Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

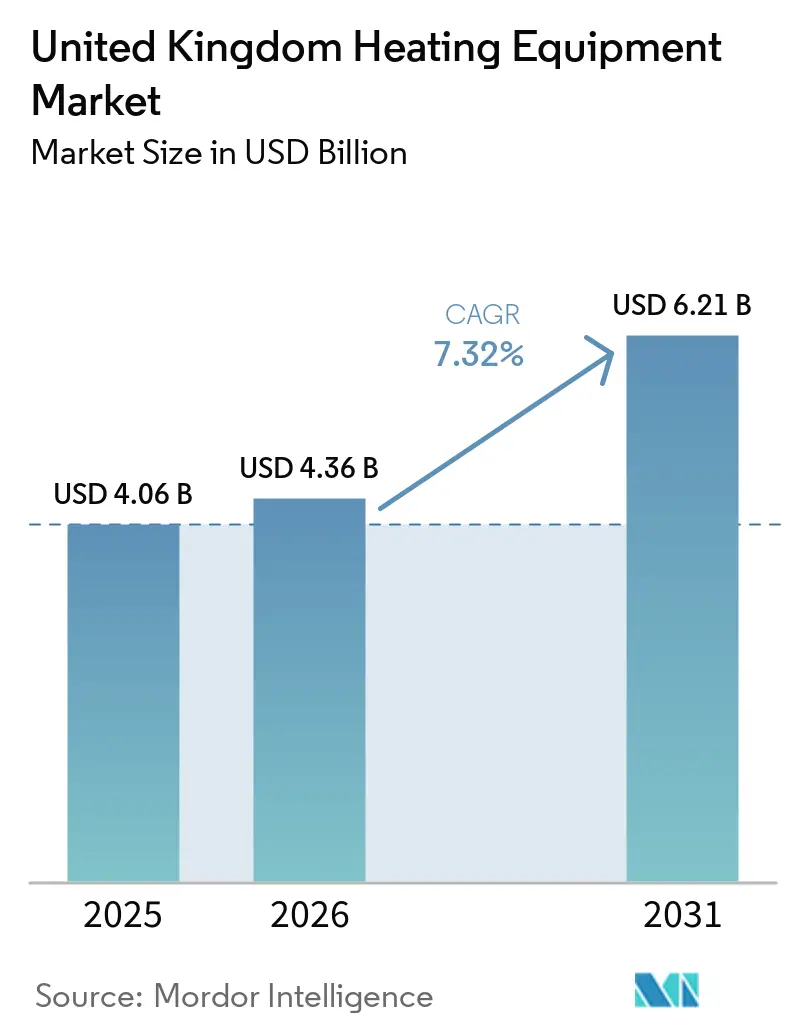

| Base Year Market Size (2025) | USD 4.06 Billion |

| Market Size (2026) | USD 4.36 Billion |

| Market Size (2031) | USD 6.21 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Heating Equipment Market Analysis by Mordor Intelligence

The United Kingdom heating equipment market size is expected to grow from USD 4.06 billion in 2025 to USD 4.36 billion in 2026 and is forecast to reach USD 6.21 billion by 2031 at 7.32% CAGR over 2026-2031. Robust policy incentives, a structurally old housing stock, and rapid heat-pump innovation collectively propel demand as households and businesses pivot away from fossil-fuel boilers. Scotland’s accelerated Net Zero timeline, coupled with an 88% year-on-year jump in Boiler Upgrade Scheme applications, illustrates how regulation converts into measurable purchasing activity. Hybrid systems that pair gas boilers with air-source pumps emerge as transitional solutions, while bundled finance packages reduce upfront costs and widen addressable demographics. Digital connectivity further enriches value propositions by enabling remote monitoring, predictive maintenance, and AI-driven optimization.

Key Report Takeaways

- By equipment type, gas boilers held 37.65% of the United Kingdom heating equipment market share in 2025, whereas heat pumps are projected to expand at an 11.24% CAGR to 2031.

- By installation type, replacements dominated with 70.65% revenue share in 2025, while new installations record the fastest growth at an 7.95% CAGR.

- By end-user, the residential segment led with a 58.41% share of the United Kingdom heating equipment market size in 2025 and is progressing at a 7.52% CAGR to 2031.

- By fuel type, natural gas commanded 65.78% of the United Kingdom heating equipment market size in 2025; electricity-based systems are expanding at an 8.55% CAGR.

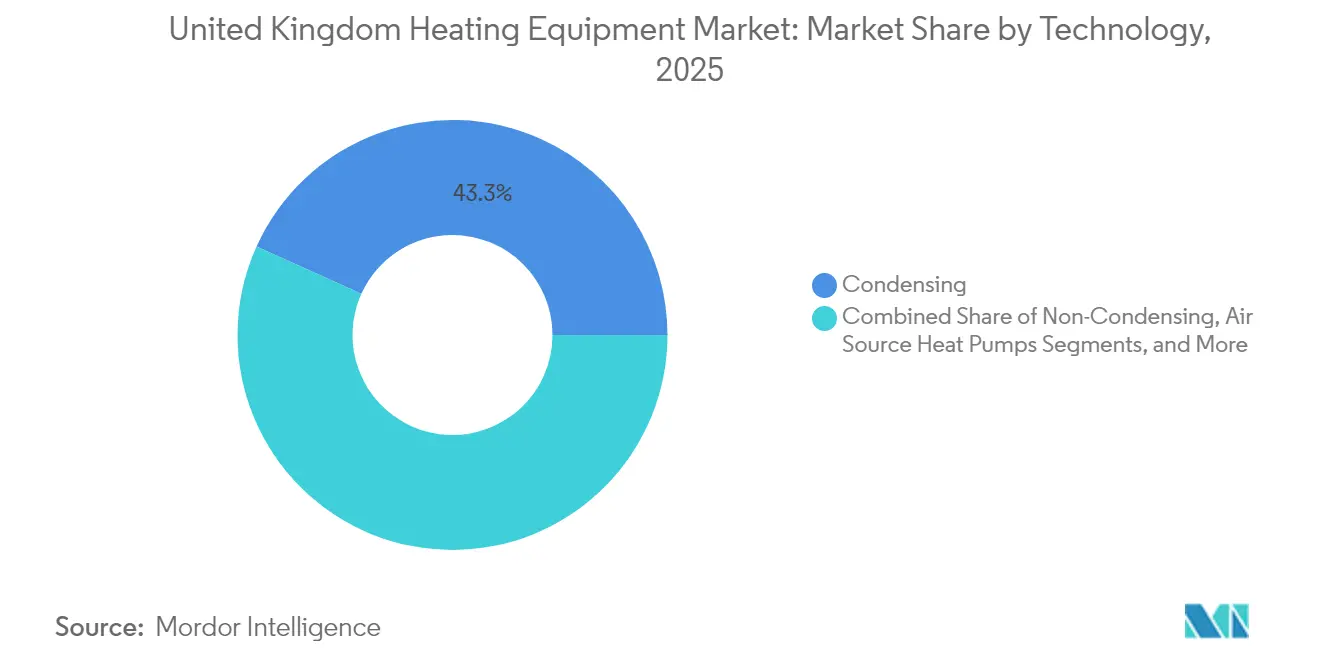

- By technology, condensing systems commanded 43.25% of the market in 2025, and air-source heat pumps are set to achieve the highest 8.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Heating Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive government decarbonisation policies and incentives | +2.1% | National, strongest in Scotland and Wales | Medium term (2-4 years) |

| Ageing boiler stock triggering replacement demand | +1.8% | National, highest in England | Short term (≤ 2 years) |

| Efficiency-boosting technology innovations | +1.4% | National, early adoption in cities | Long term (≥ 4 years) |

| Green-home finance products accelerating upgrades | +1.2% | National, higher-income regions | Medium term (2-4 years) |

| Urban district-heat network expansion | +0.9% | Major English and Scottish cities | Long term (≥ 4 years) |

| Emergence of heat-as-a-service subscription models | +0.6% | Pilot programs in large cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive Government Decarbonisation Policies and Incentives

Expanded grants, technology-neutral eligibility, and flexible leasing options are reshaping purchasing behavior across the United Kingdom heating equipment market. The Department for Energy Security and Net Zero’s consultation to widen the Boiler Upgrade Scheme now covers air-to-air units and heat batteries, aligning financial support with diverse property profiles.[1]Scottish Construction Now, “UK government plans to expand its Boiler Upgrade Scheme,” scottishconstructionnow.com Coupled with a pledge to train 18,000 additional retrofit installers, the policy mix addresses both demand creation and supply-side capacity. March 2025 applications surged 88% year on year, signaling effective stimulus. Scotland’s earlier 2045 Net Zero deadline amplifies local uptake, positioning policy as the single most powerful demand accelerator.

Ageing Boiler Stock Triggering Replacement Demand

More than 80% of U.K. homes were built before 1960, and many gas boilers installed during the 1990s now near end-of-life . This aging stock secures a baseline of predictable replacement volumes, driving 71.21% of current sales. Manufacturers exploit the cycle by offering hybrid packages that couple familiar gas units with add-on heat pumps compatible with existing pipework. As building codes tighten, each end-of-life event becomes an inflection point where owners weigh carbon and efficiency gains, sustaining both volume stability and technology upgrading within the United Kingdom heating equipment market.

Efficiency-Boosting Technology Innovations

Next-generation refrigerants and higher flow-temperature heat pumps unlock properties once deemed unsuitable. Vaillant’s R290 units supply 75 °C water at −15 °C ambient, enabling direct swaps for legacy radiators.[2]Vaillant Group, “Vaillant at the ISH 2025,” vaillant-group.com Quiet-Mark certification mitigates noise concerns in dense housing, while AI-enabled remote diagnostics optimize cycling rates to cut running costs. Collectively, these advances lower total cost of ownership and widen addressable segments, adding 1.4% to forecast CAGR across the United Kingdom heating equipment market.

Green-Home Finance Products Accelerating Upgrades

Bundled tariffs, zero-interest loans, and service subscriptions neutralize high upfront costs. Ideal Heating’s partnership with EDF delivers a 7-year servicing package plus low-carbon electricity windows that save households at least USD 404 over standard tariffs.[3]Ideal Heating, “Ideal Heating and EDF partner up to launch innovative heat pump bundle,” idealheating.com The shift from hardware purchase to managed service diminishes payback anxiety. As lenders mainstream green-mortgage products, retrofit economics improve for mid-income owners, further lifting demand momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of low-carbon heating systems | -1.9% | National, steeper in lower-income areas | Short term (≤ 2 years) |

| Skilled labour shortage for advanced installations | -1.3% | National, acute in rural zones | Medium term (2-4 years) |

| Rural grid-capacity constraints | -0.8% | Rural England, Scottish Highlands, Wales | Long term (≥ 4 years) |

| Hydrogen-infrastructure uncertainty | -0.6% | Pilot regions nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Low-Carbon Heating Systems

University of Edinburgh research found that average installed heat-pump prices have stagnated for a decade, leaving households with net costs of USD 6,500-14,000 even after grants. Properties needing electrical upgrades or radiator swaps see higher totals, deterring many until outright boiler failure. The economic barrier explains why replacement outpaces proactive retrofits despite policy support, curbing near-term acceleration of the United Kingdom heating equipment market.

Skilled Labour Shortage for Advanced Installations

The Heat Pump Association calculates that an extra 27,000 installers are required by 2028, yet current training throughput remains well below target.[4]Heat Pump Association, “New report reveals scale of skills challenge facing heat pump industry,” heatpumps.org.uk MCS-accredited engineers cluster in cities, leaving rural customers with long wait times and elevated quotes. Small-scale apprenticeship programs from Daikin and others are positive but insufficient. Limited capacity risks quality shortfalls that could erode consumer confidence and temper growth of the United Kingdom heating equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Heat Pumps Challenge Boiler Dominance

Heat pumps are expanding at an 11.24% CAGR, steadily eroding the 37.65% share currently held by gas boilers. The United Kingdom heating equipment market size for heat pumps is set to widen as government rebates and high-temperature models enable retrofits without full radiator replacement. strengthening growth in the United Kingdom heat pumps market. Gas boilers persist due to lower capital outlay and installer familiarity, but forthcoming efficiency mandates tighten margins. Hybrid offerings combine both technologies, granting manufacturers a hedging strategy that balances present sales with future readiness. Furnaces and ancillary radiators maintain niche roles in industrial and large-commercial settings, providing steady though limited demand.

Gas-fired incumbents seek relevance through hydrogen-ready prototypes, exemplified by Worcester Bosch units certified for 20% hydrogen blends. Meanwhile, heat-pump specialists leverage private-equity backing to scale domestic capacity, signaling confidence in the long-term electrification trajectory of the United Kingdom heating equipment market.

By End-User Industry: Residential Dominates Value Creation

The residential sector owned 58.41% revenue share in 2025 and is projected to expand at a 7.52% CAGR to 2031, reflecting both the sheer number of households and an aging installed base. Energy-efficiency rules for new builds are pushing developers toward low-carbon options from day one, while homeowners take advantage of grants when they replace legacy boilers. In commercial real estate, ESG commitments spur retrofits in offices, retail outlets, and hospitality venues, although project complexity can elongate decision cycles, moderating immediate growth rates across the United Kingdom heating equipment market.

Residential demand has become a proving ground for technology innovation. Heat Geek’s portfolio of optimized residential heat-pump systems reportedly achieves 50% better seasonal performance than typical U.K. installations. The public-sector subsegment-schools, hospitals, and council buildings-leans on framework agreements to procure low-carbon equipment at scale and share maintenance expertise. Industrial users prioritize furnace technologies that can integrate with process heat requirements, whereas data centers increasingly evaluate liquid-cooling heat recovery, hinting at future adjacency opportunities within the United Kingdom heating equipment market.

By Fuel Type: Gas Still Leads, Electricity Gains Ground

Natural-gas appliances retained 65.78% share of the United Kingdom heating equipment market in 2025, a figure supported by an extensive pipeline network and decades of embedded know-how. Still, electricity-powered systems post the most robust 8.55% CAGR, buoyed by falling renewable power costs and grid-greenification targets. Oil boilers fill gaps in remote off-grid communities, though their footprint is shrinking as storage requirements and emissions concerns grow.

Electricity’s advance is underpinned by widespread digital meters that facilitate time-of-use tariffs bundled with heat-pump deals, shrinking operating expenses relative to gas. Manufacturers hedge against uncertainty by offering hydrogen-blend-capable models to extend the lifespan of gas infrastructure during the transition. Biomass systems, while niche, attract eco-conscious users seeking fuel autonomy. The United Kingdom heating equipment market therefore shows a layered fuel mix that gradually tilts toward electrons without abruptly stranding legacy assets.

By Technology: Condensing Systems Remain the Benchmark

Condensing systems accounted for 43.25% of 2025 revenues and serve as the minimum legal standard for new and replacement gas installations, ensuring baseline efficiency in the United Kingdom heating equipment market. Air-source heat pumps exhibit an 8.12% CAGR, supported by R290 refrigerants that deliver high flow temperatures suitable for radiator circuits. Ground-source solutions enjoy a smaller but steady niche, particularly in new-build communities with shared loop arrays promoted by local planning authorities.

The technology landscape is rapidly digitizing. Vaillant’s iQconnect platform enables predictive fault detection, remote parameter tuning, and energy-tariff integration. Hybrid heat-pump-plus-boiler packages are gaining attention as a bridging solution for colder regions, reducing carbon intensity without fully abandoning gas. Noise-attenuation advances attract apartment dwellers who previously faced planning restrictions. Each incremental improvement broadens the customer pool and enriches service revenues, reinforcing innovation as a durable driver in the United Kingdom heating equipment market.

By Installation Type: Replacement Anchors Near-Term Demand

Replacement projects represented 70.65% of equipment sales in 2025, underlining how the aging boiler inventory dictates baseline volume. These jobs are often time-sensitive because broken boilers require immediate attention, leading installers to recommend off-the-shelf condensing units or compatible hybrids rather than wait for grid upgrades. Nevertheless, new installations are climbing at an 7.95% CAGR, propelled by housing starts, non-residential construction, and district-heating expansions clustering in major cities.

For many households, replacement is the decisive moment to switch fuels thanks to the USD 7,500 Boiler Upgrade Scheme grant and flexible leasing contracts. New-build developers, conversely, select low-carbon options upfront to comply with Future Homes Standard requirements. These dual channels ensure a reliable demand cadence, balancing steady replacement work with fresh growth venues. The combined effect secures a resilient revenue backbone for participants in the United Kingdom heating equipment market.

Geography Analysis

England absorbed the lion’s share of 2024 revenues, enabled by dense housing, mature supply chains, and strong manufacturer presence. Urban centers like Sheffield illustrate the scale of opportunity; E.ON’s project will double the district-heating network from 5 miles to 11 miles, shifting thousands of apartments toward centralized low-carbon heat. London boroughs integrate low-temperature networks with waste-heat recovery, reinforcing the push toward electrification. Rural English districts, however, wrestle with grid-capacity shortfalls and longer service lead times, slowing adoption of all-electric systems in sparsely populated zones.

Scotland accounted for 13.88% of sales in 2025 but leads growth at an 7.85% CAGR because of its more ambitious 2045 net-zero statutory target. Edinburgh’s Heat Network Partnership funds municipal infrastructure, while Highlands councils subsidize off-gas-grid heat-pump installations. Private investment supports the trend; Kensa’s USD 70 million injection aims to deliver networked ground-source systems to new residential developments. Abundant wind and hydro generation supply low-carbon electricity, creating a favorable operating environment for heat pumps and confirming Scotland as a growth spearhead in the United Kingdom heating equipment market.

Wales and Northern Ireland represent smaller slices yet exhibit distinct patterns. Welsh authorities mirror U.K. national policy but place extra emphasis on remedial insulation for older housing, thus sequencing fabric upgrades before equipment swaps. Northern Ireland operates a separate gas network and regulatory structure, leading to divergent uptake rates. Its oil-to-gas conversion programs linger, particularly where grant funding offsets tank removal. Installer scarcity remains acute in remote valleys and border counties, though local colleges are scaling vocational courses. Geographic diversity therefore requires manufacturers to tailor value propositions by region, embedding flexibility at the heart of the United Kingdom heating equipment market strategy.

Competitive Landscape

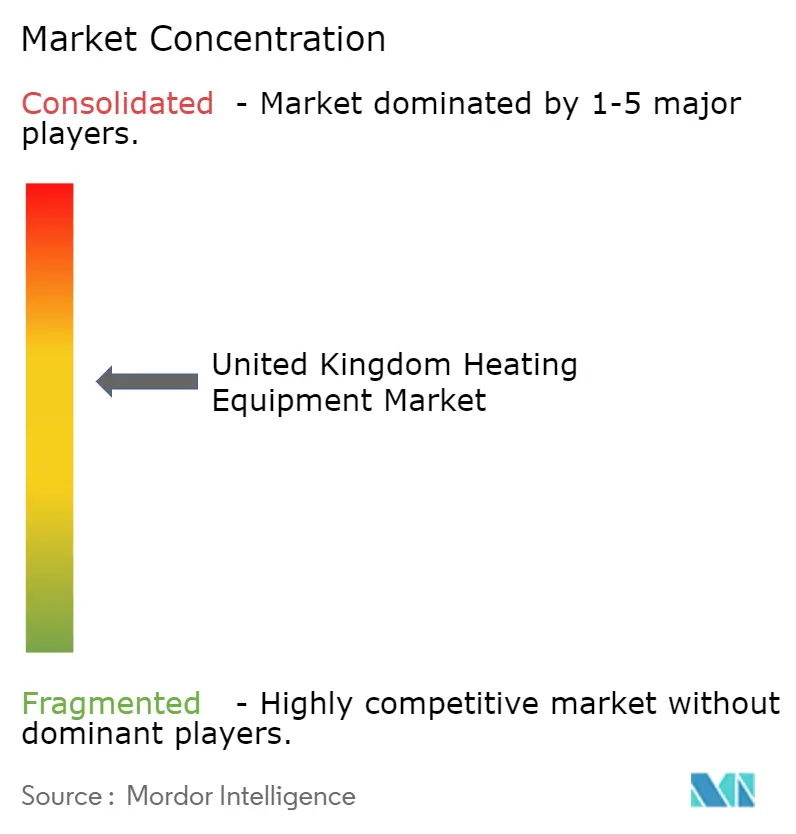

The competitive field is moderately fragmented, with the top five firms controlling roughly 40–50% of turnover. Worcester Bosch, Vaillant, Ideal Boilers, and Baxi leverage established installer networks and multi-fuel portfolios to defend share. Worcester Bosch’s early move into hydrogen-blend-ready units illustrates how incumbents protect the gas franchise while probing future fuels. Vaillant’s R290 heat-pump line and iQconnect digital services show parallel investment in electrification, signaling convergence toward integrated solutions.

Strategic partnerships blur traditional boundaries between hardware, software, and energy retail. Centrica’s alliance with Daikin embeds heat pumps into the Hive smart-home ecosystem, giving consumers a single interface for thermostat control, energy use tracking, and utility billing. Service-focused disruptors such as Heat Geek prioritize installer training and performance guarantees rather than manufacturing, elevating quality benchmarks and influencing buyer expectations. Meanwhile, institutional buyers favor turnkey offers from conglomerates like Johnson Controls, which report 53% cost savings after replacing gas boilers across 60 Hounslow Council buildings.

Capital inflows target scale-up prospects. Kensa’s financing round supports ground-source networks, and Lennox’s launch of an ultra-cold-climate heat pump underscores trans-Atlantic technology competition. Local distribution networks also consolidate, with merchants such as City Plumbing joining the Heat Pump Association to deepen technical know-how and secure supply. As regulation tightens and economies of scale matter more, merger activity is expected to rise, although regional installer relationships will continue to shape market access in the United Kingdom heating equipment market.

United Kingdom Heating Equipment Industry Leaders

Aermec SpA

Finn Geotherm UK Limited

Trane Inc.

Mitsubishi Electric Europe BV (Mitsubishi Electric Corporation)

Clivet SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Johnson Controls disclosed that replacing gas boilers with air-source heat pumps in 60 Hounslow Council properties cut heating bills by 53% and carbon emissions by 60%.

- May 2025: The Department for Energy Security and Net Zero issued a consultation on expanding the Boiler Upgrade Scheme to include air-to-air heat pumps, heat batteries, and flexible leasing, plus USD 4 million for supply-chain scaling in Copeland.

- April 2025: The government confirmed Scheme expansion after March applications surged to 4,028, marking an 88% year-on-year jump.

- March 2025: Lennox introduced a cold-climate heat pump engineered for extreme temperatures.. Vaillant unveiled aroTHERM perform 15- and 20-kW models suitable for existing radiators, alongside iQconnect digital services.

United Kingdom Heating Equipment Market Report Scope

The market study analyses the market trends and opportunities for different types of heating equipment, such as Boilers, Heat pumps, and others used in the various end-user industry applications like residential, commercial, and industrial. The study analyzes the impact of COVID-19 on the market players and its stakeholders across the supply chain. Further, the disruption factors impacting the market's growth in the near future have been covered in the study regarding drivers and restraints.

By Equipment Type

| Boilers |

| Furnaces |

| Heat Pumps |

| Radiators and Other Heater Types |

By End-User Industry

| Residential |

| Commercial |

| Industrial |

| Public/Institutional |

By Fuel Type

| Natural Gas |

| Electricity |

| Oil |

| Biomass |

| Hydrogen-Ready |

By Technology

| Condensing |

| Non-Condensing |

| Air Source Heat Pumps |

| Ground Source Heat Pumps |

| Hybrid Systems |

| Smart Connected Systems |

By Installation Type

| New Installation |

| Replacement/Retrofit |

| By Equipment Type | Boilers |

| Furnaces | |

| Heat Pumps | |

| Radiators and Other Heater Types | |

| By End-User Industry | Residential |

| Commercial | |

| Industrial | |

| Public/Institutional | |

| By Fuel Type | Natural Gas |

| Electricity | |

| Oil | |

| Biomass | |

| Hydrogen-Ready | |

| By Technology | Condensing |

| Non-Condensing | |

| Air Source Heat Pumps | |

| Ground Source Heat Pumps | |

| Hybrid Systems | |

| Smart Connected Systems | |

| By Installation Type | New Installation |

| Replacement/Retrofit |

Key Questions Answered in the Report

How big is the United Kingdom heating equipment market in 2026?

The market values at USD 4.36 billion in 2026 and is expected to reach USD 6.21 billion by 2031.

Which technology is expanding fastest?

Heat pumps lead growth with an 11.24% CAGR through 2031 because of grants, high-temperature refrigerants, and bundled tariffs.

What proportion of current sales are replacements?

Replacement jobs make up 70.65% of total installations due to an aging boiler base.

Why is Scotland growing faster than other regions?

Scotland's 2045 net-zero deadline, generous subsidies, and substantial renewable electricity supply drive an 7.85% CAGR.

What remains the biggest adoption hurdle for heat pumps?

High upfront costs persist, leaving households to fund USD 6,500-14,000 after grants, especially when electrical upgrades are required.

Are enough trained installers available to meet demand?

No, the sector needs about 27,000 more installers by 2028, and the shortage could slow market expansion.

Page last updated on: