Insulation Coating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

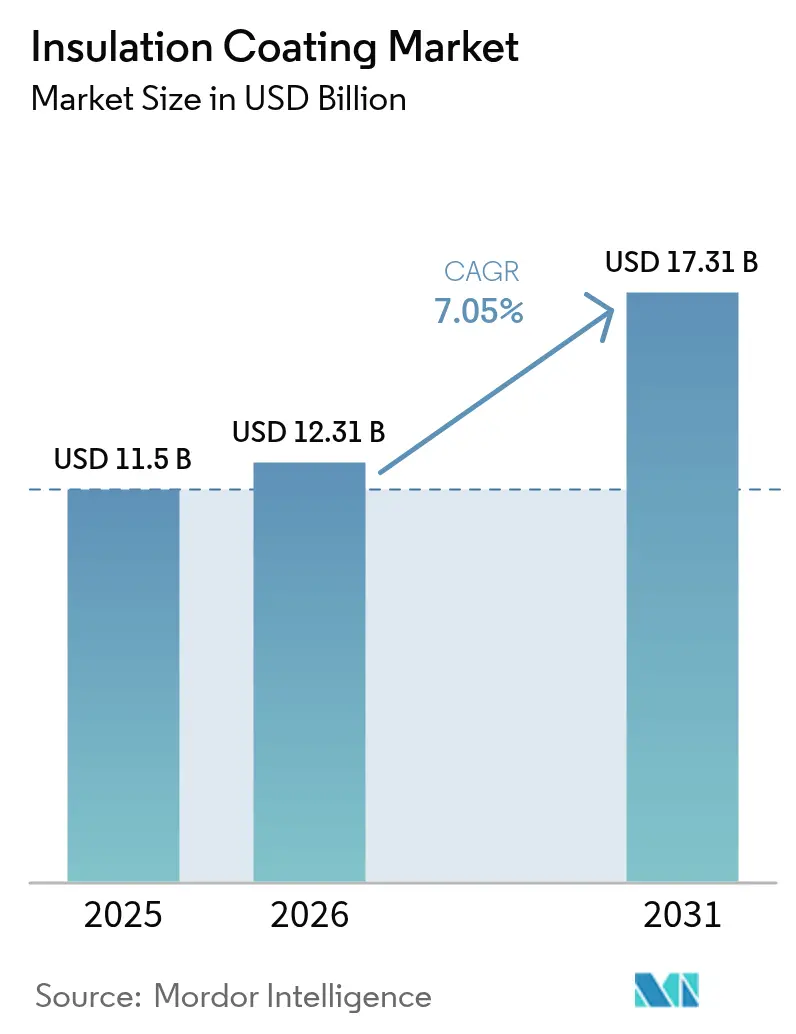

| Market Size (2026) | USD 12.31 Billion |

| Market Size (2031) | USD 17.31 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

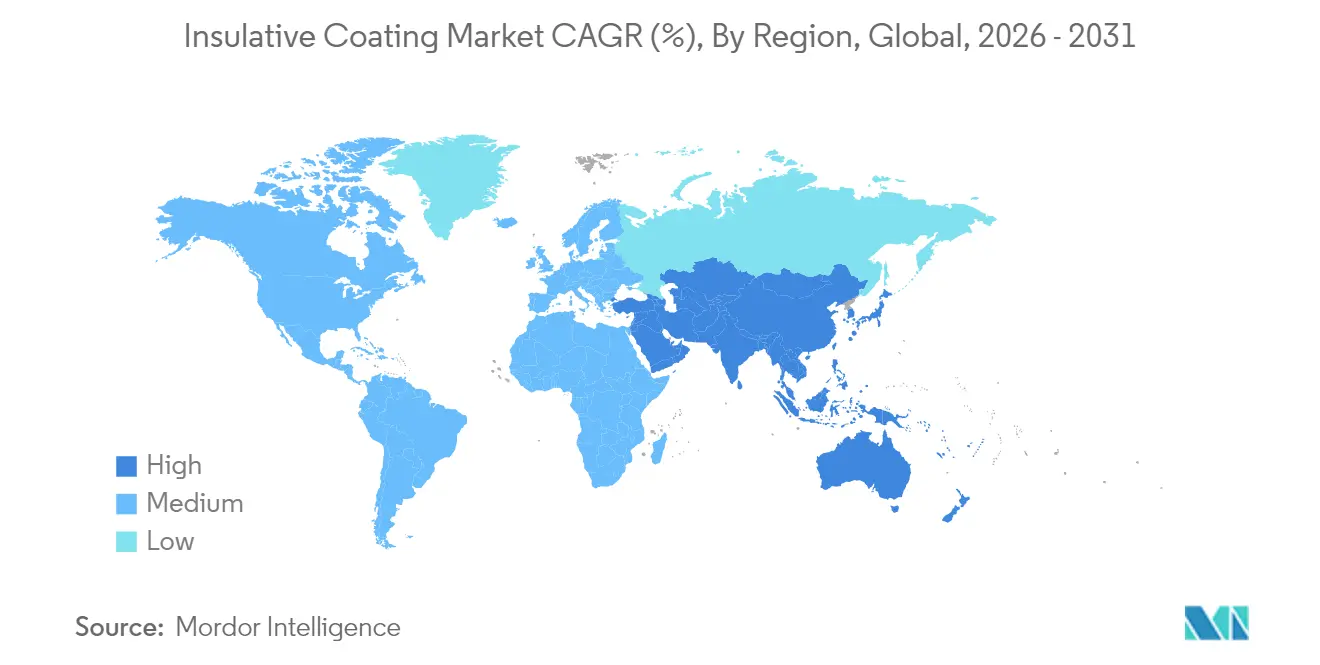

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulation Coating Market Analysis by Mordor Intelligence

The insulation coating market size is expected to grow from USD 11.50 billion in 2025 to USD 12.31 billion in 2026 and is forecast to reach USD 17.31 billion by 2031 at 7.05% CAGR over 2026-2031. This steady rise reflects global movement toward tighter energy-efficiency rules, modernization of industrial assets, and breakthrough material science that widens the performance envelope for thermal-management coatings. Product adoption spans construction, oil and gas, power generation, battery manufacturing, and other process industries, each seeking to cut heat loss, manage surface temperatures, and extend asset life. Asia-Pacific remains the demand anchor thanks to large-scale infrastructure outlays and manufacturing expansion, while North America and Europe shape product specifications through performance-based codes. Competitive strategies now emphasize portfolio realignment, R&D acceleration in aerogel and bio-based chemistries, and aftermarket service models that secure long-term revenue. Obstacles persist in the form of feedstock price swings and certification delays for new chemistries, yet the structural trend toward decarbonization keeps the insulation coating market on a growth path.

Key Report Takeaways

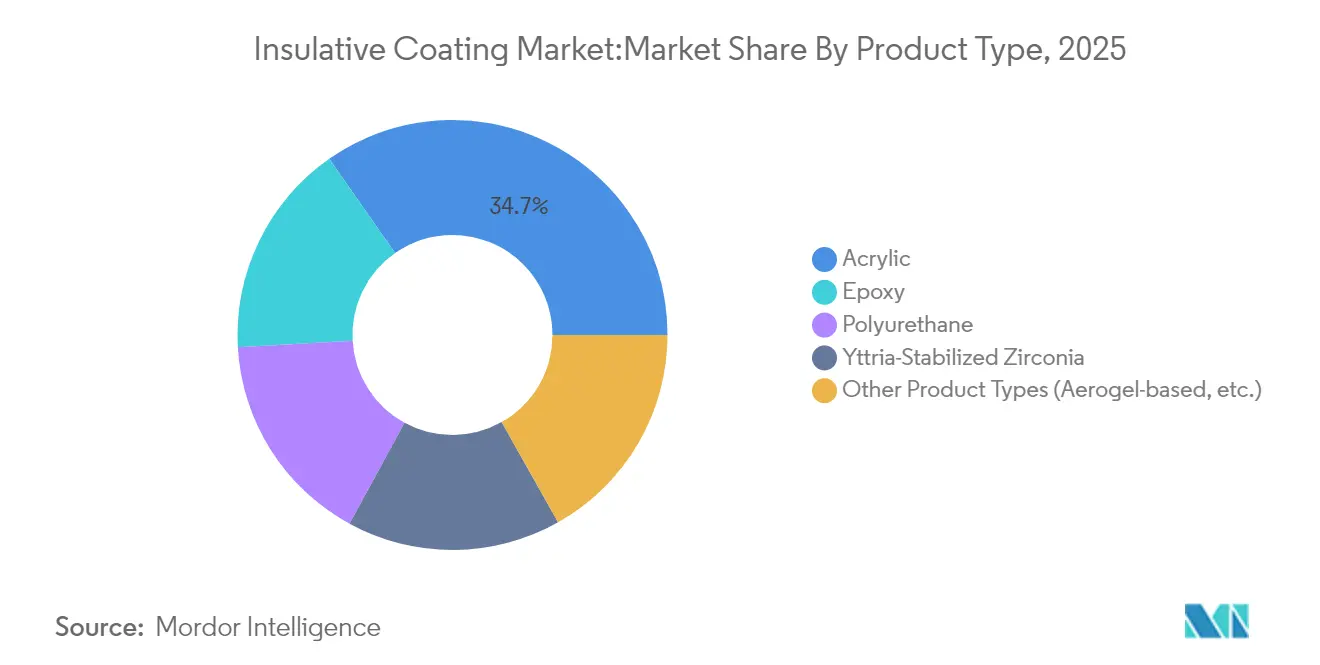

- By product type, acrylic formulations led with 34.72% revenue share in 2025; the “Other Product Types” segment is projected to grow at a 7.12% CAGR through 2031.

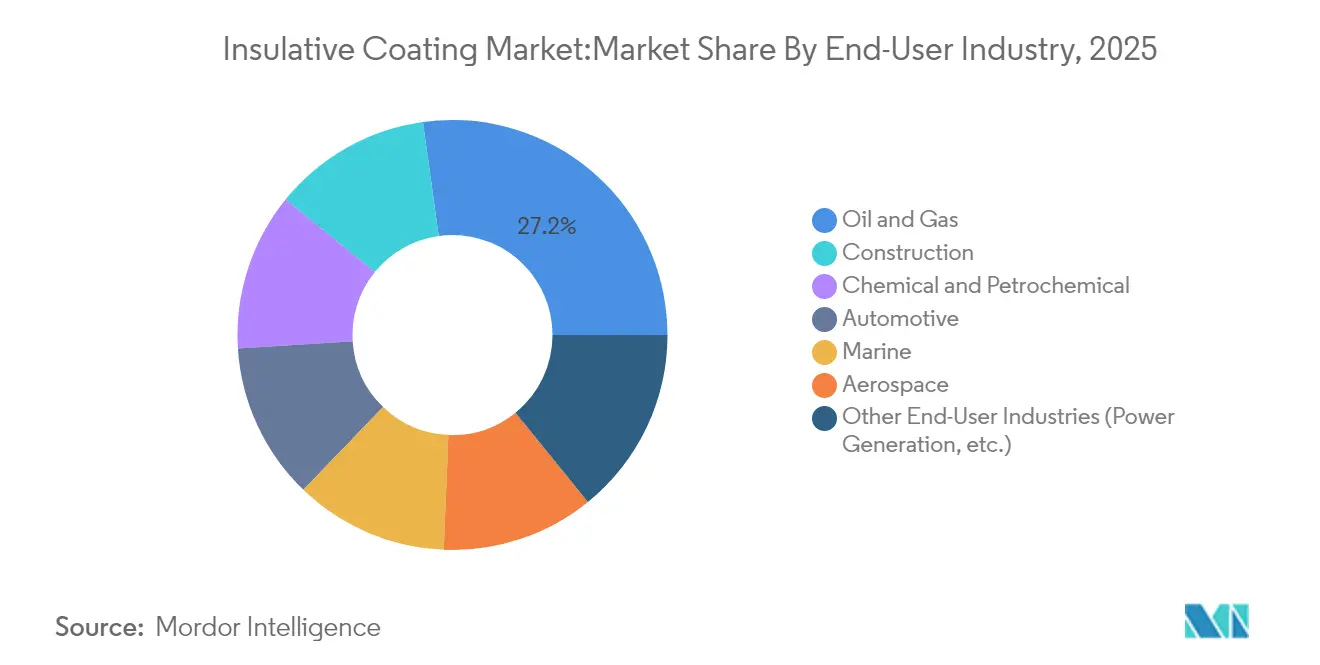

- By end-user industry, oil and gas held 27.20% of the insulation coating market share in 2025, while the “Other End-User Industries” segment is advancing at a 7.62% CAGR to 2031.

- By geography, Asia-Pacific accounted for 46.88% of the insulation coating market in 2025; the region is also the fastest growing, posting an 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insulation Coating Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in industrial LNG liquefaction trains | +1.2% | Global, with concentration in Qatar, Australia, North America | Medium term (2-4 years) |

| Tightening building-energy codes | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Retro-fit demand in aging offshore platforms | +0.9% | North Sea, Gulf of Mexico, Brazil offshore | Short term (≤ 2 years) |

| Surge in battery-gigafactory construction | +1.4% | Global, led by China, EU, North America | Medium term (2-4 years) |

| Super-insulative aerogel–filled top-coat launches | +0.7% | Global, early adoption in aerospace and industrial | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Industrial LNG Liquefaction Trains

Large-scale LNG projects require coatings that keep insulation properties intact at cryogenic temperatures as low as −162 °C. Upgraded U.S. Department of Transportation rules now cap allowable thermal conductance at 0.225 Btu h-1 ft-2 °F-1 at 60 °F for tank insulation, effectively establishing a global benchmark that favors high-performance polyurethane and aerogel systems[1]U.S. Department of Transportation, “PHMSA Final Rule on Enhanced Tank Car Standards,” transportation.gov. Project operators prioritise coatings that minimise boil-off gas and slash maintenance intervals, which in turn sustains steady volumes for suppliers across construction and maintenance cycles. Emerging Qatar North Field South megatrains, Canadian LNG sites, and new liquefaction capacity in the United States illustrate how demand clusters near production hubs. As more sovereign LNG producers chase export revenue, the insulative coating market benefits from multi-year order backlogs tied to engineering, procurement, and construction contracts. Performance differentiation is expected to intensify as operators request thinner films and lower thermal conductivities to meet total installed cost targets.

Tightening Building-Energy Codes

The 2024 International Energy Conservation Code mandates continuous insulation values ranging from R-5 to R-30, accelerating demand for coatings that deliver verifiable R-value gains on complex roof and façade geometries[2]Pro Builder Staff, “2024 IECC Raises Continuous Insulation R-Values,” probuilder.com. California’s R-30 roof rule and Washington’s climate-zone-specific standards show how state-level regulations drive immediate specification shifts. Product developers respond with low-emissivity and highly reflective coatings such as AkzoNobel’s Interpon D1036 Low-E line, which promises up to 20% energy savings for commercial buildings. Code tightening cascades into renovation cycles, because once owners experience energy savings, similar coatings are considered during retrofit events. As APAC adopts performance-based codes, multinational manufacturers position their regional plants to deliver compliant systems locally, shortening lead-times and lowering landed costs. The compound effect is sustained volume growth and higher share for coatings validated through accredited third-party testing.

Retro-fit Demand in Aging Offshore Platforms

Corrosion under insulation is a chronic problem for North Sea and Gulf of Mexico structures, many of which operate beyond original design life. Asset owners now budget for thermal-insulating topcoats that also offer corrosion resistance, a dual functionality that enables partial replacement instead of wholesale rebuilding. Tenaris’ USD 182.6 million acquisition of Mattr’s pipe-coating business signals consolidation aimed at bundling anti-corrosion and flow-assurance technologies. Field studies presented through OnePetro highlight coating systems that cut thickness by 30% while improving hydrostatic pressure resistance, critical for subsea jumpers and risers. Quick-cure polyurethane hybrids are popular because they reduce offshore downtime, while remote-application robotics lower labour risk on high sea-states. Given that retrofit budgets are capitalised across 20-year asset lives, the insulation coating market secures recurring maintenance revenue alongside initial project volumes.

Surge in Battery-Gigafactory Construction

More than 180 gigafactory projects are in various planning or construction stages worldwide, each requiring coatings that curb thermal runaway and maintain ambient process temperatures. Resonac recently introduced an insulation coating with 0.03 W m-1 K-1 conductivity for EV refrigerant pipes, delivering up to 40% energy savings compared with bare metal baselines. European plants mandated under the EU Battery Regulation favour halogen-free chemistries that satisfy both fire safety and end-of-life recycling criteria. North American facilities, backed by Inflation Reduction Act incentives, are specifying thin-film aerogel composites that double as passive fire barriers. The result is predictable multi-year demand because coating systems must be reapplied or refurbished during scheduled line overhauls. In addition, secondary markets arise for containerised energy-storage enclosures that need similar thermal-event mitigation.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fire-safety certification delays for novel chemistries | -0.8% | Global, particularly stringent in EU and North America | Medium term (2-4 years) |

| Skilled-applicator shortage in emerging markets | -0.6% | APAC emerging markets, Latin America, MEA | Short term (≤ 2 years) |

| Volatility in epoxy & isocyanate feedstock prices | -1.1% | Global, supply chain concentrated in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fire-Safety Certification Delays for Novel Chemistries

Advanced aerogel or intumescent systems must clear stringent tests such as NFPA 275 and EN 13381-8 before market release. UL Solutions notes that full evaluation cycles for innovative chemistries can extend beyond 15 months, especially when multiple fire, smoke, and toxicity metrics are required. Because building authorities rely on ICC-ES reports, suppliers must generate exhaustive fire-test data and engineering analyses, which raises market-entry costs and lengthens commercialisation timelines. Any failed test forces a reformulation loop, delaying revenue and eroding first-mover advantage. Established products therefore enjoy an incumbency edge, and project owners sometimes default to older systems to meet construction schedules. The bottleneck slows diffusion of next-generation coatings even when they promise superior thermal performance, limiting near-term growth in the insulation coating market.

Volatility in Epoxy & Isocyanate Feedstock Prices

Epoxy resins depend on bisphenol-A and epichlorohydrin supply chains centred in China, South Korea, and Taiwan. The U.S. International Trade Commission ruled in May 2025 that imports from key Asian exporters injure domestic producers, opening the door for anti-dumping duties that could inflate U.S. input costs[3]U.S. International Trade Commission, “Epoxy Resin Injury Determination,” usitc.gov. Chinese BPA producers operated at a loss of Yuan 842 per tonne on average in H1 2024 amid capacity additions, creating price whipsaws that complicate long-term purchasing agreements. Storm-related shutdowns in the U.S. Gulf Coast further demonstrate supply risk, with 69% of composites fabricators reporting resin shortages after the 2024 winter storm. Manufacturers pass some cost increases through surcharges, but margin compression still occurs when contracts fix prices for six months or longer. Feedstock volatility thus subtracts momentum from the insulation coating market until bio-based or recycled alternatives scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Acrylic dominance faces advanced material challenge

Acrylic formulations commanded 34.72% of the insulative coating market in 2025, a position earned through decades of regulatory acceptance and competitive pricing. These water-borne or solvent-borne systems deliver balanced adhesion, UV stability, and workability that make them staples in architectural and light-industrial settings. The insulation coating market size for acrylics equalled USD 3.99 billion in 2025 and is expanding, but growth is moderate as users weigh higher-performance options for demanding conditions. Epoxy-based products follow, prized for chemical resistance and strong substrate bonding in oil, gas, and petrochemical installations. Polyurethane technologies slot between acrylic and epoxy solutions by offering flexibility for substrates that experience thermal cycling, and bio-based grades are entering pilot production to meet sustainability mandates.

The “Other Product Types” cluster shows the strongest trajectory at a 7.12% CAGR as aerogel, yttria-stabilised zirconia, and other ceramic-filled formulations prove their value in cryogenic or ultra-high-temperature service. These advanced materials lower thermal conductivity to 0.01-0.03 W m-1 K-1 and enable coatings up to 50% thinner than legacy systems. Pilot projects on aerospace turbine blades and concentrated solar power receivers illustrate the technology-push pathway, while LNG and battery segments supply near-term volume. Yttria-stabilised zirconia continues to dominate extreme-heat environments, and the U.S. Department of Energy recently validated yttrium-aluminium-garnet topcoats for operation above 1 300 °C . As costs drop, advanced materials are likely to erode acrylic share in industrial applications, yet acrylics will maintain a sizeable presence where cost and code compliance outweigh performance gains.

By End-User Industry: Oil and gas leadership amid diversification

Oil and gas accounted for 27.20% of the insulative coating market in 2025, equivalent to a USD 3.13 billion slice of the insulative coating market size. Offshore platforms, LNG liquefiers, and cross-country pipelines require thermal and anti-corrosion performance that justifies premium pricing. New projects in Qatar, Texas, and Mozambique lock in multi-year demand, while retrofit campaigns sustain steady aftermarket volumes. Construction follows as the second-largest segment, propelled by continuous insulation requirements in building codes. Although individual building projects are smaller than LNG trains, the aggregate volume across commercial roofs and wall assemblies represents a significant opportunity for acrylic and polyurethane coatings.

The fastest growth belongs to “Other End-User Industries,” rising at a 7.62% CAGR as battery manufacturing, power generation, and data-centre cooling drive specialised thermal-management needs. High-energy-density facilities adopt coatings that resist thermal runaway propagation, and renewable energy installations use topcoats to minimise heat gain on equipment housings. Chemical and petrochemical plants maintain dependable consumption patterns for epoxy and ceramic solutions that handle corrosive process chemistries. Aerospace and marine remain niche by volume but act as technology incubators that later migrate into higher-volume industrial sectors. Diversification reduces dependency on oil prices and broadens the revenue base for suppliers in the insulation coating market.

Geography Analysis

Asia-Pacific led with 46.88% of the insulative coating market in 2025 and is forecast to grow at an 7.86% CAGR through 2031. Regional expansion is backed by massive industrial projects in China and India alongside manufacturing investments in Vietnam, Indonesia, and Malaysia. China’s domestic raw-material capacity, from BPA to zirconia powder, gives local producers cost leverage and reduces currency-exchange exposure for regional sales contracts. India accelerates capacity additions, as seen in the CPVC resin scale-up at Dahej, which spurs downstream demand for compatible coatings. Southeast Asia’s refinery and petrochemical build-out further anchors volume.

North America represents a mature yet innovation-rich market driven by stringent building-energy codes, offshore platform refurbishments in the Gulf of Mexico, and accelerating gigafactory construction. The insulative coating market share for North America remained robust in 2025 owing to tight alignment between regulatory frameworks and advanced product offerings. Federal incentives under the Inflation Reduction Act foster domestic battery supply chains, which elevates coating demand for thermal-runaway control. The region also benefits from well-established training networks that mitigate skilled-applicator shortages experienced elsewhere.

Europe ranks third by revenue but leads in sustainability mandates that prioritise low-VOC and bio-based formulations. Investments in hydrogen production, district-heating upgrades, and offshore wind fabrication yards underpin stable demand. South America records mid-single-digit growth, boosted by pre-salt field developments off Brazil, while Middle East and Africa activity centres on petrochemical expansion and infrastructure modernisation. The insulation coating market size for emerging Gulf Cooperation Council projects is rising as developers specify advanced coatings to manage desert heat and aggressive marine atmospheres.

Competitive Landscape

The competitive landscape is moderately fragmented, with key players like PPG, AkzoNobel, Sherwin-Williams, Hempel, and Jotun leveraging global distribution, application expertise, and regulatory knowledge to secure major contracts. Sustainability, particularly carbon footprint disclosures, increasingly influences tenders, prompting suppliers to launch life-cycle-assessment dashboards. Price competition is intense for standard acrylic and epoxy systems, but differentiated products achieve margins above 18%. Suppliers invest in installer training, digital tools, and asset-management platforms to monitor coating conditions. The market rewards firms balancing raw material cost control with technology investments and on-site application support, as the shift toward full-solution offerings blurs the line between product vendors and service providers.

Insulation Coating Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Kansai Paint Co., Ltd.

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Hempel launched Hempatherm IC, its first thermal insulation coatings system, addressing the growing need to reduce maintenance costs and manage Corrosion Under Insulation (CUI). The system, comprising Hempatherm IC 170 and IC 175, offers high film build capabilities, superior thermal insulation, and CUI mitigation, extending the service life of industrial equipment.

- February 2024: Engineers from IIT Bombay developed a hydrophobic epoxy composite coating that reflects solar heat and reduces heat absorption. This thin 65-micrometer coating minimizes heat conduction and provides high infrared reflectance, enhancing thermal insulation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the insulation coatings market as every liquid, powder, or vacuum-deposited layer engineered to curb heat flow across metal, concrete, or composite surfaces on pipes, tanks, building envelopes, and mobile assets such as ships and vehicles.

Scope Exclusions: Conventional bulk insulation boards, wraps, and purely electrical varnishes are not covered.

Segmentation Overview

- By Product Type

- Acrylic

- Epoxy

- Polyurethane

- Yttria-Stabilized Zirconia

- Other Product Types (Aerogel-based, etc.)

- By End-User Industry

- Oil and Gas

- Chemical and Petrochemical

- Construction

- Automotive

- Marine

- Aerospace

- Other End-User Industries (Power Generation, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and short surveys with plant maintenance heads, coating formulators, EPC contractors, and regional distributors across Asia-Pacific, North America, Europe, and the Gulf validate average selling prices, applied-film thickness, and service-life assumptions that secondary sources rarely quantify.

Insights from these conversations fill data gaps and help us triangulate forecasts with confidence.

Desk Research

We begin with public data on energy-efficiency codes and process-heat losses from agencies such as the U.S. DOE and Eurostat, then parse national customs ledgers that list heat-resistant paint exports across fifteen key countries.

White papers from ASTM, the National Association of Corrosion Engineers, and the International Marine Coatings Association clarify service-temperature bands that anchor product splits.

Corporate filings, refinery turnaround schedules, and capacity announcements enrich volume cues, while timely news gathered through D&B Hoovers and Dow Jones Factiva alerts us to pricing shifts and new plant start-ups.

The sources named illustrate the range; many additional references underpin our data checks.

Market-Sizing & Forecasting

A top-down reconstruction starts with global resin production, adjusts for trade flows, and allocates demand by end-use; selective bottom-up roll-ups of coated-surface area times sampled film thickness verify totals before adjustments.

Key variables like average applied thickness, coating yield per liter, refinery turnaround cycles, expansion of district-heating pipe networks, and regional ASP movement feed the model.

Multivariate regression links these drivers to macro outputs such as industrial value added and new floor-space completions, after which scenario analysis applies policy and currency sensitivities to the base case.

Gap handling relies on regional distributor mark-ups and price elasticity checks where hard data are sparse.

Data Validation & Update Cycle

Outputs undergo variance tests against historical energy-intensity ratios and peer-group revenues.

Senior analysts review anomalies, and when quarterly earnings or regulatory shocks alter fundamentals, we reopen the model; otherwise, figures refresh annually and a last-minute sweep ensures clients receive the latest view.

Why Mordor's Insulation Coating Baseline Commands Reliability

Published estimates differ because firms adopt varying resin sets, service-temperature cut-offs, and exchange-rate dates. By limiting scope to coatings delivering less than or equal to 0.1 W/mK thermal conductivity and reporting a balanced base year, Mordor minimizes bias. For context, Mordor's 2025 revenue baseline stands at USD 11.5 billion. Recent external releases range from USD 9.7 billion in 2022 to USD 10.4 billion in 2024, depending on the publisher.

Key gap drivers include some publishers folding bulk mineral wool into totals, others using list prices that ignore regional discounts, and a few relying on datasets refreshed only every three years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.5 bn (2025) | Mordor Intelligence | - |

| USD 10.4 bn (2024) | Global Consultancy A | excludes sub-200 C products and applies heavier price discounts |

| USD 9.7 bn (2022) | Trade Journal B | older currency baselines and no Asia-Pacific distributor mark-ups |

| USD 10.2 bn (2023) | Industry Association C | bundles electrical insulation varnishes with thermal coatings |

The comparison shows that once scope, price realization, and refresh cadence are harmonized, our estimate offers the most reproducible baseline for planning decisions, giving decision-makers a dependable point of departure.

Key Questions Answered in the Report

What is the current Insulation Coating Market size?

The market was valued at USD 12.31 billion in 2026 and is forecast to reach USD 17.31 billion by 2031.

Which region leads the insulative coating market?

Asia-Pacific leads with 46.88% share in 2025 and is the fastest growing at an 7.86% CAGR through 2031.

Which product type dominates sales?

Acrylic formulations held 34.72% revenue share in 2025 due to versatility and cost efficiency.

Why are building-energy codes important for demand?

New rules such as the 2024 IECC mandate higher R-values, driving increased use of performance-certified insulative coatings to meet compliance.

Page last updated on: