medical accounts. Eastern European countries such as Poland and the Czech Republic pitch lower labor costs plus European Union compliance, appealing for mid-range multilayer runs. Rest-of-world regions, including Latin America, Middle East and Africa, stay subscale, importing boards primarily from Asia for final assembly. Environmental regulations such as RoHS in Europe and TSCA in the United States drive uniform material standards worldwide, indirectly lifting quality benchmarks in emerging markets.

Competitive Landscape

Taiwanese leaders Unimicron and Nan Ya PCB remain the largest revenue earners, anchoring a top-five cohort that captured roughly 38% of 2025 sales in the printed circuit board market. Ibiden and Shinko Electric extend that grip through long-term allocations of Ajinomoto Build-up Film, keeping substrate lead times tight and margins high. Chinese specialists Shennan Circuits and DSBJ dominate cost-sensitive HDI volumes for smartphones, yet face lithography constraints under United States export controls. AT&S holds the widest European footprint, balancing Austrian automotive programs with a new Malaysian campus dedicated to radar and power devices. TTM Technologies heads the United States tier with IPC-6012 Class 3 and MIL-PRF-55110 clearances that lock in defense and aerospace contracts.

Vertical integration defines most new bets. Unimicron committed TWD 15 billion (USD 0.48 billion) for a Taoyuan clean room that will print eight-micrometer lines on 0.35 millimeter ball-grid arrays, securing share in AI accelerators. Samsung Electro-Mechanics opened a pilot line for glass-core substrates, aiming for finer pitches and lower warpage in next-generation processors. AT&S completed a EUR 1.2 billion (USD 1.4 billion) substrate plant in Kulim to diversify outside Europe while chasing automotive qualification. Ibiden bought a minority stake in a Japanese polyimide-film maker, ensuring flex supply for rigid-flex boards used in medical implants. Nan Ya PCB partnered with a European Tier-1 supplier to embed passives inside 48 volt power modules, trimming assembly steps for electric vehicles.

Disruptive dynamics persist even with these scale plays. Large Chinese electric-vehicle firms are in-housing board production, diluting volumes for stand-alone fabricators in Guangdong and Jiangsu. Patent filings in laser direct imaging and embedded-die substrates remain concentrated in Japan and Taiwan, raising entry barriers for latecomers. Smaller North American shops hedge by specializing in Class 3 prototypes and fast-turn avionics sets where quality trumps price. Overall, competitive intensity is shifting from sheer capacity toward control of materials, proprietary processes, and geographically diversified supply, an evolution that supports sustainable pricing in the printed circuit board market.

Printed Circuit Board Industry Leaders

Zhen Ding Technology Holding Ltd.

Unimicron Technology Corp.

Tripod Technology Corp.

TTM Technologies Inc.

ATandS Austria Technologie and Systemtechnik AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unimicron Technology committed TWD 15 billion (USD 470 million) to expand IC-substrate capacity in Taoyuan, Taiwan, targeting AI accelerators and high-bandwidth memory modules.

- December 2026: AT&S completed a EUR 1.2 billion (USD 1.28 billion) IC-substrate plant in Kulim, Malaysia, focused on automotive radar and power chips.

- November 2025: TTM Technologies secured a USD 75 million contract to supply rigid-flex PCBs for next-generation U.S. avionics systems.

- September 2025: Samsung Electro-Mechanics launched a pilot line for glass-core substrates aimed at future AI processors.

Global Printed Circuit Board Market Report Scope

The study tracks the revenue accrued through the sales of PCBs by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which accounts for market estimations and growth rates. The scope of this report encompasses the sizing and forecasts for the various market segments.

The Printed Circuit Board Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, HDI, Flexible Circuits, IC Substrates, Rigid-Flex, Other Types), Substrate Material (Glass Epoxy FR-4, High-Speed Low-Loss, Polyimide, Packaging Resins, Other Materials), End-User Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare, Aerospace and Defense, Other Industries), and Geography (North America, Europe, Asia-Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

By PCB Type

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

By Substrate Material

| Glass Epoxy (FR-4) |

| High-Speed and Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT and ABF) |

| Other Substrate Materials |

By End-User Industry

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare and Medical |

| Aerospace and Defense |

| Other End-User Industries |

By Region

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By PCB Type | Standard Multilayer (non-HDI) | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed and Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT and ABF) | ||

| Other Substrate Materials | ||

| By End-User Industry | Consumer Electronics | |

| Computing and Data Centers | ||

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Industrial and Power | ||

| Healthcare and Medical | ||

| Aerospace and Defense | ||

| Other End-User Industries | ||

| By Region | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the current value of the printed circuit board market?

The printed circuit board market size is USD 100.64 billion in 2026 and is forecast to reach USD 127.40 billion by 2031.

Which segment is growing fastest within PCB applications?

Telecommunications and 5G infrastructure shows the highest segment CAGR at 5.37%, driven by Open RAN base-station deployments.

How will AI servers influence PCB demand through 2031?

AI servers require 40-plus-layer boards and advanced package substrates, adding premium revenue that lifts overall industry CAGR by an estimated 1.2 percentage-points.

What impact do copper-price swings have on PCB producers?

Copper price volatility can cut up to 0.7 percentage-points from forecast CAGR, especially for commodity fabricators without hedging programs.

Which regions are benefiting from re-shoring incentives?

North America and Europe are seeing new investments under the United States CHIPS Act and European Chips Act.

Who holds the largest share in advanced IC substrates?

Unimicron, Nan Ya PCB, and Ibiden together control roughly 18% of revenue in the advanced-substrate niche.

Page last updated on: