Mild Traumatic Brain Injury Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 7.18 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

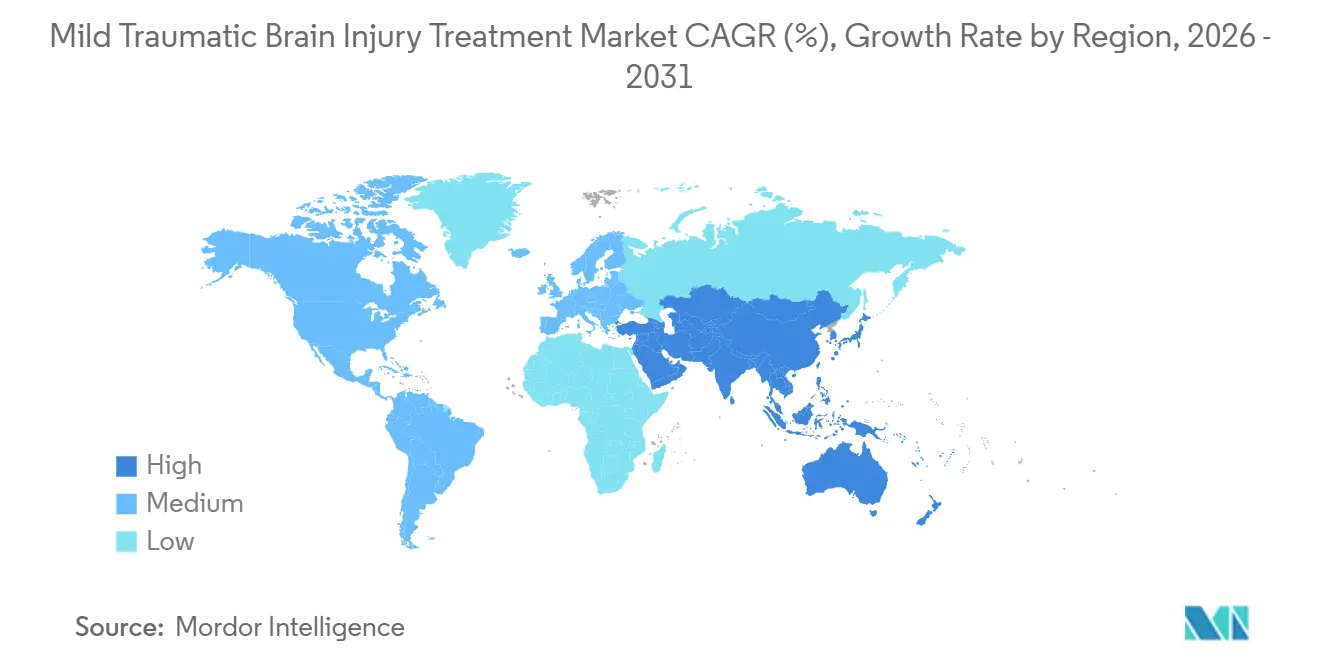

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

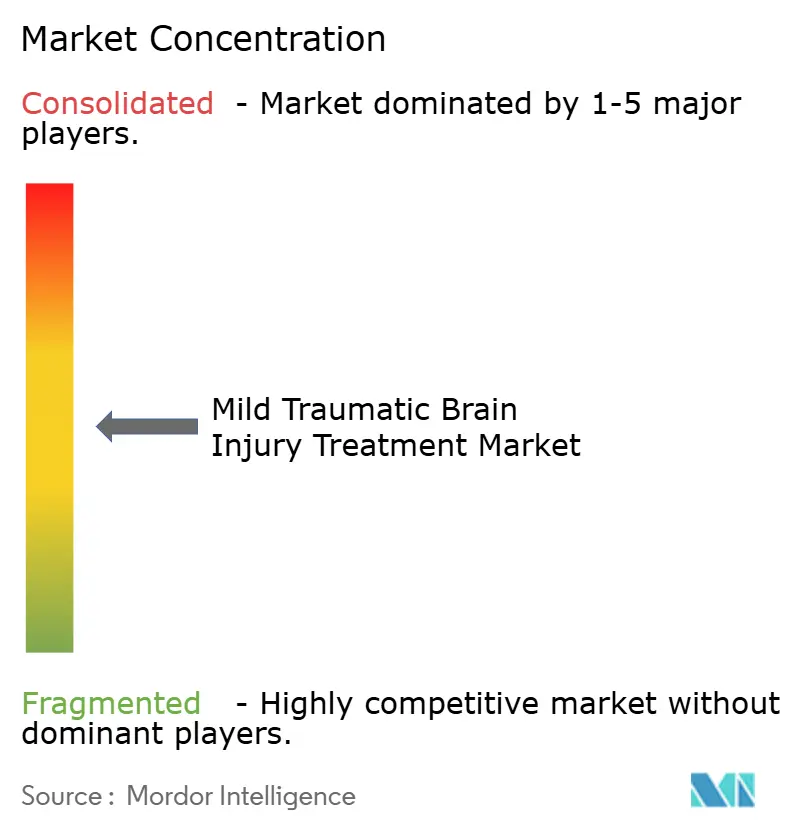

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mild Traumatic Brain Injury Treatment Market Analysis by Mordor Intelligence

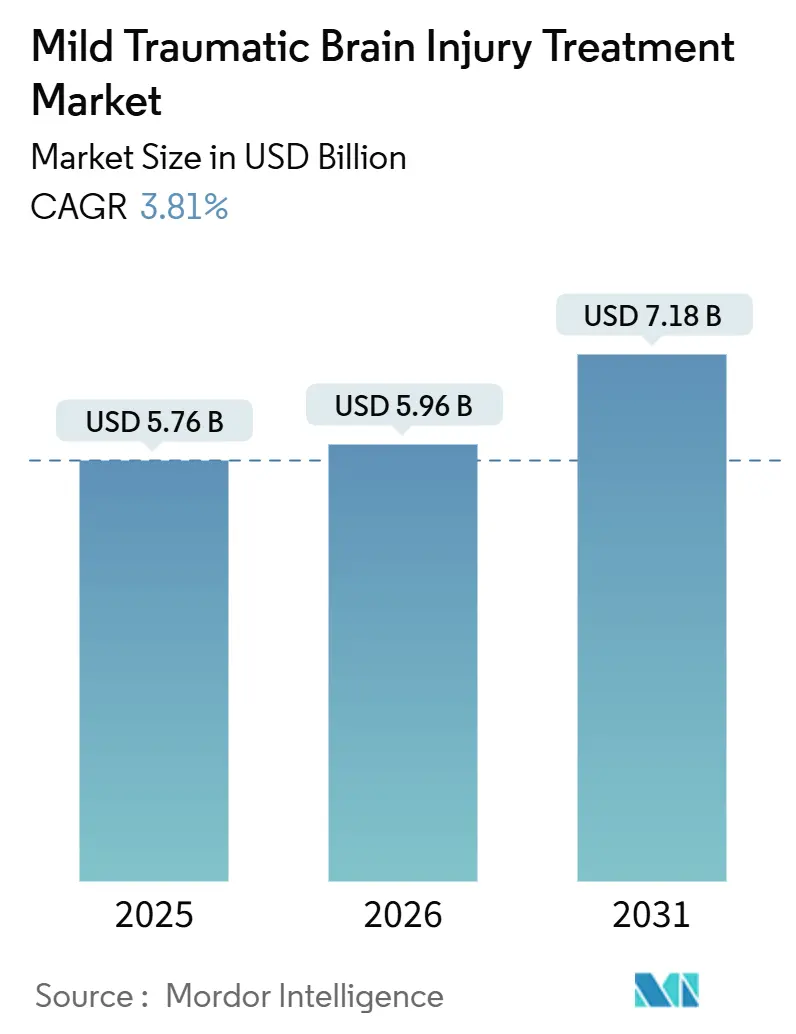

The Mild Traumatic Brain Injury Treatment Market size is expected to grow from USD 5.76 billion in 2025 to USD 5.96 billion in 2026 and is forecast to reach USD 7.18 billion by 2031 at 3.81% CAGR over 2026-2031.

Blood-based biomarker assays are steadily replacing routine CT scans in emergency departments, lowering radiation exposure and shortening length of stay. Japan’s conditional 2024 approval of trofinetide signaled that neuroprotective pharmacotherapy is moving from an experimental adjunct to a reimbursable standard, prompting developers in the United States, Australia, and South Korea to accelerate filings. Military-funded point-of-care programs have compressed biomarker validation timelines from 8 years to under 3, seeding dual-use platforms that civilian providers now adopt to reduce liability and costs. Across high-income regions, payers are shifting sub-acute care to outpatient clinics and tele-rehabilitation, while emerging economies are mandating rapid screening protocols to reduce mortality from road traffic injuries. Vendors capable of bundling fast diagnostics with clear reimbursement codes and outcome-based contracts are positioned to capture above-trend share as tariff headwinds ease and conditional drug approvals expand.

Key Report Takeaways

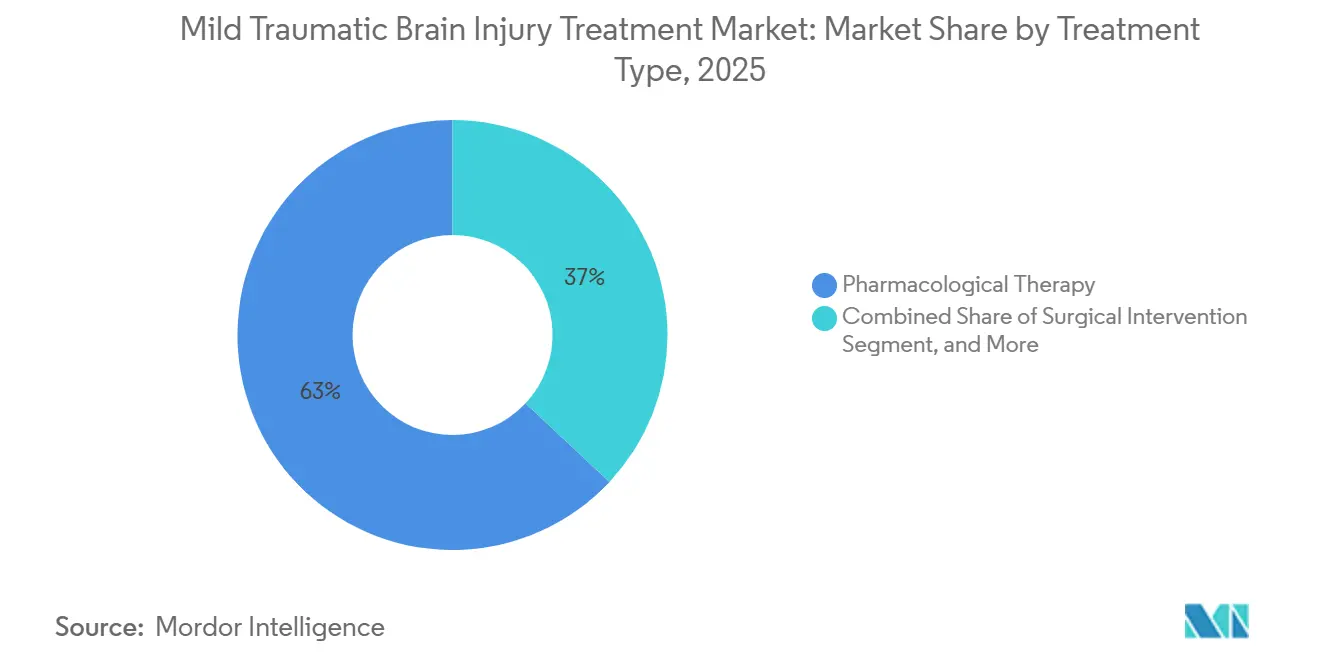

- By treatment type, pharmacological therapy led with 63.02% of the mild traumatic brain injury treatment market share in 2025. Rehabilitation & assistive technologies are forecast to register a 5.85% CAGR through 2031, the fastest among treatment categories.

- By cause of injury segment, falls accounted for 54.27% share of the mild traumatic brain injury treatment markett size in 2025. Sports & recreation injuries are projected to expand at a 7.98% CAGR between 2026 and 2031, outpacing all other causes.

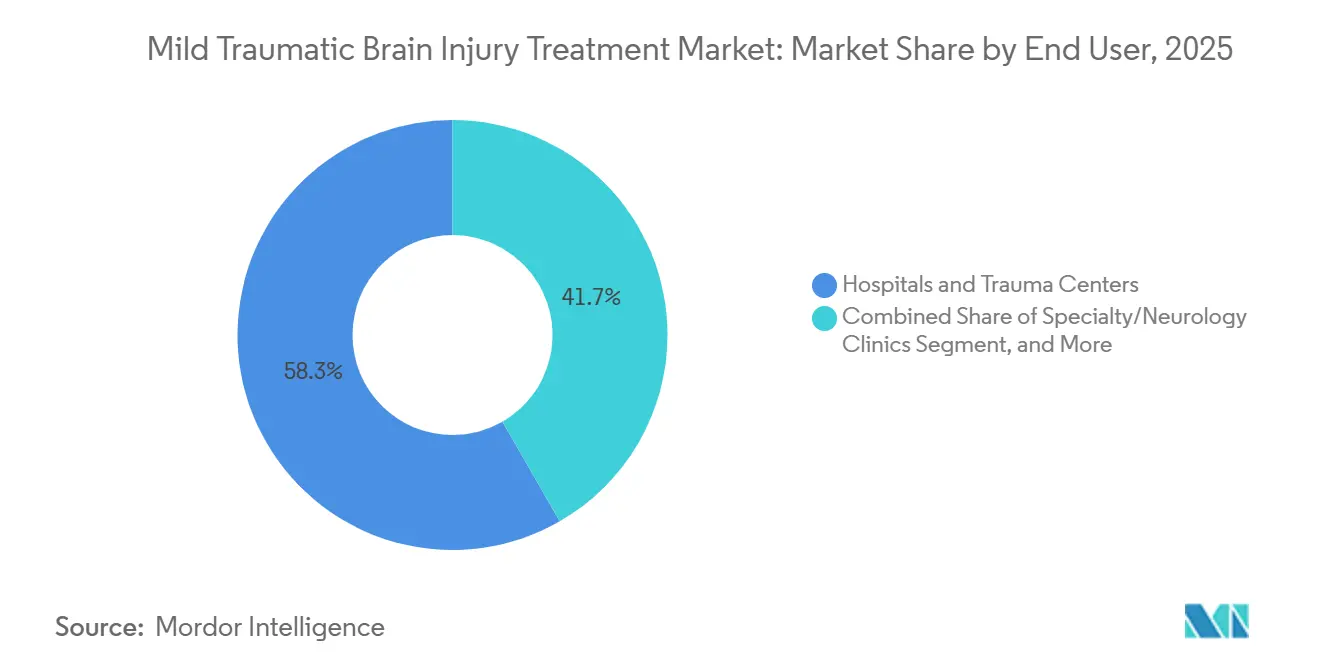

- By end user, hospitals & trauma centers held 58.32% of the mild traumatic brain injury treatment market in 2025, whereas specialty/neurology clinics are advancing at a 6.78% CAGR through 2031.

- By geography, North America accounted for 46.18% of revenue in 2025; Asia-Pacific is the fastest-growing region, with a 9.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mild Traumatic Brain Injury Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of mTBI From Falls & Road Traffic Accidents | +0.9% | Global, with acute concentration in North America and Europe due to aging demographics | Long term (≥ 4 years) |

| Rapid Adoption of Advanced Imaging & Blood-Based Diagnostics | +1.2% | North America and Europe lead; Asia-Pacific adoption accelerating post-2025 regulatory harmonization | Medium term (2-4 years) |

| Expanding Clinical Pipeline of Neuro-Protective & Regenerative Drugs | +0.7% | Global, with Japan and U.S. as early-approval jurisdictions; EU following conditional pathways | Long term (≥ 4 years) |

| Post-COVID Surge in Remote Neuro-Rehabilitation & Tele-Health Demand | +0.6% | North America and Western Europe; emerging in urban Asia-Pacific hubs | Short term (≤ 2 years) |

| Japan's AKUUGO Conditional Approval Spurring Global Regulatory Momentum | +0.5% | Japan primary; spillover to Australia, South Korea, and EU via regulatory precedent | Medium term (2-4 years) |

| Military-Funded AI Point-of-Care Biomarker Programs Accelerating Translation | +0.4% | United States and NATO allies; technology transfer to civilian trauma centers underway | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of mTBI From Falls & Road Traffic Accidents

Falls and vehicle crashes generate more than 70% of mild TBI globally, but the epidemiology diverges by income level. Geriatric falls dominate hospital admissions in North America, Europe, and Japan, whereas road-traffic collisions afflict working-age populations in India, China, and sub-Saharan Africa. The World Health Organization recorded 1.19 million road-traffic deaths in 2023 and estimated that up to half of the 20-50 million survivors sustain head trauma.[1]World Health Organization, “Global Status Report on Road Safety 2024,” who.int Japan reported a 31% increase in fall-related TBI hospitalizations among citizens aged 75+ between 2020 and 2024. These patterns fuel demand for rapid triage tools that direct patients to observation, imaging, or neurosurgical care within the first hour.

Rapid Adoption of Advanced Imaging & Blood-Based Diagnostics

Point-of-care biomarker panels are rewriting the economics of emergency departments. Abbott’s i-STAT TBI test, cleared by FDA and reimbursed by Medicare at USD 135 per assay, cut CT use by 38% and reduced median stay from 4.2 hours to 2.8 hours across 11 U.S. hospitals studied in 2024. Military prototypes proved rugged and fast, demonstrating 92% sensitivity and 87% specificity in forward surgical teams in 2025. Reimbursement certainty is now the critical catalyst for adoption as European regulators move to harmonize companion diagnostic pathways by 2027.

Expanding Clinical Pipeline of Neuro-Protective & Regenerative Drugs

Trofinetide became the first disease-modifying therapy conditionally approved for pediatric TBI in Japan in 2024, reducing symptom duration by 34% against placebo. U.S. Phase III trials of progesterone analog OXE-103 and Hope Biosciences’ stem-cell protocol target NDA filings in 2026, buoyed by a 73% surge in exosome-based patent activity between 2024 and 2025. Sponsors view conditional approval pathways and breakthrough designations as reducing capital risk and spurring broader investment.

Post-COVID Surge in Remote Neuro-Rehabilitation & Tele-Health Demand

Virtual platforms that expanded during the pandemic remain sticky. In 2025, 68% of 412 surveyed rehabilitation clinics offered hybrid programs, versus 11% in 2019. CMS preserved parity billing for remote physical and speech therapy through 2025, while 38 states enacted permanent laws, sustaining 3.2 times pre-pandemic tele-rehab volumes. Wearable neurostimulation devices such as StimRouter Neuro shipped 14,200 units in 1H 2025, pointing to rising payer acceptance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of FDA-Approved Disease-Modifying Therapies | -0.8% | Global, with most acute impact in North America and Europe where reimbursement hinges on regulatory approval | Long term (≥ 4 years) |

| High Cost of Advanced Treatment & Rehabilitation Technologies | -0.6% | Emerging markets in Asia-Pacific, Middle East, and South America; affordability gaps persist despite technology maturation | Medium term (2-4 years) |

| Low Clinician Adoption of CT-Substituting Biomarker Tests | -0.5% | United States and Europe; workflow integration and reimbursement uncertainty slow uptake | Short term (≤ 2 years) |

| US Tariffs Inflating Neuro-Monitor Device Supply-Chain Costs | -0.3% | United States primary; indirect impact on global pricing as vendors adjust manufacturing footprints | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Absence of FDA-Approved Disease-Modifying Therapies

The FDA has yet to authorize a disease-modifying drug for TBI, confining U.S. prescribing to symptomatic agents and capping growth potential. Only 14 mTBI compounds were in Phase II/III globally in 2025 versus 87 for Alzheimer’s, underscoring investor caution.[2]Biotechnology Innovation Organization, “Neuroscience Pipeline Report 2025,” bio.org CMS denies coverage for investigational agents, deterring early adopter hospitals.

High Cost of Advanced Treatment & Rehabilitation Technologies

Robotic gait-training systems cost between USD 150,000 and USD 400,000. EksoNR costs USD 180,000 plus USD 22,000 in annual service, limiting penetration to elite centers; 73% of 2025 sales were in North America and Europe. India’s per-capita spend of USD 73 leaves most public hospitals reliant on manual therapy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Pharmacological Dominance Meets Digital Rehabilitation Momentum

Pharmacological therapy accounted for 63.02% of the Mild Traumatic Brain Injury Treatment market share in 2025, driven by large patient volumes and reimbursed symptom control. Growth, however, is muted without disease-modifying agents, and payers are testing bundled payments that reward functional recovery rather than prescription counts. Rehabilitation & Assistive Technologies have a smaller base but will compound at a 5.85% CAGR to 2031, supported by persistent telehealth infrastructure and robotic platforms that shorten time to independent ambulation by 18 days on average. Surgical Intervention remains niche for hematoma evacuation or refractory intracranial pressure, and its share is stable as improved triage curtails unnecessary procedures.

EksoNR deployments rose from 54 centers in 2024 to 89 in mid-2025, aided by Japan’s 2025 insurance coverage of JPY 12,000 (USD 80) per robotic session. Payer alignment with outcome-based models is expected to tilt capital budgets toward digital and wearable solutions more than pharmacological line extensions.

By Cause of Injury: Sports Concussions Drive Standardization

Falls captured a 54.27% share of the mild traumatic brain injury treatment market size in 2025, reflecting aging demographics in OECD nations. Sports & recreation cases, though smaller, will climb at a 7.98% CAGR through 2031 as youth and professional leagues impose mandatory baseline testing and sideline biomarker screening. All 50 U.S. states require cognitive baseline tests by 2024. Abbott sold 14,200 i-STAT units to athletic programs during the 2024-2025 academic year, illustrating new demand pockets.

Motor-vehicle collisions still dominate in India and China, where helmet use lags, and tertiary hospitals must now conduct blood-based screening within 60 minutes of admission under a 2025 Chinese mandate. Violence-related head injuries rise in conflict zones, but absolute volumes remain modest compared with falls and sports incidents.

By End User: Specialty Clinics Capture Sub-Acute Complexity

Hospitals & trauma centers accounted for 58.32% of 2025 end-user revenue, yet the average stay for mild cases dropped to 1.6 days as payers push for early discharge. Specialty / Neurology Clinics are projected to grow at a 6.78% CAGR, fueled by portable EEG systems such as BrainScope Ahead 300 that allow same-day concussion clearance without hospital referral. Mild Traumatic Brain Injury Treatment market size for Specialty Clinics is on pace to double its share by 2031 as outpatient reimbursement aligns with tele-rehab and chronic symptom management.

Rehabilitation centers & home-care settings benefit from CMS telehealth parity, which remains in effect through 2025, enabling therapists to bill for remote cognitive sessions at in-clinic rates. Technology integration, especially cloud-enabled EEG and wearable sensors, differentiates providers and supports payer preference for lower-cost care pathways.

Geography Analysis

North America generated 46.18% of 2025 revenue, led by the United States, where 127 hospital systems adopted Abbott’s i-STAT and reduced CT exposure by 38%, saving USD 420 per patient. Canada followed in March 2025, reimbursing CAD 180 (USD 133) per assay in provincial trauma centers. Mexico is expanding neuro-rehab under IMSS, but still relies on out-of-pocket diagnostics.

Asia-Pacific will post a 9.34% CAGR, the fastest worldwide. China’s 2025 screening mandate covers 1,400 tertiary hospitals and 2.1 million annual TBI cases. Japan’s trofinetide approval and robotic rehab reimbursement spur local adoption, while Australia and South Korea align conditional drug pathways. India remains two-tiered, with private metros installing biomarker labs and rural districts lacking CT access.

Europe presents moderate growth amid payer scrutiny. Germany reimburses EUR 120 (USD 130) per biomarker test as of June 2025, launching adoption in 89 hospitals. The NHS Virtual Wards program served 8,900 TBI patients remotely in 2025, cutting readmissions by 19%. Southern and Eastern Europe lag in high-cost robotic setups, though EU structural funds may narrow gaps post-2027.

Middle East & Africa and South America are underpenetrated. Brazil restricts biomarker and robotic coverage to private hospitals in São Paulo and Rio, while Saudi Arabia earmarked USD 320 million in 2024 to upgrade 18 trauma centers with advanced monitors. Affordability and supply-chain tariffs limit broader uptake until local assembly and donor funding expand.

Competitive Landscape

Abbott dominates rapid diagnostics following Medicare reimbursement, posting a 41% sequential increase in adoption in 2025 across 127 U.S. centers. BrainScope and InfraScan serve the rural and military segments with battery-powered EEG and near-infrared tools. Hope Biosciences leads regenerative medicine patents with 14 filings in 2024-2025, positioning it for leadership in chronic syndrome.

Medtronic and Integra LifeSciences anchor surgical kits but face demand erosion as non-invasive triage lowers surgical volumes. GE Healthcare’s 7.0 T MRI broadens detection of microstructural lesions, yet capital intensity limits early uptake. Vendors compete on three axes: assay turnaround time, reimbursement alignments, and outcome-based contracts that shift risk from payers to manufacturers. Dual-use certifications under military procurement rules offer a durable revenue channel and a quality imprimatur valued by civilian buyers.

Mild Traumatic Brain Injury Treatment Industry Leaders

NeuroVive Pharmaceutical AB

TEVA Pharmaceutical Industries Ltd.

Integra LifeSciences Corporation

Neuren Pharmaceuticals Ltd.

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oragenics received final HREC approval in Australia to begin its Phase IIa trial of ONP‑002, an intranasal neuroprotective therapy targeting concussion/mTBI. Itr represents one of the few drug‑based interventions advancing beyond Phase I in a field historically dominated by supportive care.

- February 2026: Researchers from IRBLleida, UOC, UdL and HUAV published a predictive model in BMC Emergency Medicine to identify complications within the first 48 hours after mild or moderate TBI. AI‑based risk stratification tools are becoming a major market segment, especially in emergency departments and sports medicine.

- February 2026: Australia’s MRFF announced up to USD 5 million for research targeting improved acute and long‑term outcomes for moderate–severe TBI and better uptake of best‑practice care for mild TBI, including concussion management.

- February 2026: Oragenics, Inc. previewed 2026 milestones for advancing ONP-002, a novel intranasal neurosteroid. Positioned as the potential first pharmacological treatment for concussion/mTBI, delivered via proprietary intranasal technology.

Global Mild Traumatic Brain Injury Treatment Market Report Scope

As per the scope of the report, a patient with mild traumatic brain injury is a person who has had a traumatically induced physiological disruption of brain function. It has been recognized that patients with a mild traumatic brain injury can exhibit persistent emotional, cognitive, behavioral, and physical symptoms, alone or in combination, which may produce a functional disability.

The Mild Traumatic Brain Injury Treatment Market Report is Segmented by Treatment Type (Pharmacological Therapy, Surgical Intervention, Rehabilitation & Assistive Technologies), Cause of Injury (Falls, Motor-Vehicle Traffic, Sports & Recreation, Violence & Others), End User (Hospitals & Trauma Centers, Specialty / Neurology Clinics, Rehabilitation Centers & Home-care Settings), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Pharmacological Therapy |

| Surgical Intervention |

| Rehabilitation & Assistive Technologies |

| Falls |

| Motor-Vehicle Traffic |

| Sports & Recreation |

| Violence & Others |

| Hospitals & Trauma Centers |

| Specialty / Neurology Clinics |

| Rehabilitation Centers & Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Pharmacological Therapy | |

| Surgical Intervention | ||

| Rehabilitation & Assistive Technologies | ||

| By Cause of Injury | Falls | |

| Motor-Vehicle Traffic | ||

| Sports & Recreation | ||

| Violence & Others | ||

| By End User | Hospitals & Trauma Centers | |

| Specialty / Neurology Clinics | ||

| Rehabilitation Centers & Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the mild traumatic brain injury treatment market in 2026?

The mild traumatic brain injury treatment market size is USD 5.96 billion in 2026, on track to reach USD 7.18 billion by 2031.

What is the forecast CAGR for mild TBI treatments?

The market is projected to grow at a 3.81% CAGR from 2026 to 2031.

Which treatment segment is expanding the fastest?

Rehabilitation & assistive technologies will post a 5.85% CAGR through 2031, outpacing pharmacological and surgical categories.

Why are blood-based biomarkers important for mild TBI care?

Biomarkers reduce CT use by 38%, cut emergency length of stay by 1.4 hours, and qualify for Medicare reimbursement, improving both safety and economics.

Which region will grow quickest through 2031?

Asia-Pacific will lead with a 9.34% CAGR, propelled by Chinese and Japanese policy mandates and rising healthcare investment.

Page last updated on: