Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

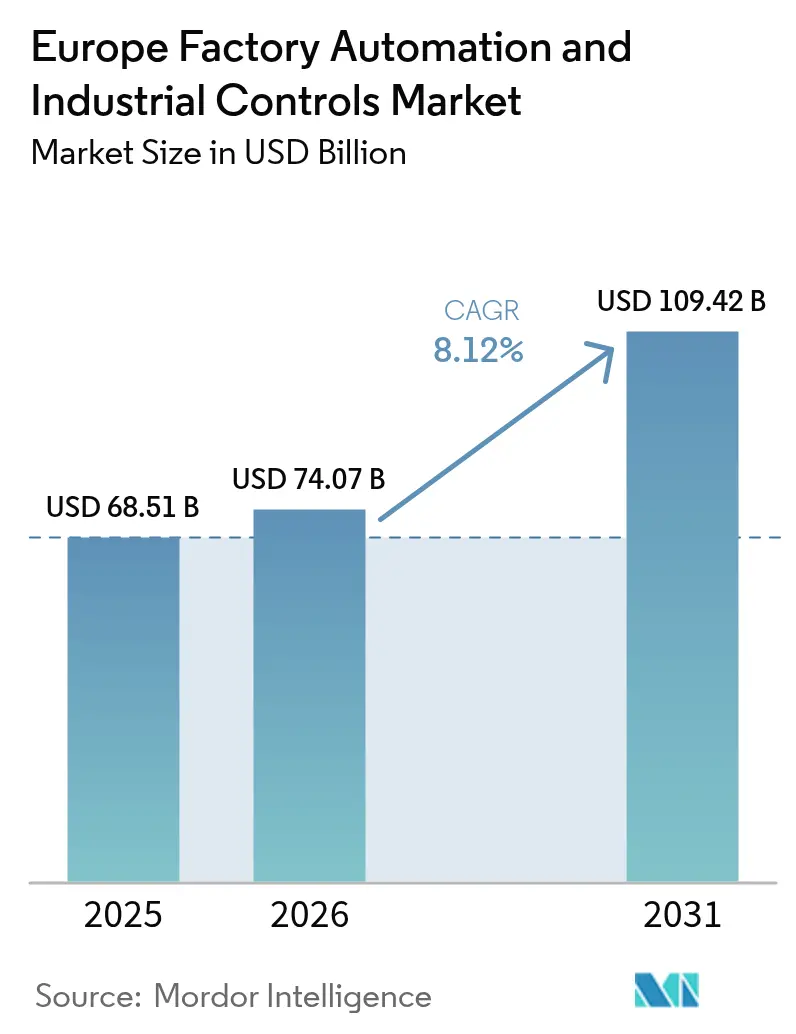

| Base Year Market Size (2025) | USD 68.51 Billion |

| Market Size (2026) | USD 74.07 Billion |

| Market Size (2031) | USD 109.42 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

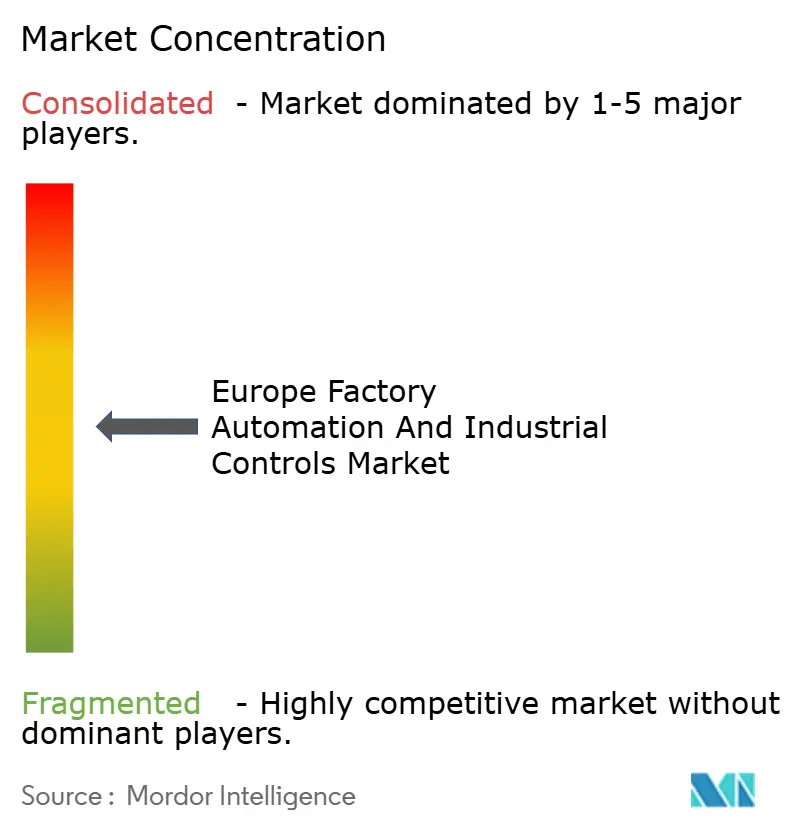

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Factory Automation And Industrial Controls Market Analysis by Mordor Intelligence

The Europe factory automation and industrial controls market size was valued at USD 68.51 billion in 2025 and estimated to grow from USD 74.07 billion in 2026 to reach USD 109.42 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). Digital transformation programs, net-zero mandates, and accelerating electric-vehicle battery production are pushing manufacturers to modernize with energy-efficient controls and AI-driven robotics. Germany still sets the pace with 429 industrial robots per 10,000 employees, yet waning competitiveness is shifting new orders toward Nordic plants powered by fossil-free electricity.[1]Germany Trade & Invest, “Robotics Industry in Germany,” gtai.de EU funding for AI Factories is widening access to high-performance computing, enabling predictive-maintenance platforms that curb downtime and shrink power bills. Intensifying semiconductor supply-chain risks and legacy-system cybersecurity gaps add urgency for cloud-connected, software-centric upgrades that safeguard operational continuity.[2]European Commission, “European Commission presents its Competitiveness Compass,” ec.europa.eu Together, these forces position the Europe factory automation and industrial controls market for sustained double-digit growth as factories seek to balance productivity gains with decarbonization requirements.

Key Report Takeaways

- By product type, programmable logic controllers captured 27.98% revenue share in 2025, while manufacturing execution systems are set to expand at a 9.78% CAGR through 2031.

- By field device type, industrial robots commanded 31.05% share in 2025, whereas machine-vision systems are forecast to advance at a 9.05% CAGR to 2031.

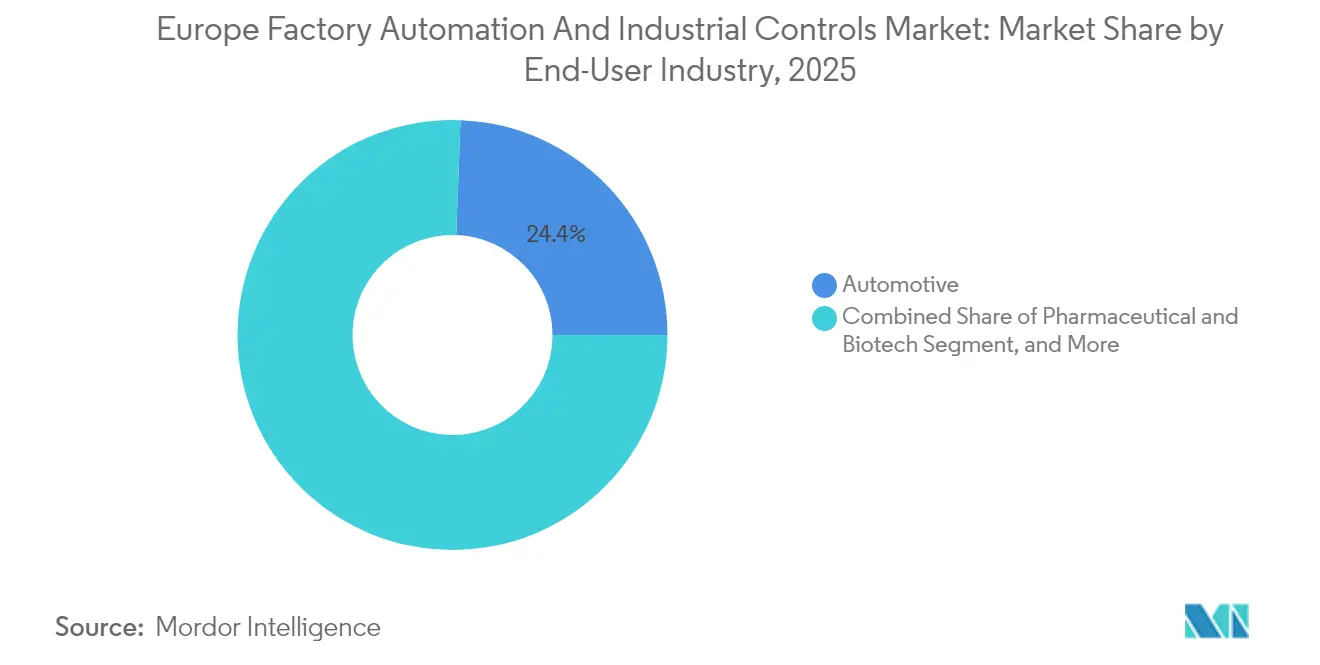

- By end-user industry, automotive applications accounted for 24.41% demand in 2025; pharmaceutical and biotech facilities are projected to rise at a 9.62% CAGR during the same period.

- By deployment model, on-premises solutions dominated with 63.35% share in 2025, yet cloud-enabled platforms are poised for a 9.96% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Factory Automation And Industrial Controls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Emphasis on Energy-Efficient Smart Factories | +2.10% | Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Accelerated Automotive Electrification Demands | +1.80% | Germany, France, Italy, Spain | Short term (≤ 2 years) |

| Regulatory Push for Net-Zero Industrial Emissions | +1.50% | EU-wide, strongest in Germany and France | Long term (≥ 4 years) |

| AI-Enabled Predictive Maintenance Adoption | +1.30% | Germany, UK, Netherlands, Sweden | Medium term (2-4 years) |

| Reshoring of Strategic Industries into Europe | +1.00% | Germany, France, Poland, Czech Republic | Long term (≥ 4 years) |

| EU Digital Twin Funding for Manufacturing | +0.60% | Germany, France, Austria, Bulgaria, Poland, Slovenia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Energy-Efficient Smart Factories

EU manufacturers are prioritizing energy-efficient automation to reduce carbon footprints and shield margins from volatile power prices. The Made in Europe Partnership, launched in April 2025, targets zero-defect and zero-downtime production by combining AI with real-time data analytics, while Sweden’s 98% fossil-free electricity underpins large-scale robotics rollouts. Danish SMEs in the Digital Factory Acceleration program report 10-20% efficiency gains after migrating to paperless workflows with live performance dashboards. ABB’s purchase of Sensorfact highlights the surge in demand for granular energy-monitoring platforms that comply with ISO 50001 and feed continuous-improvement loops across the Europe factory automation and industrial controls market.

Accelerated Automotive Electrification Demands

Battery-cell production lines now dominate greenfield projects as European automakers retool for electric-vehicle volumes. Robotic solutions built for electrode stacking, electrolyte filling, and end-of-line inspection are replacing legacy welding cells. Machine-vision systems capable of detecting defects below 10 parts per million are becoming standard on battery components. Flexible programmable logic controllers and adaptive manufacturing execution systems let plants switch between lithium-ion chemistries without extended downtime, reinforcing demand for modular, future-proof controls.

Regulatory Push for Net-Zero Industrial Emissions

The Corporate Sustainability Reporting Directive obliges thousands of factories to quantify and disclose Scope 1 and Scope 2 emissions, prompting investment in connected sensors that capture real-time energy data. The Net-Zero Industry Act directs public procurement toward technologies with 40% lower lifecycle emissions, accelerating orders for variable-frequency drives, smart sensors, and high-efficiency motors. Funding for AI Factories spanning six EU countries adds a pipeline of trustworthy industrial-AI models that optimize throughput while trimming carbon intensity.

AI-Enabled Predictive Maintenance Adoption

Two-thirds of European manufacturers intend to deploy AI-based condition monitoring within two years. Edge-to-cloud architectures analyse vibration, temperature, and acoustic signatures to flag anomalies up to four weeks before failure, cutting unplanned downtime by 30%. Automatic work-order creation and parts-inventory synchronization reduce maintenance labour hours and shrink spare-parts capital tied up in warehouses. Compliance with ISO 13374 is easing corporate-risk reviews, speeding rollouts across the Europe factory automation and industrial controls market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Legacy-System Cybersecurity Gaps | -1.20% | Global, with higher exposure in Germany and UK | Short term (≤ 2 years) |

| Trade Tensions on Semiconductor Supply Chains | -0.90% | EU-wide, particularly affecting automotive hubs | Medium term (2-4 years) |

| Fragmented SME Funding for Automation | -0.70% | Southern and Eastern Europe | Medium term (2-4 years) |

| Workforce Resistance to Hyper-Automation | -0.50% | France, Italy, traditional manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Legacy-System Cybersecurity Gaps

Nearly four-fifths of European plants still operate at least one programmable logic controller installed before modern security frameworks existed, leaving production assets exposed to ransomware. Temporary network segmentation and industrial firewalls offer partial relief, yet full IEC 62443 compliance demands controller retrofits that strain capital budgets. Insurance premiums for manufacturers with outdated controls have risen, nudging board-level approval for phased replacements but stretching project timelines.

Trade Tensions on Semiconductor Supply Chains

Three-quarters of automation-grade microcontrollers used in European factories originate in Asia, driving lead times as high as 52 weeks for niche chips during 2024. Price volatility adds 15–25% to automation project costs, forcing integrators to hedge with buffer inventory. The European Chips Act promises to widen domestic output by 2028, but interim risk persists, dampening near-term equipment orders in the Europe factory automation and industrial controls market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PLCs Anchor Market While MES Drives Digital Transformation

Programmable logic controllers accounted for 27.98% of the Europe factory automation and industrial controls market share in 2025, reflecting their ubiquity in discrete manufacturing lines that demand deterministic control. The segment remains stable as brownfield upgrades replace aging hardware with energy-efficient units featuring native cybersecurity. Manufacturing execution systems are projected to grow at a 9.78% CAGR to 2031, propelled by real-time production visibility mandates under ISO 9001 and traceability clauses in automotive and pharmaceutical standards. The Europe factory automation and industrial controls market size tied to MES adoption is widening as cloud subscriptions lower entry costs for mid-tier suppliers. Second-order gains emerge from tighter ERP integration that synchronizes demand forecasts with line scheduling, minimizing work-in-progress inventory.

Distributed control systems continue to serve process industries that value high-availability architectures, though growth is modest compared with software layers that unlock predictive-analytics functions. Supervisory control and data acquisition platforms are shifting toward browser-based clients, enabling remote oversight for multi-site operations. Human-machine interfaces integrate mobile alerts and contextual video streams that support faster troubleshooting from off-site experts. Product-lifecycle-management deployments are increasing under EU-funded digital-twin pilots, allowing designers to validate sustainability metrics in silico before capital builds.

By Field Device Type: Industrial Robots Lead While Machine Vision Accelerates

Industrial robots held 31.05% of the Europe factory automation and industrial controls market share in 2025, underpinned by Germany’s installed base of 429 units per 10,000 workers. Automotive electrification and consumer-goods packaging keep six-axis and delta robots in high demand, while collaborative variants post double-digit unit growth thanks to reduced guarding requirements. Machine-vision systems, advancing at a 9.05% CAGR, are rapidly expanding the Europe factory automation and industrial controls market size as AI algorithms cut false-rejection rates in battery-cell inspection and sterile drug filling. Edge processors inside smart cameras execute inference locally, avoiding cloud latency and securing sensitive production data.

Sensor and transmitter volumes rise alongside predictive-maintenance rollouts that depend on vibration and temperature data streams. Motors and drives are trending toward high-efficiency classes, with variable-frequency drives standardizing on IE5-rated motors to meet net-zero targets. Intelligent actuators embed self-diagnostics that flag torque anomalies, supporting decentralized architectures that improve resilience when central controllers go offline.

By End-User Industry: Automotive Dominates While Pharma Accelerates

Automotive plants accounted for 24.41% of overall demand in 2025, anchored by Germany, France, and Italy’s vehicle clusters transitioning to battery-electric models. Highly flexible welding, painting, and final-assembly cells require reconfigurable digital twins to accommodate rapid platform updates. Pharmaceutical and biotech facilities are forecast to post a 9.62% CAGR to 2031 as demand for personalized therapies pushes automation deeper into aseptic processing and high-mix packaging. The Europe factory automation and industrial controls market size within pharma is bolstered by stringent validation norms that favour robotics for contamination-free handling.

Food and beverage processors upgrade to stainless-steel robotics that meet IP69K wash-down standards, while chemical plants adopt explosion-proof drives compliant with ATEX directives. Energy-sector investments focus on automated blade manufacturing for wind turbines and power-electronics assembly for solar inverters. Metals and mining operators turn to ruggedized autonomous haulage and ore-sorting systems that withstand abrasive environments, extending the Europe factory automation and industrial controls market beyond traditional factory confines.

By Deployment Model: On-Premises Dominates While Cloud Adoption Accelerates

On-premises installations represented 63.35% share in 2025, reflecting stringent uptime and data-sovereignty requirements on critical production assets. Still, cloud-enabled deployments are projected to grow at a 9.96% CAGR, as IEC 62443-compliant gateways and zero-trust architectures address cybersecurity objections.

Hybrid edge-cloud frameworks process time-critical loops locally while off-loading long-horizon analytics to hyperscale data centers, balancing latency and cost. Subscription-based software models appeal to SMEs that prefer operating-expense budgeting, expanding the Europe factory automation and industrial controls market’s reach into previously under-automated tiers.

Geography Analysis

Germany leads regional adoption with EUR 16.2 billion in robotics and automation turnover, yet competitive pressures signal a gradual demand shift. Nordic states, spearheaded by Sweden’s EUR 24 billion industrial-technology revenue and 98% fossil-free grid, attract battery-cell and precision-machining investments that require high-density automation. The United Kingdom climbs global manufacturing rankings, buoyed by Schneider Electric’s GBP 42 million smart-factory retrofit in Scarborough that showcases edge-to-cloud controls.

France leverages aerospace and automotive clusters to sustain robotics orders, while Italy’s machinery heritage underpins steady demand for CNC-driven assembly lines. Spain’s renewable-energy build-out fosters automation for turbine-blade and solar-panel manufacturing, expanding the Europe factory automation and industrial controls market size across Iberia. The Netherlands positions itself as a controls-software hub, highlighted by Accerion’s AI-based localization tech acquired by SICK.

Poland emerges as an automation destination, exemplified by Engel’s factory near Gdansk Airport slated for 2025 completion, offering near-shoring advantages and EU-funded infrastructure. Czech Republic and Hungary target electronics reshoring with incentives for brownfield conversions. Rest-of-Europe territories tap EU cohesion funds to modernize legacy plants, though fragmented SME financing restrains pace relative to core markets.

Competitive Landscape

Moderate consolidation defines the Europe factory automation and industrial controls market, with Siemens, ABB, and Schneider Electric leveraging vertical integration across controllers, drives, and software suites. ABB’s 2025 acquisition of Sensorfact adds cloud-native energy-monitoring to its portfolio, illustrating the pivot toward data services. SICK’s purchase of Accerion broadens its autonomous-mobile-robot stack, while Prima Industrie’s integration of Sistec AM strengthens turnkey robotics capabilities. Mid-tier players focus on domain-specific software niches, such as computer vision for low-contrast inspection or edge analytics for brownfield equipment.

Start-ups exploit gaps in legacy-system cybersecurity, offering zero-trust gateways and AI threat detection tailored for operational-technology networks. Semiconductor bottlenecks spark joint ventures aimed at developing European sourcing alternatives for motion-control chips. Service providers build managed-services offerings that bundle predictive-maintenance analytics with certified technicians, reducing entry barriers for SMEs.

Strategic partnerships between robot makers and MES vendors evolve to deliver pre-integrated packages that shorten commissioning timelines. Cloud-platform alliances with automation majors promise unified dashboards combining energy, quality, and maintenance KPIs, widening cross-sell potential. Competitive intensity centers on software differentiation rather than hardware performance, amplifying value capture at the analytics layer within the Europe factory automation and industrial controls market.[4]ARC Advisory Group, “European Automation Champions Report 2023,” arcweb.com

Europe Factory Automation And Industrial Controls Industry Leaders

Rockwell Automation Inc.

Schneider Electric SE

Siemens AG

ABB Ltd

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The European Commission approved EUR 485 million for the second wave of AI Factories across six member states.

- January 2025: ABB completed the acquisition of Sensorfact to enhance cloud-connected energy-monitoring capabilities.

- January 2025: SICK AG acquired Accerion, adding AI-based image-processing localization to its autonomous-mobile-robot portfolio.

- January 2025: Prima Industrie SpA purchased Sistec AM to expand robotic-automation offerings.

Europe Factory Automation And Industrial Controls Market Report Scope

The factory automation and control solutions facilitate the automation of a production facility/entire manufacturing by constructing and designing a wholly intelligent and integrated control system, including robots, sensors, computers, industrial instruments, and advanced data processing solutions.

The Europe Factory Automation and Industrial Controls Market is segmented by type (industrial control systems, field devices), by end-user industry (automotive, chemical and petrochemical, power and utility, pharmaceutical, food and beverages, oil and gas), and by country. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Distributed Control Systems (DCS) |

| Programmable Logic Controllers (PLC) |

| Supervisory Control and Data Acquisition (SCADA) |

| Manufacturing Execution Systems (MES) |

| Product Lifecycle Management (PLM) |

| Human Machine Interface (HMI) |

| Enterprise Resource Planning (ERP) |

By Field Device Type

| Industrial Robots |

| Machine Vision Systems |

| Sensors and Transmitters |

| Motors and Drives |

| Intelligent Actuators |

By End-User Industry

| Automotive |

| Food and Beverage |

| Pharmaceutical and Biotech |

| Chemical and Petrochemical |

| Energy and Utilities |

| Metals and Mining |

| Other End-User Industries (Textile, Pulp and Paper, etc.) |

By Deployment Model

| On-premise |

| Cloud-enabled |

| Hybrid Edge-Cloud |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Rest of Europe |

| By Product Type | Distributed Control Systems (DCS) |

| Programmable Logic Controllers (PLC) | |

| Supervisory Control and Data Acquisition (SCADA) | |

| Manufacturing Execution Systems (MES) | |

| Product Lifecycle Management (PLM) | |

| Human Machine Interface (HMI) | |

| Enterprise Resource Planning (ERP) | |

| By Field Device Type | Industrial Robots |

| Machine Vision Systems | |

| Sensors and Transmitters | |

| Motors and Drives | |

| Intelligent Actuators | |

| By End-User Industry | Automotive |

| Food and Beverage | |

| Pharmaceutical and Biotech | |

| Chemical and Petrochemical | |

| Energy and Utilities | |

| Metals and Mining | |

| Other End-User Industries (Textile, Pulp and Paper, etc.) | |

| By Deployment Model | On-premise |

| Cloud-enabled | |

| Hybrid Edge-Cloud | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Germany cloud computing market in 2025?

The Germany cloud computing market size is valued at USD 56.52 billion in 2025.

What is the expected growth rate for German cloud spending through 2031?

Aggregate spending is projected to rise at a 15.51% CAGR to USD 116.22 billion by 2031.

Which deployment model is expanding fastest among German enterprises?

Hybrid cloud leads, advancing at an 18.33% CAGR as companies blend data residency with scalable off-premises compute.

Why is healthcare adoption accelerating?

Telemedicine rollouts, electronic-health-record mandates and AI-enabled diagnostics push healthcare workloads to compliant clouds, driving an 18.56% CAGR.

How does the SAP S/4HANA deadline affect demand?

The 2027 cutoff forces firms to choose cloud-hosted ERP, creating a sizable migration wave that boosts infrastructure and services revenue.

What competitive advantage do sovereign-cloud providers claim?

They highlight BSI C5 certification, client-side encryption and in-country hosting, meeting stringent German data-sovereignty requirements.

Page last updated on: