Peripheral Nerve Injuries Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

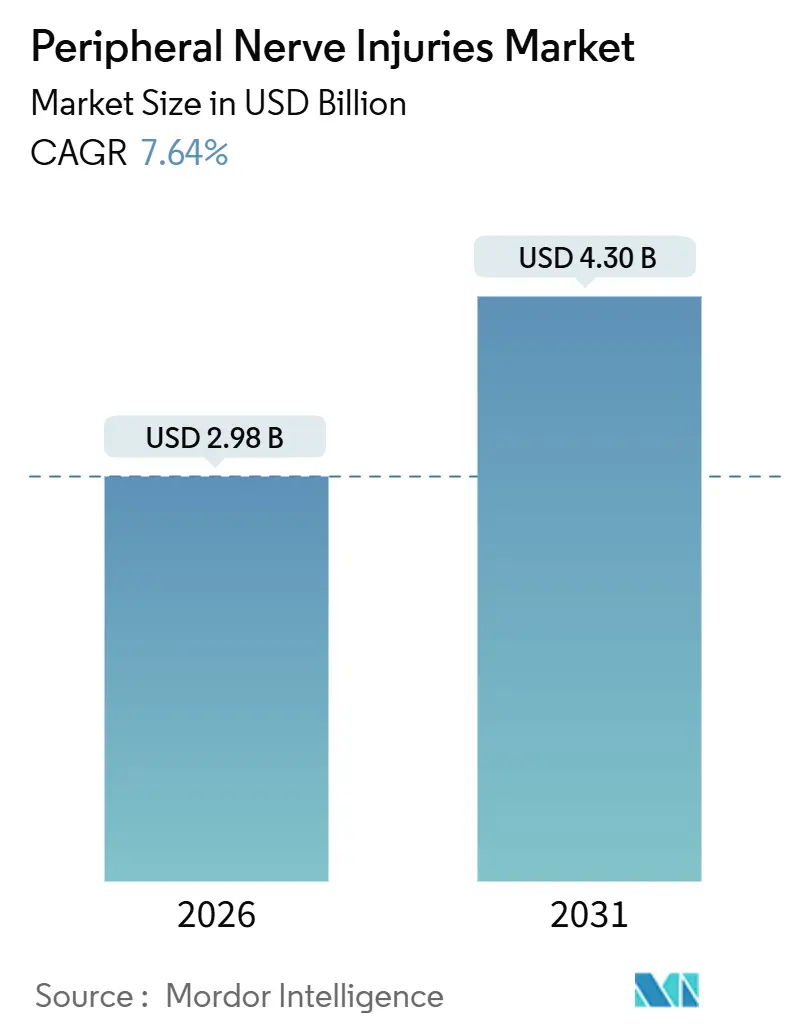

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 4.30 Billion |

| Growth Rate (2026 - 2031) | 7.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripheral Nerve Injuries Market Analysis by Mordor Intelligence

The Peripheral Nerve Injuries Market size is estimated at USD 2.98 billion in 2026, and is expected to reach USD 4.30 billion by 2031, at a CAGR of 7.64% during the forecast period (2026-2031).

Momentum stems from a decisive shift toward early microsurgical repair and the growing acceptance of bioengineered conduits, nerve wraps, and processed allografts. Diabetes-related neuropathy, which affects 33%–50% of diabetic patients, guarantees a large clinical reservoir even during economic slowdowns. In December 2025, the U.S. Food and Drug Administration cleared AxoGen’s Avance Nerve Graft for sensory nerve gaps, underscoring a more flexible regulatory stance that now extends beyond motor-nerve repairs. Payer policies are evolving just as quickly; Medicare’s 2025 National Coverage Determination unbundled reimbursement for processed allografts longer than 5 cm, allowing hospitals to recoup device costs and encouraging wider adoption. Together, these forces are pushing the peripheral nerve injuries market toward broader clinical uptake and faster innovation cycles.

Key Report Takeaways

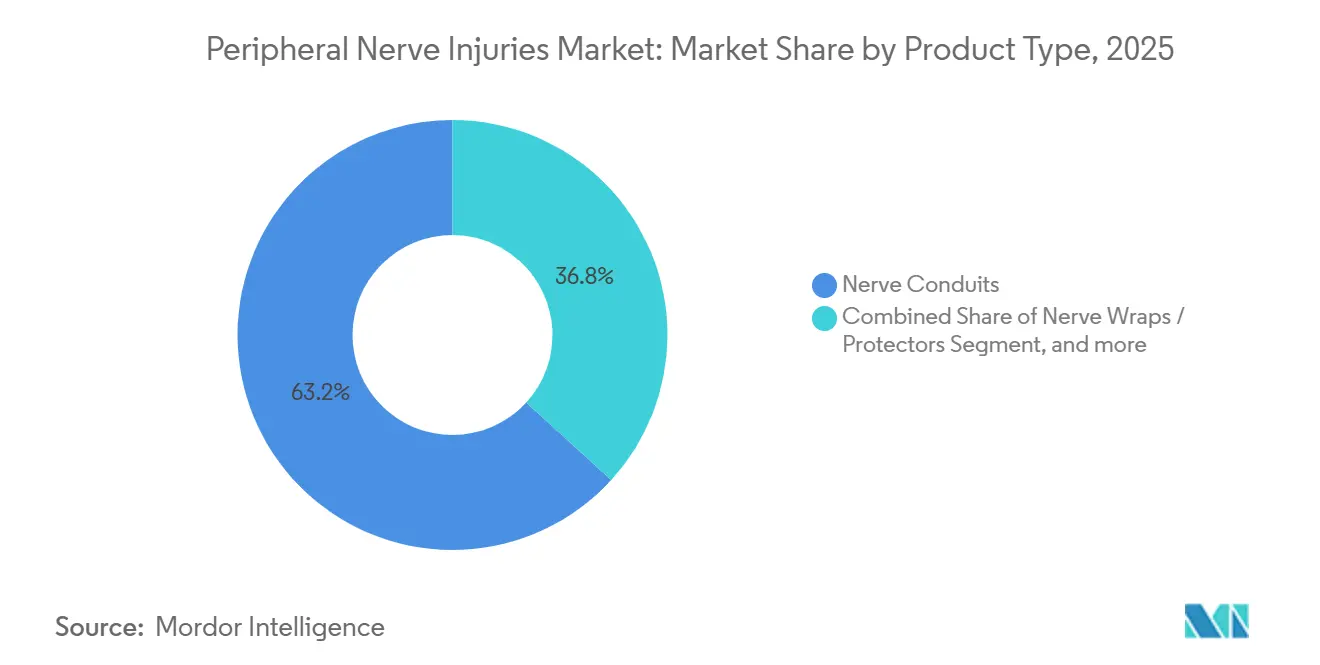

- By product type, nerve conduits led with 63.21% market share for peripheral nerve injuries in 2025, while nerve wraps are projected to expand at a 9.54% CAGR through 2031.

- By surgery or technique, direct repair accounted for 54.15% of procedures in 2025; stem-cell and regenerative adjuncts are advancing at a 9.76% CAGR.

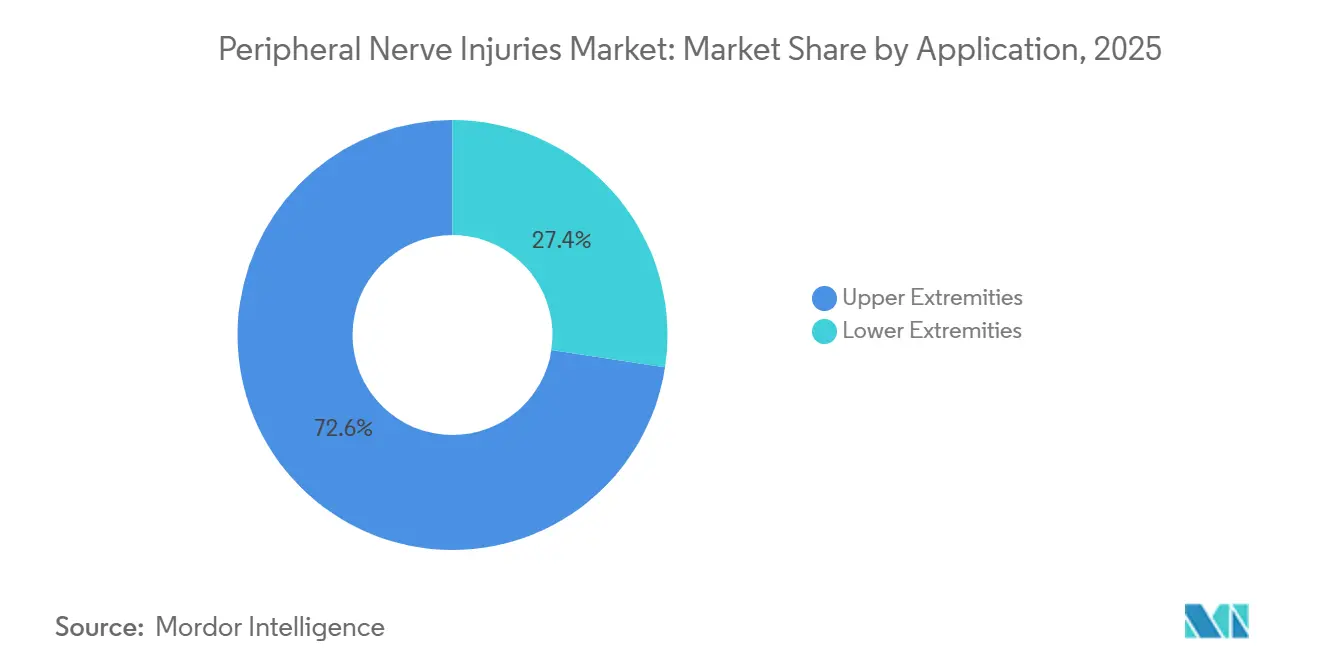

- By application, upper-extremity cases captured 72.6% of revenue in 2025 and are forecast to grow at a 10.55% CAGR.

- By end user, hospitals and clinics held 45.32% of revenue in 2025, whereas ambulatory surgical centers are expanding at a 10.43% CAGR.

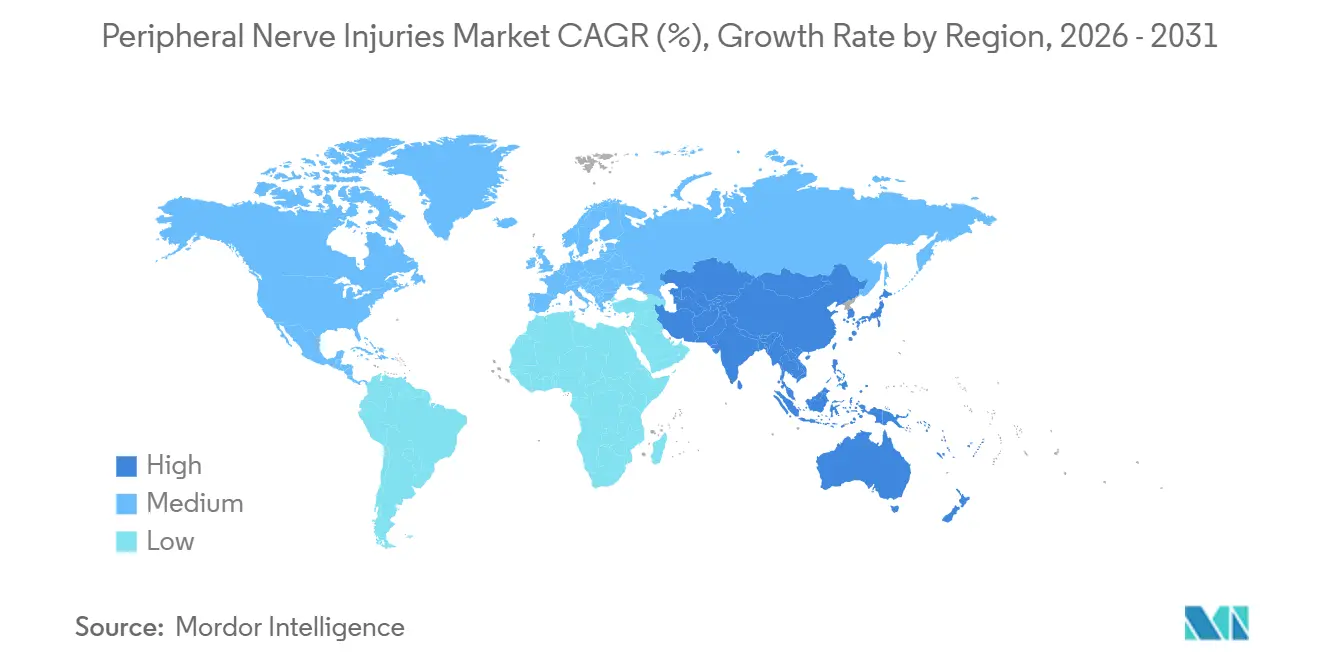

- By geography, North America accounted for 41.25% of 2025 revenue, and Asia-Pacific is the fastest-growing region, with an 8.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Peripheral Nerve Injuries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Peripheral Nerve Injuries | +1.8% | Global hot spots in South Asia and Sub-Saharan Africa | Medium term (2-4 years) |

| Technological Advances in Bioengineered Repair Materials | +2.1% | North America and Europe lead; APAC follows | Long term (≥ 4 years) |

| Favorable Reimbursement and Regulatory Support | +1.5% | North America, UK, Netherlands | Short term (≤ 2 years) |

| Expansion of Outpatient Microsurgical Facilities | +1.0% | Urban North America and APAC | Medium term (2-4 years) |

| Growing Elderly and Diabetic Population Base | +1.2% | China, India, United States | Long term (≥ 4 years) |

| Increasing Investments in Regenerative Medicine and Neurostimulation | +0.9% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Peripheral Nerve Injuries

Trauma registries show peripheral nerve damage in 1.64% of limb fractures, but rates are higher in regions with poor road safety. India recorded over 4 million non-fatal road injuries in 2024, many resulting in brachial plexus or radial-nerve lesions. The World Health Organization warns that road accidents will become the seventh-leading global cause of death by 2030, keeping injury volumes elevated[1]World Health Organization, “Global Status Report on Road Safety,” who.int. In the United States, 3 million emergency visits for falls among adults aged 65 and older in 2024 resulted in thousands of ulnar and peroneal nerve contusions. Together, trauma and an aging population funnel a steady case load into the peripheral nerve injuries market.

Technological Advances in Bioengineered Repair Materials

The National Institutes of Health awarded USD 2.8 million in 2025 to refine 3D-printed conduits that provide topographical cues for Schwann cell migration[2]National Institutes of Health, “R01HD112026 Award Abstract,” nih.gov. AxoGen’s Avive+ Soft Tissue Matrix, launched in June 2024, is already cutting adhesion rates by half, according to early surgeon reports. Polyganics’ Neurolac conduit degrades at a pace matched to axonal growth, mitigating premature resorption. Collectively, these innovations widen the clinical envelope beyond the historic 3 cm conduit limit.

Favorable Reimbursement and Regulatory Support

Medicare’s 2025 ruling guarantees separate payment for processed allografts longer than 5 cm, eliminating longstanding billing uncertainty[3]Centers for Medicare & Medicaid Services, “National Coverage Determination 64910,” cms.gov. The United Kingdom’s NICE green-lighted nerve conduits for digital repairs in March 2025, reinforcing donor-site-sparing techniques in the National Health Service. Japan’s PMDA fast-tracked Toyobo’s Nerbridge conduit in September 2024, awarding 10-year exclusivity under the SAKIGAKE scheme. Such actions expand the scope of reimbursable services and accelerate device adoption.

Expansion of Outpatient Microsurgical Facilities

U.S. ambulatory surgical centers (ASCs) handled 28.6 million procedures in 2024, with hand surgery up 12% year over year. Cedars-Sinai opened a dedicated peripheral nerve suite in its Los Angeles ASC in February 2025, demonstrating that complex microsurgery no longer mandates a hospital stay. Payers reimburse ASC cases at roughly 60% of hospital rates, steering volume toward outpatient settings and sharpening price sensitivity in the peripheral nerve injuries market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure and Implant Costs | -1.3% | Low- and middle-income regions | Short term (≤ 2 years) |

| Clinical Preference for Autograft Gold Standard | -0.9% | North America and Europe | Medium term (2-4 years) |

| Limited Long-Term Outcomes Data | -0.6% | Global | Long term (≥ 4 years) |

| Shortage of Trained Peripheral Nerve Surgeons | -0.5% | Rural and underserved areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure and Implant Costs

Processed allografts run USD 1,000–USD 5,000 per centimeter; a major brachial plexus case can top USD 30,000 in implant expenses alone. India’s Ayushman Bharat caps reimbursement at INR 50,000 (USD 600), forcing surgeons to default to autograft in many cases. Manufacturing economics—donor tissue sourcing, viral inactivation, and cold-chain shipping—make steep near-term price cuts unlikely, especially for smaller hospitals that lack purchasing leverage.

Clinical Preference for Autograft Gold Standard

A 2024 systematic review in Plastic and Reconstructive Surgery found autograft superior for motor gaps over 3 cm by 0.8 points on the Medical Research Council scale. Sixty-two percent of American Society for Surgery of the Hand members surveyed in 2025 preferred autograft for gaps larger than 2 cm, citing familiarity and medico-legal safety. Because fewer conduit cases exist, registries lack the statistical power to prove non-inferiority, reinforcing the status quo and slowing conduit uptake in the peripheral nerve injuries market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conduits Remain Core While Wraps Rapidly Advance

Nerve conduits contributed 63.21% of 2025 revenue, confirming their central role in bridging 1–5 cm gaps in digital, median, and ulnar nerves. This segment retained the largest peripheral nerve injuries market share because surgeons view it as the most versatile device class. Nerve wraps, however, are accelerating at a 9.54% CAGR as evidence mounts that preventing perineural scarring preserves glide and minimizes revision surgery. All told, the peripheral nerve injuries market size attached to wraps is forecast to cross USD 700 million by 2031.

Wrap adoption reflects a behavioral pivot: AxoGen’s AxoGuard wrap featured in 40% of the company’s repair kits in 2025, up from 25% three years earlier. Processed allografts, newly cleared for sensory repairs, compete effectively in 3–7 cm gaps, while synthetic conduits such as Integra’s NeuraGen 3D offer lower entry pricing. Hybrids combining scaffolds with embedded growth factors loom on the horizon, but regulatory pathways for combination devices remain complex and may temper near-term penetration.

By Surgery or Technique: Regenerative Adjuncts Emerge as the Fastest Grower

Direct repair accounted for 54.15% of all 2025 procedures, reflecting the frequency of short-gap injuries amenable to tension-free coaptation. Yet regenerative adjuncts—platelet-rich plasma, adipose-derived cells, and acellular matrices—are projected to rise at a 9.76% CAGR, the fastest within the peripheral nerve injuries industry. Clinical trials report 4- to 6-month accelerations in sensory or motor recovery, a meaningful benefit for wage-earning patients eager to resume work.

Nerve grafting remains vital in long gaps, especially brachial plexus and sciatic reconstructions, though its overall share is slipping as conduits prove viable beyond historical length limits. Nerve transfers—especially the “supercharged end-to-side” technique—answer proximal injuries where axons would otherwise miss the re-innervation window. This procedural diversification complicates manufacturer messaging but offers surgeons a broader toolbox, sustaining multi-product demand across the peripheral nerve injuries market.

By Application: Upper Extremity Commands Volume and Growth

Upper-extremity cases generated 72.6% of 2025 revenue and carry the highest forecast CAGR at 10.55%. These numbers translate into the largest single slice of the peripheral nerve injuries market size, driven by the functional premium on hand dexterity in knowledge-based occupations. Brachial plexus injuries and carpal tunnel decompressions dominate the case mix, while intraoperative nerve stimulators such as Checkpoint’s Altius improve fascicular targeting, enhancing surgical precision.

Lower-extremity repairs trail in both volume and outcomes. Longer regeneration distances and weight-bearing demands make full recovery harder, and surgeons sometimes default to orthotic management. However, a 2025 Foot & Ankle International study showing a 40% higher fall rate in untreated peroneal-nerve palsy among seniors is prompting payers to re-evaluate the cost-benefit of surgical intervention. This evolving evidence may incrementally boost lower-limb procedure counts, broadening the peripheral nerve injuries market footprint.

By End User: ASCs Accelerate as Payers Enforce Site Shifts

Hospitals and clinics held 45.32% of 2025 revenue because they monopolize multi-stage reconstructions and intensive monitoring. Yet ambulatory surgical centers are growing at 10.43% CAGR, buoyed by payer policies that reimburse ASC cases at 60%–70% of hospital rates. UnitedHealthcare’s January 2025 prior-authorization rule for hospital outpatient nerve repairs epitomizes this steerage.

Academic centers are adapting; Cedars-Sinai’s ASC nerve suite shows that even tertiary institutions now court outpatient economics. Specialty centers remain a niche, serving self-pay or concierge patients but facing payer resistance to elevated facility fees. A 2024 Health Affairs review tagged a 2.1% 72-hour hospital-conversion rate for ASC nerve repairs, underscoring the importance of stringent patient selection as the peripheral nerve injuries market migrates to outpatient.

Geography Analysis

North America accounted for 41.25% of 2025 revenue after Medicare’s reimbursement clarification removed financial ambiguity regarding allograft use for gaps greater than 5 cm. Surgeon scarcity, however, remains a gating factor; only 18 accredited U.S. fellowships graduate roughly 25 specialists a year, maintaining pricing power for established devices. Canada’s single-payer model covers nerve repair but imposes 6- to 9-month wait times, while Mexico’s medical-tourism industry offers 40%–50% cost savings—albeit without standardized outcome metrics—highlighting cross-border price disparities across the peripheral nerve injuries market.

Asia-Pacific is projected to grow at 8.43% CAGR through 2031, the fastest regional rate. China’s 297 million seniors face elevated fall risk, expanding the surgical backlog, and India’s 4 million annual road-traffic injuries bring high trauma volumes. Japan’s SAKIGAKE fast-track for Toyobo’s Nerbridge establishes a domestic champion with 10-year exclusivity, and South Korea lifted its autograft-failure prerequisite for conduit reimbursement in March 2025, moves that collectively widen the regional adoption funnel.

Europe and the Middle East & Africa lag due to reimbursement fragmentation and limited surgeon training. Germany reimburses autograft harvest but often denies processed allografts, and NICE’s conduit endorsement stops at digital repairs, excluding lower-extremity cases. South Africa’s private hospitals match European adoption speed, yet its public sector lacks cold-chain capacity, hampering allograft distribution. Brazil’s public system reimburses nerve repair but struggles with biologic supply to rural regions, illustrating logistical constraints that temper peripheral nerve injuries market growth.

Competitive Landscape

The peripheral nerve injuries market is moderately fragmented. AxoGen, Integra LifeSciences, and Medtronic together fall below the 50% revenue threshold, leaving room for niche innovators. AxoGen’s December 2025 FDA clearance for sensory-gap repairs extends its first-mover edge in processed allografts, an area where tissue-bank partnerships constitute high entry barriers. Integra counters on price, positioning NeuraGen 3D about 30% below Avance but lacks comparable registry data, a gap that insurers notice. Medtronic leverages its neurostimulation portfolio from the 2019 Stimwave acquisition, connecting chronic-pain devices to peripheral-nerve channels rather than structural repair.

Smaller firms occupy specific white spaces. Checkpoint Surgical’s Altius intraoperative stimulator, cleared in August 2024, targets iatrogenic nerve injury prevention and has already achieved a 30% reduction in high-risk surgeries, according to early adopters. Polyganics’ slow-resorb Neurolac conduit satisfies surgeons concerned about premature degradation, while Orthocell’s CryoShot pushes biologic adjuncts into the mainstream with an 18% early motor-recovery edge. Patent filings reveal divergent strategies—AxoGen on allograft processing, Integra on conduit microarchitecture, Checkpoint on electrode miniaturization—reducing direct intellectual-property collisions and allowing coexistence.

Clinical inertia remains a competitive wildcard. Autograft loyalists default to harvest despite donor-site morbidity, meaning suppliers must prove equivalent or superior outcomes over longer horizons to convert surgeons. As five-year data accumulate from AxoGen’s RANGER and other registries, the balance may tip, reshaping share distribution across the peripheral nerve injuries market.

Peripheral Nerve Injuries Industry Leaders

Axogen, Inc.

Integra LifeSciences Corporatio

Stryker Corporation

Baxter International Inc

Toyobo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Trace Biosciences, Inc., a clinical-stage biotechnology company developing nerve-targeted imaging agents, received U.S. Food and Drug Administration (FDA) approval for its Investigational New Drug (IND) application for LGW16-03, the company's first nerve-specific fluorescent imaging agent. The IND clearance enables Trace to initiate first-in-human clinical studies evaluating the safety and intraoperative performance of LGW16-03 in surgical settings.

- December 2025: The U.S. Food and Drug Administration approved Axogen's (AXGN.O) nerve repair graft, the health regulator, paving the way for 12 years of potential market exclusivity in the United States. Axogen's Avance Nerve Graft, a human tissue-based product, is designed to repair damaged peripheral nerves without requiring a second surgery to harvest nerve tissue from the patient, thereby reducing complications and supporting faster recovery.

- August 2025: NervGen Pharma Corp., a clinical-stage biopharmaceutical company developing first-in-class neuroreparative therapeutics for spinal cord injury and other neurologic disorders, announced positive preclinical results of two Department of Defense-sponsored studies in models of blast-induced sensorineural hearing loss and peripheral nerve injury, reinforcing the broad therapeutic application of its first and potential best-in-class candidate, NVG-291.

Global Peripheral Nerve Injuries Market Report Scope

As per the scope of the report, Peripheral nerve injuries involve damage to nerves outside the brain and spinal cord, disrupting nerve signaling. They can result from trauma, compression, or stretching, leading to sensory or motor deficits. Recovery varies depending on the injury severity and treatment.

The Peripheral Nerve Injuries Market is Segmented by Product Type (Nerve Conduits, Nerve Wraps/Protectors, Nerve Connectors/Coaptation Aids, and Nerve Grafts), Surgery/Technique (Direct Nerve Repair, Nerve Grafting, Nerve Transfer, and Stem-Cell/Regenerative Adjuncts), Application (Upper Extremities and Lower Extremities), End-User (Hospitals & Clinics, ASCs, and Specialty/Orthoplastic Centers), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Nerve Conduits |

| Nerve Wraps / Protectors |

| Nerve Connectors / Coaptation Aids |

| Nerve Grafts |

| Direct Nerve Repair |

| Nerve Grafting |

| Nerve Transfer |

| Stem-Cell / Regenerative Adjuncts |

| Upper Extremities |

| Lower Extremities |

| Hospitals & Clinics |

| Ambulatory Surgical Centers (ASCs) |

| Specialty / Orthoplastic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Nerve Conduits | |

| Nerve Wraps / Protectors | ||

| Nerve Connectors / Coaptation Aids | ||

| Nerve Grafts | ||

| By Surgery / Technique | Direct Nerve Repair | |

| Nerve Grafting | ||

| Nerve Transfer | ||

| Stem-Cell / Regenerative Adjuncts | ||

| By Application | Upper Extremities | |

| Lower Extremities | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty / Orthoplastic Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the projected value of the peripheral nerve injuries market in 2031?

The peripheral nerve injuries market is expected to reach USD 4.30 billion by 2031.

Which product segment currently leads revenue?

Nerve conduits hold the top spot with 63.21% share of 2025 revenue.

Why are ambulatory surgical centers gaining share?

Payers reimburse ASC cases at 60%Ð70% of hospital rates, encouraging surgeons to shift outpatient for cost savings.

Which region is forecast to grow fastest?

Asia-Pacific is set to expand at an 8.43% CAGR through 2031 on the strength of aging populations and high trauma incidence.

What major regulatory change boosted U.S. adoption?

Medicare's 2025 National Coverage Determination clarified separate payment for processed nerve allografts longer than 5 cm, reducing billing ambiguity.

How fragmented is supplier competition?

The top three firms control less than 50% of revenue, leaving significant space for specialized innovators to capture niches.

Page last updated on: