Automotive Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 32.40 Billion |

| Market Size (2031) | USD 40.63 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

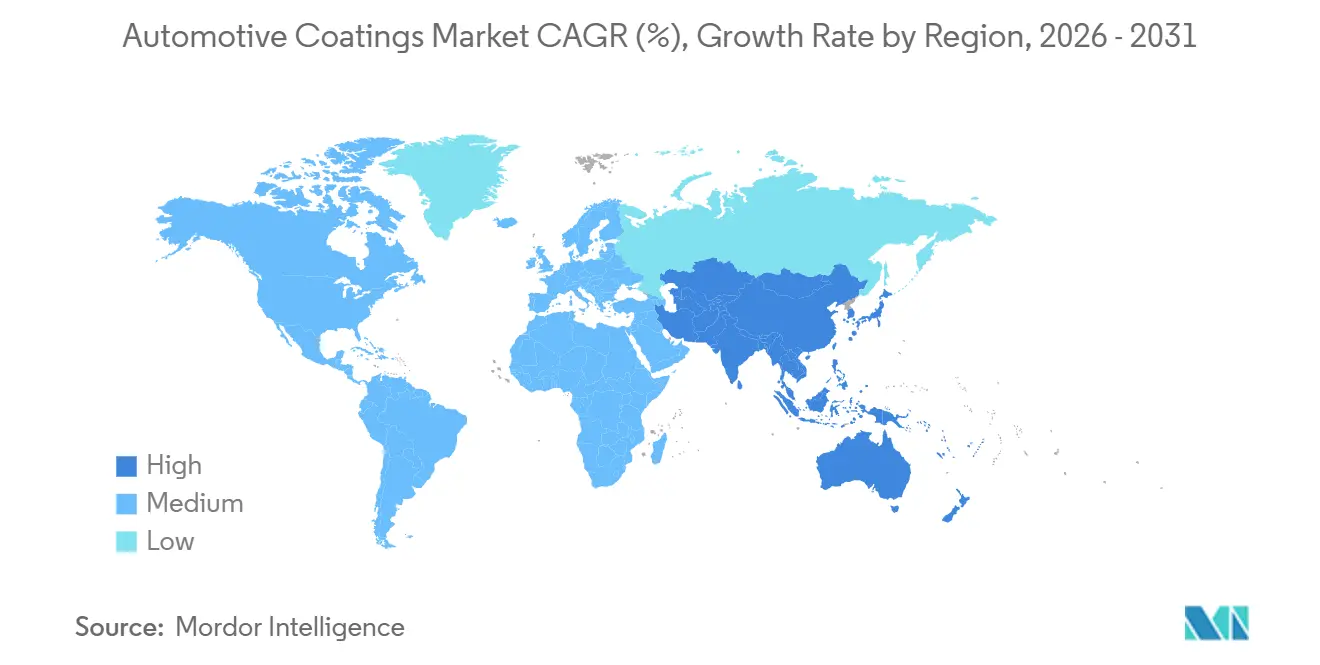

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

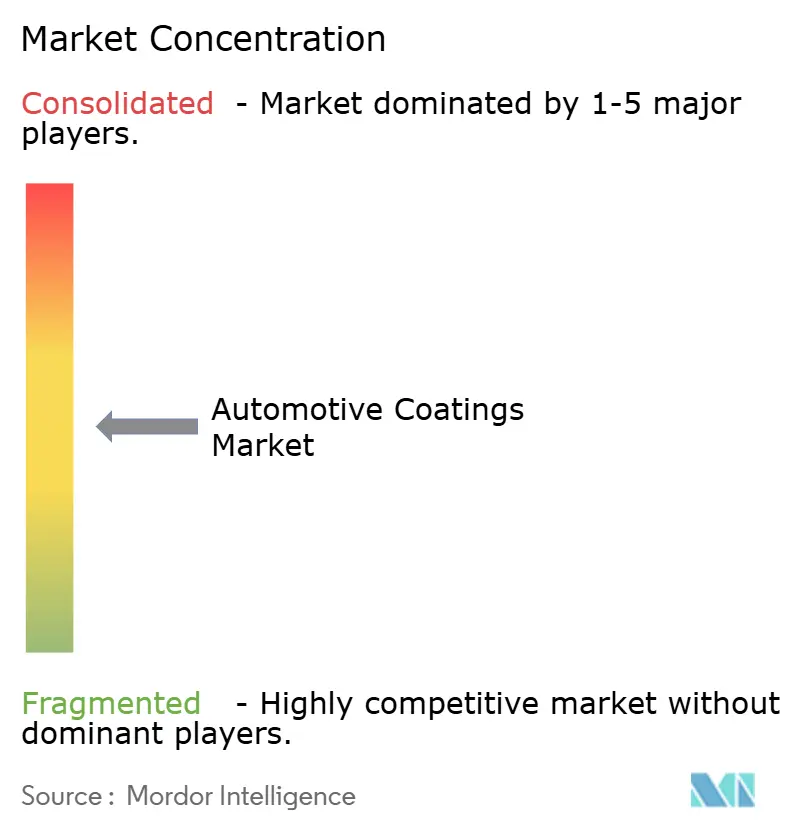

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Coatings Market Analysis by Mordor Intelligence

The Automotive Coatings Market size is expected to grow from USD 30.97 billion in 2025 to USD 32.40 billion in 2026 and is forecast to reach USD 40.63 billion by 2031 at 4.63% CAGR over 2026-2031. Rising vehicle production, fast-tracking electric-vehicle programs, and tighter volatile organic compound caps are reshaping demand toward water-borne and powder chemistries, while specialty thermal-management layers create new value pools for battery-pack designs. Suppliers are investing in regional plants across Asia-Pacific to localize water-borne capacity and cut logistics costs, a strategy that also shields them from raw-material swings linked to titanium dioxide and petrochemical feedstocks. Electric-vehicle skateboard platforms lower painted surface area by close to 15% per unit, yet higher-margin aluminum nitride and ceramic-filled coatings partly offset the volume loss. At the same time, sustainability-linked financing forces paint formulators to document measurable volatile organic compound reductions or risk higher borrowing costs, which tightens the gap between environmental compliance and competitive pricing.

Key Report Takeaways

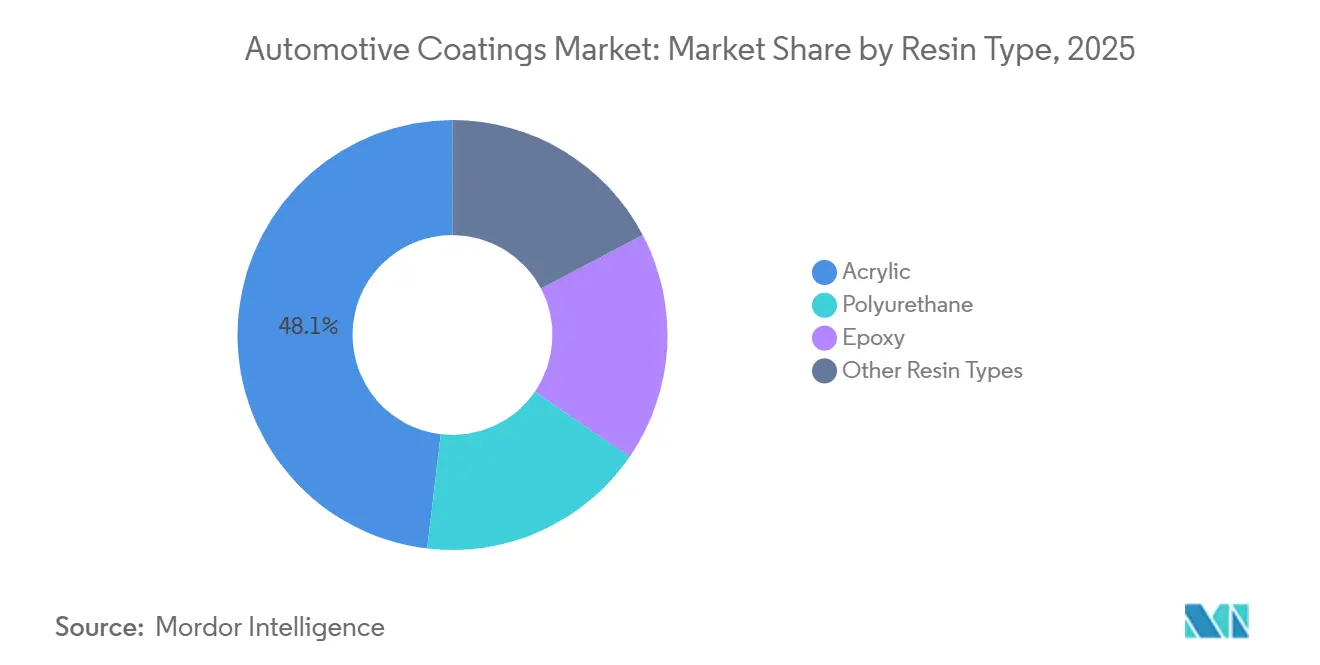

- By resin type, acrylic led with 48.12% of automotive coatings market share in 2025, while polyurethane is projected to post the fastest 5.04% CAGR through 2031.

- By technology, solvent-borne held 70.21% of 2025 volume, but powder is forecast to expand at a 4.97% CAGR over 2026-2031.

- By coating layer, clear coat captured 34.66% revenue in 2025 and E-Coat is advancing at a 4.99% CAGR through 2031.

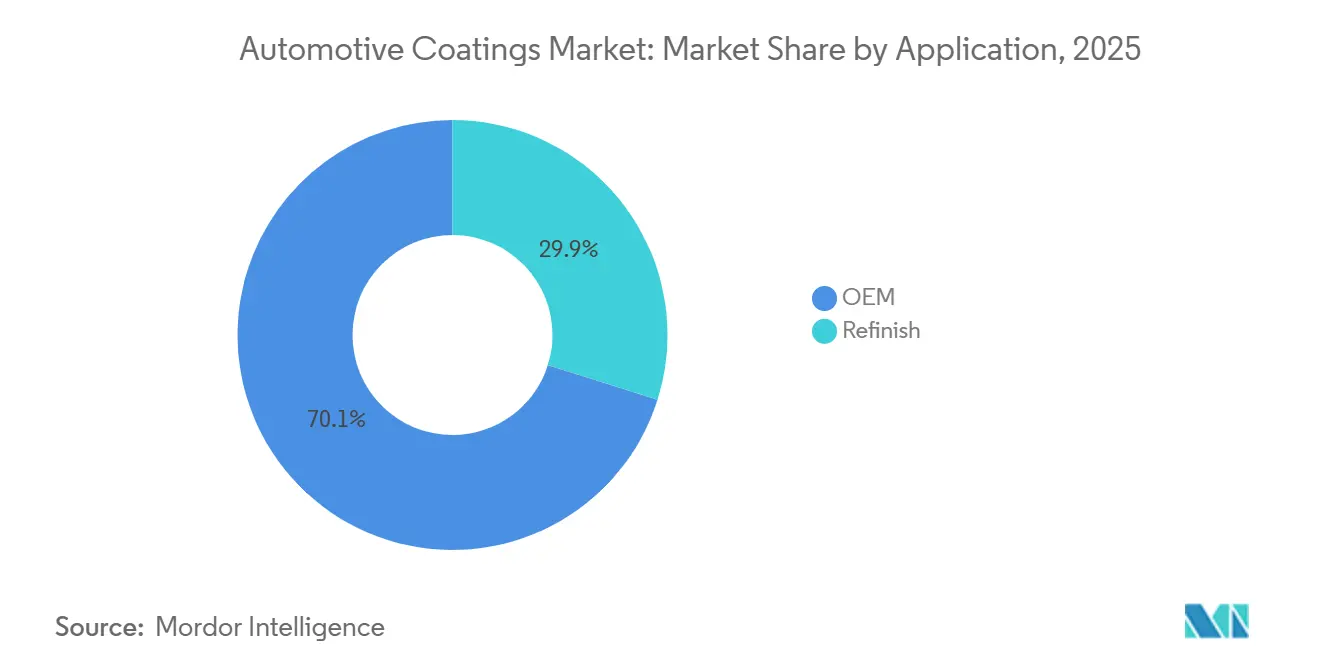

- By application, the OEM accounted for 70.13% demand in 2025, and it is set to grow at 5.04% CAGR through 2031.

- By geography, Asia-Pacific dominated with 58.89% revenue in 2025 and is on track for a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Vehicle-Production Rebound | +1.2% | Global, with APAC core accounting for 60% of incremental volume | Short term (≤ 2 years) |

| Shift Toward Water-Borne And Powder Systems To Meet Volatile Organic Content Caps | +1.5% | North America and EU leading; APAC adoption accelerating post-2027 | Medium term (2-4 years) |

| Rising EV-Specific Coating Demand for Battery Thermal Management | +0.9% | APAC core (China, South Korea), spill-over to North America | Medium term (2-4 years) |

| Recovery Of Collision-Repair Volumes in Mature Markets | +0.3% | North America and EU; limited impact in APAC | Short term (≤ 2 years) |

| Sustainability-Linked Financing Tying Interest Rates to Paint-Shop Volatile Organic Content Intensity | +0.5% | EU and North America; emerging in select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Vehicle-Production Rebound

Global light-vehicle output recovered to 92.5 million units in 2024 and is projected to surpass 95 million by 2026 as semiconductor shortages ease and new capacity comes online. China delivered 31.28 million units, while India and Japan collectively added more than 14 million units, anchoring Asia-Pacific’s dominance. Each vehicle consumes 3-5 kilograms of coatings across electro-coat, primer, basecoat, and clear-coat layers, translating the production surge directly into higher coating volumes. India’s USD 3.5 billion Production-Linked Incentive scheme accelerates investment by Maruti Suzuki, Hyundai, and Tata Motors, which will add roughly 180,000 metric tons of incremental demand by 2027. Southeast Asian assembly is expanding as firms hedge supply-chain risk, prompting suppliers to establish localized blending plants to trim tariffs and lead times.

Shift Toward Water-Borne and Powder Systems to Meet Volatile Organic Content Caps

The United States National Emission Standards for Hazardous Air Pollutants Phase II caps emissions at 420 grams per liter for primer-surfacers and 250 grams per liter for topcoats from January 2025, while the European Union’s Directive 2004/42/EC enforces even stricter limits for two-pack systems[1]U.S. Environmental Protection Agency, “NESHAP Phase II Final Rule,” epa.gov . Water-borne substitutes emit 60-80% fewer volatile organic compounds per square meter, and powder coatings remove solvents completely, which helps paint shops stay below corporate carbon-budget ceilings. PPG Industries recorded 8% revenue growth in its water-borne automotive lines during 2024, fully offsetting declines in solvent-borne demand. China’s GB 24409-2020 standard compels domestic formulators to re-engineer resin systems or risk losing OEM approvals, and investment is shifting toward large-scale water-borne lines in Jiangsu and Guangdong. Powder clearcoat technology still lacks Class A finish on exterior panels, but recent thin-film breakthroughs from Axalta close the gap, making niche adoption viable for door jambs and trunk interiors.

Rising EV-Specific Coating Demand for Battery Thermal Management

Lithium-ion cells must operate inside a narrow 20-40 °C window, and fast-charge cycles routinely spike temperatures above 60 °C. Aluminum nitride coatings showing thermal conductivity of 150-180 W/m-K cut peak cell temperature by up to 10 °C in 350 kW charge events, extending cycle life and maintaining warranty thresholds. BYD produced 4.27 million new-energy vehicles in 2024, catalyzing immediate demand for these specialty layers, while LG Energy Solution and Samsung SDI have standardized ceramic-filled coatings on cylindrical cells to safeguard performance. Suppliers are dedicating production lines in Incheon, Ulsan, and Shenzhen, capturing premium margins that run 30-50% above commodity clearcoats.

Recovery of Collision-Repair Volumes in Mature Markets

United States miles driven rebounded to 3.26 trillion in 2024, but higher total-loss frequency pushed insurers to scrap vehicles with advanced driver-assistance systems rather than repair them. Rapid-cure refinish products now cut booth time from four hours to 90 minutes, letting shops increase throughput and partially offset lower claim counts. Axalta’s 2024 ambient-cure clearcoat eliminates the need for heated booths, slicing shop energy bills by 40% and improving cash flow for independent operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Solvent and Isocyanate Exposure Limits | -0.8% | Global, with EU and North America enforcing strictest thresholds | Medium term (2-4 years) |

| Volatile Petrochemical-Based Raw-Material Pricing | -0.6% | Global, with APAC formulators facing highest input-cost sensitivity | Short term (≤ 2 years) |

| EV Skateboard Platforms Reducing Painted Surface Area | -0.4% | APAC and North America leading EV adoption; EU following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Solvent and Isocyanate Exposure Limits

The United States Occupational Safety and Health Administration caps toluene diisocyanate exposure at 0.02 ppm and methylene diphenyl diisocyanate at 0.005 ppm, obliging paint booths to upgrade local exhaust ventilation and supply respiratory protection[2]U.S. Occupational Safety and Health Administration, “Isocyanate Exposure Limits,” osha.gov . The EU’s Classification, Labelling and Packaging Regulation further mandates hazard statements on isocyanate-bearing products, pushing suppliers toward low-free-monomer polyurethane resins that cost 10-15% more and deliver lower solids. A 2024 National Institute for Occupational Safety and Health study found 5-10% of automotive painters develop sensitization within five years even when personal protective equipment is used, accelerating substitution to water-borne crosslinker systems.

Volatile Petrochemical-Based Raw-Material Pricing

Titanium dioxide prices swung 25% between early 2023 and late 2024, and average levels remain 18% above 2019 baselines, compressing gross margins for smaller formulators that lack long-term supply contracts. Epoxy and polyurethane resins that track Brent crude prices suffered 12-18% quarter-over-quarter fluctuations during 2024 when benchmark oil traded between USD 70 and USD 95 per barrel. BASF’s coatings division reported 150 basis-point margin erosion in 2023 despite quarterly price surcharges, illustrating the challenge of passing costs through OEM-pricing cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Gains as Acrylic Dominance Persists

Acrylic resins commanded 48.12% revenue in 2025, yet polyurethane systems are forecast for a 5.04% CAGR through 2031 because OEMs want scratch-resistant clear layers without mass penalties on battery-electric structures. Polyurethane clearcoats offer 2H-3H pencil hardness, about 30% higher than acrylic equivalents, and keep gloss above 85% after 2,000 hours of accelerated weathering. Epoxy resins remain the go-to for electro-coat primers thanks to uniform deposition on complex geometries including battery enclosures.

Polyurethane uptake accelerates in China as BYD and NIO chase premium positioning, while Eastman Chemical’s 140 °C low-bake epoxy widens adoption in aluminum-heavy platforms. This diversified resin slate preserves supply flexibility and shields the automotive coatings market from raw-material shocks.

By Technology: Powder Coatings Gain as Solvent-Borne Share Erodes

Solvent-borne held 70.21% of 2025 volume, but regulatory limits already steer global paint lines toward water-borne and powder alternatives, positioning powder for a 4.97% CAGR through 2031. Water-borne basecoats now cover nearly all new lines in North America and Europe, achieving 60-80% lower volatile organic compound output and offering color parity with metallic-flake orientation that rivals solvent systems.

India, Southeast Asia, and South America still rely on solvent-borne because high humidity and limited climate control make water-borne curing unpredictable. Powder uptake climbs in Europe for commercial-vehicle chassis where chip resistance outranks Class A finish, while Axalta’s thin-film powder clearcoat achieving 40-50 µm thickness at more than 90 gloss expands addressable substrates. Suppliers able to flex between chemistries and invest in humidity-controlled booths will capture future gains in the automotive coatings market.

By Coating Layer: E-Coat Expands for Battery Enclosures

Clear coats led with 34.66% revenue in 2025, yet e-coat primers will outpace others at a 4.99% CAGR through 2031 because skateboard battery packs ride closer to road debris and need uniform 15-25 µm epoxy films for ISO 12944 C5-M corrosion grades. Three-wet-on-wet processes that skip flash-off steps shave 18 minutes per vehicle, and Rivian’s Illinois facility shows capital savings of USD 12 million versus traditional booths.

Self-healing clearcoats with hydrophobic additives maintain water contact angles below 10 degrees, which reduces wash frequency and keeps gloss high. Akzo Nobel’s micro-capsule technology reflows at ambient temperatures within 24 hours, an innovation poised to command premium within the automotive coatings market size for exterior finishes.

By Application: OEM Outpaces Refinish

OEM absorbed 70.13% of 2025 demand and are on track for a 5.04% CAGR through 2031 supported by rising global assembly, while refinish slipped in 2024 as insurers totaled vehicles outfitted with expensive sensors. PPG posted an 8% OEM-coatings revenue jump in 2024 anchored by water-borne volumes that comply with North American and European emission caps.

Refinish resilience now hinges on rapid-cure chemistry and digital color-matching that shrink booth time to 60-90 minutes and raise first-spray accuracy to 98%. Multi-shop operators negotiate volume discounts that squeeze distributor margins, prompting consolidation and technology investment in the automotive coatings industry to stay competitive.

Geography Analysis

Asia-Pacific contributed 58.89% of 2025 revenue and is set for a 6.12% CAGR thanks to China’s 31.28 million-unit output, India’s USD 3.5 billion incentive fund, and Southeast Asian diversification that attracts OEM assembly. China’s volatile organic compound cap of 670 g/L pushes reformulation toward water-borne, and BYD’s vertical integration gives it bargaining muscle on pricing and specification. South Korea’s battery majors request aluminum nitride films, carving high-margin niches within the automotive coatings market.

In North America, Ultrium platform expansion and Tesla’s Texas ramp sustain OEM growth, yet refinish remains under pressure from elevated total-loss frequency. Mexico’s production drives localized capacity, and PPG runs three plants to dodge tariffs and service Ford, General Motors, and Stellantis lines in real time. Canada pushes water-borne adoption under provincial volatile organic compound rules, nudging smaller suppliers toward capital upgrades.

In Europe, Directive 2004/42/EC enforces stringent emission ceilings, and Volkswagen’s sustainability bond makes low-volatile organic compound metrics a must-have for supplier contracts. Nordic plans to shift to 100% zero-emission sales by 2030 lift thermal-management coating demand. South America and Middle-East and Africa contributed smaller share, yet grow faster than the global average as Brazil pursues flex-fuel hybrids and Saudi Arabia funds a domestic electric-vehicle brand that needs premium coatings for desert corrosion risk.

Competitive Landscape

The top five suppliers—PPG Industries, Axalta, BASF, Akzo Nobel, and The Sherwin-Williams Company—hold under 60% share, illustrating moderate concentration and room for regional challengers such as Nippon Paint Holdings, Kansai Nerolac, and KCC Corporation. Competition intensifies in refinish where switching costs are minimal, while OEM contracts lock suppliers into three-to-five-year deals with rigorous ISO 12944 and ISO 14001 audits. Multinationals scale water-borne and powder capacity in Europe and North America to meet volatile organic compound mandates, whereas regional firms sell lower-priced solvent lines in India and Southeast Asia.

Technology is a strategic wedge. Axalta’s machine-learning color-matching trims formula development to 20 minutes, delivering 98% first-spray accuracy and boosting body-shop productivity. PPG leverages its footprint to co-locate production and service centers near OEM expansions in Mexico and Thailand, shortening lead times and locking in multi-year supply deals. Akzo Nobel patents self-healing clearcoats that react to micro-scratches, creating brand differentiation and higher invoice value per liter.

Financing trends amplify environmental performance. Suppliers that document year-on-year volatile organic compound cuts secure preferred credit margins, while laggards face coupon step-ups. Shanghai Kinlita’s USD 45 million Jiangsu investment undercuts multinational pricing by up to 18%, increasing cost pressure but also extending the technology shift as OEMs demand water-borne options at emerging-market price points.

Automotive Coatings Industry Leaders

Akzo Nobel N.V.

The Sherwin-Williams Company

Axalta Coating Systems, LLC

BASF

PPG Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Covestro AG and Nippon Paint Holdings Co., Ltd. formed a strategic partnership to enhance collaboration in automotive coatings. The partnership focused on co-developing efficient, sustainable, and high-performance coatings to foster industry innovation and support downstream advancements.

- November 2025: BASF commissioned a new production plant for automotive OEM coatings at its Muenster site in Germany. This highly automated facility enhanced sustainability and ensured process stability.

Global Automotive Coatings Market Report Scope

The automotive coatings market covers the products used during the manufacture or repair of automobiles, such as passenger cars and light commercial vehicles (LCVs), etc., to protect and decorate the metal bodywork.

The automotive coatings market is segmented by resin type, technology, layer, application, and geography. By resin type, the market is segmented into polyurethane, epoxy, acrylic, and other resin types. By technology, the market is segmented into solvent-borne, water-borne, and powder. By layer, the market is segmented into e-coat, primer, base coat, and clear coat. By application, the market is segmented into OEM and refinish. The report also covers the market size and forecasts for the automotive coatings market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Acrylic |

| Polyurethane |

| Epoxy |

| Other Resin Types |

| Solvent-borne |

| Water-borne |

| Powder |

| Clear Coat |

| E-coat |

| Primer |

| Base Coat |

| OEM |

| Refinish |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic | |

| Polyurethane | ||

| Epoxy | ||

| Other Resin Types | ||

| By Technology | Solvent-borne | |

| Water-borne | ||

| Powder | ||

| By Coating Layer | Clear Coat | |

| E-coat | ||

| Primer | ||

| Base Coat | ||

| By Application | OEM | |

| Refinish | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive coatings market in 2031?

The market is forecast to reach USD 40.63 billion by 2031 based on a 4.6% CAGR from 2026-2031.

Which region contributes the largest revenue to automotive coatings?

Asia-Pacific leads with 58.89% of global revenue in 2025 and maintains the fastest regional growth.

Which resin segment is expected to grow the fastest?

Polyurethane resins are set to rise at a 5.04% CAGR, driven by scratch-resistant clearcoat demand.

How are regulations influencing technology choices in coatings?

Tight volatile organic compound caps in the United States and European Union are accelerating switches from solvent-borne to water-borne and powder chemistries.

How will EV adoption affect coating demand?

EVs create new needs for battery thermal-management coatings, partially offsetting reduced painted metal area on skateboard chassis designs.

Page last updated on: