Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The United States Integrated Circuits Market is Segmented by IC Type (Analog IC, Logic IC, Memory IC, and and Microcomponents), Process Node (≤7 Nm, 10–16 Nm, 22–28 Nm, 45–65 Nm, and >65 Nm), Wafer Size (300 Mm, 200 Mm, and 150 Mm and Below), and End-User Industry (Consumer Electronics, Automotive and EVs, IT and Telecommunications, Industrial Automation and Robotics, Aerospace and Defense, and Healthcare and Medical Devices).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

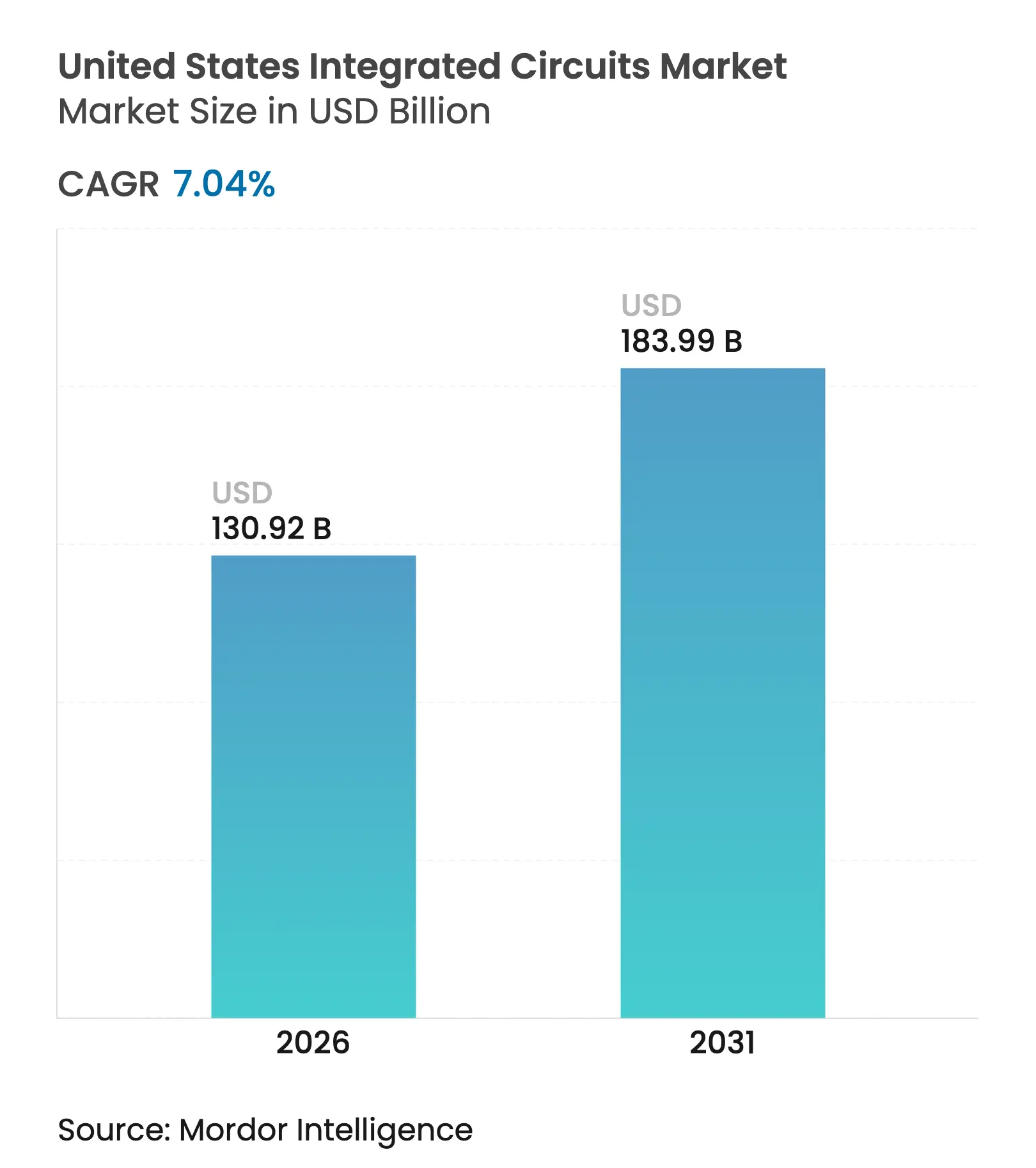

| Market Size (2026) | USD 130.92 Billion |

| Market Size (2031) | USD 183.99 Billion |

| Growth Rate (2026 - 2031) | 7.04 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The United States integrated circuits market size in 2026 is estimated at USD 130.92 billion, growing from 2025 value of USD 122.31 billion with 2031 projections showing USD 183.99 billion, growing at 7.04% CAGR over 2026-2031. This expansion stemmed from federal incentives that unlocked USD 450 billion in private-sector capacity commitments, surging demand for artificial-intelligence hardware, and renewed attention to supply-chain security. Manufacturers broadened domestic footprints to secure long-term tax credits and streamlined access to advanced manufacturing equipment, while cloud providers forged direct silicon partnerships that shortened design cycles and raised foundry utilization. Mature process nodes retained volume leadership, but aggressive node migrations at 7 nm and below realigned capital toward EUV lithography, triggering the largest equipment spending cycle since 2020. Strong tailwinds from vehicle electrification, trusted-foundry mandates in aerospace, and 5G/6G rollouts further diversified the revenue base and limited cyclicality. Heightened regulatory compliance, talent shortages near new fabs, and export-control uncertainty moderated growth yet did not derail planned investments.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Federal CHIPS and Science Act-Fuelled Capacity Expansion

Federal CHIPS and Science Act-Fuelled Capacity Expansion

| +2.1% | National, concentrated in Arizona, Texas, and Ohio | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

National, concentrated in Arizona, Texas, and Ohio

|

Impact Timeline

:

Long term (≥ 4 years)

|

Surging AI and HPC Data-Center Chip Demand from U.S. Cloud

Titans

Surging AI and HPC Data-Center Chip Demand from U.S. Cloud

Titans

| +1.8% | National, with clusters in California, Washington, and Virginia | Medium term (2-4 years) | |||

Electric-Vehicle Powertrain Shift Accelerating SiC and GaN

IC Adoption

Electric-Vehicle Powertrain Shift Accelerating SiC and GaN

IC Adoption

| +1.3% | National, with automotive hubs in Michigan, Tennessee, Texas | Medium term (2-4 years) | |||

Defense and Aerospace Secure-Microelectronics Mandates

Defense and Aerospace Secure-Microelectronics Mandates

| +0.9% | National, concentrated in defense contractor regions | Long term (≥ 4 years) | |||

5G/6G Roll-Out Catalysing U.S. RF Front-End IC Production

5G/6G Roll-Out Catalysing U.S. RF Front-End IC Production

| +0.7% | National, with a telecom infrastructure focus | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Federal CHIPS and Science Act-fuelled capacity expansion

The 2022-enacted statute encouraged more than USD 450 billion of fab announcements across 18 projects slated to break ground in 2025, including TSMC’s USD 165 billion Arizona campus and Intel’s USD 20 billion Ohio complex. Treasury rules provided 25% investment credits that lowered payback periods for advanced packaging and 2.5D/3D integration, reversing decades of offshore migration and clustering ecosystems around Phoenix, Austin, and Columbus.[1]U.S. Department of the Treasury, “U.S. Department of the Treasury Releases Final Rules to Strengthen U.S. Semiconductor Industry,” home.treasury.gov

Surging AI and HPC data-center chip demand

Cloud hyperscalers tripled demand for high-bandwidth memory, sending Micron’s HBM revenue past USD 1 billion in Q2 2025. Short supply of advanced packaging lines spurred Korean and Taiwanese foundries to localize 2 nm GAA plus 2.5D chiplet solutions for US customers, deepening direct supplier-client linkages that bypassed traditional fabless intermediaries.

Electric-vehicle powertrain shift accelerating SiC and GaN IC adoption

Wide-bandgap devices improved efficiency in traction inverters, prompting long-term supply contracts such as onsemi’s multi-year EliteSiC pact with Volkswagen Group, which also triggered a Czech wafer-expansion blueprint. Automotive qualification cycles and substrate scarcity spurred vertical integration, with U.S. fabs adding 200 mm SiC lines near Detroit and Chattanooga to shorten logistics.

Defense and aerospace secure-microelectronics mandates

DoD acquisition rules issued in 2024 barred specified Chinese chips, channeling classified programs toward trusted domestic foundries operated by Intel and BAE Systems. The policy expanded beyond missiles and satellites into critical infrastructure, generating steady, low-volume demand for anti-tamper logic and radiation-hardened memory.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Acute Fab-Level Talent Shortage in Key U.S. Hubs

Acute Fab-Level Talent Shortage in Key U.S. Hubs

| -1.4% | Arizona, Texas, Ohio | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Arizona, Texas, Ohio

|

Impact Timeline

:

Short term (≤ 2 years)

|

Escalating Environmental Compliance Costs in High-Regulation

States

Escalating Environmental Compliance Costs in High-Regulation

States

| -0.8% | California, New York | Medium term (2-4 years) | |||

Cap-Ex Intensity and Long Pay-Back Periods Limiting

Smaller Fabs' Entries

Cap-Ex Intensity and Long Pay-Back Periods Limiting

Smaller Fabs' Entries

| -0.6% | National | Long term (≥ 4 years) | |||

Export-Control Uncertainty on Advanced EUV/DUV Tools

Impacting Node Migration

Export-Control Uncertainty on Advanced EUV/DUV Tools

Impacting Node Migration

| -0.5% | National, affecting advanced node fabs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Acute fab-level talent shortage in key hubs

The United States integrated circuits market faced projections of a 67,000-70,000 worker gap by 2030, concentrated near new fabs in Arizona, Texas, and Ohio. Micron responded by forming a Minority Serving Institution Semiconductor Network spanning 15 colleges, yet technician lead-times of 18-24 months outpaced construction schedules.[2]Micron Technology, “Micron Expands Workforce Development Collaborations to Meet Future Semiconductor Job Demand,” micron.com Wage inflation ran 20-30% for critical skill sets, adding to operating costs.

Escalating environmental compliance costs in high-regulation states

California’s updated air-quality rules and PFAS restrictions lifted new-fab spending by USD 50-100 million per project, while NIST filtration guidelines raised clean-room capital by 15-20%. These burdens steered several expansion projects toward Arizona and Texas, where compliance regimes were less costly, even though water-stress considerations required further investment in reclamation systems.

By IC Type: Memory leadership in AI workloads

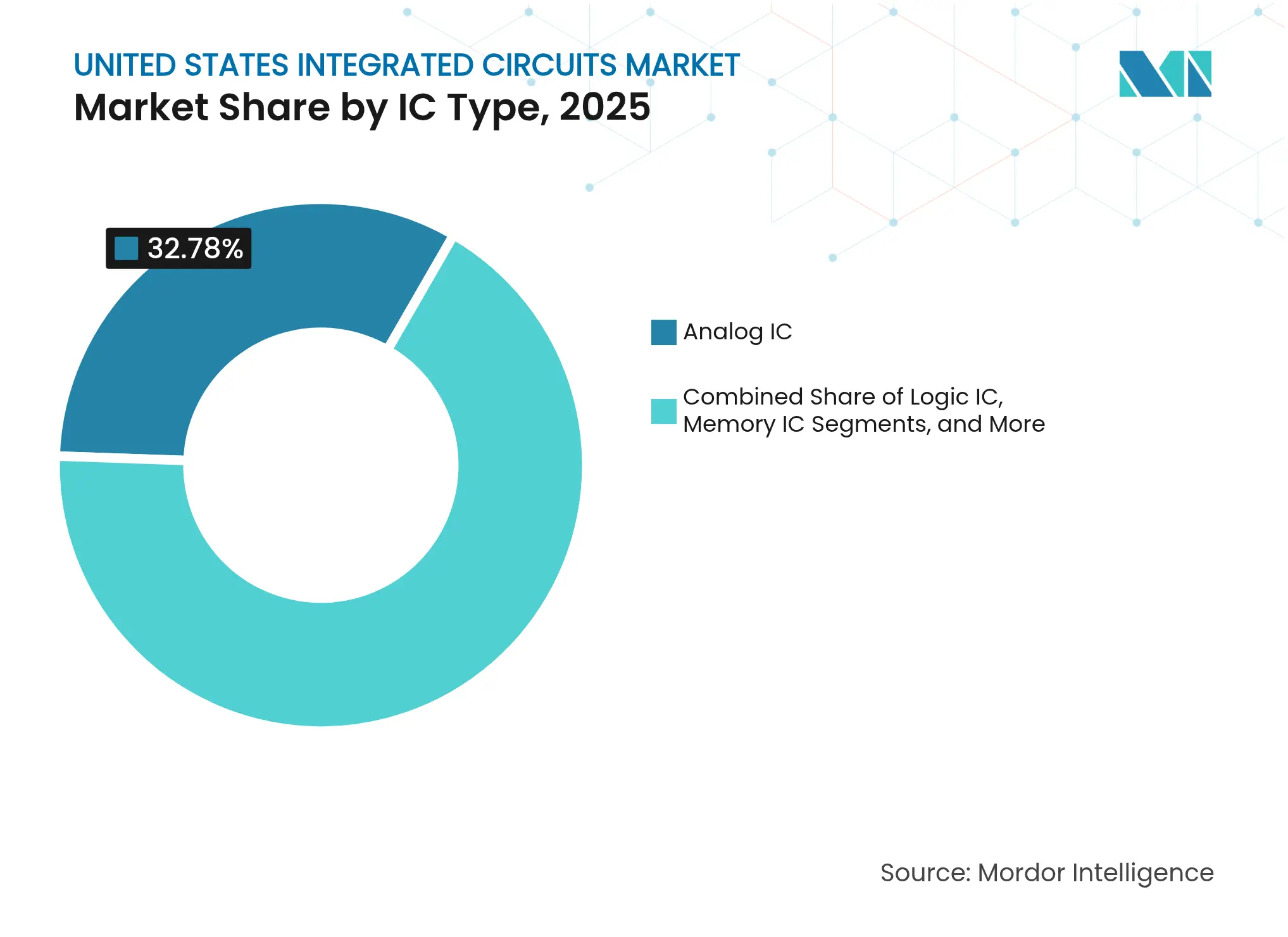

Memory devices recorded a 10.32% CAGR forecast between 2026-2031, eclipsing all other categories as AI accelerators demanded stacked HBM and lower-power LPDDR solutions. Analog ICs nonetheless controlled the largest slice of the United States integrated circuits market at 32.78% in 2025. Logic and microcomponent revenue followed, supported by embedded applications in industrial control and automotive safety.

Micron’s USD 1 billion HBM sales in Q2 2025 underscored the widening monetization window for bandwidth-hungry data centers. Continuous investment in 2.5D stack technology differentiated suppliers that could deliver through-silicon-via interposers at scale. In contrast, microcontrollers saw incremental gains as OEMs shifted toward integrated domain controllers that consolidated discrete chips.

Note: Segment shares of all individual segments available upon report purchase

By Process Node: Leadership competition intensifies

Nodes at 7 nm and below are forecast to compound at 10.18% CAGR as the principal battleground for performance-per-watt leadership, even though >65 nm remained 44.88% of shipments in 2025. Intel disclosed 18A tape‐outs for external customers, signaling intent to match TSMC and Samsung at the frontier.

High-NA EUV systems priced at USD 360 million created high entry barriers that only a handful of players could cross, reinforcing oligopoly dynamics. Export-control rules on EUV gear further tightened supply, making domestic tool procurement a strategic priority for U.S. fabs. Mature 28 nm and 45 nm nodes sustained automotive and industrial portfolios where redesign costs outweighed performance gains.

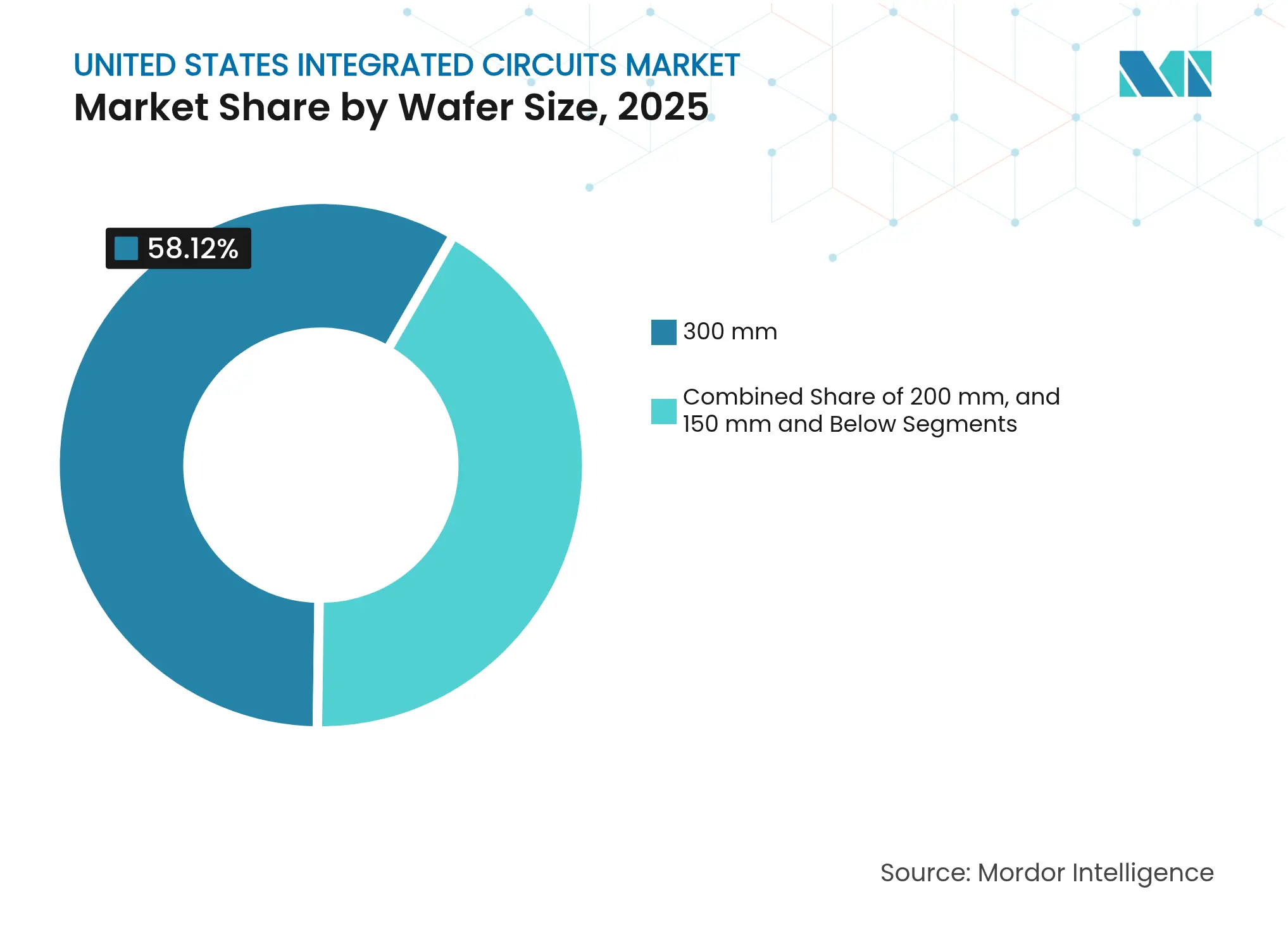

By Wafer Size: 300 mm scale advantage strengthens

The 300 mm format captured 58.12% of the United States integrated circuits market in 2025 and is forecast to grow 9.05% CAGR, buoyed by more than USD 400 billion in global equipment outlays through 2027. Eighteen fabs scheduled for 2025 start-of-construction included 15 dedicated to 300 mm, highlighting the unbroken appeal of larger substrates.

Memory and logic vendors prioritized 300 mm for cost-per-die efficiency, whereas analog and compound-semiconductor firms preserved 200 mm assets to serve lower-volume, higher-margin lines. Equipment reuse from legacy DRAM fabs partially offset capital intensity, yet new lithography, CMP, and metrology tools were still required for leading-edge conversion.

Note: Segment shares of all individual segments available upon report purchase

By End-user Industry: Automotive electrification overtakes consumer dominance

Consumer electronics held 34.72% of the United States integrated circuits market share in 2025 as smartphones, wearables, and gaming consoles continued to absorb high volumes of mixed-signal and power-management chips. Automotive and electric-vehicle applications are now the fastest-expanding user segment, with a 12.34% CAGR projected through 2031 as traction inverters, battery-management systems, and ADAS domains require wider band-gap semiconductors and domain controllers. IT and telecommunications customers—principally hyperscale data-center operators and 5G infrastructure builders—boost present-day uptake of AI accelerators and high-bandwidth memory, accelerating the shift toward advanced packaging in the United States integrated circuits market. The industrial automation and robotics arena continues to specify rugged microcontrollers and real-time processors that optimize factory throughput, reinforcing resilient demand across mature 45-65 nm nodes where cost advantages remain decisive. Collectively, these dynamics keep the consumer sector in pole position but signal a structural pivot toward mobility, cloud, and industrial platforms that demand higher semiconductor content per unit.

Defense, aerospace, and critical-infrastructure buyers intensified sourcing from trusted domestic fabs after 2024 security mandates, generating long-tail demand for radiation-hardened logic and secure memory that carry margin premiums over commercial devices. Healthcare and medical devices added a complementary growth vector, as wireless monitoring systems advanced at a 12% CAGR and the microchip-implants niche was projected to reach USD 27 billion by 2028, expanding the addressable United States integrated circuits market size for biocompatible, ultra-low-power designs. Aerospace innovators such as Honeywell adopted NXP’s high-performance MCU platforms for autonomous flight, underscoring how mixed-criticality avionics elevate demand for deterministic processing and advanced security features. Industrial end users, meanwhile, upgraded legacy PLCs and sensor networks to AI-enabled edge controllers, lifting attach rates for embedded DRAM and secure connectivity ICs. As these verticals mature, a diversified customer mix cushions cyclical swings in consumer devices and anchors long-term revenue visibility across the broader United States integrated circuits industry.

California, Arizona, and Washington historically anchored design and manufacturing activity, with Silicon Valley retaining R&D leadership and Phoenix evolving into the nation’s largest next-generation fab corridor after TSMC’s USD 65 billion phase-two commitment. Texas became a parallel powerhouse as Samsung expanded its Austin footprint and GlobalFoundries upgraded legacy lines in the state’s technology triangle.

Midwestern and Northeastern states rose quickly under CHIPS Act incentives. Ohio secured Intel’s USD 20 billion first-phase campus and lobbied for future modules that could lift aggregate spending to USD 100 billion over 10 years. Upstate New York welcomed Micron’s USD 50 billion dynamic-random-access-memory megaproject, reviving a region that lost share during the 2010s offshoring wave.

Defense and aerospace priorities reshaped regional allocations. Virginia’s proximity to federal agencies created stable demand for secure microelectronics, while Colorado’s satellite cluster spurred niche opportunities in radiation-hardened logic. These patterns illustrated how the United States integrated circuits market aligned capacity not only with cost and logistics but also with security, talent, and end-market proximity.

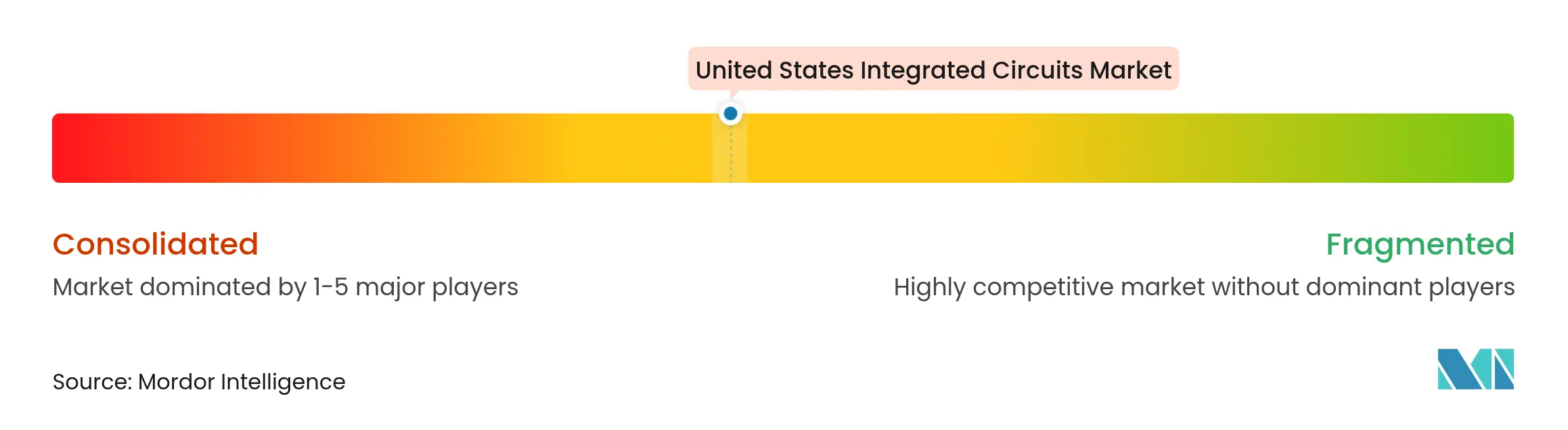

Market Concentration

The United States integrated circuits market displayed moderate concentration. Intel, TSMC, and Sasung retained scale advantages in 7 nm and smaller nodes, while Micron, Texas Instruments, and Analog Devices dominated memory and mixed-signal niches. GlobalFoundries secured long-term offtake agreements with Apple and SpaceX through its USD 16 billion re-shore program that emphasized silicon photonics and advanced packaging.[4]GlobalFoundries Inc., “GlobalFoundries Announces $16B U.S. Investment to Reshore Essential Chip Manufacturing and Accelerate AI Growth,” gf.com

Technology differentiation became the prime competitive lever. Intel’s IDM 2.0 mixed internal fabs and external foundry services, positioning the company to monetize PowerVia backside delivery alongside RibbonFET transistors. Samsung countered with 2 nm gate-all-around production paired to 2.5D interposers for AI accelerators, cementing partnerships with cloud innovators. Analog players invested in SiC, GaN, and precision power-management IP that commanded margin premiums despite lower wafer volumes.

Regulatory shifts reinforced domestic players. December 2024 export-control additions restricted rivals’ access to EUV and AI accelerator IP, funneling sensitive workloads toward trusted U.S. fabs. Simultaneously, compliance costs and documentation favored incumbents with mature governance structures, widening the moat against smaller entrants.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Integrated circuits (ICs) are compact electronic devices that integrate multiple components—such as transistors, resistors, capacitors, and diodes—onto a single piece of semiconductor material, typically silicon. This integration facilitates the creation of complex circuits capable of performing various functions within a small physical footprint.

For market estimation, the revenue generated from sales of various types of integrated circuits that are used in various industries, such as consumer electronics, automotive, IT & telecommunication, manufacturing, and automation, across the United States are being tracked.

The United States integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro [microprocessor, microcontrollers, and digital signal processors]), end-user industry (consumer electronics, automotive, IT & telecommunications, and manufacturing and automation). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.