Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.32 Billion |

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 6.31 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Customs Brokerage Market Analysis by Mordor Intelligence

The US Customs Brokerage Market size is estimated at USD 5.48 billion in 2026, and is expected to reach USD 6.31 billion by 2031, at a CAGR of 2.88% during the forecast period (2026-2031).

Import volumes have normalized above pre-2020 levels, yet brokers contend with rapidly shifting tariffs, forced-labor scrutiny, and digitization mandates that compress traditional fee structures while opening new advisory revenue streams. Integrated freight forwarders bundle clearance with transportation and warehousing, capturing scale efficiencies that squeeze standalone broker margins. In parallel, digital-first platforms grow at double-digit rates as importers demand API connectivity and real-time status visibility. Nearshoring to Mexico channels more traffic through Southwest land crossings, where cross-border expertise commands a complexity premium. Automotive and electric-vehicle components lead segment acceleration as new USMCA rules elevate origin-verification and labor-value documentation requirements.

Key Report Takeaways

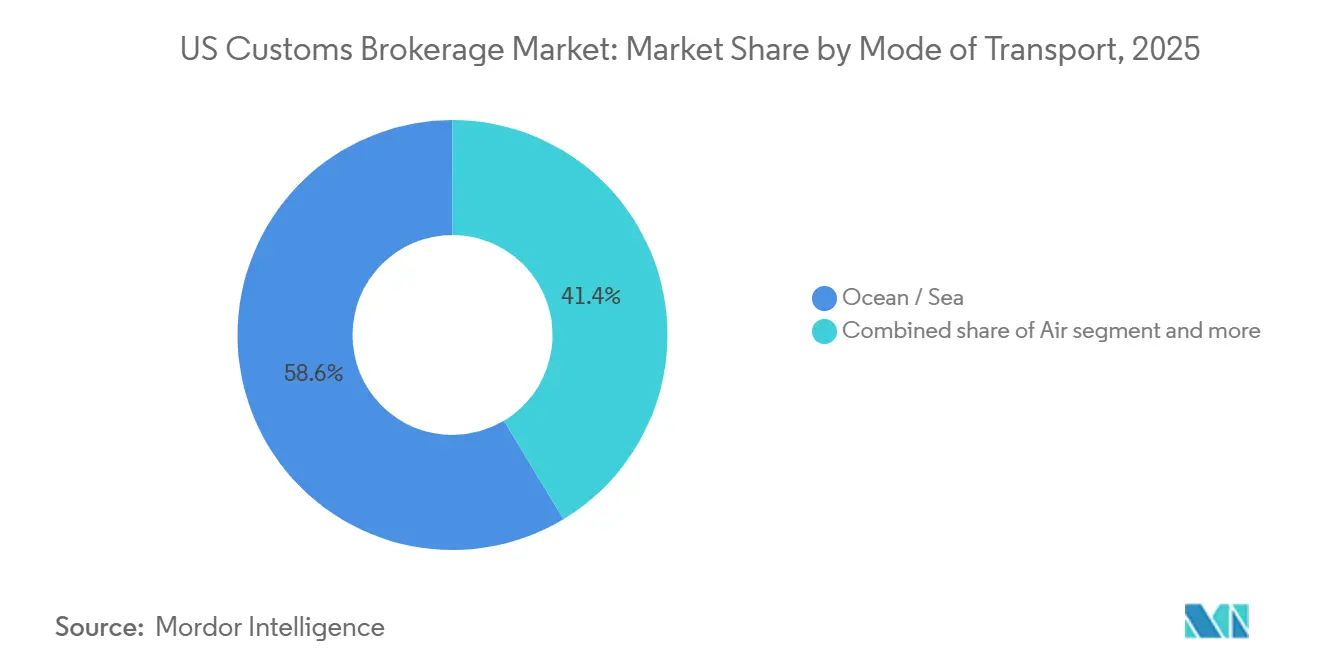

- By mode of transport, ocean freight led with 58.63% revenue share in 2025; air cargo is projected to expand at a 4.09% CAGR through 2031.

- By broker type, forwarder and 3PL-integrated operators held 65.46% of the United States customs brokerage market share in 2025, while pure customs brokers recorded the highest forecast CAGR at 3.51%.

- By importer size, large enterprises accounted for 42.69% of the United States customs brokerage market size in 2025, and SMEs/micro-shippers are advancing at a 4.72% CAGR to 2031.

- By digital adoption, traditional brokerages controlled a 77.32% share in 2025; digital-first platforms are expanding at a 10.45% CAGR.

- By end-user industry, retail and e-commerce captured 30.15% share of the United States customs brokerage market size in 2025, and automotive and EV are growing at a 5.64% CAGR.

- By geography, the West region led with 32.61% share in 2025, while the Southwest region is pacing growth at a 4.67% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Customs Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import volumes rebounding | +1.0% | National, West, Northeast | Short term (≤ 2 years) |

| Tariff and trade-agreement complexity | +0.9% | Automotive and manufacturing hubs | Medium term (2-4 years) |

| Customs digitization (ACE, PGA) | +0.7% | National, tech-forward regions | Medium term (2-4 years) |

| Rise of e-commerce micro-importers | +0.6% | Urban e-commerce hubs | Short term (≤ 2 years) |

| Monetization of ACE data | +0.5% | National | Long term (≥ 4 years) |

| 21st Century Customs Framework | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitization and Automation of Customs Processes

Automated Commercial Environment adoption stands at 98%, handling above 35 million formal entries annually. Integration with partner agencies has compressed clearance cycles from days to hours. Leading brokers deploy machine-learning classification tools that achieve more than 95% code-assignment accuracy, cutting manual touchpoints and freeing staff for advisory work[1]Avalara, “Automated Tariff Code Classification,” Avalara, avalara.com. CBP’s 2024-2028 IT roadmap earmarks USD 1.8 billion for blockchain pilots and AI-based risk scoring, further raising the technology bar for market participants.

Rise of E-commerce Micro-Importers Requiring High-Frequency Clearances

More than 400,000 US businesses imported goods in 2025, up 60% since 2019, with micro-importers representing 38% of the total. Digital brokers have responded with self-service portals and flat-fee models that appeal to entrepreneurs seeking transparent pricing. Platforms such as Amazon Global Logistics streamline cross-border fulfillment, yet many small shippers misclassify goods or overlook labeling rules, amplifying compliance risk. Brokers balancing automation with proactive education win loyalty in this dispersed client base.

Monetization of ACE Data into Value-Added Analytics Services

Large brokers leverage aggregated entry data to benchmark duty spend, identify optimization opportunities, and forecast regulatory change patterns. Proprietary dashboards visualize clearance times and PGA hold frequencies, enabling importers to fine-tune logistics strategy. Some brokers license anonymized trade-flow intelligence to third parties, creating new revenue streams that reward early investment in cloud infrastructure and data-science teams.

CBP “21st Century Customs Framework” Unlocking New Broker Roles

The framework proposes tiered broker accreditation tied to compliance history, technology integration, and data-sharing commitments. Elite status promises expedited release and lower examination rates, offering brokers a tangible competitive edge. Firms investing in supply-chain transparency tools and ESG due diligence platforms are positioning themselves to capitalize on these forthcoming benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trade-policy volatility | −0.5% | Import-dependent sectors nationwide | Short term (≤ 2 years) |

| Forced-labor and ESG compliance costs | −0.4% | China-linked supply chains | Medium term (2-4 years) |

| Shortage of licensed brokers | −0.7% | Specialized niches | Long term (≥ 4 years) |

| DIY self-filing software | −0.6% | Low-value high-frequency shipments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Licensed Customs Brokers Driving Wage Inflation

The October 2025 Customs Broker License Exam posted a sub-15% pass rate, while the average broker age exceeds 43 years. Mid-level licensed professionals now command salaries 20-30% higher than 2022 levels. Smaller firms without automation budgets face service constraints as veteran staff retire.

Expansion of DIY Self-Filing Software Eroding Fee Margins

Platforms such as Flexport and Freightos price entries at USD 25-50, well below traditional broker rates[2]Flexport, “Customs Clearance Services,” Flexport, flexport.com . Routine shipments migrate to self-service channels, leaving brokers to compete on high-touch compliance work. Subscription and retainer models are gaining traction as firms seek revenue predictability in the face of transactional erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Ocean Holds Scale While Air Gains Momentum

Ocean freight held 58.63% of the United States customs brokerage market share in 2025 as importers favored cost-efficient containerized shipping[3]Port of Los Angeles, “Facts and Figures,” Port of Los Angeles, portoflosangeles.org. The United States customs brokerage market size tied to air cargo is projected to grow at a 4.09% CAGR through 2031 as e-commerce and time-sensitive industries prioritize speed. Express integrators leverage integrated clearance to shorten cycle times, while land-border truck and rail entries gain ground in the Southwest corridor.

Container reliability improvements following pandemic disruption have reinforced the ocean’s cost advantage, yet recurring labor actions and slot allocation constraints spur some shippers to shift high-value goods to air despite the premium freight cost. Brokers with multi-modal expertise are best positioned to capture clients that balance speed and cost across seasonal demand cycles.

By Broker Type: Integrated Operators Dominate as Pure-Play Brokers Specialize

Forwarder-linked and 3PL-integrated operators controlled a 65.46% share in 2025, reflecting shippers’ preference for single-invoice logistics solutions that bundle clearance, carriage, and warehousing. Pure customs brokers grew at a 3.51% CAGR as complex verticals such as FDA-regulated goods and foreign-trade-zone operations demanded specialized knowledge.

The acquisition of Livingston International by Purolator for USD 684.4 million in February 2025 underlines consolidation momentum as integrated operators seek deep compliance capabilities. Niche brokers respond by doubling down on vertical intelligence and personalized service that larger networks struggle to replicate.

By Importer Size: SMEs Accelerate While Enterprises Explore Hybrid Filing

Large enterprises captured 42.69% of the United States customs brokerage market size in 2025, supported by multi-broker panels and embedded compliance teams. SMEs and micro-shippers are registering a 4.72% CAGR due to accessible digital-broker offerings and cross-border e-commerce programs.

Volume discounts enable corporates to negotiate aggressive fee schedules, placing margin pressure on brokers. Conversely, SMEs prioritize simplicity and education, rewarding brokers that provide intuitive portals and transparent pricing. Mid-market importers gravitate toward brokers offering a blend of cost efficiency and subject-matter expertise without enterprise-level overhead.

By Digital Adoption: API Brokerage Disrupts Legacy Workflows

Traditional brokerages held a 77.32% share in 2025, yet digital-first players are advancing at a 10.45% CAGR as importers integrate clearance data with ERP and e-commerce systems. The United States customs brokerage market size attributable to digital-only platforms is expected to triple by 2031 if current adoption trends persist.

Legacy firms accelerate technology upgrades to protect share, investing in robotic process automation and cloud-native SaaS tools. Those that succeed blend decades of regulatory know-how with modern data architectures, delivering a hybrid value proposition that resonates with risk-averse shippers.

By End-use Industry: Retail Leads, Automotive & EV Sets the Pace

Retail and e-commerce accounted for 30.15% of the United States customs brokerage market size in 2025, fueled by high-frequency parcel imports. Automotive and EV posted the fastest CAGR at 5.64% as battery and component shipments surged under USMCA rules.

Electronics and semiconductors gain momentum on the back of CHIPS Act incentives, while life-science imports require premium FDA documentation that lifts brokerage revenue per entry. Brokers with automotive rule-of-origin specialists and battery compliance expertise are well placed to ride the sector’s uptrend through 2031.

Geography Analysis

The West handled 32.61% of 2025 brokerage revenue through mega ports in Los Angeles, Long Beach, Oakland, and Seattle. Proximity to Asian suppliers and established drayage ecosystems support scale advantages, yet importers diversify to Gulf and East Coast gateways to mitigate labor disruption and congestion risk.

The Southwest is the fastest-growing region at a 4.67% CAGR, as nearshoring to Mexico channels automotive and electronics flows through Laredo, Nogales, and El Paso. Brokers with bilingual staff and cross-border regulatory expertise command premium fees. Southbound supply chains generate offsetting export clearances that further boost transactional volume.

The Southeast leverages Panama Canal expansion and capital upgrades at Savannah and Charleston to capture discretionary cargo. The Northeast remains critical for European trade and high-value goods through the Port of New York and New Jersey, while Midwest land ports manage robust Canada trade despite transitional challenges linked to Canada’s new accounting system.

Competitive Landscape

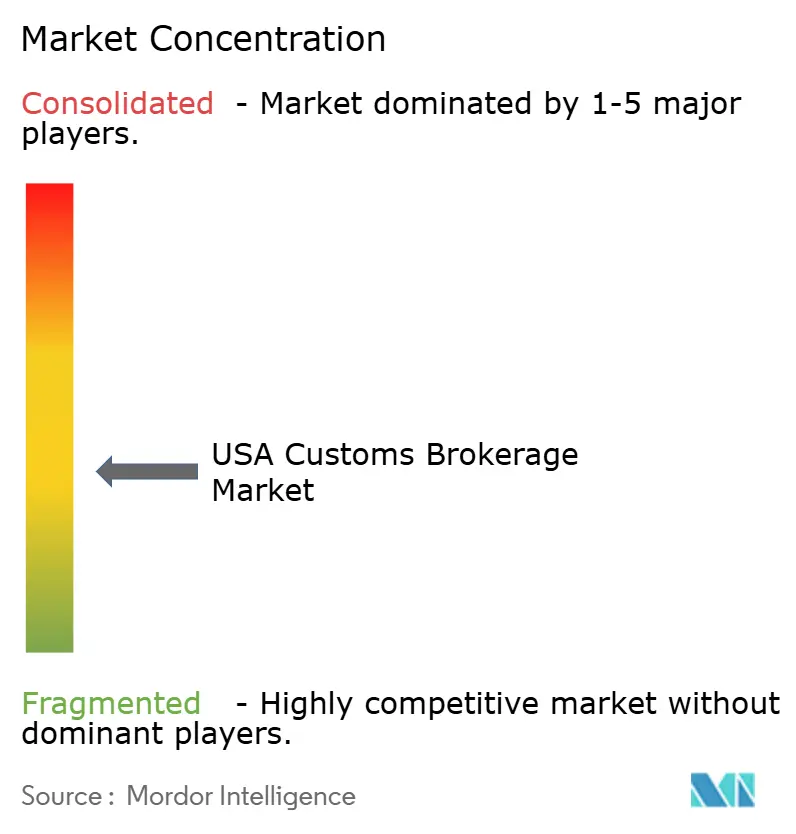

The United States customs brokerage market exhibits moderate fragmentation, with the top five firms holding 42% combined share. Consolidation is driven by technology scale ambitions as evidenced by Purolator’s Livingston takeover. C.H. Robinson reports more than 3 million shipping tasks automated via generative AI, underscoring a pivot toward digital labor[4]C.H. Robinson, “AI Shipping Tasks Milestone,” C.H. Robinson, chrobinson.com .

Leading brokers deploy AI-driven classification engines, blockchain-based origin verification, and predictive analytics dashboards to lower error rates and unlock advisory revenue. Strategic partnerships with fintechs deliver trade-credit and duty-deferral options that tie brokerage services to importer working-capital flows.

Smaller specialists defend share through vertical focus in pharmaceuticals, aerospace, and apparel that demand bespoke compliance attention. Market dynamics are coalescing around a bifurcated structure where large digitalized networks compete on price and throughput, while niche players win complex, high-margin assignments.

US Customs Brokerage Industry Leaders

FedEx Corporation

Expeditors International

C.H. Robinson

Livingston International

UPS Supply Chain Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CBP implemented the Bond Centralization Program, standardizing surety processing.

- April 2025: C.H. Robinson announced its AI platform had automated more than 3 million shipping tasks.

- March 2025: The United States imposed 25% tariffs on steel and aluminum imports effective Mar 12 2025.

- February 2025: Purolator acquired Livingston International for USD 684.4 million, expanding its clearance network.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States customs brokerage market as the total revenue earned by licensed service providers that classify goods, prepare entries, secure bonds, pay duties, and obtain U.S. Customs and Border Protection (CBP) release across ocean, air, and cross-border truck or rail flows. According to Mordor Intelligence, transloading, domestic freight forwarding, and bonded warehousing revenues are not counted, keeping the lens firmly on customs clearance itself.

Services performed purely for outbound export filings or for brokerage inside Foreign Trade Zones fall outside this market's scope.

Segmentation Overview

- By Service Type

- Customs Clearance

- Trade Compliance Advisory

- Duty Drawback & Refund Services

- Freight Forwarding-Linked Brokerage

- By Mode of Transport

- Ocean

- Air

- Truck

- Rail

- By End-user Industry

- Consumer Goods & Retail

- Automotive

- Electronics & Hi-Tech

- Agriculture & Food

- Pharmaceuticals & Healthcare

- By Client Size

- Enterprise Importers (more than $50 M annual imports)

- Mid-market Importers ($5-50 M)

- Small & Micro Importers (less than $5 M)

- By Geography

- Northeast

- Midwest

- Southeast

- Southwest

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed licensed brokers, compliance managers at large importers, and surety underwriters in Los Angeles, Laredo, New York, and Savannah. Conversations validated average entry fees, digital-filing uptake, and Section 321 parcel volumes, filling gaps that public data left open and letting us recalibrate assumptions on blended brokerage margins.

Desk Research

We began by mining open datasets such as CBP Entry Summary statistics, Bureau of Transportation Freight Flow series, U.S. Census import value tables, and USTR Section 301 duty collections, which reveal annual entry counts, shipment values, and tariff swings that shape broker workloads. Trade-association briefs from the National Customs Brokers & Forwarders Association of America and the Transportation Intermediaries Association helped us benchmark license renewals, surety bond rates, and the shrinking pool of qualified brokers. Company 10-Ks, investor decks, and port authority throughput reports then provided shipment mixes and broker fee ranges, while paid platforms including D&B Hoovers for shipper counts and Dow Jones Factiva for deal tracking offered additional financial signals. These examples are illustrative; many other sources informed the desk stage.

Market-Sizing & Forecasting

A top-down reconstruction starts with CBP entry totals by mode and applies weighted average clearance fees, adjusted for duty-refund work and post-summary corrections; selective bottom-up checks using sampled broker invoices and regional channel checks guard against over-aggregation. Key variables like de minimis threshold revisions, licensed-broker headcount, import price indices, EV-related parts inflows, and bond premium trends feed the model.

Five-year forecasts rely on multivariate regression that ties entry growth to projected U.S. goods-import elasticity, e-commerce parcel penetration, and announced port capacity additions, then cross-checks results against expert consensus on duty-rate scenarios. Any residual gaps in bottom-up samples are bridged through mode-specific penetration factors agreed during primary interviews.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags versus historic series, senior analyst peer checks, and quarterly reconfirmation calls with market participants. The report refreshes annually, with interim updates when tariff policy or port disruption materially alters entry flows.

Credibility of Our United States Customs Brokerage Baseline

Published estimates often diverge because firms apply different service mixes, fee assumptions, and refresh cadences. External 2024 values range from about USD 3.99 billion to roughly USD 5.20 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.32 B (2025) | Mordor Intelligence | - |

| USD 3.99 B (2024) | Global Consultancy A | Excludes Section 321 parcel clearances and bonded corrections |

| USD 5.20 B (2024) | Trade Journal B | Uses flat $95 entry fee, omits bond-premium surcharges |

These comparisons show that when scope misses rising parcel traffic or newer surcharge lines, totals shift noticeably. By aligning variables with CBP datasets and cross-validating fee ladders through live interviews, Mordor Intelligence delivers a balanced, transparent baseline clients can retrace and reproduce.

Key Questions Answered in the Report

How large is the United States customs brokerage market in 2026?

The United States customs brokerage market size reached USD 5.48 billion in 2026 and is projected to expand steadily through 2031.

What is the expected growth rate for customs brokerage services through 2031?

The market is forecast to grow at a 2.88% CAGR between 2026 and 2031, driven by rising import volumes and expanding advisory services.

Which broker segment is growing the fastest?

Digital-first platforms are advancing at a 10.45% CAGR as importers seek API connectivity and real-time visibility.

Why is the Southwest region the fastest growing geography?

Nearshoring to Mexico and higher USMCA trade flows are lifting clearance volumes at Southwest land ports, supporting a 4.67% CAGR.

What impact do self-filing platforms have on traditional brokers?

DIY software compresses transaction fees for routine entries, prompting brokers to pivot toward high-value compliance advisory and subscription pricing models.

Which end-user industry shows the strongest growth momentum?

Automotive and EV imports lead growth with a 5.64% CAGR due to battery component flows and stringent USMCA origin-verification rules.

Page last updated on: