Industrial Control For Process Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

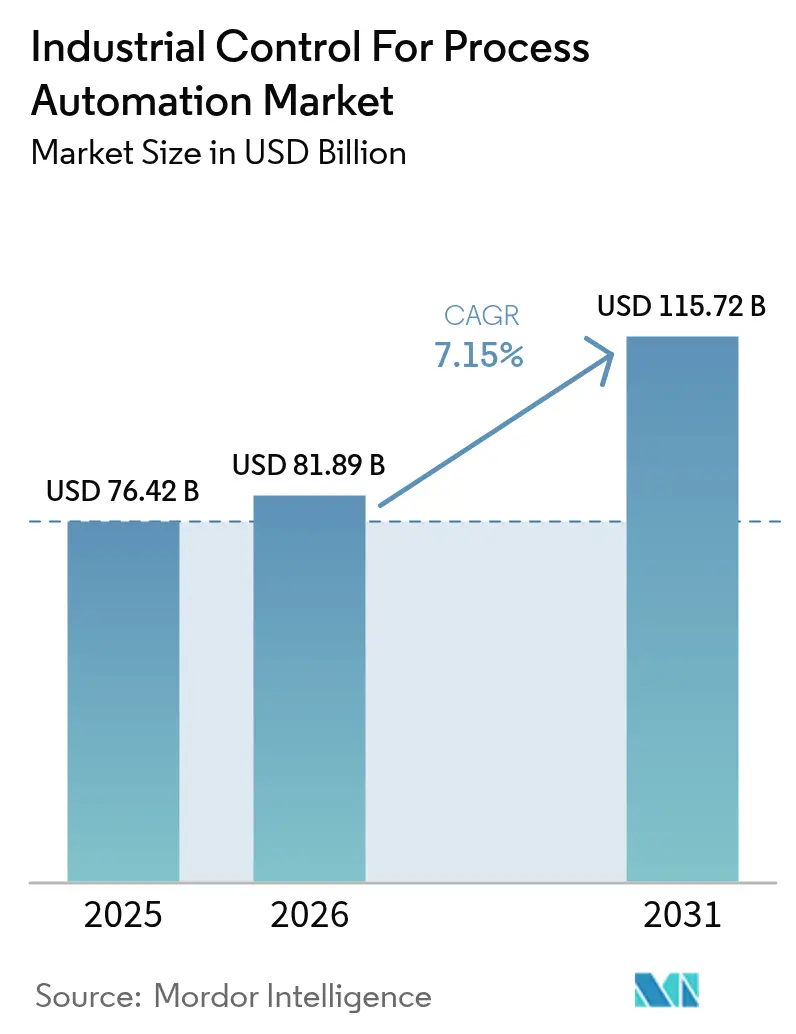

| Market Size (2026) | USD 81.89 Billion |

| Market Size (2031) | USD 115.72 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

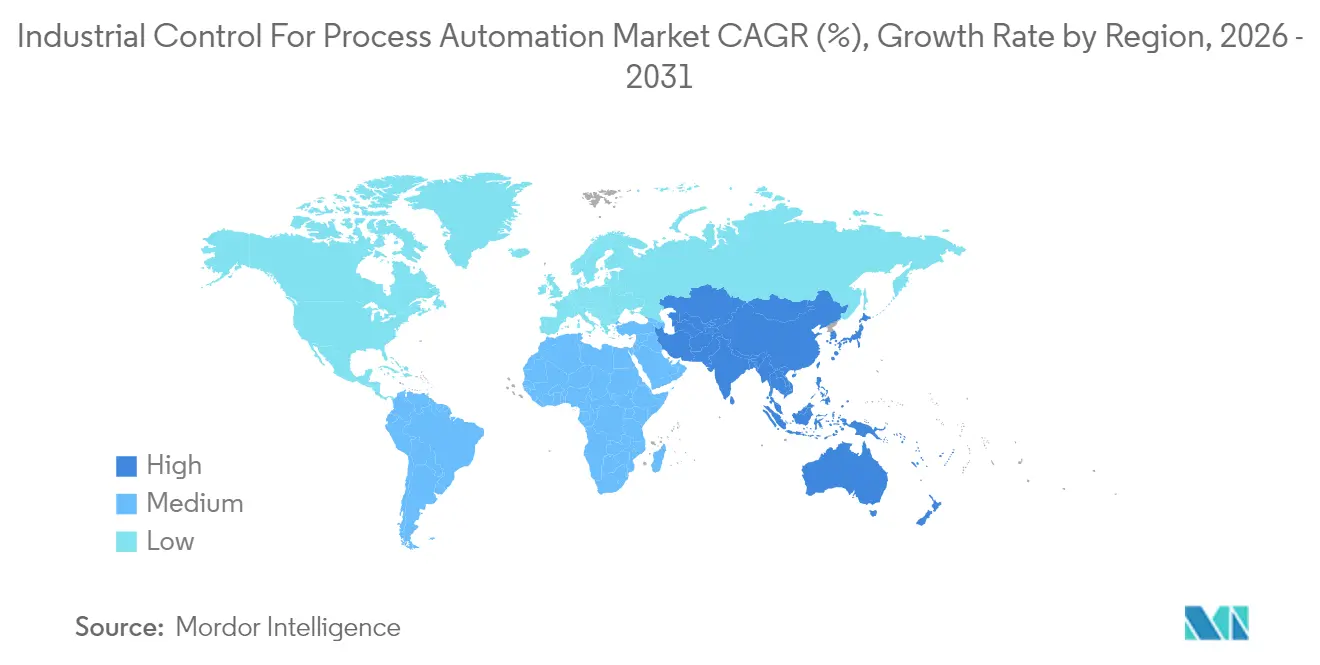

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

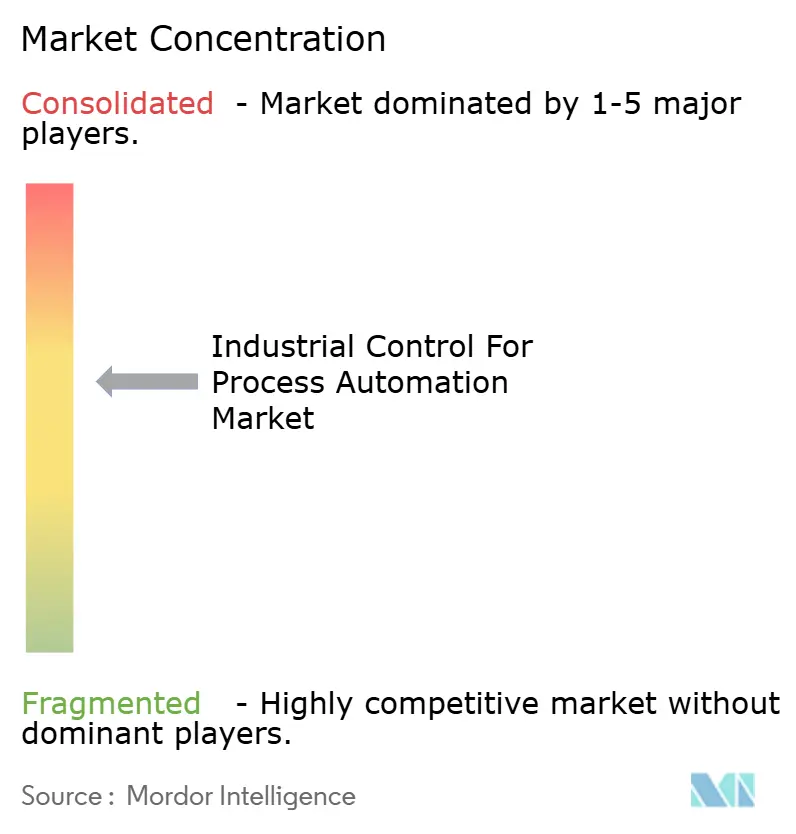

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Control For Process Automation Market Analysis by Mordor Intelligence

The industrial control for process automation market size is expected to grow from USD 76.42 billion in 2025 to USD 81.89 billion in 2026 and is forecast to reach USD 115.72 billion by 2031 at 7.15% CAGR over 2026-2031. Heightened regulatory pressure for energy efficiency, the rapid infusion of IIoT sensors, and an accelerated pivot from proprietary hardware to software-led edge intelligence are steering capital toward cloud-native control platforms and predictive analytics engines. Vendors are embedding artificial intelligence directly into controllers to reduce downtime, optimize setpoints, and automate alarm rationalization, unlocking measurable gains in throughput and energy intensity reduction. At the same time, industrial wireless, backed by 5G and time-sensitive networking, is providing operators with a retrofit path for brownfield sites without requiring the rewiring of entire plants. Competitive dynamics remain fluid as software specialists, cloud hyperscalers, and cybersecurity firms erode the legacy hardware moat, forcing traditional automation leaders to acquire, partner, and open their ecosystems to maintain their share.

Key Report Takeaways

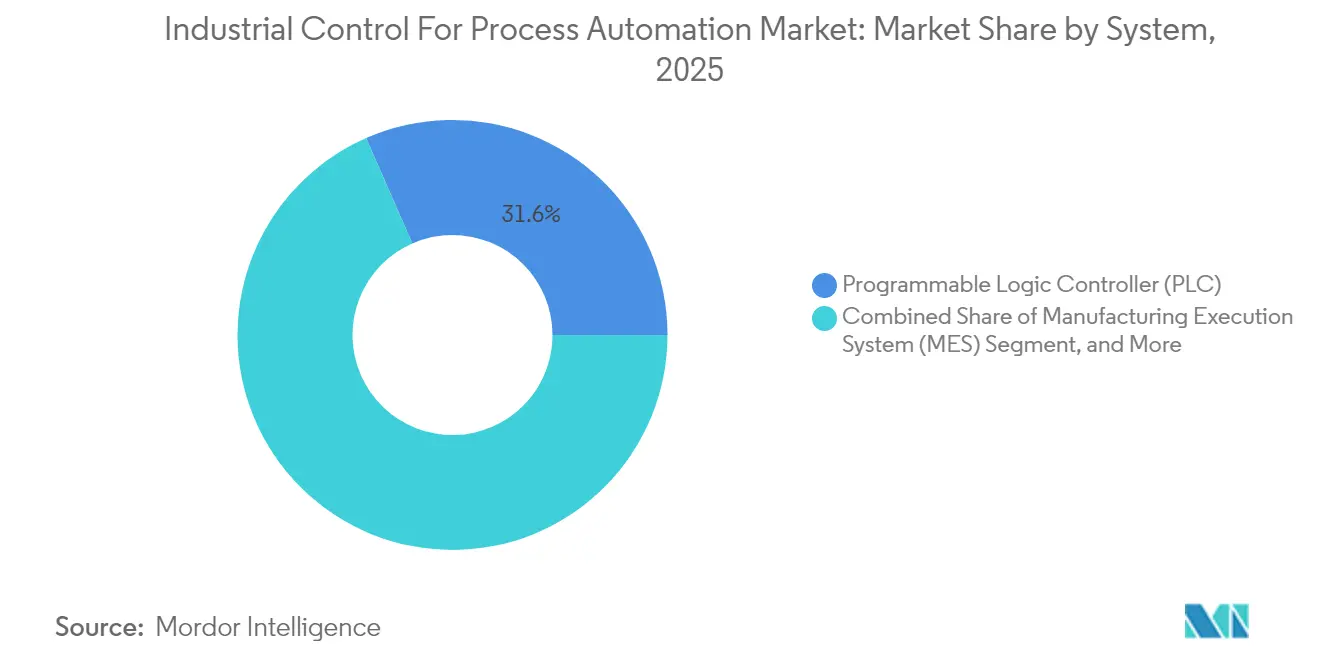

- By system, programmable logic controllers held 31.58% of the industrial control for process automation market share in 2025, while manufacturing execution systems are forecast to grow at a 10.04% CAGR through 2031.

- By component, hardware captured 46.35% of 2025 revenue, yet software is advancing at a 9.37% CAGR, underscoring the migration of control logic to microservices.

- By service, system integration and deployment accounted for 37.46% of service revenue in 2025, whereas consulting is the fastest-growing service, rising at a 9.68% CAGR as operators seek OT-IT roadmaps.

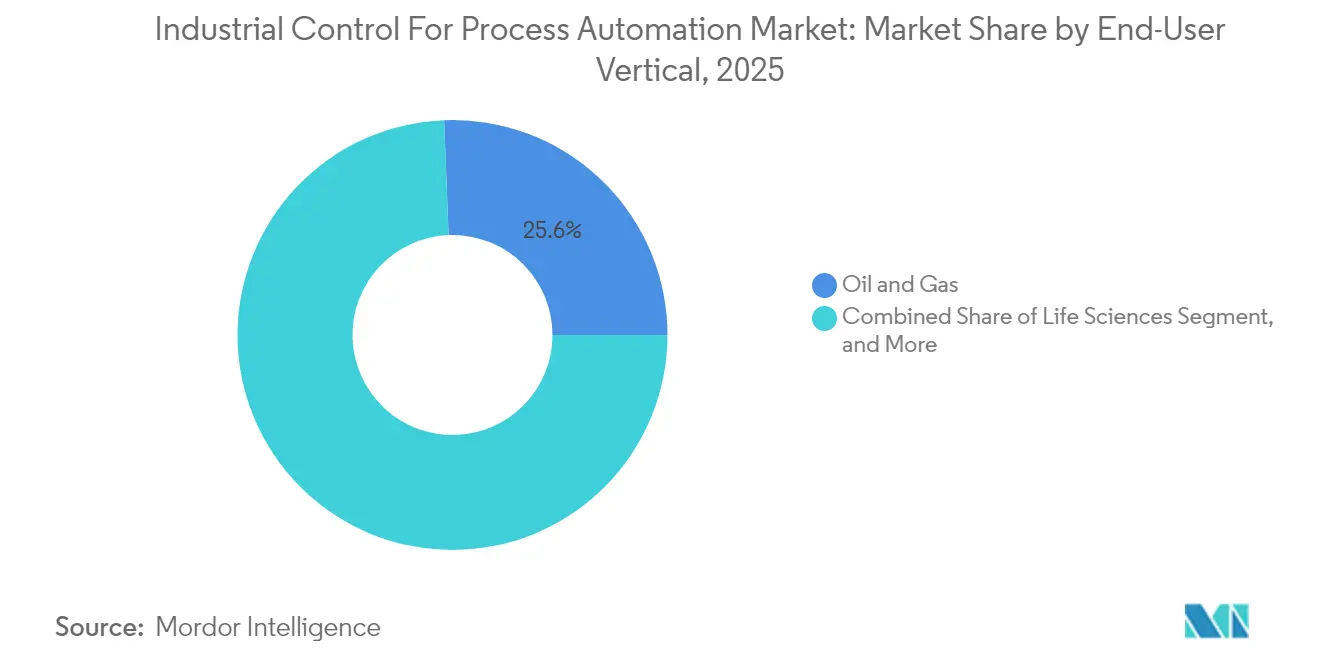

- By end-user vertical, the life sciences sector is expected to contribute the fastest vertical expansion, with an 10.96% CAGR forecast to 2031, while the oil and gas sector retained the largest share in 2025 at 25.62%.

- By communication network, industrial wireless networks are poised to expand at a 13.05% CAGR, despite wired networks maintaining a 67.35% revenue share in 2025.

- By geography, the Asia-Pacific region delivered 38.18% of the 2025 global revenue and is projected to grow at a 8.89% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Control For Process Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Industrial Automation | +1.8% | Global, with concentration in Asia-Pacific manufacturing hubs (China, India, South Korea) and North America chemical corridors | Medium term (2-4 years) |

| Expansion of Smart Process Industries | +1.5% | Asia-Pacific core, spillover to Middle East petrochemical zones (Saudi Arabia, UAE) | Medium term (2-4 years) |

| Integration of IIoT Sensors and Edge AI | +1.3% | Global, early adoption in North America and Europe, pharmaceutical and food processing facilities | Short term (≤ 2 years) |

| Energy-Efficiency Mandates in Process Plants | +1.0% | Europe (EU Energy Efficiency Directive), North America (EPA regulations), Asia-Pacific (China dual-control policy) | Long term (≥ 4 years) |

| Shift Toward Software-Defined Automation | +0.9% | Global, led by North America and Europe, brownfield modernization projects | Medium term (2-4 years) |

| Emerging Hydrogen and CCUS Projects | +0.7% | Middle East, North America, Gulf Coast, Europe, North Sea region, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Industrial Automation

Industrial facilities continue to implement programmable logic controllers and distributed control systems to mitigate labor constraints and maintain continuous operation of high-value assets. Siemens reported an 18% year-over-year increase in Simatic S7-1500 PLC orders in 2024, primarily driven by battery-cell gigafactories that require deterministic sub-10 millisecond cycle times. Chemical plants are replacing pneumatic loops with digital valve positioners that provide predictive diagnostics, resulting in a 30% reduction in unplanned shutdowns. A 2024 update to IEC 61131-3 introduced object-oriented constructs that enable engineers to reuse code across multi-site rollouts, thereby compressing commissioning schedules and reducing lifecycle costs. Automation density—measured as control points per USD million of plant assets—has increased by 12% since 2020, reflecting stricter environmental discharge limits and an uptick in real-time emissions monitoring.[1]Uday Patel, “Edge AI for Predictive Maintenance in Process Industries,” IEEE Transactions on Industrial Informatics, ieee.org

Expansion of Smart Process Industries

Plant owners are collapsing data silos by linking control layers with enterprise resource planning systems. Schneider Electric reported a 25% growth in licenses for its EcoStruxure platform in 2024, as food and beverage processors sought closed-loop optimization that aligns distillation cut points with downstream demand. The Industrial Internet Consortium has endorsed OPC UA as the cross-domain interoperability layer, providing vendors with a reference blueprint and reducing integration risk.[2]Industrial Internet Consortium, “OPC UA Reference Architecture,” iiconsortium.org China financed 150 smart process pilots in 2024, targeting a 20% reduction in energy intensity by 2027. Early adopters are already reporting payback periods shrinking from five to three years. Smart-plant investments now prioritize real-time scheduling, electronic batch records, and digital twins, shifting value from hardware to analytics and data stewardship.

Integration of IIoT Sensors and Edge AI

Shipments of ABB Ability smart sensors doubled in the first half of 2025 as operators captured hard-to-reach vibration and acoustic data from pumps and compressors. With edge gateways running containerized analytics, latency drops from seconds to milliseconds, unlocking soft-sensor models that infer unmeasured variables, such as catalyst activity. A 2024 IEEE study showed edge AI could detect bearing faults 72 hours earlier than threshold-based alarms, preventing million-dollar outages. Emerson’s DeltaV now embeds TensorFlow Lite, enabling process engineers to deploy neural networks without requiring deep coding skills. The result is a shift in budget from reactive maintenance to condition-based workflows, which extend asset life and defer capital expenditures.

Energy-Efficiency Mandates in Process Plants

The European Union’s Energy Efficiency Directive requires a 1.5% annual reduction in energy intensity, prompting refineries and chemical plants to adopt model-predictive control that stabilizes steam header fluctuations and minimizes flaring. China’s dual-control policy caps total consumption and intensity, accelerating rollout of advanced process control that shaved 8-12% specific energy at pilot sites in 2024. In the United States, Environmental Protection Agency rules on greenhouse-gas intensity are steering stimulus toward software that tunes heat exchanger duty cycles in real-time. Vendors that can pair analytics with proven payback are closing multi-year software subscriptions, which lock in recurring revenue and deepen customer stickiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of OT-Cybersecurity Talent | -0.8% | Global, acute in North America and Europe, where IEC 62443 certification is mandatory for critical infrastructure | Short term (≤ 2 years) |

| High Capital Investment and ROI Uncertainty | -1.2% | Global, most pronounced in South America and Africa, where commodity price volatility constrains capex budgets | Medium term (2-4 years) |

| Legacy System Interoperability Issues | -0.6% | North America and Europe brownfield sites with 20-30 year-old installed bases | Medium term (2-4 years) |

| Rising Threat Surface for ICS Cyberattacks | -0.9% | Global, with elevated risk in critical infrastructure sectors (power, oil and gas, water treatment) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of OT-Cybersecurity Talent

The widening gap between cyber threats and qualified defenders is slowing project execution. The International Society of Automation found that 40% of IEC 62443 posts remained vacant beyond six months in 2024, resulting in a 22% increase in median salaries.[3]International Society of Automation, “Workforce Survey: OT Cybersecurity Skills Gap,” isa.org Many operators postpone critical patching because they lack staff able to validate firmware without halting production. Universities and vendor academies trail demand, locking in a multi-year bottleneck that tempers otherwise strong growth.

High Capital Investment and ROI Uncertainty

Greenfield petrochemical complexes can earmark USD 50-100 million for distributed control, safety, and associated infrastructure, yet commodity volatility clouds payback models. Emerson reported a 15% uptick in project deferrals in 2024 as oil and gas firms awaited clarity on carbon pricing before committing.[4]Emerson Electric Co., “Annual Report 2024,” emerson.com Brownfield retrofits face even steeper economic challenges, often requiring the addition of protocol gateways and redundant I/O, which can inflate the total cost by 30-40%. Mid-sized firms struggle to secure financing when lenders demand sub-four-year payback thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: Manufacturing Execution Systems Capture Real-Time Production Intelligence

Manufacturing execution systems are projected to grow at a 10.04% CAGR to 2031, outpacing the overall industrial control for process automation market. In 2025, programmable logic controllers held a 31.58% share of the industrial control for process automation market, but incremental value is migrating toward higher-level orchestration as firms seek real-time visibility and electronic batch records. Distributed control systems continue to underpin continuous processes, such as refining and pulp production, due to their fault tolerance and embedded model-predictive control capabilities. Across the food, beverage, and pharmaceutical industries, hybrid architectures are emerging that combine a unified dashboard with process data, quality metrics, and scheduling, thereby reducing operator cognitive load and improving response to deviations.

The demand for digitally native manufacturing execution systems is underpinned by regulatory frameworks, such as the United States' FDA 21 CFR Part 11, which mandates the creation of traceable electronic records. The 2024 update to ISA-95 endorsed event-driven messaging, which speeds handoffs between enterprise resource planning systems and plant-floor controllers. As a result, the industrial control for process automation market size tied to manufacturing execution systems is shifting toward subscription revenue, anchored in analytics, quality management, and digital twin support. Vendors court this growth by pre-integrating libraries for batch genealogy, recipe management, and serialization, shortening deployment cycles and raising switching costs.

By Component: Software Outpaces Hardware as Control Logic Migrates to Edge

Software revenue is expanding at a 9.37% CAGR, eclipsing hardware’s contribution to the industrial control for process automation market. Although hardware still accounted for 46.35% of revenue in 2025, containerization is enabling control strategies to run on standard servers at the edge, thereby reducing demand for proprietary controllers. Siemens Industrial Edge saw 35% license growth in 2024 as food and beverage plants prioritized flexible recipe changes and rapid line restarts. Meanwhile, high-reliability safety instrumented modules certified to IEC 61508 SIL 3 maintain premium pricing, creating a two-speed hardware landscape.

Edge gateways that translate legacy fieldbus traffic into Ethernet and wireless protocols are a notable strength in hardware, as demonstrated by double-digit unit gains at Moxa and Advantech. Yet the broader hardware segment continues to grapple with commoditization and margin compression, prompting vendors to bundle analytics and cybersecurity subscriptions. Consequently, industrial control for process automation market size growth is disproportionately concentrated in software modules for advanced analytics, threat monitoring, and predictive control.

By Service: Consulting Surges as Operators Navigate OT-IT Convergence

Consulting services are expected to rise at a 9.68% CAGR, the sharpest within the service segment. System integration and deployment accounted for 37.46% of the revenue in 2025, but will cede share as pre-engineered libraries and digital twins reduce the need for custom engineering hours. Consulting services focus on cybersecurity assessments against the IEC 62443 and NERC CIP frameworks, as well as design and migration roadmaps for segmentation. Accenture and Deloitte have carved out operational technology practices, leveraging enterprise relationships to cross-sell modernization projects and managed services.

Support and maintenance faces disruption as vendors stream live diagnostics into cloud portals, cutting on-site service calls by up to 30%. Some integrators now offer uptime-based contracts that convert capital expenditures into operating expenditures, aligning incentives with efficiency gains. Overall, the industrial control for process automation market is seeing services revenue tilt toward advisory and managed offerings that mitigate skills gaps rather than traditional break-fix engagements.

By End-User Vertical: Life Sciences Leads Growth on Serialization and Continuous Bioprocessing

The life sciences sector is forecast to grow at 10.96% per year to 2031, the quickest among verticals, driven by the continuous adoption of bioprocesses and serialization mandates. Sterile drug manufacturers must track critical parameters in real time under the FDA’s revised Annex 1, propelling demand for electronic batch records and model-predictive control. Oil and gas retained a commanding 25.62% share in 2025, yet its growth rate lags the industrial control for process automation market average as operators favor incremental debottlenecking over greenfield builds.

The adoption of advanced process control across the chemicals and petrochemical industries is increasing as firms seek yield gains and carbon reductions. Emerson and Honeywell each tout multi-site deployments that enhance reactor throughput while lowering CO₂ emissions per ton. Power utilities are modernizing supervisory control and data acquisition systems to integrate variable renewables, and metals and mining outfits are testing autonomous haulage systems reliant on low-latency wireless. While other verticals, such as pulp, water, and cement, show steadier adoption, targeted upgrades focused on energy and emissions keep them engaged.

By Communication Network: Industrial Wireless Surges on 5G and Time-Sensitive Networking

Industrial wireless networks are projected to grow at a rate of 13.05% annually to 2031, the highest among all segmentation categories; however, wired Ethernet still held a 67.35% revenue share in 2025. The economics of trenching and conduit make wireless compelling: ISA studies peg hazardous-area cabling at USD 500-1,000 per meter, while WirelessHART gateways cover comparable footprints at one-third the cost. Release 17 of the 3GPP standardized ultra-reliable low-latency communication profiles, and Siemens, along with Nokia, demonstrated 1 millisecond latency in a German automotive plant in 2024. These performance gains meet IEC 61784-2 Class C motion-control thresholds, unlocking robotics, AGVs, and mobile inspection drones.

Time-sensitive networking overlays deterministic scheduling on standard Ethernet, enabling converged backbones that mix safety-critical and best-effort traffic. As private 5G transitions from pilots to scaled deployments, the industrial control and process automation market anticipates a new wave of retrofit spending on wireless-ready controllers, ruggedized access points, and spectrum management tools. Adoption is also facilitated by embedded encryption and mutual authentication, which surpasses legacy wired security, satisfying new cybersecurity directives without requiring massive re-cabling.

Geography Analysis

Asia-Pacific dominated with 38.18% of 2025 revenue and is poised to advance at a 8.89% CAGR through 2031, comfortably above the global trajectory. China’s dual-control policy spurred advanced control rollouts that sliced energy per unit output by up to 12% in pilot petrochemical sites. India’s INR 150 billion Production Linked Incentive scheme (USD 1.8 billion) has triggered rapid investments in distributed control and manufacturing execution across 200 API facilities. Japan’s aging workforce accelerated automation in the packaged food and chemicals industries, driving double-digit domestic orders for Yokogawa. South Korea’s battery and chip fabs adopted sub-nanometer quality loops, leaning on Siemens and Mitsubishi controllers to achieve uniformity at scale.

North America and Europe remain hotspots for modernization. The U.S. Cybersecurity and Infrastructure Security Agency issued 320 industrial control advisories in 2024, sparking an estimated USD 2.1 billion in retrofit services. The European Union’s NIS2 directive enforces IEC 62443-aligned risk management, and Germany’s chemical sector has invested EUR 1.2 billion (USD 1.3 billion) in digitalization initiatives, resulting in a 15% reduction in reactor emissions per ton. Brownfield adoption dominates spending as asset owners patch cybersecurity gaps and overlay analytics on aging control layers.

The Middle East and Africa exhibit rising potential tied to hydrogen and carbon capture megaprojects. Saudi Arabia’s NEOM green-hydrogen plant will utilize Siemens' distributed control system to orchestrate 4-gigawatt electrolyzer arrays. The United Arab Emirates expanded the Al Reyadah carbon capture facility with Emerson controls. Brazil’s pre-salt fields have introduced subsea programmable logic controllers, and South Africa’s miners are piloting private 5G and edge gateways. While currency swings and commodity price shifts temper broader adoption, lighthouse projects in hydrogen, CCUS, and mining will seed future growth.

Regulatory Landscape

Industrial control for process automation is increasingly shaped by cybersecurity and functional safety requirements that are being operationalized through widely adopted standards. In March 2026, the US Federal Energy Regulatory Commission (FERC) approved updates to NERC Critical Infrastructure Protection (CIP) Reliability Standards, including CIP-003-11 and a broader set of modified CIP standards, extending compliance attention to lower-impact bulk electric system cyber assets and virtualization-aware environments. In Europe, the EU Cyber Resilience Act introduces staged obligations for digital products, with vulnerability reporting requirements starting 11 September 2026 and broader compliance obligations effective 11 December 2027, increasing pressure on industrial automation vendors to harden software supply chains and product security processes.

Standards bodies are reinforcing IEC 62443 alignment as a compliance backbone for industrial automation and control systems (IACS). IEC PAS 62443-2-2:2025, published 11 March 2025, formalizes a security protection scheme approach for asset owners and suppliers, while work to align EN IEC 62443 component requirements with CRA conformity assessment (for example, prAA activity tied to IEC 62443-4-2) signals closer linkage between product engineering, certification, and procurement. The UK Department for Energy Security and Net Zero also published a June 2026 consultation on a Tier 1 Cyber Assessment Framework profile for large load controllers under NIS Regulations, pointing to tighter governance around remotely controllable industrial loads and associated OT remote-access practices.

Value Chain Analysis

The value chain spans component suppliers (controllers, instrumentation, drives, industrial networking, and compute), automation OEMs (PLC, DCS, SCADA, MES, and safety systems), software and data-layer providers (historians, analytics, and cloud/edge platforms), and delivery partners (system integrators, engineering procurement and construction firms, and managed service providers). Major suppliers active across these layers include Siemens, ABB, Schneider Electric, Emerson, Honeywell, Rockwell Automation, and Yokogawa, with software-centric players influencing orchestration and analytics. System integrators play an outsized commercialization role, with industry survey evidence indicating they account for the majority of automation supplier sales, and they often determine platform selection through front-end engineering design, cybersecurity architecture, and brownfield migration planning.

OT-IT convergence is reshaping how value is created and captured, shifting differentiation toward data integration, application portability, and lifecycle services rather than proprietary hardware alone. The supply chain for industrial controls also reflects geopolitical and sourcing dependencies; a 2025 system integrator survey cited notable China-origin content in North American sourcing, with industrial controls a prominent category, which increases attention on multi-sourcing, inventory strategies, and redesign for alternate components. Downstream, distribution and deployment are increasingly tied to ecosystem partnerships that combine automation with IT infrastructure and data platforms, supporting cloud-to-edge deployment, digital twins, and AI-enabled optimization across multi-vendor plants.

Competitive Landscape

The top five vendors, Siemens, ABB, Schneider Electric, Emerson, and Rockwell Automation, accounted for a significant share of 2024 revenue, indicating a moderately concentrated field. Incumbents are bolstering software depth: Schneider Electric finalized Aveva’s full integration, expanding from hardware into unified data platforms, while Siemens infused generative AI into Simatic code assistants. ABB acquired Sevensense Robotics to bridge factory control with logistics automation, and Emerson bought General Electric’s distributed control business to rank second by installed base.

Cybersecurity partnerships are proliferating. Honeywell partnered with Palo Alto Networks to integrate next-generation firewalls directly into Experion nodes, simplifying IEC 62443 compliance for asset owners. Edge compute collaborations also multiply; Rockwell Automation is embedding NVIDIA inference accelerators into controllers, enabling real-time vision inspection. Patent filings reveal a tilt toward model-based control and AI twin technologies, with ABB securing 18 patents tied to physics-informed neural networks in 2024.

Disrupters from the cloud arena offer data historians as managed services—AWS IoT SiteWise and Microsoft Azure Industrial IoT position themselves as neutral aggregation layers that bypass proprietary hardware. Wireless specialists, such as CoreTigo, bundle time-sensitive networking into retrofit modules, while HMI pure-play ICONICS leverages augmented reality to minimize downtime during changeovers. As brownfield owners demand lower capex and open ecosystems, competitive lines blur between traditional automation hardware firms, software start-ups, and hyperscalar cloud providers.

Industrial Control For Process Automation Industry Leaders

ABB Ltd.

Schneider Electric SE

Emerson Electric Co.

Rockwell Automation Inc.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Software-defined automation and modernization-as-a-service create whitespace in brownfield process plants where uptime constraints limit rip-and-replace projects. Schneider Electric introduced Industrial Automation Modernization as a Service in June 2026, built around EcoStruxure Automation Expert and HPE SimpliVity infrastructure, underscoring operator demand for phased migration, hybrid deployment models, and standardized engineering that reduces on-premise lifecycle burden. This opportunity concentrates around multi-site operators that need consistent cybersecurity posture (IEC 62443-aligned) and repeatable deployment patterns across PLC, DCS, SCADA, and MES layers.

Field connectivity and safety-rated instrumentation also represent actionable expansion areas as plants pursue higher data density for advanced process control, asset health, and autonomy. ABB activity around Ethernet-APL deployments in China (including projects with chemical and petrochemical operators) and its June 2026 SIL 2 certification for the SensyMaster FMT400 flowmeter illustrate how Ethernet-to-field upgrades and functional safety compliance are moving closer to the device layer, enabling richer diagnostics while maintaining Safety Instrumented System integration under IEC 61508. Large capital projects provide another avenue for platform wins: in July 2026, Yokogawa was awarded the main automation contractor role for the Commonwealth LNG project in Louisiana, highlighting how mega-project awards can lock in multi-year demand across control systems, safety, and lifecycle services for new-build process assets.

Recent Industry Developments

- July 2026: ABB secured an order from Zhejiang Petroleum & Chemical to supply ProcessMaster FEP600 electromagnetic flowmeters with Ethernet-APL for a major refining complex in Zhoushan, China. The award advances higher-speed, Ethernet-based field connectivity for process instrumentation, which supports denser diagnostics and faster data movement into DCS/asset performance layers. It also reinforces Ethernet-APL as a practical upgrade path for large-scale petrochemical sites pursuing digitalization without overhauling the entire control backbone.

- June 2026: Schneider Electric launched Industrial Automation Modernization as a Service, combining EcoStruxure Automation Expert with HPE SimpliVity hybrid-cloud infrastructure. The offering formalizes a consumption and lifecycle approach to modernizing legacy control environments, aligning capex constraints with phased migration and standardized deployment patterns. It also broadens the competitive battlefield to include infrastructure and platform partners as customers converge OT control and IT operations.

- May 2025: Emerson introduced Project Beyond to modernize and integrate the industrial automation technology stack across control, data, and software layers. The initiative emphasizes tighter interoperability and modernization roadmaps that help process operators connect legacy systems to newer analytics and orchestration capabilities. It supports vendor strategies aimed at increasing recurring software and services attachment around installed control bases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned from industrial control used to monitor, control, and optimize process automation in industrial plants, across hardware, software, and related services that support day-to-day operations and safe production.

Scope exclusions: Discrete factory automation-only controls (that are not used for process industries) and standalone IT enterprise software that is not tied to control or plant operations are excluded.

Segmentation Overview

- By System

- Supervisory Control and Data Acquisition System (SCADA)

- Distributed Control System (DCS)

- Programmable Logic Controller (PLC)

- Manufacturing Execution System (MES)

- Product Lifecycle Management (PLM)

- Enterprise Resource Planning (ERP)

- Human Machine Interface (HMI)

- Other Systems

- By Component

- Hardware

- Software

- Services

- By Service

- Consulting

- System Integration and Deployment

- Support and Maintenance

- By End-user Vertical

- Oil and Gas

- Chemical and Petrochemical

- Power

- Life Sciences

- Food and Beverage

- Metals and Mining

- Other End-user Verticals

- By Communication Network

- Wired Networks

- Industrial Wireless Networks

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To set a reliable starting point, we build a desk research base around public statistics and technical references that explain demand by process industry. Common inputs include sources such as the US Energy Information Administration for energy and refining signals, the USGS for mining and metals activity, the International Energy Agency for broader energy transition indicators, and the World Bank and IMF for country-level industrial output and inflation assumptions.

We also review non-paywalled publications from standards and trade bodies such as ISA and IEC, along with peer-reviewed journals that track control system trends in DCS, SCADA, PLCs, and industrial networking. Company filings, earnings decks, press releases, and plant expansion news are used to understand product mix and spending cycles, and then paid subscription data for company financials, patent lookups, and shipment-level trade checks is used selectively to validate scale and directional movement. The specific desk sources listed here are illustrative, and many other public references were reviewed for cross-checking, data clarification, and validation.

Primary Interviews and Surveys

Primary work is used to pressure test desk assumptions and convert activity signals into spend, especially where plants upgrade controls in phases and budgets move between hardware, software, and services. We speak with a mix of control system suppliers, system integrators, and process industry users across APAC, EMEA, and the Americas. The discussions focus on replacement cycles, typical project scopes, and pricing movement by system type and service line.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 47% |

| Mid tier: 59% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 15% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where plant-level automation spending is reconstructed from end-user activity indicators in oil and gas, chemicals, power, metals and mining, food and beverage, and life sciences, and then distributed across control systems and service types. The totals are corroborated with selective bottom-up approximations, such as sampling system average selling prices and typical project volumes, plus channel and integrator checks, so the final market value stays realistic.

Key inputs used in the model include process industry capex and retrofit intensity, installed base modernization cycles, the share of plants adopting industrial wireless and wired upgrades, software and service attach rates in control projects, and regional mix shifts tied to new capacity additions. When gaps appear, they are handled through ratio-based interpolation using adjacent country benchmarks and expert-validated adoption ranges, before totals are brought back in line with observed procurement patterns.

For forecasting, we rely on scenario analysis supported by a simple multivariate regression layer that links market growth to industrial production, process industry capex, energy and commodity cycles, and expected control system replacement timing. Assumptions are reviewed with interview feedback, and then applied consistently across regions to keep the forecast repeatable and easy to trace.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, so modeled totals are checked against process industry investment trends, automation project announcements, and supplier commentary on order books and pricing. Outliers are flagged, and the underlying drivers are rechecked. A separate analyst review is completed before sign-off.

The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp commodity price swings, major regulatory changes in safety or emissions, or large project pipeline shifts. Before delivery, a final pass is completed so the numbers, assumptions, and recent developments align with the latest available information.

Mordor Intelligence's Industrial Control for Process Automation Market Size Compared With Other Published Estimates

Published market sizes for industrial control in process automation can look far apart, even when the topic label sounds similar. In our experience, the gaps usually come from what gets counted as a control system versus adjacent equipment, how services are treated, and whether the number represents plant operations spend or factory-gate revenue.

Some estimates broaden the scope by bundling field devices and add-on electrical equipment, or they narrow it by focusing on only a few system categories. The split is visible in the table, because Mordor Intelligence counts SCADA, DCS, PLC, MES, PLM, ERP, and HMI within a defined process automation control stack, and then ties services to consulting, integration, and support that directly relate to those deployments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 81.89 B (2026) | |

| Global Research Publisher A | USD 45.56 B (2026) | Uses a factory-gate framing and a narrower system list, with sizing anchored to manufacturer-level revenues, which tends to undercount integration-heavy project value captured across the delivery chain. |

| Industry Research Firm B | USD 86.58 B (2024) | Uses a different base year and folds a broader hardware bucket into the pool, including items like sensors, actuators, and motion systems, so the figure behaves more like a wider process manufacturing automation spend number. |

Taken together, the spread mainly reflects scope and accounting choices, plus the year used for the headline figure. By keeping the inputs tied to process industry activity, control project mix, and service attachment logic, the resulting market size stays transparent and can be replicated with the same steps as new data comes in.

Key Questions Answered in the Report

How fast is spending on wireless control infrastructure growing?

Industrial wireless networks in the industrial control for process automation market are forecast to rise at a 13.05% CAGR through 2031, the highest of any segmentation type.

Which software layer is seeing the quickest uptake inside process plants?

Manufacturing execution systems lead with a 10.04% CAGR because companies want real-time visibility and electronic batch records for compliance.

Why is life sciences outpacing other verticals?

Serialization mandates and continuous bioprocessing push life-science facilities to adopt closed-loop control and digital batch tracking, driving an 10.96% annual growth rate.

What is the key hurdle to faster modernization?

High upfront capital and uncertain commodity pricing slow return on investment, dampening near-term adoption despite proven efficiency gains.

How are vendors addressing cybersecurity risk?

Leading suppliers integrate IEC 62443-certified firewalls, offer managed detection services, and embed threat-monitoring analytics directly in controllers to offset the OT talent shortfall.

Which region will contribute the most incremental revenue by 2031?

Asia-Pacific is expected to add the largest absolute dollar gain, expanding at a 8.89% CAGR on the back of greenfield petrochemical and pharmaceutical investments.

Page last updated on: