Market Overview

| Study Period | 2020 - 2031 |

|---|---|

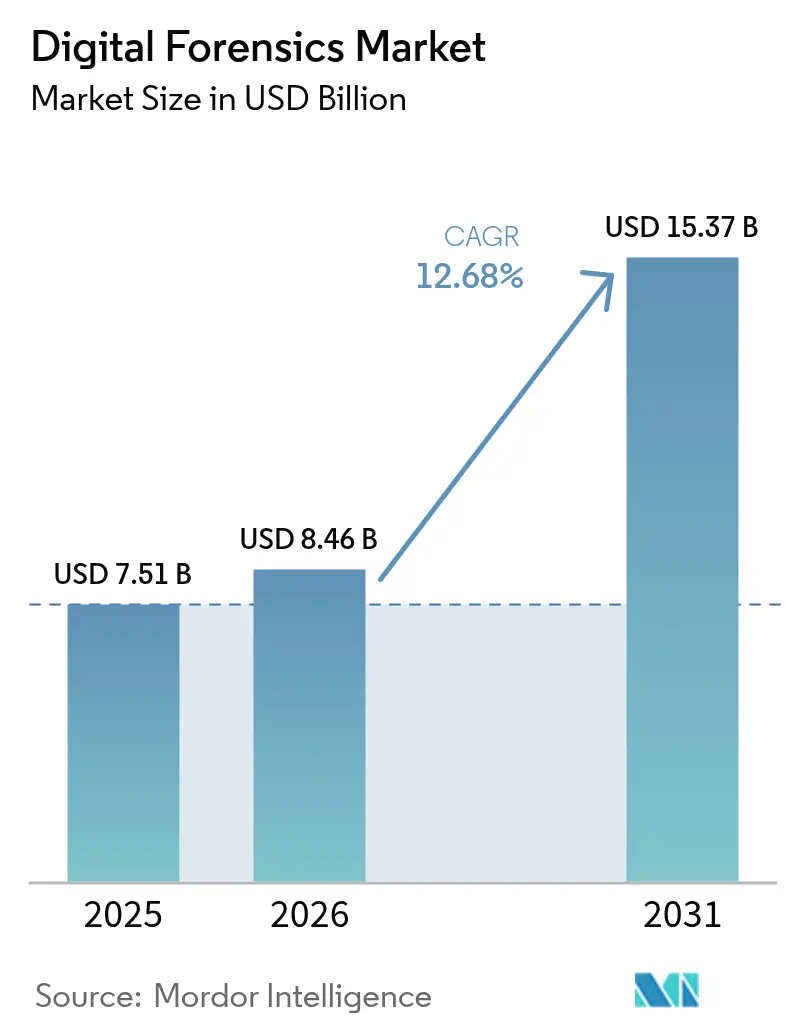

| Market Size (2026) | USD 8.46 Billion |

| Market Size (2031) | USD 15.37 Billion |

| Growth Rate (2026 - 2031) | 12.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Forensics Market Analysis by Mordor Intelligence

The digital forensics market size is projected to expand from USD 7.51 billion in 2025 and USD 8.46 billion in 2026 to USD 15.37 billion by 2031, registering a 12.68% CAGR between 2026 and 2031. Heightened migration to multi-cloud architectures, deepfake-enabled fraud, and ransomware targeting SaaS tenants are pushing enterprises to embed forensic readiness at every security layer. The digital forensics market is also benefiting from regulations that shorten breach-notification timelines, driving demand for tooling that can capture, preserve, and analyze evidence at speed. Software continues to hold the largest share of components, yet managed services are gaining traction as organizations shift away from one-time tool purchases toward outcome-based retainers. Vendors that integrate forensic data-lake connectors into extended detection and response (XDR) platforms are capturing incremental share, while cloud-native offerings are closing gaps involving container logs, serverless artifacts, and volatile memory images.

Key Report Takeaways

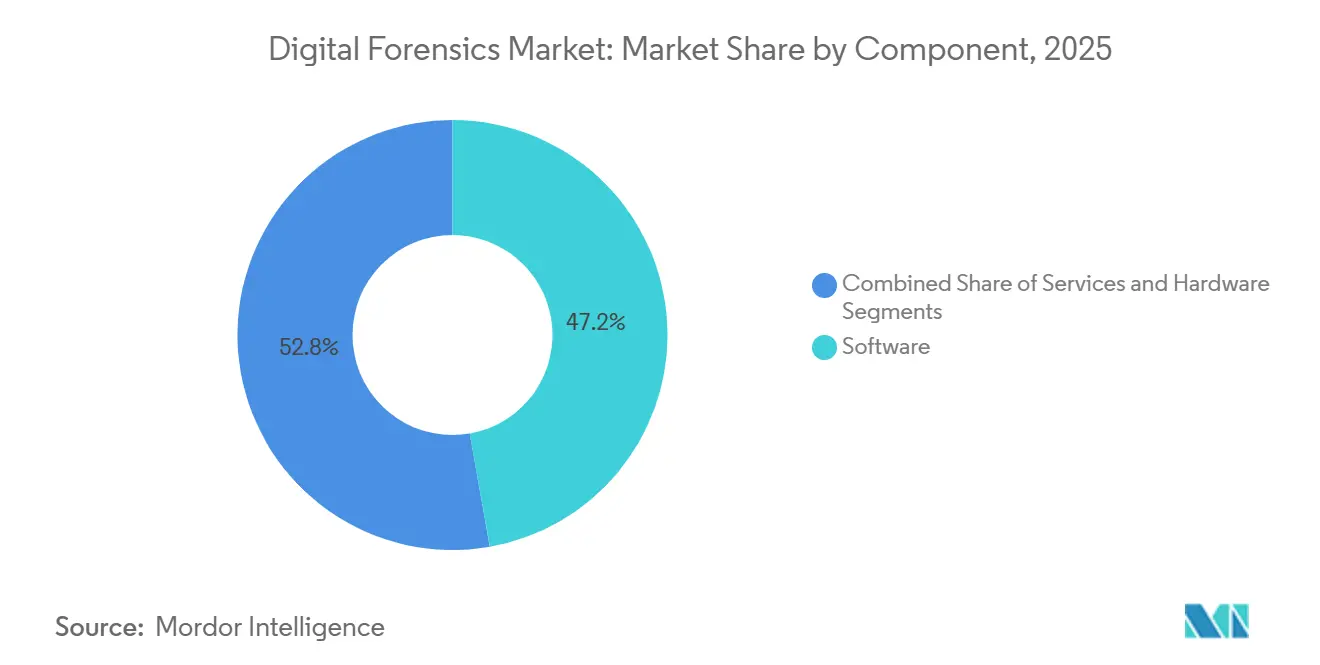

- By component, software led with 47.23% of the digital forensics market share in 2025, while services are advancing at a 13.27% CAGR through 2031.

- By type, computer forensics accounted for 32.44% of the digital forensics market size in 2025, whereas cloud forensics is projected to grow at the fastest 13.84% CAGR to 2031.

- By tool, data acquisition and preservation dominated the digital forensics market with a 28.93% share of the market size in 2025, but forensic decryption and password cracking will expand at a 13.63% CAGR through 2031.

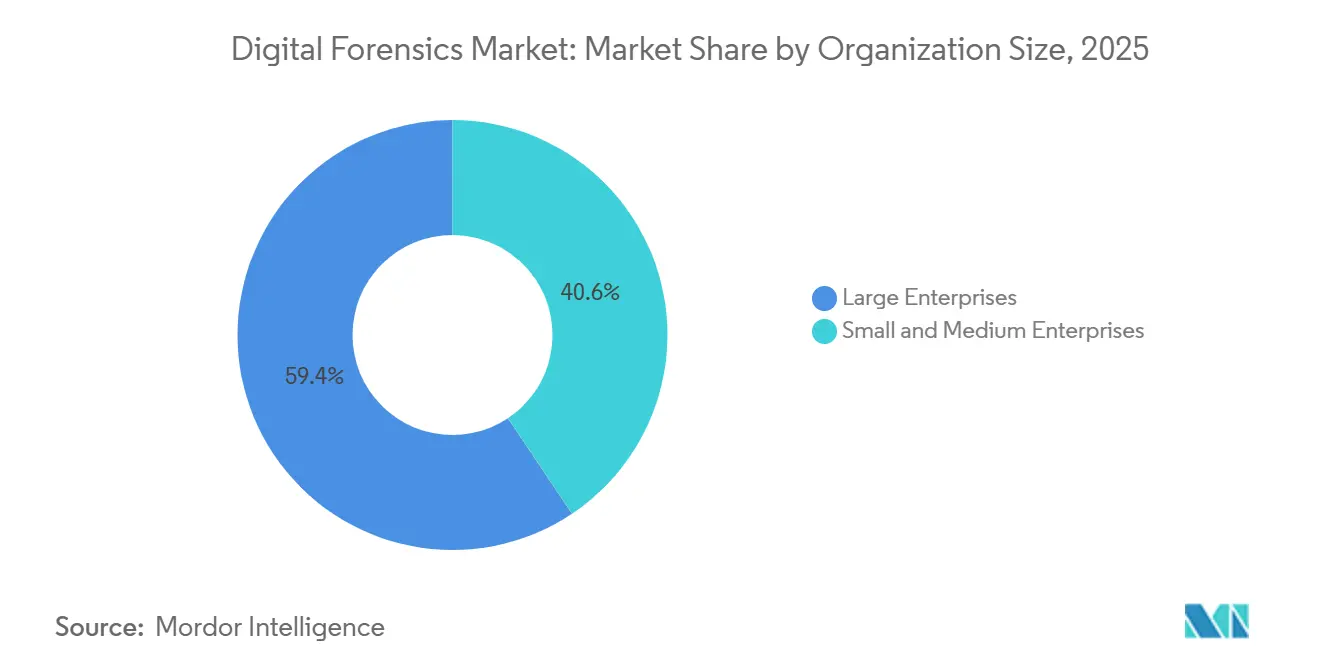

- By organization size, large enterprises held 59.37% of the digital forensics market share in 2025, yet small and medium enterprises exhibit the highest 13.06% CAGR through 2031.

- By end-user vertical, government and law enforcement agencies led with a 36.83% revenue share in 2025, while healthcare is the fastest-growing segment at a 14.63% CAGR to 2031.

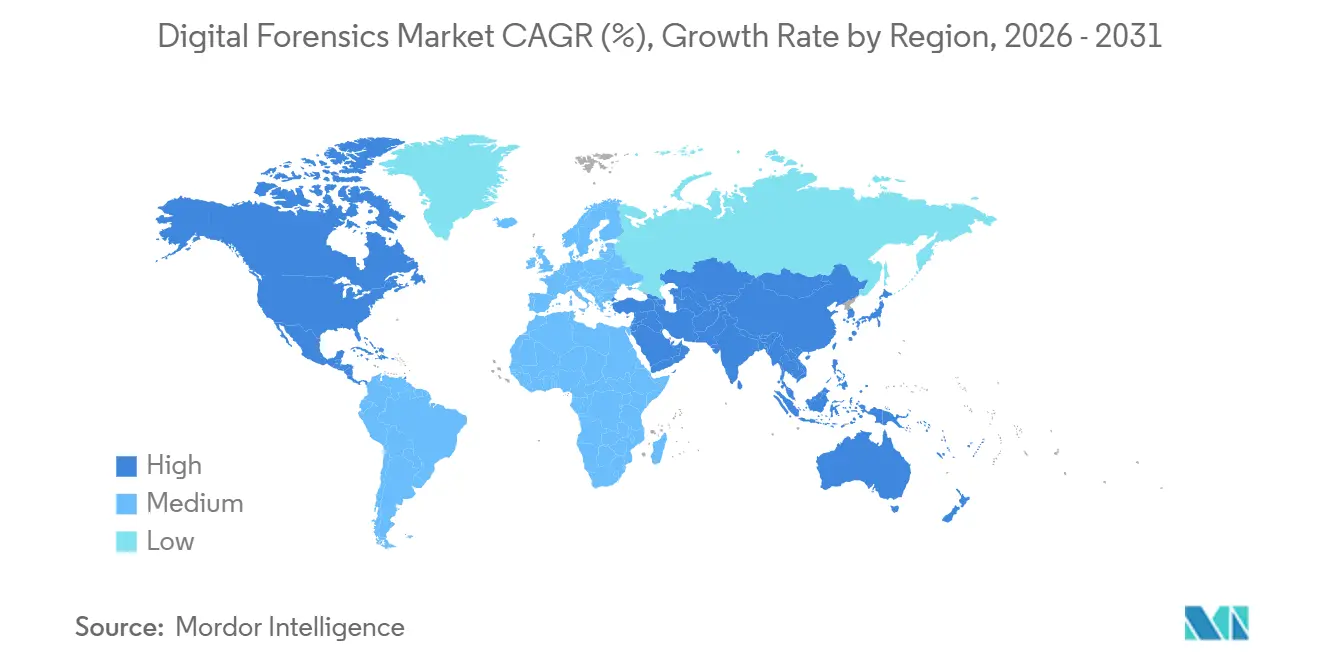

- By geography, North America accounted for 41.37% of 2025 revenue, but Asia-Pacific is forecast to register the highest CAGR of 13.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Forensics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Proliferation of Cloud-Native SaaS Creating Demand for Cloud Forensics | +2.3% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Surge in Deepfake-Enabled Fraud Driving Advanced Multimedia Analysis Needs | +1.8% | Global, early adoption in BFSI sectors across North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Extended Detection and Response (XDR) Adoption Necessitating Integrated DFIR Platforms | +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Legislated Mobile Device Extraction Mandates in U.S. and EU Law-Enforcement | +1.6% | North America and Europe | Long term (≥ 4 years) |

| Blockchain-Based Evidence Chain-of-Custody Pilots Boosting Forensic Software Upgrades | +0.9% | North America, pilot projects in Middle East | Long term (≥ 4 years) |

| Federal Cybersecurity Investments and Regulatory Compliance Requirements Expanding Forensic Deployments | +2.0% | North America, Europe, Asia-Pacific government sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Cloud-Native SaaS Creating Demand for Cloud Forensics

Agencies such as CISA now require continuous forensic data collection for every federal cloud workload, pushing enterprises worldwide to adopt a similar posture.[1]CISA, “Cloud Security Technical Reference Architecture,” cisa.gov Volatile containers and serverless functions expire logs within minutes, so organizations have adopted platforms that snapshot memory, reconstruct Kubernetes pod states, and store artifacts immutably. SaaS breaches at Okta and Snowflake underscored contractual gaps, prompting new service-level agreements that guarantee evidence preservation. ISO 27050 annexes on cloud e-discovery became an audit focal point in 2026, and non-compliant firms face escalating penalties. The digital forensics market is consequently pivoting toward turnkey cloud agents that integrate seamlessly with AWS, Azure, and Google Cloud.

Surge in Deepfake-Enabled Fraud Driving Advanced Multimedia Analysis Needs

Deepfake audio and video cost financial institutions USD 12.3 billion in fraudulent transfers during 2025, according to the Federal Trade Commission.[2]Federal Trade Commission, “Deepfake Fraud Advisory,” ftc.gov Banks and insurers now embed AI-powered forensic filters that look for unnatural phoneme transitions and skipped breaths to flag synthetic media. The European Union’s AI Act classifies deepfake generation software as high-risk and mandates traceability, spurring demand for real-time detection APIs. Forensic labs are investing in GPU clusters that process 4K frames quickly, and the U.S. National Institute of Standards and Technology launched accuracy benchmarks to validate vendor claims. These initiatives elevate the importance of multimedia forensics in the digital forensics market.

Extended Detection and Response Adoption Necessitating Integrated DFIR Platforms

SEC rules require publicly traded companies to disclose material cyber incidents within four business days, compressing investigative windows.[3]U.S. Securities and Exchange Commission, “Cybersecurity Disclosure Rules,” sec.gov XDR rollouts unify telemetry yet lack courtroom-grade chain-of-custody controls, so enterprises bolt DFIR connectors from Exterro and LogRhythm onto platforms such as Microsoft Sentinel. Queries across XDR data lakes now reconstruct attacker lateral movement in minutes, and managed security providers bundle detection, response, and evidence preservation under unified SLAs. As a result, integrated offerings are collecting a growing slice of the digital forensics market.

Legislated Mobile Device Extraction Mandates in U.S. and EU Law-Enforcement

The U.S. Justice Department standardized full-file-system extractions, driving procurement of certified tools from Cellebrite, MSAB, and Grayshift. The EU’s forthcoming E-Evidence Regulation will compel cloud providers to produce mobile backups within ten days, fueling cross-border investigations. Germany and France earmarked EUR 45 million (USD 48 million) in 2025 for lab upgrades, and universities are creating master’s programs to pipeline talent. Growing legislative clarity underpins sustained spending in this portion of the digital forensics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Encryption-by-Default on iOS/Android Elevating Acquisition Complexity and Cost | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Shortage of Court-Certified Examiners Outside Tier-1 Cities | -1.1% | Global, most severe in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Fragmented Tool Inter-Operability Increasing Total Cost of Ownership for SMEs | -0.8% | Global, disproportionate impact on SMEs in Europe and Asia-Pacific | Medium term (2-4 years) |

| Data-Residency Rules Limiting Cross-Border Evidence Transfers | -0.7% | China, Russia, emerging markets with localization mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Encryption-by-Default on iOS/Android Elevating Acquisition Complexity and Cost

Apple iOS 18 and Google Android 15 automatically activate secure-enclave keys, making logical extractions ineffective and forcing agencies toward exploit-based techniques that risk evidence contamination in court. The cost of a high-end mobile-extraction station nearly doubled to USD 85,000 in 2025, straining municipal budgets. Courts in California and New York questioned the admissibility of evidence when zero-day exploits remain undisclosed. The digital forensics market compensates by investing in quantum-resistant brute-force rigs and outsourcing complex extractions to managed service providers.

Shortage of Court-Certified Examiners Outside Tier-1 Cities

Fewer than 8,200 certified examiners practice globally, a deficit magnified in tier-2 and tier-3 urban centers. Case backlogs stretch beyond 180 days in parts of Asia-Pacific and Latin America, delaying prosecutions and civil suits. Training costs ranging from USD 8,000 to USD 15,000 deter candidates, so agencies in South Africa and Indonesia outsource work, raising concerns about the chain of custody. The NIJ funded 12 regional training hubs in 2025, yet international capacity building lags. Persistent talent gaps are holding back growth in segments of the digital forensics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Convert Capex to Opex and Gain Ground on Software

Services are advancing at a 13.27% CAGR through 2031, steadily closing the gap with software’s 47.23% share of the digital forensics market in 2025. Managed retainers bundle acquisition tools, breach analysis, and expert witness testimony under a single subscription, allowing enterprises to shift capital expenses to operating budgets. Professional services consulting, training, and on-site support formed the bulk of 2025 revenue, but cloud-delivered incident-response contracts now account for the fastest dollar growth. Hardware remained the smallest slice, yet purpose-built imaging workstations, write blockers, and rugged field kits continue to anchor law-enforcement workflows.

Software growth is tempered by feature convergence, as vendors expose open APIs that let detection platforms call forensic functions on demand. Enterprises increasingly license only core parsing engines, then outsource routine evidence processing to service providers that promise 24-hour report delivery. This dynamic sustains hardware refreshes at a slower cadence while lifting service margins, confirming that the digital forensics market is pivoting toward outcomes rather than perpetual licenses. Providers that merge software, hardware, and expertise into a single invoice are positioned to lead the next spending cycle.

By Type: Cloud Forensics Propels Shift Away From Disk-Centric Workflows

Cloud forensics is projected to grow at a 13.84% CAGR through 2031, outpacing computer forensics, which still accounted for 32.44% of the digital forensics market in 2025. Organizations now deploy agents that preserve short-lived container logs, serverless traces, and SaaS metadata in immutable object stores, reducing evidence gaps caused by volatility. Computer forensics remains foundational in breach investigations involving Windows and Linux endpoints, yet its growth slows as endpoint detection tools ingest many classic disk-imaging tasks.

Mobile-device forensics accounts for roughly one-third of public-sector budgets, but the rise of encryption is steering agencies toward extraction-as-a-service offerings hosted in secure clouds. Network forensics rebounds as packet capture pinpoints lateral movement in supply-chain attacks, while IoT and database forensics emerge wherever critical infrastructure and financial ledgers demand transaction-level validation. Collectively, expanding cloud workloads and diversified endpoints will ensure continued double-digit growth in the digital forensics market.

By Tool: Decryption and Analytics Outshine Mature Acquisition Platforms

Data acquisition and preservation tools accounted for 28.93% of the 2025 digital forensics market, yet their margins are compressing as imaging becomes commoditized. Decryption and password-cracking modules now clock a 13.63% CAGR through 2031, fueled by GPU clusters and quantum-resistant algorithms that attack file-based encryption in iOS 18 and Android 15. Advanced carving utilities resurrect ransomware-deleted evidence, while automated timeline builders correlate artifacts across disparate devices in minutes.

Review and reporting suites streamline courtroom compliance, automatically embedding hash values and chain-of-custody details into standardized templates. Vendors increasingly bundle triage AI that flags hidden volumes, encrypted containers, and deleted browser records so analysts can focus on high-value leads. Together, integrated toolchains that combine acquisition, decryption, analysis, and reporting in a seamless workflow are redefining competitive parity inside the digital forensics market.

By Organization Size: SME Adoption Accelerates Under Regulatory Spotlight

Large enterprises accounted for 59.37% of 2025 demand, leveraging internal labs and multiyear licensing deals, yet small and medium enterprises are advancing at a 13.06% CAGR through 2031. Mid-market firms face the same breach-notification deadlines as Fortune-500 peers but lack capital for standalone labs, so they gravitate toward cloud platforms that meter usage per incident. Annual retainers priced near USD 25,000 grant SMEs 24-hour analyst access, live-remote acquisitions, and template legal notices, lowering the skills barrier.

Interoperability headaches hit SMEs hardest, prompting vendors to ship turnkey suites that auto-update parsers and ship logs directly to evidence vaults. Meanwhile, large enterprises channel budgets into specialty domains mainframe memory forensics, industrial-control-system artifact capture, and AI-generated content validation areas too niche for smaller firms. The coexistence of these buyer archetypes keeps the digital forensics market balanced between scale and specialization.

By End-User Vertical: Healthcare Surges, Government Plateaus

Government and law-enforcement agencies led with a 36.83% revenue share in 2025, supported by federal grants and multiyear procurement cycles that favor validated toolsets. Their growth, however, is leveling off as private-sector groups assume greater responsibility for incident response. Healthcare now registers the fastest 14.63% CAGR through 2031, propelled by ransomware targeting electronic health records and by mounting civil penalties for delayed breach reporting.

BFSI allocates 1/5 of its cybersecurity budgets to forensic readiness, embedding artifact collectors in payment-card environments to meet PCI DSS 4.0 requirements. IT and telecom operators bolster network forensics to comply with lawful-intercept rules, while retail, energy, and transportation entities respond to credential stuffing and operational technology intrusions. This multi-vertical momentum underlines how compliance regimes, rather than pure technology cycles, are dictating where dollars flow within the digital forensics market.

Geography Analysis

North America commanded 41.37% of the 2025 digital forensics market share, supported by USD 1.2 billion in federal cyber-investigation funding that helped laboratories upgrade extraction and cloud-forensic tools. Enterprises in the United States face strict breach notification rules in California, New York, and Texas, so they routinely embed evidence-capture connectors into their security stacks. Canada tightened disclosure timelines under its revised privacy law, prompting banks and telecom operators to enhance forensic readiness. Mexico’s demand is smaller but rising as cross-border crime investigations require mobile-device imaging capabilities. Across the region, buyers show a clear preference for managed retainers over perpetual licenses as a hedge against talent shortages.

Asia-Pacific is projected to post the fastest 13.66% CAGR through 2031, lifting the regional digital forensics market size at a pace unmatched elsewhere. India is certifying thousands of new examiners, and Japan has budgeted JPY 8.5 billion for upgrades to prefectural labs focused on advanced mobile extractions. China’s data-residency rules force multinationals to build in-country forensic infrastructure, effectively segmenting global incident-response workflows. Australia’s critical infrastructure mandates are driving fresh spending on network and cloud forensics, while South Korea’s BFSI sector is expanding artifact retention to counter payment fraud. These national initiatives collectively underpin long-run growth across the region.

Europe remains a robust contributor as GDPR and the Network and Information Security Directive require formal breach assessments that rely on forensics, yet the region’s expansion is steadier than that of Asia-Pacific. The Middle East and Africa concentrate spending in the United Arab Emirates and Saudi Arabia, where smart-city and government cloud programs demand chain-of-custody controls. South America centers on Brazil and Argentina, which are upgrading police laboratories to address organized cybercrime and corruption. Although budgets in several emerging markets are limited, rising ransomware and regulatory pressure continue to broaden the addressable digital forensics market.

Regulatory Landscape

Digital forensics work is increasingly shaped by both evidentiary best practices and cybersecurity disclosure rules that compress investigation timelines. ISO/IEC 27037:2012 remains a widely referenced baseline for digital evidence identification, collection, acquisition, and preservation, while incident reporting regimes in major markets encourage organizations to build forensic readiness into security operations.

In the United States, NIST continues to influence validation and repeatability expectations through its Computer Forensic Tool Testing (CFTT) program, including the Mobile Device Forensic Tool Test Specification version 3.3 published in January 2025. NIST OSAC also expanded practitioner-facing guidance in 2025 by adding SWGDE best-practice documents to the OSAC Registry, including cloud service provider acquisition and IoT seizure and analysis, strengthening the linkage between tool selection, documented methods, and courtroom defensibility.

Value Chain Analysis

The digital forensics value chain starts with evidence sources (endpoints, mobile devices, cloud/SaaS tenants, networks, and emerging sources such as UAV telemetry) and then moves through acquisition, preservation, analysis, review and reporting, and testimony-ready outputs. Upstream inputs include device interfaces and OS artifacts (iOS/Android, Windows/Linux), cloud platform logs (AWS, Azure, Google Cloud), and specialized data feeds, with quality gates centered on hashing, chain-of-custody controls, and lab accreditation practices.

In the midstream, software vendors and integrators package parsing, decryption, and analytics into suites that increasingly interoperate with security operations tooling and centralized evidence repositories. Service providers deliver these capabilities via retainers, remote acquisition, and expert witness support, while downstream adoption is influenced by public-sector procurement and collaboration networks, including integrations with the National Center for Missing and Exploited Children (NCMEC) for CSAM-related workflows. Partnerships that add niche modules, such as Cellebrite expanding work with SkySafe in July 2026 and Veritone partnering with Thorn in April 2026, also reflect a platformization trend toward end-to-end investigation and evidence management.

Competitive Landscape

The top five vendors, OpenText, Cellebrite, Magnet Forensics, Exterro, and MSAB, accounted for about 38% of 2025 revenue, signaling moderate concentration in the digital forensics market. OpenText widened its e-discovery footprint by acquiring Micro Focus, adding forensic parsing engines that appeal to corporate legal teams. Cellebrite and MSAB maintain leadership in mobile extraction through continuous vulnerability research, yet the growing prevalence of encryption is driving them to introduce cloud-hosted unlock services that charge per device.

Magnet Forensics partnered with Microsoft to embed its Axiom engine into Sentinel, enabling enterprise customers to collect Azure and Microsoft 365 evidence without switching consoles. Exterro raised USD 120 million to accelerate the development of its cloud-native legal-hold solution and expand into Asia-Pacific and the Middle East. Managed security service providers such as Mandiant and Kroll differentiate by bundling incident response, forensic analysis, and regulatory reporting under fixed-fee retainers, an approach that resonates with resource-constrained buyers.

Specialists are carving niches in blockchain and IoT forensics, where incumbent support remains thin, and AI-native startups automate artifact triage to shrink analyst workloads. Patent filings concentrate on quantum-resistant decryption and cross-platform evidence correlation, revealing future battlegrounds. Tool interoperability is still a pain point, so vendors with open APIs gain favor as clients seek to avoid data silos. Overall competition balances scale, specialization, and service innovation, keeping the digital forensics market dynamic and moderately consolidated.

Digital Forensics Industry Leaders

OpenText Corporation

Cellebrite DI Ltd.

Exterro Inc.

Magnet Forensics Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operational pressure to handle larger and more diverse evidence sets is creating whitespace around scalable, auditable storage and workflow automation in law enforcement and regulated enterprises. A specific example is West Midlands Police deploying a Synology-based storage environment with three petabytes in June 2026 to support digital forensics workflows aligned to ISO 17025, highlighting demand for high-volume evidence retention, access control, and traceable handling at the infrastructure layer.

Cross-border and cloud evidence access frameworks are another opportunity area, pushing vendors toward built-in cloud collection, preservation, and legal process management. Government activity provides near-term proof points, including Ireland securing approval in May 2026 to publish the Criminal Justice (International Cooperation on Electronic Evidence and Other Matters) Bill 2026 to align with the EU e-Evidence package, alongside continued standards activity through NIST OSAC updates in 2026 that reinforce method documentation and tool validation. On the technology side, agentic and explainable AI is moving into routine operations for triage and remote investigations, for example Exterro introducing an agentic AI capability for FTK in July 2026, which creates room for offerings that can document model behavior, preserve provenance, and maintain chain-of-custody while reducing analyst workload.

Recent Industry Developments

- July 2026: Exterro launched ARMOUR for FTK, positioning agentic AI inside FTK Central to support remote forensic investigations. The release targets faster triage and guided analysis across distributed data sources, aligning with enterprise needs to investigate under compressed disclosure and legal timelines.

- June 2026: Cellebrite made Genesis generally available, applying agentic AI to interrogate and summarize digital evidence across 35+ formats after an early access phase. General availability broadens deployable automation for investigators and can shift buying decisions toward platforms that reduce manual review time while maintaining evidentiary rigor.

- December 2025: OpenText acquired ADF Solutions for USD 185 million, adding endpoint triage and field forensics capabilities to its portfolio. The deal strengthens OpenText coverage from e-discovery into front-line acquisition and rapid incident response, supporting more end-to-end enterprise and public-sector workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue earned from digital forensics hardware, software, and services used to identify, collect, preserve, analyze, and report digital evidence across devices, networks, and cloud environments.

Scope exclusions: General cybersecurity controls that do not perform evidence acquisition, preservation, or forensic analysis (such as basic endpoint protection and routine IT monitoring) are not counted.

Segmentation Overview

- By Component

- Hardware

- Forensic Systems, Devices and Write Blockers

- Imaging and Duplication Devices

- Other Hardwares

- Software

- Forensic Data Analysis and Visualization

- Review and Reporting

- Forensic Decryption

- Other Softwares

- Services

- Professional Services

- Incident Response and Breach Analysis

- Consulting and Training

- Managed Forensic Services

- Professional Services

- Hardware

- By Type

- Computer Forensics

- Mobile Device Forensics

- Network Forensics

- Cloud Forensics

- Database Forensics

- IoT and Embedded Device Forensics

- By Tool

- Data Acquisition and Preservation

- Data Recovery and Reconstruction

- Forensic Data Analysis

- Review and Reporting

- Forensic Decryption and Password Cracking

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-user Vertical

- Government and Law Enforcement Agencies

- BFSI

- IT and Telecom

- Healthcare

- Retail and E-commerce

- Energy and Utilities

- Manufacturing

- Transportation and Logistics

- Defense and Aerospace

- Education

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the market structure and to ground the model in observable demand signals. We reviewed public sources such as NIST publications, FBI cybercrime and complaint statistics, ENISA threat reports, and national or regional cyber incident reporting guidance that shapes forensic readiness and casework volumes.

For sizing inputs, we also relied on company annual reports, investor presentations, and product documentation that clarify what is sold as a forensics tool versus an adjacent security product. Where needed, paid subscriptions for company financials and intelligence, plus a patent database, were used to cross-check product footprints and track where forensic capabilities are emphasized. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary work focused on validating how digital forensics budgets are actually allocated across software, services, and required supporting hardware, and on checking adoption patterns for cloud forensics and decryption workflows. We spoke with a mix of solution providers, service specialists, enterprise security and compliance stakeholders, and law enforcement or government-aligned practitioners across major regions, so assumptions could be stress-tested and adjusted when secondary data stayed vague.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 38% |

| Mid tier: 47% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 19% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

The core sizing starts with a top-down reconstruction of spend by linking cyber incident volumes and reporting pressure to the share of cases that require evidence capture, preservation, and expert analysis. Once that demand pool is built, it is translated into value using observed mix shifts across software, services, and supporting hardware, then split by region based on enterprise security maturity and public-sector casework intensity.

To keep the model practical, a few market fingerprints were treated as key inputs, including breach and cybercrime reporting trends, cloud workload migration (which lifts cloud forensics need), encryption prevalence that increases decryption effort, typical case backlogs and response timelines, and the services-to-software mix in enterprise engagements. Selective bottom-up approximations were then used as a cross-check, such as sampled pricing for common software deployments, channel checks on service rates, and roll-ups from a limited set of suppliers where disclosures were clear. Where inputs were missing, gaps were handled through conservative assumptions that were re-checked in interviews.

For forecasting, scenario analysis was used because the growth path depends on how regulation, incident frequency, and cloud adoption move together. The scenarios were tuned using primary feedback on expected tool replacement cycles, services demand elasticity during major breach events, and how quickly cloud forensics skills and tooling are being operationalized.

Data Validation & Update Cycle

Estimates were validated through triangulation across independent signals, and then followed by structured variance checks at the region and component level. When an output drifted away from what case volumes, public spending cues, or pricing norms would reasonably support, assumptions were revisited and experts were re-contacted to resolve the mismatch.

Before sign-off, the model and narrative go through multiple analyst reviews so input logic, math consistency, and scope alignment are confirmed. The report is refreshed on an annual cycle, and material events are monitored for interim adjustments. Right before delivery, a final data pass is completed so clients receive the most current view available at the time.

Mordor Intelligence's Digital Forensics Market Size Measured Against Other Published Estimates

Published market sizes for digital forensics often differ because firms do not draw the same line between pure forensic work and broader incident response or cybersecurity tooling. Year choices also matter, since some sources anchor on an older base year while others begin their model at a later point when breach volumes and cloud adoption were higher.

The main gap comes from whether routine security monitoring, general threat detection, or non-evidentiary response services are included, and that alone can move totals by billions. Some estimates also assume faster price expansion for tools like decryption or cloud acquisition, while others do not test the mix shift between services and software using practitioner feedback and observable casework patterns. Evidence preservation and acquisition activities are counted only when they meet forensic use requirements in Mordor Intelligence, which keeps the scope tied to investigative workflows rather than wider cybersecurity operations.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.51 B (2025) | |

| Global Consultancy A | USD 11.27 B (2024) | Uses a later-cycle demand environment and a broader definition that can include enterprise security response activities beyond evidence preservation, which lifts the starting value. |

| Industry Publisher B | USD 13.80 B (2025) | Often aggregates incident response and managed security services into digital forensics revenue, and may apply more aggressive service intensity and pricing assumptions during breach-heavy periods. |

Overall, the spread is mainly explained by what gets counted as forensics work versus adjacent security and response activities, followed by base-year selection and price mix assumptions. By keeping inputs traceable to casework drivers, tool and service mix, and realistic pricing checks, the approach provides a steady number that can be repeated and updated as new incident and adoption signals come in.

Key Questions Answered in the Report

What is the projected value of the digital forensics market in 2031?

It is forecast to reach USD 15.37 billion by 2031, growing at a 12.68% CAGR from 2026.

Which component is growing fastest within the digital forensics market?

Services, driven by managed forensic retainers, will expand at 13.27% CAGR through 2031.

Why is cloud forensics seeing higher adoption than other types?

Ephemeral workloads in multi-cloud environments necessitate dedicated tools that capture short-lived logs and artifacts.

How are SMEs affording forensic capabilities?

Cloud-based platforms and annual retainers priced near USD 25,000 enable SMEs to outsource tooling and expertise.

Which end-user vertical has the highest forecast growth?

Healthcare, advancing at a 14.63% CAGR due to intensified ransomware targeting electronic health records.

What challenges slow the digital forensics market?

Default device encryption, examiner shortages, and data-residency laws raise acquisition costs and delay investigations.

Page last updated on: