Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.97 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Probiotics Market Analysis by Mordor Intelligence

The United Kingdom probiotics market size is expected to grow from USD 1.97 billion in 2025 to USD 2.04 billion in 2026 and is forecast to reach USD 2.43 billion by 2031 at 3.59% CAGR over 2026-2031. The market landscape is undergoing substantial transformation as consumer preferences evolve and new regulatory frameworks emerge in the post-Brexit environment. British consumers have demonstrated a notable shift in their understanding and prioritization of gut health compared to 2024. The separation from European Union regulations following Brexit has reshaped the market dynamics, presenting businesses with fresh market opportunities while simultaneously introducing new compliance requirements, particularly in areas such as health claims validation processes and the logistics of importing probiotic ingredients.

Key Report Takeaways

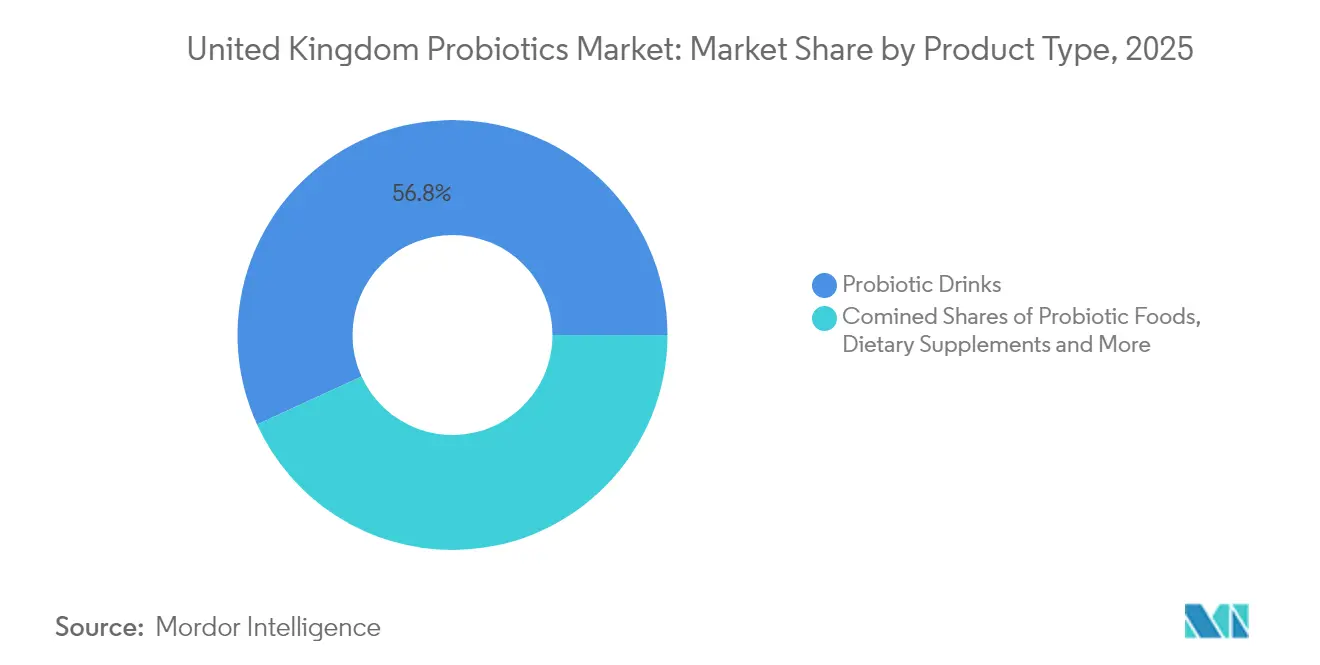

- By product type, probiotic drinks led with 56.83% of the United Kingdom probiotics market share in 2025; animal feed is projected to expand at a 4.31% CAGR through 2031.

- By source, bacterial strains commanded 82.83% share of the United Kingdom probiotics market size in 2025, while yeast-based offerings record the highest 4.63% CAGR to 2031.

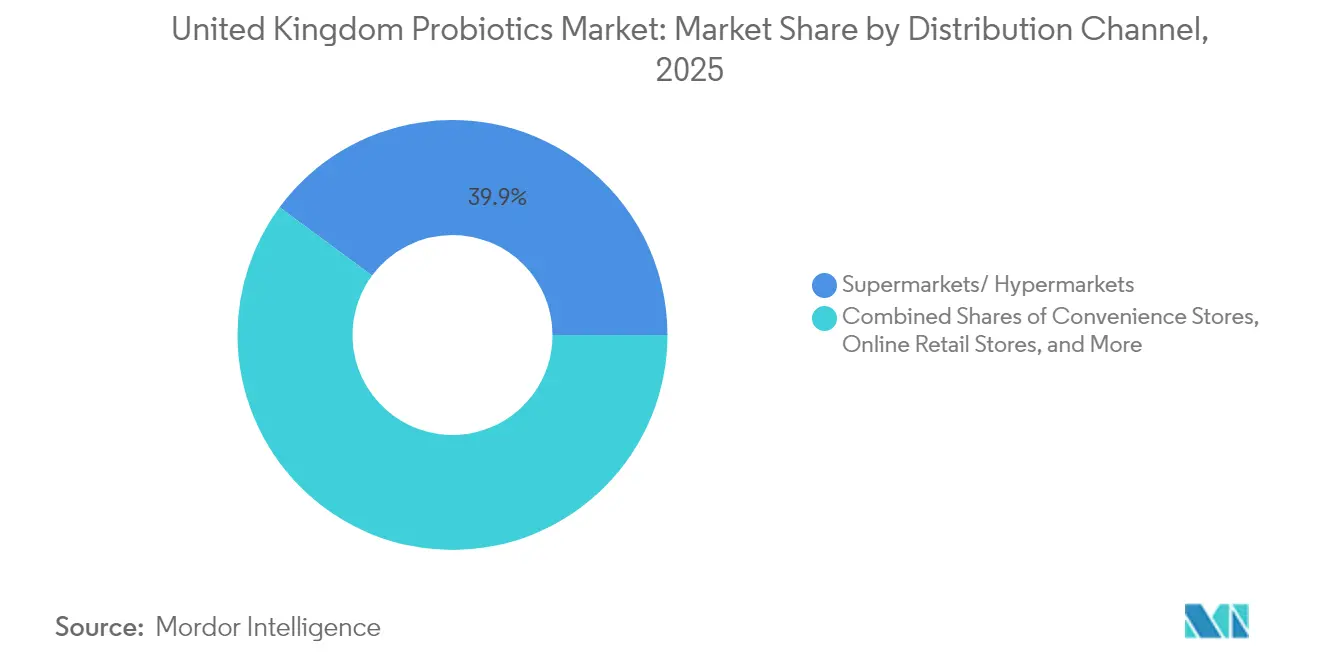

- By distribution channel, supermarkets/ hypermarkets captured 39.88% share in 2025; online retail is advancing at a 4.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Probiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer awareness about gut health and digestive wellness | +1.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| Increasing preference for preventive healthcare and natural supplements | +0.8% | National, higher adoption in affluent demographics | Long term (≥ 4 years) |

| Rising pediatric health focus promoting probiotic products | +0.6% | National, regulatory influence from FSA guidelines | Medium term (2-4 years) |

| Expanding application in animal feed | +0.9% | Rural and agricultural regions | Short term (≤ 2 years) |

| Government initiatives promoting health supplements | +0.4% | National policy implementation | Long term (≥ 4 years) |

| Technological advances improving probiotic strain stability and efficacy | +0.7% | Research hubs including Cambridge, Oxford, London | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Awareness About Gut Health and Digestive Wellness

Rising health awareness has transformed UK consumer priorities, with gut health becoming a central focus for overall wellness improvement. The NHS's 2025 probiotic guidelines confirm specific therapeutic uses while remaining conservative on general health claims. This recognition has expanded consumer acceptance of probiotic products beyond yogurt [1]Source: NHS, “Probiotics,” nhs.uk. Clinical studies demonstrating the effectiveness of probiotics in managing irritable bowel syndrome have established medical validity, with a significant majority of female participants in UK studies experiencing symptom improvement. The British Dietetic Association's 2024 guidelines emphasize the significance of specific probiotic strains, allowing companies with robust clinical research to differentiate their products [2]Source: The Association of UK Dietitians, “Probiotics and gut health,” bda.uk.com. However, consumers face challenges in distinguishing between marketing claims and scientifically validated benefits.

Increasing Preference for Preventive Healthcare and Natural Supplements

The UK government's healthcare strategy focuses on shifting from treatment to prevention, which benefits natural supplement categories, including probiotics. The Department of Health introduced "Making Prevention Everyone's Business" initiative in 2024, which promotes personalized prevention services aligned with probiotic interventions [3]Source: Department of Health & Social Care, “Making prevention everyone’s business: a transformational approach to personalised prevention in England,” gov.uk. Consumer surveys indicate that UK supplement buyers show strong preference for immune support products, with probiotics representing a significant portion of the vitamins, minerals, and supplements market. The TIGRR report recommends reforming nutraceutical regulations, which may expand the probiotics segment currently limited by EU-derived health claims requirements. This regulatory change positions the UK as a potentially more favorable market for innovation compared to the EU, encouraging investment in new probiotic formulations.

Rising Pediatric Health Focus Promoting Probiotic Products

The pediatric probiotic market faces regulatory and clinical evidence challenges that influence its growth potential. The First Steps Nutrition Trust maintains that current evidence does not support routine probiotic addition to infant formula, aligning with UK regulatory standards. Clinical research indicates beneficial applications for specific pediatric conditions, as demonstrated by ongoing trials examining probiotic effects on ADHD behavior and children's sleep patterns. Research at the University of Birmingham, focusing on pregnancy outcomes, has shown improved fetal brain development with Bifidobacterium breve supplementation. The PrePOP study, investigating Lactobacillus crispatus supplementation for preventing preterm birth, may influence future maternal health protocols. The regulatory environment for pediatric probiotics, overseen by the FSA, maintains safety standards while impacting the pace of market development.

Expanding Application in Animal Feed

The animal feed probiotics segment presents significant opportunities due to its well-structured regulatory environment and tangible economic advantages when compared to the complexities of the human consumption market. The UK's Veterinary Medicines Directorate has introduced a comprehensive regulatory modernization initiative in 2024, designed to enhance the country's attractiveness for companies developing veterinary medicines, with a specific focus on probiotic applications. While the feed additive authorization process demands thorough safety documentation, it provides manufacturers with more predictable and navigable paths to market compared to human health applications [4]Source: Food Standards Agency (FSA), “Feed additives authorisation guidance,” food.gov.uk. The industry is experiencing increased momentum as economic pressures on livestock productivity and growing concerns about antimicrobial resistance encourage farmers and producers to adopt probiotic solutions as alternatives to traditional growth promoters. Following Brexit, the UK's independent regulatory framework enables more efficient approval processes compared to EU procedures, creating valuable opportunities for both domestic and international suppliers. However, the industry continues to face operational challenges stemming from its dependence on imported raw materials and potential supply chain vulnerabilities that could affect market stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product shelf-life and storage issues due to probiotic viability | -0.7% | National, particularly affecting smaller retailers | Short term (≤ 2 years) |

| Lack of standardization in probiotic strain efficacy claims | -0.5% | National regulatory oversight | Medium term (2-4 years) |

| Taste and texture issues in some probiotic food products | -0.3% | Consumer preference variations | Short term (≤ 2 years) |

| Dependency on refrigerated supply chains for certain products | -0.4% | National distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Product Shelf-Life and Storage Issues Due to Probiotic Viability

The probiotic industry faces significant challenges in maintaining bacterial viability, which directly affects market expansion potential and increases operational costs across the supply chain. Recent advancements in microencapsulation technologies, incorporating materials such as whey protein, maltodextrin, and plant-based matrices, have shown promising results in extending probiotic survival during storage periods and maintaining FDA-standard viability levels. The development of double-layer microcapsule systems using shellac has further improved protection during both freeze-drying processes and gastrointestinal transit. However, these technological advancements come with increased production costs and operational complexity, creating barriers for smaller manufacturers to enter the market. The situation is further complicated by quality control issues, as highlighted in the UK Government Chemist's analysis of probiotic supplements, which revealed substantial gaps between advertised and actual viable bacteria counts. This discrepancy has created trust issues among consumers. For retailers, especially smaller establishments without sophisticated cold chain capabilities, managing inventory becomes particularly challenging as they attempt to balance product freshness requirements with optimal shelf-life management.

Lack of Standardization in Probiotic Strain Efficacy Claims

The complex and diverse regulatory environment, combined with inconsistent requirements for clinical evidence, creates significant market uncertainty. This uncertainty directly influences both consumer confidence in probiotics and companies' willingness to invest in research and development activities. The Advertising Standards Authority's 2023 decision to classify "probiotic" as a health claim requiring authorization demonstrates the increasing intensity of regulatory oversight [5]Source: Advertising Standards Authority Ltd., “Food: Probiotic claims,” asa.org.uk. While the UK's post-Brexit regulatory independence opens new possibilities for developing country-specific standards, the ongoing dependence on EU-derived regulatory frameworks continues to limit innovation potential in the market. The International Probiotics Association has established best practices guidelines for industry self-regulation, but these guidelines face implementation challenges due to the absence of strong enforcement mechanisms. Scientific research consistently reveals that probiotic effectiveness is highly strain-specific, making it challenging to establish broad product category claims, which in turn affects regulatory approval processes and consumer education initiatives. Companies aiming to expand their presence in international markets face additional challenges due to the absence of standardized global regulations, particularly when trying to maintain consistency in product positioning and validate their claims across different regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drinks Dominate Despite Feed Innovation

The probiotic drinks market has established a commanding position, securing a substantial 56.83% market share in 2025. This dominance stems from years of successful market development and consumer education by industry pioneers such as Yakult and Danone's Actimel brand. These companies have built robust distribution networks and fostered strong consumer trust in their products, creating a solid foundation for the entire segment.

The animal feed segment has emerged as a significant growth opportunity, demonstrating a promising 4.31% CAGR through 2031. This expansion is primarily attributed to the increasing focus on livestock productivity and mounting concerns regarding antimicrobial resistance in agricultural operations. The dietary supplements category maintains its strategic market position by capitalizing on heightened consumer health awareness, despite navigating complex regulatory restrictions on therapeutic claims. In the baby food and infant formula segments, manufacturers face rigorous safety protocols, particularly in the UK market, where regulatory bodies maintain a cautious approach toward probiotic ingredients pending further clinical validation. The industry has witnessed substantial technological progress, particularly in microencapsulation techniques, where innovative double emulsion systems utilizing pea protein and cellulose nanocrystals have demonstrated enhanced probiotic viability across various product applications.

By Source: Bacterial Dominance Faces Yeast Disruption

Bacterial sources dominated the market with an 82.83% share in 2025, reflecting the industry's long-standing commitment to researching and developing Lactobacillus and Bifidobacterium strains. These bacterial strains have consistently demonstrated their safety profiles and clinical effectiveness through numerous scientific studies and real-world applications. The yeast-based probiotics segment is projected to grow at a 4.63% CAGR through 2031, as manufacturers recognize the significant advantages of yeast strains in addressing the stability limitations commonly associated with bacterial probiotics.

Within the yeast segment, Saccharomyces boulardii has emerged as the primary growth driver, particularly in clinical environments where it proves effective in preventing antibiotic-associated diarrhea and managing various gastrointestinal disorders. The industry is also witnessing the emergence of innovative probiotic species, such as Akkermansia muciniphila, which represent the next frontier in probiotic development. These novel strains are gaining traction as FSA safety validations confirm their suitability for food supplement applications, opening new possibilities beyond traditional bacterial and yeast categories.

By Distribution Channel: Supermarkets Lead Despite Online Acceleration

Supermarkets and hypermarkets dominate the distribution landscape with a substantial 39.88% market share in 2025. This dominance stems from their ability to capitalize on well-established consumer shopping patterns and create numerous opportunities for impulse purchases. The traditional retail environment continues to serve as a primary destination for consumers seeking probiotic products alongside their regular shopping needs.

Online retail stores are projected to experience robust growth at a 4.74% CAGR through 2031, fueled by the widespread adoption of e-commerce platforms and increased direct-to-consumer initiatives from probiotic manufacturers. Pharmacies and health stores maintain their position as trusted intermediaries between mainstream retail and specialized distribution channels, leveraging healthcare professional recommendations and consumer trust in medical retail environments. The imminent launch of Tesco's "Gut Sense" private label in 2025 demonstrates the growing recognition of market potential by major retailers, which could reshape existing brand preferences through strategic pricing and optimal shelf positioning.

Geography Analysis

The United Kingdom probiotics market demonstrates robust growth potential, supported by its densely populated regions and consumers with substantial disposable income who actively seek premium health products. This market environment has created favorable conditions for both established and emerging probiotic brands. However, the post-Brexit landscape has introduced significant regulatory complexities that impact domestic manufacturers and international suppliers alike. Consumer education initiatives spearheaded by innovative companies like Zoe and established market players such as Yakult have successfully cultivated a sophisticated understanding of probiotics among UK consumers, with a notable majority reporting heightened awareness of gut health compared to 2024. The regulatory oversight provided by FSA and MHRA maintains rigorous standards for health claims validation, while potentially offering more room for innovation compared to the centralized EU systems.

Brexit's influence extends deeply into operational aspects, particularly affecting the supply chain logistics for probiotic products that require precise temperature control. The implementation of new import procedures has created additional layers of complexity and increased operational costs for international suppliers, necessitating strategic adaptations in distribution networks and inventory management systems. These challenges have prompted companies to reevaluate their supply chain strategies and invest in more robust cold chain infrastructure to maintain product integrity.

The UK market exhibits distinct regional characteristics shaped by demographic and economic factors. Major urban centers, including London, Manchester, and Edinburgh, showcase higher adoption rates for premium probiotic products, driven by health-conscious urban populations with greater spending power. In contrast, rural areas display growing interest in agricultural applications of probiotics, particularly in animal feed, as farmers seek to optimize livestock productivity and health outcomes. The presence of Scotland's independent regulatory body, Food Standards Scotland, introduces additional compliance considerations for companies operating across multiple UK regions. The country's strong research foundation, anchored by institutions like the Quadram Institute and prestigious university partnerships in Cambridge, Oxford, and London, positions the UK as an emerging hub for innovative probiotic development and scientific advancement.

Competitive Landscape

The UK probiotics market presents a balanced competitive landscape with a concentration score of 6 out of 10, indicating a market where established companies maintain significant influence while new entrants can still make their mark through innovative approaches. Traditional market leaders have built their positions through substantial investments in educating consumers about probiotic benefits and developing robust distribution channels across retail networks. However, the market dynamics are shifting as digitally native brands enter the space, bringing fresh perspectives on consumer engagement through online platforms and offering more personalized health solutions. This evolution is exemplified by Müller's strategic acquisition of Biotiful Gut Health for over GBP 100 million in April 2025, strengthening the company’s presence in the United Kingdom dairy market while demonstrating how established companies are adapting to changing market conditions.

The technological landscape within the probiotics market continues to evolve, with companies making significant strides in research and development. Organizations investing in advanced technologies such as microencapsulation and strain stability solutions are gaining competitive advantages. These innovations are protected through strategic patent filings, particularly in delivery system technologies, creating substantial barriers to entry for new market participants. The market presents notable opportunities in specialized segments, including pediatric applications, advanced probiotic strains, and personalized microbiome solutions. These opportunities have attracted attention from private equity firms, as demonstrated by Maven Capital Partners' investment in Covestus, the parent company of Probio7, highlighting the financial sector's confidence in the market's growth potential.

The regulatory environment, under the oversight of FSA and MHRA, plays a crucial role in shaping market competition. Companies with established regulatory compliance processes and comprehensive clinical evidence portfolios maintain a significant advantage over newer entrants. While emerging companies are making inroads through direct-to-consumer channels and personalized health offerings, they face considerable challenges in scaling their operations to compete with the established distribution networks and strong brand recognition of incumbent players. This regulatory framework, combined with the need for substantial clinical validation, creates a complex operating environment that rewards companies with robust operational capabilities and long-term market commitment.

United Kingdom Probiotics Industry Leaders

Danone SA

Yakult Honsha Co., Ltd.

Nestlé SA

OptiBac Probiotics Ltd.

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Müller acquired Biotiful Gut Health, the UK's leading kefir brand, for over GBP 100 million, marking the German dairy giant's strategic entry into the functional beverage market. This acquisition positions Müller to leverage Biotiful's fastest-growing brand status in the UK dairy sector during 2024 and expands its health and nutrition portfolio significantly

- March 2025: Hip Pop expanded its UK retail presence by launching in Morrisons and enlarging its Ocado range. The probiotic, gut-friendly drinks offer lower-calorie alternatives with fiber and live cultures, reflecting the rising demand for functional beverages. New packaging design enhances shelf appeal.

- April 2025: YourBiology launched a premium probiotic supplement designed specifically for women over 50. It supports digestion, immune health, hormonal balance, and skin hydration with 10 scientifically-backed strains delivering 20 billion CFUs. The formula addresses menopausal symptoms and promotes overall vitality.

United Kingdom Probiotics Market Report Scope

Probiotics are live microorganisms that are intended to have health benefits when consumed. These microorganisms are incorporated into food and beverages to enhance the nutrition profile of the final product. The probiotics market in the United Kingdom is segmented into functional food and beverages, dietary supplements, and animal feed. The market is segmented into distribution channels: supermarkets/hypermarkets, health stores/pharmacies, online retail stores, and other distribution channels. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Probiotic Foods | Yogurt |

| Bakery/Breakfast Cereals | |

| Baby Food and Infant Formula | |

| Other Probiotic Foods | |

| Probiotic Drinks | Fruit-based Probiotic Drinks |

| Dairy-based Probiotic Drinks | |

| Dietary Supplements | |

| Animal Feeds/Foods |

By Source

| Bacteria |

| Yeast |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Pharmacies and Health Stores |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Probiotic Foods | Yogurt |

| Bakery/Breakfast Cereals | ||

| Baby Food and Infant Formula | ||

| Other Probiotic Foods | ||

| Probiotic Drinks | Fruit-based Probiotic Drinks | |

| Dairy-based Probiotic Drinks | ||

| Dietary Supplements | ||

| Animal Feeds/Foods | ||

| By Source | Bacteria | |

| Yeast | ||

| By Distribution Channel | Supermarkets/ Hypermarkets | |

| Pharmacies and Health Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What growth rate is forecast for probiotics sales in the UK to 2031?

Sales are projected to rise at a 3.59% CAGR, moving from USD 2.04 billion in 2026 to USD 2.43 billion by 2031.

Which product format currently generates the most revenue?

Probiotic drinks lead with 56.83% of 2025 value because of entrenched yogurt-shot and kefir consumption.

Why are yeast-based probiotics gaining attention?

Yeasts such as Saccharomyces boulardii tolerate heat and acidity, cutting cold-chain costs and enabling ambient formats, which is driving a 4.63% CAGR for the sub-segment.

What role do animal-feed probiotics play in overall market expansion?

Livestock productivity gains and antibiotic-reduction mandates fuel a 4.31% CAGR for feed additives, providing a complementary B2B growth pillar alongside human consumption.

What is the biggest regulatory hurdle for new probiotic products?

Strain-specific health-claim authorization remains the toughest barrier, as the Advertising Standards Authority treats even the term “probiotic” as a claim requiring substantiation.

Page last updated on: