United States Electronics And Appliance Stores Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

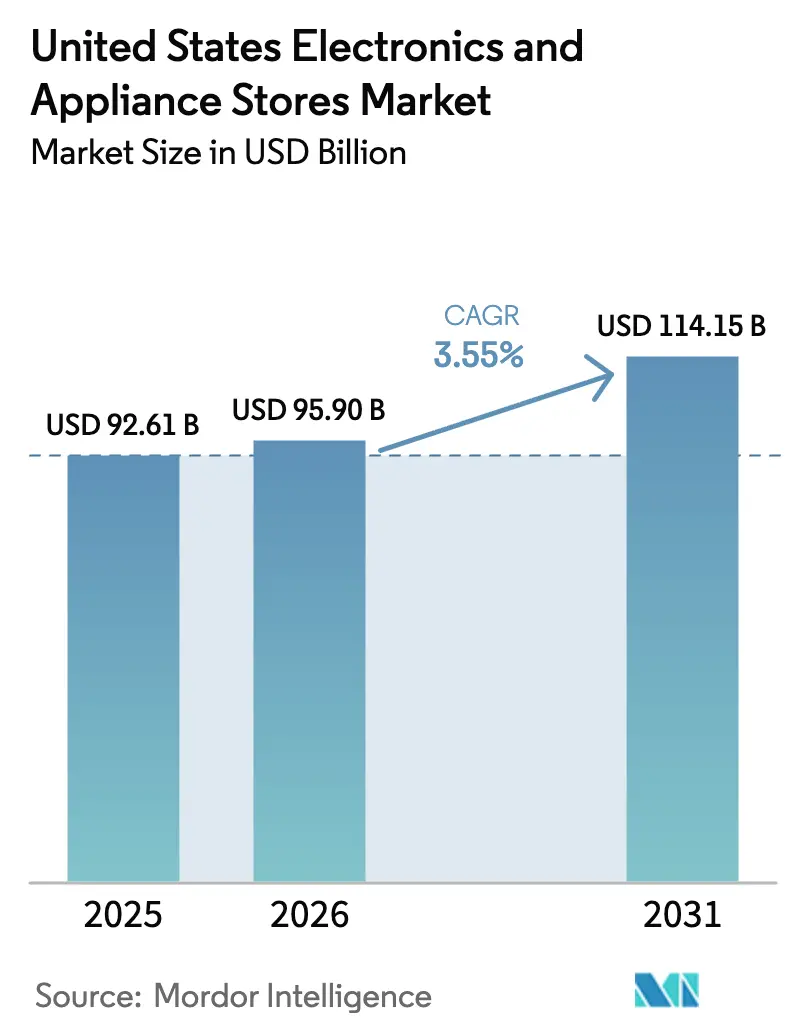

| Base Year Market Size (2025) | USD 92.61 Billion |

| Market Size (2026) | USD 95.9 Billion |

| Market Size (2031) | USD 114.15 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

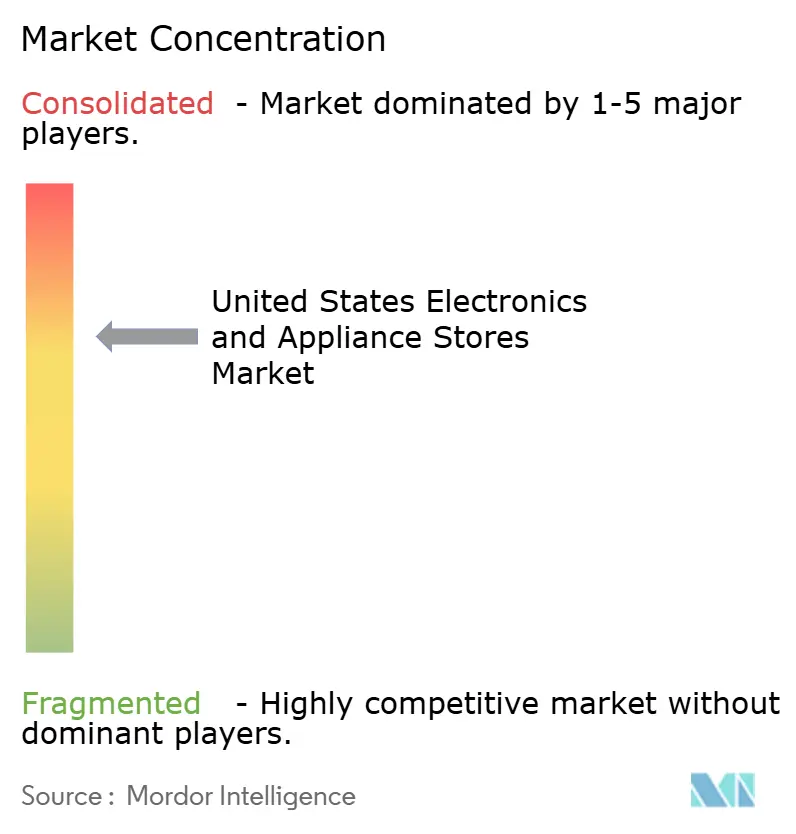

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Electronics And Appliance Stores Market Analysis by Mordor Intelligence

The US electronics and appliance stores market size was valued at USD 92.61 billion in 2025 and estimated to grow from USD 95.9 billion in 2026 to reach USD 114.15 billion by 2031, at a CAGR of 3.55% during the forecast period (2026-2031). This moderate yet steady trajectory followed a volatile pandemic period and is anchored in rising demand for connected, energy-efficient products, catalyzed by the Inflation Reduction Act’s USD 8.8 billion home-energy rebate pool. While remodeling spending declined 7% to USD 449 billion in 2024, it remained well above pre-pandemic baselines, ensuring a robust replacement cycle. Concurrently, housing starts are projected to reach 1.01 million single-family units in 2025, further sustaining appliance sales.[1]National Association of Home Builders, “A Slight Rise in Single-Family Starts as Economic Uncertainty Persists,” nahb.org Channel dynamics show in-store sales preserving a 71.5% share in 2024, but online pure-play platforms are expanding at a 5.1% CAGR as buy-now-pay-later adoption lifts both purchase incidence and basket value.

Key Report Takeaways

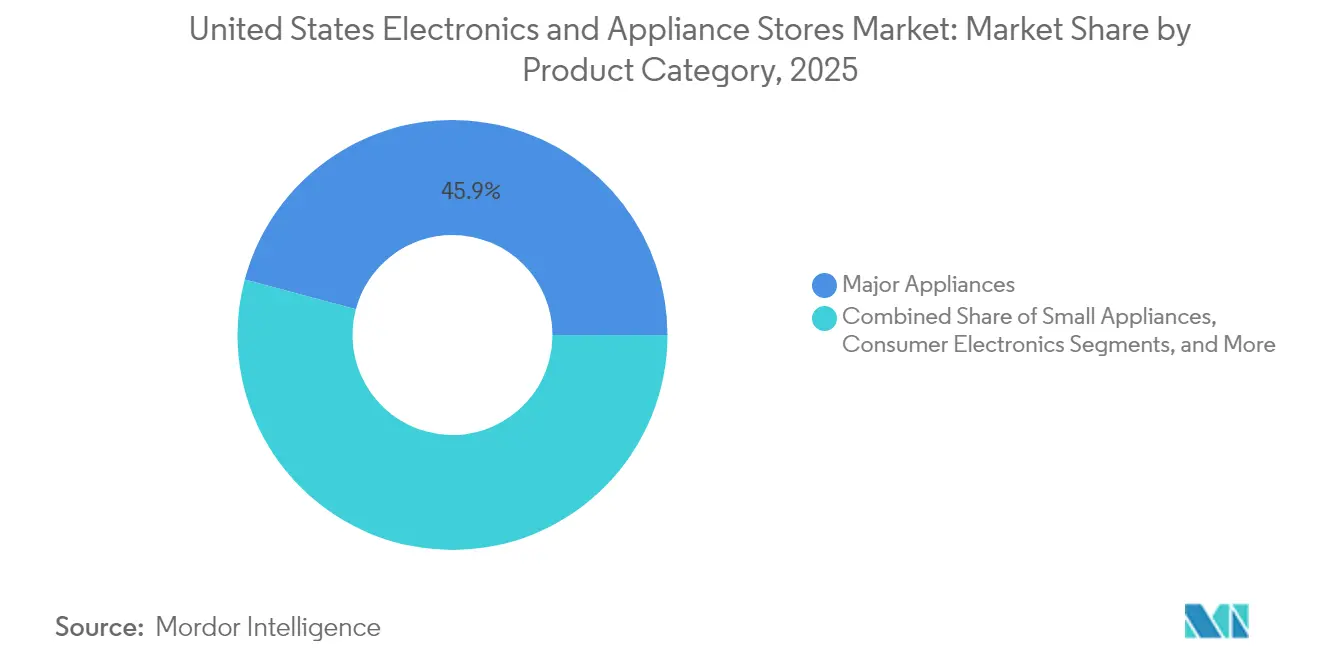

- By product category, Major Appliances held 45.85% of the US electronics and appliance stores market share in 2025, while Smart Home Devices are advancing at a 5.2% CAGR through 2031.

- By store type, Big-Box Retailers led with 51.95% revenue share in 2025; Flagship Experience Centers are forecast to expand at a 4.3% CAGR.

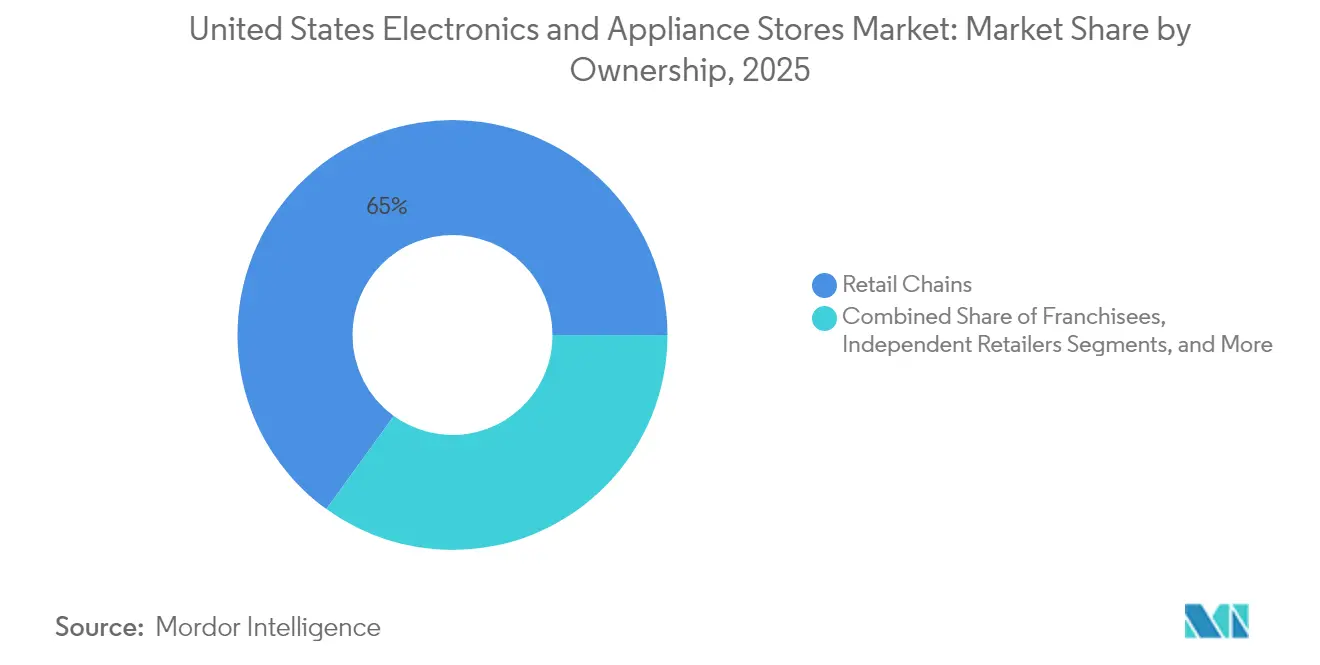

- By ownership structure, Retail Chains accounted for 65.02% of the US electronics and appliance stores market size in 2025; Manufacturer-Branded Stores are growing at a 4.2% CAGR.

- By sales channel, in-store transactions captured 70.85% share in 2025, whereas Online Pure-Play platforms are rising at 4.8% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Electronics And Appliance Stores Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in premium smart-appliance adoption | +0.8% | National, with early gains in metropolitan areas | Medium term (2-4 years) |

| Housing starts and remodeling uptrend | +0.6% | National, concentrated in Sun Belt states | Long term (≥ 4 years) |

| Omnichannel retail model expansion | +0.5% | National, with urban-suburban differentiation | Short term (≤ 2 years) |

| Inflation Reduction Act high-efficiency rebates | +0.4% | National, with state-specific implementation | Medium term (2-4 years) |

| Private-label appliance proliferation | +0.3% | National, with big-box retailer concentration | Long term (≥ 4 years) |

| Turn-key installation and service bundles | +0.2% | National, with a professional contractor focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Premium Smart-Appliance Adoption

Heightened consumer focus on connectivity and energy savings pushed smart products to the forefront, allowing premium price points to hold despite inflation. Matter-enabled platforms from BSH and peers addressed interoperability barriers, accelerating adoption among tech-savvy millennials entering peak home-buying years. Manufacturers widened smart feature penetration to offset semiconductor input cost escalation, creating scale efficiencies that lowered unit costs. These factors combined to lift premium segment resilience, with discretionary outlays shifting toward devices promising predictive maintenance and lower utility bills.

Housing Starts and Remodeling Uptrend

Although overall remodeling outlays slipped in 2024, they still hovered at USD 449 billion—well above pre-2020 levels—supporting steady appliance replacement. Forecast single-family starts of 1.01 million units in 2025 underscore sustained structural demand, especially in Sun Belt states where population inflows and corporate relocations spur new construction. High mortgage rates encouraged existing homeowners to refurbish rather than relocate, redirecting capital toward ENERGY STAR-certified models that satisfy evolving building-code requirements.

Omnichannel Retail Model Expansion

Retailers integrated online, mobile, and physical touchpoints to improve conversion. Best Buy’s turnaround showcased the value of click-and-collect and AR-enhanced apps that let shoppers visualize appliances, curbing returns. Lowe’s debut of a third-party marketplace expanded assortment without inventory risk. Home Depot leveraged AI for predictive stocking, turning stores into experience hubs that pair service with immediate fulfillment.

Inflation Reduction Act High-Efficiency Rebates

The Home Electrification and Appliance Rebates program earmarked USD 4.5 billion for efficient upgrades, granting households earning below 150% of the area median income up to USD 14,000 in combined incentives. Point-of-sale application simplifies uptake, steering consumers toward higher-margin, high-efficiency models. Early-adopter states like New York have already secured USD 158 million, accelerating local market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor and logistics bottlenecks | -0.7% | Global, with concentrated impact on smart appliances | Short term (≤ 2 years) |

| Price sensitivity amid inflation | -0.4% | National, with regional income variations | Medium term (2-4 years) |

| Stricter e-waste compliance costs | -0.3% | National, with state-specific regulations | Long term (≥ 4 years) |

| BNPL financing margin pressure | -0.2% | National, with demographic variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor and Logistics Bottlenecks

The October 2024 shutdown at North Carolina quartz mines highlighted fragile supply chains for high-purity materials essential to chips.[2]CNBC, “How a tiny town hit by Helene could upend the global semiconductor chip industry,” cnbc.com Component shortages raised smart-appliance input costs 20–30%, lengthened lead times, and forced retailers to carry excess inventory for safety stock. The geographic concentration of chip fabrication in Asia compounded risk through extended freight lanes and port congestion.

Price Sensitivity Amid Inflation

May 2025 saw appliance prices edge 0.77% higher while durable-goods CPI advanced 0.53%, squeezing discretionary budgets. Although BNPL volumes ballooned to USD 300 billion in 2023, new caps on credit card late fees to USD 8 curtailed retailer financing income. As a result, mid-tier consumers deferred upgrades, bifurcating the market into premium adopters and value-oriented buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Smart Devices Lift Premium Mix

Smart Home Devices posted the fastest CAGR at 5.2% through 2031 as households embraced connected ecosystems that integrated thermostats, lighting, and appliances. The US electronics and appliance stores market size for Smart Home Devices is projected to climb in tandem with Matter protocol rollouts that resolved compatibility concerns. Major Appliances, holding 45.85% revenue in 2025, gained from replacement demand tied to aging housing stock and IRA rebates. Small Appliances enjoyed tailwinds from urban living’s need for compact multifunction units spotlighted at IFA 2024. Consumer Electronics lagged due to lengthening replacement cycles and a 2% overall tech-sales decline in 2024.

Manufacturers used AI-driven predictive maintenance to differentiate refrigerators and washing machines, encouraging service-bundle sales. Energy-efficient heat-pump water heaters became rebate magnets, exemplified by New Hampshire’s USD 1,750 incentives. In parallel, semiconductor scarcity prompted OEMs to prioritize premium SKUs to preserve margins, indirectly supporting the smart segment’s ascendancy inside the broader US electronics and appliance stores market.

By Store Type: Experience Centers Redefine Engagement

Flagship Experience Centers grew at a 4.3% CAGR, propelled by BSH’s 14,847 sq ft Houston showroom that combines live cooking, personalized design, and after-sales consultation. These venues let consumers trial connected features, elevating confidence in complex installations. Big-Box Retailers retained a 51.95% share by leveraging logistics scale and cross-category traffic, demonstrating Home Depot’s appliance gains via exclusive brand deals.

Warehouse Clubs exploited bulk-buying economics to target value-seeking households, while Discount Outlets cleared prior-generation inventory to price-sensitive shoppers. Specialty Appliance Stores differentiated through bespoke kitchen design, but online competition pressured margins. Together, format diversity ensured wide coverage across demographic tiers, anchoring the US electronics and appliance stores market in omnichannel flexibility.

By Ownership: Brands Seek Direct Consumer Links

Retail Chains commanded 65.02% of the 2025 turnover by pooling purchasing power and national marketing. Yet, Manufacturer-Branded Stores, expanding at 4.2% CAGR, let producers control storytelling and capture retail margins. Bosch, Samsung, and LG accelerated pilot showrooms in major metros to display full connected ecosystems, strengthening loyalty.

Franchisees blended corporate branding with local agility but faced fee-related headwinds. Independent Retailers turned to buying-group partnerships for leverage, specializing in luxury built-ins and installation services. Private-equity deal-making, such as IQVentures’ USD 504 million Aaron’s acquisition, highlighted investor belief that digital transformation can unlock value in under-modernized chains. These shifts injected fresh competition into the US electronics and appliance stores market.

By Sales Channel: Digital Share Accelerates, Stores Endure

Online Pure-Play platforms rose at a 4.8% CAGR, buoyed by BNPL’s 9-point lift in purchase incidence and 10% hike in ticket size. Amazon’s 19.2% appliance dollar share underscored the power of logistics and data at scale. Still, in-store sales kept a 70.85% share as shoppers valued tactile assessment for big-ticket items.

Click-and-Collect bridged digital convenience with immediate possession, aligning inventory economics for retailers. Mobile-app AR tools reduced return rates by visualizing fit and finish, reinforcing loyalty to chains like Best Buy. The channel mosaic reflected consumer desire for flexibility, ensuring each modality remains integral to the US electronics and appliance stores market.

Geography Analysis

Sun Belt dominance persisted as Texas, Florida, and North Carolina captured the lion’s share of new-construction-driven demand. These states benefited from population inflows, favorable regulations, and land availability, funneling large appliance sales through regional big-box outlets. Metropolitan zones such as Dallas-Fort Worth and Tampa recorded above-average smart-appliance penetration due to higher household incomes and technology affinity.

The Midwest and Rust Belt exhibited slower growth but steady replacement activity. Aging housing stock required energy-efficient upgrades, and IRA rebates mitigated upfront cost anxiety. Retailers tailored assortments to budget-minded consumers by emphasizing private-label value lines. Rural regions remained underserved for premium assortments, prompting Lowe’s to extend rural product offerings across 150 stores, widening reach.

West Coast markets led in sustainability adoption. California’s early-stage rebate allocation and strict efficiency codes prompted quick uptake of ENERGY STAR-certified devices. High concentrations of technology workers in San Francisco and Seattle fostered early experimentation with AI-powered appliances. Income dispersion across the United States shaped merchandising; premium brands clustered in affluent suburbs, while discount assortments met lower-income rural and exurban needs. This geographic tapestry remained a core consideration for retailers optimizing the broader US electronics and appliance stores market.

Competitive Landscape

The structure of the US electronics and appliance stores market revealed a dual reality: Walmart and Amazon collectively held the majority of category revenue in 2024, dwarfing Best Buy’s revenue share despite its specialization. The scale of general merchandisers enabled price leadership and nationwide same-day logistics. Best Buy adapted by doubling down on membership services and experience-centric stores.

Strategic investments in professional contractors reshaped competitive moats. Home Depot’s USD 18.25 billion SRS Distribution purchase and subsequent USD 4.3 billion GMS buyout enlarged its pro-sales footprint, boosting bundled appliance installation offers. Lowe’s announced AI-enabled cost-savings targets of USD 1 billion under its Total Home Strategy. Vertical integrations continued as Walmart agreed to acquire Vizio for USD 2.3 billion, aiming to harness ad revenue through connected televisions.[4]CNBC, “Walmart to buy TV maker Vizio for USD 2.3 billion,” cnbc.com

Emerging challengers focused on direct-to-consumer and subscription maintenance. Appliance brands opened flagship showrooms to capture end-user data, while fintech partners financed service bundles. White-space opportunities lie in rural territories and e-waste collection compliance services. Competitive intensity, therefore, remained high, compelling retailers to balance price, service, and technology to sustain share inside the evolving US electronics and appliance stores market.

United States Electronics And Appliance Stores Industry Leaders

Haier

Philips

Bosch

GE Appliance

Whirlpool

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Home Depot’s SRS Distribution subsidiary agreed to acquire GMS for USD 4.3 billion, bolstering reach among professional contractors.

- February 2025: BSH opened its eighth Experience and Design Center in Houston, a 14,847 sq ft immersive showroom for Bosch, Thermador, and Gaggenau brands.

- December 2024: Lowe’s unveiled its 2025 Total Home Strategy, including 10–15 new stores annually and the sector’s first product marketplace.

- November 2024: Bose bought McIntosh Group to deepen access to the USD 2.8 billion luxury-audio niche.

United States Electronics And Appliance Stores Market Report Scope

Stores that sell appliances and electronics to end consumers from fixed point-of-sale locations are known as electronics and appliance stores. The premises where electronics and appliance stores are normally run include space for floor displays and electricity to power product demonstrations.

The United States Electronics And Appliance Stores Market Is Segmented By Type (Hardware Suppliers, Security Stores, Consumer Electronics Stores), By Ownership (Retail Chain, Independent Retailer), And By Type Of Store (Exclusive Retailers/Showrooms, Inclusive Retailers/Dealer Stores, Online). The Report Offers Market Size And Forecasts For The United States Electronics And Appliance Stores Market In Volume (Number Of Stores) And Value (USD) For All The Above Segments.

| Major Appliances |

| Small Appliances |

| Consumer Electronics |

| Smart Home Devices |

| Big-Box Retailers |

| Specialty Appliance Stores |

| Flagship Experience Centers |

| Warehouse Clubs |

| Discount Outlets |

| Retail Chains |

| Franchisees |

| Independent Retailers |

| Manufacturer-Branded Stores |

| In-Store Sales |

| Click-and-Collect |

| Online Pure-Play Platforms |

| Mobile App |

| By Product Category | Major Appliances |

| Small Appliances | |

| Consumer Electronics | |

| Smart Home Devices | |

| By Store Type | Big-Box Retailers |

| Specialty Appliance Stores | |

| Flagship Experience Centers | |

| Warehouse Clubs | |

| Discount Outlets | |

| By Ownership | Retail Chains |

| Franchisees | |

| Independent Retailers | |

| Manufacturer-Branded Stores | |

| By Sales Channel | In-Store Sales |

| Click-and-Collect | |

| Online Pure-Play Platforms | |

| Mobile App |

Key Questions Answered in the Report

What is the current size of the US electronics and appliance stores market?

The US electronics and appliance stores market size reached USD 95.9 billion in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 3.55% CAGR, touching USD 114.15 billion by 2031.

Which segment is growing the fastest?

Smart Home Devices lead with a 5.2% CAGR through 2031 as consumers adopt connected, energy-efficient products.

How do federal rebates influence demand?

The Inflation Reduction Act offers up to USD 14,000 per household for efficient upgrades, channeling purchases toward premium appliances and supporting long-term growth.

What risks could slow market expansion?

Persistent semiconductor shortages and heightened price sensitivity amid inflation could trim the growth trajectory by roughly 1.1 percentage points combined.

Page last updated on: