Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

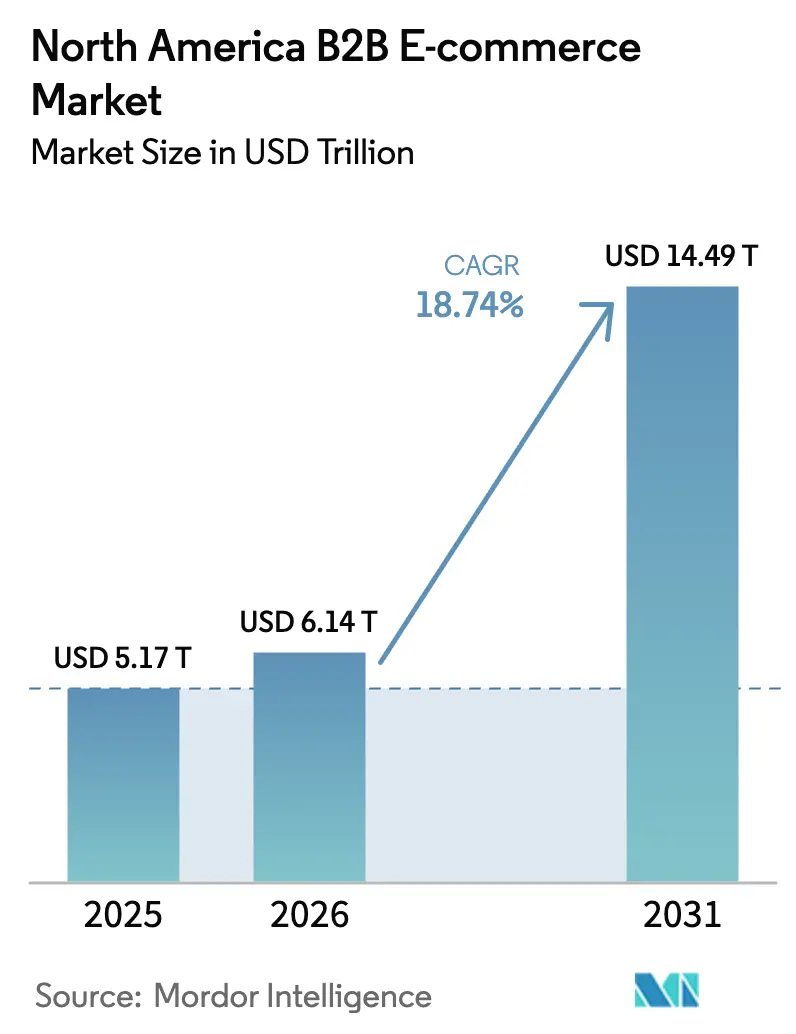

| Base Year Market Size (2025) | USD 5.17 Trillion |

| Market Size (2026) | USD 6.14 Trillion |

| Market Size (2031) | USD 14.49 Trillion |

| Growth Rate (2026 - 2031) | 18.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America B2B E-commerce Market Analysis by Mordor Intelligence

North America B2B E-commerce market size in 2026 is estimated at USD 6.14 trillion, growing from 2025 value of USD 5.17 trillion with 2031 projections showing USD 14.49 trillion, growing at 18.74% CAGR over 2026-2031. Growth is propelled by widescale digital transformation, stronger cloud and 5G connectivity, and mounting pressure on procurement teams to cut cycle times and lower total cost of ownership. A sharp rise in cross-border trade under USMCA, rapid uptake of embedded finance, and the spread of AI-driven product discovery tools are further accelerating channel migration. Competitive intensity is increasing as platform operators recalibrate fee structures, while rising cyber-risk and warehouse capacity constraints temper the overall trajectory. Against this backdrop, the North America B2B e-commerce market continues to offer sizable white-space opportunities in vertical specialization, cross-border enablement, and payment innovation.

Key Report Takeaways

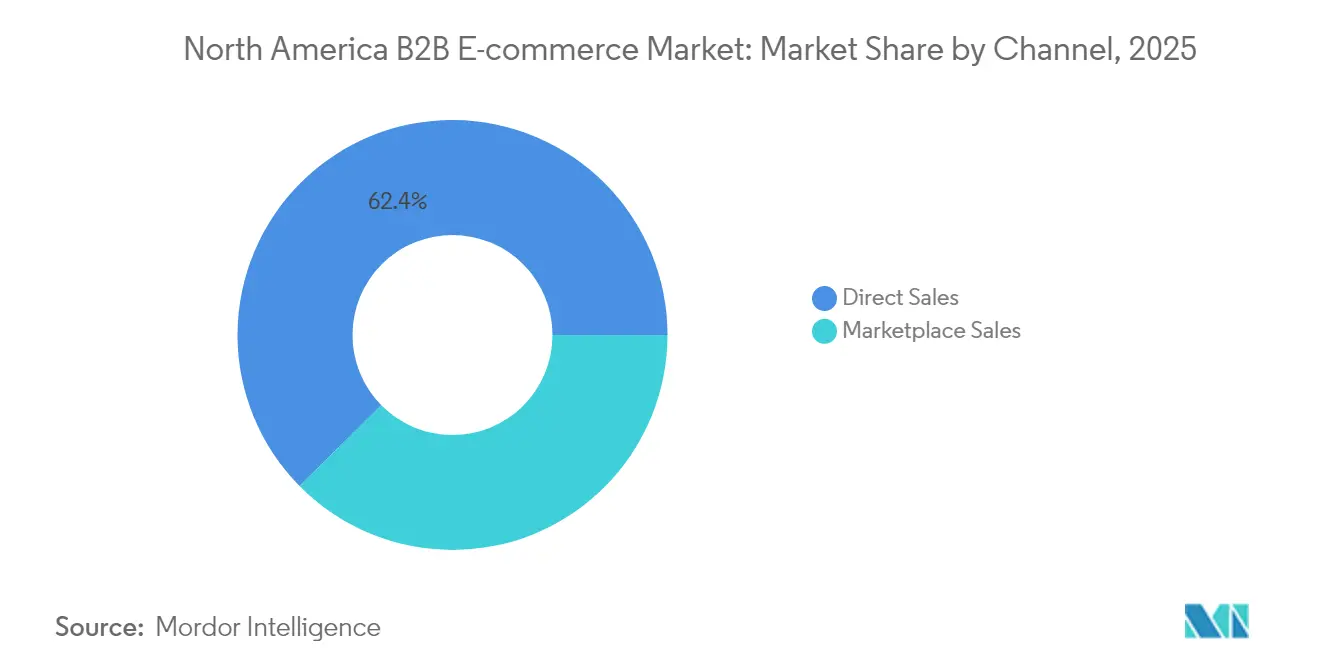

- By channel, direct sales held 62.40% of the North America B2B e-commerce market share in 2025, whereas marketplaces are forecast to scale at 20.95% CAGR through 2031.

- By industry vertical, manufacturing led with 41.20% revenue share in 2025; healthcare and life sciences is projected to expand at a 22.35% CAGR to 2031.

- By transaction model, domestic flows captured 64.30% of the North America B2B e-commerce market size in 2025, while cross-border trade is set to grow at 19.88% CAGR between 2026-2031.

- By geography, the United States commanded 78.40% revenue share in 2025; Mexico is forecast to progress at a 21.25% CAGR through 2031.

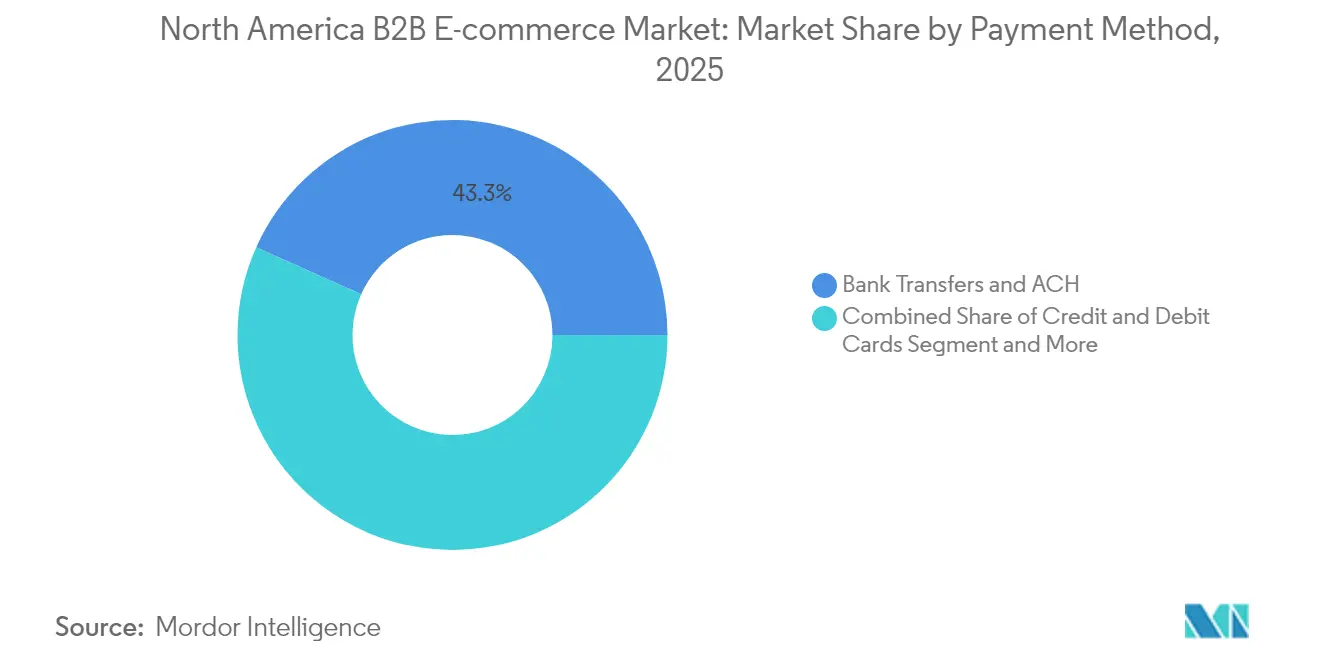

- By payment method, bank transfers and ACH represented 43.30% share of the North America B2B e-commerce market size in 2025, with alternative payments advancing at 21.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America B2B E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Omnichannel fulfillment preference | +4.8% | North America, with strongest adoption in US urban centers | Medium term (2-4 years) |

| Migration from EDI and fax to self-service portals | +3.8% | United States, Canada, with later adoption in Mexico | Short term (≤ 2 years) |

| Surge in marketplace adoption by mid-market firms | +3.4% | United States, with spillover to Canada | Medium term (2-4 years) |

| Procurement-cost reduction mandates | +2.9% | North America, with emphasis in manufacturing sectors | Medium term (2-4 years) |

| Embedded-finance APIs unlocking high-ticket check-out | +2.3% | United States, Canada | Medium term (2-4 years) |

| Cross-border (US-MX-CA) USMCA duty-free thresholds | +1.9% | Border regions, with emphasis on US-Mexico trade corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Omnichannel Fulfillment Preference

Omnichannel models now define purchasing expectations as 94% of decision-makers view unified buying experiences as productive for their organizations. [4]Balance, “B2B Ecommerce Trends and How to Grow Online in 2024,” getbalance.com Integrated inventory visibility and centralized order orchestration lift order accuracy by up to 20% and trim processing times by nearly one-quarter. Industrial distributors observe that buyers often start online, consult a representative, and complete pickup at a branch, blending physical and digital hand-offs within the same transaction. Accelerated digital payment adoption accompanies this shift, with 73% of companies transitioning to electronic settlement methods to support real-time reconciliation. As omnichannel fulfillment matures, platform operators differentiate on inventory depth, last-mile reliability, and payment flexibility, giving rise to ecosystem partnerships between carriers, ERP vendors, and embedded-finance providers. The North America B2B e-commerce market, therefore, tilts towards players that can synchronize data across every interaction node without introducing process friction.

Migration from EDI and Fax to Self-Service Portals

Legacy EDI links and fax orders are giving way to modern portals as 62% of buyers prefer to self-educate online before engaging sales staff. Portal functionality has evolved to include role-based permissions, contract pricing, and tailored catalogs, mirroring complex approval hierarchies inside large enterprises. Millennial procurement professionals, now driving 73% of buying decisions, expect consumer-grade speed and transparency, accelerating portal adoption. Organizations that deploy robust portals report double-digit cuts in administrative overhead and measurable decreases in Maverick spend. Short implementation timelines, often under six months when leveraging composable commerce, further catalyze upgrade cycles. Strong early traction in the United States and Canada suggests near-term upside for solution providers able to integrate portal workflows directly into ERP and inventory systems.

Surge in Marketplace Adoption by Mid-Market Firms

Marketplace adoption among mid-market companies is reshaping distribution economics, with marketplace sales growing 2.5 times faster than direct e-commerce alternatives. Amazon Business alone processed USD 25 billion in 2025 sales, expanding seller networks to more than 5 million suppliers. Mid-market buyers cite greater assortment and faster vendor qualification as top reasons for shifting spend. The speed and transparency of these platforms are forcing traditional distributors to enhance value-added services or adopt marketplace storefronts of their own. Channel mix optimization thus becomes a strategic imperative as the North America B2B e-commerce market gravitates toward platform-centric procurement.

Procurement-Cost Reduction Mandates

Management directives to curb procurement outlays push companies to digitize purchasing. Indirect spend optimization through volume consolidation and automated approvals is delivering cost savings between 5-10% in year one. Inflationary cost pressures and supply-chain volatility intensify the drive for process transparency, making digital procurement a high-return investment. Manufacturing and healthcare operators lead adoption because purchased materials constitute more than half of operating expenses. Early savings often finance subsequent technology upgrades, producing a self-reinforcing adoption cycle that sustains momentum through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-attacks and data-sovereignty litigation | -3.8% | United States, Canada, with increasing impact in Mexico | Medium term (2-4 years) |

| Fragmented payment rails for Net-30/60 terms | -2.9% | North America, with particular impact on cross-border transactions | Short term (≤ 2 years) |

| Growing seller resistance to marketplace fee inflation | -2.3% | United States, with spillover to Canada | Medium term (2-4 years) |

| Warehouse-capacity crunch at inland ports | -1.5% | Major logistics hubs in United States and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-attacks and Data-Sovereignty Litigation

Business email compromise schemes, ransomware, and supply-chain intrusions add material risk to digital channels, with annual losses measured in billions. Heightened regulatory scrutiny, especially around health and financial data, elevates compliance costs as firms must localize sensitive records to satisfy jurisdictional rules. Security budgets are climbing 15-20% each year, yet mid-market players often lack the scale to absorb such expense, delaying platform upgrades. Class-action litigation surrounding breaches causes further hesitation among regulated industries. The policy environment, therefore, represents a meaningful drag on overall adoption, even though security-first architectures promise long-term risk mitigation.

Fragmented Payment Rails for Net-30/60 Terms

High-value B2B orders still rely on extended credit terms that common online gateways do not natively support, leading firms to run dual manual and digital processes. Reconciliation delays impair cash-flow forecasting and dilute the efficiency gains of e-procurement. Cross-border flows add currency conversion and compliance friction, raising transaction costs. While embedded-finance APIs aim to synchronize credit assessment with checkout, integration hurdles with aging ERP instances curb short-term proliferation. Until standardized solutions gain critical mass, the fragmented payment infrastructure will weigh on the growth trajectory of the North America B2B e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Marketplaces Reshape Distribution Dynamics

Marketplace momentum is reshaping the North America B2B e-commerce market. Direct channels retained a 62.40% share in 2025, underpinned by bespoke pricing agreements in regulated environments. Marketplaces, however, are forecast to log a 20.95% CAGR, outpacing the overall North America B2B e-commerce market size. Demand for broad assortments and rapid vendor onboarding fuels migration, particularly among mid-size manufacturers seeking scale without heavy technology investment.

Intensifying rivalry pushes legacy distributors to augment digital storefronts and explore marketplace partnerships. Many pursue a dual-track approach, selling through proprietary portals while listing commodity SKUs on leading marketplaces. As customers blend channels, 85% of firms now report multi-channel engagement strategies. The North America B2B e-commerce market therefore evolves into a hybrid network where channel choice hinges on product complexity, service expectations, and total landed cost.

By Transaction Model: Cross-Border Commerce Accelerates

Domestic orders represented 64.30% of the North America B2B e-commerce market share in 2025, yet cross-border flows are projected to advance at 19.88% CAGR, narrowing the gap. USMCA provisions that lift de minimis thresholds lower customs friction, promoting smaller, higher-frequency shipments. Automated duty calculation and digital customs documentation further remove process hurdles.

Tariff announcements in February 2025 added a 25% levy on select goods from Canada and Mexico, prompting supply-chain re-routing and localized stockholding tactics. Platform providers integrating duty estimation and alternative routing tools stand to gain as firms navigate cost volatility. Over the forecast horizon, the North America B2B e-commerce market size in cross-border trade will hinge on policy stability, logistics modernization, and harmonized data standards.

By Payment Method: Alternative Payments Gain Momentum

Bank transfers and ACH payments held a 43.30% slice of the North America B2B e-commerce market size in 2025, reflecting entrenched trust in conventional rails. Alternative payments, led by embedded-finance credit lines, BNPL, and digital wallets, are expected to surge at 21.75% CAGR. Integrated financing removes the need for separate credit vetting, shortening purchase-to-pay cycles and unlocking working-capital relief for SMB buyers.

Embedded-finance volume could reach USD 16 trillion globally by 2030, lifting platform stickiness through one-click checkout for high-ticket orders. BNPL penetration in B2B is rising from USD 14 billion in 2023 to a projected USD 687 billion by 2028. Adoption remains uneven due to ERP integration gaps and risk-management concerns, yet early movers are already recording higher average order values and lower cart abandonment. As standards coalesce, the North America B2B e-commerce market is set to converge on payment experiences that mirror B2C simplicity without sacrificing credit-term flexibility.

By Industry Vertical: Healthcare Digitalization Accelerates

Manufacturing generated 41.20% of 2025 revenue, demonstrating deep penetration of e-procurement for MRO items and direct materials. Healthcare and life sciences, while smaller today, are forecast to post a 22.35% CAGR, the fastest within the North America B2B e-commerce industry. Heightened focus on supply-chain resilience after recent disruptions has prompted hospitals and laboratories to embrace specialized platforms featuring regulatory compliance workflows and credentialed supplier catalogs.

Four megatrends—consumer-centric health management, interoperable data, B2C-like user experiences, and reinforced data security—underpin vertical growth. Payment innovation adds momentum as embedded-finance programs address reimbursement timing mismatches. The resulting expansion will gradually reduce the manufacturing sector’s dominance, diversifying revenue across a broader spectrum of industries and enhancing overall resilience in the North America B2B e-commerce market.

Geography Analysis

The United States contributed 78.40% of 2025 revenue, benefiting from a dense supplier base and best-in-class digital infrastructure. Amazon Business and other platform leaders continue to scale, while warehouse capacity shortages in inland hubs cause fulfillment delays that spur investment in automation and micro-fulfillment centers. Digital budgets remain a priority, with 83% of U.S. B2B leaders planning to boost spending on composable commerce and AI.

Canada ranks second but shows a sophisticated omnichannel profile, with buyers engaging through an average of 10 touchpoints per transaction. Tariff changes introduced in early 2025 have injected uncertainty into cross-border flows, accelerating contingency planning and localized inventory positioning. Marketplace penetration among mid-market Canadian firms continues to grow as they leverage established logistics links with U.S. partners.

Mexico is the fastest-growing component of the North America B2B e-commerce market, expanding at 21.25% CAGR through 2031. Manufacturing clusters near the U.S. border are digitizing procurement as part of near-shoring strategies. The USD 117 de minimis ceiling restricts small-parcel cross-border volumes, yet rising adoption of regional distribution centers offsets the limitation. Digital wallet uptake lags the northern neighbors, creating an opening for payment specialists targeting high-growth sectors like automotive and electronics.

Competitive Landscape

Competition in the North America B2B e-commerce market blends scale advantages with niche specialization. Amazon Business, projecting USD 80 billion revenue by 2025, leverages logistics reach and rich data to win enterprise contracts. Incumbent distributors such as W.W. Grainger are ramping digital investments, reporting 75% of sales through electronic channels and using endless-assortment strategies to meet long-tail demand. Fastenal and RS Group deploy AI-guided product discovery and regional fulfillment hubs to sustain relevance.

Platform differentiation is increasingly anchored in technology. AI-driven personalization, composable commerce back-ends, and embedded-finance modules serve as critical levers for customer retention. Identity-management specialists highlight that composable adopters ship new features 80% faster, translating into quicker response to customer feedback. Niche marketplaces surface in sectors where regulatory or technical depth deters generalist platforms, for instance, medical implants or specialized chemicals.

White-space is evident in cross-border enablement, where tariff navigation and landed-cost transparency remain pain points. Integrated payment and logistics bundles are expected to gain traction, particularly among SMB exporters. Strategic acquisitions, such as RS Group’s purchase of Distrelec and Risoul, illustrate a trend toward capability consolidation to accelerate digital reach. Overall, the competitive outlook favors firms capable of coupling supply-chain control with data-driven customer engagement as the North America B2B e-commerce market matures.

North America B2B E-commerce Industry Leaders

Amazon.com Inc. (Amazon Business)

W.W. Grainger Inc.

Fastenal Company

MSC Industrial Supply Co.

Ferguson plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: W.W. Grainger posted USD 4.2 billion Q1 revenue, up 5.9% year-over-year, with Endless Assortment sales rising 15.1%, underscoring continued digital traction.

- April 2025: Amazon Business confirmed USD 25 billion in annual sales, noting the fastest growth among public entities and large enterprises.

- February 2025: The U.S. government imposed 25% tariffs on imports from Canada and Mexico and 10% on imports from China, prompting supply-chain realignment.

- January 2025: RS Group closed the acquisitions of Distrelec and Risoul, lifting digital-channel revenue contribution to 61%.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study regards the North America B2B e-commerce market as the value of goods and services ordered through dedicated B2B websites or e-procurement portals by firms located in the United States, Canada, and Mexico. Orders routed via application-program interfaces, punch-out catalogs, and embedded checkout tools are included because they settle on an e-commerce rail.

Scope exclusion: Electronic Data Interchange (EDI) transactions are outside the frame.

Segmentation Overview

- By Channel

- Direct Sales

- Marketplace Sales

- By Transaction Model

- Domestic

- Cross-border

- By Payment Method

- Bank Transfers and ACH

- Credit and Debit Cards

- Other Payment Methods

- By Industry Vertical

- Manufacturing

- Retail and Wholesale

- Healthcare and Life Sciences

- Automotive

- Construction and Building Materials

- Other Industry Verticals

- By Geography

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

We interviewed procurement directors in mid-sized manufacturing plants, marketplace operators, logistics integrators in Mexico, and senior bankers handling B2B payment rails across the three countries. These discussions validated digital adoption rates, average selling prices, and cross-border frictions, while regional online surveys clarified buyer frequency patterns.

Desk Research

Mordor analysts gathered baseline inputs from tier-1 public sources such as the U.S. Census Bureau's quarterly e-shipments tables, Statistics Canada's Digital Economy surveys, Banco de México cross-border payment data, UN Comtrade trade flows, and policy notes issued under USMCA. Company filings, investor presentations, and respected trade bodies like the National Association of Wholesaler-Distributors helped us chart channel mix and industry shift. Paid databases, D&B Hoovers for supplier revenues and Dow Jones Factiva for large GMV announcements, supplied firm-level clues. Customs dashboards from Volza, ACH volume statistics from NACHA, and patent landscaping through Questel revealed adoption hotspots and fintech enablers, giving the desk phase depth. The list above is illustrative only; many other public and subscription resources fed into our evidence stack.

Market-Sizing & Forecasting

A top-down construct converts official manufacturing and wholesale sales into an online pool by applying industry-specific penetration ratios that trend with our Digital Maturity Index, ACH ticket sizes, and marketplace share. Results are then challenged through selective bottom-up checks, direct GMV disclosures from leading platforms, sampled ASP × order counts, and channel partner roll-ups to smooth obvious gaps. Multivariate regression captures the influence of variables such as internet bandwidth costs, corporate card issuance, supplier directory traffic, and cross-border duty shifts before projecting through 2030. Top-down and bottom-up values converge after iterative adjustments when variance falls below three percent.

Data Validation & Update Cycle

Output is stress-tested through anomaly scans, year-on-year change caps, and peer review by a second analyst. Any divergence above preset thresholds triggers re-contact with sources. Reports refresh annually, with mid-cycle revisions when policy or macro shocks materially alter demand.

Why Mordor's North America B2B E-Commerce Baseline commands trust

Published estimates differ because firms pick unique cut-off geographies, channels, and refresh cadences. Our disciplined scope, country trio coverage, and exclusion of EDI make the numbers directly comparable with digital-only invoices, which some publishers blend with offline trade, inflating or deflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.17 T | Mordor Intelligence | - |

| USD 1.48 T | Regional Consultancy A | Omits Mexico and counts only five supply categories, narrowing revenue base |

| USD 2.50 T | Global Consultancy A | Mixes EDI with portal sales and uses 2023 penetration frozen for full forecast |

| USD 4.79 T | Trade Journal B | Relies on manufacturer e-shipment ratios, excludes marketplace GMV, undercounts service verticals |

The comparison shows how differing inclusions, data vintages, and validation rigor create wide gaps. By anchoring on transparent variables, refreshed annually, Mordor Intelligence delivers a balanced, repeatable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the North America B2B e-commerce market?

The market is valued at USD 6.14 trillion in 2026 and is projected to reach USD 14.49 trillion by 2031.

Which sales channel is growing fastest within the market?

B2B marketplaces are expanding at a 20.95% CAGR, outpacing direct e-commerce channels.

How important is cross-border trade to market growth?

Cross-border transactions are forecast to grow at 19.88% CAGR to 2031, driven by USMCA provisions and logistics digitization.

Why are alternative payment methods gaining traction?

Embedded-finance, BNPL, and digital wallets simplify credit management and reduce settlement friction, leading to a 21.75% CAGR for alternative payments.

Which industry vertical is expected to grow quickest?

Healthcare and life sciences are projected to register a 22.35% CAGR as specialized platforms address regulatory and workflow needs.

What are the main restraints limiting market expansion?

Cyber-attacks paired with data-sovereignty litigation and fragmented payment rails for extended credit terms collectively reduce the forecast CAGR by nearly 7 percentage points.

Page last updated on: