United States Cryptocurrency Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

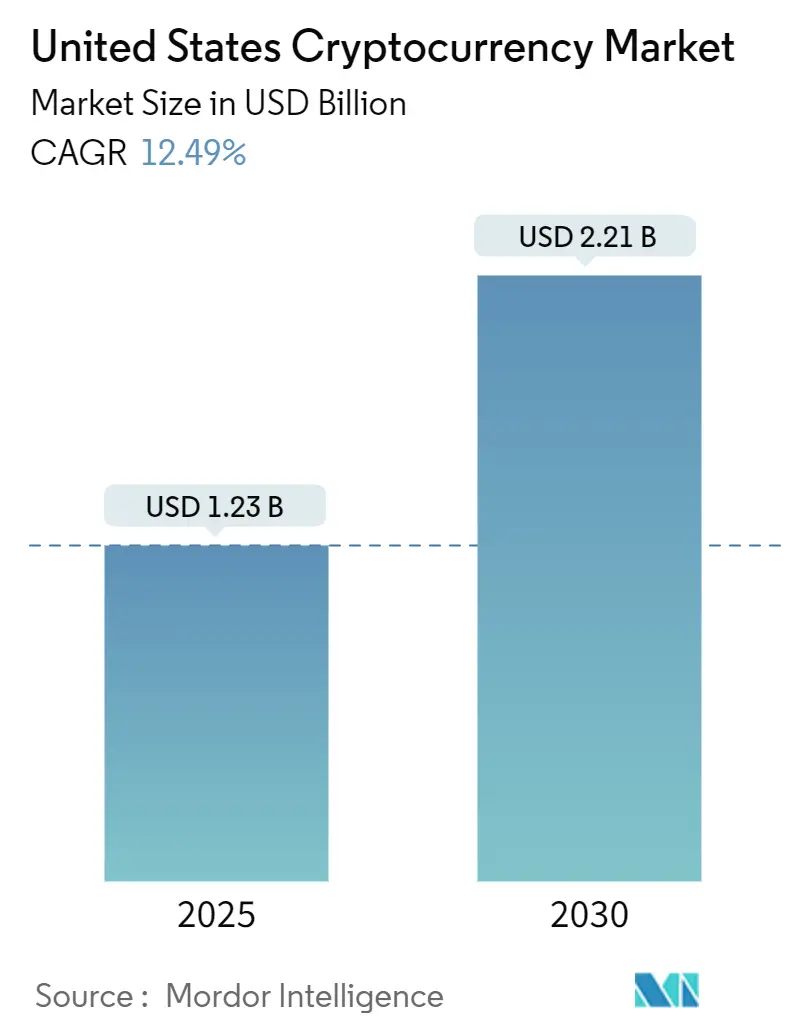

| Market Size (2025) | USD 1.23 Billion |

| Market Size (2030) | USD 2.21 Billion |

| Growth Rate (2025 - 2030) | 12.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cryptocurrency Market Analysis by Mordor Intelligence

The United States cryptocurrency market size stands at USD 1.23 billion in 2025 and is projected to reach USD 2.21 billion by 2030, reflecting a 12.49% CAGR during the forecast period. The expansion rests on three pillars: federal regulatory clarity, institutional product launches, and continued improvement in blockchain scalability. Approval of 11 spot bitcoin exchange-traded funds created a deep pool of regulated exposure, attracting USD 17.5 billion in net inflows within twelve months. Simultaneously, the Office of the Comptroller of the Currency’s 2024 letter permitting banks to offer custody services reduced operational risk for asset managers. Ethereum’s EIP-4844 upgrade reduced typical Layer-1 fees by 85%, catalyzing the development of new decentralized applications. These factors, together with robust venture funding on the West Coast and favorable mining policies in southern states, are expected to sustain double-digit growth despite near-term regulatory headwinds.

Key Report Takeaways

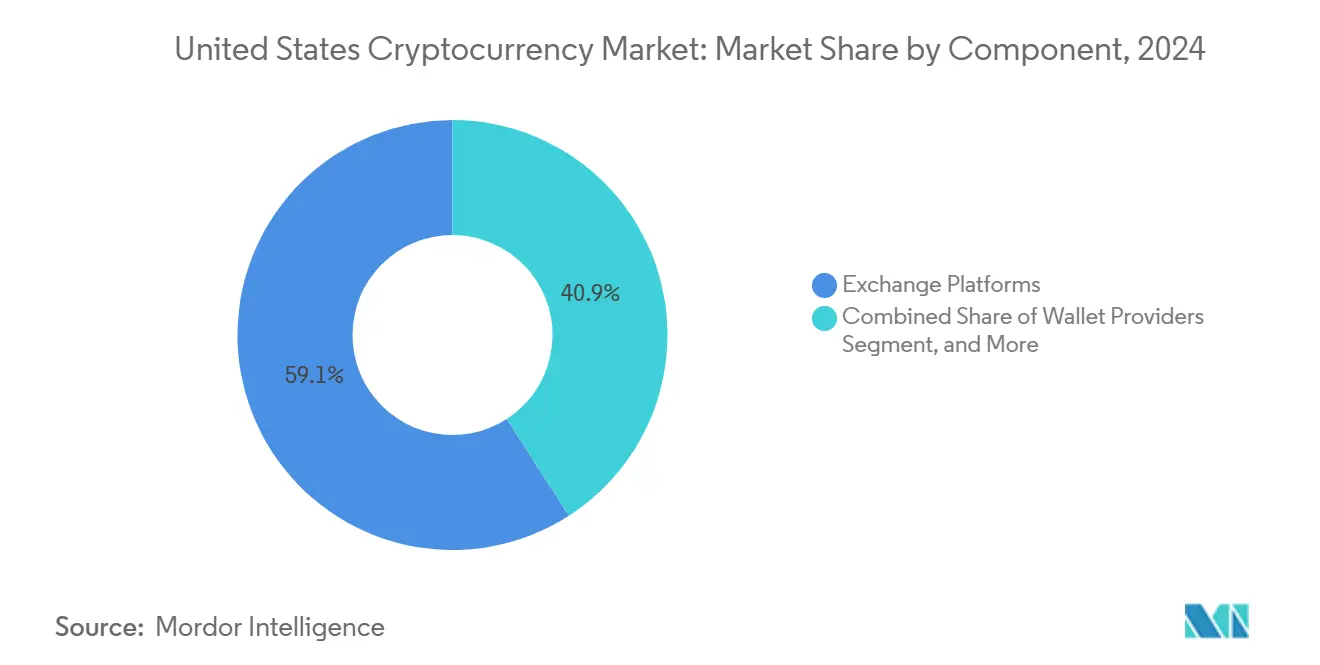

- By component, exchange platforms led with a 59.12% share of the United States cryptocurrency market in 2024, while payment gateways are expected to advance at a 12.84% CAGR to 2030.

- By cryptocurrency type, Bitcoin accounted for a 42.31% share of the United States cryptocurrency market in 2024, whereas stablecoins held the fastest trajectory at a 12.61% CAGR through 2030.

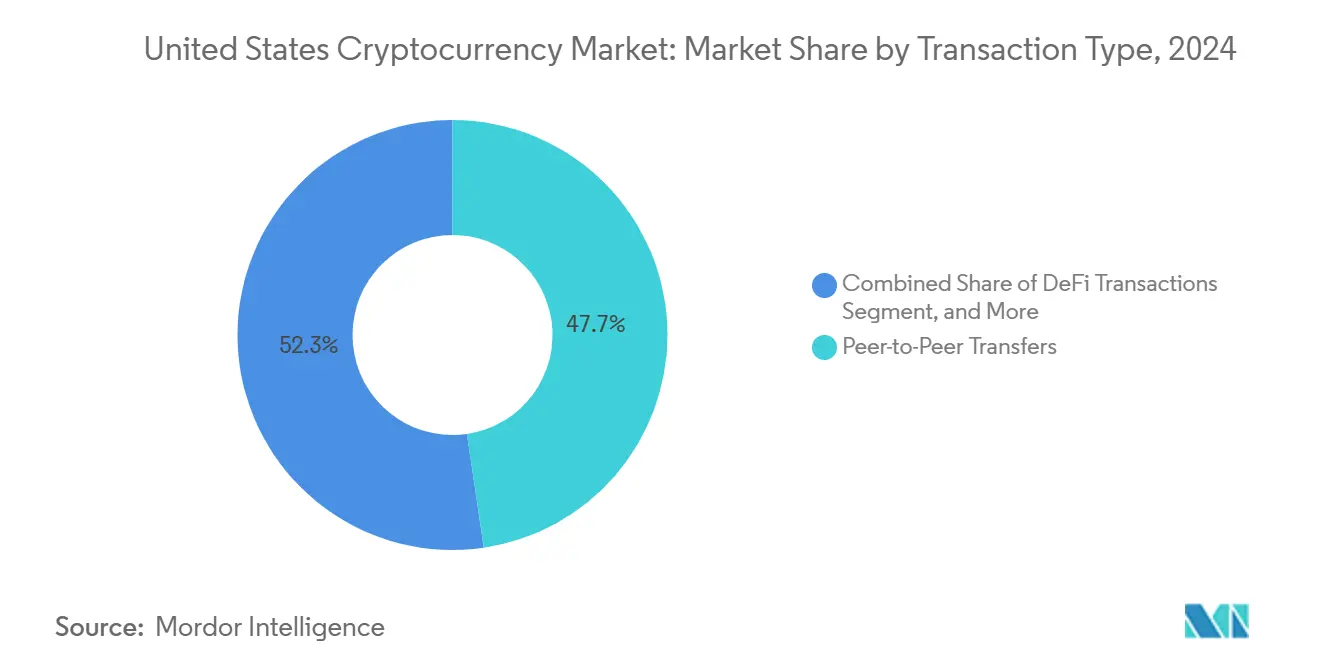

- By transaction type, peer-to-peer transfers commanded a 47.68% share of the United States cryptocurrency market in 2024, and decentralized finance transactions are expected to expand at a 12.72% CAGR through 2030.

- By end user, individuals represented 68.32% share of the United States cryptocurrency market in 2024; institutional investors exhibit the quickest climb at a 12.79% CAGR through 2030.

- By geography, the West captured a 35.67% share of the United States cryptocurrency market in 2024, while the South is forecasted to grow at a 12.91% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on cryptocurrency market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Cryptocurrency Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Institutional Adoption of Cryptocurrencies | +2.1% | National (Northeast and West) | Medium term (2-4 years) |

| Expansion of Regulated Digital Asset Custody Services | +1.8% | National (financial centers) | Short term (≤ 2 years) |

| Increasing Integration of Crypto Payment Gateways by Major Retailers | +1.5% | National (West Coast leadership) | Medium term (2-4 years) |

| Emergence of Layer-2 Scalability Solutions Reducing Transaction Costs | +1.3% | Global, U.S. DeFi hubs | Short term (≤ 2 years) |

| Rising Popularity of Stablecoin-Backed Remittances | +1.0% | National (Southern states) | Medium term (2-4 years) |

| Tokenization of Real-World Assets in Capital Markets | +0.9% | National (financial centers) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Institutional Adoption of Cryptocurrencies

Institutional allocations have evolved from pilot programs to multi-billion-dollar mandates, signaling a fundamental shift in portfolio allocation among U.S. asset owners. MicroStrategy alone held 331,200 bitcoins, valued at USD 29.7 billion in late 2024, exceeding its market capitalization by 29%.[1]MicroStrategy Inc., “Fourth Quarter 2024 Financial Results,” microstrategy.com California’s CalPERS approved a USD 300 million digital asset sleeve, validating crypto as an investable asset class for public pensions. Daily settlement volume on JPMorgan’s JPM Coin rose past USD 1 billion, demonstrating large-bank readiness for on-chain liquidity. Federal Reserve research into a U.S. CBDC further normalizes digital assets, even as implementation remains a long-term prospect. The classification of Bitcoin and Ethereum as commodities by the Commodity Futures Trading Commission (CFTC) reduced legal ambiguity for futures and spot derivative products, thereby spurring faster institutional onboarding.

Expansion of Regulated Digital Asset Custody Services

Custody has transitioned from a technical hurdle to a competitive service layer for capital markets. The 2024 OCC interpretive letter authorized federally chartered banks to provide crypto custody, opening a pipeline of bank-backed solutions.[2]Office of the Comptroller of the Currency, “Cryptocurrency Custody Interpretive Letter,” occ.gov Fidelity Digital Assets’ AUC climbed 180% year-on-year to USD 15 billion, evidence that asset managers prefer household custodians over standalone tech vendors. Wyoming’s Special Purpose Depository Institutions have attracted USD 8.2 billion by promoting balance-sheet isolation and favorable tax treatment. Insurance capacity expanded, with Lloyd’s syndicates underwriting limits up to USD 100 million per policy, lowering residual risk for institutional allocators. Qualified custodian rules under the Investment Advisers Act standardized controls, accelerating adviser participation nationwide.

Increasing Integration of Crypto Payment Gateways by Major Retailers

Mainstream merchants view digital assets as a tool to unlock premium customer segments and reduce chargebacks. PayPal processed USD 7.6 billion in crypto checkouts during 2024, with average ticket sizes 23% higher than conventional cards.[3]PayPal Holdings Inc., “Full-Year 2024 Results,” paypal.com Shopify enabled 1.7 million stores to accept tokens, particularly in the luxury goods sector, where the risk of fraud reversal is expensive. BitPay quantified a 67% reduction in payment disputes compared to credit networks, highlighting significant merchant savings. Circle’s USD Coin settled USD 4.3 trillion, underscoring the suitability of stablecoins for cross-border ecommerce. While FedNow intensifies domestic payment competition, crypto retains a cost advantage for international transfers under USD 1,000.

Emergence of Layer-2 Scalability Solutions Reducing Transaction Costs

Layer-2 frameworks fundamentally reprice the cost of on-chain interactions. Polygon handled 3.2 billion transactions in 2024 with sub-cent fees. Arbitrum’s TVL closed the year at USD 18.3 billion as developers migrated from the Ethereum mainnet to optimistic rollups for better economics. Coinbase’s Base network surpassed 500 million transactions in its inaugural year, demonstrating brand-driven traffic capture. Zero-knowledge proofs on Starknet pushed throughput to 1,000 TPS without compromising Ethereum security. These advances unlock new market niches, including pay-per-view media and micro-lending, extending the addressable user base for the United States cryptocurrency market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty Around Classification of Digital Assets | -1.9% | National (state variations) | Medium term (2-4 years) |

| Persistent Security Breaches and High-Profile Exchange Hacks | -1.4% | Global (centralized platforms) | Short term (≤ 2 years) |

| Rising Compliance Costs from Treasury Digital Asset Reporting Rules | -1.1% | National | Medium term (2-4 years) |

| Environmental Impact of Proof-of-Work Mining Energy Consumption | -0.8% | National (high-load mining states) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty Around the Classification of Digital Assets

Overlapping agency mandates complicate compliance strategies and slow capital formation. SEC enforcement has generated USD 8.2 billion in fines since 2024, often applying securities rules retroactively. Concurrent CFTC claims over spot markets create forum shopping that undermines consistency. New York’s BitLicense caps the number of industry participants at 34 licensees, thereby shrinking local competition. Proposed federal legislation could rationalize oversight but faces a polarized Congress. Internationally, Europe’s MiCA rules outpace those of the U.S., placing domestic firms at a strategic disadvantage when serving global clients.

Persistent Security Breaches and High-Profile Exchange Hacks

High-value hacks periodically erode consumer trust and raise insurance premiums. The DMM Bitcoin incident in May 2024 siphoned USD 305 million, spotlighting continued vulnerabilities in hot wallet management. DeFi exploits totaled USD 1.8 billion, with smart contract flaws driving two-thirds of the losses, according to CertiK. Concentration risk is elevated because the top five exchanges process 70% of U.S. volume. Private insurance costs range from 2.5% to 5% of assets, limiting coverage for retail platforms. FDIC confirmation that crypto deposits lack federal insurance underscores the sector’s risk-bearing burden until on-chain audit standards mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Exchange Dominance Softens as Payment Infrastructure Accelerates

Exchange platforms accounted for 59.12% of the United States' cryptocurrency market size in 2024; however, their proportional control is trending lower as specialized infrastructure emerges. Payment gateways, while starting from a smaller base, record a 12.84% CAGR that outpaces every other component. This rise mirrors merchant demand for instant cross-border settlement and low dispute rates. Wallet providers evolved, with MetaMask surpassing 100 million monthly active users in 2024, shifting from passive storage to integrated Web3 identity management. Mining hardware revenues stabilized after the Ethereum merge, prompting ASIC manufacturers to repurpose their fabrication lines for artificial-intelligence chips, thereby hedging against cyclical mining demand risk.

Over the forecast horizon, custody solutions and compliance software are expected to absorb a larger portion of the United States cryptocurrency market share as institutional mandates tighten. Automated surveillance platforms help exchanges meet Bank Secrecy Act standards, while know-your-customer engines reduce onboarding costs for financial institutions. The Federal Reserve’s supervisory guidelines, published in early 2025, require banks to quantify operational crypto risk, spurring demand for third-party analytics. Consequently, exchange operators are expanding into lending, staking, and brokerage to defend wallet share, blurring classic component boundaries.

By Cryptocurrency Type: Stablecoins Lead Growth as Utility Outweighs Speculation

Bitcoin retained 42.31% of the United States cryptocurrency market share in 2024, but the metric is inching downward as functional tokens proliferate. Stablecoins are expected to lead growth with a 12.61% CAGR through 2030. Dual fiat on-ramps, compliance certainties, and 24-hour settlement windows position USD-backed tokens as preferred collateral in decentralized finance and remittances. During 2024, USD 8 trillion in volume moved through Circle’s USD Coin and Tether’s USDT combined. Ethereum’s shift to proof-of-stake cut energy consumption by 99.9%, taming a key ESG critique and reinforcing its dominance in smart-contract issuance.

Altcoins such as Solana, Aptos, and Avalanche compete on bandwidth and programming languages, capturing developers who need low-latency systems for gaming and real-time trading. Regulatory clarity surrounding derivatives supports bitcoin and Ethereum futures at CME, yet many governance tokens remain in a gray area that restricts institutional inflows. Central-bank digital currency pilots could alter the value proposition of private stablecoins, but most experts foresee coexistence rather than displacement. The net result is continued diversification of market capitalization, diluting Bitcoin’s weight but expanding its aggregate market utility.

By Transaction Type: DeFi Innovation Reshapes Usage Patterns

Peer-to-peer transfers accounted for 47.68% of the United States' cryptocurrency market size in 2024, underscoring crypto’s origins as a retail money transfer system. However, decentralized finance transactions are surging at a 12.72% CAGR, energized by high-yield liquidity pools and automated market-making. Smart contracts account for over 60% of Ethereum calls, indicating a shift from passive holding to active protocol participation. Mastercard’s post-acquisition integration of CipherTrace broadened merchant acceptance networks, inviting compliance-ready retail payments at scale.

Remittances benefit stateside migrant workers sending transfers of less than USD 200; stablecoins are completed in under five minutes, compared to multiple days through correspondent banks. The Lightning Network, which hosts more than 5,000 nodes, supports nano-payments for content streaming and pay-per-article journalism, thereby widening the cryptocurrency’s micropayment niche. Meanwhile, non-fungible token trading cooled from 2022 peaks but still underpins interactive media rights and gaming assets. The breadth of transaction types expands the total addressable opportunity, reinforcing momentum in the United States cryptocurrency market.

By End User: Institutional Momentum Redefines the Profile of Demand

Individuals commanded 68.32% of the United States cryptocurrency market size in 2024, a legacy of early retail dominance. Institutional investors, although smaller today, are clocking the highest CAGR at 12.79%, reflecting improved custody, clearer accounting guidance, and the availability of ETFs. BlackRock’s iShares Bitcoin Trust amassed more than USD 25 billion AUM within twelve months, demonstrating traditional-manager potency in distribution channels.

Large enterprises integrate tokens for balance-sheet optimization and supplier payments; Tesla still holds a meaningful bitcoin position, while Microsoft offers notarization services on Azure Blockchain. SMEs utilize low-cost remittances for supply chain purchases in Latin America and Asia. Public-sector engagement remains niche—largely limited to asset forfeiture auctions and IRS enforcement-yet research by the Federal Reserve signals potential CBDC rollouts that could further influence public sentiment. The emergence of federally chartered crypto banks also enhances institutional confidence by aligning with the governance standards of traditional finance.

Geography Analysis

The West controlled 35.67% of the United States cryptocurrency market share in 2024, thanks to Silicon Valley’s deep venture ecosystem and Washington’s cloud infrastructure cluster. California’s Department of Financial Protection and Innovation has issued detailed compliance guidance, lowering licensing ambiguity even as proposed money-transmission rules would increase overhead. Apple and Google initiatives in crypto payments, together with venture capital dry powder exceeding USD 6 billion, sustain pipeline growth in the region. Seattle’s talent pool, anchored by Bittrex and Coinme, diversifies the geography beyond San Francisco, supporting the development of a resilient ecosystem.

The South is the expansion engine, forecast to post a 12.91% CAGR to 2030, buoyed by deregulated electricity markets and pro-business legislation. Texas attracted more than USD 2 billion in mining infrastructure after 2024, supplying roughly 25% of the national hash rate under the Electric Reliability Council of Texas' load-balancing framework. Florida’s zero-income tax and progressive digital asset laws drew companies such as FTX.US and Blockchain.com to Miami, generating USD 12 billion in transactional throughput in 2024. Tennessee and North Carolina passed statutory protections for node operators and miners, further widening southern appeal.

The Northeast and Midwest continue to experience steady, mid-single-digit expansion. New York’s BitLicense offers legal certainty, yet its rigorous capital requirements deter new entrants, capping the state at 34 licensed operators. Conversely, institutional desks in Manhattan and Boston dominate OTC liquidity and innovation in custody. Illinois and Ohio leverage renewable energy and abandoned industrial sites to host new mining farms, hedging against Texas grid volatility. Banking access remains uneven; some conservative Midwestern lenders still restrict crypto accounts, although federal regulators encourage risk-based engagement. Despite disparities, interstate competition continues to spread infrastructure investment across all four Census regions, supporting nationwide depth for the United States cryptocurrency market.

Competitive Landscape

Competition remains moderately concentrated, with the five largest exchanges and custody firms controlling an estimated 55% of spot trading and assets under custody. Coinbase’s regulatory positioning following its bank holding approval gives it a cost-of-capital and product breadth edge; however, fee pressures from Binance.US and Kraken have narrowed average retail commissions by 35% over the past eighteen months. Spot bitcoin ETFs intensified rivalry among asset managers; BlackRock, Fidelity, and Invesco collectively carved out a USD 55 billion sleeve within a year, driving expense-ratio compression below 0.20%.

Technological differentiation is critical. Exchanges that invest in Layer-2 integrations offer cheaper withdrawals and faster clearing, thereby improving client stickiness. Anchorage Digital and Paxos emphasize SOC-2-certified custody, winning mandates from registered investment advisers migrating client accounts. Meanwhile, Riot Platforms and Marathon Digital scale renewable-powered mines, appealing to ESG-conscious institutional buyers of freshly minted bitcoin. Chainalysis and Elliptic provide transaction monitoring APIs that have become de facto compliance utilities, deeply embedding themselves in exchange technology stacks.

Mergers and cross-industry partnerships blur traditional boundaries: payment giants license crypto analytics, while crypto natives acquire broker-dealer licenses to underwrite tokenized equities. Overall, the strategic landscape suggests a moderate concentration score driven by regulatory burdens that favor capital-rich incumbents yet leave innovation windows for agile specialists.

United States Cryptocurrency Industry Leaders

Coinbase Global Inc.

Payward Ventures Inc. (Kraken)

BAM Trading Services Inc. (Binance US)

Gemini Trust Company LLC

Bitstamp USA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tesla released its 2024 Impact Report, reaffirming the company's cryptocurrency treasury strategy under updated ESG guidelines.

- February 2025: MicroStrategy's bitcoin holdings reached 331,200 tokens valued at USD 29.7 billion as of December 2024, representing 129% of the company's market capitalization.

- January 2025: PayPal's cryptocurrency checkout service processed USD 7.6 billion in transactions during 2024, with average transaction values 23% higher than traditional payment methods.

- January 2025: BlackRock's iShares Bitcoin Trust surpassed USD 30 billion in assets under management, becoming the largest cryptocurrency ETF within 12 months of launch.

United States Cryptocurrency Market Report Scope

| Exchange Platforms |

| Wallet Providers |

| Mining Hardware |

| Payment Gateways |

| Other Component |

| Bitcoin |

| Ethereum |

| Stablecoins |

| Altcoins |

| Other Cryptocurrency Types |

| Peer-to-Peer Transfers |

| Retail and Ecommerce Payments |

| Remittances |

| DeFi Transactions |

| Other Transaction Type |

| Individuals |

| SMEs |

| Large Enterprises |

| Institutional Investors |

| Government and Public Sector |

| By Component | Exchange Platforms |

| Wallet Providers | |

| Mining Hardware | |

| Payment Gateways | |

| Other Component | |

| By Cryptocurrency Type | Bitcoin |

| Ethereum | |

| Stablecoins | |

| Altcoins | |

| Other Cryptocurrency Types | |

| By Transaction Type | Peer-to-Peer Transfers |

| Retail and Ecommerce Payments | |

| Remittances | |

| DeFi Transactions | |

| Other Transaction Type | |

| By End User | Individuals |

| SMEs | |

| Large Enterprises | |

| Institutional Investors | |

| Government and Public Sector |

Key Questions Answered in the Report

How large is the United States cryptocurrency market in 2025?

It is valued at USD 1.23 billion and is projected to grow at a 12.49% CAGR through 2030.

Which segment is expanding fastest?

Payment gateways post the highest component growth at a 12.84% CAGR to 2030.

Why are stablecoins gaining traction?

Stablecoins offer 24-hour settlement and lower volatility, driving a 12.61% CAGR in the segment.

Which region leads in market share?

The West holds 35.67% share due to dense venture funding and tech infrastructure.

What restrains wider adoption today?

Primary hurdles include regulatory uncertainty and high-profile security breaches.

How concentrated is competition among U.S. exchanges?

The largest five operators command about 55% of volume, indicating moderate concentration.

Page last updated on: