Bitcoin Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.28 Billion |

| Market Size (2031) | USD 31.49 Billion |

| Growth Rate (2026 - 2031) | 11.24% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bitcoin Technology Market Analysis by Mordor Intelligence

The Bitcoin technology market size is expected to grow from USD 16.43 billion in 2025 to USD 18.28 billion in 2026 and is forecast to reach USD 31.49 billion by 2031 at 11.24% CAGR over 2026-2031. Institutional balance-sheet adoption, the April 2024 block subsidy halving, and United States spot ETF approvals are transforming the Bitcoin technology market from retail-trading-led to enterprise-infrastructure driven. Hardware demand is plateauing as application-specific integrated circuit (ASIC) shipments face a post-halving oversupply, while services, such as custody, compliance, and Lightning Network processing, are scaling rapidly in response to new rules for qualified custodians. The Asia Pacific mining base is relocating toward renewable-powered hubs, and the Middle East is emerging as the fastest-growing treasury and hosting destination. Competitive dynamics are shifting from hash rate accumulation toward full-stack service provision and renewable energy arbitrage, opening up opportunities for Layer 2 providers and tokenization platforms.

Key Report Takeaways

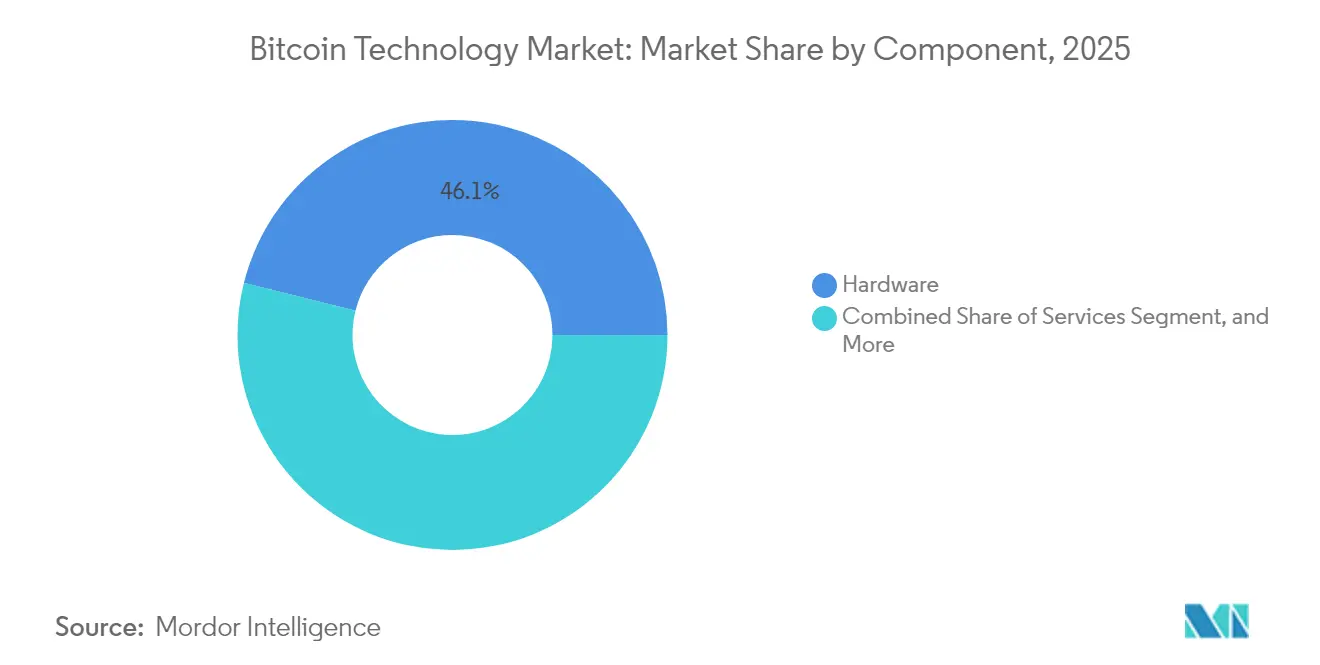

- By component, hardware led with a 46.10% share of the Bitcoin technology market in 2025; services are forecast to expand at a 11.74% CAGR through 2031.

- By application, payments accounted for 38.70% of the Bitcoin technology market size in 2025, while smart contracts are expected to advance at a 12.34% CAGR through 2031.

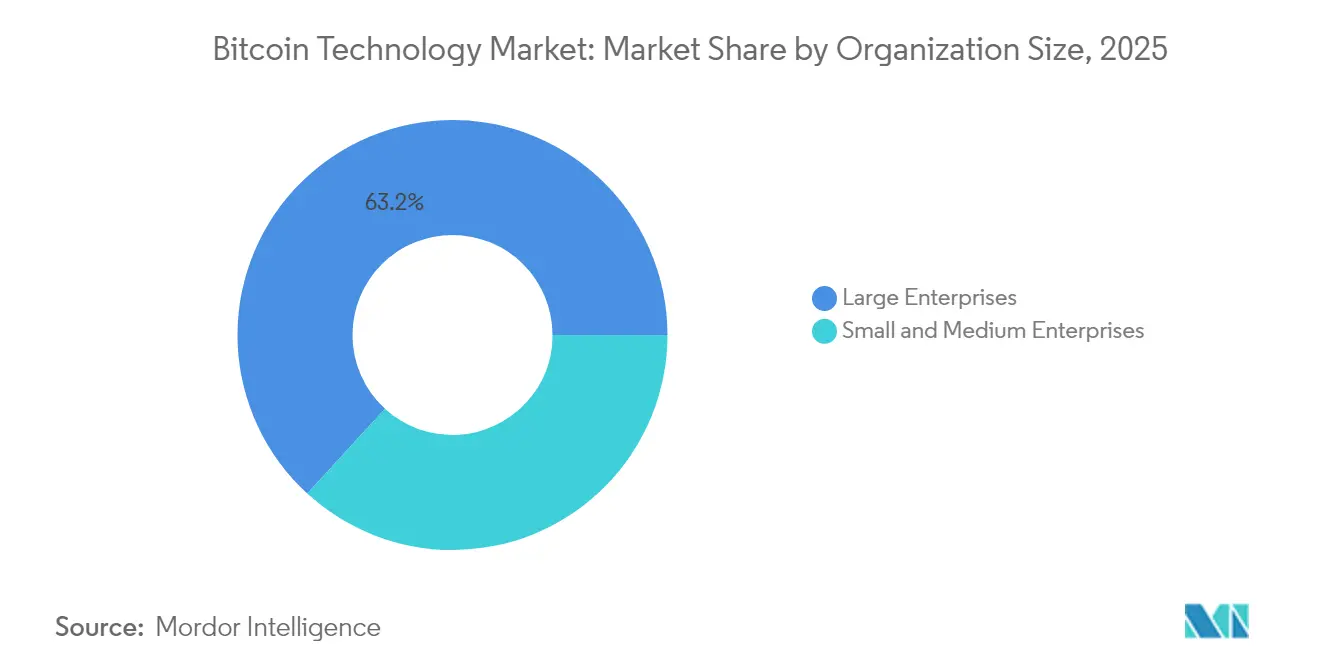

- By organization size, large enterprises held a 63.20% share of the Bitcoin technology market in 2025, whereas small and medium enterprises are expected to grow at a 11.55% CAGR to 2031.

- By end-user industry, financial services dominated with a 41.75% share of the Bitcoin technology market in 2025; healthcare is forecast to grow at a 12.29% CAGR between 2026 and 2031.

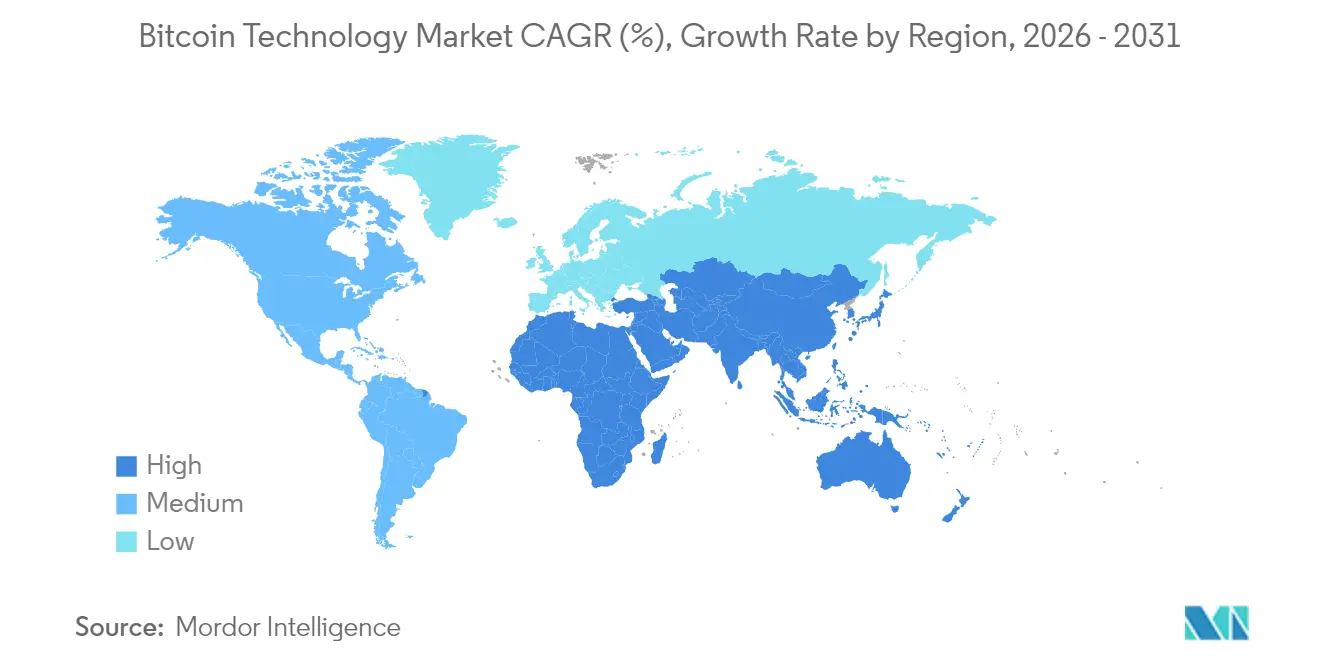

- By geography, the Asia Pacific captured 37.40% of the Bitcoin technology market share in 2025, and the Middle East is projected to register a 12.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bitcoin Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Institutional Adoption by Fortune 500 Treasuries | +2.8% | North America and Europe, spillover to Asia Pacific | Medium term (2-4 years) |

| Regulatory Clarity in Major Economies | +2.3% | Global, concentrated in North America, Europe, and Middle East | Short term (≤ 2 years) |

| Renewable Energy Integration for Mining Economics | +1.7% | North America, Middle East, and Nordic Europe | Long term (≥ 4 years) |

| Halving-Driven Supply Contraction Effects | +1.5% | Global | Short term (≤ 2 years) |

| Layer 2 Scaling Solutions Maturity | +1.4% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Tokenization of Real-World Assets on Bitcoin | +1.2% | North America, Europe, and Asia Pacific financial hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Institutional Adoption by Fortune 500 Treasuries

Balance-sheet allocations by public corporations are reframing Bitcoin as a macro treasury hedge rather than a speculative trade. MicroStrategy exceeded 402,000 BTC holdings by December 2024, catalyzing peer adoption across technology and financial firms.[1]Michael Saylor, “MicroStrategy Acquires Additional Bitcoin,” MicroStrategy, microstrategy.com Tesla disclosed USD 184 million in digital assets, signaling mainstream corporate validation. Mid-cap CFOs follow suit because Bitcoin offers liquidity and non-correlation alongside bond-like fungibility. Impairment-only accounting remains a headwind, yet the Financial Accounting Standards Board’s 2023 proposal to allow fair-value marks could resolve the asymmetry by 2026. As clarity improves, treasury desks are integrating multi-signature custody and automated tax workflows to manage risk at scale.

Regulatory Clarity in Major Economies

United States approval of spot Bitcoin ETFs in January 2024 ended a decade of uncertainty over securities status and unlocked registered-investment-advisor allocations.[2]U.S. Securities and Exchange Commission, “Statement on Spot Bitcoin ETFs,” sec.gov Europe’s Markets in Crypto-Assets Regulation brought passportable licensing across 27 member states, cutting compliance duplication. Japan removed consumption tax on retail Bitcoin payments in March 2024, eliminating a 10% cost barrier. These milestones compress the regulatory risk premium, enabling banks, insurers, and pension funds to allocate without fear of retroactive action. Fragmentation persists in India and Nigeria, yet global liquidity deepens as the largest capital markets adopt harmonized rules.

Renewable Energy Integration for Mining Economics

Post-halving subsidy reductions amplify the need for low-cost power. Miners are co-locating with stranded wind and solar assets to purchase electricity near zero marginal cost. Marathon Digital’s 250 MW Texas wind farm exemplifies the model. The International Energy Agency estimated 52% renewable penetration in Bitcoin mining for 2024, higher than most heavy industries.[3]International Energy Agency, “Electricity 2024,” iea.org Grid operators now classify miners as flexible load resources, paying for demand-response services that stabilize frequency. This non-subsidy revenue hedge is crucial as block rewards keep halving.

Halving-Driven Supply Contraction Effects

The April 2024 halving cut new issuance to 3.125 BTC per block, tightening daily supply at the precise moment institutional inflows accelerated via ETFs. Reduced sell-pressure historically precedes multi-year appreciation as scarcity narratives gain traction. Miners face compressed revenues, prompting consolidation and hardware efficiency races, but holders benefit from supply-demand imbalance. Futures basis has narrowed, indicating arbitrageurs expect persistent spot demand in the Bitcoin technology market. The next halving cycle is already priced into treasury models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Consumption Criticism | -1.6% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Cybersecurity Threats to Exchanges | -1.3% | Global, acute in Asia Pacific and emerging markets | Short term (≤ 2 years) |

| Regulatory Fragmentation Across Emerging Markets | -0.9% | Africa, South Asia, and Latin America | Long term (≥ 4 years) |

| Hashrate Centralization Risk | -0.7% | Global, concentrated in North America and Central Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption Criticism

Environmental NGOs pressure policymakers to curtail proof-of-work mining. New York State extended a moratorium on fossil-fuel-powered facilities through 2024, forcing relocations. Europe’s MiCA now mandates public energy-use disclosure, raising compliance overhead for small miners. Asset managers face shareholder resolutions that link Bitcoin exposure to ESG targets, constraining capital inflows. Public perception lags renewable adoption rates, keeping the narrative risk alive through 2027.

Cybersecurity Threats to Exchanges

Exchange hacks continue to erode retail confidence. DMM Bitcoin’s USD 305 million loss in May 2024 triggered stricter Japanese custody rules. U.S. custody amendments require advisors to use qualified custodians, centralizing assets and creating single points of failure. Insurance and multi-signature wallets mitigate risks, yet human error and social-engineering persist. Regulatory penalties for breaches are rising, elevating compliance costs for smaller venues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Hardware as Infrastructure Matures

Services are projected to grow at an 11.74% CAGR through 2031 as enterprises prefer custody, compliance, and Lightning processing to capital-intensive mining gear. The Bitcoin technology market size for services benefits from the SEC’s qualified-custodian mandate, which pushed institutional assets toward regulated providers that can offer proof-of-reserve audits. Hardware retained 46.10% Bitcoin technology market share in 2025 but faces margin compression due to ASIC oversupply and energy-efficiency races.

Custody firms differentiate via insurance and geographic key sharding, while payment processors integrate instant Lightning settlement to bypass card-network fees. Tax-automation platforms are embedding compliance rules for over 50 jurisdictions, accelerating adoption among CFOs who require auditable reporting. Hardware vendors now market joules-per-terahash rather than absolute hashrate, acknowledging that electricity cost, not chip count, decides miner profitability. The service pivot signals that the Bitcoin technology market is entering a platform era where value accrues to usability and compliance rather than raw compute.

By Application: Smart Contracts Challenge Payments Dominance

Payments accounted for 38.70% of the Bitcoin technology market size in 2025 as remittances and e-commerce embraced instant settlement. Smart contracts, however, are projected to expand at a 12.34% CAGR, narrowing the gap by 2031. Taproot Assets and RGB enable tokenization without leaving Bitcoin’s security umbrella, lowering gas-fee risk for real-world asset sponsors.

Private equity funds now pilot real estate tokens, and supply-chain operators embed automated delivery-versus-payment clauses. Remittance providers cut corridor fees below 1% using Lightning channels, pressuring traditional money transfer operators. Regulatory scrutiny constrains centralized trading applications, nudging liquidity toward decentralization where self-custody reduces counterparty risk. The diversification of use cases underscores the Bitcoin technology market’s evolution from simple value transfer to programmable settlement.

By Organization Size: SMEs Accelerate Adoption Through Treasury Software

Large enterprises captured 63.20% Bitcoin technology market share in 2025 thanks to scale advantages in custody fees and over-the-counter liquidity. Yet small and medium enterprises are set to grow at an 11.55% CAGR as turnkey multi-signature platforms remove technical hurdles. Accounting suites now auto-import Bitcoin transactions into general ledgers, erasing manual entry bottlenecks.

SMEs in Latin America and Africa adopt Lightning-based payroll to avoid volatile local currencies, while North American tech start-ups hold Bitcoin as a hedge against inflationary fiat expansion. Large corporates focus on diversification strategies but move slower due to governance layers. The democratization of custody and tax tooling is flattening the adoption curve across firm sizes, expanding total addressable demand in the Bitcoin technology market.

By End User Industry: Healthcare Emerges as Fastest-Growing Vertical

Financial services dominated with 41.75% revenue in 2025, anchored by banks integrating settlement rails and asset managers listing ETFs. Healthcare is projected to grow at a 12.29% CAGR as clinical-trial sponsors deploy Bitcoin-based milestone contracts that trigger payments upon data submission. Immutable audit trails meet stringent compliance needs, while supply-chain track-and-trace satisfies Medical Device Regulation rules.

Retail and e-commerce merchants adopt Lightning checkout to eliminate chargeback fraud, boosting net margins by up to 300 basis points. Logistics companies timestamp custody transfers for high-value goods, reducing disputes. The vertical mix illustrates that the Bitcoin technology market is no longer finance-only; operational efficiency in heavily regulated industries drives incremental demand.

Geography Analysis

Asia Pacific held 37.40% of Bitcoin technology market share in 2025, underpinned by Kazakhstan’s mining infrastructure and Hong Kong’s April 2024 ETF greenlight. Japan’s tax exemption spurred retail payment innovation, while South Korea introduced travel-rule compliance that increased exchange overhead. India maintains a punitive 30% capital-gains tax, pushing volumes to peer-to-peer venues. Australia’s Iris Energy expands renewable-powered facilities, aligning with local ESG mandates.

The Middle East is the fastest-growing region at a 12.18% CAGR through 2031. Dubai’s Virtual Assets Regulatory Authority delivers licensing clarity, attracting custody and liquidity desks. UAE’s central bank opened consultation on Bitcoin reserve diversification, and Saudi Arabia’s Public Investment Fund explores renewable-powered mining, meshing with Vision 2030 sustainability goals. Remittance corridors from Gulf states to South Asia accelerate Lightning adoption, lowering fees for migrant workers.

North America hosts roughly 38% of global hashrate after China’s 2021 exit, with cheap Texan wind and deregulated power markets boosting economics. The United States ETF approval catalyzes institutional flows, while Canada’s commodity treatment of Bitcoin attracts exchanges seeking legal certainty. Europe lags in mining due to high energy prices but leads Lightning merchant deployment and tokenization pilots as MiCA provides consistent rules. South American adoption is volatile yet deepens in Argentina and Brazil where inflation incentivizes non-sovereign stores of value.

Regulatory Landscape

The regulatory environment for Bitcoin technology is shifting toward formal licensing, reporting, and clearer market-structure boundaries in major economies, which increases demand for custody, audit, and monitoring tooling that can stand up to compliance reviews. In the United States, a March 2025 Executive Order (Federal Register 2025-03992) established a Strategic Bitcoin Reserve framework for Treasury management of forfeited BTC, reinforcing government-level handling standards that shape institutional custody and chain-of-title practices. In March 2026, U.S. agencies issued updated guidance on applying federal securities laws to crypto assets and digital-asset intermediaries, increasing compliance requirements for exchanges, brokers, and service providers supporting trading, custody, and payment flows.

In Europe, Markets in Crypto-Assets Regulation (MiCA) continues to standardize requirements across the EU, and the June 2026 end of the MiCA transitional period for existing Crypto-Asset Service Providers (CASPs) to obtain authorization raises the importance of authorization readiness, technical standards alignment, and operational resilience. In the United Kingdom, The Reporting Cryptoasset Service Providers (Due Diligence and Reporting Requirements) Regulations 2025 entering into force in January 2026 implements OECD Crypto-Asset Reporting Framework style obligations, pushing wallets, exchanges, and intermediaries to expand KYC, transaction reporting, and audit trails. Together, these milestones raise compliance spend and pull enterprise procurement toward qualified-custodian solutions, proof-of-reserves workflows, and surveillance capabilities across global operations.

Value Chain Analysis

The Bitcoin technology value chain spans chip design and wafer supply into ASIC manufacturing and assembly, followed by distribution and logistics to miners and hosting providers, then deployment and operations (power procurement, facilities, cooling, firmware, and pool connectivity), and finally downstream software and services such as custody, compliance, payments, and Lightning routing or liquidity. Hardware production is concentrated among a small set of vendors (notably Bitmain, MicroBT, and Canaan), while public miners and hosting firms (including MARA, Riot Platforms, Core Scientific, and CleanSpark) act as major buyers that translate equipment deliveries into installed exahash and service capacity. Mining pools and protocol-layer developers also sit on the critical path, because pool policies and client software releases affect transaction selection, fee capture, and node performance, feeding back into hardware ROI and service SLAs.

Key bottlenecks and risk points center on cross-border trade, tariffs, and supplier scrutiny, which can disrupt delivery timing, raise landed costs, and encourage partial localization of assembly. Reuters reported Chinese mining-machine makers setting up U.S. production to manage tariff exposure, and supply-chain workarounds have included shifting shipments toward electronic components for local assembly rather than fully assembled units. On the software and services side, upgrades to Lightning implementations (for example, Blockstream Core Lightning releases) and emerging protocol proposals (BIPs) influence the cadence of wallet and payment-provider feature rollouts. At the same time, exchange and custodian security requirements (highlighted by major theft events in 2024) continue to drive demand for multi-signature orchestration, insurance integration, and operational controls across the services layer.

Competitive Landscape

The Bitcoin technology market shows moderate concentration as the top miners and hardware vendors control outsized hashrate and chip supply; however, service verticals are fragmenting rapidly. Marathon Digital and Riot Platforms executed distressed-asset roll-ups in 2024, scaling economies of renewable power procurement. Bitmain and MicroBT fight margin pressure by pushing energy-efficiency below 20 J/TH. Custody players such as Coinbase and BitGo emphasize insurance coverage and regulatory audits to secure institutional mandates.

Layer 2 infrastructure specialists Lightning Labs and Blockstream capture white-space demand for instant settlement and Taproot-based tokenization. Patent filings for multi-signature orchestration and channel-routing algorithms grew 23% in 2024, signaling that intellectual property moats will shape future advantage. Decentralized mining pools reduce coordinator risk, though hashrate centralization remains a governance concern. Competitive strategy is shifting toward renewable integration and compliance readiness, as miners morph into grid-stabilization partners and service firms become risk-management vendors.

Emerging disruptors include algorithmic liquidity providers that rebalance Lightning channels autonomously, and custody start-ups offering jurisdictional key sharding for geopolitical resilience. As block subsidies decline, transaction fees and ancillary grid-services revenue will dictate profitability, favoring operators with diversified income streams. The Bitcoin technology industry therefore rewards strategic alignment with energy markets and regulatory foresight.

Bitcoin Technology Industry Leaders

Bitmain Technologies Ltd.

Canaan Inc.

Ebang International Holdings Inc.

Blockstream Corporation Inc.

Lightning Labs Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise-grade Layer 2 payment and asset infrastructure remains a central whitespace as Bitcoin adoption shifts from retail trading toward regulated, auditable operations. Lightning Network utilization has moved into larger-scale rails, with reported monthly transaction volume exceeding USD 1 billion by November 2025 and exchange participation cited as an adoption driver, including Coinbase. This supports use cases in liquidity management, routing optimization, and merchant reliability services. The June 2026 Taproot Assets v0.8 release from Lightning Labs, alongside a public Taproot Assets SDK, clarifies the product path for multi-asset issuance and stablecoin management on Lightning, which in turn creates demand for issuer tooling, compliance workflows, wallet UX, and risk controls that fit regulated institutions and cross-border payment providers.

Security hardening and cryptographic agility also present a practical opportunity area as capabilities move from research into deployed features. Blockstream executed post-quantum-signed transactions on the Liquid Network mainnet in March 2026 using the SHRINCS signature scheme, and it also shipped Core Lightning v26.06 with experimental quantum-resistant channel support. In parallel, Bitcoin Improvement Proposals activity, including BIP 446 assignment in February 2026 and BIP 448 merging in March 2026, points to a pipeline of Taproot-native transaction and programmability enhancements that vendors can productize through node software, developer tooling, and managed infrastructure. These developments support new service categories around post-quantum readiness assessments, key management upgrades, and migration tooling for custodians, exchanges, and large treasury holders that need long-lived security guarantees.

Recent Industry Developments

- July 2026: Bitmain provided computing power technology services for the launch of HashKey Capital's Bitcoin Hashrate Fund and also released the Antminer S21 Pro with 234 TH/s performance and 15 J/T efficiency. The combination links a leading ASIC vendor more directly to regulated, fund-linked mining exposure while pushing the hardware efficiency frontier for operators competing on cost per terahash after the 2024 halving.

- June 2026: Ebang International announced its subsidiary acquired industrial land in Xinghe County, Inner Mongolia, to build production facilities for amorphous and nanocrystalline new materials used to improve transformer efficiency. The move broadens Ebang's industrial footprint beyond pure crypto hardware, aligning with power-efficiency themes that shape mining economics and data center operations.

- May 2024: DMM Bitcoin disclosed a theft of approximately USD 305 million, prompting tighter focus on custody controls in Japan. The incident increased urgency for exchange and custodian investments in multi-signature architecture, insurance, and operational monitoring, reinforcing the market shift toward institutional-grade security and compliance services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the bitcoin technology market is defined as the revenues earned from bitcoin-focused hardware, software, and services that enable holding, transacting, securing, integrating, or operating bitcoin networks for users and organizations across regions.

Scope exclusions: We exclude trading gains, coin price movements, and non-bitcoin crypto networks when they are not directly tied to bitcoin technology spending.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Application

- Payments

- Trading and Exchange

- Remittances

- Smart Contracts

- Other Application

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End User Industry

- Financial Services

- Retail and E-Commerce

- Healthcare

- Supply Chain and Logistics

- Other End User Industry

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to align the market language and confirm demand signals before assumptions were built. We relied on public and repeatable references such as Federal Reserve publications, BIS papers, IMF and World Bank datasets, OECD digital economy indicators, and official regulator releases such as SEC communications and ESMA updates. These sources were used to understand adoption patterns, payment behavior, and policy direction.

To translate activity into spend, we also reviewed company filings, annual reports, investor presentations, product documentation, open technical documentation, and reputable press for revenue-mix clues and pricing ranges. Where needed, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to fill ownership and product-footprint gaps, and then those points were cross-checked back to public disclosures. The desk sources listed here are illustrative only, and additional references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what portion of wallet, exchange, payment acceptance, security, and infrastructure spend is truly bitcoin-led, and what portion is shared with broader crypto stacks. We discussed allocation logic with solution providers, integrators, large buyers, and industry specialists across APAC, EMEA, and the Americas. This input was used to correct model inputs when desk signals were delayed or too generalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 18% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 20% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts from a top-down reconstruction of the spend pool by mapping bitcoin technology use cases to observable activity and adoption signals, and then converting them into value using price and monetization patterns. In practice, inputs such as active wallet usage trends, payment acceptance penetration, enterprise security and compliance spending direction, infrastructure investment cycles that affect bitcoin operations, and transaction throughput patterns were used as checks so totals stayed realistic.

After that, results were corroborated with selective bottom-up approximations, such as sampled pricing for custody and wallet services, typical take rates for exchange-related services, and hardware revenue proxies where public disclosures exist. Totals were then adjusted when gaps appeared. Where company reporting blended bitcoin with broader crypto, revenue splits were estimated using product-level cues and validated through interviews, which helped avoid double counting across applications. For forecasting, scenario analysis was used because regulation and adoption can shift quickly. The scenarios were anchored to agreed drivers from primary discussions, followed by year-by-year smoothing to avoid sudden jumps.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including regional adoption narratives, policy timing, and spend-intensity indicators from public datasets, and then mismatches were reviewed before sign-off. When a value moved sharply, the assumptions behind pricing, adoption, or revenue splits were re-tested, and respondents were re-contacted if the change could not be explained by a clear market event.

Each study goes through multi-step analyst review so arithmetic, unit logic, and scope alignment are consistent across regions and years. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the latest updated view.

Mordor Intelligence's Global Bitcoin Technology Market Market Size Compared Against Other Published Estimates

Published market sizes for bitcoin technology rarely match because the line between bitcoin-only spend and wider crypto infrastructure is not drawn the same way, and the timing of price and adoption inputs is not consistent across studies. Different studies also vary on whether they count only technology revenues or extend the definition into financial activity enabled by the technology.

Mining hardware and mining pool revenues sit outside Mordor Intelligence's scope here, which is why some broader totals look higher even when they use a similar forecast window. Other gaps usually come from mixing consumer crypto usage with enterprise deployment spend, using aggressive adoption curves without re-checking against payment acceptance or wallet usage, and applying different currency timing when converting multi-region revenues into USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.43 B (2025) | |

| Global Consultancy A | USD 20.00 B (2025) | Includes mining infrastructure and related hardware within the market total, and applies a factory-gate framing that can increase the counted value versus a buyer spend view for technology services. |

| Industry Publisher B | USD 95.16 B (2025) | Uses a broader definition that blends digital currency activity and adjacent crypto-enabled use cases, which can pull in value that is not directly paid for bitcoin technology products and services. |

Looking across the three figures, the spread is mainly explained by what gets counted as technology revenue versus what is treated as downstream financial activity or mining-related value. By keeping the model tied to observable adoption signals and validated revenue splits, the resulting number stays traceable to clear inputs and can be repeated year to year with the same steps.

Key Questions Answered in the Report

How large will the Bitcoin technology market be by 2031?

Forecasts place the Bitcoin technology market size at USD 31.49 billion by 2031, representing an 11.24% CAGR over 2026-2031.

Which segment is growing fastest within Bitcoin technology?

Services, which include custody, compliance, and Lightning processing, are projected to grow at an 11.74% CAGR through 2031.

What region is seeing the quickest adoption of Bitcoin technology?

The Middle East is expanding at a 12.18% CAGR as Dubai grants clear licenses and Gulf sovereign funds explore Bitcoin reserves.

Why are healthcare companies adopting Bitcoin technology?

Healthcare firms deploy Bitcoin-based smart contracts to automate milestone payments and ensure immutable clinical-trial data.

How is renewable energy affecting Bitcoin mining economics?

Co-location with curtailed wind and solar assets lowers power costs and earns grid-stabilization fees, improving post-halving miner margins.

What risks threaten Bitcoin exchange users?

Cybersecurity breaches remain the primary risk, with recent hacks prompting regulators to enforce stricter custody and insurance standards.

Page last updated on: