United Kingdom Industrial Automation System Integrator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

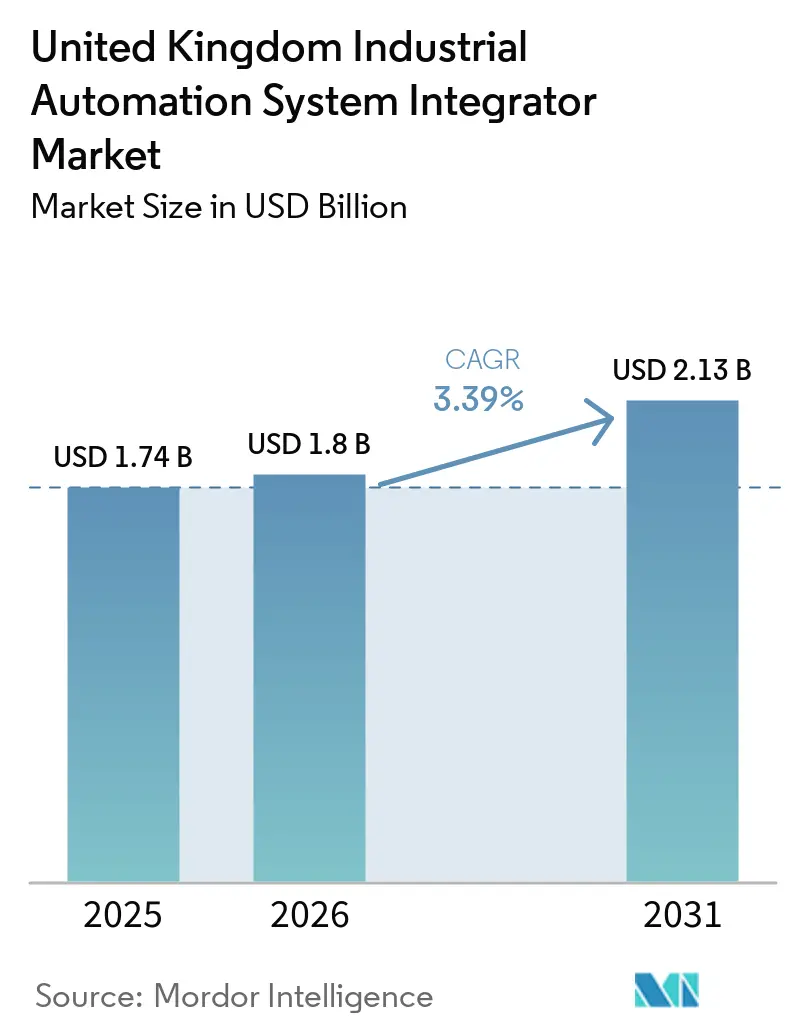

| Base Year Market Size (2025) | USD 1.74 Billion |

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

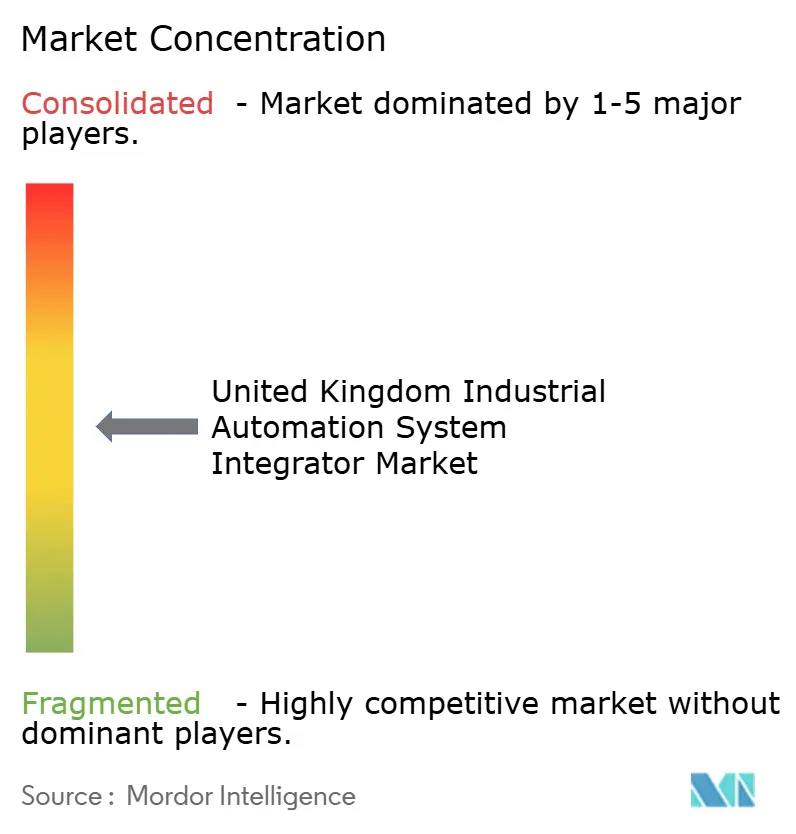

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Industrial Automation System Integrator Market Analysis by Mordor Intelligence

The United Kingdom Industrial Automation System Integrator Market size is expected to increase from USD 1.74 billion in 2025 to USD 1.8 billion in 2026 and reach USD 2.13 billion by 2031, growing at a CAGR of 3.39% over 2026-2031.

Selective, high-return automation investments now dominate capital-allocation decisions, and the GBP 4.5 billion (USD 6.12 billion) Invest 2035 program is steering funds toward advanced-manufacturing corridors rather than legacy factories. Buyers are favoring turnkey projects that bundle hardware, software, and multi-year managed-service contracts, a model that shifts risk to vendors and eases the engineering-talent bottleneck. Competitive intensity is increasing as niche integrators capture verticals, such as water and wastewater treatment, where real-time compliance monitoring is mandatory. Meanwhile, the National Semiconductor Strategy and the DRIVE35 electric-vehicle roadmap are accelerating demand for high-precision robotics, edge computing, and machine-vision systems to meet stringent tolerance and traceability requirements.

Key Report Takeaways

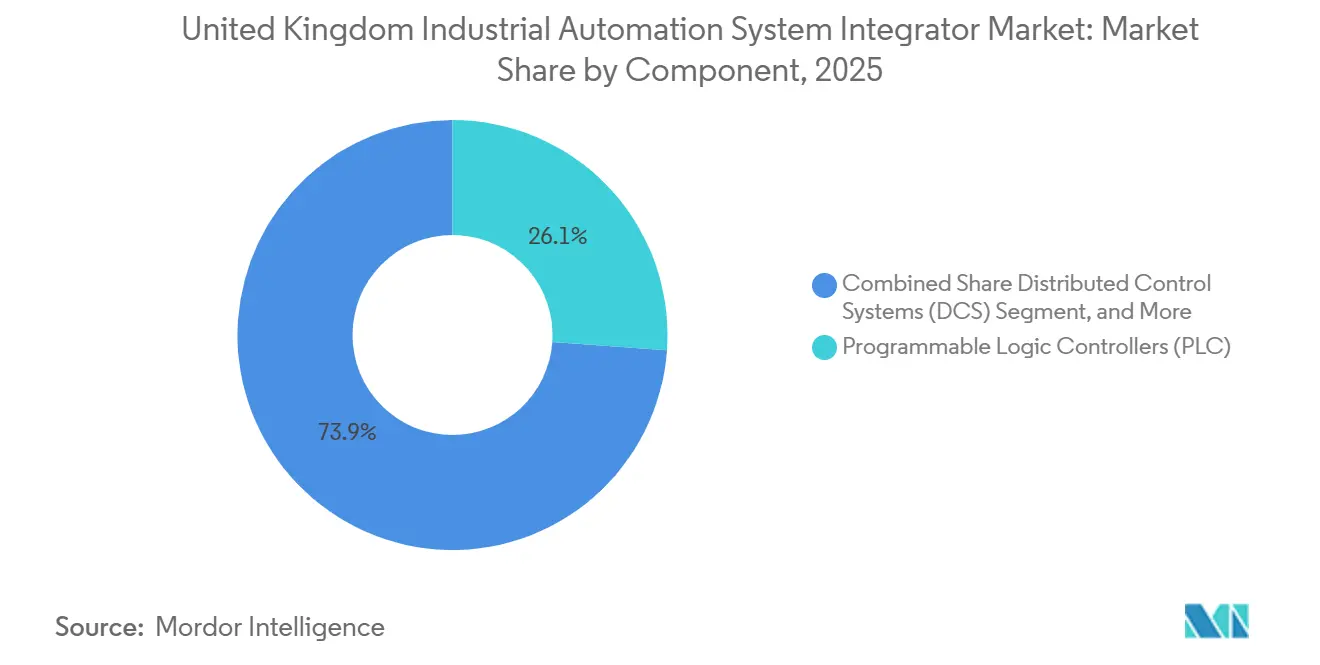

- By component, programmable logic controllers led with 26.13% of United Kingdom industrial automation system integrator market share in 2025, while industrial robots and machine-vision systems are advancing at a 3.92% CAGR to 2031.

- By service type, installation and commissioning held 32.53% share of the United Kingdom industrial automation system integrator market size in 2025, and managed services plus remote monitoring are projected to expand at a 4.02% CAGR through 2031.

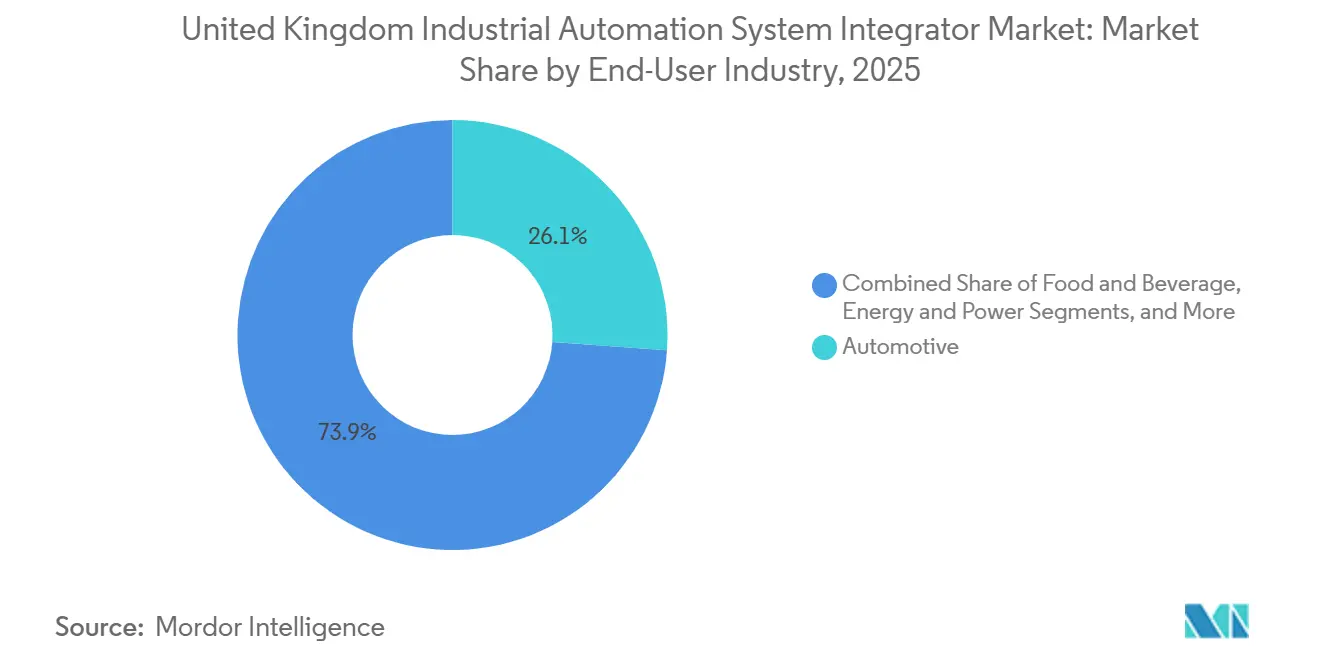

- By end-user industry, automotive accounted for 24.16% of the 2025 United Kingdom industrial automation system integrator market size, but electronics and semiconductors will post the fastest 5.13% CAGR to 2031.

- By technology platform, industrial internet of things solutions captured 34.87% of United Kingdom industrial automation system integrator market share in 2025, yet artificial intelligence and predictive analytics will grow at a 5.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Industrial Automation System Integrator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation and Industry 4.0 adoption | +0.9% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| Rising demand for productivity amid UK labor shortages | +0.7% | England (Midlands, North), Scotland | Short term (≤ 2 years) |

| Accelerated robotics uptake in automotive re-tooling for EVs | +0.6% | England (West Midlands, Sunderland), Wales | Medium term (2-4 years) |

| Network Rail Target 190plus digital signaling rollout | +0.4% | England (ECML, GWR), Scotland | Long term (≥ 4 years) |

| Food and drink vanishing-horizon automation funding | +0.3% | England (East Anglia, Yorkshire), Scotland, Northern Ireland | Medium term (2-4 years) |

| Regional smart-machine hubs backed by UK government | +0.3% | Scotland, Wales, Northern Ireland, North England | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation and Industry 4.0 Adoption

Nearly half of mid-sized British factories had at least one IIoT pilot by the end of 2025, overtaking peers in France and Germany.[1]Make UK, “Manufacturing Monitor 2025,” makeuk.org Grant eligibility under Invest 2035 depends on demonstrable digital-maturity benchmarks, so applicants integrate real-time data platforms early in project planning. Pharmaceutical producers are embedding serialization modules to satisfy Medicines and Healthcare products Regulatory Agency traceability mandates. System integrators therefore bundle SCADA software with edge gateways that preprocess sensor streams locally, cutting cloud-transmission outlay by 60% while preserving audit trails for inspectors. The shift is expanding demand for solutions that converge operational-technology data and enterprise analytics without disrupting validated manufacturing lines.

Rising Demand for Productivity Amid UK Labor Shortages

Engineering vacancies reached 150 000 in 2025 and control-systems specialists earned 22% wage premiums, driving manufacturers to substitute labor with cobots and automated guided vehicles. Brexit-related immigration rules reduced skilled-trades inflows by 34% between 2021 and 2025, so even large plants are automating repetitive tasks to maintain output. Unilever’s Port Sunlight site installed 18 cobots in 2025 and lowered per-unit labor cost by 28% while keeping 24-hour shifts. The Made Smarter Adoption grants helped 1 200 SMEs automate at least one cell without straining cash flow. Human-machine interfaces that allow non-technical staff to supervise automated lines are now essential, mitigating the shortage of licensed control engineers.

Accelerated Robotics Uptake in Automotive Re-Tooling for EVs

Automakers pledged GBP 8.2 billion to EV infrastructure during 2024-2025, dedicating 63% to robotics, battery-pack assembly, and AI-driven inspection. The DRIVE35 roadmap mandates 80% zero-emission vehicle output by 2035, compelling plants such as Nissan Sunderland to install 47 six-axis robots that trimmed cycle time by 14 minutes per car. Tier-one supplier GKN invested GBP 120 million in automated eDrive lines targeting 30% cost reduction by 2027. Machine-vision systems check battery alignment tolerances of ±0.1 mm, a precision beyond human capacity, cementing demand for high-resolution optics paired with AI defect detection. System integrators able to deliver turnkey robotic cells with predictive-maintenance packages are securing multi-year frame agreements.

Network Rail Target 190plus Digital Signaling Rollout

The GBP 1.8 billion (USD 2.45 billion) program is replacing lineside lights with European Train Control System Level 2 across 190 route-kilometers, feeding a multiyear pipeline of distributed-control projects. Real-time position data must travel with sub-100-ms latency, so integrators deploy time-sensitive networking that conforms to IEC 61375. The East Coast Main Line upgrade will raise throughput to 18 trains per hour and cut cost per passenger by GBP 4.2 (USD 5.72), yet proprietary interfaces oblige bespoke licensing that inflates budgets by 15% and adds up to a year to schedules. Vendors that bundle control software, fiber backhaul, and remote diagnostics win contracts by offering Network Rail a single point of accountability over 25-year asset lives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex and integration costs | -0.5% | England (SME regions), Wales, Northern Ireland | Short term (≤ 2 years) |

| Scarcity of skilled automation engineers | -0.4% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| OEM-locked intellectual-property barriers in rail signaling | -0.2% | England (rail corridors), Scotland | Long term (≥ 4 years) |

| Fragmented legacy OT-IT cybersecurity standard | -0.2% | England, Scotland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capex and Integration Costs

SMEs make up 99% of manufacturers yet control only 38% of automation spend because a typical retrofit costs GBP 250 000, well above the annual capital budget of most firms with under 50 employees. Leasing is available but interest rates hover at 6-8%, doubling total ownership cost over five years. Made Smarter grants cap at GBP 20 000 and reached only 1 200 companies in 2024-2025, leaving tens of thousands without support. Legacy sites often need panel rewiring and actuator upgrades, which swallow 40-50% of budgets and add half a year to commissioning. Consequently, demand is tilting toward modular, skid-mounted solutions that bolt onto existing utilities and minimize civil works.

Scarcity of Skilled Automation Engineers

The country had 150 000 engineering vacancies in 2025, and 64% of integrators said talent scarcity throttled project throughput. Immigration curbs worsened the gap while domestic apprenticeship completions in automation fell 9% between 2021 and 2025. Firms now decline nearly one in five RFPs because they cannot staff concurrent jobs.[2]Institution of Engineering and Technology, “Engineering Skills Survey 2025,” theiet.org ABB opened a 12-month robotics academy that enrolled 80 entrants in 2025, and Siemens Mobility co-launched a master’s program aiming for 150 graduates a year by 2028 . These initiatives will take several years to ease the crunch, so vendors with remote-operations centers gain an edge by supervising dispersed assets from centralized hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: PLCs Anchor Legacy Upgrades While Vision Systems Capture EV Spend

Component revenue continues to pivot toward precision robotics and high-resolution vision platforms. Industrial robots and vision systems are expanding at a 3.92% CAGR, outstripping the 3.19% United Kingdom industrial automation system integrator market average as EV assembly lines demand ±0.1 mm alignment accuracy. Programmable logic controllers held 26.13% of 2025 revenue, cementing their role in discrete manufacturing where deterministic control is critical. However, buyers now pair compact PLCs with edge gateways, a pairing that trims cloud-data costs by 60%.

Distributed control systems remain indispensable in pharmaceuticals and utilities where safety-instrumented loops are mandatory under IEC 61511. Supervisory control and data acquisition platforms are rising fast in the water sector following Environment Agency rules for real-time discharge monitoring.[3]Environment Agency, “Real-Time Discharge Monitoring Requirements,” gov.uk Human-machine interfaces are shifting toward augmented-reality overlays, which cut maintenance onboarding time by 35% in Rolls-Royce’s Derby plant. Industrial sensors and networks benefit from 5G private networks; a standalone 5G core at the Port of Felixstowe now supports 12 000 endpoints with sub-10-ms latency.

By Service Type: Managed Services Gain as Buyers Outsource Uptime Risk

Installation and commissioning captured 32.53% of 2025 revenue because automotive EV re-tooling created a surge of greenfield activity. As those lines stabilize, the revenue mix is tilting to managed services and remote monitoring, which will post a 4.02% CAGR to 2031. Buyers favor contracts that guarantee 98-99% availability, transforming capex into opex and aligning vendor incentives with plant uptime.

Design-engineering services are expanding in regulated industries like pharma, where serialization mandates inflate software-integration budgets. Maintenance agreements now stretch five years instead of three to secure scarce talent through the life of installed assets. Upgrades and retrofits intensify in food processing, with Unilever replacing 14 legacy PLCs and saving 19% energy in 2025. Remote diagnostics are mandatory in rail projects because Target 190plus requires continuous fault detection across 190 route-kilometers.

By End-User Industry: Electronics Overtakes Automotive Growth as Reshoring Accelerates

Automotive retained 24.16% of the 2025 United Kingdom industrial automation system integrator market size, yet its growth rate now matches the market average after the initial EV-conversion wave. Electronics and semiconductors will grow at 5.13% CAGR, buoyed by a GBP 1 billion National Semiconductor fund that prioritizes domestic assembly for defense and telecom supply chains.

Food and beverage manufacturers face acute vacancies and therefore automate repetitive tasks, leveraging Made Smarter subsidies that already supported 1 200 SME projects. Pharmaceuticals race toward 2027 FMD deadlines, demanding serialization and track-and-trace systems integrated at machine level. Energy utilities deploy distributed control to oversee grid-edge batteries after 2024 outages caused USD 2.9 billion in lost output. Water utilities automate 4 200 plants to comply with faster discharge-reporting cycles.

By Technology: AI Predictive Analytics Surge as Edge Computing Cuts Cloud Costs

Industrial internet of things platforms commanded 34.87% of 2025 revenue, cementing their role as data backbones for sensors and actuators. The maturation of connectivity shifts spending toward analytics; artificial intelligence and predictive algorithms will post a 5.01% CAGR to 2031. Manufacturers deploy edge-based anomaly detection to avert unplanned downtime, a priority after capacity constraints cost USD 2.9 billion in 2024.

Digital twins are now standard for pharmaceutical validation, shaving 4-6 months off commissioning cycles. Edge computing and private 5G enable latency-sensitive cobot applications; the Port of Felixstowe example cut container dwell time by 18 minutes. Predictive maintenance models at Rolls-Royce reach up to 92% accuracy on bearing-failure forecasts, reducing spares inventory by 23%.

Geography Analysis

England dominated with 61.37% share of the United Kingdom industrial automation system integrator market in 2025 thanks to the Midlands Engine and Northern Powerhouse corridors, which funnel Invest 2035 funds into automotive, aerospace, and food clusters. The West Midlands hosts intensive robotics deployments at Jaguar Land Rover and GKN facilities aligned with the DRIVE35 zero-emission target, while East Anglia food processors double down on cobots to offset labor shortages. Greater London pharmaceutical lines embed serialization modules ahead of 2027 compliance deadlines, and Network Rail’s East Coast Main Line upgrade underpins sizable distributed-control opportunities over the next four years.

Scotland will show the fastest 4.18% CAGR through 2031, energized by GBP 1.2 billion Scottish Enterprise capital for precision-engineering hubs in Glasgow and Aberdeen. The Clyde Gateway zone is attracting battery-storage and hydrogen-electrolyzer investors, and Aberdeen leverages offshore engineering expertise to automate North Sea platforms with remotely operated vehicles and predictive-maintenance suites. These projects elevate demand for integrators versed in IEC 61511 safety loops and subsea robotics assembly.

Wales and Northern Ireland are scaling adoption through regional grants. The Welsh Tech Valleys program earmarked GBP 100 million for smart-factory pilots in Port Talbot and Bridgend, emphasizing food processing and advanced materials. Northern Ireland benefits from dual UK-EU market access and secured GBP 180 million in foreign direct investment for Belfast and Derry plants in 2025. Cross-border supply chains create niche openings for integrators that can harmonize UK regulatory frameworks with EU automation standards.

Competitive Landscape

Moderate fragmentation characterizes the United Kingdom industrial automation system integrator market. The top five Siemens Mobility, ABB, Schneider Electric, Rockwell Automation, and Honeywell collectively held about 42% share in 2025. Multinationals capture megaprojects, such as the GBP 320 million (USD 435.50 million) Great Western Main Line signaling contract won by Siemens Mobility in 2026, because they carry product certifications, 24-hour support centers, and financing arms. Local specialists thrive in water and food segments where rapid site access and flexible billing trump global scale.

Strategic differentiation is migrating toward recurring revenue. Honeywell’s 2025 launch of a managed-services platform that guarantees 98.5% availability illustrates the pivot from project to service income. Smaller firms such as Cougar Automation ride cloud partnerships to deliver industrial internet of things stacks without owning data centers, enabling them to underbid multinationals by nearly 20% on mid-tier food-processing jobs. Vendors are also investing in immersive-reality maintenance aids and digital-twin commissioning to reduce onsite man-hours and engineer visits, a decisive factor as 150 000 engineering vacancies persist nationwide.

White-space opportunities center on water-treatment compliance, pharmaceutical serialization, and offshore wind maintenance. Environment Agency mandates for 4 200 wastewater plants, the FMD 2027 traceability deadline, and Scotland’s offshore renewables boom expand addressable spend for integrators that blend functional-safety know-how, real-time analytics, and harsh-environment robotics. Partnerships between automation houses and academic institutions are emerging to train a fresh cohort of control engineers, signaling that skills development is becoming a competitive weapon as much as technology innovation.

United Kingdom Industrial Automation System Integrator Industry Leaders

Wood PLC

Jacobs U.K. Limited

Siemens Mobility Limited

Altec Engineering Limited

Cougar Automation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens Mobility secured a GBP 320 million (USD 435.50 million) contract from Network Rail to deploy ETCS Level 2 signaling across 85 route-kilometers of the Great Western Main Line, with commissioning due December 2028.

- December 2025: ABB UK committed GBP 45 million to expand its Milton Keynes robotics plant, adding 12 000 m² and 180 jobs to satisfy food-sector cobot demand.

- November 2025: Schneider Electric UK and Scottish Enterprise announced a GBP 28 million smart-manufacturing demonstration center in Glasgow focused on edge gateways and digital twins.

- October 2025: Rockwell Automation UK won a GBP 18 million contract to automate GKN Automotive eDrive lines in Birmingham and Telford using 34 robots and machine-vision cells.

United Kingdom Industrial Automation System Integrator Market Report Scope

System integrators are companies that help manufacturing plants deploy and install hardware and software solutions. In relation to industrial automation, system integrators are the entities that provide clients the services for consultation, hardware installation, software integration, and system maintenance.

The United Kingdom Industrial Automation System Integrator Market Report is Segmented by Component (Programmable Logic Controllers, Distributed Control Systems, Supervisory Control and Data Acquisition, Human-Machine Interface, Industrial Robots and Machine Vision, Industrial Sensors and Networks), Service Type (Design and Engineering, Installation and Commissioning, Maintenance and Support, Upgrades and Retrofits, Managed Services and Remote Monitoring), End-User Industry (Automotive, Food and Beverage, Pharmaceuticals and Medical Devices, Energy and Power, Water and Wastewater, Metals and Mining, Electronics and Semiconductors, Oil and Gas, Other End-User Industries), Technology (Industrial Internet of Things Platforms, Artificial Intelligence and Predictive Analytics, Digital Twin and Simulation, Edge Computing and 5G Connectivity), and Geography (England, Scotland, Wales, Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

| Programmable Logic Controllers (PLC) |

| Distributed Control Systems (DCS) |

| Supervisory Control and Data Acquisition (SCADA) |

| Human-Machine Interface (HMI) |

| Industrial Robots and Machine Vision |

| Industrial Sensors and Networks |

| Design and Engineering |

| Installation and Commissioning |

| Maintenance and Support |

| Upgrades and Retrofits |

| Managed Services and Remote Monitoring |

| Automotive |

| Food and Beverage |

| Pharmaceuticals and Medical Devices |

| Energy and Power |

| Water and Wastewater |

| Metals and Mining |

| Electronics and Semiconductors |

| Oil and Gas |

| Other End-User Industries |

| Industrial Internet of Things (IIoT) Platforms |

| Artificial Intelligence and Predictive Analytics |

| Digital Twin and Simulation |

| Edge Computing and 5G Connectivity |

| By Component | Programmable Logic Controllers (PLC) |

| Distributed Control Systems (DCS) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Human-Machine Interface (HMI) | |

| Industrial Robots and Machine Vision | |

| Industrial Sensors and Networks | |

| By Service Type | Design and Engineering |

| Installation and Commissioning | |

| Maintenance and Support | |

| Upgrades and Retrofits | |

| Managed Services and Remote Monitoring | |

| By End-User Industry | Automotive |

| Food and Beverage | |

| Pharmaceuticals and Medical Devices | |

| Energy and Power | |

| Water and Wastewater | |

| Metals and Mining | |

| Electronics and Semiconductors | |

| Oil and Gas | |

| Other End-User Industries | |

| By Technology | Industrial Internet of Things (IIoT) Platforms |

| Artificial Intelligence and Predictive Analytics | |

| Digital Twin and Simulation | |

| Edge Computing and 5G Connectivity |

Key Questions Answered in the Report

How large will UK demand for system-integration services be by 2031?

The United Kingdom industrial automation system integrator market is forecast to reach USD 2.13 billion by 2031, growing at a 3.39% CAGR from 2026.

Which component category is growing fastest?

Industrial robots and machine-vision systems together are projected to expand at 3.92% CAGR through 2031 as EV and semiconductor plants require sub-millimeter accuracy.

Why are managed services gaining traction?

Buyers want 98-99% equipment availability and prefer to shift capex to opex, so remote monitoring and multi-year uptime guarantees are expanding at 4.02% CAGR.

How are labor shortages influencing automation investments?

With 150 000 engineering vacancies in 2025 and rising wage premiums, manufacturers are accelerating collaborative-robot deployments and user-friendly HMIs to sustain output.

Which technology area offers the highest upside?

Artificial intelligence-based predictive analytics will grow at 5.01% CAGR as edge platforms slash cloud costs and cut unplanned downtime across energy-intensive sectors.

Page last updated on: